jpmorgan investment funds global macro opportunities … · for professional clients / qualified...

TRANSCRIPT

FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

JPMorgan Investment Funds – Global Macro Opportunities Fund

2018

1 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

JPMorgan Investment Funds – Global Macro Opportunities Fund

Targets cash +7% annualised with <10% volatility over the medium term, gross of fees

Potential to deliver positive returns regardless of the market environment

Attractive risk/return

target over cash

Daily liquid,

transparent and

low cost

Luxembourg registered UCITS open-ended, daily liquid fund

Fees - C share class 0.60% AMC1, 0.15% O&A2, no performance fee

Seek to take advantage of the mispricing of macroeconomic trends using a focused and

flexible approach.

Proven macro

investment

approach

Dedicated macro managers and strategists determine most relevant macro themes

Macro managers select focused investment strategies

Risk-aware approach supported by fully integrated, proprietary system

The above target risk/return are the investment manager’s internal guidelines to achieve the Fund’s investment

objective and policy as stated in the prospectus. There is no guarantee that these objectives will be met.1Annual Management and Advisory fee. 2Operating and Administrative expenses.

2 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

A difficult environment for traditional investors

Based on our long-term asset class expectations investors will have to take more risk for less return going forward

As monetary policy normalises, volatility is likely to pick up and investors will be more reliant on funds that can deliver attractive

returns regardless of the market environment

5.1%

8.9% 8.7%

7.3%

3.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Since Euro introduction Post-GFC Last five years Last three years The next 10 years?

Investors will have to take more risk for less return going forward, 50/50 allocation returns, % annualised in EUR

Source: J.P. Morgan Asset Management, Bloomberg. Expectations are based on our Long-Term Capital Market Assumptions (LTCMA) for the relevant years. 50% MSCI World Index and 50%

JPMorgan Global GBI Index, both hedged to EUR. Data as at 30 November 2017 (updated annually). Opinions, estimates, forecasts, projections and statements of financial market trends are based on

market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

Past performance and forecasts are not reliable indicators of current and future results.

3 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Strong, synchronised growth has implications on monetary policy normalisation

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-2000

2000

6000

10000

14000

18000

10 11 12 13 14 15 16 17 18 19 20 21Fed forecast ECB forecast

BoJ forecast Growth impulse (RHS)

G3 Central Bank Balance Sheet, $U.S. Billions %y/y

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

US EMU JP UK CN Ex-CN EM

2017 2018

Regional growth vs trend for 2017 and 2018, % Flow of central bank purchases will decrease from here

Source: J.P. Morgan Asset Management, as at 31 January 2018. Left-hand chart, regional growth vs trend for 2017 and 2018. Right-hand chart: Fed, ECB, BoJ, Haver Analytics, as at 30 June 2017.

RHS: Right-hand side. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and

are subject to change without notice. There can be no guarantee they will be met.

4 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

JPMorgan Investment Funds – Global Macro Opportunities Fund uses in a client portfolio

2. Global hedge fund allocation

Daily liquidity can improve profile of alternatives allocation

Lower cost than traditional macro hedge funds

Transparent and clear reporting of portfolio holdings

1. Complement to traditional assets

Unconstrained by an asset-based benchmark

Not solely reliant on rising markets to generate return

Focused implementation can boost return potential

Adding Global Macro Opportunities Fund to a 50% equity

/50% bond allocation can improve risk-adjusted returns

7%

8%

9%

4% 5% 6% 7% 8%

40% = 1.61 Sharpe ratio

30% = 1.59 Sharpe ratio

20% = 1.53 Sharpe ratio10% = 1.42 Sharpe ratio

Re

turn

Risk

Source: J.P. Morgan Asset Management, as at 31 December 2017. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of

the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met. Annualised return of traditional 50/50 equity/bond portfolio 15 February

2013 to 31 December 2017, represented by 50% MSCI World Index Daily Net Total Return (EUR hedged) and 50% J.P. Morgan Global Government Bond Index (EUR hedged) using weekly returns

with net income reinvested. The indices do not include fees or operating expenses and are not available for actual investment. The index returns are calculated using the weighted market value returns

for the underlying securities, as determined by the index calculation methodology. Performance returns are weekly and shown based on the quoted price of the Global Macro Opportunities Fund using

the C (acc) share class in EUR. All calculations are net of any applicable charges and taxes incurred by the Fund, but gross of any entry/exit fees or taxes charged to the shareholders. Volatility is the

annualised standard deviation using weekly returns. Past performance is not a reliable indicator of current and future results. The portfolio risk

management process includes an effort to monitor and manage risk, but does not imply low risk.

5 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

-3%

-2%

-1%

0%

1%

2%

3%

Equity down

(19 months)

Fixed income down

(28 months)

50/50 balancedportfolio down(18 months)

Equity up

(47 months)

Fixed income up

(38 months)

50/50 balancedportfolio up(48 months)

Retu

rn

Fund average return

Market indices average return

Delivering positive returns in varying market environments

Average monthly fund returns (net of C share class fees) vs. average performance of equity and fixed income

DOWN

MARKETS

UP

MARKETS

Source: J.P. Morgan Asset Management. Fund performance is shown based on the NAV of the share class C in EUR with income (gross) reinvested including actual ongoing charges excluding any

entry and exit fees. Indices do not include fees or operating expenses. Indices used: for equity, MSCI World Index Daily Net Total Return hedged to EUR; and for fixed income, JPM Global Government

Bond Index hedged EUR. Indices do not include fees or operating expenses. Past performance is not a reliable indicator of current and future results.

JPMorgan Investment Funds – Global Macro Opportunities Fund from 30 November 2012 to 31 May 2018

6 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Dedicated global macro investment team and broad research resources

Multi-Asset Solutions research platform

9 qualitative strategists 8 quantitative analysts

Source: J.P. Morgan Asset Management, as at 31 May 2018. First number represent years of industry experience, second number represents years at the firm.

James Elliot, 22/21

Lead portfolio manager

Shrenick Shah, 15/7

Lead portfolio manager

Global macro investment team, years in industry/years at JPMAM

Joshua Berelowitz, 6/6 Benoit Lanctot, 12/6 Rose Thomas, 3/3 Lucy Reid, 2/2

7 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

An investment process founded in macroeconomic research

Less than 10% volatility*8 macro themes 20-40 strategies

Generate macro themes

Establish and maintain set of themes

that encompasses structural and

cyclical trends in the global

macroeconomic environment

Select investment strategies

Seek mix of focused strategies.

Criteria for selection:

1. Reflect at least one macro theme

2. Offer positive return potential

3. Desired impact on portfolio

Risk management

Fully integrated, real-time risk

analysis informs decision making and

ensures continued robustness

*annualised over the medium term.

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

8 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Update on our global macroeconomic views

Global policy

divergence

Maturing US cycle

Japan beyond

Abenomics

Europe

growth recovery

China in transition

Emerging market

convergence

Supply side

weakness

18%

17%

12%5%

5%

17%

17%

9%

Risk breakdown by theme

Generate

macro themes

DAILY MACRO AND

MICRO MONITORING

WEEKLY MACRO

DISCUSSION

MONTHLY CORE VIEWS

UPDATE

QUARTERLY STRATEGY

SUMMIT

Widespread

technology adoption

Source: J.P. Morgan Asset Management, as at 31 May 2018. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the

publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

9 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Select a mix of complementary strategies

Select

investment

strategies

Sophisticated strategiesTraditional strategies

Long physical equity (focused baskets of stocks)

Long fixed income

Equity long, short or relative value

Fixed income short or relative value

Currency

Equity derivatives

Volatility

Each strategy must be driven by a macro theme, be attractively valued, have favourable market dynamics and

provide the desired impact on portfolio exposure and risk

Use in portfolio:

Deliver market beta-linked returns

Provide interest-rate exposure Use in portfolio:

Provide exposure to long/short market beta

and idiosyncratic risk premia

Can offer protection from adverse scenarios

Traditional strategy examples

Equity - consumer staples

Equity - financials

Equity - health care

Equity - industrials

Equity - information technology

Equity - utilities

Fixed income - US 10-year Treasuries

Sophisticated strategy examples

Equity - long China (via H shares index futures)

Equity - short US consumer staples

Equity - long EU basic resources vs short UK

Fixed income - short German 30-year Bunds

Currency - long Australian dollar vs short US dollar

Equity - Long EU puts

Volatility - long US volatility (via VIX index futures)

Traditional and sophisticated investment strategies in a risk-aware framework.

