law, ethics and communication question 1

TRANSCRIPT

LAW, ETHICS AND COMMUNICATION

Question 1

Communication and revocation of acceptance when complete: The problem is related with the

communication and time of acceptance and its revocation. As per Section 4 of the Indian Contract Act,

1872, the communication of an acceptance is complete as against the acceptor when it comes to the

knowledge of the proposer.

Whereas section 5 of the Indian Contract Act, 1872 says that an acceptance may be revoked at anytime

before the communication of the acceptance is complete as against the acceptor, but not afterwards.

Referring to the above provisions

i) Yes, the revocation of acceptance by Mr. N (the acceptor) is valid.

ii) If Mr. K opens the telegram first (and this would be normally so in case of a rational person) and reads

it, the acceptance stands revoked. If he opens the letter first and reads it, revocation of acceptance is not

possible as the contract has already been concluded.

Question 2:

The fundamental principles relating to ethics may be summarized as under:

1. The Principle of Integrity: It calls upon all accounting and finance professionals to

adhere to honesty and straightforwardness while discharging their respective

professional duties.

2. The Principle of Objectivity: This principle requires accounting and finance

professionals to stick to their professional and financial judgment.

3. The Principle of Confidentiality: This principle requires practitioners of

accounting and financial management to refrain from disclosing confidential

information related to their work.

4. The Principle of Professional Competence and due care: Finance and

accounting professionals need to update their professional skills from time to time in

order to provide competent professional services to their clients.

5. The Principle of Professional Behaviour: This principle requires accounting and

finance professionals to comply with relevant laws and regulations and avoid such

actions which may result in discrediting the profession

Question 3:

Common Policies under Corporate Social Responsibilities are as under:

♦ Commitment to diversity in hiring employees and barring discrimination;

♦ Adoption of internal controls reform;

♦ Management teams that view employees as assets rather than costs;

♦ High performance workplaces that integrate the views of line employees into decision-making processes;

♦ Adoption of operating policies that exceed compliance with social and environmental laws;

♦ Advanced resource productivity, focused on the use of natural resources in a more productive, efficient

and profitable fashion (such as recycled content and product recycling); and

♦ Taking responsibility for conditions under which goods are produced directly or by

contract employees domestically or abroad.

Question 4:

A4. Functions of Interpersonal Communication: Interpersonal communication is important because of the

following functions it achieves:

Gaining Information: One reason, we engage in interpersonal communication, is to gain knowledge about

another individual. We attempt to gain information about others so that we can interact with them more

effectively.

Building Understanding: Interpersonal communication helps us to understand better what someone says

in a given context. Words can mean very different things depending on how they are said or in what

context. Content Messages refer to the surface level meaning of a message. Relationship Messages refer to

how a message is said. The wo are sent simultaneously, but each affects the meaning assigned to the

communication and helps us understand each other better.

Establishing Identity: We also engage in interpersonal communication to establish an identity based on

our relationships and the image we present to others.

Interpersonal Needs: We also engage in interpersonal communication to express interpersonal needs.

William Schutz has identified three such needs: inclusion, control, and affection.

• Inclusion is the need to establish identity with others.

• Control is the need to exercise leadership and prove one's abilities.

• Affection is the need to develop relationships with people. Groups are an excellent way to make friends

and establish relationships.

Question 5:

A formal communication flows along prescribed channels which all organizational members desirous of

communicating with one another are obliged to follow. Every organization has built-in hierarchical system,

communication in an organization is multidirectional. On the basis of various directions in which

communications are sent, we can classify formal communication in these forms:

(i) Downward Communication

(ii) Upward Communication

(iii) Horizontal or Lateral Communication

(iv) Diagonal or Crosswise Communication

Communication generally flows from top to bottom. Downward communication means communication

from superior to subordinate in the hierarchical system of the organization. It includes orders and

instructions. In upward communication, message flows from the subordinate to superior in the form of

request, reports, instructions complaints and suggestions. Communication between co-workers with

different areas of responsibility is called horizontal (lateral) communication. Communication among the

functional managers of a company is the best example of horizontal communication. Diagonal

communication means communication among the various Department/ employees of the organization

without any hierarchical system in case of emergency

Question 6:

