june 2008 cfa institute annual conference inside ... documents/newsletter/cfa...seller freakonomics,...

TRANSCRIPT

June 2008InsIde:

edItor’s note . . . . . . . . . . . . . . . . 2

PresIdent’s Letter . . . . . . . . . . 3

CFA ConFerenCe FeAtures: unobserved Incentives & the Impact of economics on daily Life . . . . . . . . 4

Impact of the Highly Improbable: randomness & Black swan Blindness . . . . . . . . . . 8

Investment tHeme: this is Your Brain on the market . . . . . . . . . . . . . . 5 – 7

IndustrY deveLoPment: Global Integration and Growth of Global middle Class during the next 25 Years . . . . . . . . . . . . . 10

uPComInG events . . . . . . . . . 10

memBer rePort . . . . . . . . . . . . 11

CFA Victoria members Millie Chow, CFA, (left) and Vicky Ng, CFA, (right) warm up to the spirit of the

2008 CFA Institute Annual Conference in Vancouver.

“You can’t reward people for making bad eco-nomic choices.” Steven Levitt discusses incorrect assumptions about causations and correlations and how economics often disproves conventional wisdom. Presentation synopsis on page 4.

Published by CFA Victoriawww.cfavictoria.com

CFA Institute Annual Conference vancouver 2008

Nassim Nicholas Taleb hits his stride as he expounds upon the pitfalls related to statistical techniques and financial modeling in estimating risk. Presentation synopsis on page 8.

opinions expressed in the CFA victoria newsletter do not necessarily represent those of the authors’ firms of employment or of CFA victoria and do not constitute a solicitation for the purchase or sale of any financial instruments . Information herein is obtained from various sources and is not guaranteed for accuracy or completeness . the authors’ firms and CFA victoria there-fore disclaim any liability arising from the use of information in this publication .

newsletter

Do you have a story idea or a topic that will interest and inform CFA Victoria members? Send an e-mail to let us know what you would like to see in the newsletter or if you want to write something yourself.

Potential topic areas include, but are not limited to:• Industrydevelopments• Investmentthemes• Profilesofnotablemembers

Ifyouhaveanideaforanarticle, please send it toGord Walker, [email protected]

editor’s noteGord Walker, CFA

Welcome to the inaugural issue of the CFA victoria newsletter . this issue is a milestone for CFA victoria . the society has grown to where it can now regularly provide such a report to members and others, al-lowing them to become more aware of CFA victoria’s goals and activities . I hope you enjoy reading this first effort and all of our subsequent issues .

the launch of this newsletter fortuitously coincided with CFA vancouver hosting the 2008 CFA Institute Annual Conference, whose theme was Connecting theory and Practice: Investment management in the Global economy . Given the added interest of this year’s Conference being held just a short float-plane ride away, this issue of the CFA victoria newsletter prominently features material from the Conference . We have two CFA Conference features, provided by Philippe monier, CFA, and vicky ng, CFA, who at-tended . the first is Philippe’s synopsis of the presentation by the Conference’s opening speaker – steven Levitt of Freakonomics fame . the second is vicky’s synopsis of nassim nicholas taleb’s presentation on the Impact of the Highly Improbable: randomness and Black swan Blindness . Both speakers were a pleasure to listen to, enlightening and entertaining, and Philippe and vicky have each done a fine job of capturing the spirit and content of these sessions for you to enjoy .

A common thread that ran through Levitt’s and taleb’s presentations is that neither of them seemed to have much faith in homo economicus – that rational, perfectly informed, and self-interested individual who is the theoretical cornerstone of conventional economic and investment theory . Following this thread a little further, this issue’s Investment theme examines how flesh-and-blood investors really make decisions and explains some of the biological underpinnings of innate cognitive functions that shape our decision-making processes . We thank the toronto CFA society for allowing us to reprint this article by Anne maggisano, this is Your Brain on the market, from its newsletter, the Analyst .

much of the groundwork necessary to launch the CFA victoria newsletter was done by CFA victoria board members Chelsea Kittleson and Landon downs . they each exemplify how volunteers can best give back to the profession and the community, and I thank them for their efforts .

Wrapping up, I’d like to say how much I personally enjoyed attending the CFA Institute Annual Confer-ence in vancouver and how impressed I was with the character of the individuals I spoke to there, evi-dent in their knowledge, intelligence, and commitment to enhancing our profession . the CFA charter is not a credential easily earned, but charterholders can deservedly take pride in belonging to a select group whose membership is based on merit and integrity . In a small way, the CFA victoria newsletter is intended to help CFA victoria members benefit more fully from the privilege of belonging to this com-munity and enable others to better understand what the CFA designation represents .