10 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Equity: Long information technology

The sector is benefitting from broad global growth which is

supporting demand and near-term pricing of end products

The stocks we hold in this strategy also benefit from strong secular

trends, including:

- exponential improvement in computing power and data

storage capacity

- growing use of cloud-based applications and computer

networks

- rising adoption of internet and connected devices

- increasing prominence of automation from advances in

artificial intelligence and robotics

These companies have reported strong earnings recently and have

experienced better sales and earnings surprises than the broader

market

Cost of DDR31 4GB and DDR42 4GB memory, US dollars

Widespread technology adoption Maturing US cycle

Notional exposure (cash equity) 17.5%

Number of stocks 18

Quarterly earnings surprise vs estimates, %

Emerging market convergence

Source: J.P. Morgan Asset Management, as at 31 May 2018. Charts, Bloomberg, as at 31 March 2018. Quarterly earnings is for the S&P500 Information Technology sector index. The fund is an

actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the Investment Manager without notice. Opinions, estimates,

forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There

can be no guarantee they will be met. 1DDR3: Double data rate 3, 2DDR4: Double data rate 4.

0

2

4

6

2013 2014 2015 2016 2017

DDR3 4GB DDR4 4GB

Positioning

update

0

5

10

15 S&P Information Technology

11 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Chinese bank valuations are low given their profitability

Equity: Long financials

Emerging market convergence

Positioning

update

China in transition

JapanSouth Korea

Taiwan Singapore

Malaysia

Philippines

Thailand

India

Indonesia

Australia

China

Hong Kong

0.5

1

1.5

2

2.5

3

3.5

6 8 10 12 14 16 18

Price-t

o-b

ook (

last

report

ed)

Average of 2017 & 2018 RoE

Maturing US cycle

Notional exposure (cash equity) 11.9%

Number of stocks 13

Banks’ CCAR1 payout ratios are rising

56%

84%

101%

2015 2016 2017

China: Banks should benefit from a stable domestic growth

environment and a focus from the authorities on financial stability.

There is scope for re-rating as markets price in a lower probability of

a sharp growth slowdown

US: Banks are likely to benefit from continued strong growth, a

positive impulse from the tax reform package and gradual monetary

policy tightening. Potential for an increasingly favourable regulatory

environment and improving capital return are a further support

Emerging markets: Singapore banks are well placed to benefit from

global cyclical momentum, along with rising US rates, while insurance

companies with significant exposure in the region are seeing strong

structural growth driven by demographics and low penetration rates

Source: J.P. Morgan Asset Management, as at 31 May 2018. Charts, Bloomberg, as at 30 September 2017. The fund is an actively managed portfolio. Holdings, sector weights, allocations and

leverage, as applicable, are subject to change at the discretion of the Investment Manager without notice. Opinions, estimates, forecasts, projections and statements of financial market trends are based

on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met. 1Comprehensive Capital Analysis and

Review.

12 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Portfolio positioning

Source: J.P. Morgan Asset Management, as at 31 May 2018. The fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the

discretion of the Investment Manager without notice. Duration excludes inflation and credit default swaps. Currency breakdown accounts for all active currency strategies. *Global Industry

Classification Standards®. Equity derivatives is the delta from futures and options broken down into the sectors from which the derivative is derived. Equity includes ETFs.

Positioning

update

Active currency positionsDuration, yearsGICS* Sector breakdown

Total duration now 0.5 years

-20% -10% 0% 10%

USD

JPY

KRW

BRL

SEK

MXN

INR

AUD

EUR

Equity exposure (delta)

Total equity delta now 30.7%

-20% 0% 20%

Europe ex-UK

UK

Emerging market

Japan

North America

Asia ex-Japan

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

-2 -1 0 1 2

Europe ex-UK

UK

Emerging market

Japan

North America

Asia ex-Japan

-10% 0% 10% 20%

Utilities

Telecommunication services

Real estate

Materials

Information technology

Industrials

Health care

Financials

Energy

Consumer staples

Consumer discretionary

Axis Title

Equity

Equity derivatives

Total-50% 0% 50% 100%

13 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Historical equity delta exposure (using 3 month moving averages)

Asia ex-Japan & Emerging Market North America

Europe & UK Japan

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-20%

-10%

0%

10%

20%

30%

40%

0%

5%

10%

15%

20%

25%

30%

35%

-5%

0%

5%

10%

15%

20%

25%

Positioning

update

Source: J.P. Morgan Asset Management, as at 31 May 2018. Time series calculated using a 3 month moving average. In November 2012 the internal investment process and team changed with no

impact on Fund investment policy and objective. The fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the

Investment Manager without notice. The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

14 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

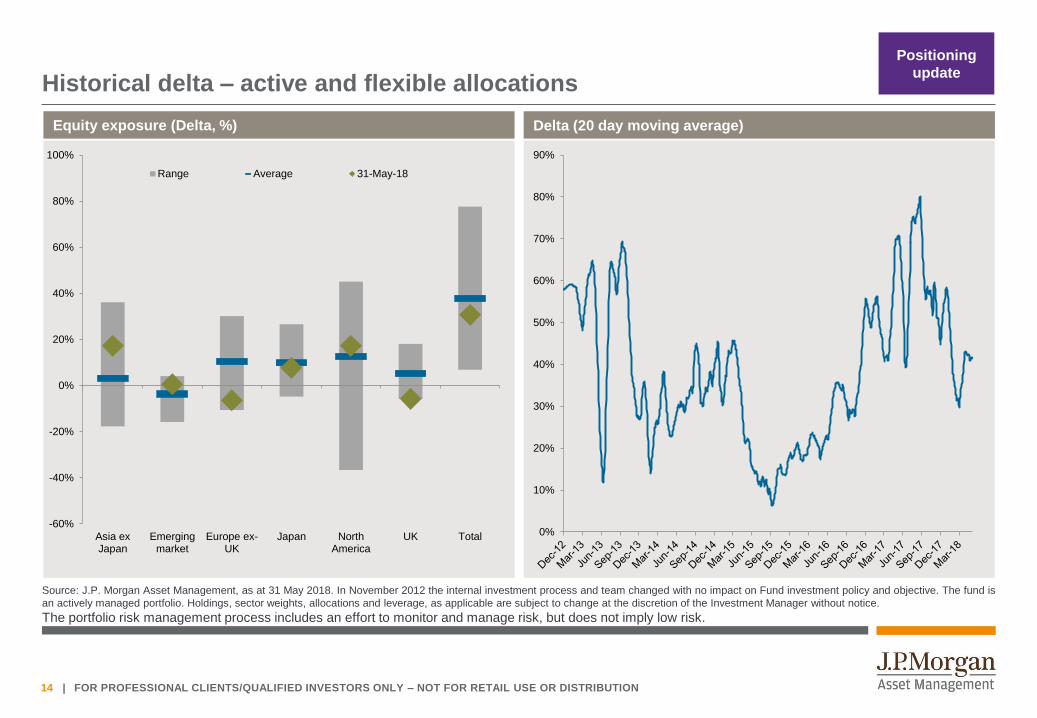

Historical delta – active and flexible allocations

Equity exposure (Delta, %)

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Asia exJapan

Emergingmarket

Europe ex-UK

Japan NorthAmerica

UK Total

Range Average 31-May-18

Delta (20 day moving average)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Positioning

update

Source: J.P. Morgan Asset Management, as at 31 May 2018. In November 2012 the internal investment process and team changed with no impact on Fund investment policy and objective. The fund is

an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager without notice.