Characteristics of Group Personality: Following are the characteristics of group personality:

i) Spirit of Conformity: Individual members soon come to realize that in order to gain recognition,

admiration and respect from others they have to achieve a spirit of conformity. Our beliefs, opinions, and

actions are influenced more by group opinion than by an individual’s opinion, even if it is an expert’s

opinion.

ii) Respect for group values: Any working group is likely to maintain certain values and ideals which

make it different from others. In order to deal effectively with a group we must understand its values

which will guide us in foreseeing its programmes and actions.

iii) Resistance to change: It has been observed that a group generally does not take kindly to social

changes. On the other hand the group may bring about its own changes, whether by dictation of its leader

or by consensus. The degree to which a group resists change serves as an important index of its

personality. It helps us in dealing with it efficiently.

iv) Group prejudice: Just as hardly any individual is free from prejudice, groups have their own clearly

evident prejudices. It is a different matter that the individual members may not admit their prejudiced

attitude to other’s race, religion, nationality etc. But the fact is that the individual’s prejudices get further

intensified while coming in contact with other members of the group holding similar prejudices.

v) Collective power: It need not be said that groups are always more powerful than individuals, how so

ever influential the individual may be. That is why individuals may find it difficult to speak out their

minds in groups. There is always the risk of the one-against-many situation cropping up.

Question 7:

The Companies Act, 2013 vide sections 34 and 35 lay down the criminal and civil liabilities of the guilty

parties in case of mis-statements and misleading inclusions and omissions in a prospectus. Further, section

36 lays down the punishment for fraudulently inducing persons to invest moneys. However, the present

case before us is not in respect of liability for a possible misstatement but on the right of the allottee to

avoid the contract of purchasing the shares from the company. In order to decide this, key factor is to

determine if any material misrepresentation or concealment of a material fact has taken place and if such

misrepresentation is fraudulent.

The non disclosure of the fact that dividends were paid out of capital profits is a concealment of material

fact as a company is normally required to distribute dividend only from trading or revenue profits and

under exceptional circumstances can do so out of capital profits. Hence, a material misrepresentation has

been made.

Hence, in the given case the allottee can avoid the contract of allotment of shares.

Question 8:

Small Company: Under Section 2 (85) of the Companies Act, 2013, “small company” means a company,

other than a public company:-

i) having paid-up share capital not exceeding fifty lakh rupees or such higher amount as may be prescribed

which shall not be more than five crore rupees; and

ii) having turnover as per its last profit and loss account not exceeding two crore rupees or such higher

amount as may be prescribed which shall not be more thantwenty crore rupees.

Exceptions: This section shall not apply to:

A holding company or a subsidiary company;

A Company registered under section 8, or

A Company or body corporate governed by any special Act.

Question 9:

The Companies Act 2013 has made alteration of memorandum simpler. Under Section 13(1) of the Act

allows the company to alter provisions of the Memorandum by a Special Resolution. In the case of

alteration of the Objects clause Section 13(6) requires filing of the Special Resolution with the Registrar.

Section 13(9) states that the Registrar shall register any alteration to the Memorandum with respect to the

objects of the company and certify the registration within 30 days from date of filing of Special Resolution

by the company.

Section 13(10) states no effect will be realized unless registration is done as above.

Hence Vardhman Industries can make the required changes.

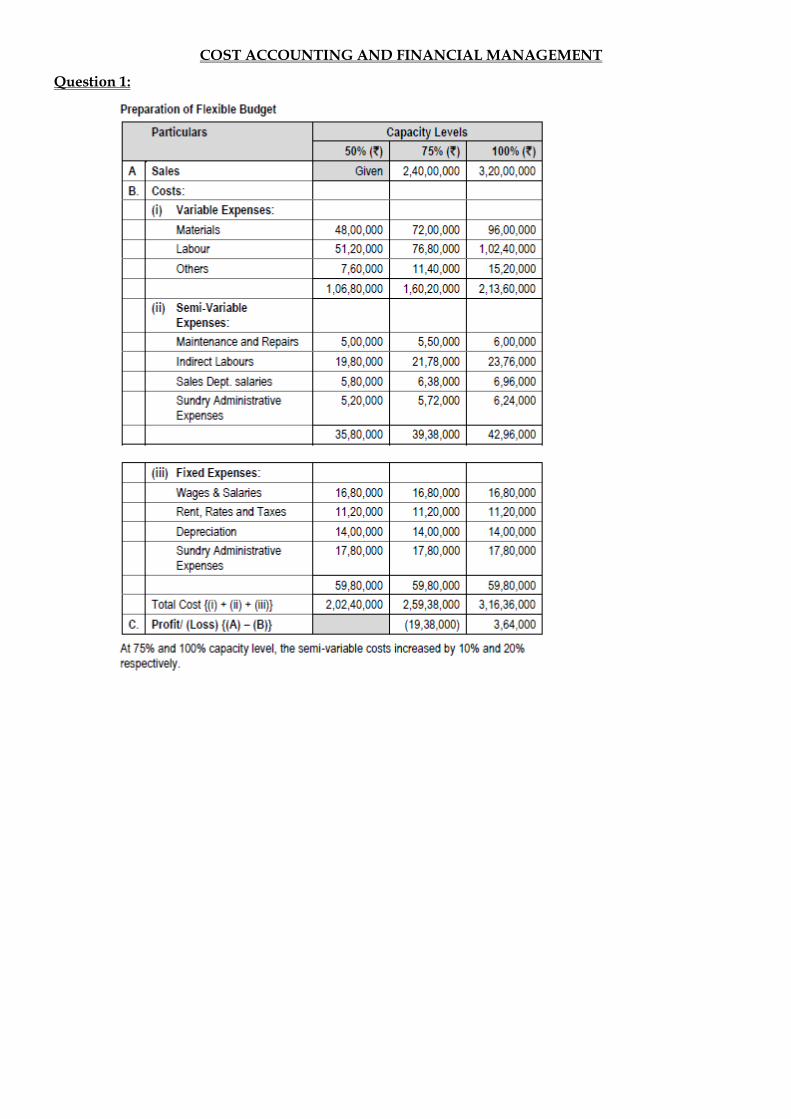

COST ACCOUNTING AND FINANCIAL MANAGEMENT

Question 1:

Question 2:

Question 3:

Question 4:

Question 5:

TAXATION

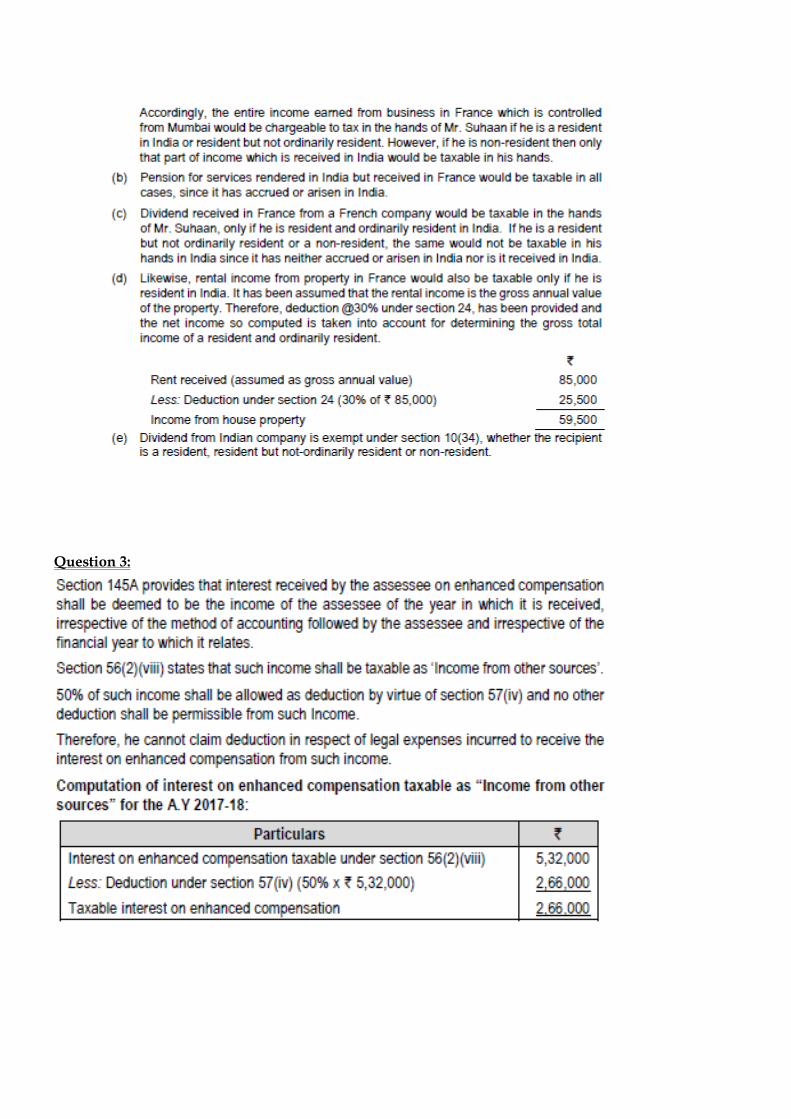

Question 1:

Question 2:

Question 3:

Question 4:

Question 5:

Question 6:

Question 7:

1. Reduced Tax evasion

2. Increased Tax Compliance

3. Certainty

4. Transparency

5. Cheaper exports

6. Better accounting systems

7. Neutrality

ADVANCED ACCOUNTING

Question 1:

Question 2: As per para 41 of AS 26 ‘Intangible Assets’, no intangible asset arising from research (or from the research phase of an internal project) should be recognized. Expenditure on research (or on the research phase of an internal project) should be recognized as an expense when it is incurred. Thus the company cannot treat the expenditure as deferred revenue expenditure. The entire amount of `33 lakhs spent on research project should be charged as an expense in the year ended31st March, 2016.

Question 3: AS 29 “Provisions, Contingent Liabilities and Contingent Assets” provides that when an enterprise has a present obligation, as a result of past events, that probably requires an outflow of resources and a reliable estimate can be made of the amount of obligation, a provision should be recognized. Alpha Ltd. has the obligation to deliver the goods within the scheduled time as per the contract. It is probable that Alpha Ltd. will fail to deliver the goods within the schedule and it is also possible to estimate the amount of compensation. Therefore, Alpha Ltd. should provide for the contingency amounting ` 2 crores as per AS 29.

Question 4:

Question 5:

.a) An asset is defined as:

a resource controlled by the entity; as a result of past events; and from which future economic benefits are expected to flow to the entity.

b) A liability is defined as:

a present obligation of an entity arising from past events the settlement of which is expected to result in an outflow of resources that embody economic

benefits.

c) Equity is the remaining interest in an entity, after all its liabilities have been deducted from the value of its assets. It’s purely a ‘balance sheet valuation’ of the entity’s net assets and it not representative of the entity’s market value.In the financial reports of an entity, equity will be broken down into share capital, share premium account and retained earnings.

d) Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or other liabilities, which arise.

They include:

Expenses which arise in the normal course of activities, such as the cost of sales and operating costs, including depreciation of non-current assets. These result in the outflow of assets and increase in liabilities.

Losses include for example, the loss on disposal of a non-current asset, and losses arising from damage caused to assets. Losses are usually reported as net of any related income.

Losses may also be unrealised. Unrealised losses occur when an asset’s value decreases but is not disposed of. For example, and unrealised loss occurs when property owned by the entity is revalued downwards, but kept.

Expenses are recognised in the statement of profit or loss and other comprehensive income when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably.

e) Revenue:

is income that arises in the course of ordinary activities of an entity and is comes from a number of sources including sales, fees, interest, dividends and royalties.

Gains:

represent other items that meet the definition of income, and may or may not include items arising in the normal course of business.

represent increases in the future economic benefits, and as such are no different in nature from revenue.

Realised gains are those where an asset has been sold for more than its carrying amount. Realised gains are often reported in the financial statements net of related expenses. Gains might also be unrealised. Unrealised gains occur whenever an assets value increases, but is

not disposed of. For example, an unrealised gain occurs when marketable securities owned by the entity are

revalued upwards.

A6. As per AS 26 ‘Intangible Assets’, the depreciable amount of an intangible asset should be allocated on a systematic basis over its useful life. Also there is a rebuttable presumption that the useful life of an intangible asset will not exceed 10 years from the date it is available for use. The amortization should commence when the asset is available for use. As per para 78 of AS 26, if there has been a significant change in the expected pattern of economic benefits from the asset, the amortisation method should be changed to reflect the changed pattern. The company has been following a policy of amortization over a period of 8 years. As on 01-4-2015, 5 years have passed and the carrying amount stands at ` 30 lakhs. If the same treatment were to be continued, this would have been amortized over the next 3 years. But the revised estimate of remaining useful life would extend the period by another 5 years to amortize the carrying amount, the Company would be advised to amortise the carrying value over the next 5 years. Thus after revision in estimated useful life, the amount of ` 30 lacs would be amortised over next 5 years.

AUDITING AND ASSURANCE:

Question 1: Defalcation of Cash: Defalcation of cash has been found to perpetrate generally in the following ways - a) By inflating cash payments. Examples of inflation of payments: i) Making payments against fictitious vouchers. ii) Making payments against vouchers, the amounts whereof have been inflated. iii) Manipulating totals of wage rolls either by including therein names of dummy workers or by inflating them in any other manner. iv) Casting a larger totals for petty cash expenditure and adjusting the excess in the totals of the detailed columns so that cross totals show agreement. b) By suppressing cash receipts. Few Techniques of how receipts are suppressed are: i) Teeming and Lading: Amount received from a customer being misappropriated; also to prevent its detection the money received from another customer subsequently being credited to the account of the customer who has paid earlier. Similarly, money received from the customer who has paid thereafter being credited to the account of the second customer and such a practice is continued so that no one account is outstanding for payment for any length of time, which may lead the management to either send out a statement of account to him or communicate with him. ii) Adjusting unauthorized or fictitious rebates, allowances, discounts etc. to customer’ accounts and misappropriating amount paid by them. iii) Writing off as debts in respect of such balances against which cash has already been received but has been misappropriated. iv) Not accounting for cash sales fully. v) Not accounting for miscellaneous receipts e.g. sale of scrap, quarters allotted to the employees etc. vi) Writing down asset values in entirety, selling them subsequently and misappropriating the proceeds. c) By casting wrong totals in the cash book. Question 2: Identification of Significant Risks: SA 315 “Identifying and Assessing the Risk of Material Misstatement through understanding the Entity and its Environment” defines ‘significant risk’ as an identified and assessed risk of material misstatement that, in the auditor’s judgment, requires special audit consideration. As part of the risk assessment, the auditor shall determine whether any of the risks identified are, in the auditor’s judgment, a significant risk. In exercising this judgment, the auditor shall exclude the effects of identified controls related to the risk. In exercising judgment as to which risks are significant risks, the auditor shall consider at least the following) i) Whether the risk is a risk of fraud; ii) Whether the risk is related to recent significant economic, accounting or other developments like changes in regulatory environment etc. and therefore requires specific attention; iii) The complexity of transactions; iv) Whether the risk involves significant transactions with related parties; v) The degree of subjectivity in the measurement of financial information related to the risk, especially those measurements involving a wide range of measurement uncertainty; and vi) Whether the risk involves significant transactions that are outside the normal course of business for the entity or that otherwise appear to be unusual.

Question 3: Tests of Control: Tests of control are performed to obtain audit evidence about the effectiveness of the - i) Design of the accounting and internal control systems, that is, whether they aresuitably designed to prevent or detect and correct material misstatements; and ii) Operation of the internal controls throughout the period. Tests of control include tests of elements of the control environment where strengths in the control environment are used by auditors to reduce control risk. Tests of control may include:

Inspection of documents supporting transactions and other events to gain audit evidence that internal controls have operated properly, for example, verifying that a transaction has been authorised.

Inquiries about, and observation of, internal controls which leave no audit trail, for example, determining who actually performs each function and not merely who issupposed to perform it.

Re-performance of internal controls, for example, reconciliation of bank accounts, to ensure they were correctly performed by the entity.

Testing of internal control operating on specific computerised applications or over the overall information technology function, for example, access or program change controls. Question 4: Concept of “True and Fair”: The concept of “true and fair” is a fundamental concept in auditing. The phrase “true and fair” in the auditor’s report signifies that the auditor is required to express his opinion as to whether the state of affairs and the results of the entity as ascertained by him in the course of his audit are truly and fairly represented in the accounts under audit. This requires that the auditor should examine the accounts with a view to verifying that all assets and liabilities, incomes and expenses are stated at the amounts which are in accordance with accounting principles and policies, and no material item has been omitted. The importance of the concept of true and fair view can also be understood and appreciated from the facts that sections 128, 129 and 143 of the Companies Act, 2013 also discusses this concept in relation to account books, financial statements and reporting on financial statements respectively. Section 128(1) of the said Act provides that every company shall prepare and keep at its registered office books of account and other relevant books and papers and financial statement for every financial year which give a true and fair view of the state of the affairs of the company, including that of its branch office or offices, if any. The company shall be in a position to explain the transactions effected both at the registered office and its branches. Such books of Accounts shall be kept on accrual basis and according to the double entry system of accounting. Section 129(1) of the Companies Act, 2013 provides that the financial statements shall give a true and fair view of the state of affairs of the company or companies, comply with the accounting standards notified under section 133 of the Companies Act, 2013, (in which the Central Government may prescribe the standards of accounting or any addendum thereto, as recommended by the Institute of Chartered Accountants of India, constituted under section 3 of the Chartered Accountants Act, 1949, in consultation with and after examination of the recommendations made by the National Financial Reporting Authority) and shall be in the form or forms as may be provided for different class or classes of companies in Schedule III to the said Act. The term “financial statement” shall include any notes annexed to or forming part of such financial statement, giving information required to be given and allowed to be given in the form of such notes under the said Act. It may be noted that nothing contained in sub-section (1) shall apply to any insurance or banking company or any company engaged in the generation or supply of electricity, or to any other class of company for which a form of financial statement has been specified in or under the Act governing such class of company.

However, the financial statements shall not be treated as not disclosing a true and fair view of the state of affairs of the company, merely by reason of the fact that they do not disclose- (a) in the case of an insurance company, any matters which are not required to be disclosed by the Insurance Act, 1938, or the Insurance Regulatory and Development Authority Act, 1999; (b) in the case of a banking company, any matters which are not required to be disclosed by the Banking Regulation Act, 1949; (c) in the case of a company engaged in the generation or supply of electricity, any matters which are not required to be disclosed by the Electricity Act, 2003; (d) in the case of a company governed by any other law for the time being in force, any matters which are not required to be disclosed by that law. It may be noted that where the financial statements of a company do not comply with the accounting standards referred to in sub-section (1), the company shall disclose in its financial statements, the deviation from the accounting standards, the reasons for such deviation and the financial effects, if any, arising out of such deviation. Further, according to section 143(2) of the said Act, the auditor is required to make a report to the members of the company indicating that, to the best of his information and knowledge, the financial statements give a true and fair view of the state of the company’s affairs as at the end of its financial year and profit or loss and cash flow for the year and such other matters as may be prescribed. SA 700 “Forming an Opinion and Reporting on Financial Statements”, requires the auditor to form an opinion on the financial statements based on an evaluation of the conclusions drawn from the audit evidence obtained; and express clearly that opinion through a written report that also describes the basis for the opinion. The auditor is required to express his opinion on the financial statements that it gives a true and fair view in conformity with the accounting principles generally accepted in India (a) in the case of the Balance Sheet, of the state of affairs of the Company as at March 31, 20XX; (b) in the case of the Statement of Profit and Loss, of the profit/ loss for the year ended on that date; and (c) in the case of the Cash Flow Statement, of the cash flows for the year ended on that date. Question 5: a) Incorrect: SA 700 deal with forming an opinion and reporting of financial statement whereas SA 705 deals with modifications to the opinion in the Independent Auditor’s Report. b)

Question 6: Sufficient appropriate audit evidence: The auditor shall design and perform audit procedures that are appropriate in the circumstances for the purpose of obtaining sufficient appropriate audit evidence. SA 500 on ‘Audit Evidence’ further expounds this concept. According to it, the sufficiency and appropriateness of audit evidence are interrelated. Sufficiency is the measure of the quantity of audit evidence. The quantity of audit evidence needed is affected by the auditor’s assessment of the risks of misstatement (the higher the assessed risks, the more audit evidence is likely to be required) and also by the quality of such audit evidence (the higher the quality, the less may be required). Obtaining more audit evidence, however, may not compensate for its poor quality. Appropriateness is the measure of the quality of audit evidence; that is, its relevance and its reliability in providing support for the conclusions on which

the auditor’s opinion is based. The reliability of evidence is influenced by its source and by its nature, and is dependent on the individual circumstances under which it is obtained. SA 330 requires the auditor to conclude whether sufficient appropriate audit evidence has been obtained. Whether sufficient appropriate audit evidence has been obtained to reduce audit risk to an acceptably low level, and thereby enable the auditor to draw reasonable conclusions on which to base the auditor’s opinion, is a matter of professional judgment. Further, SA 200 contains discussion of such matters as the nature of audit procedures, the timeliness of financial reporting, and the balance between benefit and cost, which are relevant factors when the auditor exercises professional judgment regarding whether sufficient appropriate audit evidence has been obtained. In general the various factors which may influence the auditor’s judgment as to what is sufficient and appropriate audit evidence are as under: (i) Degree of risk of misstatements which may be affected by factors such as the nature of items, adequacy of internal control, nature and size of businesses carried out by the entity, situations which may exert an unusual influence on management and the financial position of the entity. (ii) The materiality of the item. (iii) The experience gained during previous audits. (iv) The results of auditing procedures, including fraud and errors which may have been found. (v) The type of information available. (vi) The trend indicated by accounting ratios and analysis. Question 7: Disclosure of Accounting Policies: The view presented in the financial statements of an enterprise of its state of affairs and of the profit or loss can be significantly affected by the accounting policies followed in the preparation and presentation of the financial statements. The accounting policies followed vary from enterprise to enterprise. Disclosure of significant accounting policies followed is necessary if the view presented is to be properly appreciated. The disclosure of some of the accounting policies followed in the preparation and presentation of the financial statements is required by some cases. The purpose of AS 1 is to promote better understanding of financial statements by establishing through an accounting standard and the disclosure of significant accounting policies and the manner in which such accounting policies are disclosed in the financial statements. Such disclosure would also facilitate a more meaningful comparison between financial statements of different enterprises. To ensure proper understanding of financial statements, it is necessary that all significant accounting policies adopted in the preparation and presentation of financial statements should be disclosed. Such disclosure should form part of the financial statements. It would be helpful to the reader of financial statements if they are all disclosed at one place instead of being scattered over several statements, schedules and notes which form part of financial statements. Any change in accounting policy, which has a material effect, should be disclosed. The amount by which any item is in the financial statement is affected by such change should also be disclosed to the extent ascertainable. Where such amount is not ascertainable, wholly or in part, the fact should be indicated. If a change is made in the accounting policies, which has not material effect on the financial statements for the current period, which is reasonably expected to have material effect in latter periods, the fact of such change should be appropriately disclosed in the period in which the change is adopted.

INFOTECH & STRATEGIC MANAGEMENT

Question 1: (a) Corporate strategy is basically the growth design of the firm; it spells out the growth objective - the direction, extent, pace and timing of the firm's growth. It also spells out the strategy for achieving the growth. It serves as the design for filling the strategic planning gap. It also helps build the relevant competitive advantages. (b) A Strategic vision is a road map of a company’s future – providing specifics about technology and customer focus, the geographic and product markets to be pursued, the capabilities it plans to develop, and the kind of company that management is trying to create. Question 2: (a) Incorrect: No, Strategic management is not a bundle of tricks and magic. It is much more serious affair. It involves systematic and analytical thinking and action. Although, the success or failure of a strategy is dependent on several extraneous factors, it cannot be stated that a strategy is a trick or magic. Formation of strategy requires careful planning and requires strong conceptual, analytical, and visionary skills. (b) Correct: Corporate strategy in the first place ensures the growth of the firm and ensures the correct alignment of the firm with its environment. It serves as the design for filling the strategic planning gap. It also helps to build the relevant competitive advantages. Question 3: Individuals in organisations relate themselves with the vision of their organisations in different manner. When the individuals are able to bring organisational vision close to their hearts and minds they have "shared vision". Shared vision is a force that creates a sense of commonality that permeates the organization and gives coherence to diverse activities. However, 'vision shared' shows imposition of vision from the top management. It may demand compliance rather than commitment. For success of organisations having shared vision is better than vision shared. Question 4: A typical large organization is a multidivisional organisation that competes in several different businesses. It has separate self-contained divisions to manage each of these. There are three levels of strategy in management of business - corporate, business, and functional. The corporate level of management consists of the chief executive officer and other top level executives. These individuals occupy the apex of decision making within the organization. The role of corporate-level managers is to oversee the development of strategies for the whole organization. This role includes defining the mission and goals of the organization, determining what businesses it should be in, allocating resources among the different businesses and so on rests at the Corporate Level. The development of strategies for individual business areas is the responsibility of the general managers in these different businesses or business level managers. A business unit is a self-contained division with its own functions - for example, finance, production, and marketing. The strategic role of business-level manager, head of the division, is to translate the general statements of direction and intent that come from the corporate level into concrete strategies for individual businesses. Functional-level managers are responsible for the specific business functions or operations such as human resources, purchasing, product development, customer service, and so on. Thus, a functional manager's sphere of responsibility is generally confined to one organizational activity, whereas general managers oversee the operation of a whole company or division.

Question 1:

Question 2: Pre-requisites of ACID TEST for any TPS are as follows:

• Atomicity: This means that a transaction is either completed in full or not at all.

TPS systems ensure that transactions take place in their entirety. For example, if funds are transferred from one account to another, this only counts as a bonafide transaction if both the withdrawal and deposit take place. If one account is debited and the other is not credited, it does not qualify as a transaction.

• Consistency: TPS systems exist within a set of operating rules (or integrity

constraints). If an integrity constraint states that all transactions in a database must have a positive value, any transaction with a negative value would be refused.

• Isolation: Transactions must appear to take place in seclusion. For example,

when a fund transfer is made between two accounts the debiting of one and the crediting of another must appear to take place simultaneously. The funds cannot be credited to an account before they are debited from another.

• Durability: Once transactions are completed they cannot be undone. To ensure

that this is the case even if the TPS suffers failure, a log will be created to document all completed transactions.

Question 3: Information is a significant resource to an organization as it represents the organization’s tangible and intangible resources and all transactions relating to those resources. Information influences the way an organization operates. The right information, if it is transported to the right person, in the right fashion, and at the right time, can progress and guarantee organizational effectiveness and competence. The Business Information System is the mechanism used to manage and control the information resource. An Information System is an integrated process of components for collecting, storing, processing, and communicating information. Any specific Information System aims to support operations, management and decision making. Information Systems (IS) refers to the interface of People, Processes, and Technology. People are considered as a Frontline Employees, executives and managers that need technology to process the information in fast and accurate manner. The role of information systems in the organization is shifting to support business processes rather than individual functions. The focus is outwards to customers, rather than inwards to procedures. Information Technology is an exceptionally imperative and acquiescent resource offered to organizations. As information systems have facilitated supplementary varied human

activities, they have put forth a thoughtful power over civilization. These systems have impacted the pace of growth of day-to-day activities, expanded the scope of service offerings and empowered enterprises to reach out to customers across the world without the limitations of time and space. People require information for many reasons and in varied ways. For example, we probably seek information for entertainment and enlightenment by viewing television, watching movies, browsing the Internet, listening to the radio, and reading newspapers, magazines, and books. In business, however, people and organizations seek and use information specifically to make sound decisions and to solve problems - two closely related practices that form the foundation of every successful company.

Question 4: