kentucky inheritance and estate tax forms and …revenue.ky.gov/forms/2008_92a200p1008.pdf ·...

TRANSCRIPT

COMMONWEALTH OF KENTUCKYDEPARTMENT OF REVENUE

KentuckyInheritance and Estate Tax

Forms and Instructions

Kentucky Department of RevenueMission Statement

The mission of the Kentucky Department of Revenue is to administer tax laws, collect revenue, andprovide services in a fair, courteous, and efficient manner for the benefit of the Commonwealth and itscitizens.

For Dates of Death on or After July 1, 1998(Revised for Web Site

October, 2008)

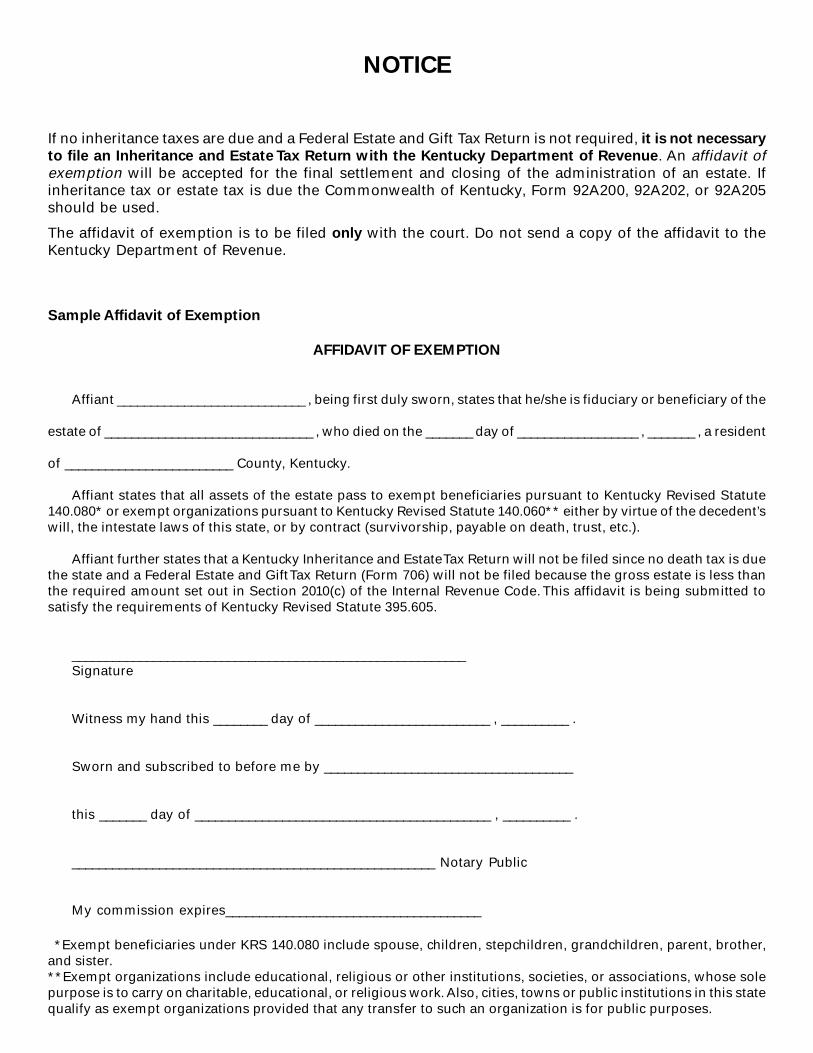

NOTICE

If no inheritance taxes are due and a Federal Estate and Gift Tax Return is not required, it is not necessary

to file an Inheritance and Estate Tax Return with the Kentucky Department of Revenue. An affidavit ofexemption will be accepted for the final settlement and closing of the administration of an estate. Ifinheritance tax or estate tax is due the Commonwealth of Kentucky, Form 92A200, 92A202, or 92A205should be used.

The affidavit of exemption is to be filed only with the court. Do not send a copy of the affidavit to theKentucky Department of Revenue.

Sample Affidavit of Exemption

AFFIDAVIT OF EXEMPTION

Affiant ____________________________ , being first duly sworn, states that he/she is fiduciary or beneficiary of the

estate of _______________________________ , who died on the _______ day of __________________ , _______ , a resident

of _________________________ County, Kentucky.

Affiant states that all assets of the estate pass to exempt beneficiaries pursuant to Kentucky Revised Statute140.080* or exempt organizations pursuant to Kentucky Revised Statute 140.060** either by virtue of the decedent’swill, the intestate laws of this state, or by contract (survivorship, payable on death, trust, etc.).

Affiant further states that a Kentucky Inheritance and Estate Tax Return will not be filed since no death tax is duethe state and a Federal Estate and Gift Tax Return (Form 706) will not be filed because the gross estate is less thanthe required amount set out in Section 2010(c) of the Internal Revenue Code. This affidavit is being submitted tosatisfy the requirements of Kentucky Revised Statute 395.605.

__________________________________________________________Signature

Witness my hand this ________ day of __________________________ , __________ .

Sworn and subscribed to before me by _____________________________________

this _______ day of ____________________________________________ , __________ .

______________________________________________________ Notary Public

My commission expires______________________________________

*Exempt beneficiaries under KRS 140.080 include spouse, children, stepchildren, grandchildren, parent, brother,and sister.**Exempt organizations include educational, religious or other institutions, societies, or associations, whose solepurpose is to carry on charitable, educational, or religious work. Also, cities, towns or public institutions in this statequalify as exempt organizations provided that any transfer to such an organization is for public purposes.

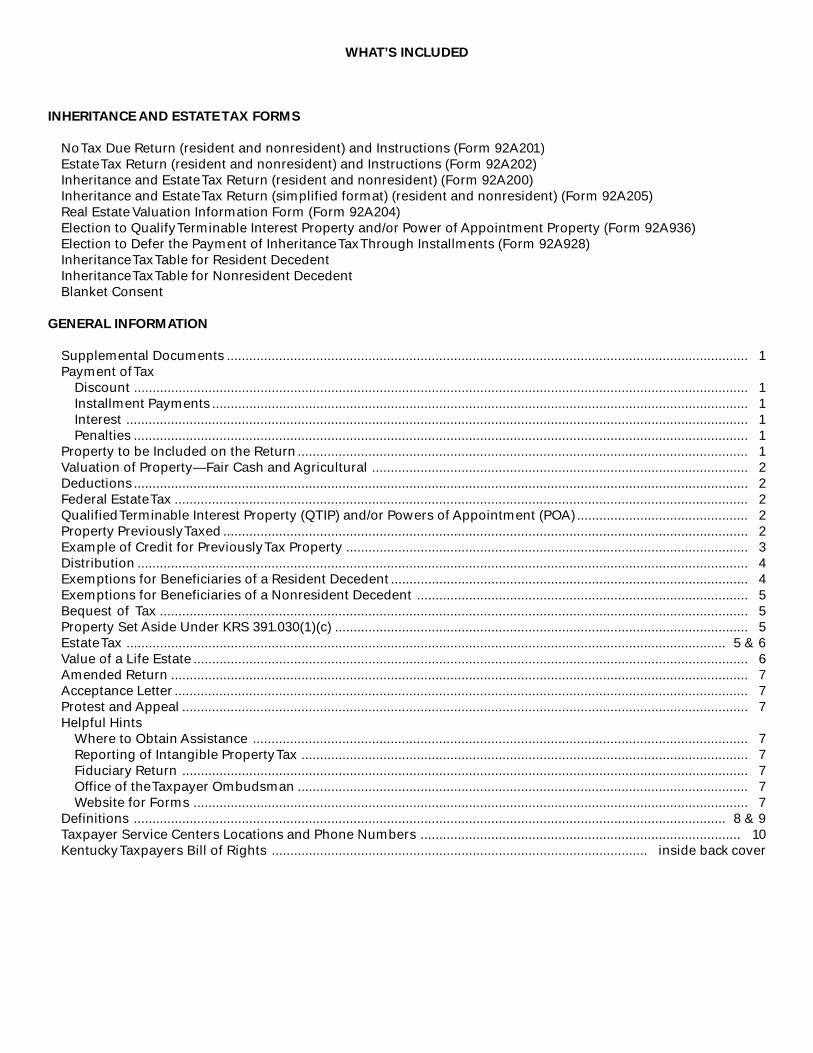

WHAT’S INCLUDED

INHERITANCE AND ESTATE TAX FORMS

No Tax Due Return (resident and nonresident) and Instructions (Form 92A201)Estate Tax Return (resident and nonresident) and Instructions (Form 92A202)Inheritance and Estate Tax Return (resident and nonresident) (Form 92A200)Inheritance and Estate Tax Return (simplified format) (resident and nonresident) (Form 92A205)Real Estate Valuation Information Form (Form 92A204)Election to Qualify Terminable Interest Property and/or Power of Appointment Property (Form 92A936)Election to Defer the Payment of Inheritance Tax Through Installments (Form 92A928)Inheritance Tax Table for Resident DecedentInheritance Tax Table for Nonresident DecedentBlanket Consent

GENERAL INFORMATION

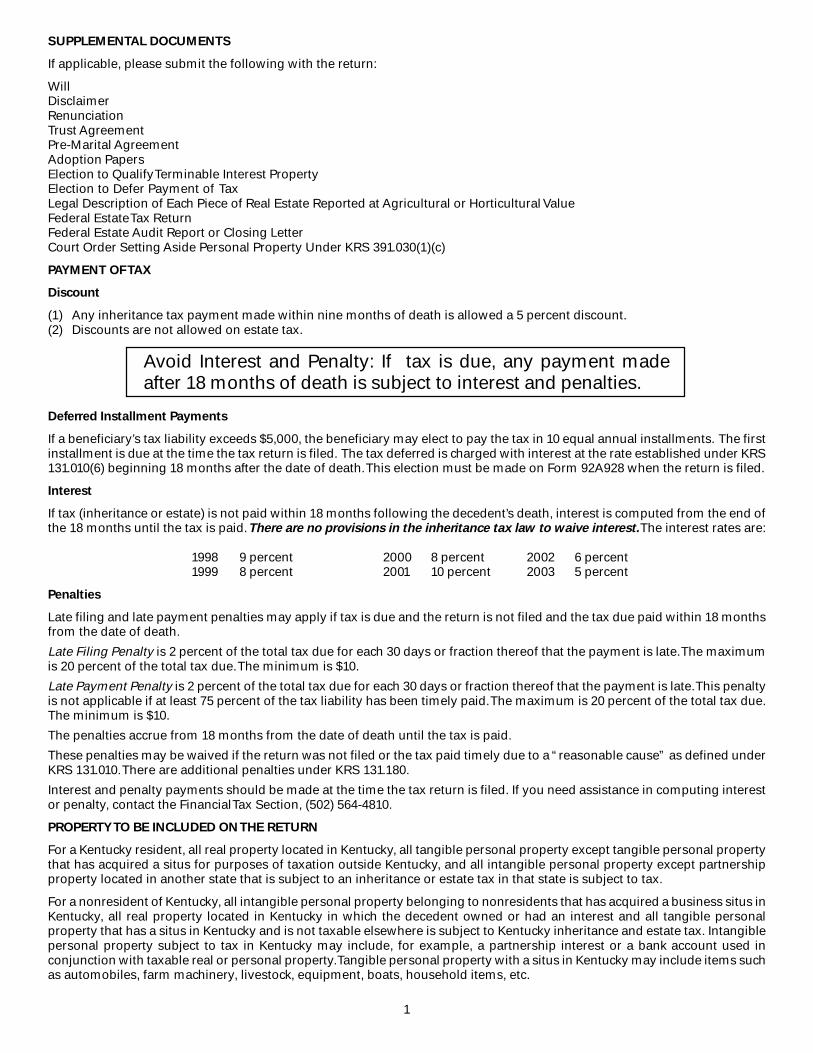

Supplemental Documents ............................................................................................................................................ 1Payment of Tax

Discount ..................................................................................................................................................................... 1Installment Payments ................................................................................................................................................ 1Interest ....................................................................................................................................................................... 1Penalties ..................................................................................................................................................................... 1

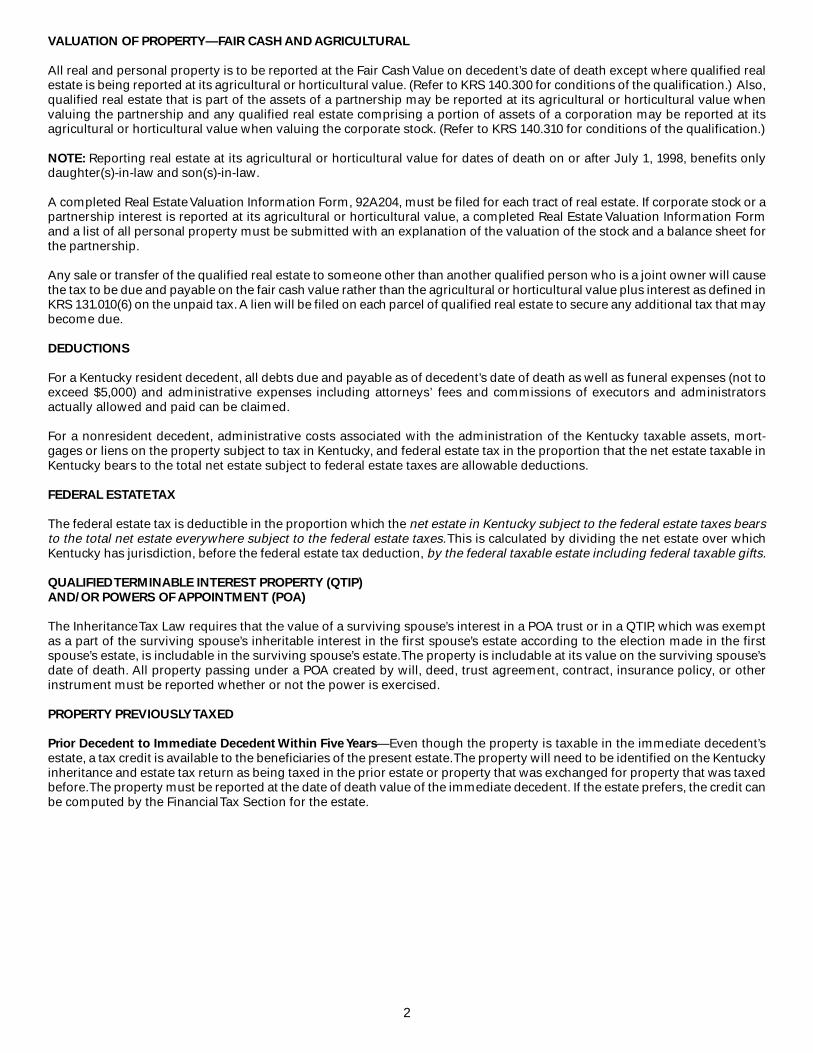

Property to be Included on the Return......................................................................................................................... 1Valuation of Property—Fair Cash and Agricultural ..................................................................................................... 2Deductions..................................................................................................................................................................... 2Federal Estate Tax .......................................................................................................................................................... 2Qualified Terminable Interest Property (QTIP) and/or Powers of Appointment (POA).............................................. 2Property Previously Taxed ............................................................................................................................................. 2Example of Credit for Previously Tax Property ............................................................................................................ 3Distribution .................................................................................................................................................................... 4Exemptions for Beneficiaries of a Resident Decedent ................................................................................................ 4Exemptions for Beneficiaries of a Nonresident Decedent ......................................................................................... 5Bequest of Tax .............................................................................................................................................................. 5Property Set Aside Under KRS 391.030(1)(c) ............................................................................................................... 5Estate Tax ................................................................................................................................................................. 5 & 6Value of a Life Estate ..................................................................................................................................................... 6Amended Return ........................................................................................................................................................... 7Acceptance Letter .......................................................................................................................................................... 7Protest and Appeal ........................................................................................................................................................ 7Helpful Hints

Where to Obtain Assistance ..................................................................................................................................... 7Reporting of Intangible Property Tax ........................................................................................................................ 7Fiduciary Return ........................................................................................................................................................ 7Office of the Taxpayer Ombudsman ......................................................................................................................... 7Website for Forms ..................................................................................................................................................... 7

Definitions ............................................................................................................................................................... 8 & 9Taxpayer Service Centers Locations and Phone Numbers ...................................................................................... 10Kentucky Taxpayers Bill of Rights ..................................................................................................... inside back cover

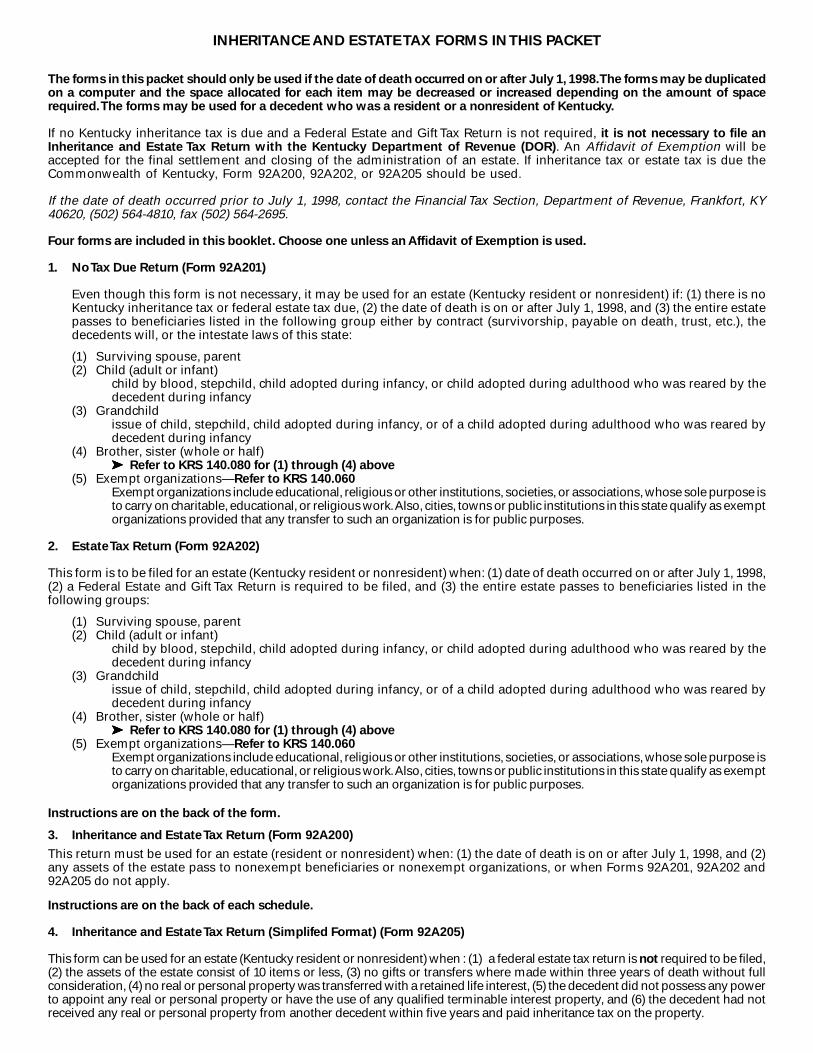

INHERITANCE AND ESTATE TAX FORMS IN THIS PACKET

The forms in this packet should only be used if the date of death occurred on or after July 1, 1998. The forms may be duplicatedon a computer and the space allocated for each item may be decreased or increased depending on the amount of spacerequired. The forms may be used for a decedent who was a resident or a nonresident of Kentucky.

If no Kentucky inheritance tax is due and a Federal Estate and Gift Tax Return is not required, it is not necessary to file anInheritance and Estate Tax Return with the Kentucky Department of Revenue (DOR). An Affidavit of Exemption will beaccepted for the final settlement and closing of the administration of an estate. If inheritance tax or estate tax is due theCommonwealth of Kentucky, Form 92A200, 92A202, or 92A205 should be used.

If the date of death occurred prior to July 1, 1998, contact the Financial Tax Section, Department of Revenue, Frankfort, KY40620, (502) 564-4810, fax (502) 564-2695.

Four forms are included in this booklet. Choose one unless an Affidavit of Exemption is used.

1. No Tax Due Return (Form 92A201)

Even though this form is not necessary, it may be used for an estate (Kentucky resident or nonresident) if: (1) there is noKentucky inheritance tax or federal estate tax due, (2) the date of death is on or after July 1, 1998, and (3) the entire estatepasses to beneficiaries listed in the following group either by contract (survivorship, payable on death, trust, etc.), thedecedents will, or the intestate laws of this state:

(1) Surviving spouse, parent(2) Child (adult or infant)

child by blood, stepchild, child adopted during infancy, or child adopted during adulthood who was reared by thedecedent during infancy

(3) Grandchildissue of child, stepchild, child adopted during infancy, or of a child adopted during adulthood who was reared bydecedent during infancy

(4) Brother, sister (whole or half)➤➤➤➤➤ Refer to KRS 140.080 for (1) through (4) above

(5) Exempt organizations—Refer to KRS 140.060Exempt organizations include educational, religious or other institutions, societies, or associations, whose sole purpose isto carry on charitable, educational, or religious work. Also, cities, towns or public institutions in this state qualify as exemptorganizations provided that any transfer to such an organization is for public purposes.

2. Estate Tax Return (Form 92A202)

This form is to be filed for an estate (Kentucky resident or nonresident) when: (1) date of death occurred on or after July 1, 1998,(2) a Federal Estate and Gift Tax Return is required to be filed, and (3) the entire estate passes to beneficiaries listed in thefollowing groups:

(1) Surviving spouse, parent(2) Child (adult or infant)

child by blood, stepchild, child adopted during infancy, or child adopted during adulthood who was reared by thedecedent during infancy

(3) Grandchildissue of child, stepchild, child adopted during infancy, or of a child adopted during adulthood who was reared bydecedent during infancy

(4) Brother, sister (whole or half)➤➤➤➤➤ Refer to KRS 140.080 for (1) through (4) above

(5) Exempt organizations—Refer to KRS 140.060Exempt organizations include educational, religious or other institutions, societies, or associations, whose sole purpose isto carry on charitable, educational, or religious work. Also, cities, towns or public institutions in this state qualify as exemptorganizations provided that any transfer to such an organization is for public purposes.

Instructions are on the back of the form.

3. Inheritance and Estate Tax Return (Form 92A200)

This return must be used for an estate (resident or nonresident) when: (1) the date of death is on or after July 1, 1998, and (2)any assets of the estate pass to nonexempt beneficiaries or nonexempt organizations, or when Forms 92A201, 92A202 and92A205 do not apply.

Instructions are on the back of each schedule.

4. Inheritance and Estate Tax Return (Simplifed Format) (Form 92A205)

This form can be used for an estate (Kentucky resident or nonresident) when : (1) a federal estate tax return is not required to be filed,(2) the assets of the estate consist of 10 items or less, (3) no gifts or transfers where made within three years of death without fullconsideration, (4) no real or personal property was transferred with a retained life interest, (5) the decedent did not possess any powerto appoint any real or personal property or have the use of any qualified terminable interest property, and (6) the decedent had notreceived any real or personal property from another decedent within five years and paid inheritance tax on the property.

FOR DEPARTMENT USE ONLY

__ __ __ __ __ __ / __ __ / __ __ __ __Account Number Tax Year

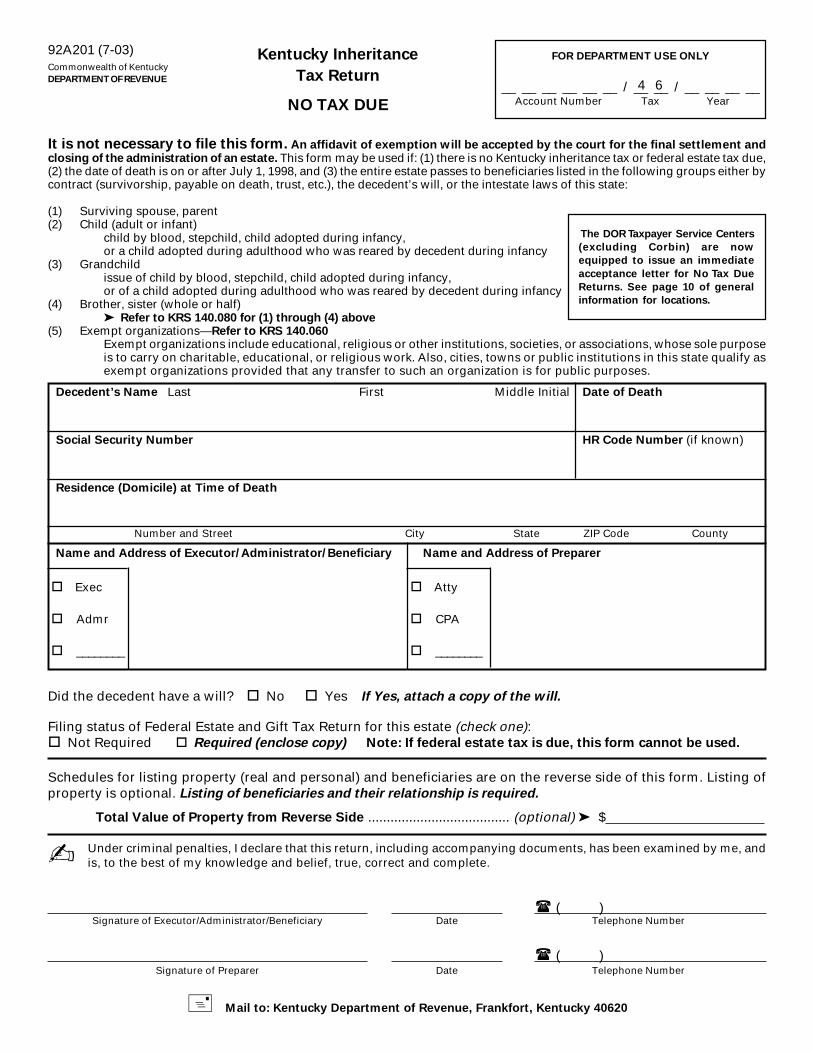

92A201 (7-03)Commonwealth of KentuckyDEPARTMENT OF REVENUE

Kentucky Inheritance

Tax Return

NO TAX DUE

It is not necessary to file this form. An affidavit of exemption will be accepted by the court for the final settlement andclosing of the administration of an estate. This form may be used if: (1) there is no Kentucky inheritance tax or federal estate tax due,(2) the date of death is on or after July 1, 1998, and (3) the entire estate passes to beneficiaries listed in the following groups either bycontract (survivorship, payable on death, trust, etc.), the decedent’s will, or the intestate laws of this state:

(1) Surviving spouse, parent(2) Child (adult or infant)

child by blood, stepchild, child adopted during infancy,or a child adopted during adulthood who was reared by decedent during infancy

(3) Grandchildissue of child by blood, stepchild, child adopted during infancy,or of a child adopted during adulthood who was reared by decedent during infancy

(4) Brother, sister (whole or half)➤ Refer to KRS 140.080 for (1) through (4) above

(5) Exempt organizations—Refer to KRS 140.060Exempt organizations include educational, religious or other institutions, societies, or associations, whose sole purposeis to carry on charitable, educational, or religious work. Also, cities, towns or public institutions in this state qualify asexempt organizations provided that any transfer to such an organization is for public purposes.

Signature of Executor/Administrator/Beneficiary Date Telephone Number

Signature of Preparer Date Telephone Number

4 6

Mail to: Kentucky Department of Revenue, Frankfort, Kentucky 40620

✍

( )

( )

Decedent’s Name Last First Middle Initial Date of Death

Social Security Number HR Code Number (if known)

Residence (Domicile) at Time of Death

Number and Street City State ZIP Code County

Name and Address of Executor/Administrator/Beneficiary Name and Address of Preparer

Did the decedent have a will? No Yes If Yes, attach a copy of the will.

Filing status of Federal Estate and Gift Tax Return for this estate (check one):Not Required Required (enclose copy) Note: If federal estate tax is due, this form cannot be used.

Schedules for listing property (real and personal) and beneficiaries are on the reverse side of this form. Listing ofproperty is optional. Listing of beneficiaries and their relationship is required.

Total Value of Property from Reverse Side ...................................... (optional) ➤ $

Under criminal penalties, I declare that this return, including accompanying documents, has been examined by me, andis, to the best of my knowledge and belief, true, correct and complete.

The DOR Taxpayer Service Centers

(excluding Corbin) are now

equipped to issue an immediate

acceptance letter for No Tax Due

Returns. See page 10 of general

information for locations.

Exec

Admr

________

Atty

CPA

________

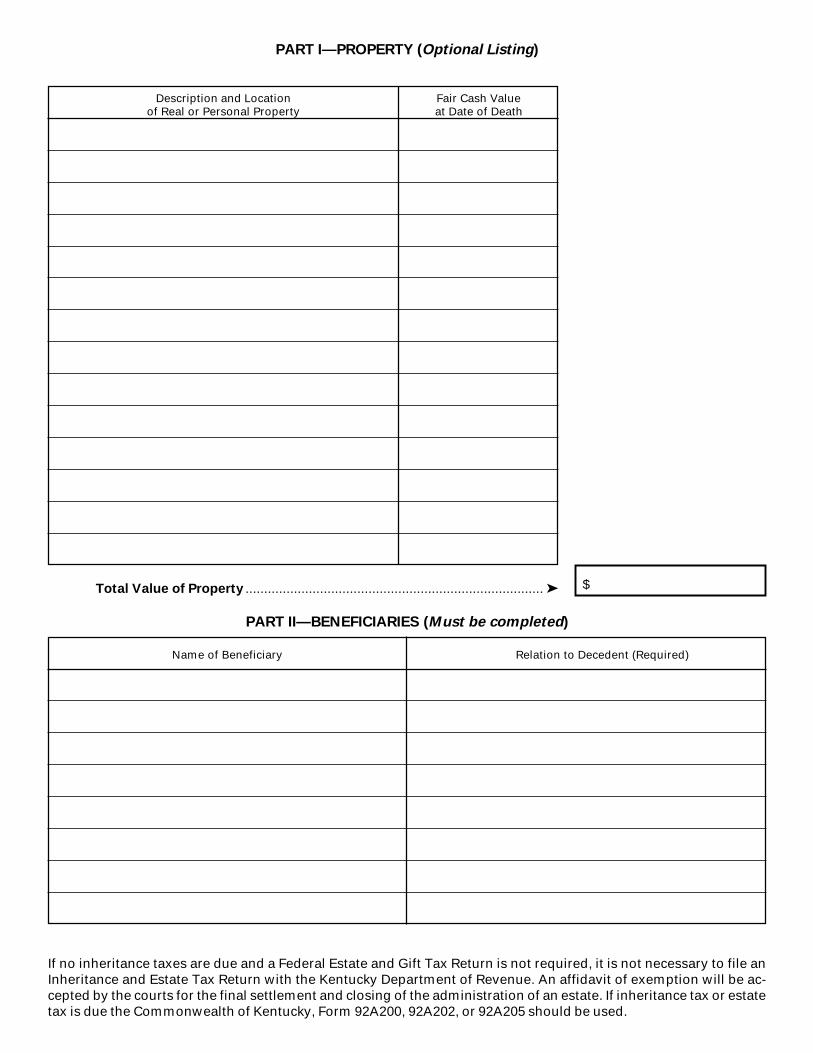

PART I—PROPERTY (Optional Listing)

Total Value of Property ................................................................................ ➤ $

Description and Location Fair Cash Valueof Real or Personal Property at Date of Death

Name of Beneficiary Relation to Decedent (Required)

If no inheritance taxes are due and a Federal Estate and Gift Tax Return is not required, it is not necessary to file anInheritance and Estate Tax Return with the Kentucky Department of Revenue. An affidavit of exemption will be ac-cepted by the courts for the final settlement and closing of the administration of an estate. If inheritance tax or estatetax is due the Commonwealth of Kentucky, Form 92A200, 92A202, or 92A205 should be used.

PART II—BENEFICIARIES (Must be completed)

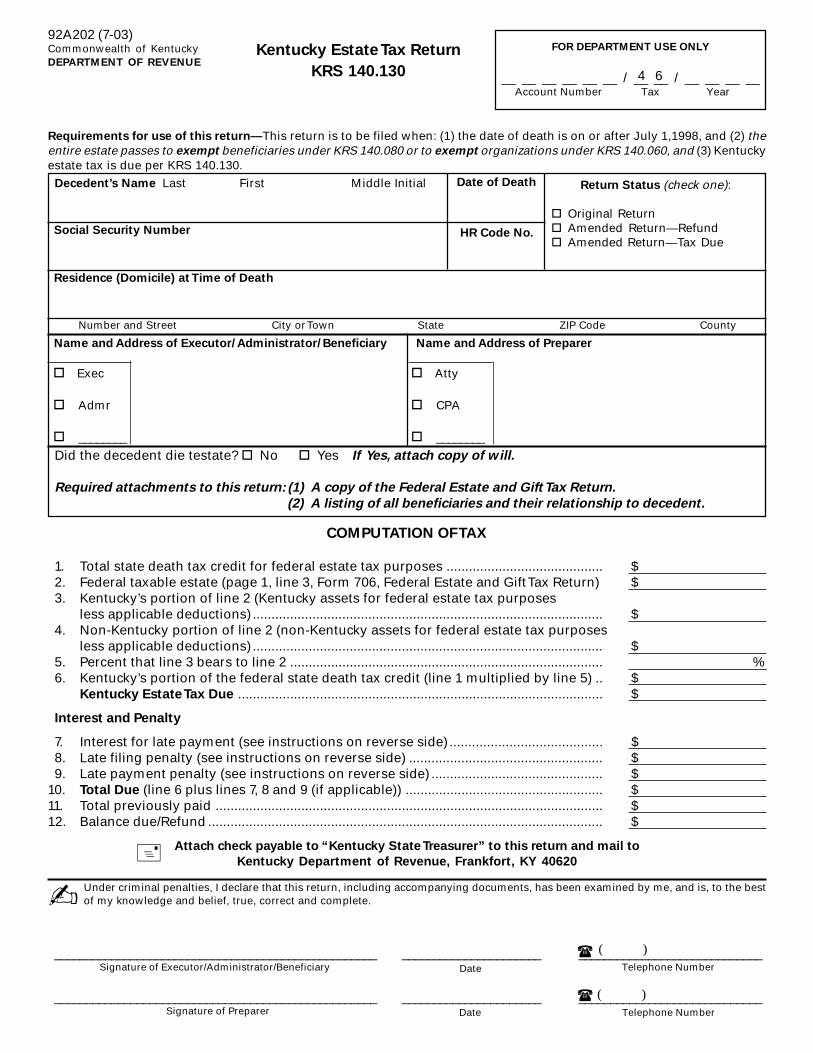

92A202 (7-03)Commonwealth of KentuckyDEPARTMENT OF REVENUE

Kentucky Estate Tax Return

KRS 140.130

Decedent’s Name Last First Middle Initial

Social Security Number

Residence (Domicile) at Time of Death

Number and Street City or Town State ZIP Code County

Date of Death

HR Code No.

Return Status (check one):

Original ReturnAmended Return—RefundAmended Return—Tax Due

Name and Address of Executor/Administrator/Beneficiary Name and Address of Preparer

Did the decedent die testate? No Yes If Yes, attach copy of will.

Required attachments to this return: (1) A copy of the Federal Estate and Gift Tax Return.

(2) A listing of all beneficiaries and their relationship to decedent.

COMPUTATION OF TAX

1. Total state death tax credit for federal estate tax purposes .......................................... $2. Federal taxable estate (page 1, line 3, Form 706, Federal Estate and Gift Tax Return) $3. Kentucky’s portion of line 2 (Kentucky assets for federal estate tax purposes

less applicable deductions) .............................................................................................. $4. Non-Kentucky portion of line 2 (non-Kentucky assets for federal estate tax purposes

less applicable deductions) .............................................................................................. $5. Percent that line 3 bears to line 2 .................................................................................... %6. Kentucky’s portion of the federal state death tax credit (line 1 multiplied by line 5) .. $

Kentucky Estate Tax Due .................................................................................................. $

Interest and Penalty

7. Interest for late payment (see instructions on reverse side) ......................................... $8. Late filing penalty (see instructions on reverse side) .................................................... $9. Late payment penalty (see instructions on reverse side) .............................................. $

10. Total Due (line 6 plus lines 7, 8 and 9 (if applicable)) ..................................................... $11. Total previously paid ........................................................................................................ $12. Balance due/Refund .......................................................................................................... $

Attach check payable to “Kentucky State Treasurer” to this return and mail to

Kentucky Department of Revenue, Frankfort, KY 40620

✍ Under criminal penalties, I declare that this return, including accompanying documents, has been examined by me, and is, to the bestof my knowledge and belief, true, correct and complete.

Signature of Executor/Administrator/Beneficiary___________________________________________________ ______________________ _____________________________

___________________________________________________ ______________________ _____________________________Signature of Preparer Date

Date Telephone Number

Telephone Number

( )

( )

FOR DEPARTMENT USE ONLY

__ __ __ __ __ __ / __ __ / __ __ __ __Account Number Tax Year

4 6

Requirements for use of this return—This return is to be filed when: (1) the date of death is on or after July 1,1998, and (2) theentire estate passes to exempt beneficiaries under KRS 140.080 or to exempt organizations under KRS 140.060, and (3) Kentuckyestate tax is due per KRS 140.130.

Exec

Admr

________

Atty

CPA

________

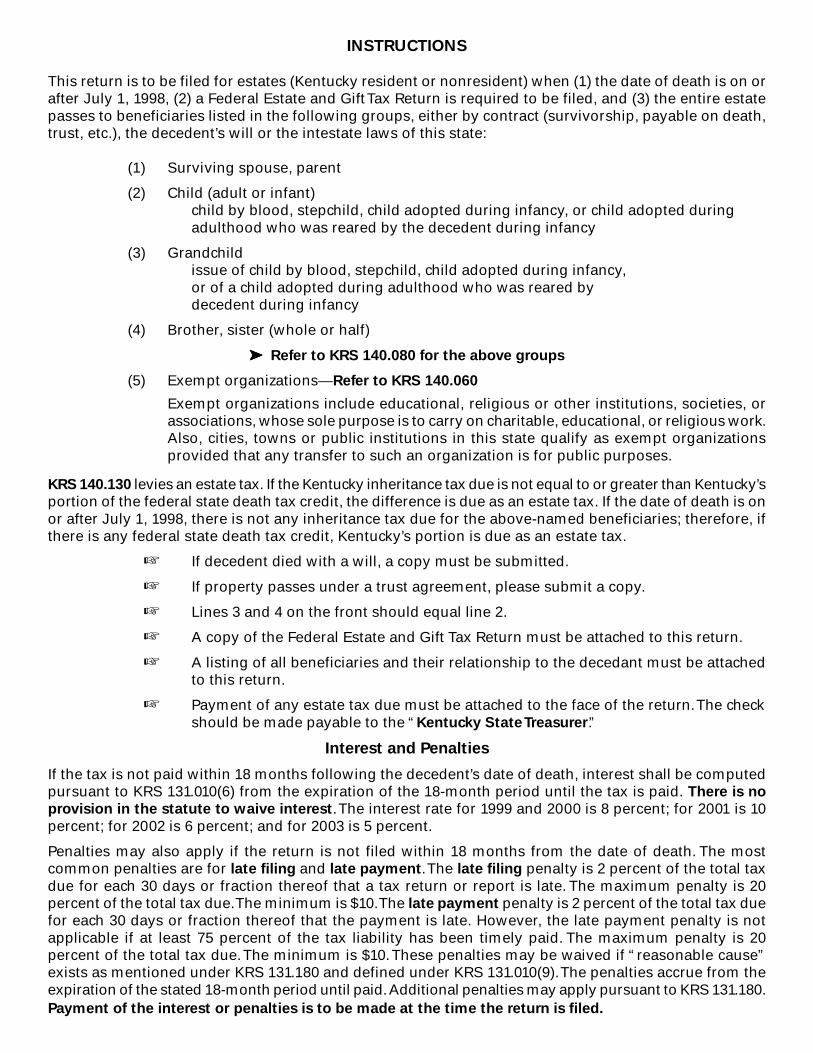

INSTRUCTIONS

This return is to be filed for estates (Kentucky resident or nonresident) when (1) the date of death is on orafter July 1, 1998, (2) a Federal Estate and Gift Tax Return is required to be filed, and (3) the entire estatepasses to beneficiaries listed in the following groups, either by contract (survivorship, payable on death,trust, etc.), the decedent’s will or the intestate laws of this state:

(1) Surviving spouse, parent

(2) Child (adult or infant)child by blood, stepchild, child adopted during infancy, or child adopted duringadulthood who was reared by the decedent during infancy

(3) Grandchildissue of child by blood, stepchild, child adopted during infancy,or of a child adopted during adulthood who was reared bydecedent during infancy

(4) Brother, sister (whole or half)

➤➤➤➤➤ Refer to KRS 140.080 for the above groups

(5) Exempt organizations—Refer to KRS 140.060

Exempt organizations include educational, religious or other institutions, societies, orassociations, whose sole purpose is to carry on charitable, educational, or religious work.Also, cities, towns or public institutions in this state qualify as exempt organizationsprovided that any transfer to such an organization is for public purposes.

KRS 140.130 levies an estate tax. If the Kentucky inheritance tax due is not equal to or greater than Kentucky’sportion of the federal state death tax credit, the difference is due as an estate tax. If the date of death is onor after July 1, 1998, there is not any inheritance tax due for the above-named beneficiaries; therefore, ifthere is any federal state death tax credit, Kentucky’s portion is due as an estate tax.

☞ If decedent died with a will, a copy must be submitted.

☞ If property passes under a trust agreement, please submit a copy.

☞ Lines 3 and 4 on the front should equal line 2.

☞ A copy of the Federal Estate and Gift Tax Return must be attached to this return.

☞ A listing of all beneficiaries and their relationship to the decedant must be attachedto this return.

☞ Payment of any estate tax due must be attached to the face of the return. The checkshould be made payable to the “Kentucky State Treasurer.”

Interest and Penalties

If the tax is not paid within 18 months following the decedent’s date of death, interest shall be computedpursuant to KRS 131.010(6) from the expiration of the 18-month period until the tax is paid. There is no

provision in the statute to waive interest. The interest rate for 1999 and 2000 is 8 percent; for 2001 is 10percent; for 2002 is 6 percent; and for 2003 is 5 percent.

Penalties may also apply if the return is not filed within 18 months from the date of death. The mostcommon penalties are for late filing and late payment. The late filing penalty is 2 percent of the total taxdue for each 30 days or fraction thereof that a tax return or report is late. The maximum penalty is 20percent of the total tax due. The minimum is $10. The late payment penalty is 2 percent of the total tax duefor each 30 days or fraction thereof that the payment is late. However, the late payment penalty is notapplicable if at least 75 percent of the tax liability has been timely paid. The maximum penalty is 20percent of the total tax due. The minimum is $10. These penalties may be waived if “reasonable cause”exists as mentioned under KRS 131.180 and defined under KRS 131.010(9). The penalties accrue from theexpiration of the stated 18-month period until paid. Additional penalties may apply pursuant to KRS 131.180.Payment of the interest or penalties is to be made at the time the return is filed.

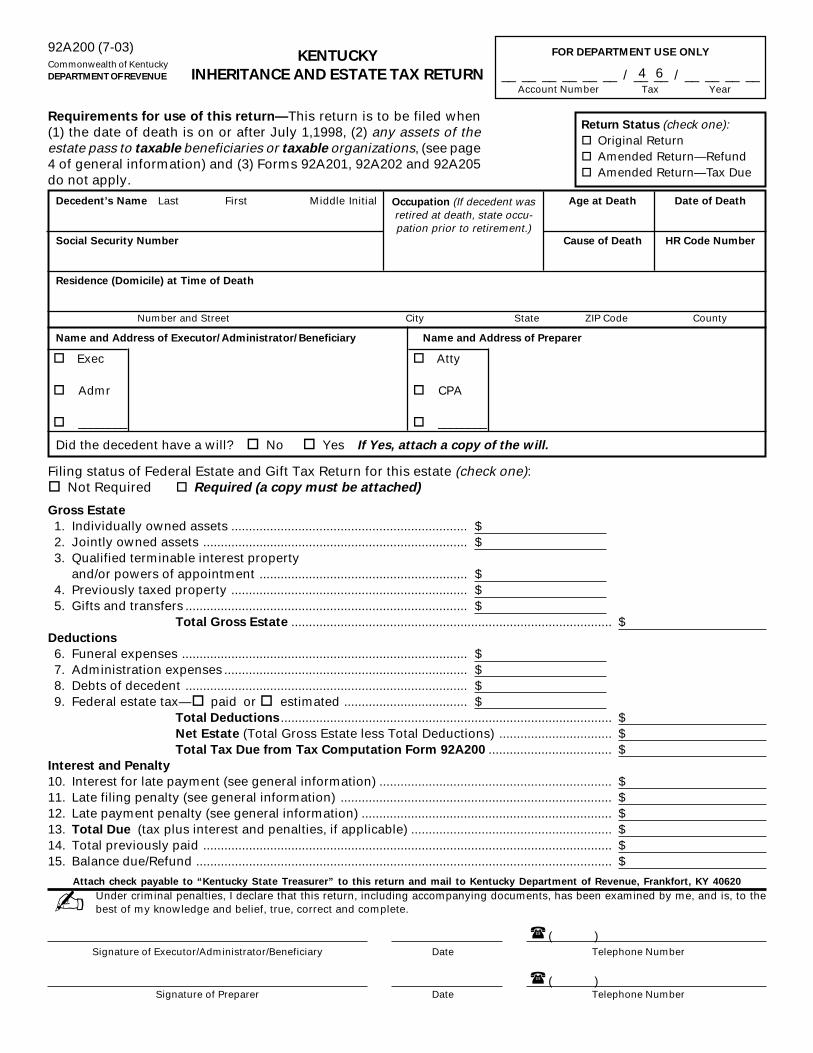

92A200 (7-03)Commonwealth of KentuckyDEPARTMENT OF REVENUE

KENTUCKY

INHERITANCE AND ESTATE TAX RETURN

Requirements for use of this return—This return is to be filed when(1) the date of death is on or after July 1,1998, (2) any assets of theestate pass to taxable beneficiaries or taxable organizations, (see page4 of general information) and (3) Forms 92A201, 92A202 and 92A205do not apply.

Decedent’s Name Last First Middle Initial Age at Death Date of Death

Social Security Number Cause of Death HR Code Number

Residence (Domicile) at Time of Death

Number and Street City State ZIP Code County

Name and Address of Executor/Administrator/Beneficiary Name and Address of Preparer

Did the decedent have a will? No Yes If Yes, attach a copy of the will.

Filing status of Federal Estate and Gift Tax Return for this estate (check one):Not Required Required (a copy must be attached)

Gross Estate

1. Individually owned assets ................................................................... $2. Jointly owned assets ........................................................................... $3. Qualified terminable interest property

and/or powers of appointment ........................................................... $4. Previously taxed property ................................................................... $5. Gifts and transfers ................................................................................ $

Total Gross Estate ........................................................................................... $Deductions

6. Funeral expenses ................................................................................. $7. Administration expenses ..................................................................... $8. Debts of decedent ................................................................................ $9. Federal estate tax— paid or estimated ................................... $

Total Deductions .............................................................................................. $Net Estate (Total Gross Estate less Total Deductions) ................................ $Total Tax Due from Tax Computation Form 92A200 ................................... $

Interest and Penalty

10. Interest for late payment (see general information) .................................................................. $11. Late filing penalty (see general information) ............................................................................. $12. Late payment penalty (see general information) ....................................................................... $13. Total Due (tax plus interest and penalties, if applicable) ......................................................... $14. Total previously paid .................................................................................................................... $15. Balance due/Refund ...................................................................................................................... $

Under criminal penalties, I declare that this return, including accompanying documents, has been examined by me, and is, to thebest of my knowledge and belief, true, correct and complete.