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

15 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

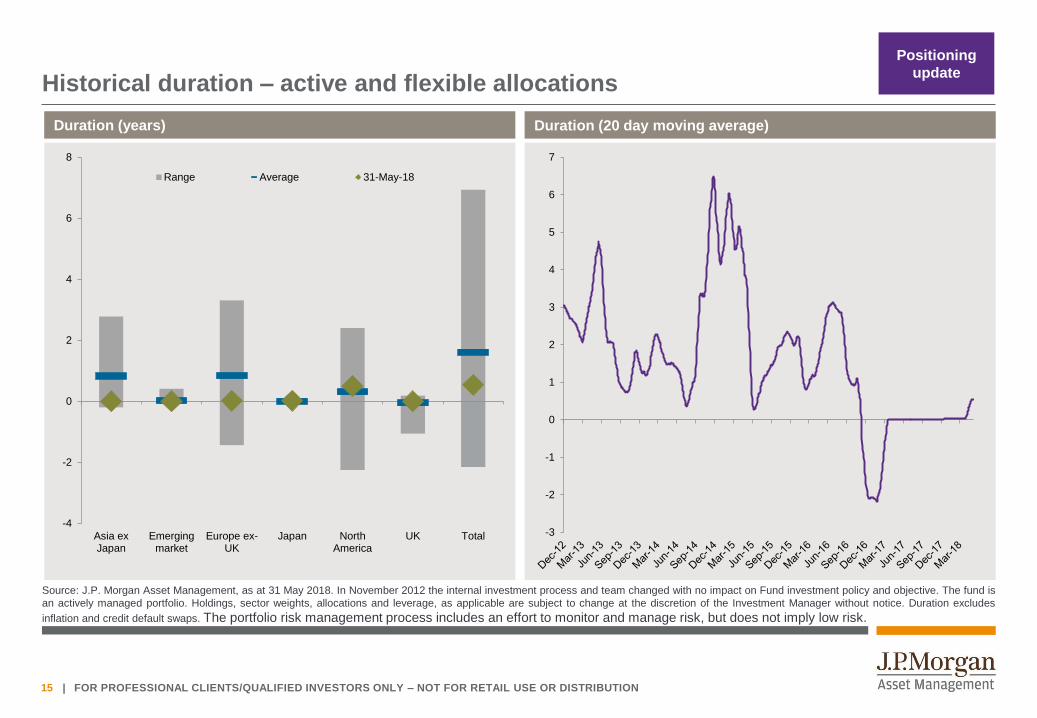

Historical duration – active and flexible allocations

Duration (20 day moving average)

-3

-2

-1

0

1

2

3

4

5

6

7

Duration (years)

-4

-2

0

2

4

6

8

Asia exJapan

Emergingmarket

Europe ex-UK

Japan NorthAmerica

UK Total

Range Average 31-May-18

Positioning

update

Source: J.P. Morgan Asset Management, as at 31 May 2018. In November 2012 the internal investment process and team changed with no impact on Fund investment policy and objective. The fund is

an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager without notice. Duration excludes

inflation and credit default swaps. The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

16 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Multi-dimensional risk analysis

Source: J.P. Morgan Asset Management, as at 31 May 2018. The fund is an actively managed portfolio, holdings, sector weights, allocations and leverage, as applicable are subject to change at

the discretion of the Investment Manager without notice. In November 2012 the internal investment process and team changed with no impact on Fund investment policy and objective.

By macro theme Current breakdown

Risk

management

18%

17%

12%

5%5%

17%

17%

9%

0%

20%

40%

60%

80%

100% Widespread technology adoption

US economic strength

Maturing US cycle

Europe growth recovery

Europe gradual growth recovery

Low growth Europe

Supply side weakness

Japan beyond Abenomics

Japan economic recovery

Global policy divergence

Emerging market rebalancing

Emerging market convergence

China in transition

Low inflation

By asset class Current breakdown

0%

20%

40%

60%

80%

100%

Equity

Fixed income

Currency

Advanced derivatives74%

3%

11%

12%

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

17 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Fund exposure

0%

2%

4%

6%

8%

10%

12%

14%

Realised volatility (rolling 3 year)Ex-ante volatility

Source: J.P. Morgan Asset Management, as at 31 May 2018. Ex-ante volatility is calculated with a 2-year look back and a 6 month half life (prior to 31st January 2018 a 3 month half life was

used). Realised volatility uses monthly 3 year rolling volatility

Risk

management

Total standalone volatility Total nominal gross exposure

0%

100%

200%

300%

400%

500%

0%

5%

10%

15%

20%

25%

30%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

18 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Summary

JPMorgan Investment Funds – Global Macro Opportunities Fund as at 31 May 2018

Expertise

Experienced team of macro investors and strategists

Dedicated macro investment team of six with two lead managers

Nine strategists and economists support macro-thematic research

Fully integrated, proprietary portfolio management system provides detailed analysis

Portfolio

Research-oriented and focused approach with risk-aware implementation

Fundamental macro views lead to selection of a focused set of strategies to build robust portfolio

Targets cash +7% annualised with <10% volatility over the medium term, gross of fees

Fees - C share class 0.60% AMC1, 0.15% O&A2, no performance fee

Success

Attractive risk-adjusted returns over the medium term through varying market environments

9.3% annualised return since people and process change in November 2012 (net of C share class fees)

Positive returns regardless of the market environment since inception

The above target risk/return are the investment manager’s internal guidelines to achieve the Fund’s investment objective and policy as stated in the

prospectus. There is no guarantee that these objectives will be met. Past performance is not a reliable indicator of current and future results.1Annual Management and Advisory fee. 2Operating and Administrative expenses.

19 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Performance analysis

20 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Market value EUR 5,479 m

Performance

Source: J.P. Morgan Asset Management. Fund performance is shown based on the NAV of the share class C (acc) in EUR with income reinvested including actual ongoing charges excluding any entry

and exit fees. Returns over 1 year are annualised. Excess return is calculated geometrically. Until 8 April 2014, the fund was subject to a performance fee, which is included in the performance track

record for periods up to this date. Excess returns are geometric. *In November 2012 the internal investment process and team changed with no impact on Fund investment policy and objective. **The

fund launched in October 1998, and data is available from April 2005 when it moved to using a cash benchmark and a total return approach. Benchmark is ICE 1 month EUR LIBOR. . Indices do not

include fees or operating expenses. Past performance is not a reliable indicator of current and future results. ^As of 30 April 2018

JPMorgan Investment Funds – Global Macro Opportunities Fund as at 31 May 2018

Annualised performance (%)

Performance summary 1 month 3 month YTD 1 Year 3 Year 5 year

Since people

& process

change*

Since

inception

30/04/2005**

Global Macro Opportunities Fund -0.9 -3.9 1.1 15.3 4.4 7.5 9.3 5.6

Benchmark 0.0 -0.1 -0.2 -0.4 -0.3 -0.2 -0.1 1.2

Excess return -0.9 -3.8 1.3 15.7 4.8 7.7 9.5 4.4

Volatility - - - 8.5 7.7 7.6 7.5 7.5

50% MSCI World Index: 50%

JPM GBI Index0.6 0.4 -0.3 3.8 3.6 5.9 6.8 5.1

Blended index volatility - - - 3.2 4.8 4.6 4.7 6.5

MSCI World Index (EUR

hedged)1.1 0.4 0.1 8.6 6.2 9.5 11.6 6.3

MSCI World volatility - - - 7.1 10.0 9.3 9.1 13.4

HFRI Fund Weighted Composite

Index (EUR)^0.7 6.4 1.9 6.4 2.9 4.0 4.2 8.4

HFRI Macro Total Index^ 0.6 2.3 2.4 2.3 0.7 1.4 1.6 3.6

Performance

21 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Performance

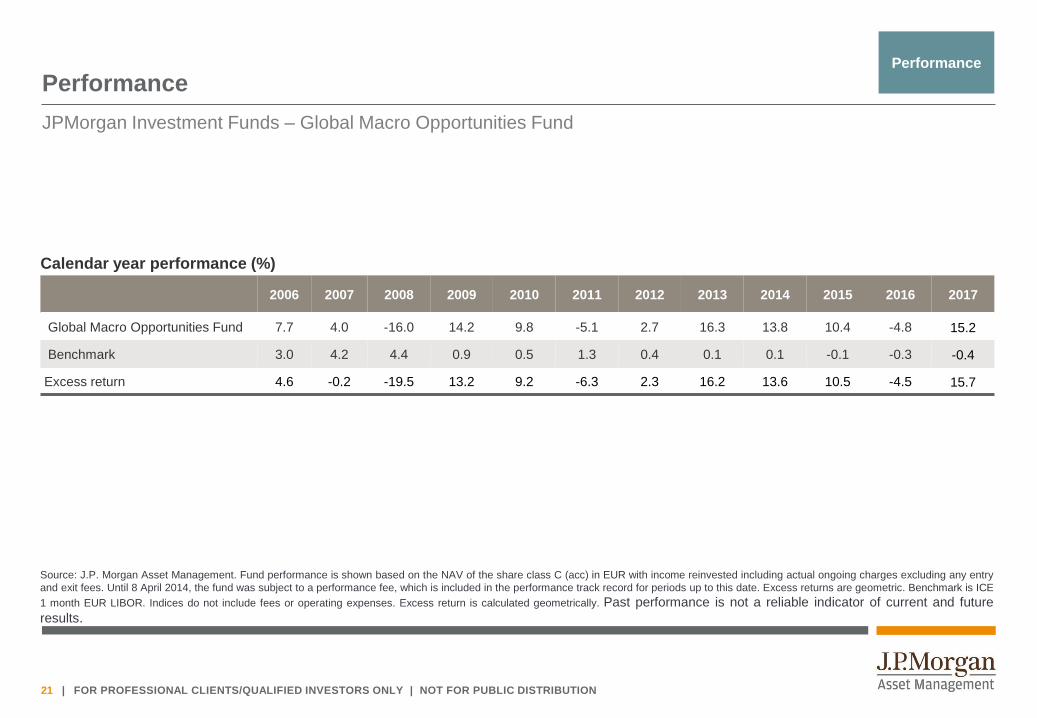

JPMorgan Investment Funds – Global Macro Opportunities Fund

Performance

Calendar year performance (%)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Global Macro Opportunities Fund 7.7 4.0 -16.0 14.2 9.8 -5.1 2.7 16.3 13.8 10.4 -4.8 15.2

Benchmark 3.0 4.2 4.4 0.9 0.5 1.3 0.4 0.1 0.1 -0.1 -0.3 -0.4

Excess return 4.6 -0.2 -19.5 13.2 9.2 -6.3 2.3 16.2 13.6 10.5 -4.5 15.7

Source: J.P. Morgan Asset Management. Fund performance is shown based on the NAV of the share class C (acc) in EUR with income reinvested including actual ongoing charges excluding any entry

and exit fees. Until 8 April 2014, the fund was subject to a performance fee, which is included in the performance track record for periods up to this date. Excess returns are geometric. Benchmark is ICE

1 month EUR LIBOR. Indices do not include fees or operating expenses. Excess return is calculated geometrically. Past performance is not a reliable indicator of current and future

results.

22 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Fund correlation to different assets

Source: J.P. Morgan Asset Management, as at 31 May 2018. Fund = JPMorgan Investment Funds – Global Macro Opportunities Fund. Fund correlation is based on the NAV of the share class C in

EUR with income (gross) reinvested including actual ongoing charges excluding any entry and exit fees. Correlation data computed using weekly returns, Friday to Friday. Indices used: 50% MSCI

World Index:50% JPM GBI Index. *Since process change 30 November 2012. In November 2012 the internal investment process and team changed with no impact on Fund investment policy and

objective. Past performance is not a reliable indicator of current and future results.

Performance

1 year to 31 May

20182017 2016 2015 2013-2014

Since process

change*

50/50 balanced fund 39% 17% -5% -15% 55% 24%

Developed market equity 44% 37% -18% -25% 57% 23%

Emerging market equity 58% 34% -27% -47% 0% -3%

Global sovereign bonds -26% -38% 45% 33% -12% 3%

US corporate bonds (HY) 32% -1% -21% -21% 13% -2%

US 10 year inflation (implied) 16% 15% -48% -40% 1% -16%

JPM trade-weighted USD index 0% 35% 17% 44% 29% 25%

Gold -5% -3% 21% -11% -23% -13%

Oil 12% -38% -31% -28% -14% -15%

US Cyclicals vs. defensives 53% 44% -59% -22% 15% 3%

23 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Fund performance relative to equity and bond performancePerformance

Source: J.P. Morgan Asset Management, Bloomberg, as at 31 May 2018. Fund = JPMorgan Investment Funds – Global Macro Opportunities Fund. Fund performance is shown based on the NAV of the

share class C in EUR with income (gross) reinvested including actual ongoing charges excluding any entry and exit fees. Until 8 April 2014, the fund was subject to a performance fee, which is included in

the performance track record for periods up to this date. In November 2012 the internal investment process and team changed with no impact on Fund investment policy and objective. Maximum

drawdown calculated using monthly data. Indices are total return indices: 50% MSCI World Index and 50% JPM GBI Index (hedged to EUR). Indices do not include fees or operating expenses.

2013 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2013

Fund 3.66% 1.96% 1.61% 2.47% 2.53% -1.75% -0.16% -2.41% 1.73% 1.90% 2.52% 1.32% 16.29%

MSCI World 5.15% 1.50% 2.68% 2.69% 1.41% -2.44% 4.63% -2.09% 3.67% 3.92% 2.14% 2.05% 28.07%

JPM GBI -0.58% 0.62% 0.70% 1.03% -1.70% -1.11% 0.25% -0.30% 0.68% 0.84% -0.12% -0.77% -0.49%

50:50 Balanced 2.28% 1.06% 1.69% 1.86% -0.14% -1.78% 2.44% -1.19% 2.18% 2.38% 1.01% 0.64% 13.03%

2014 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2014

Fund 1.53% 0.28% -1.53% -0.83% -0.29% 1.66% -0.79% 1.83% 4.09% -0.76% 3.96% 4.04% 13.75%

MSCI World -3.31% 4.15% 0.19% 0.72% 2.28% 1.37% -0.81% 2.64% -1.05% 1.12% 2.83% -0.81% 9.48%

JPM GBI 1.68% 0.38% 0.09% 0.64% 0.88% 0.31% 0.34% 1.39% -0.29% 0.74% 1.18% 0.84% 8.47%

50:50 Balanced -0.82% 2.27% 0.14% 0.68% 1.58% 0.84% -0.24% 2.02% -0.67% 0.93% 2.00% 0.02% 9.04%

2015 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2015

Fund 3.46% 1.42% 4.56% -2.72% 0.80% -0.07% 2.35% 4.26% -1.00% -2.50% -1.10% 0.83% 10.43%

MSCI World -0.73% 5.89% -0.49% 1.01% 1.25% -2.96% 2.48% -6.62% -3.60% 7.93% 0.63% -2.17% 1.75%

JPM GBI 2.37% -1.02% 0.80% -0.80% -0.64% -1.32% 1.26% -0.23% 0.91% 0.07% 0.00% -0.29% 1.05%

50:50 Balanced 0.82% 2.44% 0.16% 0.10% 0.31% -2.14% 1.87% -3.43% -1.35% 4.00% 0.31% -1.23% 1.65%

2016 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2016

Fund 2.53% 0.65% -2.57% -1.12% 0.79% 1.86% -0.05% -3.12% -0.32% -1.60% -3.47% 1.72% -4.81%

MSCI World -5.46% -1.59 5.04% 0.78% 1.73% -1.45% 4.01% 0.33% 0.10% -0.79% 2.61% 2.65% 7.79%

JPM GBI 2.06% 1.22 0.36% -0.26% 0.51% 2.38% 0.25% -0.46% -0.22% -1.57% -1.98% 0.03% 2.25%

50:50 Balanced -1.70% -0.19 2.70% 0.26% 1.12% 0.46% 2.13% -0.06% -0.06% -1.18% 0.31% 1.34% 5.18%

2017 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2017

Fund -1.87% -1.78% 2.24% 0.41% 2.15% 1.71% 3.24% 1.16% 3.41% 5.15% -1.39% 0.07% 15.20%

MSCI World 1.15% 3.07% 0.86% 1.05% 1.34% -0.11% 1.28% 0.02% 2.21% 2.46% 1.41% 0.94% 16.80%

JPM GBI -0.83% 0.80% -0.25% 0.55% 0.38% -0.53% 0.05% 0.90% -0.88% 0.27% 0.09% -0.12% 0.40%

50:50 Balanced 0.16% 1.93% 0.30% 0.80% 0.86% -0.32% 0.66% 0.46% 0.67% 1.36% 0.75% 0.41% 8.33%

2018 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2018

Fund 3.86% 1.35% -3.35% 0.34% -0.93% 1.13%

MSCI World 3.53% -3.72% -2.47% 1.80% 1.13% 0.09%

JPM GBI -0.95% -0.23% 0.99% -0.65% 0.10% -0.75%

50:50 Balanced 1.29% -1.97% -0.74% 0.58% 0.61% -0.27%

Past performance is not a reliable indicator of current and future results

24 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

-5% 0% 5% 10% 15%

Advanced derivativesCurrency

Fixed incomeEquity futures

Total cash equity

Contribution by asset class as at 31 May 2018Performance

1 yearYear-to-date

From process change (November 2012, annualised)3 years (annualised)

-4% -2% 0% 2% 4%

Advanced derivativesCurrency

Fixed incomeEquity futures

Total cash equityAsia

Emerging markets

Europe

Japan

UK

US

-2% 0% 2% 4% 6% 8%

Advanced derivativesCurrency

Fixed incomeEquity futures

Total cash equity

Source: J.P. Morgan Asset Management. Contributions based on gross of fee returns, and may not match the official returns due to differences in system rounding.

Past performance is not a reliable indicator of current and future results.

Asia

Emerging markets

Europe

Japan

UK

US

Asia

Emerging markets

Europe

Japan

UK

US

-5% 0% 5% 10% 15%

Advanced derivativesCurrency

Fixed incomeEquity futures

Total cash equityAsia

Emerging markets

Europe

Japan

UK

US

25 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Contribution through time

Calendar year asset class contribution

% 2013 2014 2015 2016 2017 2018 YTD

Equity 21.2 7.9 5.0 1.1 25.3 -2.1

Asia -0.6 0.0 -0.1 0.2 7.7 0.7

Emerging markets 0.0 - - - 1.4 0.0

Europe 4.0 1.4 1.7 0.1 1.9 -0.8

Japan 5.8 -0.7 2.3 -0.6 4.9 -1.4

UK 2.5 1.5 0.9 0.8 1.0 -0.1

US 9.6 5.8 0.1 0.5 8.3 -0.5

Equity futures 0.6 0.1 0.1 -5.8 -1.0 1.4

Cash equity + equity futures 21.8 8.0 5.1 -4.7 24.4 -0.7

Fixed income -1.9 3.5 -0.9 0.2 0.2 0.0

Currency -0.9 1.5 4.1 2.4 -2.4 -0.5

Advanced derivatives -1.2 1.3 3.0 -1.9 -6.0 2.6

Total 17.8 14.4 11.3 -4.1 16.1 1.4

Performance

% 2013 2014 2015 2016 2017 2018 YTD

MSCI World 28.1 9.5 1.7 7.8 16.8 0.1

JPM GBI -0.5 8.5 1.1 2.2 0.4 -0.8

50:50 Balanced 13.0 9.0 1.6 5.2 8.3 -0.3

Source: J.P. Morgan Asset Management, as at 31 May 2018. Contributions based on gross of fee returns, and may not match the official returns due to differences in system rounding. Indices used:

50% MSCI World Index and 50% JPM GBI Index. Indices do not include fees or operating expenses. Past performance is not a reliable indicator of current and future results.

FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Appendix

27 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY | NOT FOR PUBLIC DISTRIBUTION

Fund information

Inception date* 31 October 1998

Benchmark ICE 1 Month EUR LIBOR

Volatility <10%

Fund size €5,479 million

ISIN LU0095623541

Bloomberg ticker JPMECAC LX

Fund characteristics

JPMorgan Investment Funds - Global Macro Opportunities Fund

As at 31 May 2018

Portfolio risk by asset class Portfolio risk by theme

James Elliot

Portfolio Manager

London

Experience: 22/21

Shrenick Shah

Portfolio Manager

London

Experience: 15/7

Equity 74%

Fixed income 3%

Currency 11%

Advanced derivatives 12%

China in transition 18%

Emerging market convergence 17%

Europe growth recovery 12%

Global policy divergence 5%

Japan beyond Abenomics 5%

Widespread technology adoption 17%

Maturing US cycle 17%

Supply side weakness 9%

Source: J.P. Morgan Asset Management. The Fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the

Investment Manager without notice. *The fund was incepted in October 1998 but its performance track record was restated from April 2005, when the fund changed to using a cash benchmark and total

return approach. The fund underwent further changes to the investment approach in November 2012, which included moving to a macro-thematic investment framework in which we are asset class

agnostic. The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

28 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Global macro research platform leveraged for macro investing

Global macro research meeting cycle

John Bilton

Head of Global Multi-Asset Strategy

Thushka Maharaj

DAILY MACRO AND

MICRO MONITORING

WEEKLY MACRO

DISCUSSION

MONTHLY CORE VIEWS

UPDATE

QUARTERLY STRATEGY

SUMMIT

Chaired by the Global Multi-Asset Strategy team Chaired by the PM team

Economists and market strategists

Michael Hood

Mark Richards Patrik Schöwitz

Benjamin Mandel

Michael Albrecht Diego Gilsanz

Tim Lintern

Quantitative research analysts

Katherine Santiago

Head of Global Multi-Asset Research

Grace Koo

Boqui Liu

Livia Wu

The Global Multi-Asset Strategy and Research teams provide deep and broad macro and market analysis that forms

a key input to our research-oriented investment approach

Generate macro

themes

Nandini Srivastava

Xiao Xiao

Source: J.P. Morgan Asset Management, as at 31 May 2018.

Ivan Chong

Abhinav Verma

29 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Summary of current macro themes

Generate macro

themes

Source: J.P. Morgan Asset Management Multi-Asset Solutions, as at 31 May 2018. 1Global Financial Crisis 2European Central Bank 3Bank of Japan 4Emerging Markets 5Developed Markets. Opinions,

estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without

notice. There can be no guarantee they will be met.

Theme Update

Global policy divergencePost GFC1 recoveries have been multi-speed and asynchronous,

reflected in differing policy responses from fiscal authorities and

central banks.

Monetary policy divergence may have peaked for now although is

evident in the varying pace at which policy support is being removed

A further source of divergence is coming from fiscal policy.

Supply side weaknessWeaknesses on the supply-side in labour force, capital and

productivity growth lead to lower trend growth. Supply constraints

may bind more quickly, accelerating inflation.

Unemployment rates have dropped more rapidly than was typical in

the past. Some signs of cost-push inflation is materialising in the US,

although not yet strongly.

Maturing US cycleThe US economy has entered the late phase of a long and flat

business cycle, against a backdrop of generally steady growth.

Solid labour markets and rising wages are supporting the consumer,

while business investment is firming. An additional boost to growth

should come from fiscal stimulus.

Europe growth recoveryEuro area growth has steadily accelerated to an above-trend

pace, with room for this to continue due to years of slow growth,

and monetary policy remains accommodative.

Growth momentum has moderated but remains above-trend and

dispersion across the region has fallen. However, inflation remains

subdued, pointing to a gradual removal of ECB2 policy

accommodation.

Japan beyond AbenomicsMonetary policy has limited scope for further easing. Demand is

decent, but structural problems remain, with a broad range of

possible outcomes for growth and policy.

Growth has stalled a little but is expected to remain firm; inflation is

showing tentative signs of a gradual pickup. Monetary policy remains

extremely ease however the BoJ3 will start to consider its future

policy path later in the year.

Emerging market convergenceConvergence between EM4 and DM5 economies is becoming

more pronounced. A lower level of activity in EM provides scope

to converge, in areas such as income and consumption.

