lbs july 2016

TRANSCRIPT

Monthly Economic News and Views

Presented by B.J. Rewane Financial Derivatives Company Limited

Lagos Business School

Executive Breakfast Meeting July 13, 2016

Nigeria Stumbles into Economic Reform

2

Nigeria Responds to Crisis

Market economy in sequence

Policy Reform: hard choices and change

The Outcome: difficult and uncertain

Outlook: positive but painful

3 Outline: Making Sense of the New Normal

Highlights & Indicators

Long Winding Path towards Reform

Winners & Losers- Markets

The Political Pushback

Outlook for July

June Highlights

5 Finally A Month of Inflection

From month of woe to June of glow

In May, another lull in economic activities

Q2 GDP growth estimated to fall to -1.5%

Meaning that Nigeria is in Recession

IMF fears that 2016 will be a full year of negative growth

EIU revised full year GDP down to 0.4% from 2.1%

Fitch downgrades sovereign rating to B+

6 Finally A Month of Inflection

CBN published PMI shrank 8.5% from 45.8 to 41.9

Output, new orders, inventories & hiring all down sharply

Power supply from national grid down to 2,828MW

Average airline load factors declined for the 3rd consecutive month

7 Finally A Month of Inflection

Oil production crashed to 1.4mbpd from a high of 1.9mbpd

Mainly from the offshore and deepwater assets

From where the FGN earns more dollars

FAAC shared amongst states increased fractionally to N305bn

Mainly due to improved collection from FIRS

Average oil price in June was $49.99pb

41.8% above Q1 price of $35.21pb

8 Finally A Month of Inflection

Rig count in Nigeria down by 16.67% to 5

At the peak, Nigeria had 22 rigs

Headline inflation spikes to 16.5%

Highest level in 6 years

Nigeria now has the 8th highest inflation rate in SSA

6.6% above the 9% inflation ceiling of the CBN

9 Finally A Month of Inflection

Money supply now N20.72trn, annualized growth of 2.1%

Average opening position of banks up to N189.64bn

Average interbank interest rates surged to 75% p.a. before

dropping to 4.5%

CBN introduced a new forex policy – managed floating rate

Sold $532m in the spot and $3.48bn in the forward market

10 Finally A Month of Inflection

CBN sacks board of Skye Bank on solvency concerns

Also showing zero tolerance for financial delinquency

Silverbird, R.T Briscoe, Jimoh Ibrahim and MRS petroleum on

AMCON hit list

NNPC gets a new board at last

Governance structure could slow the dynamism of the sole

administrator

Global & Regional Context

12 Global and Regional Context

U.S. economy grew at 1.1% in Q1’16

Slightly higher than 0.8%, the original estimate

Slowest pace in 12 months

Nearly all the 33 banks passed the Federal Reserve annual stress

test

The U.S. subsidiaries of Deutsche Bank and Santander had their

dividend and share buybacks plans rejected

13

Brexit – London is not the U.K.

The surprise outcome of the Brexit vote left global markets in turmoil

Wiping $3trn off global market valuations

British companies and investment trusts lost 14% in 3 days

Trading in Barclays and Royal Bank of Scotland shares were suspended

The Bank of England promised to pump $350bn into the financial

system

14

The market turbulence spread to Italy’s beleaguered banks

Bank of England relaxed capital requirements for banks

The next Monetary Policy Committee (MPC) meeting tomorrow

would move to ease rates and increase QE

The Chancellor also plans to cut corporate income tax to below

15%

Brexit – London is not the U.K.

15 Brexit - Implications

The Empire on which the Sun never sets – Christopher North 1829

The British Empire spanned the entire globe

The Empire is now where the sun hardly rises

Nigerian global diaspora remittances in 2014 approximately $22bn

Approx 33% from the U.K.

An 11% pound sterling fall equals $800m decline in remittances to

Nigeria

16

A shrinking U.K. economy means possible lay-offs for Nigerian

diaspora

British schools now cheaper for education

U.K. will become a more affordable destination for holidays, tourism

& medical services

Nigerian/British trade N2.3trn in 2015

Brexit - Implications

17 The African Entrepreneur

SSA’s number of small businesses is only 25%

of Asia’s, relative to its population –World Bank

Africa has produced just one of the world’s

169 “unicorns”: African Internet Group (AIG)

Label given to privately held tech start-ups

with a valuation of more than $1 billion

AIG adapts foreign business models such as e-

commerce and mobile cab-hailing to African

circumstances

18 The African Entrepreneur

Crowding out effect of the government continues to limit Africa’s

ability to produce profitable start-ups

Banks continue to channel savings to the government rather than

entrepreneurs

Treasury bills offer juicy rate of interest

Government borrowing pushing interest rates up

19

SSA - Economic Review

The African Union has announced a proposal for a “single African

Passport”

Proponents for this agenda argue that it would boost Africa’s

regional integration

The single passport would promote free movement of labor, capital,

goods and services

This proposal is set to materialize by 2018 to all AU citizens

Ghana has scrapped visa requirements for all African citizens

20

SSA - Economic Review

The World Bank has revised their growth estimates for SSA in

2016 to 2.5% in 2016 from 2015’s 3.0%

The downward revision of South Africa is weighing on the region’s

outlook

The economy contracted by 1.2% in Q1’16 from 0.6% in Q4’15

Nigeria Responds to Crisis and Stumbles into Reform

23

Act I Scene I - May 2016

Helpless Petroleum minister sees unending petrol queues

National security threatened by possible backlash and social chaos

Needs to act swiftly and wisely

Desperately meets with downstream players

Earlier attempts to get multinationals to fund local subsidiaries failed

24

Act I Scene I - May 2016

Ministers asks: what’s the Constraint????

Operators say: subsidy, delay and forex scarcity

Government offers: forex at N285/$ and PMS at N145

Bingo!!! queues disappear

Market in equilibrium

Operators dump import of diesel and kerosene

Price of diesel and kerosene up 100%

Free markets also create scarcity

25

Act I Scene 2 - May 2016

MPC meets against backdrop of NNPC determining a shadow

exchange rate

Lame duck MPC with the dog wagging the tail

Announces new forex policy with no guidelines

Market relieved, anything is better than nothing

Guidelines expected at the appropriate time, meaning??

Dual exchange rate muted knock wood

26

Act 1 Scene 3 - June 15

CBN releases guidelines

Surprise! Surprise!! single exchange rate

Barriers to entry, only a select club of primary dealers

The lobbying begins against a possible cabal

The big boys lobby for barriers

CBN is between a rock and a hard place

27

Act 2 Scene 1- June 20

June 20- markets open

All authorised dealers are allowed as primary dealers

Another blow to the allocation cabal

Spot market on 2-way quote basis

Starts tentatively at N253/$

Average rate rises to N280/$

28

Act 3 Scene 1 – CBN Shocks the Market

11 am – June 20

CBN calls for bids for 90-day forward to be paid spot

Bids to be in 2 hours, objective is to clear forex backlog

Investors, banks, airlines, manufacturers scratching their heads

Use it or loose it, market in confusion

CBN sells $3.48bn to be delivered September 23

29

Act 3 Scene 2

Market in shock, N1.1trn sucked out of the system

Naira money market in turbulence, rates rise to 12% p.a.

Almost every bank goes to the CBN discount window

Market in shock for one week

Digests the spot plus forward and is gasping for more dollars

30 Act 3 Scene 3

CBN resorts to aggressive moral suasion

Compelling the banks to sell within an artificial band of N280/$ -N285/$

Spot market becomes totally illiquid

Act 4 Scene 1 CBN abandons the rigid artificial band

Dealers allowed to trade naturally

31

Outlook for exchange rate

The naira is 6.51% overvalued, needs to depreciate to N300/$

Spot market is illiquid

Non-deliverable forwards of N292/$ is a joke

Moral suasion is a regulatory shake down

Fair value (sweet spot) is approximately N295-N310/$

Markets fear that Sept 23rd delivery of forwards may not happen

32

Policy Shift – Fiscal Policy

Increased capital spending in 2016 budget

Subsidy removal increases revenue to government by 21%

State bailouts now possibly over

Impact:

Higher official price for PMS – N145/litre

National average price has declined from N163/litre to N150

No more queues

Partial deregulation first step to fully competitive market

33

Market settles at N295/$ spot

Sets the stage for a more realistic forward market

The parallel market is now trading at N365/$ - N375/$

Will appreciate towards 340 in August

Policy Shift – Fiscal Policy

Leading, Coincidental & Lagging Indicators:

The New Normal

35

Leading Indicators

Indicator Direction Comment

Oil price

$47.81pb

•Average for the year: $45pb

•Possibly of a further decline subject to slowing Asian

demand and supply glut

Oil production

1.8mbpd

•Recovery subject to further attacks

•Passage PIB a possibility in H2’16

•MoU with China is a positive development

Market Cap

N9.9trn

•Corporate earnings expected to flat line in H2’16

•Full recovery expected in 2017

36

Leading Indicators

Indicator Direction Comment

CBN PMI

41.8

•Recovery expected in Q3’16

•Driven by fiscal stimulus & forex accessibility

FAAC

N305.12bn

•Naira depreciation implies more oil revenue in naira

•Savings on subsidy frees up government funds

37

Coincidental Indicators

Indicator Direction Comment

Exchange Rate

N282.12/$

•Sustainability of forward market dependent

on spot market liquidity

•Risk of policy reversal remote

•Subject to further decline in oil price and

production

Treasury Bills

9.99%

•Government spending to dampen rates

MPR

12%

•Monetary policy to skew towards growth

enhancement and currency stability

38

Lagging Indicators

Indicator Direction Comment

GDP

(-0.36)%

•To bottom out in Q3, gradual recovery expected

from Q4

•Not enough to negate contraction in H1

•Year-end growth projected to be negative

External

Reserves

$26.4bn

•Forward transaction of $3.4bn yet to be

deducted

•Reserve accretion subject to new dollar inflows

Vacancy

Factor

Commercial : 34%

Residential : 49%

•Lower disposable income and high rates to shrink

demand

•Government activity to increase supply in the

market

Stock Market

Irrational Exuberance vs False Expectations

41 Stock Market – Highlights

Global market shaken by the Brexit surprise

Wiping out over 1.28% of market

capitalization in the month of June

The Nigerian market had its own problems

Initial reaction to forex policy was a rally

(dead cat bounce)

International investors said not so fast

Market retreated into choppy waters Source: FDC Think Tank & NSE

26,000

28,000

30,000

32,000

NSEASI

42 How Corporates see the Policy Change

Forex market where the spot rate is closer to equilibrium

CBN more willing to fund market

CBN chooses growth ahead of inflation

No need to increase interest rates if forex rate does the mopping

up

Disposable income temporary

Shift in income to government as subsidies reduce

Removal of subsidy means availability of fuel and less time on

queues

Effective lower price of petrol

43 Implication on Corporates Earnings

Short-run higher costs

Lower margins and profitability

Most sectors to consolidate after a shake out

Critical success factors

Level of import content

Currency strength of exporting countries

Price elasticity of demand of the products manufactured

Ability of companies to extract cost efficiencies

Capacity to switch to local substitute

While keeping the average cost curve unchanged

44 Winners are Companies that have:

Tenacity to source raw materials from countries with weak

currencies

Argentina, South Africa, Brazil, U.K and China

Leverage on multinational parent to lock down volatile raw

materials in the futures market

Financial clout to pay lower finance costs

45 MTN Listing an Hail Mary Pass

The listing of MTN in 2017 could increase market capitalization by

50%

Bringing about sector diversity in the exchange

Force Etisalat, Airtel and Glo to follow suit

This is the tonic the Exchange has been waiting for

46

NSE-ASI July 2016 – Irrational Exuberance vs False Expectation

Stocks rebounded after a low of 22,456.32

points in January

Low oil prices, soft economic data,

currency conundrum had a significant

negative effect

Monetary policy action took center stage

in May/June thus bolstered investors

sentiment

Source: FDC Think Tank & NSE

21,000

23,000

25,000

27,000

29,000

31,000

33,000

NSEASI Performance YTD

Jan

-16.5%

Mar

2.99%

May

10.38%

Apr

-0.96%

Jun

6.99%

Feb

2.74%

Q1: -11.65% Q2: +16.96%

47

NSE-ASI July 2016 – Dead Cat Bounce

Stock advanced on the month of June by 6.99%

Pulling returns to positive territory of 3.34% (YTD)

Market upheaval over Brexit but was short-lived

Average turnover declined by 44.7% to N2.5bn from prior period

Market capitalization increased by 3.2% to N10.16trn from N9.85trn

for half-year

The average daily volume of trade increased by 20.33% to N496.2mn

from N412.3mn prior period

Average market PE ratio currently at 9.1x

48

Scott-Free Index

BC30 index gained 5.93% in June

The SFNG Blue-Chip 30 Index (USD) was down

25.30% while the SFNG Blue-Chip Index (EUR) was

down 25.19% for the month of June

Adoption of a floating exchange rate

attributable factor

30 day volatility of 40.61%

Sharpe ratio of 0.13x

1 year return of -17.54%

Trailing P/E 6.77x

Scott-Free BC 30

Sectors to Watch

FMCG

50 Sectors to Watch – FMCGs

Will consolidate into fewer players

Flour millers that can source raw materials globally

Reduce shipping costs by large volumes and presence across

ECOWAS

Switch packaging materials and miniaturise to gain share

Staying power to fight price wars

Companies to watch include Nestle, NB, Guinness, 7up

51

FMCGs

Companies will reduce logistics & distribution costs

Taking advantage of the General Electric (G.E.) railway concession:

Lagos to Kano

Sector average price earning ratio (P/E) now 9.1x

Sector profit margins still have room to withstand shocks

Will recover rapidly as stimulus package becomes impactful

Downstream Petroleum

53 Downstream Petroleum

Sector consolidating more rapidly than any other

Total subsidiary in Nigeria will leverage on the resources of a solid

parent into the market

Mobil will do same drawing on the clout of the Fairfax Virginia

headoffice

Oando, now acquired by Vitol and Helios, will be the most lethal

competitor

After it sorts out its liquidity concerns

54 Downstream Petroleum

The former subsidy kings and overnight sensations of 2013/14 are

now dead on arrival

AMCON is in no mood to piggy back anybody or tolerate free

loaders

FGN may privatise downstream infrastructure

Pipelines, depots and lubricant plants

The downstream giants will gobble limping competitors

Industry will be dominated by a maximum of 4 players in 2017

Banking

56

Banking – Further Consolidation

Soundness of the financial system called into question by recent

developments

Historically, banking system weaknesses follows 12-24 months after

every currency adjustment

Gross border risk crystallising into domestic systemic crisis

1996 NERFUND crisis and the failed Bank decree

After exchange rate declined from N22 to N88/$

57 Banking – Further Consolidation

Killing approx 20% of all banks

The 2008 devaluation from N118- N160

Led to banking sector distress

Compounded by margin loans

8 out of 21 banks kicked the bucket

CBN AMCON to the rescue

N620bn of tax payers money used for a bail out of the system

58

No depositor lost any money

Shareholders lost their shirts

Industry now set for more consolidation

Asset quality will deteriorate further

4% of NPLs are in power, 7% in public sector & 26% oil and gas

45% of loans are dollar denominated

Banking – Further Consolidation

59

Capital is in naira: huge potential translation losses

Will erode shareholders’ value

Banking sector earnings will decline in 2016/17 by no less than 30-

40%

Sector will still be profitable, will recover in 2017/18 period

Banking – Further Consolidation

Nigerian Banking Sector

NPLs expected to rise to 6% in 2016 from 5.5% in 2015 above the

prudential CBN ceiling of 5% (BofAML)

Data from Q1’16 results of the largest banks shows average NPLs of 7%

Recovery in oil prices will to some extent be offset by lower oil

production

Regulatory authority remains unflinched about the sector

60

Nigerian Banking Sector

Delayed July 1 date for compliance with the new minimum capital

adequacy ratio of 16% from 15% this year (plus a 1% capital surcharge for

systemically important banks)

CBN’s power sector intervention fund

N620 billion sector bailout in August 2009

61

Real Estate

Lagos Vacancy Up Again

64

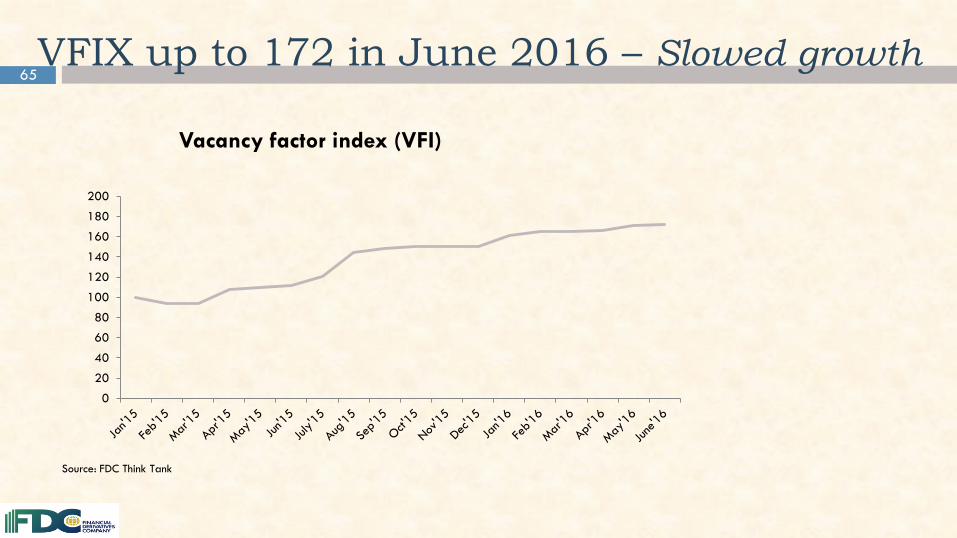

VFIX up to 172 in June 2016

The LVFIX increased marginally from 171 to 172 in May 2016

Reflects a slowed but continued deterioration in the real estate

market

Due to the lagging effect of the indicator

The number of vacant properties increased by 72% in 18 months

Base month is January 2015

Vacant properties higher in Lekki and Victoria Island

65 VFIX up to 172 in June 2016 – Slowed growth

0

20

40

60

80

100

120

140

160

180

200

Vacancy factor index (VFI)

Source: FDC Think Tank

66

VFIX Outlook

Housing market hit by economic realities

Increased supply of residential properties

Continued retrenchment increasing delinquency

High-end tenants in the oil and gas industry suffer the most

Overvalued properties are dampening demand further

Dollar denominated rents are most affected negatively

As the new forex market settles, housing demand will increase

Vacancy factor will decline in Q1 2017

67

VFIX up to 172 in June 2016

Month/Year VFIX Residential Index Commercial Index

January 2015 100 100 100

January 2016 160.2 169.2 148

March 2016 165.3 176.9 148

April 2016 165.9 180.8 143

May 2016 170.5 188.5 143

June 2016 172.2 188.5 148

Source: FDC Research

68

Outlook

No quick recovery

Effect of new policies will take some time before manifesting in

the industry

We expect market forces to shift rental prices downwards

As current rates are unsustainable in the long run

Airlines Hit By Forex Rates

70

The Aviation Problem

$700 million blocked funds

Only dollar tickets sold

Industry consolidation taking place

New normal: flexible exchange rate

Massive transaction losses

40% haircut equivalent to $280million

71

Aviation Update

International carriers had borne the brunt of the Nigerian forex

issue

Discontinued cheap fares and cut capacity

7% pulled out of the market

But it is not yet time for eureka

72

In the Global markets

Global airline share prices dropped by 11.6% in June

Year-to-date decline of over 21%

Affected by Brexit and ISIS

Oil price rebound eating into margins

Exchange rate adjustments not affecting demand

Fares are US dollar denominated

Share price of European stocks hit by downgrades to U.K. and EU

economies

73 Global Aviation

Traffic into the U.K. to increase

GBP at 35-year low

After terrorism, bankruptcies and consolidation

U.S. airlines face increasing demand

Now facing shortage of pilots

Airbus A380 faces an uncertain future

No US carrier has bought the aircraft

Airlines are shifting away from “superjumbos”

74

Who’s Buying the Biggest Planes?

75

Global Aviation

Global average yield has fallen by about 9% y-o-y

Due to current economic realities

Annual global traffic growth remained unchanged at 4.6%

Partly due to disruptions like the Brussels terrorist attack

Available seat kilometers grew by 5.5%

Annual growth of passenger capacity exceeded passenger traffic

Africa constitutes 2.2% of global aviation market

Up from 1.8% in 2014

76

Airlines Exit Nigeria

Sky team Star alliance One World Others

Existing Delta Airlines

Alitalia

KLM

Air France

Kenya Airways

China Southern Airlines

Virgin Atlantic Airways

Lufthansa

Ethiopian Airlines

Egypt Air

Turkish Airlines

South African

British Airways

US Airways

Qatar

Emirates

Exit

Total available seat

kilometers lost- 8958

United Airlines- 787-8

Flights per week- 7

No of seats per flight-

219

Seats per week -3066

Iberia-A319

Flights per week- 3

No of seats per flight-

156

Seats per week- 936

Emirates-Airbus 777-ER

Flights per week-7

No of seats per flight-

352

Seats per week- 4956

77 Nigerian Aviation - Regional and West Africa

Medview and Arik playing the price game

Quality not important

“Take your sleeping pills” before boarding

Risk of return flight cancellations

Kenya Airways expected to receive payment of outstanding fares

from Nigerian government within a month

78

Nigerian Aviation - After Forex Adjustment, What Next?

Medical tourism down by 40%

Shift from India to Israel and now U.K.

In search of quality and weak currencies

Education- UK vs. US vs. Canada and others

79 After Forex Adjustment What Next?

Trading will be directed towards regions with cheaper air fares

Professionals will most likely change routes and flights

Airlines that benefit from FOREX adjustment include Emirates,

Kenya Airways, and Qatar

80

Qatar Airways Group - Profits up in 2016

Qatar Airways group reported a net profit of $439m

Operating profits increased 172% in 2016 to $824m

Increased traffic following currency adjustment

The airline plans to launch 17 new destinations in 2016/2017 fiscal

year

81

Nigerian Aviation-International Network

Lagos airport receives newest aircraft in the world

Ethiopian airlines Airbus A-350

Due to its strategic position in Africa

NCAA deregulates airline tariffs

Urges domestic airlines to increase fares

Tariff composition will be appropriately filed with the authority

Foreign airlines still selling dollar tickets

Despite warnings from the NCAA

82

Outlook

Nigerian aviation will consolidate

Airports concessioning

Fares this summer will drop due to competition

Positive effects from new forex policy will take time to manifest

The Political Fallout

85 Political Push Back

The Nigerian political class is under pressure

Fallout from the anti-corruption war

And the demolition of the rent seeking structure

Party members are becoming impatient in waiting for handouts

The APC is under fire for waging a one-sided war against corruption

The war is only at federal government level a PDP government

Naturally only the PDP is affected

86

Political Push Back

No state government has been investigated

Nepotism and key appointments are raising eyebrows

Just like Jonathan favored South East and South South

No justification for lopsided appointments

The APC needs to address nationwide representation both in numbers

and effective control

To reduce concentration and dictatorial tendencies

87

Political Push Back

Niger Delta Avengers avenging nothing

The militancy has become a proxy war for the anti-corruption

drive

The militants are likely to splinter as the pressure increases

The solution is better intelligence and constructive engagement

Buhari will need to fight past and present corruption

88

Political Push Back

The country will be looking out to see how many people have

been fired and prosecuted for new corruption

The level of impunity is sharply lower than in the past

Edo State and Ondo State elections a litmus test for INEC

PDP squabbles undermining opposition capacity to fight

Outlook For July

91

Outlook for July

Inflation in July will increase marginally to 16.8%

Rate of change of inflation will slow to 0.3%

Stock market to remain choppy on poor corporate earnings

Naira will slip towards N310/$ in the interbank market

The parallel market will appreciate towards to N340/$

Airline load factors will increase in August, mainly in economy class

92

Outlook for July

MPC meeting will not change stance, monetary policy status quo

Waiting for a more sustainable inflation trend and forex market

stability

Banking sector systemic risks will dominate investor concerns

More appointments to Boards and agencies by Buhari

Investors will remain cautiously optimistic

93

Nigeria will start the international debt raising process

90-180days rates will spike closer to 14%

Housing vacancy factor to decline after forex market settles

The military will step up attacks on militants

Oil production will remain flat at 1.7mbpd

Outlook for July

94

Corporate Humour

The trouble with life in the fast

lane is that you get to the other

end in awful hurry – John Jensen

If you can see the light at the end of

the tunnel, you are looking the wrong

way – Barry Commoner

95 Corporate Humour

The entire economy of the

Western World is built on things

that cause cancer – The Movie

Bliss 1985

Muscles come and go but flab

stays

96 Corporate Humour

The lovely thing about being forty

is that you appreciate twenty five

year old men more – Colleen

Mccullough

Hard work never killed anybody

who supervised it – Harry Bomer

97 Corporate Humour

My problem is reconciling

my gross habits with my net

income – Errol Flynn

A lawyer with a brief case can

steal more than a thousand men

with guns – Mario Puzo

98 Corporate Humour

Gambling is getting nothing for

something – Wilson Mizner

Riches don’t make a man richer,

only busier – Conquest of

Paradise

99 Corporate Humour

On wall street enough is never

enough – Alison Cowan

There was a time when only a

fool and his money were soon

parted, but now it happens to

everybody – Adlai Stevenson

100 Corporate Humour

Economic forecasters exist to make

astrologers look good – Robert Reich

Bismarck J. Rewane, MD/CEO Financial Derivatives Company Ltd.

Lagos, Nigeria 01-7739889

© 2016. “This publication is for private circulation only. Any other use or publication without the prior express consent of Financial Derivatives Company Limited is prohibited.”