llp are you on the for a fasb standard

TRANSCRIPT

6/5/2019

1

©2018 CliftonLarsonAllen LLP

Financial: Are you on the Right Track? Brake for a FASB Standard Update

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

©2018 CliftonLarsonAllen LLP

Agenda

• Presentation of Financial Statements

• Expense Reporting and Allocations

• Liquidity Disclosures

• Revenue Recognition • Grants and Contracts

Create Opportunities 2

• Lease Standard

6/5/2019

2

©2018 CliftonLarsonAllen LLP

Learning Objectives

• Recognize how your organization’s financialstatements will changestatements will change

• Review the new liquidity disclosures

• Discuss expense allocation methodologies

• Discuss the impact of revenue recognitionchanges on nonprofit organizations starting in2019

Create Opportunities

2019

• Review the upcoming lease standard

3

©2018 CliftonLarsonAllen LLP

ASU 2016‐14Presentation of Financial Statements of Not‐for‐Profit Entities

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

6/5/2019

3

©2018 CliftonLarsonAllen LLP

Key Areas Affected

Net Assets Classes

Key Changes in ASU

2016-14

Classes

Liquidity & Availability

Statement of Cash Flows

Create Opportunities

Not‐for‐Profit Section

5

Expense Reporting

Investment Return

©2018 CliftonLarsonAllen LLP

Net Assets

Create Opportunities 6

6/5/2019

4

©2018 CliftonLarsonAllen LLP

Balance Sheet Presentation

Create Opportunities 7

©2018 CliftonLarsonAllen LLP

Board‐Designated Net Assets Presentation

May disclose on the face of the statement of financial position or in the notes

Could present in narrative or tab lar form

Net Assets Without donor restrictions

Undesignated 3,057,607 Designated by the Board for operating reserve 300,000 Designated by the Board for endowment 15,511,186 Invested in property and equipment, net of related debt 21,150,885

40,019,678

Create Opportunities

tabular form in the note.

8

6/5/2019

5

©2018 CliftonLarsonAllen LLP

Adjustments Upon Adoption

Without Donor Restrictions• Reclassify “unrestricted net assets” to “net assets without donor

restrictions”

• Reclassify any “temporarily restricted net assets” related to implied restrictions on contributions restricted for acquisition or construction of PP&E to “net assets without donor restrictions” (to adopt placed‐in service approach)

With Donor Restrictions• Reclassify “temporarily restricted” and “permanently restricted net

Create Opportunities

• Reclassify temporarily restricted and permanently restricted net assets” to “net assets with donor restrictions”

• Reclassify any “unrestricted net assets” related to underwater endowments to “net assets with donor restrictions”

9

©2018 CliftonLarsonAllen LLP

Net Asset Conversion Activity (Handout)

Instructions:

Using the Current GAAP (with Detail) section, convert the net assets to the new presentation under FASB 2016‐14.

1. Convert the Statement of Financial Position from Unrestricted, Temporarily Restricted and Permanently Restricted to Without Donor Restrictions and With

Create Opportunities

Donor Restrictions.2. Complete the Footnote for Net Assets with Donor

Restrictions.

10

6/5/2019

6

©2018 CliftonLarsonAllen LLP

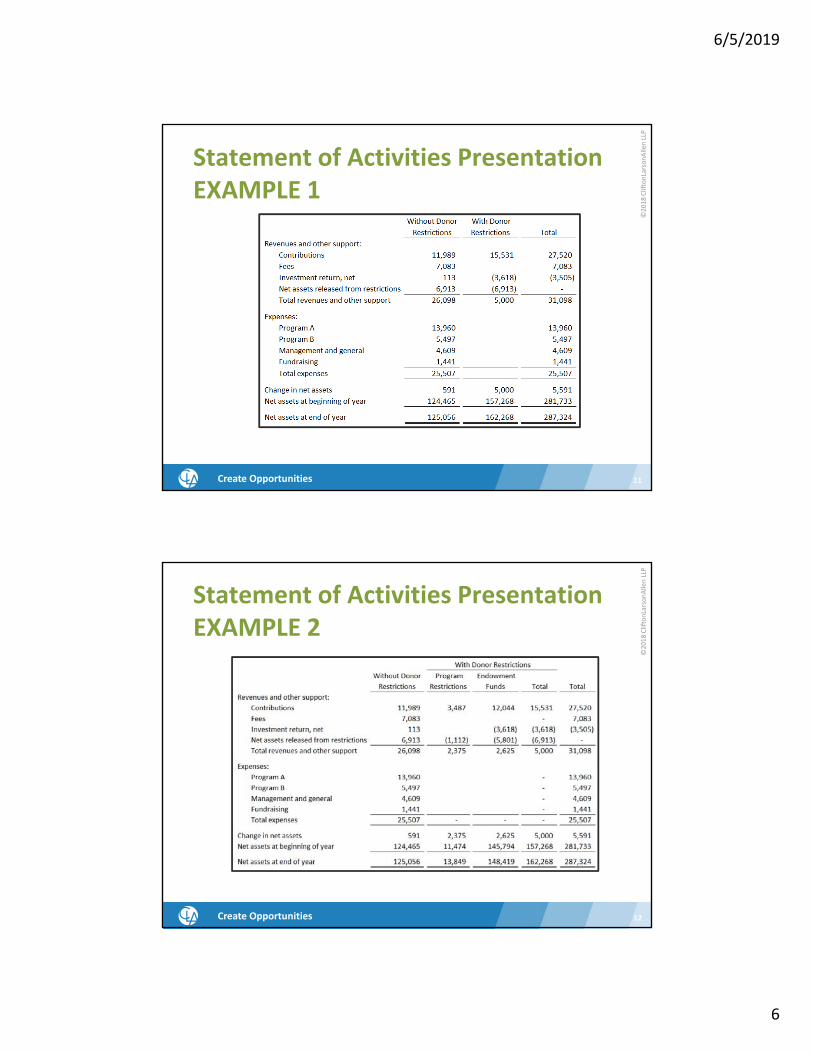

Statement of Activities Presentation EXAMPLE 1

Create Opportunities 11

©2018 CliftonLarsonAllen LLP

Statement of Activities PresentationEXAMPLE 2

Create Opportunities 12

6/5/2019

7

©2018 CliftonLarsonAllen LLP

Operating Measure Considerations

Create Opportunities 13

©2018 CliftonLarsonAllen LLP

Reporting of Investment Return

Create Opportunities 14

6/5/2019

8

©2018 CliftonLarsonAllen LLP

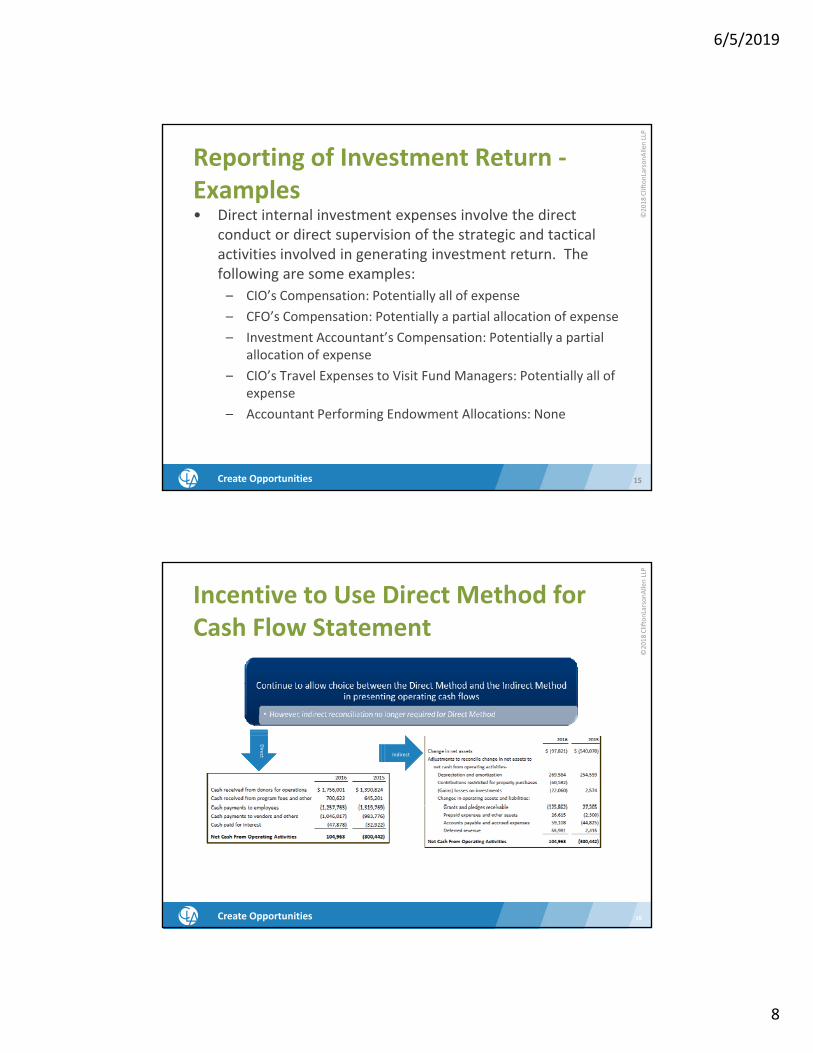

Reporting of Investment Return ‐Examples• Direct internal investment expenses involve the direct

conduct or direct supervision of the strategic and tactical activities involved in generating investment return. The following are some examples:

– CIO’s Compensation: Potentially all of expense– CFO’s Compensation: Potentially a partial allocation of expense– Investment Accountant’s Compensation: Potentially a partial

allocation of expense

Create Opportunities

– CIO’s Travel Expenses to Visit Fund Managers: Potentially all of expense

– Accountant Performing Endowment Allocations: None

15

©2018 CliftonLarsonAllen LLP

Incentive to Use Direct Method for Cash Flow Statement

Direct Indirect

Create Opportunities 16

6/5/2019

9

©2018 CliftonLarsonAllen LLP

ASU 2016‐14Expense Reporting

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

©2018 CliftonLarsonAllen LLP

Expense Reporting

Report expenses by function and nature in one place

Where to Report?

Statement of Functional Expenses

Statement of Activities

Notes to Financial Statements

Do not report as supplementary information

Create Opportunities 18

information

Describe allocation methods used

6/5/2019

10

©2018 CliftonLarsonAllen LLP

Expense Reporting (cont’d.)

Create Opportunities 19

©2018 CliftonLarsonAllen LLP

Example 1Analysis of ExpensesPresentation in the notes or a separate statement

Create Opportunities 20

6/5/2019

11

©2018 CliftonLarsonAllen LLP

Example 2Analysis of ExpensesPresentation on the face of the statement of activities

Create Opportunities 21

©2018 CliftonLarsonAllen LLP

What are Program Service Expenses?

Per 958‐720‐45‐3:

Program services are the activities that result in goods and services being distributed to beneficiaries, customers, or members that fulfill the purposes or mission for which the NFP exists. Those services are the major purpose for and the major output of the NFP and often relate to

Create Opportunities

several major programs.

22

6/5/2019

12

©2018 CliftonLarsonAllen LLP

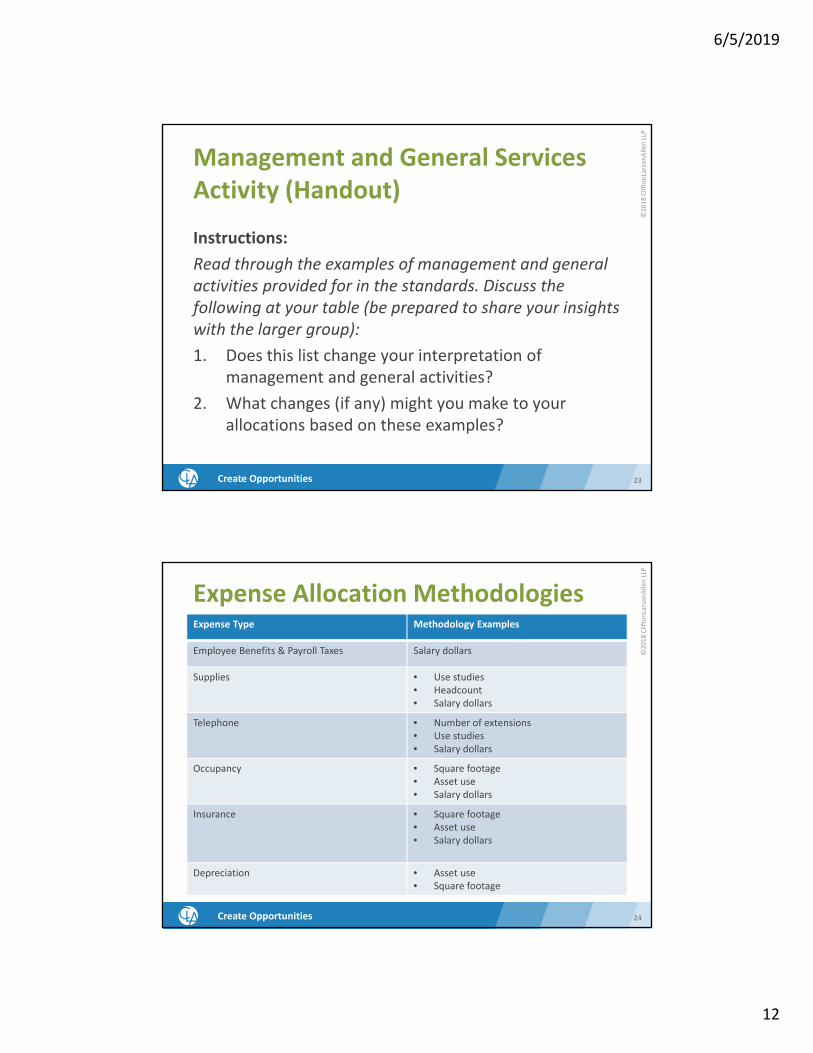

Management and General Services Activity (Handout)

Instructions:

Read through the examples of management and general activities provided for in the standards. Discuss the following at your table (be prepared to share your insights with the larger group):

1. Does this list change your interpretation of

Create Opportunities

management and general activities?2. What changes (if any) might you make to your

allocations based on these examples?

23

©2018 CliftonLarsonAllen LLP

Expense Allocation MethodologiesExpense Type Methodology Examples

Employee Benefits & Payroll Taxes Salary dollars

Supplies • Use studies• Headcount• Salary dollars

Telephone • Number of extensions• Use studies• Salary dollars

Occupancy • Square footage• Asset use• Salary dollars

Create Opportunities

Insurance • Square footage• Asset use• Salary dollars

Depreciation • Asset use • Square footage

24

6/5/2019

13

©2018 CliftonLarsonAllen LLP

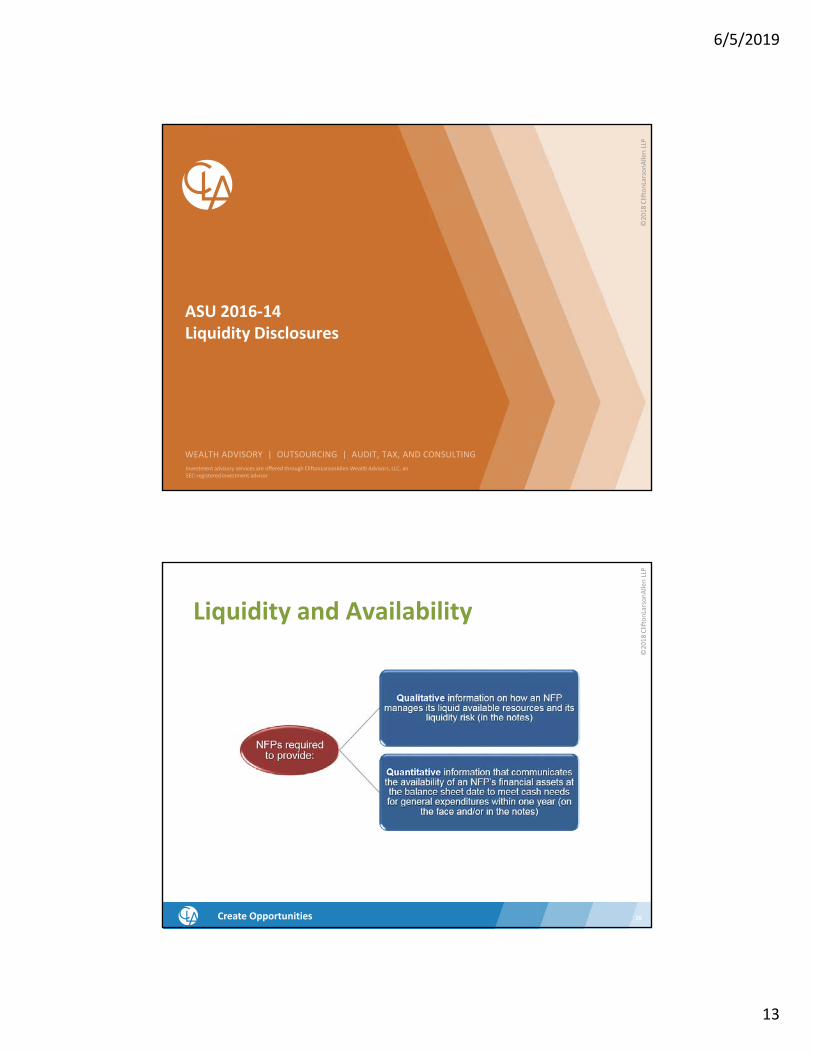

ASU 2016‐14Liquidity Disclosures

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

©2018 CliftonLarsonAllen LLP

Liquidity and Availability

Create Opportunities 26

6/5/2019

14

©2018 CliftonLarsonAllen LLP

Liquidity Disclosure Activity (Handout)

Instructions:

Read your assigned example disclosure(s). Discuss the following at your table (be prepared to share your insights with the larger group):

1. What do you like about the example(s)?

2. What do you dislike about the example(s)?

Create Opportunities

3. Would this/these example(s) meet the needs of your financial statement readers? Why or why not?

27

©2018 CliftonLarsonAllen LLP

ASU 2014‐09Revenue Recognition

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

(And Amendments: 2016‐08, 2016‐10, 2016‐12, 2016‐20, 2017‐05)

6/5/2019

15

©2018 CliftonLarsonAllen LLP

Final U.S. GAAP Model for Revenue Recognition

Core Principle:

Steps to apply the core principle:5 Recognize

Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services

Create Opportunities

1. Identify the contract(s) with the customer

2. Identify the performance obligations

3. Determine the transaction price

5. Recognize revenue when (or as) a performance obligation is satisfied

4. Allocate the transaction price

29

©2018 CliftonLarsonAllen LLP

Major Changes Relative to Current Guidance• Focus is now on the contract rather than on transactions of

certain types or within certain industries• Variable consideration and constraints on revenue• Licenses

• Recognition and measurement guidance applies to transfers and sales of nonfinancial assets to non‐customers (Topic 610)

• Guidance on accounting for costs to obtain and fulfill a

Create Opportunities

• Guidance on accounting for costs to obtain and fulfill a contract with a customer, if not addressed in other topics (Subtopic 340‐40)

• Disclosures 30

6/5/2019

16

©2018 CliftonLarsonAllen LLP

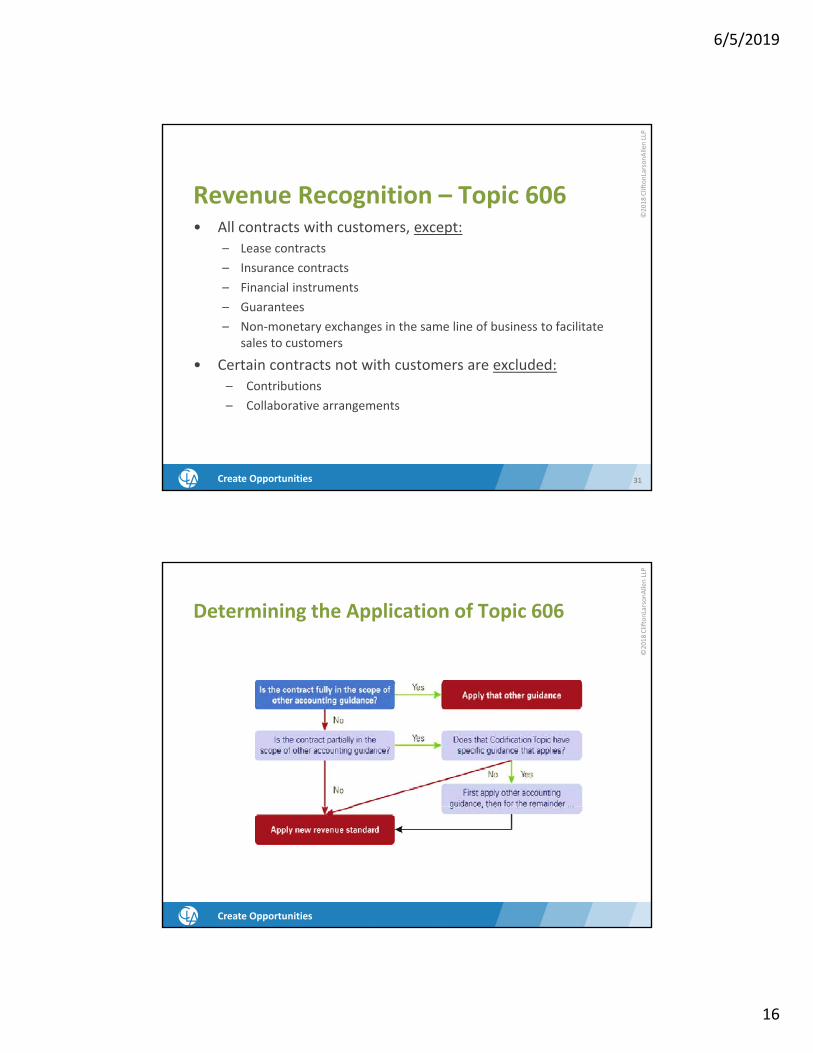

Revenue Recognition – Topic 606• All contracts with customers, except:

Lease contracts– Lease contracts– Insurance contracts– Financial instruments

– Guarantees

– Non‐monetary exchanges in the same line of business to facilitate sales to customers

• Certain contracts not with customers are excluded:

Create Opportunities 31

Certain contracts not with customers are excluded:– Contributions

– Collaborative arrangements

©2018 CliftonLarsonAllen LLP

Determining the Application of Topic 606

Create Opportunities

32

6/5/2019

17

©2018 CliftonLarsonAllen LLP

• Qualitative and quantitative* disaggregation of revenue into t i th t d i t h d h flDi ti f

Disclosure

categories that depict how revenue and cash flows are affected by economic factors

Remaining performance obligations

Information about contract balances

Q i i di l *

• Opening and closing balances *• Amount of revenue recognized from contract liabilities * • Explanation of significant changes in contract balances *

• Transaction price allocated to remaining performance obligations *• Quantitative or qualitative explanation of when amounts will be recognized as revenue *

Disaggregation of revenue

Create Opportunities

Interim requirements • Quantitative disclosures *

* for public entities only, including conduit debt obligors

33

©2018 CliftonLarsonAllen LLP

Rev. Rec. – Some Areas of Focus for NFPs as Discussed by AICPA Task Forces

Create Opportunities

6/5/2019

18

©2018 CliftonLarsonAllen LLP

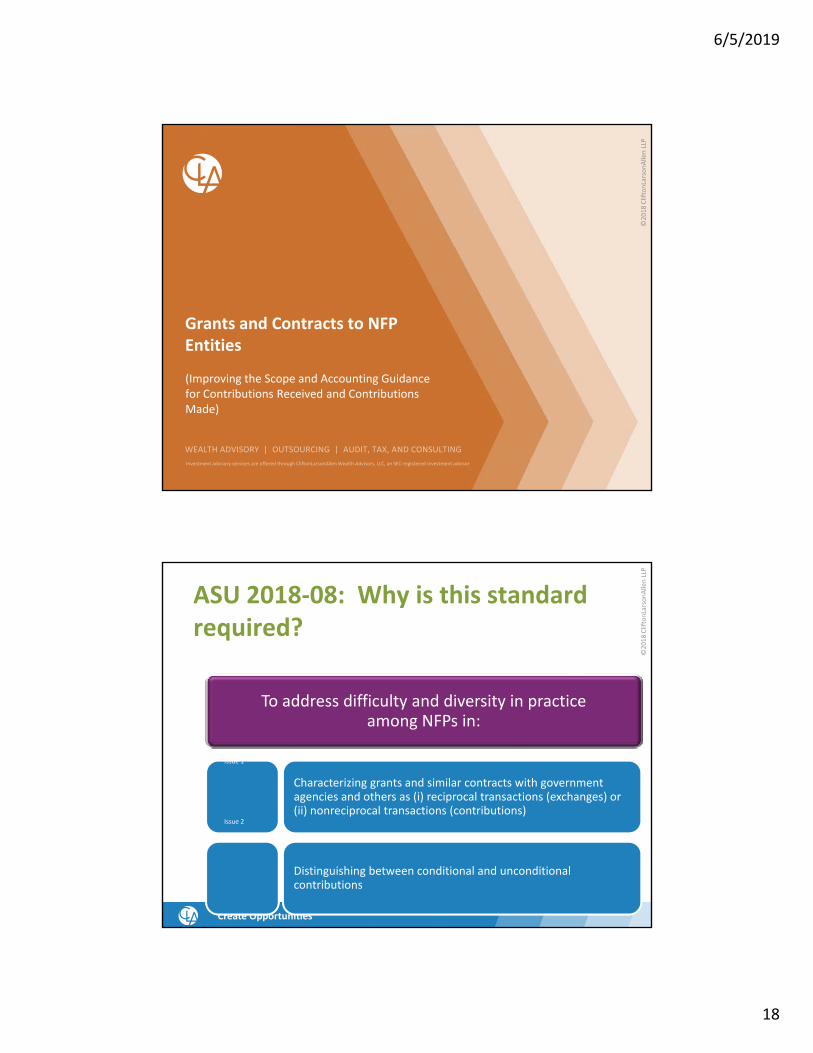

Grants and Contracts to NFP Entities

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

(Improving the Scope and Accounting Guidance for Contributions Received and Contributions Made)

©2018 CliftonLarsonAllen LLP

ASU 2018‐08: Why is this standard required?

To address difficulty and diversity in practiceamong NFPs in:

Characterizing grants and similar contracts with government agencies and others as (i) reciprocal transactions (exchanges) or ( ) l ( b )

Issue 1

Create Opportunities

(ii) nonreciprocal transactions (contributions)

Distinguishing between conditional and unconditional contributions

Issue 2

6/5/2019

19

©2018 CliftonLarsonAllen LLP

Scope

Applies to all entities (NFPs and business entities) that receive or make contributions unless otherwise indicated.

Excludes transfers of assets from the government to business entities.

Applies to both contributions received by a recipient and contributions made by a resource provider. The intent is simply that both apply the same guidance, the entities do not need to track each other’s accounting to achieve the same reporting results

Create Opportunities

accounting to achieve the same reporting results.

The term used in the presentation of financial statements to label revenue (for example, contribution, grant, donation) that is accounted for within the Scope of Subtopic 958‐605 is not a factor for determining whether an agreement is within the scope of that guidance.

37

©2018 CliftonLarsonAllen LLP

Issue 1: Reciprocal (Exchange) vs. Nonreciprocal (Nonexchange/Contribution) TransactionsWho Receives the Benefit?

Create Opportunities 38

*The revenue recognized would actually be the underlying contract’s patient service revenue, tuition revenue, etc.**A focus on whether or not there is a “performance obligation” could even ultimately include some contracts where the general public is the primary beneficiary.

6/5/2019

20

©2018 CliftonLarsonAllen LLP

Issue 1: Reciprocal vs. Nonreciprocal Transactions: Key Clarifications to the Scope of Subtopic 958‐605

The ASU 2018‐08 clarifies and refines existing guidance in S b i 958 605 b ddi h h ld l ifSubtopic 958‐605 by adding paragraphs that would clarify the scope of the Subtopic as well as illustrative examples.

• The resource provider is not synonymous with the general public, even a governmental entity. If a resource provider receives value indirectly by providing a societal benefit, this would be considered a nonreciprocal transaction.

• If the primary beneficiary of a grant or contract is a third party, an NFP must use judgment to determine if the transaction is reciprocal or nonreciprocal.

Create Opportunities 39

judgment to determine if the transaction is reciprocal or nonreciprocal.

• Furthering a resource provider’s mission or “feel good” sentiment does not constitute commensurate value received.

• The type of resource provider should not override the substance of the transaction.

©2018 CliftonLarsonAllen LLP

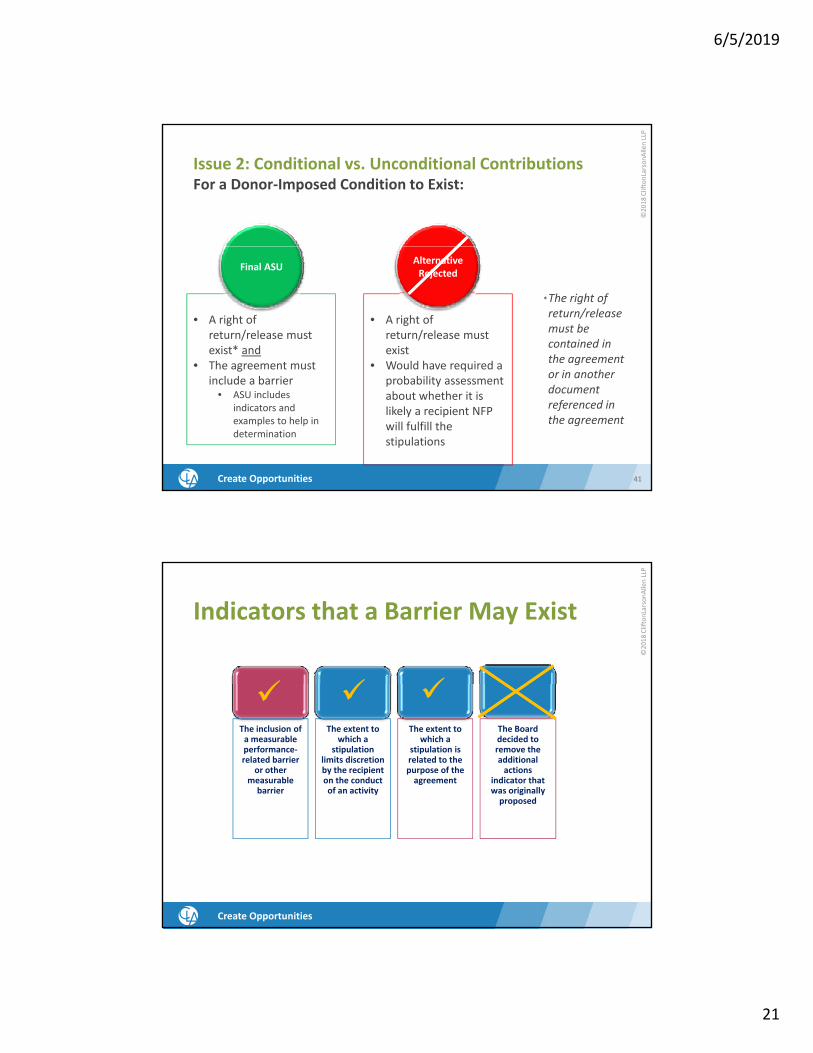

Issue 2: Conditional vs. Unconditional ContributionsFor a Donor‐Imposed Condition to Exist:

• A right of return/release must exist; and

• The agreement must include a barrier

• A right of return/release must exist

• Would have required

Final ASU

Alternative Rejected

Create Opportunities 40

include a barrier• Indicators and examples

to help in determination

Would have required a probabilityassessment about whether it is likely a recipient NFP will fulfill the stipulations

6/5/2019

21

©2018 CliftonLarsonAllen LLP

Issue 2: Conditional vs. Unconditional ContributionsFor a Donor‐Imposed Condition to Exist:

• A right of return/release must exist* and

• The agreement must

• A right of return/release must exist

• Would have required a

Final ASUAlternative Rejected

*The right of return/release must be contained in the agreement

Create Opportunities 41

The agreement must include a barrier

• ASU includes indicators and examples to help in determination

Would have required a probability assessment about whether it is likely a recipient NFP will fulfill the stipulations

or in another document referenced in the agreement

©2018 CliftonLarsonAllen LLP

Indicators that a Barrier May Exist

The inclusion of a measurable performance‐related barrier

or other measurable

barrier

The extent to which a

stipulation limits discretion by the recipient on the conduct of an activity

The extent to which a

stipulation is related to the purpose of the agreement

The Board decided to remove the additional actions

indicator that was originally proposed

Create Opportunities

6/5/2019

22

©2018 CliftonLarsonAllen LLP

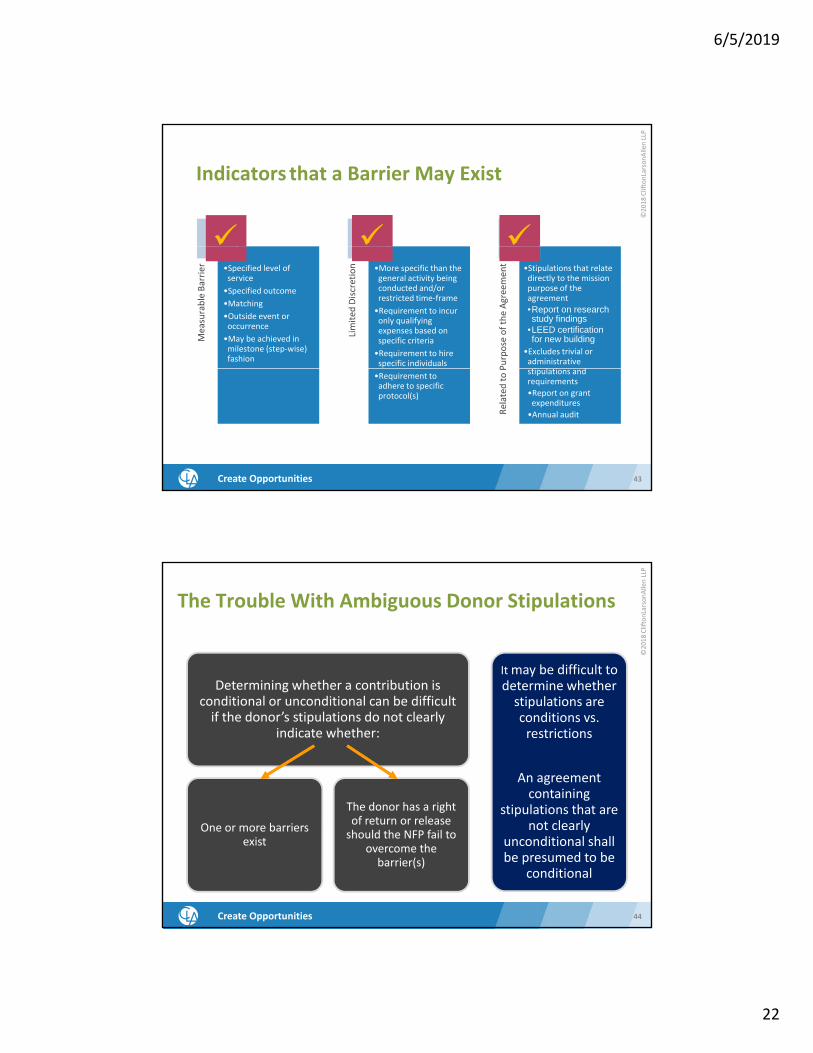

Indicators that a Barrier May Exist

Measurable Barrier •Specified level of

service

•Specified outcome

•Matching

•Outside event or occurrence

•May be achieved in milestone (step‐wise) fashion

Limited

Discretion •More specific than the

general activity being conducted and/or restricted time‐frame

•Requirement to incur only qualifying expenses based on specific criteria•Requirement to hire specific individuals P

urpose of the Agreemen

t •Stipulations that relate directly to the mission purpose of the agreement

•Report on research study findings

•LEED certification for new building

•Excludes trivial or administrative i l i d

Create Opportunities

•Requirement to adhere to specific protocol(s)

Related

to P stipulations and

requirements

•Report on grant expenditures

•Annual audit

43

©2018 CliftonLarsonAllen LLP

The Trouble With Ambiguous Donor Stipulations

Determining whether a contribution isIt may be difficult to determine whetherDetermining whether a contribution is

conditional or unconditional can be difficult if the donor’s stipulations do not clearly

indicate whether:

The donor has a right

determine whether stipulations are conditions vs. restrictions

An agreement containing

ti l ti th t

Create Opportunities 44

One or more barriers exist

The donor has a right of return or release should the NFP fail to

overcome the barrier(s)

stipulations that are not clearly

unconditional shall be presumed to be

conditional

6/5/2019

23

©2018 CliftonLarsonAllen LLP

NFP Revenue Recognition Decision Process

Create Opportunities

*Includes third‐party payments on behalf of identified customers. These do not create new revenue.

45

©2018 CliftonLarsonAllen LLP

Revenue Recognition Activity (Handout)

Instructions:

Read your assigned example disclosure(s). Discuss the following at your table (be prepared to share your insights with the larger group):

1. Determine if the example is an exchange or nonexchange transaction.

Create Opportunities

2. If the example is a nonexchange transaction, determine if it is conditional or unconditional and restricted or unrestricted.

46

6/5/2019

24

©2018 CliftonLarsonAllen LLP

Lease Standard

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTINGInvestment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC‐registered investment advisor

©2018 CliftonLarsonAllen LLP

Leases (Topic 842)

A lease contract conveys the right to control the use of an asset (the underlying aset) for athe use of an asset (the underlying aset) for a period of time in exchange for consideration

Create Opportunities

48

6/5/2019

25

©2018 CliftonLarsonAllen LLP

Implications: We Have a Lease…Now What?

•Virtually all leases will require balance sheet recognition as a right‐of‐use (ROU) asset and lease liabilityof‐use (ROU) asset and lease liability

•The lease classification (operating or finance) will impact the amount and timing of lease income or expense in the income statement

•Balance sheet accounting is identical for operating and finance leases–Record a right‐of‐use asset and a lease liability

•Activities (income) statement accounting is a little more complex

Create Opportunities

49

©2018 CliftonLarsonAllen LLP

How to Determine Lease Classification

•Finance Lease if ANY of the following 5 criteria are met:

1. Transfer of ownership at end of lease term2. Option to purchase is reasonably certain3. Lease term is a major part of the economic life of the asset4. The present value of the lease payments is substantially all of the fair

value of the asset5. The asset is of a specialized nature

•Operating Lease if NONE of the above criteria are met

Create Opportunities

•Operating Lease if NONE of the above criteria are met

50

6/5/2019

26

©2018 CliftonLarsonAllen LLP

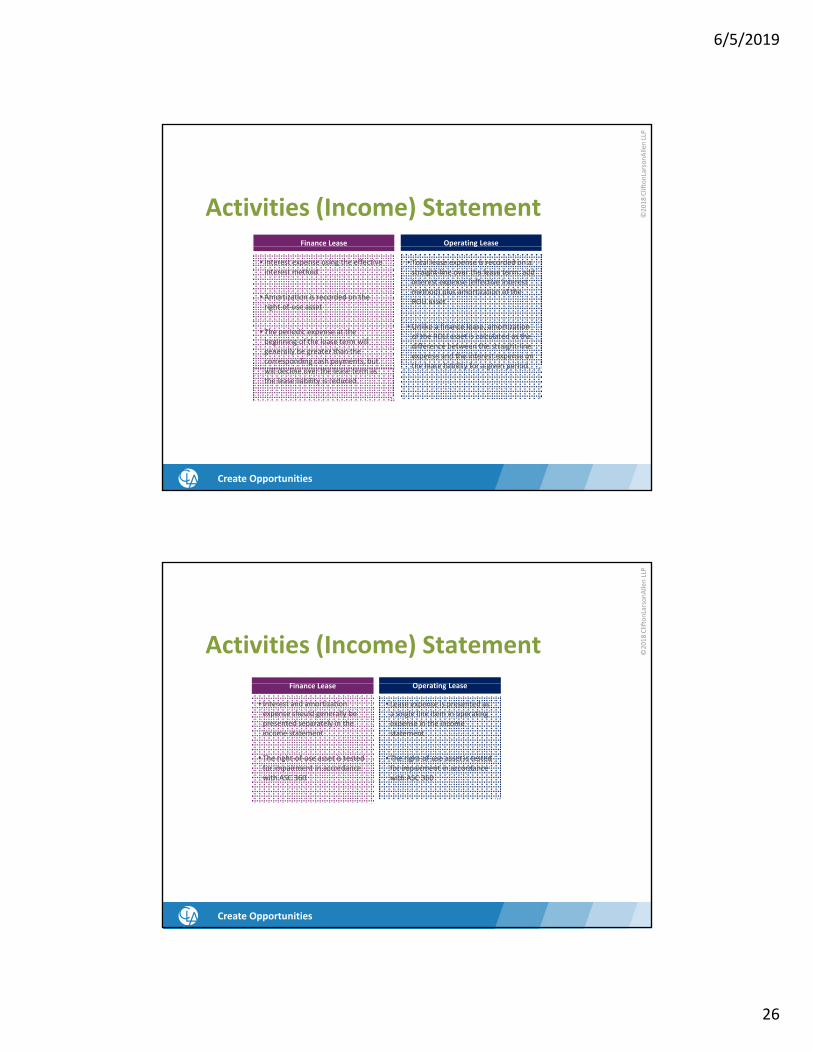

Activities (Income) StatementFinance Lease Operating Lease

• Interest expense using the effective interest method

• Amortization is recorded on the right‐of‐use asset

• The periodic expense at the beginning of the lease term will generally be greater than the corresponding cash payments, but ill d li h l

• Total lease expense is recorded on a straight‐line over the lease term: add interest expense (effective interest method) plus amortization of the ROU asset

• Unlike a finance lease, amortization of the ROU asset is calculated as the difference between the straight‐line expense and the interest expense on the lease liability for a given period.

p g

Create Opportunities

will decline over the lease term as the lease liability is reduced.

y g p

51

©2018 CliftonLarsonAllen LLP

Activities (Income) Statement

Fi L O ti L

• Interest and amortization expense should generally be presented separately in the income statement

• The right‐of‐use asset is tested for impairment in accordance with ASC 360

Finance Lease

• Lease expense is presented as a single line item in operating expense in the income statement

• The right‐of‐use asset is tested for impairment in accordance with ASC 360

Operating Lease

Create Opportunities

52

6/5/2019

27

©2018 CliftonLarsonAllen LLP

Short‐Term Lease Exception

• Lessee may make an accounting policyelection by class of underlying asset not toelection by class of underlying asset not torecognize lease assets and liabilities whenthe lease term is twelve (12) months or less

• Two criteria for short‐term leases:

Create Opportunities

– Lease term of 12 months or less

53

©2018 CliftonLarsonAllen LLP

Other Lease Considerations for Nonprofits

• Donated Rent and Below‐Market Leases

– ROU asset will not include FMV of donated facilities

• Fewer Lease Origination Costs Will Be Capitalized

• Significant Judgment Still Exists in Recording Leases on the Statement of Financial Position

– Estimates related to lease term, discount rate, etc.

Create Opportunities

, ,

• Lessee Reassessments

54

6/5/2019

28

©2018 CliftonLarsonAllen LLP

Lease Disclosures

Disclosure Requirements under ASU 2016‐02

Lessee Lessor

Nature of its leases Nature of its leasesMaturity analysis of lease liabilities Maturity analysis of lease investments

Lease expense, split between operating and financing leases

Profit or loss recognized at leasecommencement (for sales‐type leases)

Short term and variable lease expense Lease income

Weighted average remaining lease term

Changes in residual value of leasedassets

Weighted average discount rate

Create Opportunities

Weighted average discount rate

55

©2018 CliftonLarsonAllen LLP

Lease Accounting

Effective Date:– Public entities (including NFP with conduit debt)– 12/31/19 or

6/30/20

– Nonpublic entities – 12/31/20 or 6/30/21

– Early adoption permitted for all entities

– At transition – recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach

Create Opportunities

app oac

◊ A number of practical expedients are available

56

6/5/2019

29

©2018 CliftonLarsonAllen LLP

Lease Example

• Lessee enters into a 10‐year lease of an asset with an option to extend for anasset, with an option to extend for an additional 5 years.

• It is not reasonably certain to exercise the option to extend the lease and, therefore, determines the lease term to be 10 years.

Create Opportunities 57

• Lease payments are $50,000 per year, all payable at the beginning of each year.

• Lessee incurs initial direct costs of $15,000.

©2018 CliftonLarsonAllen LLP

Lease Example (Continued)• At the commencement, Lessee measures lease liability at the PV of the

remaining 9 payments of $50,000, discounted at the rate of 5.87 percent, which is $342,017.

Both Methods Financing Lease Straight-Line Lease

Interest Amortization Total Lease ROU Lease Reduction of ROULease Expense Expense Expense Asset Expense ROU Asset Asset

Year Liability [X] [Y] [X]+[Y] Balance [Z] [Z]-[X] Balance342,017 407,017 407,017

1 312,093 20,076 40,702 60,778 366,315 51,500 31,424 375,593 2 280,413 18,320 40,702 59,022 325,614 51,500 33,180 342,413 3 246,874 16,460 40,702 57,162 284,912 51,500 35,040 307,374 4 211,365 14,491 40,702 55,193 244,210 51,500 37,009 270,365 5 173 772 12 407 40 702 53 109 203 509 51 500 39 093 231 272

Create Opportunities 58

5 173,772 12,407 40,702 53,109 203,509 51,500 39,093 231,272 6 133,973 10,200 40,702 50,902 162,807 51,500 41,300 189,973 7 91,837 7,864 40,702 48,566 122,105 51,500 43,636 146,337 8 47,228 5,391 40,702 46,093 81,403 51,500 46,109 100,228 9 - 2,772 40,702 43,474 40,702 51,500 48,728 51,500 10 - - 40,702 40,702 - 51,500 51,500 -

Total 107,983 407,017 515,000 515,000 407,017

6/5/2019

30

©2018 CliftonLarsonAllen LLP

CLAconnect.com

Questions?

K i L d CPA Michele Pratt CPAKevin Leder, CPAPartner kevin.leder@@CLAconnect.com(919) 239‐8527

Jordan Miller, CPAPrincipal

Michele Pratt, CPAPartnermichele.pratt@@CLAconnect.com(919) 239‐8549

Principaljordan.miller@@CLAconnect.com(704) 998‐5222

Exercises

NET ASSET CONVERSION ACTIVITY

Instructions: Using the Current GAAP (with Detail) section, convert the net assets to the new presentation under FAS 2016‐14. 1. Convert the Statement of Financial Position from Unrestricted, Temporarily Restricted and Permanently Restricted to Without Donor Restrictions and With Donor Restrictions 2. Complete the Footnote for Net Assets with Donor Restrictions.

CURRENT GAAP (WITH DETAIL)

Unrestricted

Undesignated $ 5,000 Board Designated 100,000

105,000 Temporarily Restricted Program A 800,000 Program B 500,000 Program C 200,000

Future Use 300,000 1,800,000

Permanently Restricted

Program A 1,000,000 Program B 500,000 Program C 25,000 Future Use 2,500,000 Land Required to be Held 25,000

4,050,000

Total $5,955,000

AFTER IMPLEMENTATION 1. FACE OF STATEMENT OF FINANCIAL POSITION

Without Donor Restrictions With Donor Restrictions

Total Net Assets

2. NOTE X NET ASSETS WITH DONOR RESTRICTIONS

Subject to Expenditure for Specified Purpose:

Subject to the Passage of Time:

Subject to the Organization's Spending Policy and Appropriation

Investment in perpetuity, which, once appropriated, is expendable to support:

Not Subject to Appropriation or Expenditure:

Total Net Assets With Donor Restrictions

Example 1

Note X - Information Regarding Liquidity and Availability The Association strives to maintain liquid financial assets sufficient to cover 90 days of general expenditures. Financial assets in excess of daily cash requirements are invested in certificates of deposit, money market funds and other short-term investments.

The following table reflects the Association’s financial assets as of December 31, 2017 and 2016, reduced by amounts that are not available to meet general expenditures within one year of the statement of financial position date because of contractual restrictions or internal board designations. Amounts not available include certain alternative investments with redemption limitations as more fully described in note XX and a board-designated special projects fund that is intended to fund special board initiatives not considered in the annual operating budget. In the event the need arises to utilize the board-designated funds for liquidity purposes, the reserves could be drawn upon through board resolution. Amounts not available to meet general expenditures within one year also may include net assets with donor restrictions. There were no net assets with donor restrictions at December 31, 2017 and 2016.

2017 2016 Cash and cash equivalents $ 2,740,000 $ 2,690,000 Investments 11,100,000 12,250,000 Accounts receivable 325,000 650,000 Total financial assets 14,165,000 15,590,000

Investments with liquidity horizons greater than one year (1,250,000)

(1,450,000) Cash collateral related to letter of credit (275,000) (325,000) Board-designated special projects fund (1,000,000) (1,000,000) Financial assets available to meet cash needs for general

$ 11,640,000

$ 12,815,000

expenditures within one year

Example 2

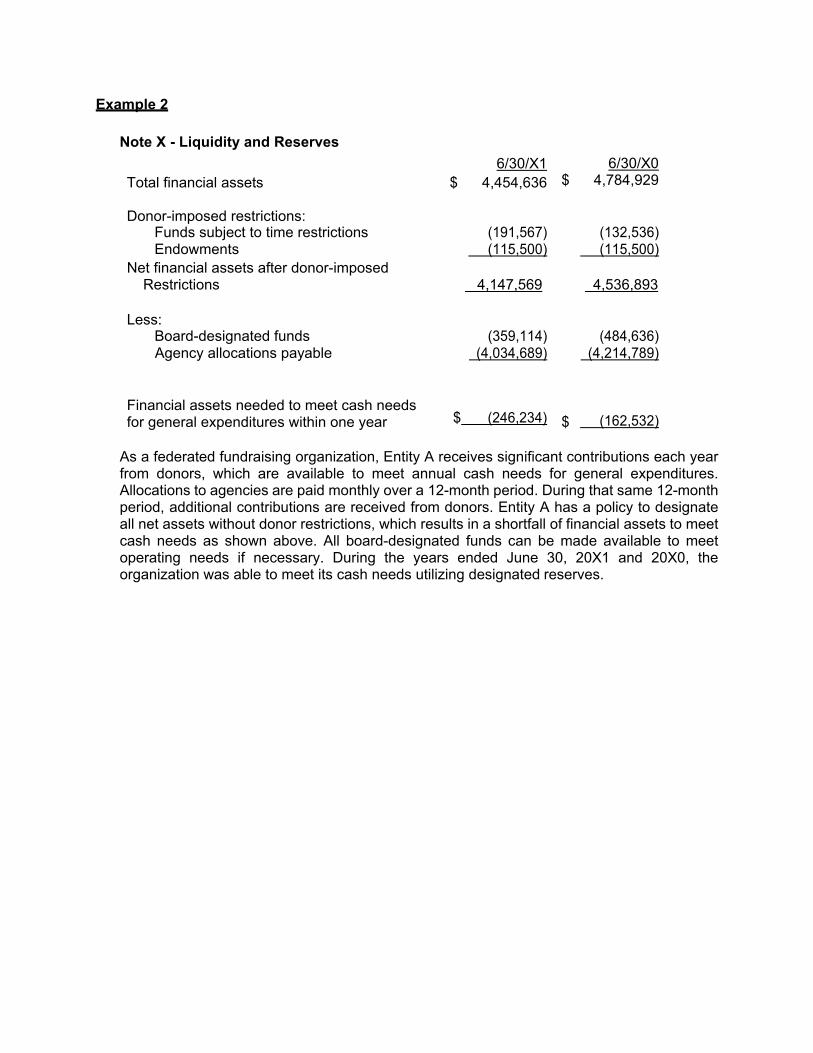

Note X - Liquidity and Reserves

Total financial assets

6/30/X1 $ 4,454,636

6/30/X0 $ 4,784,929

Donor-imposed restrictions: Funds subject to time restrictions

(191,567)

(132,536)

Endowments (115,500) (115,500) Net financial assets after donor-imposed

Restrictions 4,147,569 4,536,893

Less: Board-designated funds (359,114) (484,636) Agency allocations payable (4,034,689) (4,214,789)

Financial assets needed to meet cash needs for general expenditures within one year

$ (246,234)

$

(162,532)

As a federated fundraising organization, Entity A receives significant contributions each year from donors, which are available to meet annual cash needs for general expenditures. Allocations to agencies are paid monthly over a 12-month period. During that same 12-month period, additional contributions are received from donors. Entity A has a policy to designate all net assets without donor restrictions, which results in a shortfall of financial assets to meet cash needs as shown above. All board-designated funds can be made available to meet operating needs if necessary. During the years ended June 30, 20X1 and 20X0, the organization was able to meet its cash needs utilizing designated reserves.

Example 3

NOTE X - AVAILABLE RESOURCES AND LIQUIDITY

The Organization regularly monitors liquidity required to meet its operating needs and other contractual commitments. The Organization has various sources of liquidity at its disposal, including cash and accounts receivables. For the purpose of analyzing resources available to meet general expenditures over a 12-month period, the Organization considers all expenditures related to its ongoing program activities as well as the conduct of services undertaken to support those activities to be general expenditures.

In addition to the financial assets available to meet general expenditures over the next 12 months, the Organization operates with a balanced budget and anticipates collecting sufficient revenues to cover general expenditures.

As of December 31, 2018, the Organization had $495,497 of financial assets available within one year of the balance sheet date, consisting of cash of $435,307 and accounts receivable of $60,190. These financial assets are not subject to donor or other contractual restrictions that make them unavailable for general expenditure within one year of the balance sheet date.

Example 4

NOTE X - LIQUIDITY

Financial assets available for general expenditure, that is, without donor or other restrictions limiting their use, within one year of the statement of financial position date, comprise the following:

2018 2017

Cash 3,863,207$ 3,630,752$ Accounts Receivable, Net 880,920 938,699 Investments 38,223,392 43,928,869

Total Financial Assets 42,967,519$ 48,498,320$

As a part of ABC Nonprofit’s liquidity management plan, it maintains a line of credit totaling $500,000 with a financial institution. At both of December 31, 2018 and 2017, $500,000 remained available on Organization’s line of credit.

ABC holds investments for long-term purposes of $44,989,697 and $53,062,944 as of December 31, 2018 and 2017, respectively, which includes illiquid funds. Although ABC does not intend to spend from investments other than the amount budgeted during its annual budget approval and appropriation, amounts from its investment portfolio could be made available, if necessary.

Illiquid funds consist of $6,766,305 and $9,134,075 as of December 31, 2018 and 2017, respectively.

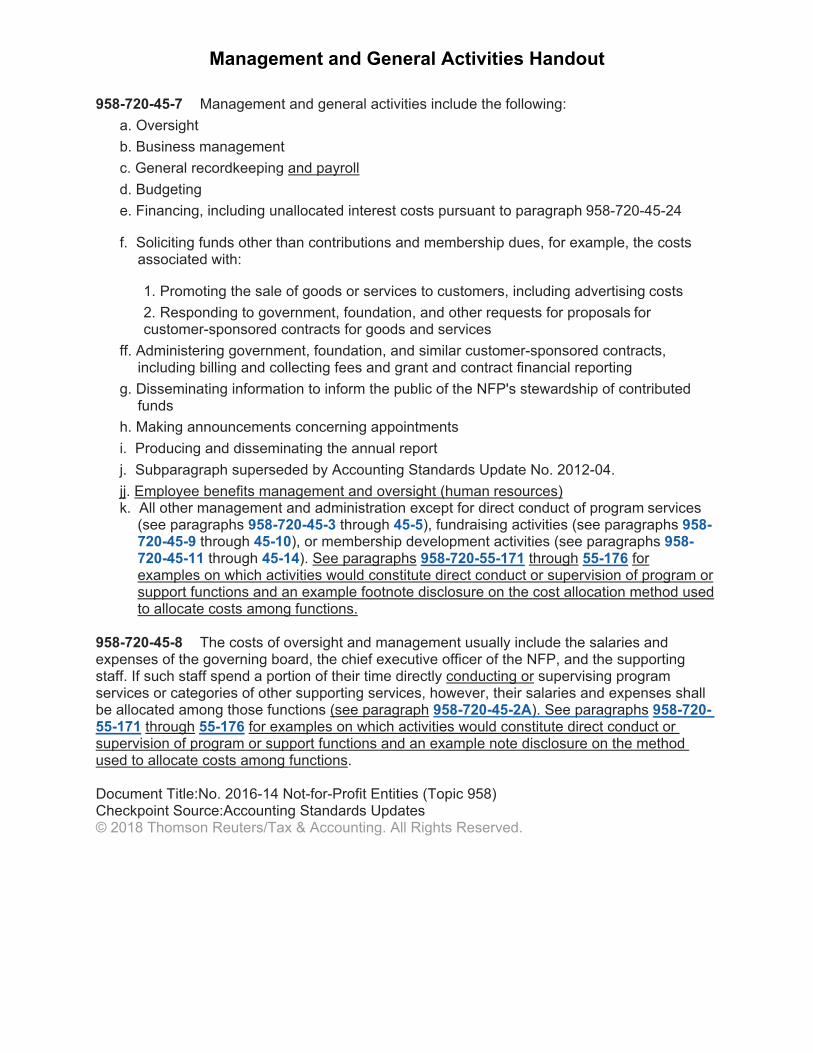

Management and General Activities Handout 958-720-45-7 Management and general activities include the following:

a. Oversight b. Business management c. General recordkeeping and payroll d. Budgeting e. Financing, including unallocated interest costs pursuant to paragraph 958-720-45-24

f. Soliciting funds other than contributions and membership dues, for example, the costs

associated with:

1. Promoting the sale of goods or services to customers, including advertising costs 2. Responding to government, foundation, and other requests for proposals for customer-sponsored contracts for goods and services

ff. Administering government, foundation, and similar customer-sponsored contracts, including billing and collecting fees and grant and contract financial reporting

g. Disseminating information to inform the public of the NFP's stewardship of contributed funds

h. Making announcements concerning appointments i. Producing and disseminating the annual report j. Subparagraph superseded by Accounting Standards Update No. 2012-04. jj. Employee benefits management and oversight (human resources) k. All other management and administration except for direct conduct of program services

(see paragraphs 958-720-45-3 through 45-5), fundraising activities (see paragraphs 958- 720-45-9 through 45-10), or membership development activities (see paragraphs 958- 720-45-11 through 45-14). See paragraphs 958-720-55-171 through 55-176 for examples on which activities would constitute direct conduct or supervision of program or support functions and an example footnote disclosure on the cost allocation method used to allocate costs among functions.

958-720-45-8 The costs of oversight and management usually include the salaries and expenses of the governing board, the chief executive officer of the NFP, and the supporting staff. If such staff spend a portion of their time directly conducting or supervising program services or categories of other supporting services, however, their salaries and expenses shall be allocated among those functions (see paragraph 958-720-45-2A). See paragraphs 958-720- 55-171 through 55-176 for examples on which activities would constitute direct conduct or supervision of program or support functions and an example note disclosure on the method used to allocate costs among functions.

Document Title:No. 2016-14 Not-for-Profit Entities (Topic 958) Checkpoint Source:Accounting Standards Updates © 2018 Thomson Reuters/Tax & Accounting. All Rights Reserved.

Revenue Recognition Activity

Instructions:

Read your assigned example(s). Determine if the example is an exchange or nonexchange transaction. If the example is a nonexchange transaction, determine if it is conditional or unconditional and restricted or unrestricted.

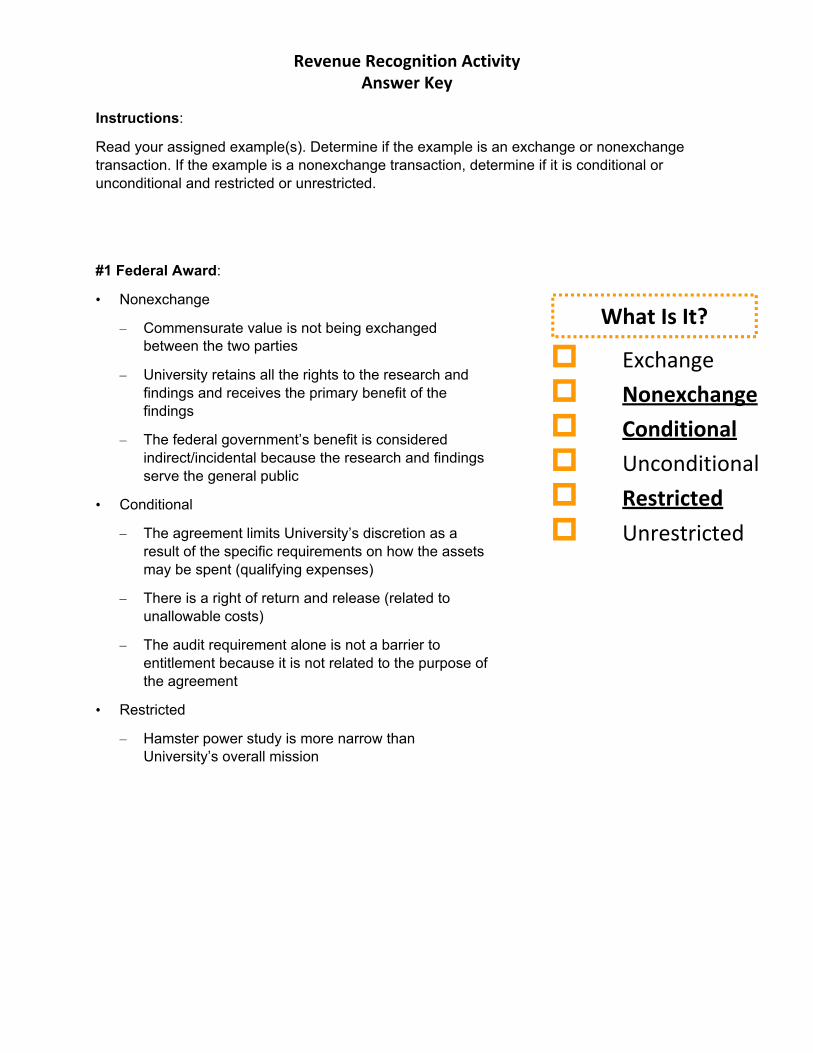

#1 Federal Award:

Power Association is awarded a research grant from the U.S. Department of Energy to study hamster power as an alternative energy source.

• The agreement requires the Association to:

– Follow the rules and regulations established by the Office of Management and Budget (OMB)

– Incur certain expenses (or costs) in compliance with rules and regulations established by the OMB and the federal awarding agency

– Obtain an annual audit in accordance with OMB guidelines

– Submit a summary of research findings to the federal government

• Any unused assets are forfeited, and any unallowed costs that have been drawn down by University are required to be refunded.

• Power Association retains the rights to the findings.

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

What Is It?

Revenue Recognition Activity

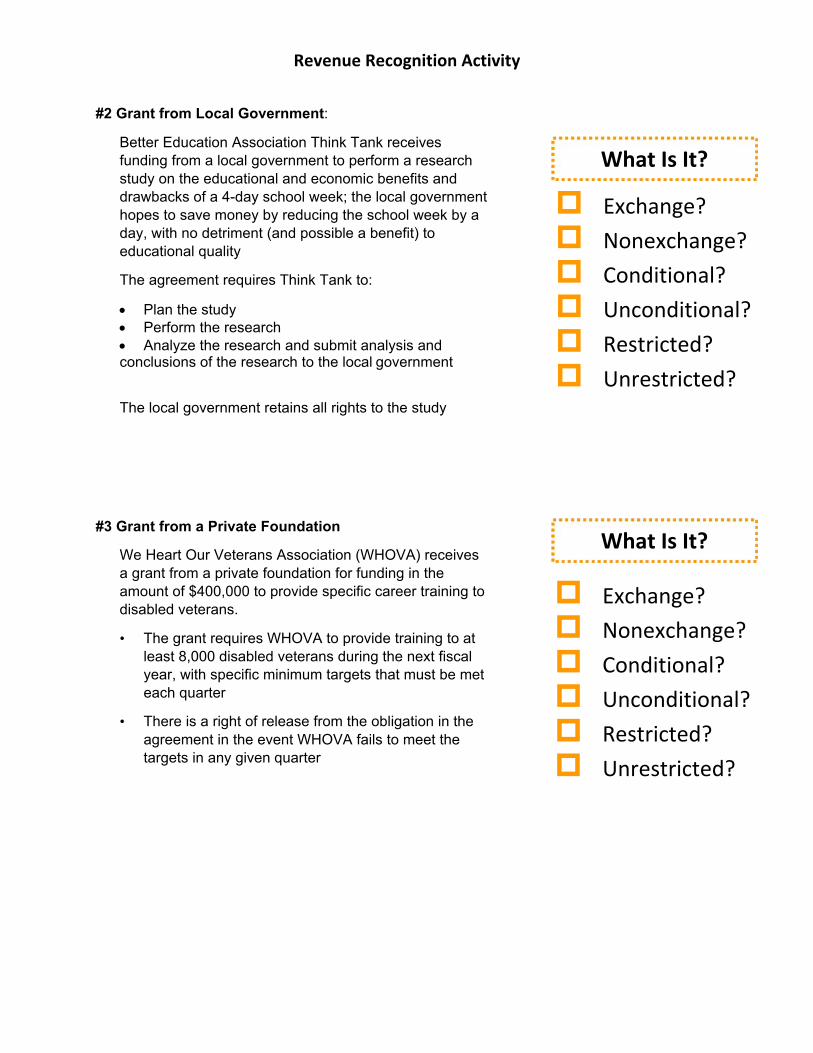

#2 Grant from Local Government:

Better Education Association Think Tank receives funding from a local government to perform a research study on the educational and economic benefits and drawbacks of a 4-day school week; the local government hopes to save money by reducing the school week by a day, with no detriment (and possible a benefit) to educational quality

The agreement requires Think Tank to:

Plan the study Perform the research Analyze the research and submit analysis and conclusions of the research to the local government

The local government retains all rights to the study

#3 Grant from a Private Foundation

We Heart Our Veterans Association (WHOVA) receives a grant from a private foundation for funding in the amount of $400,000 to provide specific career training to disabled veterans.

• The grant requires WHOVA to provide training to at least 8,000 disabled veterans during the next fiscal year, with specific minimum targets that must be met each quarter

• There is a right of release from the obligation in the agreement in the event WHOVA fails to meet the targets in any given quarter

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

What Is It?

What Is It?

Revenue Recognition Activity

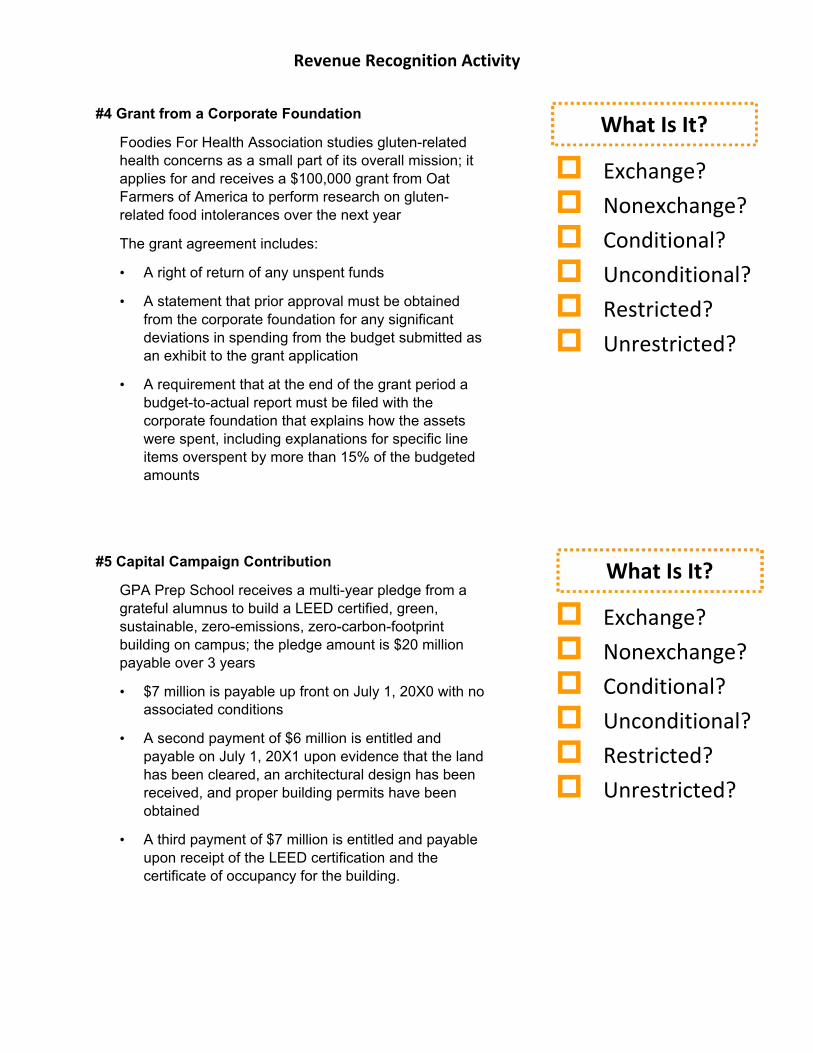

#4 Grant from a Corporate Foundation

Foodies For Health Association studies gluten-related health concerns as a small part of its overall mission; it applies for and receives a $100,000 grant from Oat Farmers of America to perform research on gluten- related food intolerances over the next year

The grant agreement includes:

• A right of return of any unspent funds

• A statement that prior approval must be obtained from the corporate foundation for any significant deviations in spending from the budget submitted as an exhibit to the grant application

• A requirement that at the end of the grant period a budget-to-actual report must be filed with the corporate foundation that explains how the assets were spent, including explanations for specific line items overspent by more than 15% of the budgeted amounts

#5 Capital Campaign Contribution

GPA Prep School receives a multi-year pledge from a grateful alumnus to build a LEED certified, green, sustainable, zero-emissions, zero-carbon-footprint building on campus; the pledge amount is $20 million payable over 3 years

• $7 million is payable up front on July 1, 20X0 with no associated conditions

• A second payment of $6 million is entitled and payable on July 1, 20X1 upon evidence that the land has been cleared, an architectural design has been received, and proper building permits have been obtained

• A third payment of $7 million is entitled and payable upon receipt of the LEED certification and the certificate of occupancy for the building.

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

What Is It?

What Is It?

Revenue Recognition Activity

#6 Grant from Association Assessments

Happy Valley Community Association (Association) is a recreational organization that provides various sports programs to residents in the community. The Association receives a $40,000 cash grant from the Happy Valley Homeowners Association to be used to initiate a tennis program.

• The grant agreement includes stipulations about how the Association should use the assets (for example, to hire 10 tennis instructors, and to provide a youth summer camp for 9 weeks)

• The agreement does not specify that the Association’s entitlement to the $40,000 is dependent upon meeting any of the stipulations in the agreement as long as the funds are used toward the tennis program.

• The grant contains a right of return of any funds not spent on the tennis program.

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

What Is It?

Revenue Recognition Activity

#7 Event Sponsorship

Youth for Yodeling receives $5,000 from Earl’s Earplugs to be the lead sponsor for Youth for Yodeling’s 5k race/yodel biathlon fundraising event to be held next spring

• Earl’s Earplugs receives no direct value in return for the sponsorship

• The sponsorship agreement is silent as to what happens if Youth for Yodeling cancels the event, or if unforeseen circumstances prevent the biathlon from occurring as planned

Exchange? Nonexchange? Conditional? Unconditional? Restricted? Unrestricted?

What Is It?

Answer Key for Exercises

NET ASSET CONVERSION ACTIVITY ANSWER KEY

Instructions: Using the Current GAAP (with Detail) section, convert the net assets to the new presentation under FAS 2016‐14. 1. Convert the Statement of Financial Position from Unrestricted, Temporarily Restricted and Permanently Restricted to Without Donor Restrictions and With Donor Restrictions. 2. Complete the Footnote for Net Assets with Donor Restrictions.

CURRENT GAAP (WITH DETAIL)

Unrestricted

Undesignated $ 5,000 Board Designated 100,000

105,000 Temporarily Restricted Program A 800,000 Program B 500,000 Program C 200,000 Future Use 300,000

1,800,000 Permanently Restricted Program A 1,000,000 Program B 500,000 Program C 25,000 Future Use 2,500,000 Land Required to be Held 25,000

4,050,000

Total $5,955,000

AFTER IMPLEMENTATION 1. FACE OF STATEMENT OF FINANCIAL POSITION

Without Donor Restrictions With Donor Restrictions

Total Net Assets

$ 105,000

5,850,000 $ 5,955,000

2. NOTE X NET ASSETS WITH DONOR RESTRICTIONS

Subject to Expenditure for Specified Purpose: Program A $ 800,000 Program B 500,000 Program C 200,000

Subject to the Passage of Time:

Future Use 300,000

Subject to the Organization's Spending Policy and Appropriation Investment in perpetuity (including amounts above original gift amounts of $4,025,000), which, once appropriated, is expendable to support: Program A 1,000,000 Program B 500,000 Program C 25,000 Any activities of the organization 2,500,000

Not Subject to Appropriation or Expenditure: Land Required to be Held 25,000

Total Net Assets With Donor Restrictions

$ 5,850,000

Revenue Recognition Activity Answer Key

Instructions:

Read your assigned example(s). Determine if the example is an exchange or nonexchange transaction. If the example is a nonexchange transaction, determine if it is conditional or unconditional and restricted or unrestricted.

#1 Federal Award:

• Nonexchange

– Commensurate value is not being exchanged between the two parties

– University retains all the rights to the research and findings and receives the primary benefit of the findings

– The federal government’s benefit is considered indirect/incidental because the research and findings serve the general public

• Conditional

– The agreement limits University’s discretion as a result of the specific requirements on how the assets may be spent (qualifying expenses)

– There is a right of return and release (related to unallowable costs)

– The audit requirement alone is not a barrier to entitlement because it is not related to the purpose of the agreement

• Restricted

– Hamster power study is more narrow than University’s overall mission

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

What Is It?

Revenue Recognition Activity Answer Key

#2 Grant from Local Government:

• Exchange

– Commensurate value is exchanged between the two parties

– The local government retains the rights to the study #3 Grant from a Private Foundation

• Nonexchange

– The foundation does not receive commensurate value in return

• Conditional

– The agreement contains a right of release from obligation if targets are not met

– The foundation requires NFP to achieve a specific level of service (at least 8,000 veterans trained, with minimums of 2,000 per quarter) on which entitlement depends – this is considered a measurable performance-related barrier

– The likelihood of serving those minimums is not considered.

• Restricted

– The specific training program is narrower than WHOVA’s overall mission

What Is It?

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

What Is It?

Revenue Recognition Activity Answer Key

#4 Grant from a Corporate Foundation

• Nonexchange

– While Oat Farmers of America could receive an incidental benefit should the study results indicate that oat consumption is superior to wheat consumption, there is no commensurate exchange of value

• Unconditional

– The general budget included in the grant proposal is not a barrier to entitlement because adherence to a general budget allows for broad discretion

– There are no additional requirements in the agreement that would indicate a barrier exists

– The budget-to-actual reporting and prior approval for budget deviations requirements are administrative and not related to the purpose of the agreement

• Restricted

– Gluten-related studies are more narrow than Foodies’ overall mission

#5 Capital Campaign Contribution

• Nonexchange

– The individual is not receiving commensurate value for the $20 million transferred

• Unconditional – $7 million; Conditional – $13 million

– GPA will receive the initial $7 million payment without having to satisfy any conditions

– GPA will not be entitled to or receive the two remaining payments ($13 million in total) unless it overcomes the respective performance barriers (this is because the individual retained a right of return should the barriers not be met)

– The likelihood of meeting the performance barriers is not a consideration when assessing whether the contribution is conditional

• Restricted

– Construction of the building is more narrow than GPA’s overall mission

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

What Is It?

What Is It?

Revenue Recognition Activity Answer Key

#6 Grant for Tennis Program

• Nonexchange

– The residents receive the benefits, not the Homeowners Association

• Unconditional

– The agreement does not contain a barrier to overcome to be entitled to the transferred assets

– While the grant agreement contains stipulations as to how the Association may spend the $40,000, it does not specify that entitlement to the transferred assets is dependent upon meeting any of the stipulations, therefor, there is no barrier to overcome

• Restricted

– The tennis program is more narrow than the Association’s overall mission

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

What Is It?

Revenue Recognition Activity Answer Key

#7 Event Sponsorship

• Nonexchange

– Earl’s Earplugs receives no direct value in return for the sponsorship

• Unconditional

– The sponsorship agreement is silent as to what happens if Youth for Yodeling cancels the event, or if unforeseen circumstances prevent the biathlon from occurring as planned, therefore Youth for Yodeling concludes there is neither a barrier to overcome nor a right of return of the payment

• Unrestricted

– Youth for Yodeling determined that the sponsorship payment was made in furtherance of the organization’s overall mission, and that no purpose or time restrictions were stipulated in the sponsorship agreement (Youth for Yodeling could have made a different determination)

Exchange Nonexchange Conditional Unconditional Restricted Unrestricted

What Is It?