Share your knowledge and insights with readers of the CFA Victoria Newsletter

Newsletter June 2008

2

President’s LetterAnna nemeth, CIm, CFA

In 1997 CFA victoria was founded, with just 14 members, as a Chapter of the vancouver society of Financial Analysts . today we have our own society, which has grown to 80 members . to guide the future development of CFA victoria, our board of directors recently developed the society’s first strategic plan to lead CFA victoria to 2012 and beyond . our mission is to

1 . Promote professional excellence and the highest ethical standards

2 . support society members and CFA candidates through informative, relevant education, and networking opportunities

3 . Build awareness of the CFA Charter within the local community

In keeping with this mission, CFA victoria has held many events over the past year where attendees had the opportunity to hear interesting and highly qualified speakers discourse upon various financial issues . Andrew shortreid, vice President and Program Chair, has done a wonderful job organizing these events, which altogether represent six hours of Professional development (Pd) credits . notable among the speakers was noreen Harrington, the whistle-blower who tipped off new York Attorney General eliot spitzer to illicit trading in mutual funds in 2003; noreen captivated attendees at both our CFA victoria Candidate reception and our Christmas dinner/Charter Award Ceremony .

We have also sought to raise the profile of the CFA designation and of CFA victoria . Jeff Good, Pub-lic Awareness Chair, and Chelsea Kittleson, education Chair, have both been instrumental in this . A highlight of our public awareness campaign is the society’s sponsorship of the arts in victoria through the victoria symphony, Pacific opera of victoria, the victoria operatic society, and the Belfry and the Langham Court theatres . CFA victoria is also lead sponsor for two upcoming shows at the Art Gallery of Greater victoria .

on the educational side, Chelsea has organized information sessions at uvIC for CFA candidates as well as the Boston mock exam for candidates wishing to confirm their ‘battle-readiness’ a month before the actual CFA exams . Furthermore, she has administered our scholarship program through which we award up to 10 scholarships to worthy candidates each year .

Financially, CFA victoria is on solid footing . We thank our treasurer, trent moore, for keeping us well within budget and in a surplus position . revenues from job postings and from annual dues are the two biggest contributors to our earnings .

Jeffrey Hamel, our membership and technology chair, has been key in getting our new and improved CFA victoria website launched (www .cfavictoria .com) . moreover, during his tenure the society member-ship has grown by 14% and we are now striving for 100 members within the next three years .

CFA victoria’s success has come through the hard work and countless volunteer hours of our current and past boards . I am fortunate to have had the privilege of working with such enthusiastic, creative and dedicated individuals during my six years of involvement with the society . Leaving our board this year are Chelsea Kittleson and Landon downs, both of whom have contributed much to the society . I thank them on behalf of our board and our members . In addition, I offer special thanks to sue-Anne Fimrite, Past President, who has been involved with the board since inception and has contributed hundreds of volunteer hours over the past 11 years . We will miss her energy and effervescence .

In closing, I urge all members to consider volunteering to help CFA victoria better serve our members and fulfill our mission . Participating on a society committee is a good way to expand your network with-in the financial community and enhance your career opportunities . We are always looking for members willing to contribute some of their time, energy and ideas . Please contact me at anna .nemeth@td .com if you would like more information on how you can help .

NewsletterJune 2008

3

steven d . LevItt, CoAutHor oF the best-

seller Freakonomics, and dubbed “the Indiana

Jones of economics” by the Wall street

Journal, was opening speaker at the CFA

Institute Annual Conference in vancouver on

may 11, 2008 . director of the Becker Center

on Chicago Price theory at the university of

Chicago, Levitt is noted for his pioneering

work on natural experiments in econom-

ics . A witty and entertaining presenter who

analyses economic activities with a somewhat

disconcerting approach, there is little doubt

that he entertains his students while educat-

ing them in his brand of economics .

Levitt began by illustrating the value of

incentives, telling the story of an Inter-

nal revenue services employee, John

szilagyi, who was struck by the odd

names of children listed as dependents

on tax returns – names such as “Fido” .

szilagyi suggested in the early 1980s that a

social security number be required for each

child claimed on the tax form, but it took five

years and considerable persistence on his

part before the change was implemented .

After the change, a sudden ‘disappearance’

of some seven million children in the u .s .

occurred, obviously children invented for

the purpose of cheating on income tax . this

simple innovation championed by szilagyi

saved the government roughly $2 billion

a year from fraudulent claims, but the only

reward he eventually received was a $25,000

bonus .

one lesson from this story is that incentives

strongly influence not only the decision to

cheat, but also the generation of ideas . thou-

sands of Irs employees over several decades

could have had the same insight as szilagyi,

but in a situation where initiative and change

were not valued they had little incentive to

act on such an idea . Another lesson is that

while ideas seem scarce, even breakthrough

ideas are easy to find if you really look . Levitt

stated, though, that one often needs to “fight

through conventional wisdom” .