The EM bloc is in the early stages of a new cyclical expansion and

this provides room for convergence to accelerate. Risks stem from

widening fiscal deficits and any slowdown in credit.

China in transitionChina is transitioning from an industrial to services led economy

with lower trend growth. The authorities are focusing on financial

stability - a positive development.

Growth has been steady with only modest monetary policy

tightening. The National Party Congress consolidated President Xi’s

power and this political stability should enable structural reforms.

Widespread technology adoptionEmerging information technologies are reaching inflection points

in innovation and adoption rates. The technology cycle likely

boosts productivity growth providing upside risks to trend growth.

Information technologies are disrupting existing business models

and creating new opportunities, resulting in an environment of

winners and losers.

30 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

New theme: Widespread technology adoption

Source: Left-hand side, Asymco, compiled from various sources with support from the Clayton Christensen Institute. Right-hand chart, Bureau of Labor Statistics, as at 31 August 2017. Opinions,

estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without

notice. There can be no guarantee they will be met.

This tech cycle is likely to boost productivity growth, providing upside risks to trend growth, however, this positive impulse may be

dampened by other, potentially disruptive, side effects.

The proliferation of mobile and connected devices combined with the improvement of communication networks is leading to an

explosion of data that can now be stored, processed and analysed more cheaply and more efficiently.

Information technologies are creating new opportunities but also disrupting existing industries, creating winners and losers.

This tech cycle is likely to boost productivity growth

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

1955 1965 1975 1985 1995 2005 2015

Tech shock Output/hour Output/hour trend

Generate

macro themes

Disruption from technology advances by industry

Banking Electronic payments, online banking

Consumer products Smart devices, hyper personalisation

Healthcare Computer assisted diagnosis, surgical robots

Insurance Real-time tracking, usage-based pricing

Logistics Warehouse automation, delivery drones

Manufacturing Industrial robots

Retail e-commerce, automated stores

Transportation Electric and autonomous vehicles

Utilities Smart grid, distributed power

31 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Dynamic reduction of equity risk: Feb 2018

Macro event riskMacro research enables identification of possible risk

Broad-based strong growth through 2017 prompted rising

inflation expectations in markets. In this risk-on environment,

equity markets and global bond yields moved sharply higher.

We believed there was a potential for market volatility to rise

as markets navigate the removal of ultra-easy monetary policy.

While the macro backdrop remained positive, the speed and

magnitude of these markets moves led us to reduce aggregate

portfolio risk.

Strategy selectionFlexible Implementation

We took advantage of the move higher in equity markets by

taking profit on some of our long equity strategies, including

Chinese and US financials and global materials.

We added to protection strategies, adding attractively-priced

long US volatility futures and long US large cap put option

strategies.

In the event…

After the strong start to the year, risk assets suffered in February

and volatility increased. While our cash equity positions broadly

detracted, the losses were more than offset by our long volatility

strategy and short US equity exposure.

Select

investment

strategies

January 2018 – Actively reduced risk as equity markets soared

February 2018 Portfolio outcome (return)

MSCI World Index (Euro hedged) -3.7%

Total portfolio 1.3%

Advanced derivatives 2.1%

Portfolio delta

MSCI World Index (Euro hedged)

Source: J.P. Morgan Asset Management, Bloomberg, as at 28 February 2018. Advanced derivatives included long VIX futures and long US large cap put options. Performance returns are for JPM

Global Macro Opportunities Fund and are shown gross of fees. Past performance is not a reliable indicator of current and future results.

0%

20%

40%

60%

80%

100%

205

210

215

220

225

230

235

240

1-Jan 8-Jan 15-Jan 22-Jan 29-Jan

32 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

So

ph

isti

ca

ted

Tra

dit

ion

al

Supply side

weakness

China in

transition

Emerging

market

convergence

Global policy

divergence

Japan beyond

Abenomics

Europe growth

recovery

Maturing US

cycle

Widespread

technology

adoption

Macro themes and strategies are interlinked

Str

ate

gy

Select

investment

strategies

Source: J.P. Morgan Asset Management, as at 31 May 2018. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the

publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

Equity - consumer discretionary

Equity - energy

Equity - financials

Equity - health care

Equity - industrials

Equity - information technology

Equity - materials

Equity - telecommunication services

Equity - utilities

Fixed income - France

Fixed income - Japan

Fixed income - US

Equity - long China

Equity - long emerging markets

Equity - long Singapore

Equity - long US energy

Equity - long US financials

Equity - short Australia

Equity - short EU staples

Equity - short Europe

Equity - short UK

Equity - short US utilities

Equity - long US autos via options

Equity - long US large cap calls

Volatility - long VIX

FX - long AUD short USD

FX - long EUR short USD

FX - long USD short JPY

FX - long USD short KRW

FX - short USD long BRL

FX - short USD long INR

FX - short USD long MXN

FX - short USD long SEK

33 | FOR PROFESSIONAL CLIENTS/QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

-1% 0% 1% 2% 3%

Equity - short Europe

Volatility - long VIX

Equity - short UK

Equity - short Australia

FX - long USD short KRW

Equity - short EU staples

Equity - short US utilities

FX - long USD short JPY

FX - short USD long INR

Equity - long US autos via options

FX - short USD long SEK

FX - short USD long BRL

Equity - long Singapore

FX - long EUR short USD

FX - short USD long MXN

FX - long AUD short USD

Equity - long US financials

Equity - long US energy

Equity - long emerging markets

Equity - long China

Fixed income - US

Fixed income - France

Fixed income - Japan

Equity Utilities

Equity Telecommunication Services

Equity Consumer Discretionary

Equity Materials

Equity Health Care

Equity Industrials

Equity Energy

Equity Financials

Equity Information Technology

0% 1% 2% 3% 4%

Equity - short EU staples

FX - short USD long SEK

Equity - long Singapore

FX - short USD long INR

FX - short USD long BRL

FX - long USD short KRW

Equity - long US autos via options

FX - long USD short JPY

FX - long EUR short USD

FX - long AUD short USD

FX - short USD long MXN

Equity - long US financials

Equity - short Australia

Equity - long emerging markets

Equity - long China

Equity - long US energy

Equity - short US utilities

Equity - short UK

Volatility - long VIX

Equity - short Europe

Fixed income - France

Fixed income - Japan

Fixed income - US

Equity Telecommunication Services

Equity Materials

Equity Health Care

Equity Consumer Discretionary

Equity Utilities

Equity Industrials

Equity Energy

Equity Financials

Equity Information Technology

Volatility across traditional and sophisticated allocations

Source: J.P. Morgan Asset Management, as at 31 May 2018. The Fund is an actively managed portfolio, holdings, sector weights, allocations and leverage, as applicable are subject to change at the

discretion of the Investment Manager without notice.

Tra

dit

ion

al

56

%

So

ph

isti

ca

ted

44

%

Volatility in isolation Marginal volatility

So

ph

isti

ca

ted

Tra

dit

ion

al

So

ph

isti

ca

ted

Tra

dit

ion

al

Increase riskDecrease risk

Risk

management

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

34 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Gross exposure over time

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%Equity Fixed Income Currency Advanced derivatives

Fund gross exposure by asset class and total net exposure since process change*

Risk

management

Source: J.P. Morgan Asset Management, as at 31 May 2018. Equity, fixed income and currency derivatives are included in ‘Equity’, ‘Fixed Income’ and ‘Currency’ respectively; the remaining derivative

strategies are reflected in ‘Advanced derivatives’. The fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of

the Investment Manager without notice.

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

35 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Regular and detailed client communication

Webcast is available through BrightTalkTM.

Semi-annual macro theme updatesMonthly webcast on macro strategy Monthly fund commentary

36 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

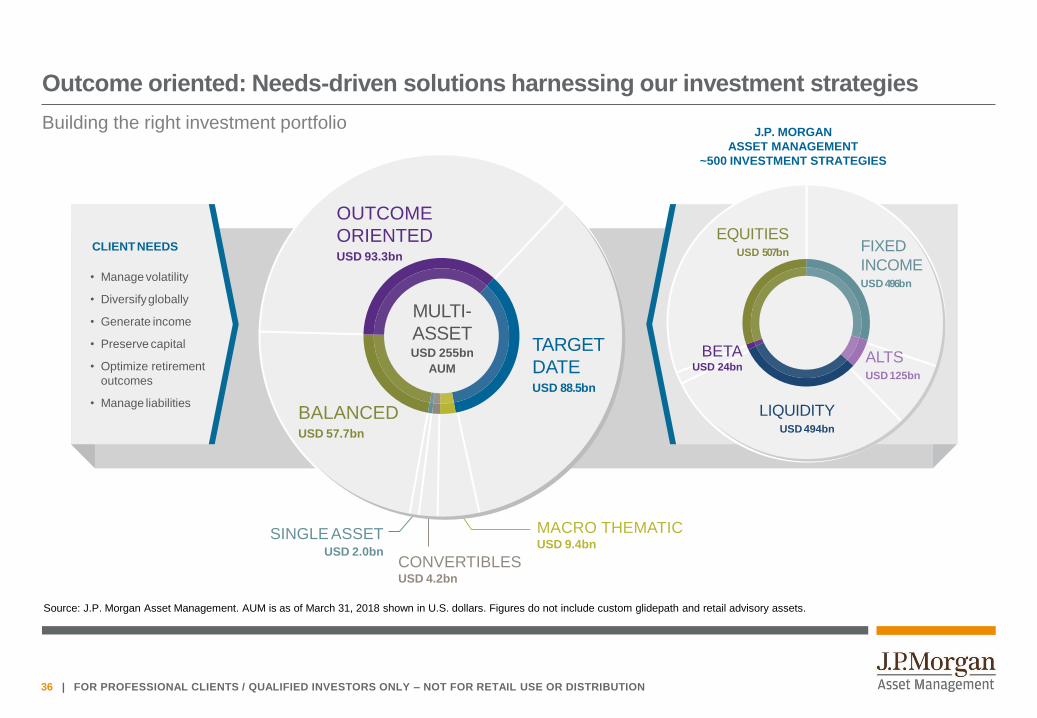

Outcome oriented: Needs-driven solutions harnessing our investment strategies

Building the right investment portfolio

Source: J.P. Morgan Asset Management. AUM is as of March 31, 2018 shown in U.S. dollars. Figures do not include custom glidepath and retail advisory assets.

CLIENTNEEDS

• Manage volatility

• Diversifyglobally

• Generate income

• Preserve capital

• Optimize retirement

outcomes

• Manage liabilitiesBALANCEDUSD 57.7bn

TARGET

DATEUSD 88.5bn

OUTCOME

ORIENTEDUSD 93.3bn

MACRO THEMATICUSD 9.4bn

CONVERTIBLESUSD 4.2bn

SINGLEASSETUSD 2.0bn

J.P. MORGAN

ASSET MANAGEMENT

~500 INVESTMENT STRATEGIES

MULTI-

ASSETUSD 255bn

AUM

FIXED

INCOMEUSD 496bn

EQUITIESUSD 507bn

ALTSUSD 125bn

LIQUIDITYUSD 494bn

BETAUSD 24bn

37 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

J.P. Morgan Multi-Asset Solutions: An integrated approach to multi-asset investing

See “Additional information” at the back page of this presentation for further information.

ACTIVELY SHARING

EXPERTISE

Global integration is central to our research-driven investment process

• 80+ multi-asset investment professionals, one dedicated research platform

• Access to USD 1.7 trillion global platform with ~500 investment strategies

• Ability to leverage 1,100 investment professionals across asset classes and regions

BUILDING THE RIGHT

PORTFOLIO

Outcome-oriented solutions built around client needs

• Grown to USD 255 billion AUM across 79 multi-asset strategies

• Innovative portfolios integrating investment needs of institutional and individual clients

• Multi-dimensional approach to risk analysis and management

EMPOWERING BETTER

DECISIONS

Insights and guidance to invest with conviction

• Proprietary Long-Term Capital Market Assumptions

• Asset allocation views based on a combination of quantitative and qualitative insights

• Insights from portfolio managers and analysts across investment platforms

TAPPING INTO

PROVEN SUCCESS

45-year history of leadership and innovation

• Top 10 multi-asset mutual fund manager

• 34 multi-asset funds rated 4- or 5-stars by Morningstar

38 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

JAMES ELLIOTManaging Director

Chief Investment Officer (“CIO”) of the International business of the Multi-Asset Solutions team, based in London. James is responsible for investment oversight of all mandates managed by the Multi-Asset Solutions team in London and Hong Kong, in addition to contributing to the team’s views on broad macroeconomic themes that are reflected across all portfolios managed globally by the Multi-Asset Solutions team. James is also responsible for managing global macro portfolios. James joined J.P. Morgan in 1995. Prior to his current role, James was CIO for the JPMAM Japanese Equity Portfolio Group based in Tokyo and, previously, was co-head of the JPMAM European Equity Group based in London. James left J.P. Morgan for a period of time and worked at RAB Capital plc, where he served as the Director of Europe Equities and manager of the RAB Europe Long/Short Fund. He obtained a B.A. in Modern History from the University of Oxford and is a CFA charterholder.

SHRENICK SHAHManaging director

Portfolio manager in the Multi-Asset Solutions team, based in London, with responsibility for managing global macro portfolios. An employee since

September 2010, Shrenick previously worked in the equity divisions at Deutsche Bank and Credit Suisse. Shrenick obtained a M.Sc. in Econometrics

and Mathematical Economics from the London School of Economics.

Biographies

Portfolio Managers

Source: J.P. Morgan Asset Management, as at 31 May 2018.

39 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

J.P. Morgan Asset Management

Contacts

Nicola Rawlinson

Executive Director

Client Portfolio Manager, Multi-Asset Solutions

+44 (0) 20 7742 5385

Yuejue Jin

Vice President

Client Portfolio Manager, Multi-Asset Solutions

+852 2800 2891

Mark Jackson

Vice President

Client Portfolio Manager, Multi-Asset Solutions

+44 (0) 20 7742 7022

Olivia Mayell

Managing Director

Client Portfolio Manager, Multi-Asset Solutions

+44 (0) 207 742 5467

Jakob Tanzmeister

Executive Director

Client Portfolio Manager, Multi-Asset Solutions

+44 (0) 20 7742 4914

Jeffrey Wang

Vice President

Client Portfolio Manager, Multi-Asset Solutions

+852 2800 6055

Source: J.P. Morgan Asset Management, as at 31 May 2018.

40 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Share classes

Source: J.P. Morgan Asset Management. Minimum subscriptions may vary depending on initial /subsequent subscriptions. Please note that certain share classes have eligibility criteria which must be

met, details can be obtained from the prospectus.

Share class

Launch date ISINBloomberg

identifierSEDOL

Minimum

subscription1

JPM Global Macro Opportunities A (acc) - EUR 10/23/1998 LU0095938881 JPMECAA LX 5671304 35,000

JPM Global Macro Opportunities A (dist) - EUR 06/1/2006 LU0247991580 JPMGCAA LX B11P3F6 35,000

JPM Global Macro Opportunities A (inc) - EUR 06/1/2006 LU0247992398 JPMGCAI LX B11P3S9 35,000

JPM Global Macro Opportunities C (acc) - EUR 02/26/1999 LU0095623541 JPMECAC LX 5671360 10,000,000

JPM Global Macro Opportunities C (dist) - EUR 07/22/2015 LU0848065107 JPMGCAB LX B89LQW3 10,000,000

JPM Global Macro Opportunities C (inc) - EUR 02/4/2016 LU1314349108 JPGMCIE LX BYSRL29 10,000,000

JPM Global Macro Opportunities D (acc) - EUR 12/12/2001 LU0115098948 JPMECAD LX 7322020 5,000

JPM Global Macro Opportunities I (acc) - EUR 02/8/2016 LU0248010471 JPGMIAE LX B12CMT3 10,000,000

JPM Global Macro Opportunities T (acc) - EUR 06/27/2011 LU0605964500 JPMGCET LX B609VF0 5,000

JPM Global Macro Opportunities X (acc) - EUR 04/25/2006 LU0098446601 JPMECAX LX 7249215

JPMorgan Investment Funds – Global Macro Opportunities Fund

as at 31 May 2018

41 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Fees and expenses

*Shares of X Share Classes may only be acquired by Institutional Investors who are clients of the Management Company or JPMorgan Chase & Co. and (i) which meet the minimum account

maintenance or qualification requirements established from time to time for JPMorgan Chase & Co. client accounts and/or (ii) whose Share Class X Shares will be held in a JPMorgan Chase & Co. client

account subject to separate advisory fees payable to the Investment Manager or any of its affiliated companies.