Signature of Executor/Administrator/Beneficiary Date Telephone Number

( )

( )

FOR DEPARTMENT USE ONLY

__ __ __ __ __ __ / __ __ / __ __ __ __Account Number Tax Year

4 6

Return Status (check one):Original ReturnAmended Return—RefundAmended Return—Tax Due

Occupation (If decedent wasretired at death, state occu-pation prior to retirement.)

✍

Signature of Preparer Date Telephone Number

Exec

Admr

________

Atty

CPA

________

Attach check payable to “Kentucky State Treasurer” to this return and mail to Kentucky Department of Revenue, Frankfort, KY 40620

Estate of:

Individually Owned Assets

List in this schedule all items individually owned by the decedent including life insurance payable to the estate.(Additional instructions are on reverse side.)

92A200 (7-03)

Total (including continuation page(s)) (enter on page 1, line 1) ............................................. ➤

Description of Property/Name of Corporationor Obligor/ Name of Bank or Debtor

Fair Cash Valueon Date of Death

Numberof Shares

ItemNumber

Accrued Rents/Interest/Dividends

1.

Page ____ of ____

If additional space is needed, duplicate this page and attach as a continuation page(s).

INSTRUCTIONS

INDIVIDUALLY OWNED ASSETS

All real property individually owned must be listedin this schedule. For reporting agricultural orhorticultural land, see General Information—Valuation of Property—Fair Cash and Agricultural.

Stocks and bonds individually owned areincludable in this schedule. In case of inactivestock such as closely held corporations, explainthe method used in computing the value at thedate of death. A balance sheet, at a date nearestthe decedent’s death, together with a statementof net earnings and dividends paid for the five-year period immediately preceding the date ofdeath, must be supplied in support of thesevaluations.

Dividends declared and of record in the decedent’sname but not paid prior to death must be includedin this schedule.

United States bonds individually owned as wellas those payable upon death to another shouldbe included in this schedule. Indicate series,maturity value and date of purchase of all UnitedStates bonds.

In some instances, the estate will include stocksand bonds listed on a stock exchange that did notmake sales on the date of the decedent’s death.When this occurs, their value must be determinedon the date nearest to decedent’s death that thestock exchange made sales. For reporting stockof a corporation owning qualified real estatepassing to a qualified person(s), see GeneralInformation—Valuation of Property—Fair Cash

and Agricultural.

Mortgages, notes and cash individually ownedmust be listed in this schedule. List accruedinterest to date of death. The description ofmortgages and notes must include interest rate,the date the last payment of interest was madepreceding the date of the decedent’s death, andthe due date of the mortgages or notes. If anaccount is held out of state, show name andaddress of financial institution on the tax return.

List life insurance payable to the insured or tothe estate. Life insurance payable to a designatedbeneficiary, including a testamentary or intervivos trustee, is tax-free.

List in this schedule other individually owneditems of the gross estate, such as debts duedecedent; business or partnership (attach balancesheet showing capital accounts); claims, exclusiveof those claimed under KRS 411.130 (wrongfuldeath); rights; royalties; leaseholds; judgments;shares in trust funds; contracts; household goodsand personal effects, including antiques, jewelryand collections of any type; farm products andgrowing crops; livestock; farm machinery;automobiles; etc.

The value of an annuity or other payment madeto a beneficiary of a deceased employee (otherthan the executor or equivalent) under (1) anexempt trust or qualified nontrusted annuity planas described by the Internal Revenue Code or (2)a contract purchased by an educational orcharitable organization as referred to in Section170(b)(1)(A)(ii) or (vi) of the Internal Revenue Codeor a religious organization exempt from tax underInternal Revenue Code Section 501(a), is taxablein the proportion that the total contributions madeby the decedent bears to the total contributionsmade. The proceeds from a Retired Serviceman’sFamily Protection Plan or Survivor Benefit Planare exempt under KRS 140.015(2). Refer to KRS140.063(3) and (4) regarding the taxation ofindividual retirement accounts and annuities asdescribed in Section 408(a) and (b) of the InternalRevenue Code. Lump-sum distributions of an IRAare taxable.

All other annuities, including deferredcompensation plans, or payments other thanthose described in the preceding paragraph madeto a beneficiary, executor or equivalent, are fullytaxable if the decedent retained ownership atdeath such as the right to name or change thebeneficiary and must be listed in this schedule.

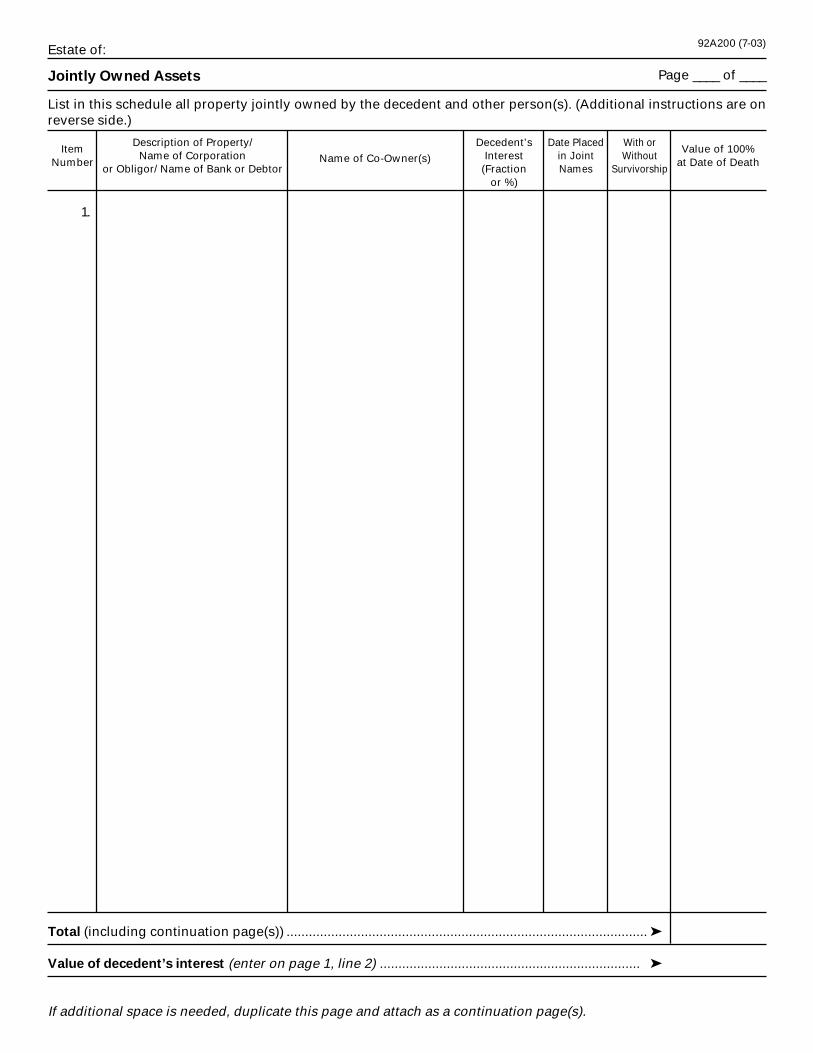

Estate of:

Jointly Owned Assets

List in this schedule all property jointly owned by the decedent and other person(s). (Additional instructions are onreverse side.)

92A200 (7-03)

Total (including continuation page(s)) ................................................................................................. ➤

Value of decedent’s interest (enter on page 1, line 2) ...................................................................... ➤

If additional space is needed, duplicate this page and attach as a continuation page(s).

ItemNumber

Value of 100%at Date of DeathName of Co-Owner(s)

Date Placedin JointNames

With orWithout

Survivorship

Decedent’sInterest

(Fractionor %)

Description of Property/Name of Corporation

or Obligor/ Name of Bank or Debtor

1.

Page ____ of ____

INSTRUCTIONS

JOINTLY OWNED ASSETS

All jointly owned property whether real estate (for reporting agricultural or horti-cultural land, see General Information—Valuation of Property—Fair Cash and

Agricultural), tangible personal property, bank accounts, stocks, bonds, etc., mustbe reported (see KRS 140.050 below). All property placed in joint ownership by thedecedent within three years of the date of death is subject to the tax in its entirety(see KRS 140.020(2) below). However, there is no presumption of contemplationof death as to certificates of deposit jointly owned, and only the percent of owner-ship of the decedent is taxable (see KRS 140.020(3) below).

KRS 140.020(2) reads as follows: Every transfer made within three (3)years prior to the death of the grantor, vendor or donor of a material partof his estate, or in the nature of a final disposition or distribution thereof,and without an adequate valuable consideration, shall be construed primafacie to have been made in contemplation of death within the meaningof this chapter. If a transfer was made more than three (3) years prior tothe death of the decedent it shall be a question of fact, to be determinedby the proper tribunal, whether the transfer was made in contemplationof death.

KRS 140.020(3) reads as follows: There shall be no presumption of con-templation of death as to certificates of deposit jointly owned and allsuch certificates of deposit shall be taxed pursuant to KRS 140.050.

KRS 140.050 reads as follows: Whenever any real or personal property isheld jointly in the names of two (2) or more persons, or as tenants by theentirety, or is deposited in banks or other depositories jointly in the namesof two (2) or more persons and is payable to either or to the survivorupon the death of the other, the right of the surviving tenant by the en-tirety or the surviving joint tenant or joint depositor to the immediateownership or possession and enjoyment of the property shall be deemeda transfer of one-half (1/2) or other proper fraction thereof, taxable underthe provisions of this chapter in the same manner as though the part ofthe property to which the transfer relates belonged to the tenants by theentirety, joint tenants or joint depositors as tenants in common, and hadbeen bequeathed or devised to the surviving tenant by the entirety, jointtenant or joint depositor by the deceased tenant by the entirety, jointtenant or just depositor.

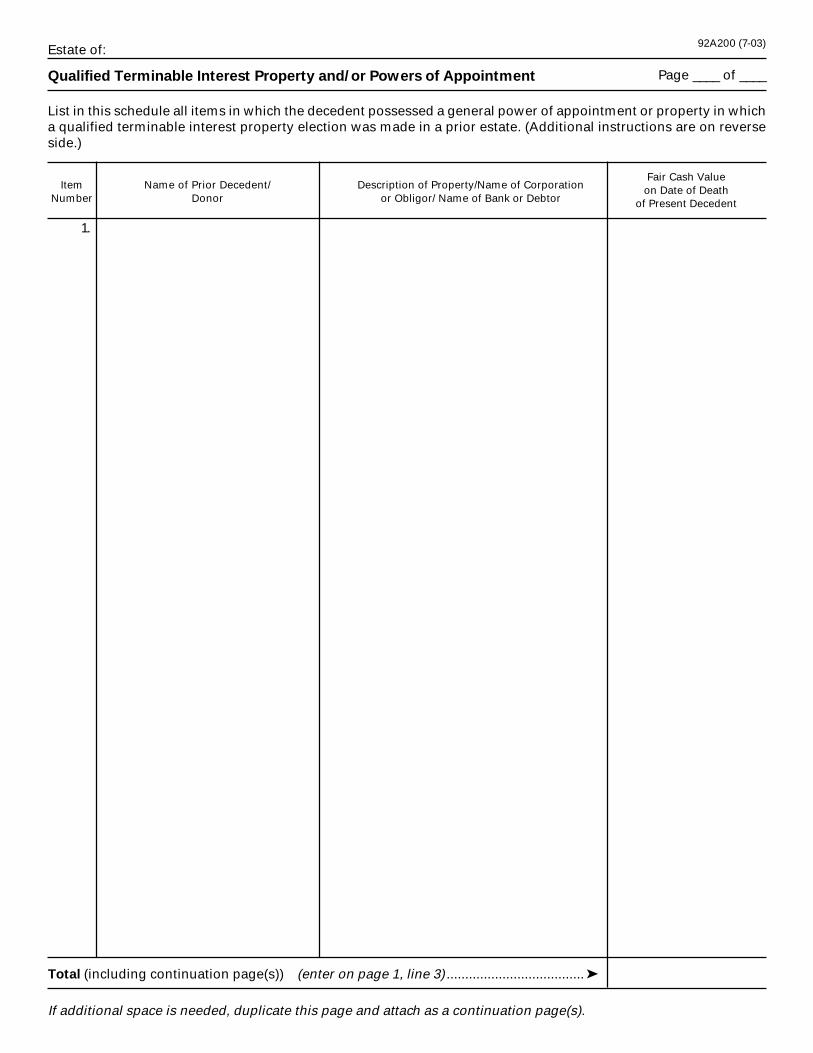

Estate of:

Qualified Terminable Interest Property and/or Powers of Appointment

List in this schedule all items in which the decedent possessed a general power of appointment or property in whicha qualified terminable interest property election was made in a prior estate. (Additional instructions are on reverseside.)

92A200 (7-03)

Total (including continuation page(s)) (enter on page 1, line 3) ..................................... ➤

ItemNumber

Fair Cash Valueon Date of Death

of Present Decedent

Description of Property/Name of Corporationor Obligor/ Name of Bank or Debtor

Name of Prior Decedent/Donor

1.

If additional space is needed, duplicate this page and attach as a continuation page(s).

Page ____ of ____

INSTRUCTIONS

QUALIFIED TERMINABLE INTEREST PROPERTY

AND/OR

POWERS OF APPOINTMENT

KRS 140.100(4) requires that the value of a surviving spouse’s interest in a power of appointment trust orin qualified terminable interest property which was exempt as a part of the surviving spouse’s inheritableinterest in the first spouse’s estate pursuant to an election made under KRS 140.080(1)(a) is includable inthe surviving spouse’s estate. The property is includable at its value on the surviving spouse’s date ofdeath. The personal representative of the decedent’s estate is entitled to recover from the trust or lifeestate the tax attributable to the trust unless the decedent directs otherwise in his will.

Powers of Appointment

All property passing under a power of appointment created by will, deed, trust agreement, contract, insur-ance policy or other instrument must be reported in this schedule whether or not the power of appoint-ment is exercised. For taxation of transfers by power of appointment, refer to KRS 140.040 and 140.100(4).

The method of computing the inheritance tax on any power of appointment property as described underKRS 140.040 is irrelevant in both the donor’s and the donee’s estates when such property is elected to beincluded in the surviving spouse’s total inheritable interest as property which qualifies for the federalestate tax marital deduction under Section 2056(b)(5) or 2056(b)(7) of the Internal Revenue Code.

KRS 140.100(4) requires that the trust or life estate for which an election relates be included in the surviv-ing spouse’s estate for Kentucky inheritance tax purposes at its value on the death of the surviving spouseregardless of where spouse is domiciled. If the surviving spouse has the power to appoint the remainder-men of the qualified trust or life estate, the property is taxed to the remaindermen named in the survivingspouse’s will and the rates and exemptions are based on their relationship to the surviving spouse. If thesurviving spouse has no power to appoint the remaindermen of the qualified trust or life estate, the prop-erty is taxed to the remaindermen named in the first spouse’s will and the rates and exemptions are basedon their relationship to the second spouse unless such rates and exemptions prove to increase the taxliability. If this occurs, the beneficiary may use the rates and exemptions in effect at the death of the firstspouse. If the first decedent was a nonresident of Kentucky or died prior to July 1, 1985, the trust or lifeestate is not includable in the surviving spouse’s estate.

Qualified Terminable Interest Property

For purpose of the spousal exemption, the term total inheritable interest may include at the election of thepersonal representative (or trustee or transferee, if no personal representative) the entire value of a trustor property in which the surviving spouse was devised a life estate and which otherwise qualifies for thefederal estate tax marital deduction under Section 2056(b)(5) or 2056(b)(7) of the Internal Revenue Code of1954, as amended through December 31, 1984. The election is irrevocable and must be made on Form92A936 on or before the due date of the tax return (as extended) or with the first tax return filed, whicheveroccurs last. It is not necessary that a similar election be made for purposes of the federal estate tax maritaldeduction or that a Federal Estate and Gift Tax Return be filed. The effect of the election is that the property(interest) will be treated as passing to the surviving spouse for purposes of the spousal exemption.

Estate of:

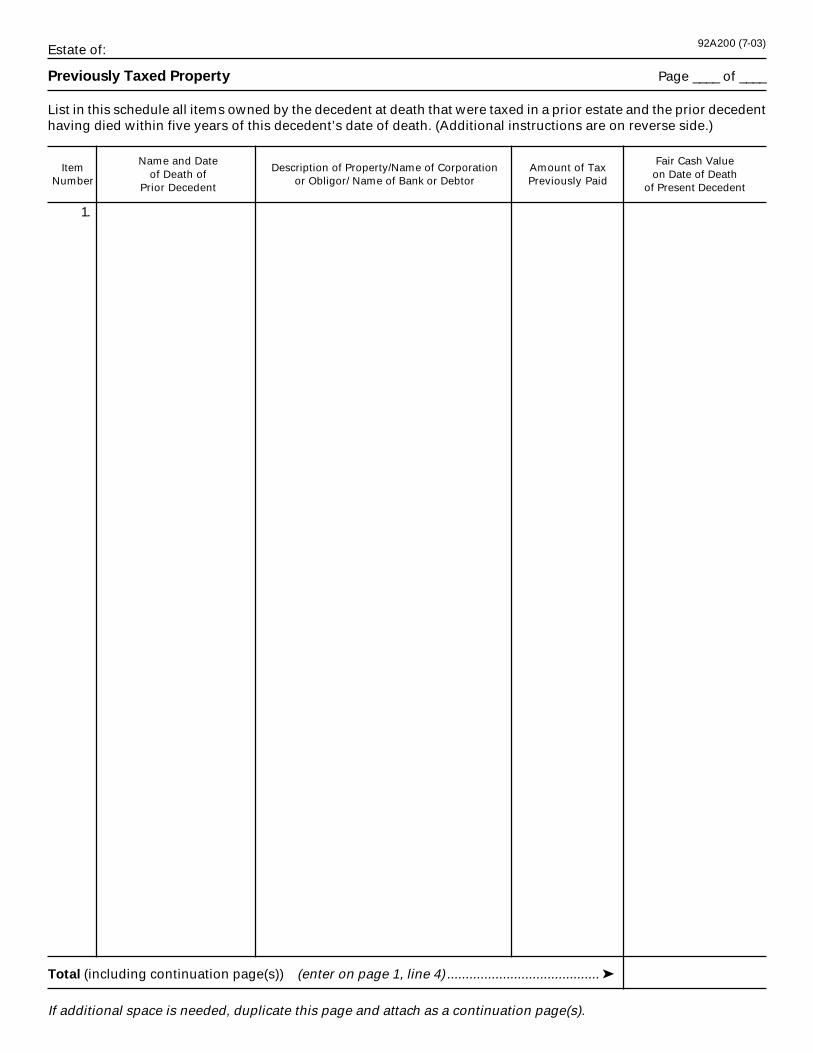

Previously Taxed Property

List in this schedule all items owned by the decedent at death that were taxed in a prior estate and the prior decedenthaving died within five years of this decedent’s date of death. (Additional instructions are on reverse side.)

92A200 (7-03)

Total (including continuation page(s)) (enter on page 1, line 4) ......................................... ➤

ItemNumber

Fair Cash Valueon Date of Death

of Present Decedent

Name and Dateof Death of

Prior Decedent

Amount of TaxPreviously Paid

Description of Property/Name of Corporationor Obligor/ Name of Bank or Debtor

1.

If additional space is needed, duplicate this page and attach as a continuation page(s).

Page ____ of ____

INSTRUCTIONS

PREVIOUSLY TAXED PROPERTY

(PRIOR DECEDENT TO IMMEDIATE DECEDENT WITHIN FIVE YEARS)

List all property owned by the immediate decedent at death that was taxed underthe Kentucky Inheritance and Estate Tax Law (KRS Chapter 140) and received froma prior estate, the prior decedent having died within five years of the immediatedecedent’s date of death. Property listed in this schedule must be specifically iden-tified as having been so taxed or as having been acquired in exchange for prop-erty so taxed. All property correctly listed in this schedule is subject to a tax creditas provided in KRS 140.095. Separate tax credit computations must be made if

the decedent paid tax in two or more prior estates.

Identify the property previously taxed and take full credit for the tax paid by theimmediate decedent in the prior estate. If full credit is not allowable, you will bebilled for the additional tax plus applicable interest, if due. The credit is taken onthe Tax Computation schedule as a part of this return.

The methods used in evaluating property listed in this schedule will be the sameas those used in evaluating like property listed in other schedules. Property listed

in this schedule must be valued as of the date of the immediate decedent’s death

and must not appear in any other schedule.

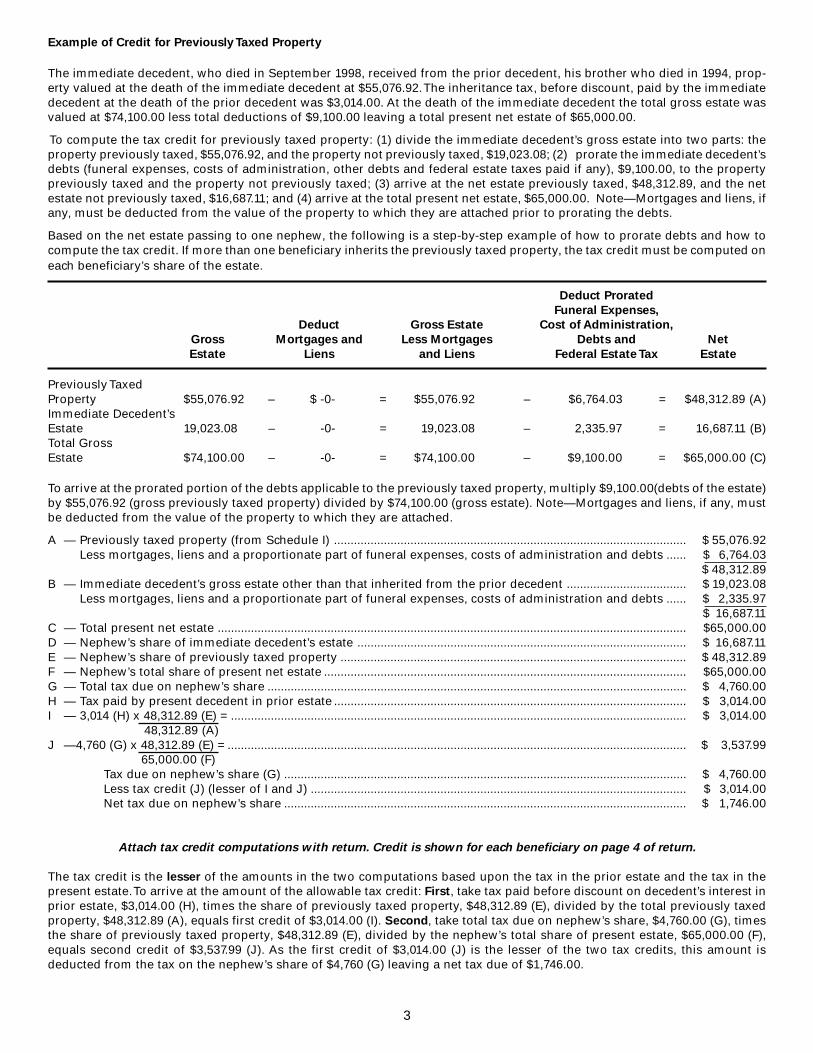

See page 3 of general information for an example.

Estate of:

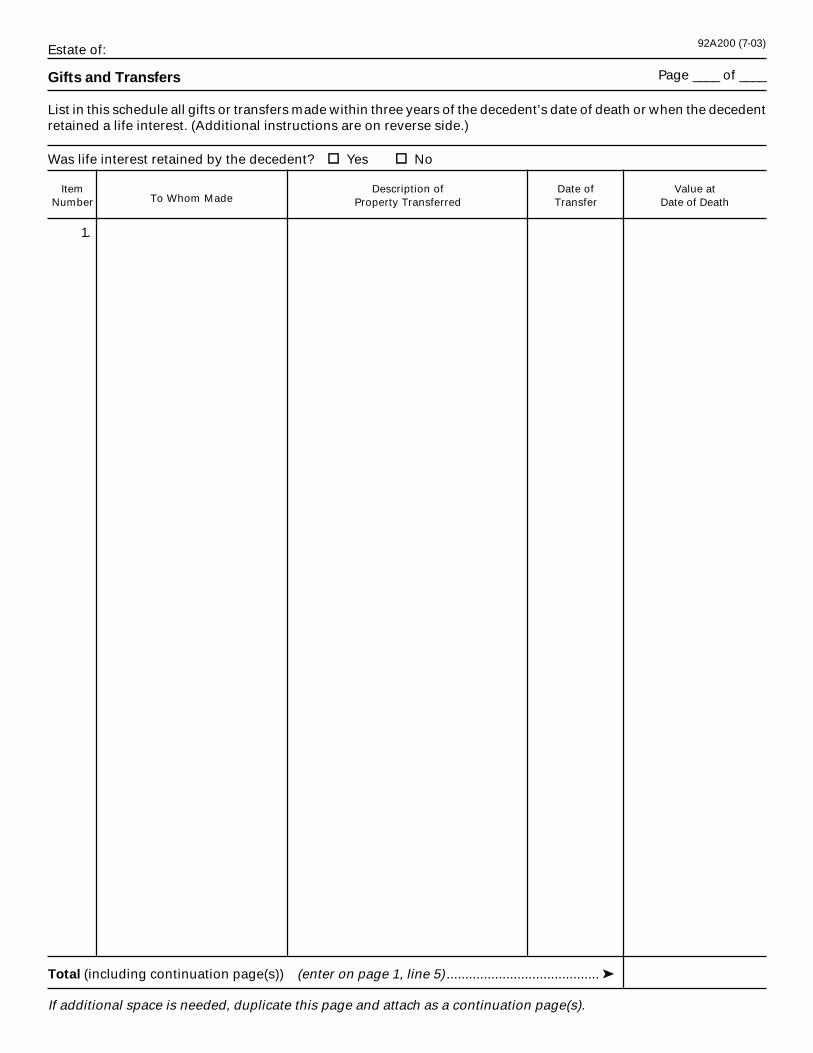

Gifts and Transfers

List in this schedule all gifts or transfers made within three years of the decedent’s date of death or when the decedentretained a life interest. (Additional instructions are on reverse side.)

92A200 (7-03)

Total (including continuation page(s)) (enter on page 1, line 5) ......................................... ➤

ItemNumber

Value atDate of Death

Description ofProperty TransferredTo Whom Made

Date ofTransfer

Was life interest retained by the decedent? Yes No

1.

Page ____ of ____

If additional space is needed, duplicate this page and attach as a continuation page(s).

INSTRUCTIONS

GIFTS AND TRANSFERS

Include all gifts and transfers of property in this schedule made by the dece-dent within three years prior to death and any gift or transfer of propertyduring the decedent’s lifetime in which a life estate or the income was re-tained by the decedent. If made by deed or trust, a copy of such instrument

must be attached. In the event the taxability of the gift or transfer is not in-cluded in the taxable estate, submit details of the transfer and the reason forthe exclusion. To determine the proper taxation of gifts and transfers, refer toKRS 140.020 (see below). For reporting agricultural or horticultural land, seeGeneral Information—Valuation of Property—Fair Cash and Agricultural.

KRS 140.020 reads in part as follows: (1) Any property or interesttherein, of which the decedent has made a transfer by trust or other-wise, in contemplation of or intended to take effect in possession orenjoyment at or after death, including a transfer under which thetransferor has retained for his life or any period not ending beforehis death (a) the possession or enjoyment of, or the income fromthe property; or (b) the actual or contingent power to designate thepersons who shall possess the property or the income therefrom,except in the case of a bona fide sale for an adequate and full con-sideration in money or money’s worth. It shall further apply to anyproperty conveyed in trust over which the settlor has a power ofrevocation exercisable by will.

(2) Every transfer made within three (3) years prior to the death ofthe grantor, vendor or donor of a material part of his estate, or in thenature of a final disposition or distribution thereof, and without anadequate valuable consideration, shall be construed to have beenmade in contemplation of death within the meaning of this chapter.

Estate of:

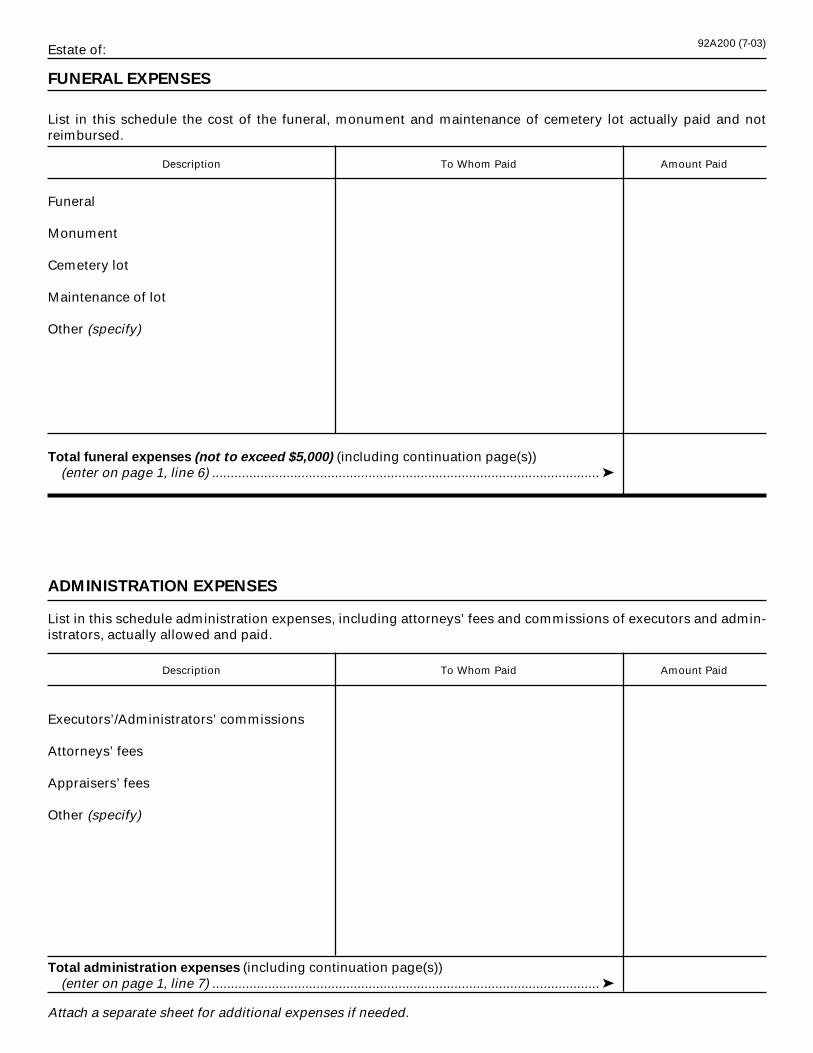

FUNERAL EXPENSES

List in this schedule the cost of the funeral, monument and maintenance of cemetery lot actually paid and notreimbursed.

92A200 (7-03)

Total administration expenses (including continuation page(s))(enter on page 1, line 7) ........................................................................................................ ➤

Description To Whom Paid Amount Paid

Description To Whom Paid Amount Paid

Executors’/Administrators’ commissions

Attorneys’ fees

Appraisers’ fees

Other (specify)

Funeral

Monument

Cemetery lot

Maintenance of lot

Other (specify)

Total funeral expenses (not to exceed $5,000) (including continuation page(s))(enter on page 1, line 6) ........................................................................................................ ➤

ADMINISTRATION EXPENSES

List in this schedule administration expenses, including attorneys’ fees and commissions of executors and admin-istrators, actually allowed and paid.

Attach a separate sheet for additional expenses if needed.

Estate of:

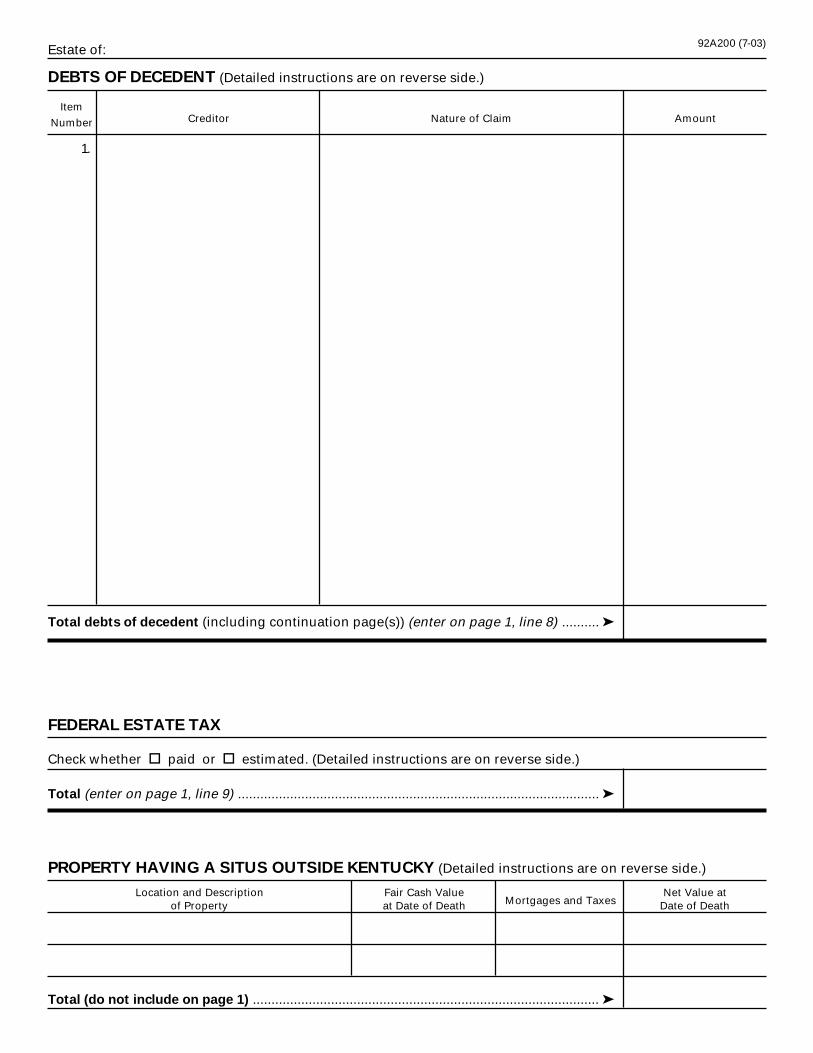

DEBTS OF DECEDENT (Detailed instructions are on reverse side.)

92A200 (7-03)

Total (do not include on page 1) ............................................................................................. ➤

Item

Number

1.

Total debts of decedent (including continuation page(s)) (enter on page 1, line 8) .......... ➤

FEDERAL ESTATE TAX

Check whether paid or estimated. (Detailed instructions are on reverse side.)

Total (enter on page 1, line 9) ................................................................................................. ➤

PROPERTY HAVING A SITUS OUTSIDE KENTUCKY (Detailed instructions are on reverse side.)

Mortgages and TaxesFair Cash Valueat Date of Death

Net Value atDate of Death

Creditor Nature of Claim Amount

Location and Descriptionof Property

INSTRUCTIONS

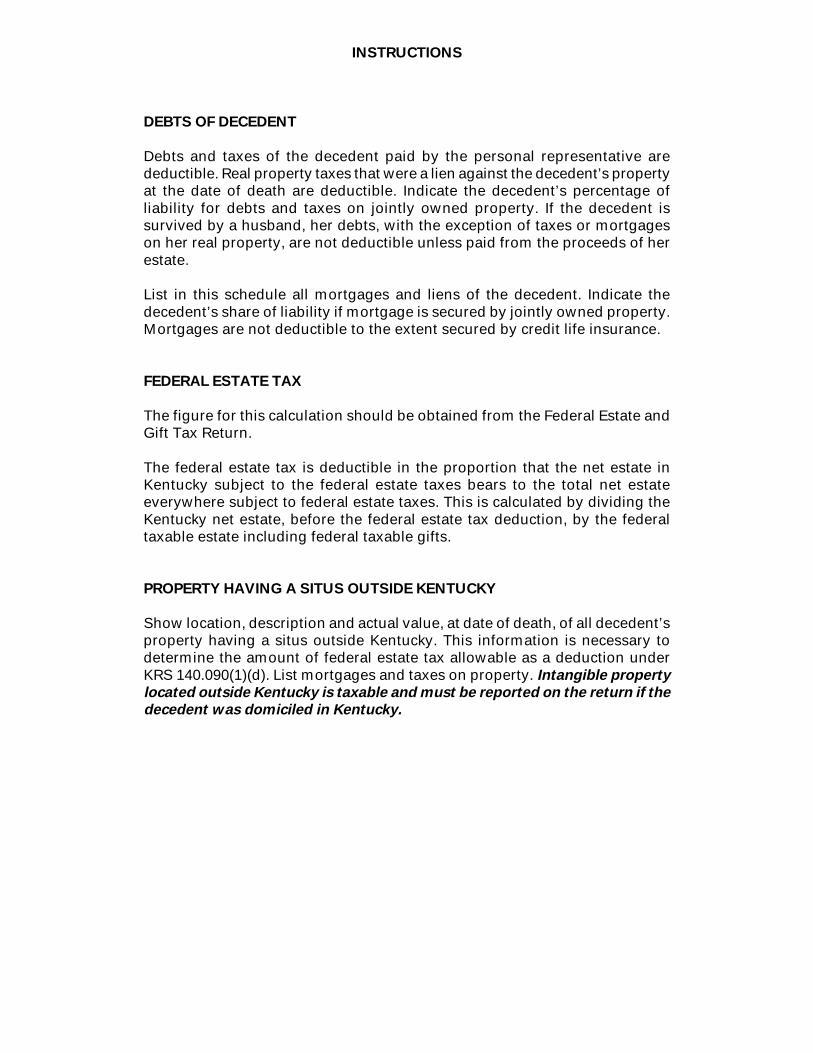

DEBTS OF DECEDENT

Debts and taxes of the decedent paid by the personal representative aredeductible. Real property taxes that were a lien against the decedent’s propertyat the date of death are deductible. Indicate the decedent’s percentage ofliability for debts and taxes on jointly owned property. If the decedent issurvived by a husband, her debts, with the exception of taxes or mortgageson her real property, are not deductible unless paid from the proceeds of herestate.

List in this schedule all mortgages and liens of the decedent. Indicate thedecedent’s share of liability if mortgage is secured by jointly owned property.Mortgages are not deductible to the extent secured by credit life insurance.

FEDERAL ESTATE TAX

The figure for this calculation should be obtained from the Federal Estate andGift Tax Return.

The federal estate tax is deductible in the proportion that the net estate inKentucky subject to the federal estate taxes bears to the total net estateeverywhere subject to federal estate taxes. This is calculated by dividing theKentucky net estate, before the federal estate tax deduction, by the federaltaxable estate including federal taxable gifts.

PROPERTY HAVING A SITUS OUTSIDE KENTUCKY

Show location, description and actual value, at date of death, of all decedent’sproperty having a situs outside Kentucky. This information is necessary todetermine the amount of federal estate tax allowable as a deduction underKRS 140.090(1)(d). List mortgages and taxes on property. Intangible property

located outside Kentucky is taxable and must be reported on the return if the

decedent was domiciled in Kentucky.

Estate of: ___________________________________________________92A200 (7-03)

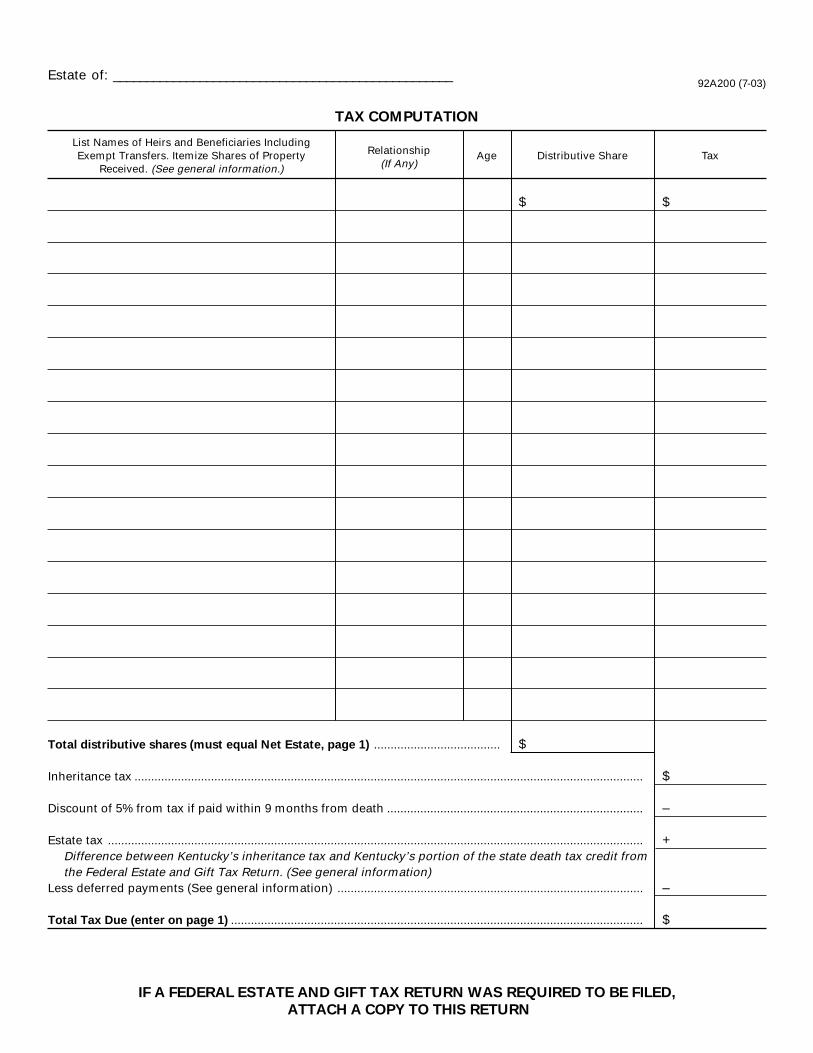

List Names of Heirs and Beneficiaries IncludingExempt Transfers. Itemize Shares of Property

Received. (See general information.)

Relationship(If Any)

Age Distributive Share Tax

$ $

Total distributive shares (must equal Net Estate, page 1) ...................................... $

Inheritance tax ......................................................................................................................................................... $

Discount of 5% from tax if paid within 9 months from death ............................................................................. –

Estate tax ................................................................................................................................................................. +Difference between Kentucky’s inheritance tax and Kentucky’s portion of the state death tax credit fromthe Federal Estate and Gift Tax Return. (See general information)

Less deferred payments (See general information) ............................................................................................ –

Total Tax Due (enter on page 1) ............................................................................................................................ $

TAX COMPUTATION

IF A FEDERAL ESTATE AND GIFT TAX RETURN WAS REQUIRED TO BE FILED,

ATTACH A COPY TO THIS RETURN

FOR DEPARTMENT USE ONLY

__ __ __ __ __ __ / __ __ / __ __ __ __Account Number Tax Year

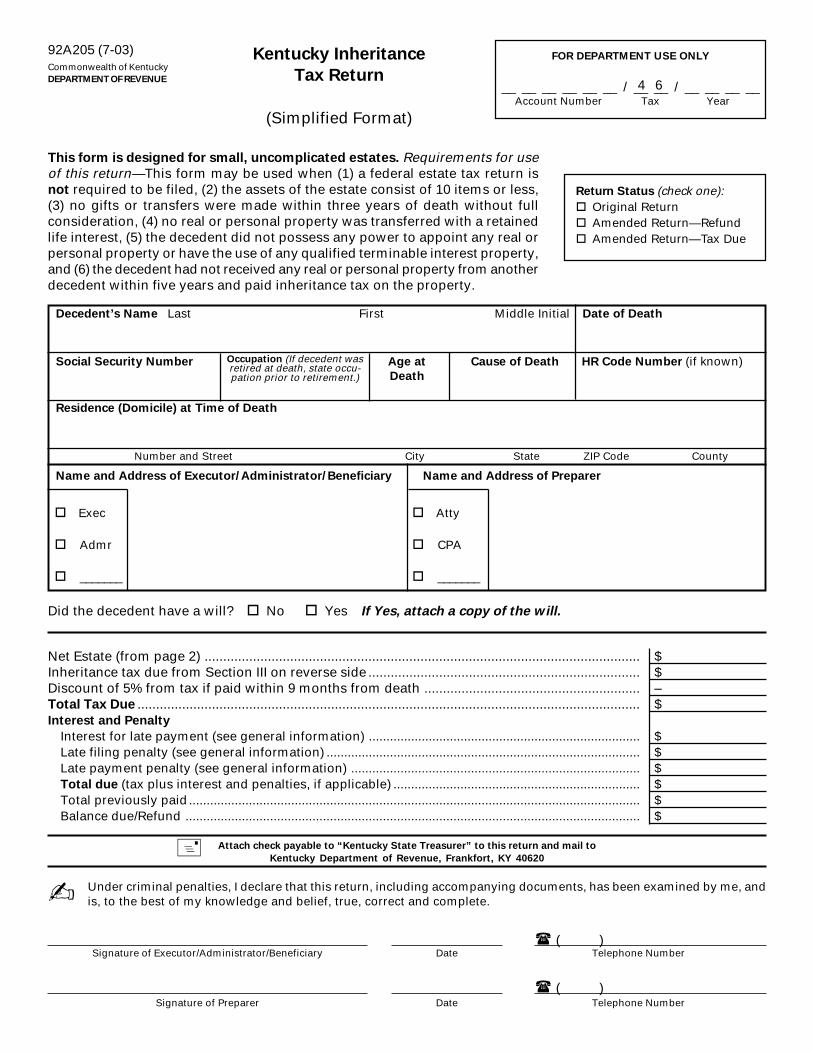

92A205 (7-03)Commonwealth of KentuckyDEPARTMENT OF REVENUE

Kentucky Inheritance

Tax Return

(Simplified Format)

This form is designed for small, uncomplicated estates. Requirements for useof this return—This form may be used when (1) a federal estate tax return isnot required to be filed, (2) the assets of the estate consist of 10 items or less,(3) no gifts or transfers were made within three years of death without fullconsideration, (4) no real or personal property was transferred with a retainedlife interest, (5) the decedent did not possess any power to appoint any real orpersonal property or have the use of any qualified terminable interest property,and (6) the decedent had not received any real or personal property from anotherdecedent within five years and paid inheritance tax on the property.

4 6

Decedent’s Name Last First Middle Initial Date of Death

Social Security Number Age at Cause of Death HR Code Number (if known)Death

Residence (Domicile) at Time of Death

Number and Street City State ZIP Code County

Name and Address of Executor/Administrator/Beneficiary Name and Address of Preparer

Did the decedent have a will? No Yes If Yes, attach a copy of the will.

Net Estate (from page 2) ..................................................................................................................... $Inheritance tax due from Section III on reverse side ......................................................................... $Discount of 5% from tax if paid within 9 months from death .......................................................... –Total Tax Due ....................................................................................................................................... $Interest and Penalty

Interest for late payment (see general information) ............................................................................. $Late filing penalty (see general information) ......................................................................................... $Late payment penalty (see general information) .................................................................................. $Total due (tax plus interest and penalties, if applicable) ...................................................................... $Total previously paid................................................................................................................................ $Balance due/Refund ................................................................................................................................. $

Attach check payable to “Kentucky State Treasurer” to this return and mail to

Kentucky Department of Revenue, Frankfort, KY 40620

Exec

Admr

_______

Atty

CPA

_______

Signature of Executor/Administrator/Beneficiary Date Telephone Number

Signature of Preparer Date Telephone Number

✍

( )

( )

Under criminal penalties, I declare that this return, including accompanying documents, has been examined by me, andis, to the best of my knowledge and belief, true, correct and complete.

Return Status (check one):Original ReturnAmended Return—RefundAmended Return—Tax Due

Occupation (If decedent wasretired at death, state occu-pation prior to retirement.)

92A205 (7-03)SECTION I—GROSS ESTATE

List all items which decedent owned or in which the decedent had an interest. Complete Form 92A204, Real EstateValuation Information Form, for each parcel of real estate.

Ownership (Check or fill in applicable blocks)

Description and Locationof Real or Personal Property

Indi-vidual

With

JointSurvivorship

Without

DatePlaced in

Joint Names

Name ofCo-Owner

Fair CashValue of 100%

Interest atDate of Death

Decedent’sInterest

SECTION II—DEDUCTIONS

Funeral expenses .................................................................................. $ _____________________________

Monument .............................................................................................. $ _____________________________

Cemetery lot and maintenance of lot ................................................. $ _____________________________

Subtotal (not to exceed $5,000) ...................................................................................................................................... $ ________________________

Personal representatives’ commissions ........................................................................................................................ $ ________________________

Attorneys’ fees ................................................................................................................................................................... $ ________________________

Appraisers’ fees and court costs ..................................................................................................................................... $ ________________________

Mortgages and liens (decedent’s share) ........................................................................................................................ $ ________________________

Other debts of decedent (itemize only if total debts exceed $500):________________________________________________________________________________________ .......................... $ ________________________

________________________________________________________________________________________ .......................... $ ________________________

________________________________________________________________________________________ .......................... $ ________________________

________________________________________________________________________________________ .......................... $ ________________________

TOTAL DEDUCTIONS ....................................................................................................................................................... $ ________________________

NET ESTATE (Total Gross Estate Less Total Deductions) (enter on page 1) ........ $ ________________________

List Names of Heirs and Beneficiaries or Exempt Organizations.Itemize shares of property received. (See General Information)

Relationship(If Any)

$ $

SECTION III—TAX COMPUTATION

Distributive Share Tax

Total distributive shares (must equal net estate) ............................................................................. $

Total Inheritance Tax Due (enter on page 1) ............................................................................................................................... $

Age

TOTAL GROSS ESTATE ..................................................................................................................................................... $ ________________________

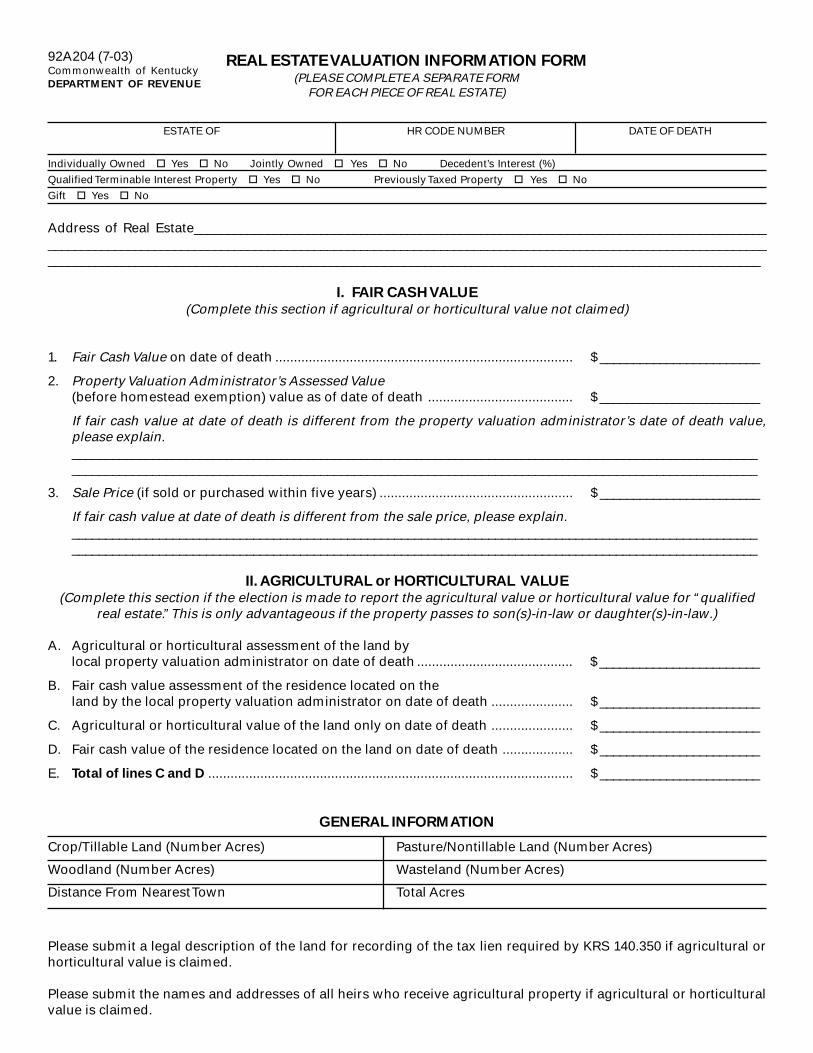

92A204 (7-03)Commonwealth of KentuckyDEPARTMENT OF REVENUE

REAL ESTATE VALUATION INFORMATION FORM(PLEASE COMPLETE A SEPARATE FORM

FOR EACH PIECE OF REAL ESTATE)

ESTATE OF HR CODE NUMBER DATE OF DEATH

Individually Owned Yes No Jointly Owned Yes No Decedent’s Interest (%)

Qualified Terminable Interest Property Yes No Previously Taxed Property Yes No

Gift Yes No

Address of Real Estate____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

I. FAIR CASH VALUE(Complete this section if agricultural or horticultural value not claimed)

1. Fair Cash Value on date of death ................................................................................ $ ________________________

2. Property Valuation Administrator’s Assessed Value(before homestead exemption) value as of date of death ....................................... $ ________________________

If fair cash value at date of death is different from the property valuation administrator’s date of death value,please explain.____________________________________________________________________________________________________________________________________________________________________________________________________________

3. Sale Price (if sold or purchased within five years) .................................................... $ ________________________

If fair cash value at date of death is different from the sale price, please explain.____________________________________________________________________________________________________________________________________________________________________________________________________________

II. AGRICULTURAL or HORTICULTURAL VALUE(Complete this section if the election is made to report the agricultural value or horticultural value for “qualified

real estate.” This is only advantageous if the property passes to son(s)-in-law or daughter(s)-in-law.)

A. Agricultural or horticultural assessment of the land bylocal property valuation administrator on date of death .......................................... $ ________________________

B. Fair cash value assessment of the residence located on theland by the local property valuation administrator on date of death ...................... $ ________________________

C. Agricultural or horticultural value of the land only on date of death ...................... $ ________________________

D. Fair cash value of the residence located on the land on date of death ................... $ ________________________

E. Total of lines C and D .................................................................................................. $________________________

GENERAL INFORMATION

Please submit a legal description of the land for recording of the tax lien required by KRS 140.350 if agricultural orhorticultural value is claimed.

Please submit the names and addresses of all heirs who receive agricultural property if agricultural or horticulturalvalue is claimed.

Crop/Tillable Land (Number Acres) Pasture/Nontillable Land (Number Acres)

Woodland (Number Acres) Wasteland (Number Acres)

Distance From Nearest Town Total Acres

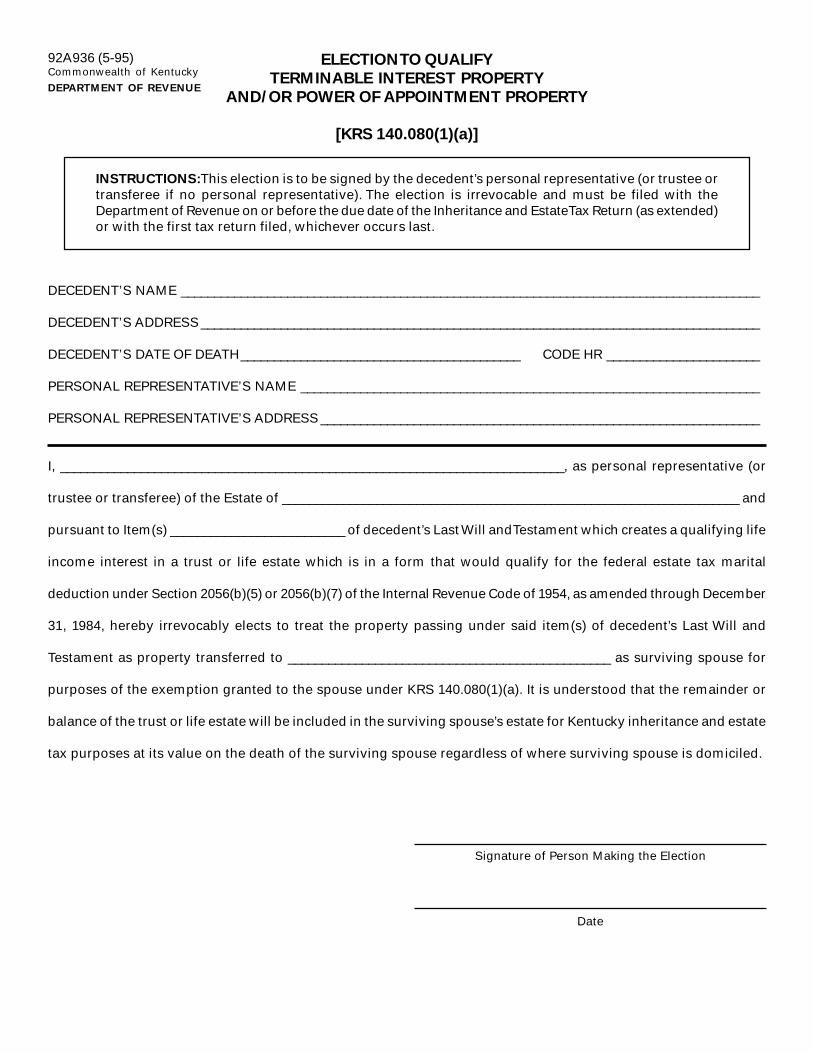

92A936 (5-95)Commonwealth of Kentucky

DEPARTMENT OF REVENUE

ELECTION TO QUALIFY

TERMINABLE INTEREST PROPERTY

AND/OR POWER OF APPOINTMENT PROPERTY

[KRS 140.080(1)(a)]

DECEDENT’S NAME _______________________________________________________________________________________

DECEDENT’S ADDRESS ____________________________________________________________________________________

DECEDENT’S DATE OF DEATH__________________________________________ CODE HR _______________________

PERSONAL REPRESENTATIVE’S NAME _____________________________________________________________________

PERSONAL REPRESENTATIVE’S ADDRESS __________________________________________________________________

I, ___________________________________________________________________________, as personal representative (or

trustee or transferee) of the Estate of ____________________________________________________________________ and

pursuant to Item(s) __________________________ of decedent’s Last Will and Testament which creates a qualifying life

income interest in a trust or life estate which is in a form that would qualify for the federal estate tax marital

deduction under Section 2056(b)(5) or 2056(b)(7) of the Internal Revenue Code of 1954, as amended through December

31, 1984, hereby irrevocably elects to treat the property passing under said item(s) of decedent’s Last Will and

Testament as property transferred to ________________________________________________ as surviving spouse for

purposes of the exemption granted to the spouse under KRS 140.080(1)(a). It is understood that the remainder or

balance of the trust or life estate will be included in the surviving spouse’s estate for Kentucky inheritance and estate

tax purposes at its value on the death of the surviving spouse regardless of where surviving spouse is domiciled.

INSTRUCTIONS: This election is to be signed by the decedent’s personal representative (or trustee ortransferee if no personal representative). The election is irrevocable and must be filed with theDepartment of Revenue on or before the due date of the Inheritance and Estate Tax Return (as extended)or with the first tax return filed, whichever occurs last.

Date

Signature of Person Making the Election

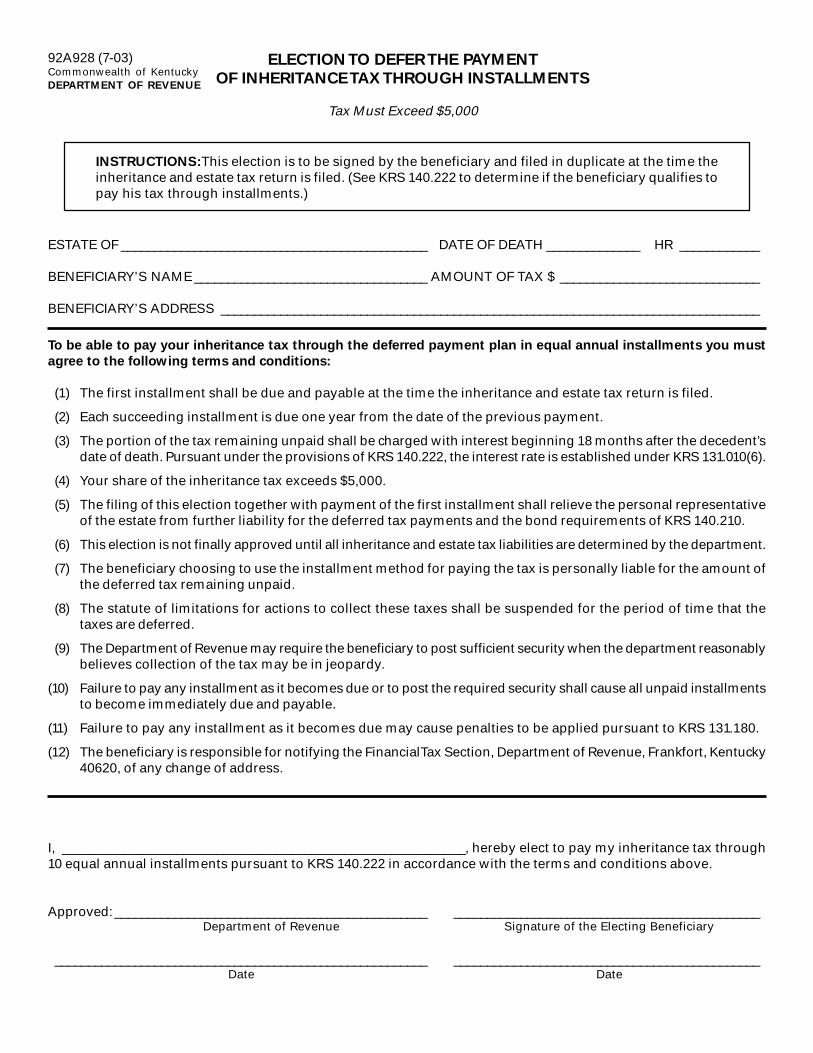

92A928 (7-03)Commonwealth of KentuckyDEPARTMENT OF REVENUE

ELECTION TO DEFER THE PAYMENT

OF INHERITANCE TAX THROUGH INSTALLMENTS

Tax Must Exceed $5,000

INSTRUCTIONS: This election is to be signed by the beneficiary and filed in duplicate at the time theinheritance and estate tax return is filed. (See KRS 140.222 to determine if the beneficiary qualifies topay his tax through installments.)

ESTATE OF ______________________________________________ DATE OF DEATH ______________ HR ____________

BENEFICIARY’S NAME ___________________________________ AMOUNT OF TAX $ ______________________________

BENEFICIARY’S ADDRESS _________________________________________________________________________________

To be able to pay your inheritance tax through the deferred payment plan in equal annual installments you must

agree to the following terms and conditions:

(1) The first installment shall be due and payable at the time the inheritance and estate tax return is filed.

(2) Each succeeding installment is due one year from the date of the previous payment.

(3) The portion of the tax remaining unpaid shall be charged with interest beginning 18 months after the decedent’sdate of death. Pursuant under the provisions of KRS 140.222, the interest rate is established under KRS 131.010(6).