Levitt explained that he is not the kind of

economist who makes big statements on

how the world works, and claimed that many

economists today are actually less interested

in the economy than in math . A Harvard

graduate and a Ph .d . in economics from mIt,

he surprisingly admitted to being poor in

mathematics himself, relying in his work on

not much more than a good knowledge of

economics .

explaining why his career took the path it has,

Levitt said his father advised young steven

to follow his example and concentrate on

what steven was good at . Levitt senior was a

medical doctor who specialized in medicine

regarding intestinal gas, an area where he

expected little competition . ultimately, he

became a top-ranked specialist in that area .

taking his father’s advice to heart, steven

Levitt concentrated on the empirical study of

the stuff and riddles of everyday life, and his

conclusions regarding these matters regularly

turn conventional wisdom on its head . In this

area, now sometimes referred to as Freako-

nomics, Levitt expected little competition

among economists!

to give an example of the sort of questions

that interest him, Levitt told the story of a

man who started a business selling dough-

nuts in company offices . trusting people

to be honest, in each office he left a box of

doughnuts with a price list and a locked box

in which people paid . most people liked the

service and paid honestly, so the business was

a success with net annual revenues of some

$100,000 in the 1980s . the entrepreneur then

offered Levitt a mass of data on his business,

which he had conscientiously recorded each

day for 15 years, asking if Levitt could find

ways to improve the business . Levitt then

built a model to optimize profitability,

but his complex algorithm showed that

he could improve net revenues by, at

best, $200 a year!

during the process, though, Levitt dis-

covered that this business operator had

raised prices only four times in those 15 years .

Levitt thought that although the business

model was good, the operator was probably

under-pricing . While the operator had daily

feedback on the quantities of doughnuts he

should supply at each location, he had little

feedback on how customer demand reacted

to price changes . Without empirical data, his

ability to confidently make pricing decisions

was limited .

Levitt said that since the publication of

Freakonomics, other business leaders had

asked him for advice . He generally was happy

to provide his services … for free … the

only condition being that these businesses

allow him to use the data he collected for his

published research . However, the impact of

his efforts has not always been as productive

as it could be .

unobserved Incentives and the Impact of economics on daily LifePhilippe monier, CFA

Continued on page 9.

CFA ConFerenCe FeAtures

If you give people bad incentives, then things go wrong.

Newsletter June 2008

4

this is Your Brain on the marketBy Anne maggisano, CIm Reprinted from The Analyst, March 2008, courtesy of the Toronto CFA Society.

“Man will become better when you show him what he is like.” – Anton Chekhov, as quoted by Steven Pinker in The New York Times Magazine (January 13, 2008)

Continued on next page.

Investment tHeme

tHe ImPACt And sCoPe oF evolutionary

psychology is hard to ignore these days .

In the popular press, the new York times

magazine recently featured an article by

steven Pinker as its cover story, arguing that

human morality must be understood to have

a biological cause . If this isn’t indicative of a

move to the mainstream, then one only has

to look to the institutional bastions of finance

to understand how what was at one time a

controversial topic has now become

the norm . Harvard university offers an

annual education course for executives,

“Investment decisions and Behav-

ioural Finance,” designed to illuminate

how our human decision-making

process can be applied to the invest-

ment context . the most prestigious of

finance institutions, CFA Institute, chooses to

offer their “efficient markets and Behavioural

Finance” webcast program for free on their

web page . our very own toronto CFA society

re-invited terry Burnham, author of mean

markets and Lizard Brains: How to Profit from

the new science of Irrationality, to speak for a

second time at a luncheon seminar in January

of this year .

this article reviews developments in the

realm of cognitive psychology and their

implications for our understanding of market

efficiency . specifically, it demonstrates how

our individual and collective decision-making

processes provide a mechanism to explain

how and why markets become inefficient

for periods of time . through understanding

the mechanism of irrationality, investors can

profit in two ways . First, by learning how to

systematically manage their own individual

decision-making biases . second, by identify-

ing opportunities that arise when capital mar-

kets become inefficient due to widespread

biased decision-making .

Involuntary decision-making

Functional mrI neuroimaging studies show

that much of our decision-making is low-level

processing, occurring in the oldest parts of

the brain from an evolutionary standpoint:

the limbic system, basal ganglia and brain-

stem . these low-level processes are designed

to pick up regularities in the environment

unconsciously and automatically, without our

control or awareness of them . For example,

daniel Levitin in his book this Is Your Brain on

music summarizes how this part of the brain

detects and processes the meter, pitch, and

loudness of a song instinctively, motivating

our assumptions about the song even before

higher-level cortical areas that are involved in

knowledge, cognition, and memory become

involved . For investors looking at stock mar-

ket price fluctuations, the hard-wiring in our

brain unconsciously recognizes patterns such

as rising prices, motivating our conviction

that future prices will follow that trend . the

brain continuously updates its expectations

about the future, taking immense satisfaction

(an emotional response) when the real world

matches our predicted expectations .

In fact, scientists have discovered that our an-

ticipation or expectation of a reward (i .e . that

stock prices will go up) activates the nucleus

accumbens, the part of the ancient brain that

mediates pleasure and positive well-being

through the neurotransmitter dopamine . this

sets up a positive feedback “reward system”

whereby past performance sets up expecta-

tions that the trend will continue, activating

the release of dopamine into the nucleus

accumbens and creating emotions of excite-

ment, pleasure, and greed . For example,

when we buy a lottery ticket or a stock that

we believe is a clear winner, the possibility of

financial gain activates the reward sys-

tem even without the outcome of win-

ning the money . moreover, if in fact we

do make money, we will become more

excited about the possibility of making

money again and we will be more likely

to re-create the conditions that entail

the possibility of making money again .

many things other than money that are found

rewarding also work through this positive

feedback system: beautiful faces, exercise,

food, the anticipation of narcotics . Because

the greed and emotion from this reward sys-

tem lies below our level of awareness, it drives

our behaviour without any involvement of

the higher cortical areas of the brain that are

intimately involved in conscious cognition .

there is a second system that is implicated

in our unconscious decision-making: the

loss-avoidance system . once we understand

that our ancestral brain is designed to detect

regularities in our environment, we can

conceive how it is equally responsive to any

change in that environment because change

could signal imminent danger . For example,

Many things other than money that are found rewarding also work through this

positive feedback system: beautiful faces, exercise, food, the anticipation of narcotics.

NewsletterJune 2008

5

when we predict that a stock price will con-

tinue to follow its upward trend, but it in fact

reverses direction, our brain senses the break

in trend and activates that part of the brain

that generates our emotional responses of

fear and anxiety (the amygdala) . once again,

it is the anticipation that something bad will

happen—the pain of loss—that guides our

intuitive response to flee, whether that be

running away from a lion, or selling a stock

immediately . Implicated in the loss-aversion

system is the release of noradrenaline from

the locus coeruleus, a hormone that leads

to the panic reaction that can shut down

other systems, including the frontal cortex .

once again we can see that contrary to what

we would expect, it is our primal base-level

responses that are driving our behaviour, and

they operate somewhat independently of

our higher cognitive levels of thinking and

rational decision-making .

Collective decision-making

these studies have been extended to

understand how individuals make decisions

in the context of a large group . the most

well-known study of social conformity and

social independence was performed in the

1950s by solomon Ash . Individuals are asked

which line (A, B, or C) is equal in length to line

X . most people choose the correct answer A

when they are asked on their own . However,

when positioned in a group setting where a

significant proportion of the members are

primed to give an incorrect answer, that same

individual will change his/her answer to con-

form to the group norm .

Friday July 11, 2008

Olympic View Golf Course(www.golfbc.com/courses/olympic_view)

Golf (including cart) and dinner$125 (CFA Victoria Members) and $150

(non-Members), Dinner only: $40Ifyourcompanywouldliketosponsorahole,

the cost is $100(Prizes are encouraged as well)

Please contact Charles (see below) for more information

First tee-off time is 12:00, last tee-off time will be approximately 14:00

Texas Scramble formatPrizes for Best score, Worst score,

Closest to the pin, Longest drive, etc.BBQ dinner starts at approximately 6:00pm

To reserve, please send the following information as soon as possible to:

GOLF TOURNAMENTAttn: Charles Volkovskis

Email: [email protected], Fax: (250) 387-7874

Name, Company Society Member: Yes/No

Club Rentals: Yes/No Skill Level: Good/Average/Bad

Special Requests: foursome, tee-time, etc.

Make cheques payable to: CFAVICTORIA

Forward to: Charles Volkovskis

bcIMC,3rdFloor,2940JutlandRoad,Victoria, BC, V8T 5K6

“This is Your Brain on the Market” continued from page 5.

CFAVICTORIA

12th Annual Golf Tournament

Continued on next page.

Investment tHemeNewsletter June 2008

6

Gregory Burns extended this study to deter-

mine if social conformity, or agreeing with the

group even when the group is incorrect, is a

result of conscious decision-making . using

functional mrI technology to map the brain,

he discovered that social conformity does

not result in activation of the cortex and

hence is not a result of conscious decision-

making . more significantly, social conformity

activates the regions of the brain involved in

instantaneous perception, suggesting that

our perception can be altered by social influ-

ences . In contrast, social independence from

the group, or standing up for one’s beliefs in

the face of group opposition, activates the

amygdala—that region of the brain that is

involved in the emotion of fear and the

activation of the loss-aversion system .

these studies suggest that social

conformity is once again an instinctive

process, mediated either by an uncon-

scious change in our perception or an

aversion to the fear response and the

potential for pain .

How does our decision-making affect

market efficiency?

under conditions of market efficiency, the

market price of an investment reflects an

unbiased estimate of its value . For practical

purposes, what this means is that investors

are unable to consistently and systemati-

cally beat the market and the best course of

action is to choose indexation over active

management . However, there are moments

when markets display inefficiencies—most

noticeably during speculative bubbles and

crashes—and investors can choose to exploit

these moments for profit .

one explanation for how market efficiency

comes about is put forward by William sharpe

and michael mauboussin among others as the

“Wisdom of Crowds” approach . the Wisdom

of Crowds theory of market efficiency argues

that there are three necessary and sufficient

conditions under which markets are efficient:

diversity, aggregation, and incentives . A

market is efficient if it is cognitively diverse,

if there is a method by which to bring the

information together, and if there are incen-

tives for being right . However, if one of these

three conditions breaks down, then markets

become inefficient .

Accepting the assumptions of the Wisdom

of Crowds theory, the results of behavioural

finance threaten market efficiency at the level

of diversity . more specifically, as mauboussin

points out, it is not the irrational behaviour of

individuals that threatens market efficiency,

but rather the behavioural tendencies for so-

cial conformity that are implicated in market

inefficiencies . this view is also expressed by

William sharpe, nobel prize winning econo-

mist: “the basic argument [of the Wisdom

of Crowds] is that if we have enough people

even though they may be ill-informed and

irrational coming to market, it is entirely pos-

sible the prices of assets, thereby true risks

and rewards, are what you would get if they

were all rational and well informed .”

What this means is that investors must look

for signs of behavioural social conformity in

the marketplace as an indicator for market

inefficiency . such signs can appear in the

popular press and/or in the markets them-

selves and take the form of extreme bullish-

ness or bearishness, or sentiments of fear and

greed . In learning to locate social conformity,

one can take advantage of investments that

are priced below their intrinsic value .

How can individuals become

better investors?

the evidence of behavioural studies of

decision-making suggests that humans

generally behave in a sub-optimal manner

when it comes to investing . the studies show

that, broadly speaking, decisions are made

unconsciously in reaction to our hard-wired

tendencies to look for regularities in our

environment and create expectations based

on those patterns or on violations of those

patterns . moreover, our perception of our

environment is unconsciously influenced by

the group context in which we are placed

either out of fear of independence, or

by a change in perception .

studies of our behavioural tendencies

argue implicitly that investors must

put policies and procedures in place

by which to counteract our human,

instinctive drive to act based on sub-

optimal decision-making . For example, one

must objectively calculate the full spectrum

of outcomes for an investment in order to

counteract our instinctive belief that past

trends will continue into the future . Also, it is

imperative to create a list of stocks to buy at

low prices in order to counteract our instinc-

tive drive to sell at market bottoms . third, one

must insulate oneself from daily fluctuations

in market price in order to prevent oneself

from making investment decisions based on

price instead of value . Finally, one can favour

long-term decision-making to counteract

short-term emotional responses . the number

of behavioural modifications to counteract

our instinctive tendencies is endless; however,

by putting into place systematic procedures

to override these tendencies, we may become

better investors .

“This is Your Brain on the Market” continued from page 6.

Investors must put policies and proce-dures in place by which to counteract

our human, instinctive drive to act based on sub-optimal decision making.

Investment tHeme NewsletterJune 2008

7

over tHe PAst 12 montHs a number of

events have rocked the financial markets,

and how many of us can honestly say that

we clearly anticipated such incidents or their

severity? speaking at the CFA Institute Annual

Conference in vancouver on may 12, nassim

nicholas taleb explained why extreme events

are hard to predict and why these events

often have catastrophic impacts . Currently a

visiting professor at London Business school

and formerly dean’s professor in the sciences

of uncertainty at the university of massachu-

setts, Professor taleb is the author of Fooled

by randomness and more recently the Black

swan: the Impact of the Highly Improbable,

two highly regarded books that discuss, often

through anecdote, taleb’s thoughts on how

uncertainty works .

In his presentation, taleb explained that the

central problem concerning extreme events

is that the smaller an event’s probability, the

larger our sample set must be to reliably

estimate that probability, and as the probabil-

ity becomes smaller the more consequential

the impact of any error in estimating it will

be on the magnitude of the actual outcome .

Investors and others in the prediction busi-

ness have to be conscious not only of the

uncertain probability of extreme events, but

also the uncertain magnitude, good or bad,

of these events . How, he asked, do analysts

justify labelling something a 1-in-10,000-year

event when their sample sets cannot cover

nearly so long a time period? His answer:

purely from theory .

Mediocristan vs. Extremistan

modern portfolio management often uses

statistical theory based on the Gaussian

distribution (the normal distribution) to

forecast event probabilities . taleb believes

such theory is valid only in situations of “mild

randomness”, a world he calls mediocristan .

For example, adding one additional data

point to a reasonably large sample set of hu-

man heights will probably not greatly change

the distributive properties of the set because

extreme human heights are not that far from

the mean . In contrast, adding the annual

income of the world’s richest person to a

random sample set of the incomes of 10,000

people would change the sample distribution

considerably . In other words, in some cases

a small number of occurrences can account

for a large proportion of the total outcome .

Another example is that there are about

267,000 drugs available on the market, but

only 5% of all drugs account for most of the

profits of pharmaceutical companies . taleb

provided further examples, pointing out that

tail distributions dominate the likelihood of

social and economic events . these situations

belong to another world, one that taleb

calls extremistan . He warns that there is no

reliable structure in the probability distribu-

tions of extremistan .

taleb believes that statistics and probabil-

ity estimates are irrelevant in forecasting

extreme events and our world is shaped by

the dynamics of extremistan . Although most

people rely on past experience (i .e . data from

previous periods) to forecast the future, past

extreme probability distributions – gener-

ally referred to as tail distributions – are

not indicative of future extreme probability

distributions: previous outliers do not predict

future outliers .

to illustrate the difficulty in more worldly

terms, taleb compared the characteristics

of government change in Italy and in saudi

Arabia: the Italian government changes fre-

quently and somewhat unpredictably (high

volatility), but each change has relatively little

impact; the saudi government changes very

little (low volatility), but a change in govern-

ment could have a severe impact in many

ways (consider the 1979 revolution in Iran) .

Prognosticators also suffer from the fallacy of

single event probability . events in extremistan

do not follow a typical pattern . one might

successfully predict the occurrence of an

event yet be totally wrong about the form

that the event actually takes . An example

of this was the confidence of many knowl-

“I shiver at the thought that something fails.”

the Impact of the Highly Improbable: randomness and Black swan Blindnessvicky ng, CFA

Nassim Nicholas Taleb

CFA ConFerenCe FeAtures

Continued on next page.

Newsletter June 2008

8

edgeable people in 1914 that a few weeks of

limited battle would be enough to decide the

outcome of what tragically became the First

World War .

taleb stated that we therefore need to

consider two layers of stochasticity – one re-

garding event occurrence and one regarding

an event’s impact . even if we could reliably

predict the probability distribution of an ex-

treme event, it will remain difficult to predict

the event’s consequences .

moving on to discuss financial institutions, ta-

leb said that the global banking system used

to look like the governance situation in Italy,

but now looks more like that in saudi Arabia

– “I shiver at the thought that something fails” .

As the banking network (and other networks

such as power transmission grids) comes to

consist of fewer but larger entities, there will

probably be fewer and fewer small shocks

(e .g ., bank runs), but network effects due to

concentration and nonlinearities could make

large, infrequent shocks more consequential

than in the past .

Hedge fund returns are a case of life in

extremistan . A problem in the hedge industry

cited by taleb is that a steady stream of

positive returns (suggestive of an option-writ-

ing strategy) can be suddenly followed by a

suddenly ruinous negative return . one cause

of this problem is the difference between

the time scale used for manager compensa-

tion and that needed to realistically analyze

performance data – a hedge fund manager

will be well compensated during the steady

performance periods, but when disaster

strikes investors could lose all their profits

even though the manager keeps any bonuses

based on previous gains . taleb believes that

many investors expose themselves to such a

hazard because they do not understand the

nature of risk . For example, some people fail

to recognize that exposure to a 1-in-30-year

event is still risky even if their exposure lasts

for only 15 years .

during Q & A, taleb prescribed the use of

qualitative methods in extremistan to avoid

the pitfalls of black swans and wonders why

anybody would rely on a single number to

measure risk, especially one already proven

to be a poor measure . He also reminded the

audience that black swans can have a positive

impact, but cautioned that good black swans

usually happen over time while bad black

swans tend to go “Boom!” .

“The Impact of the Highly Improbable: Randomness and Black Swan Blindness” continued from page 8.

“Unobserved Incentives and the Impact of Economics on Daily Life” continued from page 4.

In one case, a consumer electronics company

approached him for marketing advice . For a

long time, this company had used both tv

advertising three times a year and full-page

ads in sunday newspapers every week in

each major newspaper market . Consultants

brought into investigate the effectiveness of

this advertising had reported a high correla-

tion between sales and the tv advertising,

but found that the newspaper advertising

was much less effective . Levitt was suspi-

cious of these findings and found that the tv

advertising had coincided with dates such

as Christmas and Fathers’ day when sales are

higher than normal regardless of advertising .

In other words, the consultants had confused

correlation with causality .

Levitt suggested testing the newspaper

advertising effectiveness through an experi-

ment where the company would stop adver-

tising in selected markets and compare sales

in those markets with sales in markets where

the ads continued . the company refused to

do this, since the local salespeople in the first

set of markets would be up in arms if news-

paper advertising was interrupted . Interest-

ingly, Levitt found that such an ‘experiment’

had been done inadvertently: an intern’s

mistake had led to no newspaper ads in the

Pittsburgh market for three months – without

any noticeable impact on sales . despite this

evidence, which Levitt felt warranted a more

thorough test, the company continues to

advertise in the sunday papers every week

without knowing if this is a total waste of

money . such is the battle against conven-

tional wisdom!

during the Q & A session, Levitt was asked

what incentives the government should

provide to prevent the sort of problems that

have damaged the Cdo and credit markets

since last summer .

After commenting on various aspects of this

issue, stating that “if you give people bad

incentives, then things go wrong”, he opined

that a government bailout is the worst thing

to do since “you can’t reward people for mak-

ing bad economic choices”, drawing applause

from the audience .

NewsletterJune 2008

9

WARHOL: Larger Than Life Art Gallery of Greater victoria CFA Victoria – lead sponsor

Exhibition may 30 to August 24, Gallery Hours

Reception and Mixer Friday, July 11, 8:00pm

one of the major artistic innovators of the 20th century, Warhol’s fame spread well beyond paint-ing and printmaking . Filmmaker, sculptor, author, collector, publisher, provocateur, music producer, celebrity—Warhol understood and negotiated the ride of fame, a sophisticated arbiter and ma-nipulator of popular culture and fashion .

Warhol: Larger than Life is an expansive project of over 150 paintings, drawings, prints, sculptures, photographs, archival ephemera and films span-ning some four decades of production . Work-ing directly with the Andy Warhol museum in Pittsburgh, PA, the Winnipeg Art Gallery enjoyed full access to its considerable collection of art and archives in organizing this exhibition .

CFA Victoria Annual General Meeting monday June 9, 4:30pm BC Investment management Corporation Boardroom 3rd Floor, 2940 Jutland road, victoria, BC

rsvP: Anna nemeth @ 356-4098 or anna .nemeth@td .com

CFA Victoria hosts Lunch with Westport Innovations Corporate Presentation Late June, check CFA victoria website for details

since 1995, Westport Innovations has engaged in the research, development, and marketing of high-performance engines and fuel systems which use gaseous fuels such as compressed natural gas (CnG), liquefied natural gas (LnG), hydrogen, and hydrogen-enriched compressed natural gas (HCnG) .

For more information on Westport Innovations, go to www .westport .com

CFA Victoria 12th Annual Golf Tournament Friday July 18 olympic view Golf Course See page 6 for further tournament details.

Moss St. Paint-In CFA Victoria – lead sponsor July 19

the Art Gallery of Greater victoria’s Annual moss street Paint-In (a not-for-profit event) features invited professional and emerging artists from victoria and region who demonstrate their art to 30,000 visitors walking moss street from Fort street to dallas road . the Paint-In offers visitors an opportunity to meet and discuss the artists’ work and methods and to see an enormous vari-ety of professional work at one time .

CFA Victoria and Polaris Minerals host a Site Visit to the Orca Quarry Company sponsored visit to industrial site for CFA victoria members and Friends

Port mcneil, BC

mid-August, check CFA victoria website for details For more information on Polaris minerals or the orca Quarry, go to www .polarmin .com

Upcoming CFA Victoria Programs, Events and News

At the CFA Institute 61st Annual Conference,

thomas P .m . Barnett, author of the forthcom-

ing book Great Powers: America and the

World After Bush (January 2009), discussed

the dominant trends that will shape the world

during the next 25 years .

In his presentation, Barnett divided the world

into two groups: those regions that have fully

integrated and those regions that have not .

the former group, which has largely recog-

nized the benefits of economic integration

and globalization, includes north America,

europe, russia, Australia, and parts of south

America . the latter group − Africa, the middle

east, and southeastern Asia − has resisted

the benefits of economic integration and

globalization .

According to Barnett, globalization can act

on a regional basis to reduce the number of

countries that have not integrated . For exam-

ple, China could help vietnam emerge from

the gap, whereas Brazil may eventually have

a similar impact on countries like venezuela .

Barnett suggests the united states could

serve as a model in this process because its

states unified out of mutual self-interest to

promote commerce and common security .

Barnett believes that this integration, with its

own regional variations, will be the dominant

dynamic of the next 25 years .

Additionally, the shift will serve as a catalyst

for interesting, unexpected results . For ex-

ample, Barnett believes that the 21st century

could be the most religious in human history .

He argues that as residents of newly integrat-

ing countries begin to lose a local culture − a

culture that may have been substantially

unchanged for hundreds of years − they

will need to find a new basis for a code of

behaviour . According to Barnett, this search

for spiritual guidance will result in greater

religious pluralism in which far more choices

will be available than in the past .

Global Integration And Growth of Global middle Class during the next 25 Years the 21st century will be “the most religious in human history .”

Continued on page 12.

IndustrY deveLoPmentNewsletter June 2008

10

members on the moveLandon n . downs

to macquarie Capital markets Canada Ltd .

landon .downs@gmail .com

Would you like to be included in members on the move?

It’s important to keep your contact infor-mation up to date and let others know where they can reach you .

Please let us know if you’re changing jobs or making any other move . send your information to Gordon .Walker@rBC .com with “members on the move” in the subject line .

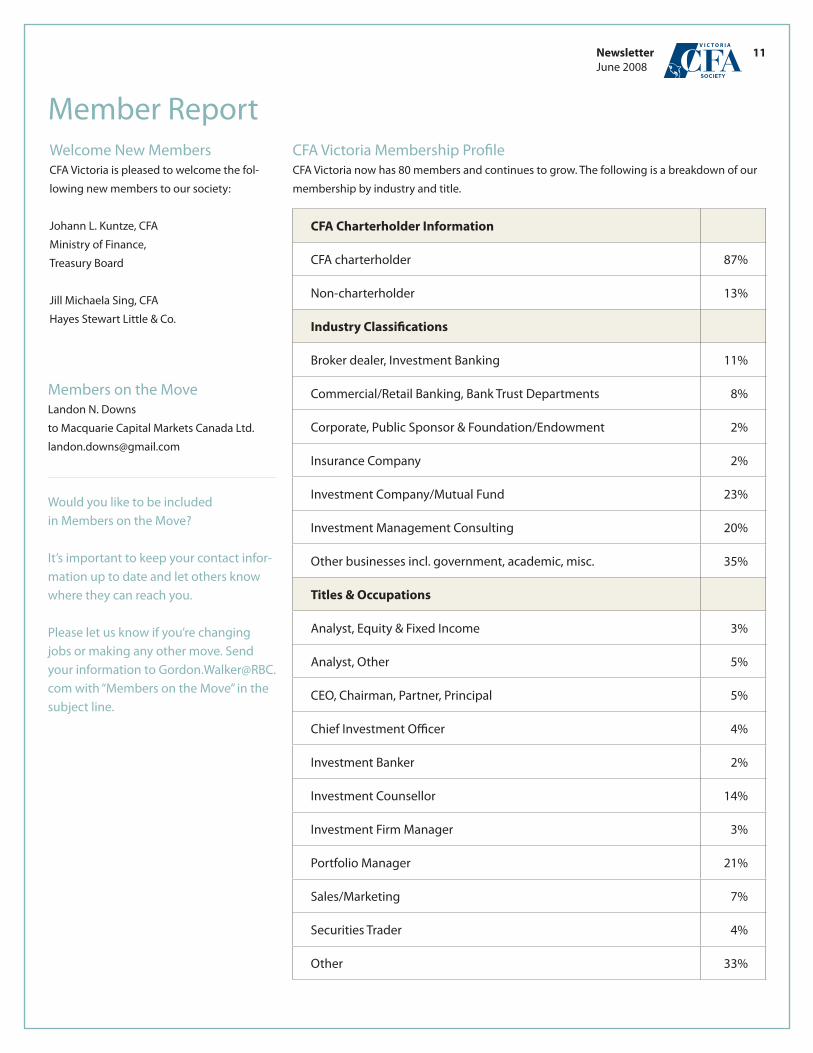

CFA Charterholder Information

CFA charterholder 87%

non-charterholder 13%

Industry Classifications

Broker dealer, Investment Banking 11%

Commercial/retail Banking, Bank trust departments 8%

Corporate, Public sponsor & Foundation/endowment 2%

Insurance Company 2%

Investment Company/mutual Fund 23%

Investment management Consulting 20%

other businesses incl . government, academic, misc . 35%

Titles & Occupations

Analyst, equity & Fixed Income 3%

Analyst, other 5%

Ceo, Chairman, Partner, Principal 5%

Chief Investment officer 4%

Investment Banker 2%

Investment Counsellor 14%

Investment Firm manager 3%

Portfolio manager 21%

sales/marketing 7%

securities trader 4%

other 33%

CFA victoria membership ProfileCFA victoria now has 80 members and continues to grow . the following is a breakdown of our

membership by industry and title .

member reportWelcome new membersCFA victoria is pleased to welcome the fol-

lowing new members to our society:

Johann L . Kuntze, CFA

ministry of Finance,

treasury Board

Jill michaela sing, CFA

Hayes stewart Little & Co .

NewsletterJune 2008

11

officersPresIdent

Annamaria nemeth, CFA

vICe PresIdentAndrew P .A . shortreid, CFA

seCretArYLandon n downs

treAsurertrent Karl moore, CFA

Board of directors sue-Anne Fimrite, CFA

Jeffrey Kenneth Good, CFAJeffrey michael Hamel, CFA

Chelsea m . Kittleson, CFAtrent Karl moore, CFA

Annamaria nemeth, CFAAndrew P .A . shortreid, CFA

Committee Chairs ProGrAm

Andrew P .A . shortreid, CFA

eduCAtIon Chelsea m . Kittleson, CFA

memBersHIP & teCHnoLoGY

Jeffrey michael Hamel, CFA

PuBLIC AWArenessJeffrey Kenneth Good, CFA

voLunteer PuBLIC

AWAreness & ProGrAmsPhilippe monier, CFA

CFA victoria promotes the highest stan-dards of integrity, professionalism and ethical behaviour within the investment industry, and encourages professional development through the CFA Program . We facilitate the open exchange of infor-mation and opinions between members of victoria’s investment community .

CFA victoria mission

A Call for VolunteersCFA Victoria depends on volunteers to enable all of our activities and initiatives.

Youcanhelpbyapplyingyourtimeandskillsinanynumberofways.It’sagreatwaytomeetothersinthelocalfinancialcommunityandshowoffyourtalent.

Interested?Ofcourseyouare!ContactAnnaNemeth at [email protected] for more information.

2007 / 2008 CFA victoria Leadership

the Last Wordthe story that I have to tell is marked all the way through by a persistent tension between

those who assert that the best decisions are based on quantification and numbers, determined

by the patterns of the past, and those who base their decision on more subjective degrees of

belief about the uncertain future . this is a controversy that has never been resolved .

Peter L. Bernstein, Against the Gods – The Remarkable Story of Risk

Barnett’s presentation concluded with obser-

vations about China and its future . He noted

that the Chinese phenomenon is only 25

years old . In that quarter century, China has

gained economic experience that took the

united states 125 years to accumulate .

For a country that would otherwise be char-

acterized as an emerging economy, China has

rather unusual demographics, Barnett said .

the country’s one-child policy has resulted

in a population in which males significantly

outnumber females .

Additionally, China’s population is rapidly

aging . Barnett said that by the year 2036,

20 percent of the population of both China

and the united states will be older than 65 .

Whereas it took 64 years for the u .s . popula-

tion age 65 or older to go from 10 percent to

20 percent, the same change took China less

than 20 years .

Barnett noted that, historically, aging societ-

ies are generally nonbelligerent, and when

they also have rising incomes tend to move

toward political pluralism .

Reprinted in part courtesy of CFA Institute.

“Global Integration...” continued from page 10.

NewsletterJune 2008

12