Unless stated otherwise in the Fund specific details, Shares of X Share Classes are designed to accommodate an alternative charging structure whereby a fee for the management of the Fund is

administratively levied and collected by the Management Company or through the relevant JPMorgan Chase & Co. entity directly from the Shareholder. The Annual Management and Advisory Fee is

therefore listed as "Nil" in the Fees and Expenses tables in this appendix, due to it not being levied on the Fund.

The fund will charge an AMC of 0.60% per annum, with operating and administrative expenses of 0.15% per annum

for C share classes.

Share class Initial chargeAnnual management

& advisory fee

Operating &

administrative

expenses

Redemption charge Distribution fee

JPM Global Macro Opportunities A 5.00% 1.25% 0.20% 0.50% Nil

JPM Global Macro Opportunities C Nil 0.60% 0.15% Nil Nil

JPM Global Macro Opportunities D 5.00% 1.25% 0.20% 0.50% 0.70%

JPM Global Macro Opportunities I Nil 0.60% 0.11% Nil Nil

JPM Global Macro Opportunities T Nil 1.25% 0.20% Nil 0.70%

JPM Global Macro Opportunities X* Nil Nil 0.10% Nil Nil

Available hedged share classes

CHF PLN

USD SEK

SGD JPY

GBP AUD

42 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Investment objective and risk profile

JPMorgan Investment Funds – Global Macro Opportunities Fund

Risk profile– The value of equity securities may go down as well as up in response to the performance of individual companies and general market conditions.

– The value of debt securities may change significantly depending on economic and interest rate conditions as well as the credit worthiness of the issuer.

Issuers of debt securities may fail to meet payment obligations or the credit rating of debt securities may be downgraded. These risks are typically increased

for emerging market and below investment grade debt securities.

– In addition, emerging markets may be subject to increased political, regulatory and economic instability, less developed custody and settlement practices,

poor transparency and greater financial risks. Emerging market currencies may be subject to volatile price movements. Emerging market and below

investment grade debt securities may also be subject to higher volatility and lower liquidity than non emerging market and investment grade debt securities

respectively.

– The credit worthiness of unrated debt securities is not measured by an independent credit rating agency.

– The value of securities in which the Sub-Fund invests may be influenced by movements in commodity prices which can be very volatile.

– Convertible bonds are subject to the credit, interest rate and market risks stated above associated with both debt and equity securities and to risks specific to

convertible securities. Convertible bonds may also be subject to lower liquidity than the underlying equity securities.

– The Sub-Fund may be concentrated in, and have net long or net short exposure to, industry sectors, markets and/or currencies. As a result, the Sub-Fund

may be more volatile than more broadly diversified funds.

– The value of financial derivative instruments can be volatile. This is because a small movement in the value of the underlying asset can cause a large

movement in the value of the financial derivative instrument and therefore, investment in such instruments may result in losses in excess of the amount

invested by the Sub-Fund.

– The possible loss from taking a short position on an asset may be unlimited as there is no restriction on the price to which the asset may rise. The short

selling of investments may be subject to changes in regulations, which could adversely impact returns to investors.

– Movements in currency exchange rates can adversely affect the return of your investment. The currency hedging that may be used to minimise the effect of

currency fluctuations may not always be successful.

Investment objectiveTo achieve capital appreciation in excess of its cash benchmark by investing primarily in securities, globally, using financial derivative instruments where appropriate.

43 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Additional information

The number of ‘investment professionals’ includes portfolio managers, research analysts, traders and investment specialists with VP title and above. Sourced from J.P. Morgan Asset Management; as

of March 31, 2018

‘Top 10 multi-asset mutual fund manager’ is sourced from J.P. Morgan Asset Management analysis based on data from Strategic Insight; multi-asset mutual fund peer group is global and excludes

target date funds; based on global data as of March 31,2018.

DC Multi-Asset Fund Manager of the Year – UK Pension Awards. 2017 UK Pension Awards.

Morningstar® Awards 2014. Morningstar, Inc. All rights reserved. The 2014 U.S. Allocation Fund Manager of the Year was awarded to the SmartRetirement team for the management of the JPMorgan

SmartRetirement Target Date Series (Institutional shares). Subsequent winners in the Allocation category were not target date funds. In 2015, Michael Reckmeyer and John Keogh won in the

Allocation category for Vanguard Wellesley Income Fund. In 2016, the Equity and Fixed Income Investment Policy Committees won the Allocation and Alternatives (combined) category for Dodge &

Cox Balanced Fund. Nominations in Morningstar’s Allocation or Allocation/Alternatives categories were awarded in 2012, 2014 and 2017.

The “mutual funds with a 4/5 star rating” analysis is sourced from Morningstar for all funds with the exception of Japan-domiciled funds; Nomura was used for Japan-domiciled funds. The analysis

includes Global Investment Management open-ended funds that are rated by the aforementioned sources. The multi-asset classification used in the illustration is based on J.P. Morgan’s own

categorization. The share class with the highest Morningstar star rating represents its respective fund. The Nomura star rating represents the aggregate fund. Other share classes may have different

performance characteristics and may have different ratings; the highest rated share class may not be available to all investors. All star ratings sourced from Morningstar reflect the Morningstar Overall

RatingTM. For Japan-domiciled funds, the star rating is based on the Nomura 3-year star rating. Funds with fewer than three years of history are not rated by Morningstar nor Nomura and hence

excluded from this analysis. Other funds which do not have a rating are also excluded from this analysis. Ratings are based on past performance and are not indicative of future results.

The Morningstar RatingTM for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end

funds, and separate accounts) with at least a three-year history. Exchange traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated

based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding

consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom

10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable)

Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10- year

rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most

recent three-year period actually has the greatest impact because it is included in all three rating periods. Rankings do not take sales loads into account.

44 | FOR PROFESSIONAL CLIENTS / QUALIFIED INVESTORS ONLY – NOT FOR RETAIL USE OR DISTRIBUTION

Important Information

For Professional Clients / Qualified Investors only – not for Retail use or distribution

This is a marketing communication and as such the views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto.

Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan

Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan

Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P.

Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed

as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in

accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on

the value, price or income of the products or underlying overseas investments. Past performance and yield are not a reliable indicator of current and future results. There is no

guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no

assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates

worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and

internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy

www.jpmorgan.com/jpmpdf/1320694304816.pdf. As the product may not be authorized or its offering may be restricted in your jurisdiction, it is the responsibility of every reader to

satisfy himself as to the full observance of the laws and regulations of the relevant jurisdiction. Prior to any application investors are advised to take all necessary legal, regulatory

and tax advice on the consequences of an investment in the products. Shares or other interests may not be offered to, or purchased, directly or indirectly by US persons. All

transactions should be based on the latest available Prospectus, the Key Investor Information Document (KIID) and any applicable local offering document. These documents

together with the annual report, semi-annual report and the articles of incorporation for the Luxembourg domiciled products are available free of charge upon request from

JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, your financial adviser or your J.P. Morgan Asset

Management regional contact. In Switzerland, JPMorgan Asset Management (Switzerland) LLC, Dreikönigstrasse 21, 8002 Zurich, acts as Swiss representative of the funds and

J.P. Morgan (Suisse) SA, 8 Rue de la Confédération, 1204 Geneva, as paying agent of the funds.

This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg,

R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited which is authorised and

regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

0903c02a8101cd9e