(4) Your share of the inheritance tax exceeds $5,000.

(5) The filing of this election together with payment of the first installment shall relieve the personal representativeof the estate from further liability for the deferred tax payments and the bond requirements of KRS 140.210.

(6) This election is not finally approved until all inheritance and estate tax liabilities are determined by the department.

(7) The beneficiary choosing to use the installment method for paying the tax is personally liable for the amount ofthe deferred tax remaining unpaid.

(8) The statute of limitations for actions to collect these taxes shall be suspended for the period of time that thetaxes are deferred.

(9) The Department of Revenue may require the beneficiary to post sufficient security when the department reasonablybelieves collection of the tax may be in jeopardy.

(10) Failure to pay any installment as it becomes due or to post the required security shall cause all unpaid installmentsto become immediately due and payable.

(11) Failure to pay any installment as it becomes due may cause penalties to be applied pursuant to KRS 131.180.

(12) The beneficiary is responsible for notifying the Financial Tax Section, Department of Revenue, Frankfort, Kentucky40620, of any change of address.

I, ____________________________________________________________, hereby elect to pay my inheritance tax through10 equal annual installments pursuant to KRS 140.222 in accordance with the terms and conditions above.

Approved:_______________________________________________ ______________________________________________

________________________________________________________ ______________________________________________

Department of Revenue

Date

Signature of the Electing Beneficiary

Date

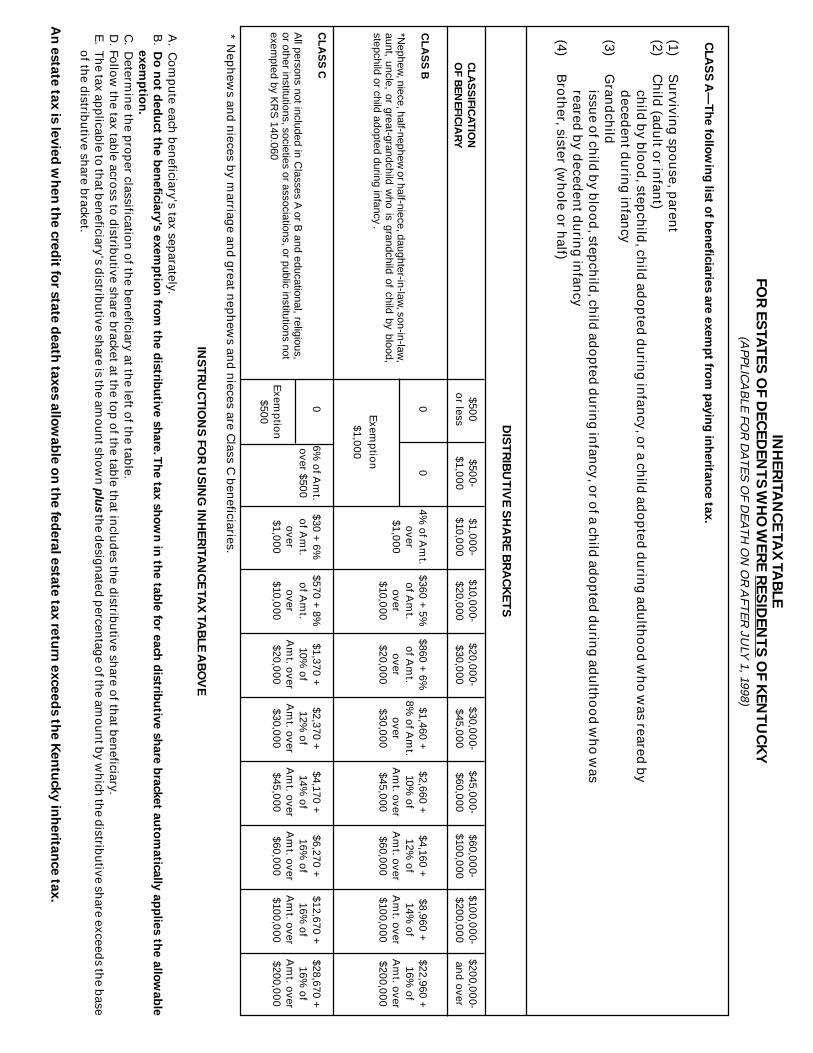

$500$50

0-$1,0

00-

$10,00

0-$20,0

00-

$30,00

0-$45,0

00-

$60,00

0-$10

0,00

0-$20

0,00

0-o

r less$1,0

00

$10,000

$20,000

$30,000

$45,000

$60,000

$100,000

$200,00

0an

d over

INH

ER

ITA

NC

E T

AX

TA

BLE

FO

R E

STA

TE

S O

F D

EC

ED

EN

TS

WH

O W

ER

E R

ES

IDE

NT

S O

F K

EN

TU

CK

Y(A

PPLICA

BLE FO

R D

ATES

OF D

EATH

ON

OR

AFTER

JULY

1, 1998)

CLA

SS

A—

Th

e fo

llow

ing

list o

f ben

efic

iarie

s a

re e

xem

pt fro

m p

ayin

g in

herita

nce ta

x.

CL

AS

S C

All persons not included in C

lasses A or B

and educational, religious,or other institutions, societies or associations, or public institutions notexem

pted by KR

S 140.060

CL

AS

S B

*Nephew

, niece, half-nephew or half-niece, daughter-in-law

, son-in-law,

aunt, uncle, or great-grandchild who is grandchild of child by blood,

stepchild or child adopted during infancy .

Exem

ptio

n

$1,00

0

Exem

ptio

n$500

00

4% o

f Am

t.$360 + 5%

$860 + 6%$1,460 +

$2,660 +$4,160 +

$8,960 +$22,960 +

over

of A

mt.

of A

mt.

8% o

f Am

t.10%

of

12% o

f14%

of

16% o

f$1,0

00o

vero

vero

verA

mt. over

Am

t. overA

mt. over

Am

t. over$10,0

00$20,0

00$30,0

00$45,0

00$60,0

00$100,0

00$200,0

00

06%

of A

mt.

$30 + 6%$570 + 8%

$1,370 +$2,370 +

$4,170 +$6,270 +

$12,670 +$28,670 +

over $50

0o

f Am

t.o

f Am

t.10%

of

12% o

f14%

of

16% o

f16%

of

16% o

fo

vero

verA

mt. over

Am

t. overA

mt. over

Am

t. overA

mt. over

Am

t. over$1,0

00$10,0

00$20,0

00$30,0

00$45,0

00$60,0

00$100,0

00$200,0

00

CLA

SS

IFIC

AT

ION

OF B

EN

EFIC

IAR

Y

* Nep

hew

s and

nieces b

y marriag

e and

great n

eph

ews an

d n

ieces are Class C

ben

eficiaries.

INS

TR

UC

TIO

NS

FO

R U

SIN

G IN

HE

RIT

AN

CE

TA

X T

AB

LE

AB

OV

E

A.

Co

mp

ute each

ben

eficiary's tax separately.

B.

Do

no

t ded

uct th

e b

en

efic

iary

's e

xem

ptio

n fro

m th

e d

istrib

utiv

e s

hare

. Th

e ta

x s

ho

wn

in th

e ta

ble

for e

ach

dis

tribu

tive s

hare

bra

cket a

uto

matic

ally

ap

plie

s th

e a

llow

ab

le

exe

mp

tion

.

C.

Determ

ine th

e pro

per classificatio

n o

f the b

eneficiary at th

e left of th

e table.

D.

Follo

w th

e tax table acro

ss to d

istribu

tive share b

racket at the to

p o

f the tab

le that in

clud

es the d

istribu

tive share o

f that b

eneficiary.

E.

Th

e tax app

licable to

that b

eneficiary's d

istribu

tive share is th

e amo

un

t sho

wn

plu

sth

e desig

nated

percen

tage o

f the am

ou

nt b

y wh

ich th

e distrib

utive sh

are exceeds th

e base

of th

e distrib

utive sh

are bracket.

An

esta

te ta

x is

lev

ied

wh

en

the

cre

dit fo

r sta

te d

ea

th ta

xe

s a

llow

ab

le o

n th

e fe

de

ral e

sta

te ta

x re

turn

exce

ed

s th

e K

en

tuck

y in

he

ritan

ce

tax

.

DIS

TR

IBU

TIV

E S

HA

RE

BR

AC

KE

TS

(1)S

urvivin

g sp

ou

se, paren

t(2)

Ch

ild (ad

ult o

r infan

t)ch

ild b

y blo

od

, stepch

ild, ch

ild ad

op

ted d

urin

g in

fancy, o

r a child

ado

pted

du

ring

adu

ltho

od

wh

o w

as reared b

yd

eceden

t du

ring

infan

cy(3)

Gran

dch

ildissu

e of ch

ild b

y blo

od

, stepch

ild, ch

ild ad

op

ted d

urin

g in

fancy, o

r of a ch

ild ad

op

ted d

urin

g ad

ulth

oo

d w

ho

was

reared b

y deced

ent d

urin

g in

fancy

(4)B

roth

er, sister (wh

ole o

r half)

*Th

e p

rora

ted

exe

mp

tio

n is

ap

plie

d a

t th

e lo

wes

t ta

x ra

tes.

See

gen

eral

info

rmat

ion

, pag

e 5.

** N

eph

ews

and

nie

ces

by

mar

riag

e an

d g

reat

nep

hew

s an

d n

iece

s ar

e C

lass

C b

enef

icia

ries

.A

n e

sta

te t

ax

is le

vie

d w

he

n t

he

cre

dit

fo

r sta

te d

ea

th t

axe

s a

llo

wa

ble

on

th

e fe

de

ral e

sta

te t

ax

re

turn

exce

ed

s t

he

Ke

ntu

ck

y in

he

rita

nce

ta

x.

Cla

ssif

icati

on

of

Ben

efi

cia

ryE

xe

mp

tio

n

(To

Be P

rora

ted

)*B

en

efi

cia

ry's

Taxab

le S

hare

Gra

du

ate

d

Tax R

ate

Tax D

ue

CLA

SS

B

**N

eph

ew, n

iece

, hal

f-n

eph

ew o

r h

alf-

nie

ce,

dau

gh

ter-

in-l

aw, s

on

-in

-law

, au

nt,

un

cle,

or

gre

at-g

ran

dch

ild w

ho

is g

ran

dch

ild o

f ch

ildb

y b

loo

d, s

tep

child

or

child

ad

op

ted

du

rin

gin

fan

cy.

$1,0

00*$

10,0

00 le

ss p

rora

ted

exe

mp

tio

nn

ext $

10,0

00n

ext $

10,0

00n

ext $

15,0

00

nex

t $15

,00

0n

ext $

40,0

00

nex

t $10

0,00

0n

ext $

300,

000

Bal

ance

4% 5% 6% 8% 10%

12%

14%

16%

16%

as c

om

pu

ted

$50

0$

600

$1,

200

$1,

500

$4,

800

$14,

000

$48,

000

as c

om

pu

ted

CLA

SS

C

All

per

son

s n

ot

incl

ud

ed in

Cla

sses

A o

r B

and

ed

uca

tio

nal

, rel

igio

us

or

oth

er in

stit

u-

tio

ns,

so

ciet

ies

or

asso

ciat

ion

s, o

r p

ub

licin

stit

uti

on

s n

ot e

xem

pte

d b

y K

RS

140

.060

.

$50

0*$

10,0

00 le

ss p

rora

ted

exe

mp

tio

nn

ext $

10,0

00n

ext $

10,0

00n

ext $

15,0

00

nex

t $15

,00

0n

ext $

40,0

00

Bal

ance

6% 8% 10%

12%

14%

16%

16%

as c

om

pu

ted

$80

0$

1,00

0$

1,80

0$

2,10

0$

6,40

0as

co

mp

ute

d

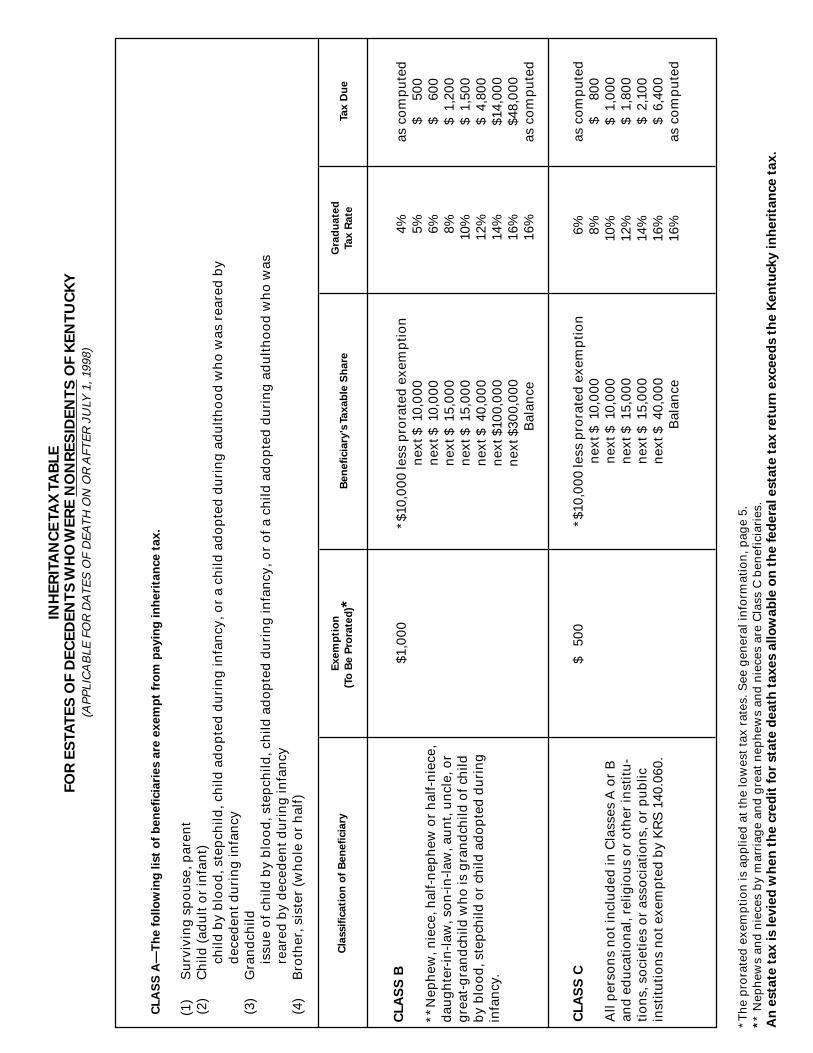

INH

ER

ITA

NC

E T

AX

TA

BLE

FO

R E

STA

TE

S O

F D

EC

ED

EN

TS

WH

O W

ER

E N

ON

RE

SID

EN

TS

OF K

EN

TU

CK

Y(A

PPLI

CA

BLE

FO

R D

ATE

S O

F D

EATH

ON

OR

AFT

ER J

ULY

1, 1

998)

CLA

SS

A—

Th

e f

ollo

win

g l

ist

of

ben

efi

cia

ries a

re e

xem

pt

fro

m p

ayin

g i

nh

eri

tan

ce t

ax.

(1)

Su

rviv

ing

sp

ou

se, p

aren

t(2

)C

hild

(ad

ult

or

infa

nt)

child

by

blo

od

, ste

pch

ild, c

hild

ad

op

ted

du

rin

g in

fan

cy, o

r a

child

ad

op

ted

du

rin

g a

du

lth

oo

d w

ho

was

rea

red

by

dec

eden

t d

uri

ng

infa

ncy

(3)

Gra

nd

child

issu

e o

f ch

ild b

y b

loo

d, s

tep

child

, ch

ild a

do

pte

d d

uri

ng

infa

ncy

, or

of

a ch

ild a

do

pte

d d

uri

ng

ad

ult

ho

od

wh

o w

asre

ared

by

dec

eden

t d

uri

ng

infa

ncy

(4)

Bro

ther

, sis

ter

(wh

ole

or

hal

f)

GENERALINFORMATION

SUPPLEMENTAL DOCUMENTS

If applicable, please submit the following with the return: