leverage to the gold price - · pdf fileleverage to the gold price tommy mckeith paydirt...

TRANSCRIPT

LEVERAGE TO THEGOLD PRICE

Tommy McKeithPaydirt Conference – Perth15 March 2010

2

Forward Looking StatementsINTRODUCTION

Certain statements in this document constitute “forward looking statements” within the meaning ofSection 27A of the US Securities Act of 1933 and Section 21E of the US Securities Exchange Act of1934.

Such forward looking statements involve known and unknown risks, uncertainties and otherimportant factors that could cause the actual results, performance or achievements of the companyto be materially different from the future results, performance or achievements expressed or impliedby such forward looking statements. Such risks, uncertainties and other important factors includeamong others: economic, business and political conditions in South Africa, Ghana, Australia, Peruand elsewhere; the ability to achieve anticipated efficiencies and other cost savings in connectionwith past and future acquisitions, exploration and development activities; decreases in the marketprice of gold and/or copper; hazards associated with underground and surface gold mining; labourdisruptions; availability terms and deployment of capital or credit; changes in governmentregulations, particularly environmental regulations; and new legislation affecting mining andmineral rights; changes in exchange rates; currency devaluations; inflation and other macro-economic factors, industrial action, temporary stoppages of mines for safety reasons; and theimpact of the AIDS crisis in South Africa. These forward looking statements speak only as of thedate of this document.

The company undertakes no obligation to update publicly or release any revisions to these forwardlooking statements to reflect events or circumstances after the date of this document or to reflectthe occurrence of unanticipated events.

Certain statements in this document constitute “forward looking statements” within the meaning ofSection 27A of the US Securities Act of 1933 and Section 21E of the US Securities Exchange Act of1934.

Such forward looking statements involve known and unknown risks, uncertainties and otherimportant factors that could cause the actual results, performance or achievements of the companyto be materially different from the future results, performance or achievements expressed or impliedby such forward looking statements. Such risks, uncertainties and other important factors includeamong others: economic, business and political conditions in South Africa, Ghana, Australia, Peruand elsewhere; the ability to achieve anticipated efficiencies and other cost savings in connectionwith past and future acquisitions, exploration and development activities; decreases in the marketprice of gold and/or copper; hazards associated with underground and surface gold mining; labourdisruptions; availability terms and deployment of capital or credit; changes in governmentregulations, particularly environmental regulations; and new legislation affecting mining andmineral rights; changes in exchange rates; currency devaluations; inflation and other macro-economic factors, industrial action, temporary stoppages of mines for safety reasons; and theimpact of the AIDS crisis in South Africa. These forward looking statements speak only as of thedate of this document.

The company undertakes no obligation to update publicly or release any revisions to these forwardlooking statements to reflect events or circumstances after the date of this document or to reflectthe occurrence of unanticipated events.

p

3

Our value propositionINTRODUCTION

Rapidly developing exploration portfolio

Growth opportunities at operations

Rising production outlook

81Moz of reserves

No hedging

Gold Fields - Leverage to the gold price

4

Our value propositionINTRODUCTION

0

2

4

6

8

10

12

14

16

18

AU ABX NEM GFI

2009 Trailing EV / EBITDA

Source: BMO Nesbitt Burns

5

Our strategyINTRODUCTION

Growth on a per share basis - no M&A heroics

South America~1Moz

South Africa~2.2 to ~2.5Moz

West Africa~1Moz

Australasia~1Moz

International Diversification5-year target

Deliver consistency

Grow existing assets

Exploration success

58%42%

F2010 Production Split*

South AfricaInternational

40%60%

Production Split Target – 5 Years

South AfricaInternational

* F2010 YTD annualised

6

Total Cash Costs

740

760

780

800

820

840

860

880

900

920

-100200300400500600700800900

1,000 1,100 1,200

Q1

F200

9

Q2

F200

9

Q3

F200

9

Q4

F200

9

Q1

F201

0

Q2

F201

0

Production Gold price Cash costs NCE

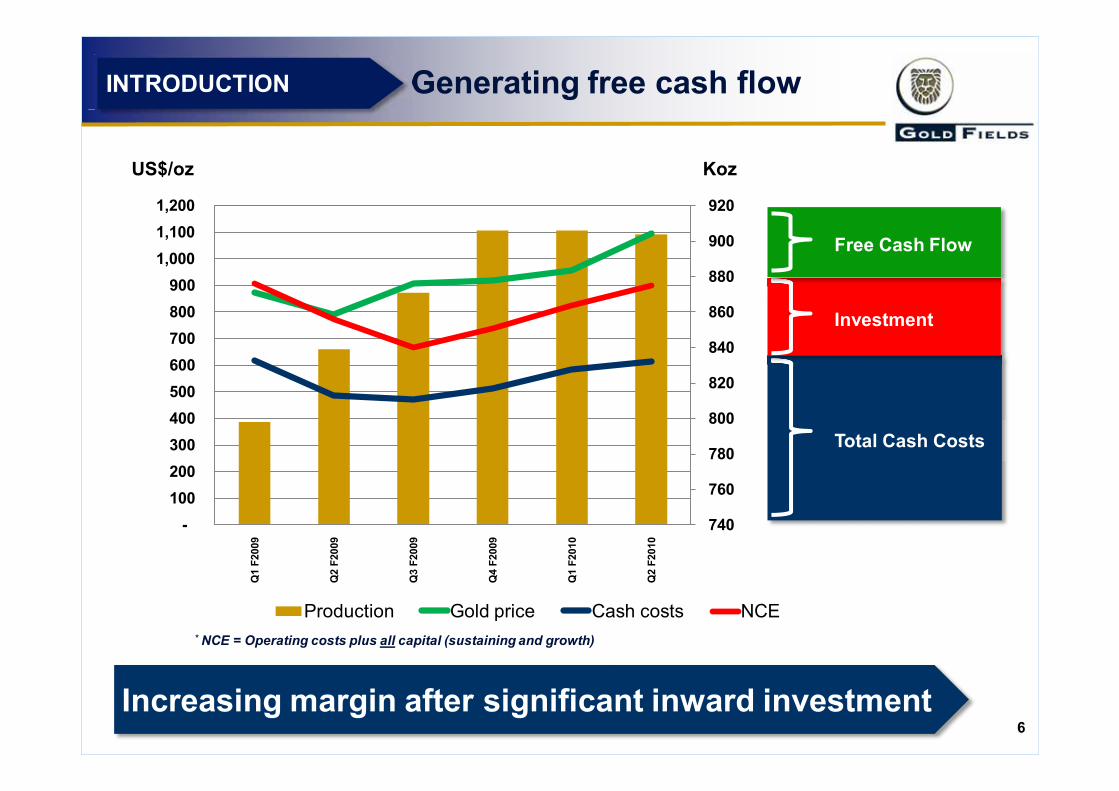

Generating free cash flowINTRODUCTION

163

* NCE = Operating costs plus all capital (sustaining and growth)

Increasing margin after significant inward investment

Koz

33Investment

33

Free Cash Flow

US$/oz

7

Leverage to the gold priceINTRODUCTION

20

112

163

* NCE = Operating costs plus all capital (sustaining and growth)

Gold price up 14% delivers operating profit up 30%

Gold production Steady at 900koz

Gold price Up 14% to US$1,096/oz

Total cash cost Up 5% to US$613/oz

NCE Up 3% to US$900/oz

Operating profit Up 30% to US$463 million

Operating margin Up 13% to 43%

Net earnings Up 45% to US$187 million

*Changes relative to Q1 F2010 Results

8

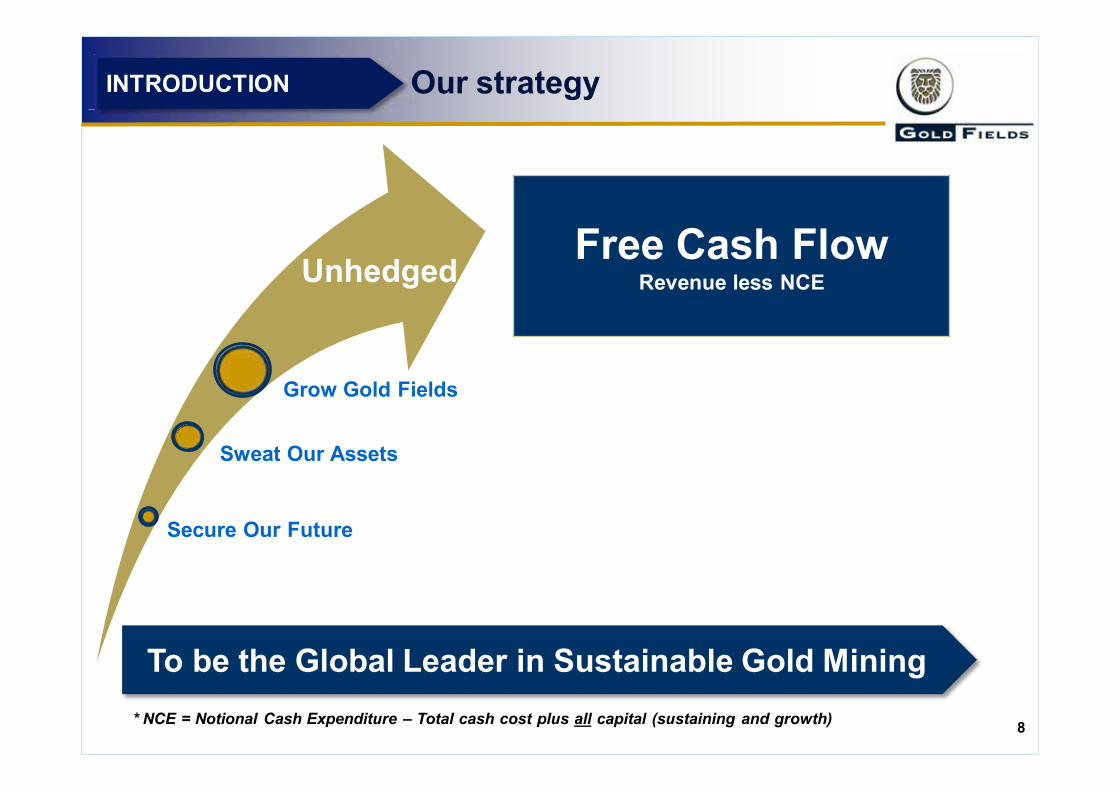

Our strategyINTRODUCTION

To be the Global Leader in Sustainable Gold Mining

Free Cash FlowRevenue less NCE

Sweat Our Assets

Grow Gold Fields

Secure Our Future

* NCE = Notional Cash Expenditure – Total cash cost plus all capital (sustaining and growth)

Unhedged

9

• Sweating our assets• South Deep developing a world class mine

• St Ives exploring a world class camp

• Agnew delivering continuously

• Growing Gold Fields• Chucapaca discovering a mine in Peru

• Yanfolila exploring an emerging camp in Mali

Presentation focusINTRODUCTION

To be the Global Leader in Sustainable Gold Mining

10

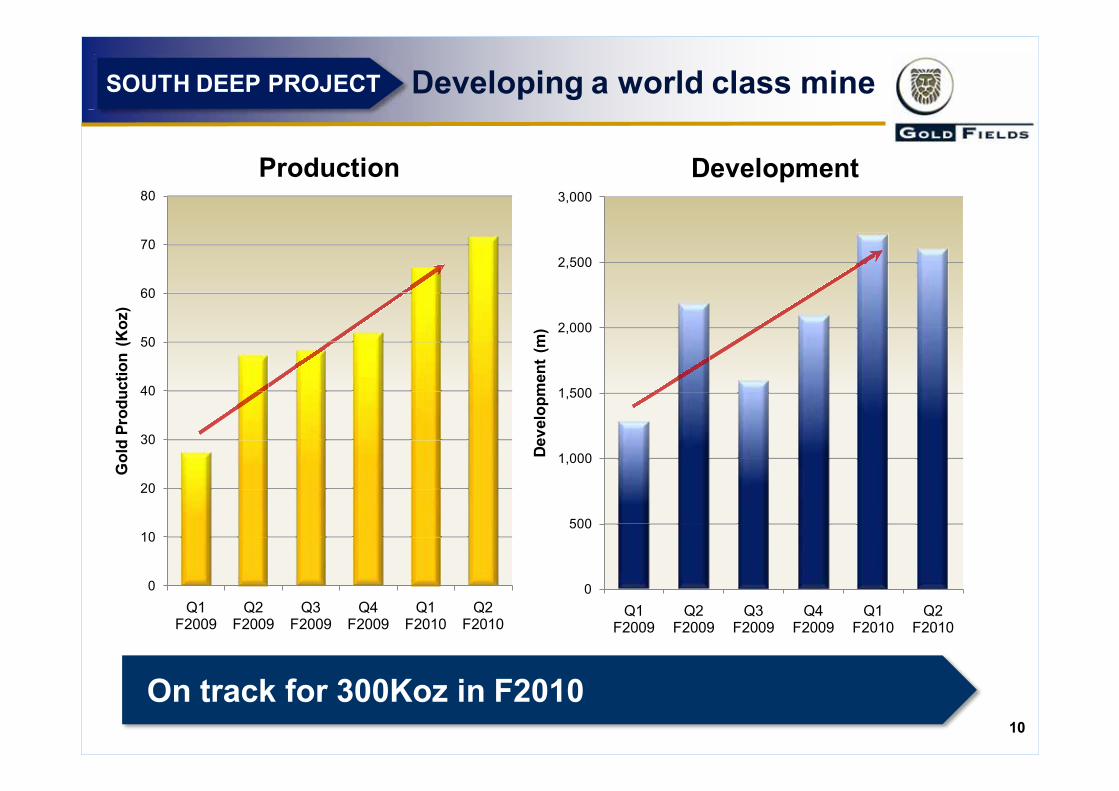

Developing a world class mineSOUTH DEEP PROJECT

20

112

163

20

112

163

196

0

500

1,000

1,500

2,000

2,500

3,000

Q1 F2009

Q2 F2009

Q3 F2009

Q4 F2009

Q1 F2010

Q2 F2010

Dev

elop

men

t (m

)

0

10

20

30

40

50

60

70

80

Q1 F2009

Q2 F2009

Q3 F2009

Q4 F2009

Q1 F2010

Q2 F2010

Gol

d Pr

oduc

tion

(Koz

)

On track for 300Koz in F2010

Production Development

11

SOUTH DEEP PROJECT

20

112

163

20

112

163

196111111116

1999999999666666661111111111111111

50 Lvl

70 Lvl

71 Lvl

78 Lvl

90 Lvl

95 Lvl

100 Lvl105 Lvl

110 Lvl

Colour Coding: Red Up Cast.GreenDown CastGold Rock Handling Capacity

Rock Capacity 120ktpm Rock Capacity 175ktpmRock Capacity 195ktpm

SV 1

South Shaft

SV 3

Twins Ventilation Shaft

TwinsMain Shaft

Metallurgical Plant

SV 2

Deepened Section 110a Pump

1.4km

Initial mining to focus on 78 Level – east

Shaft Complex

51 Lvl

84 Lvl

90 Lvl

95 Lvl

20

112

50 Lvl0 Lvl

70 Lvl

71 Lvl

90 Lvl

95 Lvl

Rock Capacity 120ktpmmm

SV 1

South Shaft

SV 3SV 2

20Initial mining to

focus on 78 2020Level 22Leve22Level 2020– east 00east0eastShaft Complex

77787787888777878787887877877787878787778 7878788 LL lLLLLLL llL lLLvlL lLvlLvlLvlvlLvlLvLLvlL

70

Will increase base case hoisting capacity from 330 to 450Ktpm

Developing a world class mine

Refurbishing south shaft creating additional upside

12

ItemYear

F2010 F2011 F2012 F2013 F2014

94 Level Refrigeration Plant No 2

Twin Vent Shaft (for rock hoisting)

Tailings Storage Facility

Plant Expansion to 330ktpm or above

New Mine DevelopmentPhase 1

Total Capital (Allprojects) R1,770M R1,875M R2,079M R1,484M R1,198M

SOUTH DEEP PROJECT

Note: Capital estimates in July 2009 money

Capital programme on track

Developing a world class mine

13

SOUTH DEEP PROJECT

Notes: Excludes VCRFurther optimisation in progressExchange rate R7.50 : US$1.00

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

100

200

300

400

500

600

700

800

900

F2010 F2011 F2012 F2013 F2014 F2015 F2016

Gold Production (koz) Operating Costs (US$/oz) NCE (US$/oz

Koz US$/oz

Developing a world class mine

Building up to +750Kozpa in F2015

14

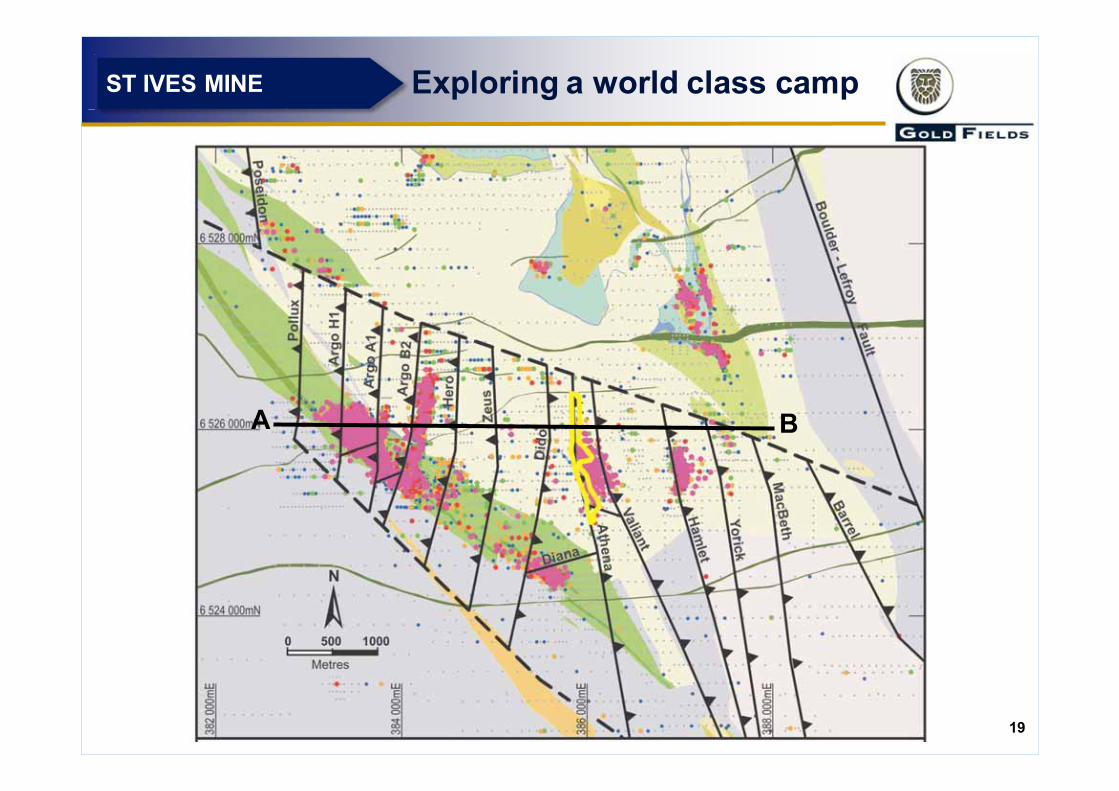

Exploring a world class campST IVES MINE

Gold first discovered at Red Hill 1897, mined to 1930’s

15

Re-started in 1980

10Moz production milestone in December 2009

Exploring a world class campST IVES MINE

16

Exploring a world class campST IVES MINE

-500

1,000 1,500 2,000 2,500 3,000 3,500 4,000

Vict

ory

Are

a

Rev

enge

Are

a

Junc

tion

Arg

o-A

then

a A

rea

Intr

epid

e A

rea

Orc

hin

Are

a

Sant

a A

na A

rea

Cav

e R

ocks

Nel

sons

Fle

et A

rea

Kam

bald

a D

ome

Clif

ton

Are

a

Oth

er

WMC Production GFA Production Reserve 09

• Multiple ore sources

• Lefroy Mill 4.2Mtpa – 2004

• Four +2Moz sources

Endowment ‘000s oz

17

Exploring a world class campST IVES MINE

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

0.0

2.0

4.0

6.0

8.0

10.0

12.0

F198

0F1

981

F198

2F1

983

F198

4F1

985

F198

6F1

987

F198

8F1

989

F199

0F1

991

F199

2F1

993

F199

4F1

995

F199

6F1

997

F199

8F1

999

F200

0F2

001

F200

2F2

003

F200

4F2

005

F200

6F2

007

F200

8F2

009

F201

0

Gra

de (g

/t)

Oun

ces

Prod

uced

(mill

ions

)

WMC Ounces GFA Ounces Cumulative Grade

WMC5.6Mozin 21 years

Gold Fields4.5Mozin 9 years

18

• June 2009• Reserves 2.3Moz

• Resources 5.6Moz

• New discoveries• Athena, Hamlet, Yorrick

etc.

• Significant impact

• Potential to increase life and throughput

Exploring a world class campST IVES MINE

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Rev

enge

Are

a

Arg

o-A

then

a A

rea

Vict

ory

Are

a

Junc

tion

Cav

e R

ocks

Sant

a A

na A

rea

Intr

epid

e A

rea

Orc

hin

Are

a

Nel

sons

Fle

et A

rea

Oth

er

Endo

wm

ent

‘000

s oz

Initial Reserve GFA Production to June 2009 June 2009 Reserve

Gold Fields added 3.65Moz reserves since purchase

19

Exploring a world class campST IVES MINE

A B

20

Exploring a world class campST IVES MINE

750mA B

Argo1Moz produced889Koz Resource

Athena771Koz Resource

Hamlet251Koz Resource

June 2009 endowment 2.9Moz ~120km drilled

21

Exploring a world class campST IVES MINE

First gold from underground by December 2010

-300m

0m

309mNorthSouth

500m

ParingaBasalt

AthenaBasalt

South Shoot2-3m wide

8-20g/t

Central Shoot5-12m wide

5-12g/t

North Shoot3-7m wide

3-9g/t

OxideLake Sediment

Athena LongSection

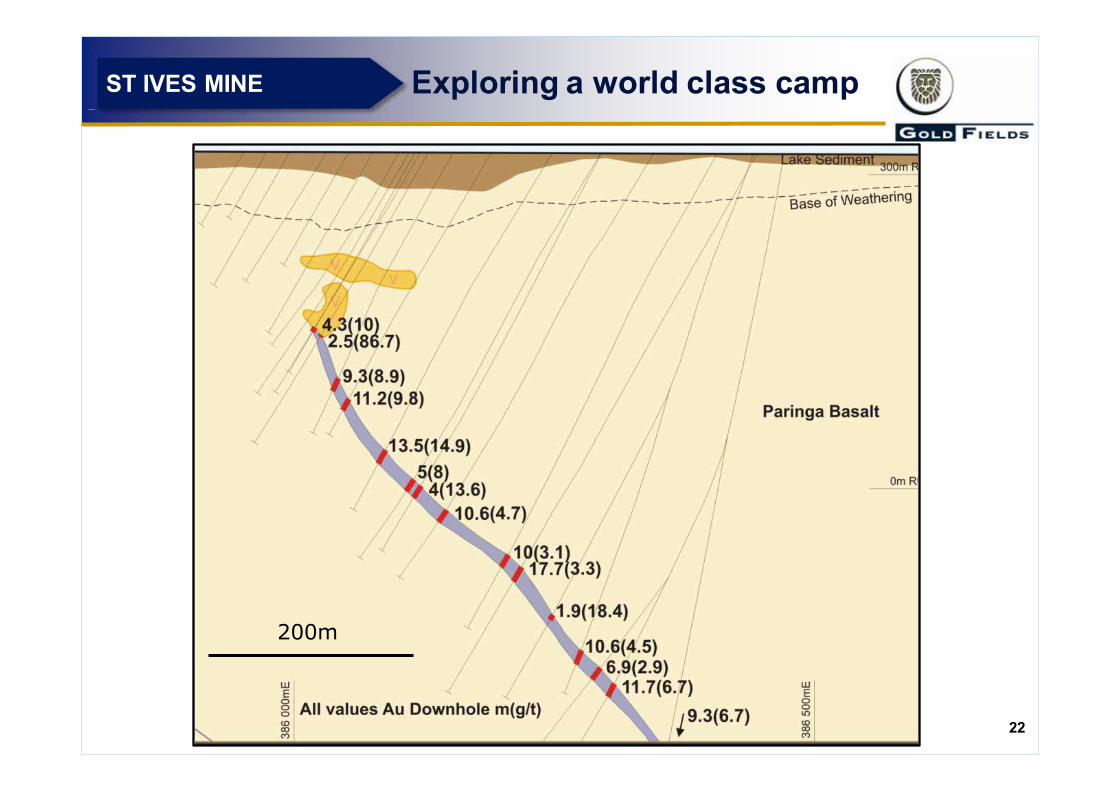

22

Exploring a world class campST IVES MINE

200m

23

Delivering continuouslyAGNEW MINE

163196

20

112

20

112

163

-1400m

-1000m

-850m

Kim S Extension Project

Existing Reserve/Resource

-1850m

Projected Intersection of Kim Lode with Barrick Tenement

Kim Lode 4m @ > 5g/t

DrillholeCompleted

DrillholePlanned

Projected Kim LodeExtension

Current Development Level

Zone with Bulk Mining Potential

North South

Deep surface drilling1,400m below surface at Kim

Drill Main at depth

Targeting 1Moz reserve

24

Discovering a mine in PeruCHUCAPACA PROJECT

163196

Chucapaca

CHUCAPACA

Gold Fields - 94,100Ha

Buenaventura – 18,400Ha

Aruntani

Canteras del Hallazgo – 12,700HaMINING CONCESSIONS

Dirt Road

Back Road

Main Road

!

SYMBOLOGY

CHCHCHCHCHCHCHUCUCUCUCUCUCUCAPAPAPAPAPAPAPACACACACACACACAAAAAAAChucapaca

Cerro Corona

Gold Fields 51% (operator) and Buenaventura 49%

25

Discovering a mine in PeruCHUCAPACA PROJECT

163196

20

112

20

112

163

222222

1111166

GF

BVN

Canahuire

KatrinaKatrina

Katrina South

Cerro Chucapaca

CanahuireFirst resource June 2010~1km strike definedOpen to the west and at depthRobust mineralisation

SatellitesInitial drilling March 2010Community access agreement

Interim Scoping StudyJune 2010Canahuire only

26

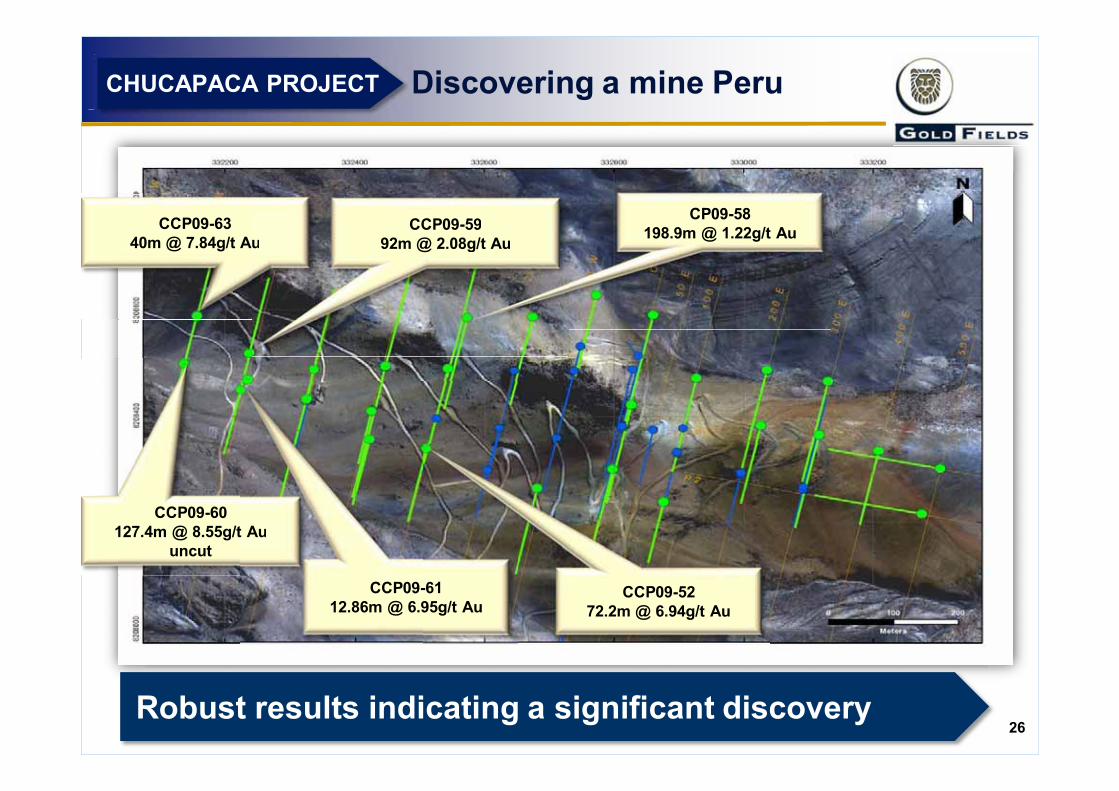

Discovering a mine PeruCHUCAPACA PROJECT

20

112

163

20

112

163

196

CCP09-60127.4m @ 8.55g/t Au

uncut

CCP09-6340m @ 7.84g/t Au

CCP09-5272.2m @ 6.94g/t Au

t Au

CCP09-6112.86m @ 6.95g/t Au

uCCP09-59

92m @ 2.08g/t Au59g/t Au

CP09-58198.9m @ 1.22g/t Au

Robust results indicating a significant discovery

27

Exploring an emerging campYANFOLILA PROJECT

20

112

163

20

112

163

196

Loulo

Morila

SyamaSiguiri

YANFOLILA SadiolaEssakane

Endowed Siguri Basin - concealed by shallow cover

Mali

28

Exploring an emerging campYANFOLILA PROJECT

112

163163

196

20

20

112

Komana

Kobada

Bagama Bokoro

Glencar acquisition successfully concluded

Consolidation of extensive ground holding

Komana framework drilling progressing rapidly

Initial drill testing completed over Bokoro target

Re-stated Komana resource June 2010

29

Rising production trend

Significant leverage to the gold price

Strong balance sheet

South Deep gaining momentum

Growth opportunities at operations

Developing exploration portfolio29

CONCLUSIONS

LEVERAGE TO THE GOLD PRICE

ENQUIRIES:Willie [email protected]: +1 508 839 1188Mobile: +1 857 241 7127www.goldfields.coza