kambale kisumba kamungele, Éts. tsongo kasereka ... · Éts. tsongo kasereka association des...

TRANSCRIPT

Kambale Kisumba Kamungele, MCE&S

Éts. TSONGO KASEREKA

Association des Exportateurs du Cacao & Café de la R.D. Congo

The 4th African Coffee Symposium« Inclusive Value Chain Transformation of the African Coffee Industry »

Yaoundé, 28 novembre 2016

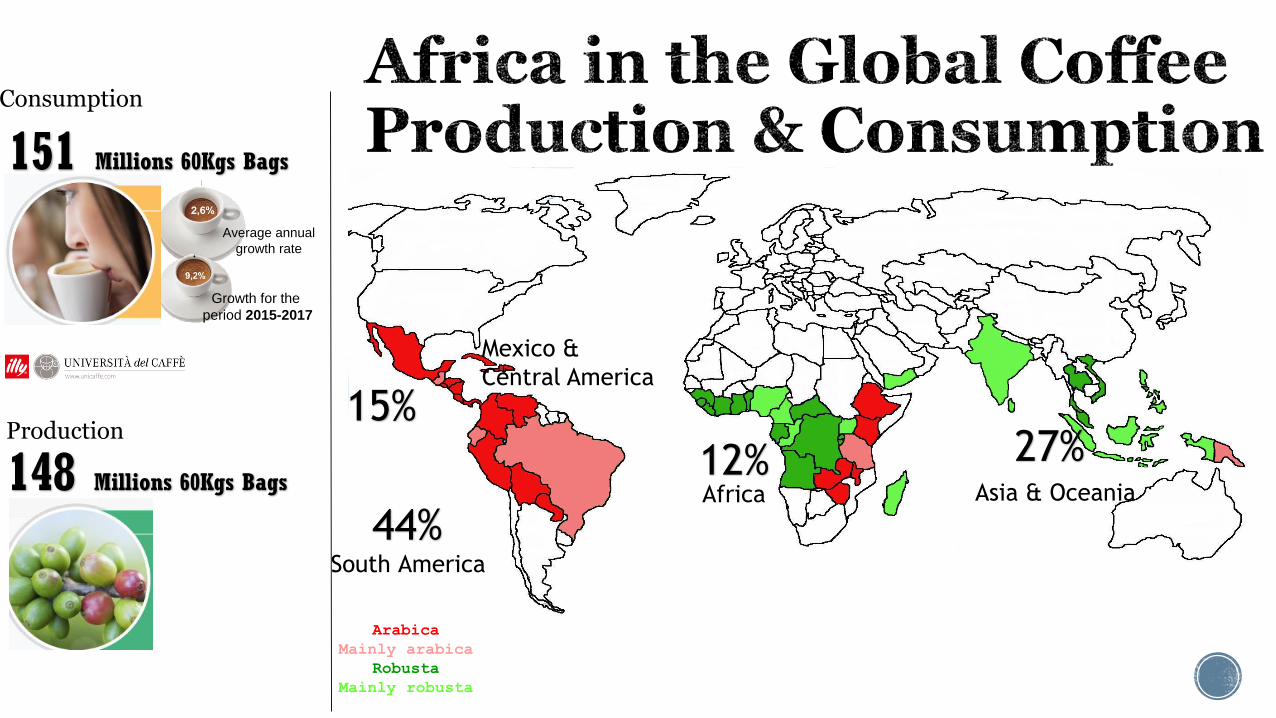

1. Global Coffee Production & Consumption

2. The DR Congo & Coffee

3. The DRC Value Chain

4. Sector Challenges

5. Current Changes in Sector

6. Observed Results

7. Final Comments

Arabica

Mainly arabica

Robusta

Mainly robusta

44%

15%27%12%

151 Millions 60Kgs Bags

148 Millions 60Kgs BagsAfrica Asia & Oceania

South America

Mexico &

Central America

Consumption

Production

Average annual

growth rate

Growth for the

period 2015-2017

THE RDC AT A

GLANCE Area

:

2’345’410 km2

Population : 67’700’000

Coffee-Dependant

Households (ITC) :

800’000

Planted Surface

(ITC) :

200’000 ha

Production (ONC :

2012) :

63’000 MT

Exports Volume

(ONC : 2015) :

9’148 MT

• 3’149 MT Robusta (34%)

• 6’038 MT Arabica (66%)

Endowed with good climate and soil, the DRC has favorable

conditions for the cultivation of both species of Coffee

(Arabica & Robusta)

In 70s & 80s, the DRC was one of Africa’s leading exporters of

coffee.

A new rebirth is on its way in the Congoloee Coffee Sector

-

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

20 Years DR Congo Coffee

Production & Export

(1992 - 2012)

Production Export

Metric Tons

Source : Office National du Café

Marketing System : Direct Sale

Done through 2 channels:

The informal sector : Illicit exit across

porous borders

The formal sector : Officially registered

exporters

• Insufficient ExtensionServices

• Low Quality Produce

• Low Income for Farmers

• Ageing Farmer

PRODUCTION

• Limited & InadequateProcessing Facilities

• Constrained Finance

Limited Quality Knowldge

PROCESSING

COMMERCIALIZATION

• Limited Research Dedicated

to Coffee

• Less Agro-Chemical

Fertilizer Application

• Unsufficient Seedling Access

• Rudimentary Agricultural

Practices

• CWD Outbreak

• Limited & Artisanal Primary

Processing Units

• Old/Limited/Under-utilized

Processing Facilities

• High Cost of Opetation

• Unsuffifcient Roasting

capacity

• Over-Taxation

• High Logistical Cost & Delays

• Inconsistency in Quality

• Contract Fulfillment Reliability

• Finance (Liquidity)

PRO

DU

CTIO

N

TRAN

SFO

RM

ATIO

N

CO

MM

ERCIA

LIZ

ATIO

NFarmers

Aggregation

International

NGO’s Support

Farmer ’s Traning

Emergence of

Organic, Utz, and

FairTrade

Certifications

Washing Stations

Set-up

Coffee Quality

Events (Taste of Harvest & Saveurs du Kivu)

New Dry Mill

(Coffee Lac, Goma)

PPP Development

Farmers-to-Buyer

linking Model by

Int. NGOs

Tax Reform

Advocacy,

spearheaded by

ASSECCAF

Value Chain Actors Consultations

PPP Strengthening

International Development Community Involvement

Business Enviroment Improvement Advocacy

,

:

7 000 000

7 500 000

8 000 000

8 500 000

9 000 000

9 500 000

2011 2012 2013 2014 2015

Export

s (K

gs)

5 Years DRC COFFEE EXPORTS

-

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

2011 2012 2013 2014 2015

EXPO

RTS (

KG

S)

5 YEARS DRC COFFEE EXPORTS

ROBUSTA

ARABICA

60% Vol.

40% Vol.

1) Café (⬆️ 45,3 %)

2015 /2016 - 7'239 tonnes

2014 /2015 - 4'982 tonnes

2) Cacao (⬆️33.6 %)

2015 /2016 - 11'076 tonnes

2014 /2015 - 8'288 tonnes

3) Quinquina (⬆️2,1%)

2015 /2016 - 5'267 tonnes

2014 /2015 - 5'156 tonnes

4) Papaine (⬆️ 40,5 %)

In October 2015, the Government signed a Ministerial Order,

Bringing to 0.25% FOB Export Taxes on Agricultural Products

For Services acting on the borders:

As a result, an increase in official export volumes has been recorded

+ 11’000 tonnes 2015/2016 (expected)

vs 8’742 tonnes 2014/2015

BENI Sector

The DRC Coffee potential is immense

Despite the multiple historic challenges facing the sector, the DRC Coffee shows sign of recovery

The last 5 years have shown that more stakeholderscollaboration, combined with partnerships and appropriate policies application can bring positive change

This trend needs to continue : DRC Coffee could be a catalyst for socio-economic change and contributor to the Sustainable Resurgence of the African Coffee Insustry.