long term care insurance sponsored group program* ltc-3170 10/05 policy series ltc-03 in idaho:...

TRANSCRIPT

Long Term Care Insurance

Sponsored Group Program*

Long Term Care Insurance

Sponsored Group Program*

LTC-3170 10/05

Policy Series LTC-03In Idaho: Policy Form LTC-03ID

In Pennsylvania: LTC-03FRPAIn New York: SG-03NY

In North Carolina: LTC-03NCIn Oklahoma: LTC-03OKIn California: LTC-02CA

In Florida: LTC_02FL

*Marketing Group Discount in NY and TX

Long-Term Care Insurance is individually underwritten by John Hancock Life Insurance Company, Boston, Massachusetts 02117

For use with Employers Only. Not for use with Consumers.

OverviewOverview

• Sponsored Group Program Advantages• Tax Advantages• The Need for LTCI: Facts and Statistics• How Long Term Care Can Affect Your Business• Why John Hancock?

Sponsored Group Program AdvantagesSponsored Group Program Advantages

• Offer Long Term Care Insurance (LTCI) to employees with a 5% discount.¹

• Added benefit to offer employees

• Once the policy is purchased it is portable. If the employee leaves the company they can take it with them and keep the discount.

1. In NY, Employer pay cannot exceed 50% of total premium in order to receive discount

Sponsored Group Program AdvantagesSponsored Group Program Advantages

• Little or no cost to the employer for employees

to purchase.

• Discounts are available to spouses, partners¹, parents, parents-in-law grandparents and children (including adopted and fostered) of an employee.

1. Only spouses are eligible in LA and MD. In NY only spouses and partners (same sex or opposite sex are eligible.

Sponsored Group Program AdvantagesSponsored Group Program Advantages

• Employers who pay LTC insurance premiums on behalf of an employee may be entitled to deduct 100% of the premiums as a business expense.

• Employer can be selective when paying LTC insurance premiums – does not have to pay premiums for all employees.

• Reduction in absenteeism among employees who otherwise need more time off from work to care for a family member.

Clients should consult with their financial advisor or tax consultant regarding tax issues

IndividualIndividual

• Tax qualified premiums are considered a medical expense deduction

• Medical expenses deductible to the extent they exceed 7.5% of Adjusted Gross Income (AGI)

• Limited to Eligible Premium

Clients should consult with their financial advisor or tax consultant regarding tax issues

Tax Advantages

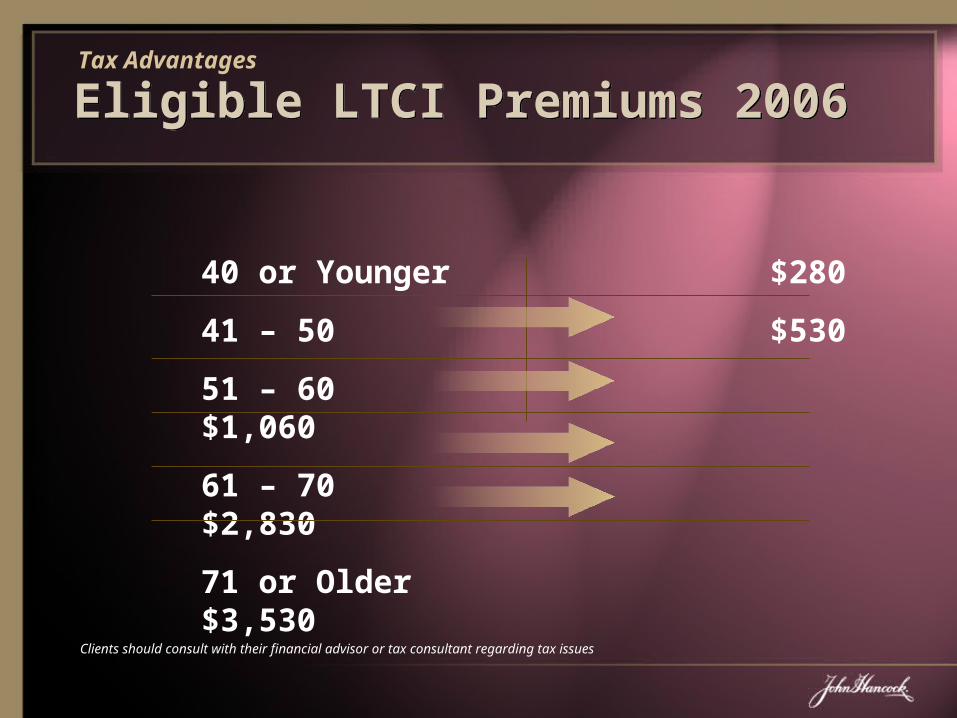

Eligible LTCI Premiums 2006Eligible LTCI Premiums 2006

40 or Younger $280

41 – 50 $530

51 – 60$1,060

61 – 70$2,830

71 or Older$3,530

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

Employee Benefit PlanEmployee Benefit Plan

• Employer establishes employee accident and health plan

• Explains need for a plan

• Participation may be limited to key employees, including shareholder employees, and their spouses and dependents

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

Employee Benefit PlanEmployee Benefit Plan

• Employer pays premiums on personally owned policies

• Employer deducts premiums; deduction not limited to eligible premiums

• Premiums excluded from employee’s gross income

• Works for all subchapter C Corporation employees and Subchapter S Corporation employees who own 2% or less of the corporation

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

Self-EmployedSelf-Employed

• Tax qualified premiums can be deducted up to the age-based Eligible Premium.

• The amount that exceeds Eligible Premium is not deductible

• Not subject to the 7.5% AGI threshold• Limited to earned income from the business

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

Employee Benefit PlanEmployee Benefit Plan

• The following are taxed as self-employed individuals– Partners in a partnership– LLC taxed as a partnership– More than 2% shareholder/employee of a

subchapter S Corporation• Tax qualified premiums can be deducted up to

the age-based Eligible Premium• Not subject to the 7.5% AGI threshold

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

John Hancock SupportJohn Hancock Support

If there are any further questions regarding the tax

deductibility of Long Term Care Insurance please

review:

– 2005 Tax Guide (GFR-TX 8/2005)– Technical Release, January 2005 (Adv-1289

1/05)– Specimen Agreement (VIIAI 3/03)– Or contact your tax advisor

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

Example 1Example 1

• Ann, age 55, is the President and sole shareholder of XYZ, Inc., a C Corporation. The Corporation adopts an accident and health plan that calls for it to pay the premiums for Ann’s Qualified LTCI policy. The premium is $1,500.

• The Corporation deducts $1,500

• Ann excludes the $1,500 from her gross income

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

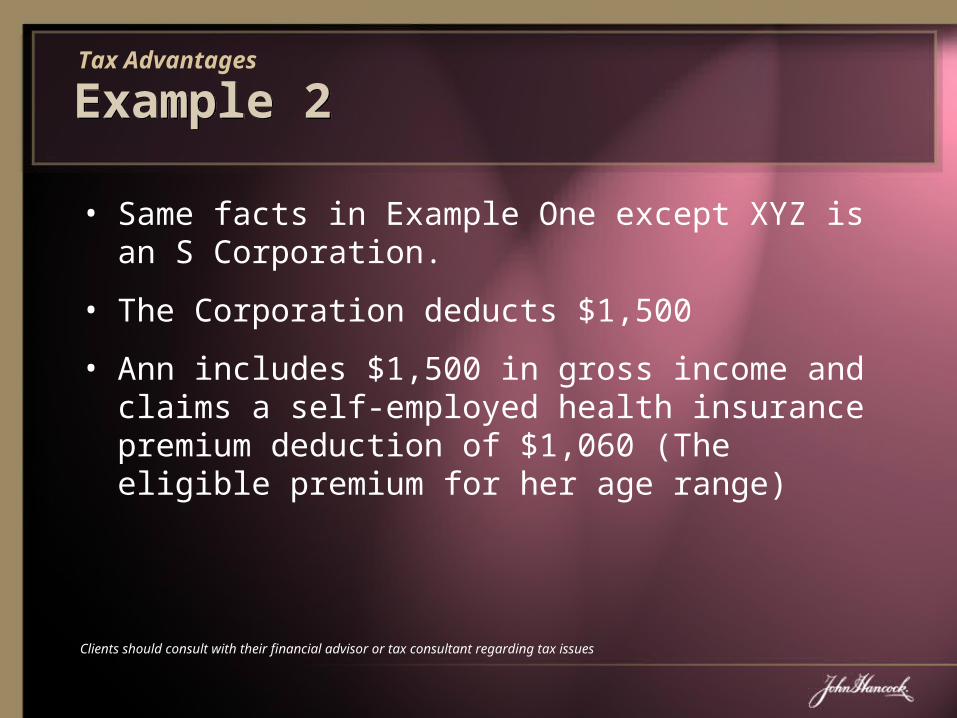

Example 2Example 2

• Same facts in Example One except XYZ is an S Corporation.

• The Corporation deducts $1,500

• Ann includes $1,500 in gross income and claims a self-employed health insurance premium deduction of $1,060 (The eligible premium for her age range)

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

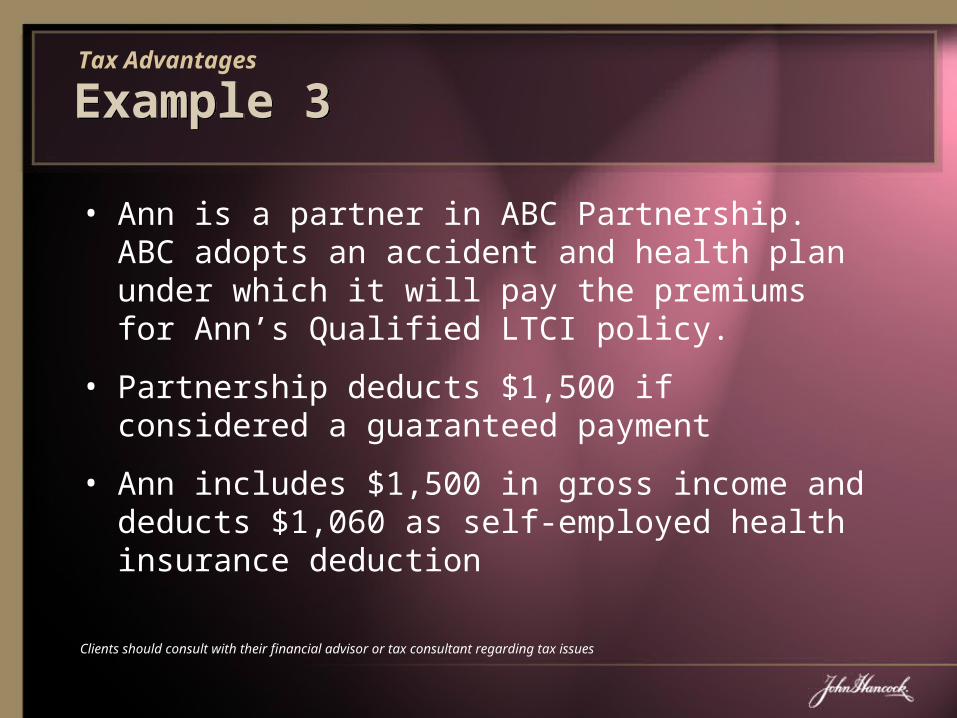

Example 3Example 3

• Ann is a partner in ABC Partnership. ABC adopts an accident and health plan under which it will pay the premiums for Ann’s Qualified LTCI policy.

• Partnership deducts $1,500 if considered a guaranteed payment

• Ann includes $1,500 in gross income and deducts $1,060 as self-employed health insurance deduction

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

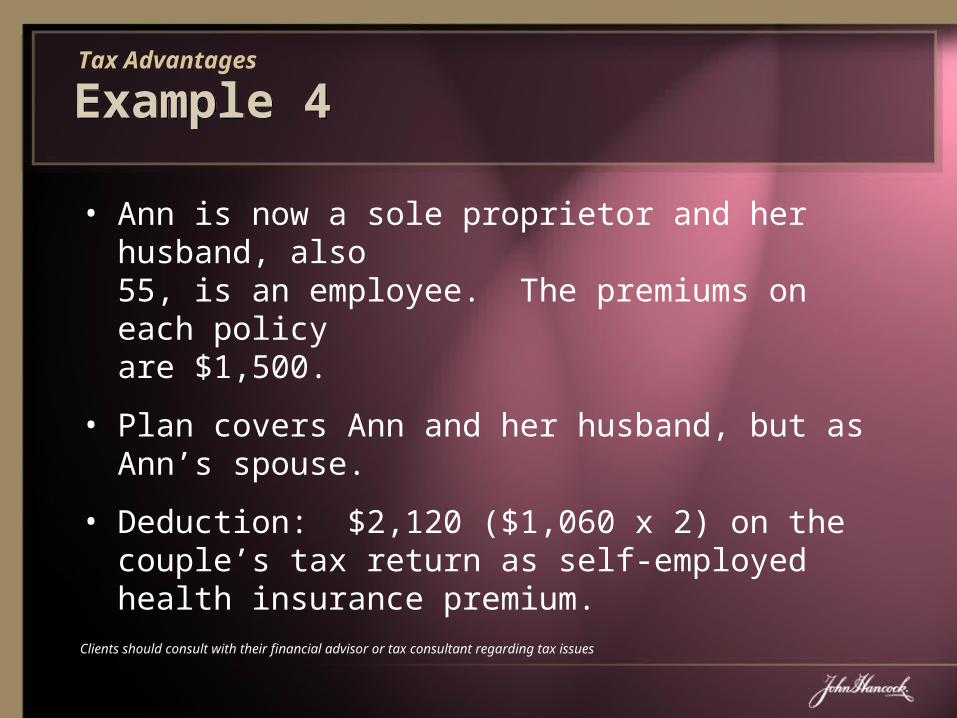

Example 4Example 4

• Ann is now a sole proprietor and her husband, also 55, is an employee. The premiums on each policy are $1,500.

• Plan covers Ann and her husband, but as Ann’s spouse.

• Deduction: $2,120 ($1,060 x 2) on the couple’s tax return as self-employed health insurance premium.

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

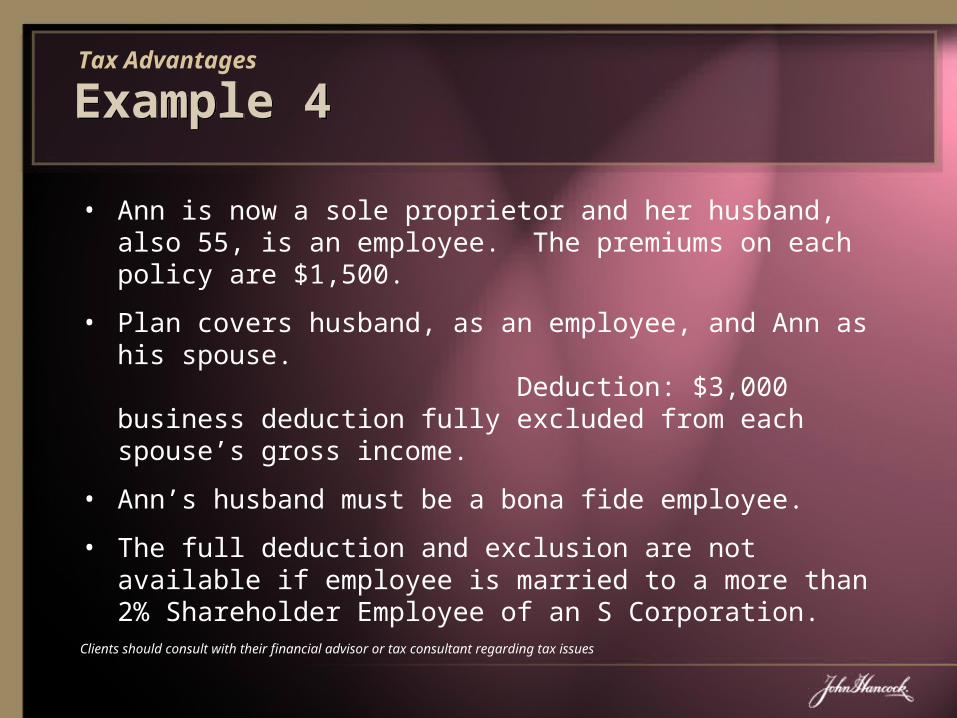

Example 4Example 4

• Ann is now a sole proprietor and her husband, also 55, is an employee. The premiums on each policy are $1,500.

• Plan covers husband, as an employee, and Ann as his spouse. Deduction: $3,000 business deduction fully excluded from each spouse’s gross income.

• Ann’s husband must be a bona fide employee.

• The full deduction and exclusion are not available if employee is married to a more than 2% Shareholder Employee of an S Corporation.

Tax Advantages

Clients should consult with their financial advisor or tax consultant regarding tax issues

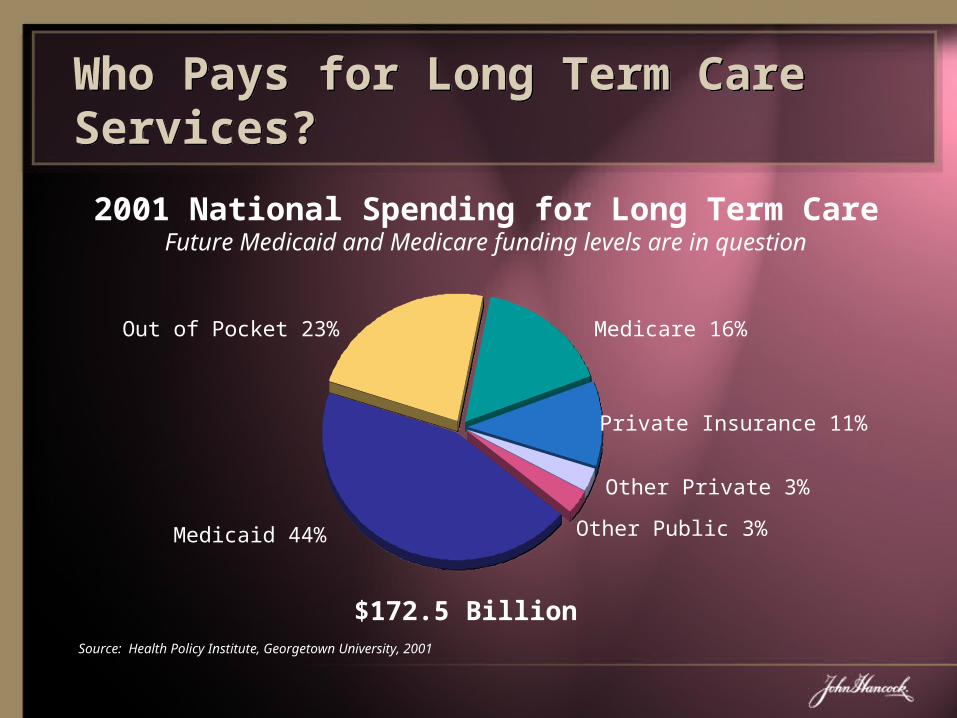

Who Pays for Long Term Care Services?Who Pays for Long Term Care Services?

Out of Pocket 23%

Private Insurance 11%

Other Private 3%

$172.5 Billion

Other Public 3%

Medicare 16%

Medicaid 44%

Source: Health Policy Institute, Georgetown University, 2001

2001 National Spending for Long Term CareFuture Medicaid and Medicare funding levels are in question

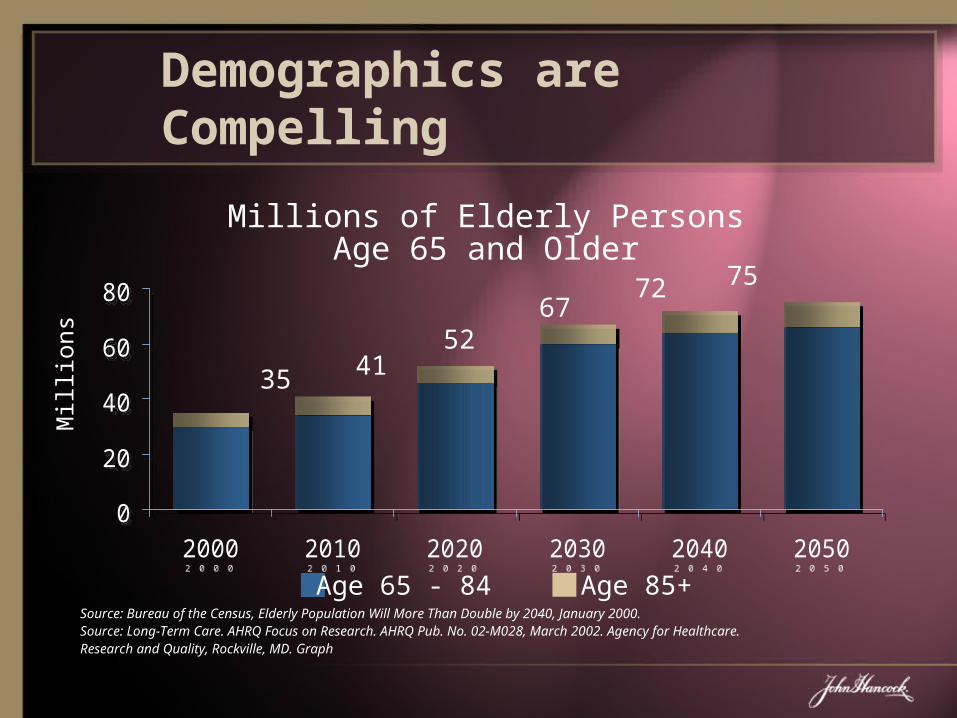

0

20

40

60

80

2000 2010 2020 2030 2040 2050

0

20

40

60

80

2000 2010 2020 2030 2040 2050

Demographics are Compelling

Source: Bureau of the Census, Elderly Population Will More Than Double by 2040, January 2000.Source: Long-Term Care. AHRQ Focus on Research. AHRQ Pub. No. 02-M028, March 2002. Agency for Healthcare. Research and Quality, Rockville, MD. Graph

Millions of Elderly PersonsAge 65 and Older

35 4152

6772 75

Age 65 - 84 Age 85+

Mill

ions

Demographics are CompellingDemographics are Compelling

• Baby Boomers (Ages 39-57) represent a total of 77.7M in 2003. Boomers will begin turning 65 in year 2011 at the rate of 10,000 per day¹.

1. A profile American Baby Boomers: Mature Market Institute, 2003

The Need for Long Term Care InsuranceThe Need for Long Term Care Insurance

• One illness or injury requiring long term care could deplete your savings.

• On average, one year in a nursing home or 24-hour home care can cost more than $66,000 today.¹ In states such as New York, the cost can run as high as $115,340.

1. Congressional Budget Office, “Financing Long-Term Care for the Elderly,” April 20042. New York State Partnership for Long Term Care, 2003

2

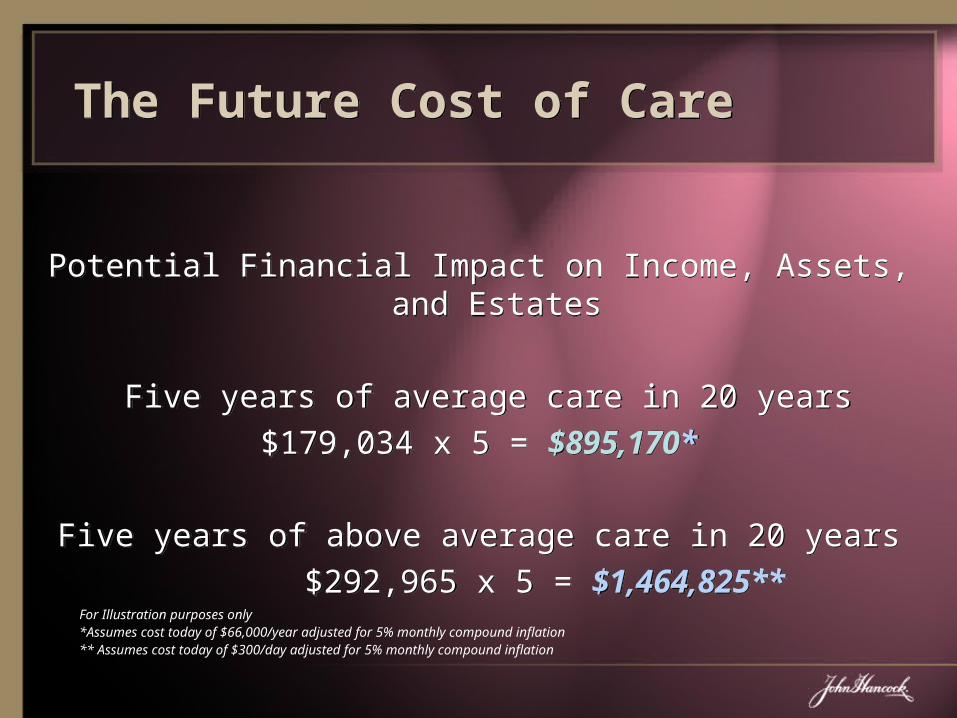

The Future Cost of CareThe Future Cost of Care

Potential Financial Impact on Income, Assets, and Estates

Five years of average care in 20 years$179,034 x 5 = $895,170*

Five years of above average care in 20 years$292,965 x 5 = $1,464,825**

Potential Financial Impact on Income, Assets, and Estates

Five years of average care in 20 years$179,034 x 5 = $895,170*

Five years of above average care in 20 years$292,965 x 5 = $1,464,825**

For Illustration purposes only*Assumes cost today of $66,000/year adjusted for 5% monthly compound inflation** Assumes cost today of $300/day adjusted for 5% monthly compound inflation

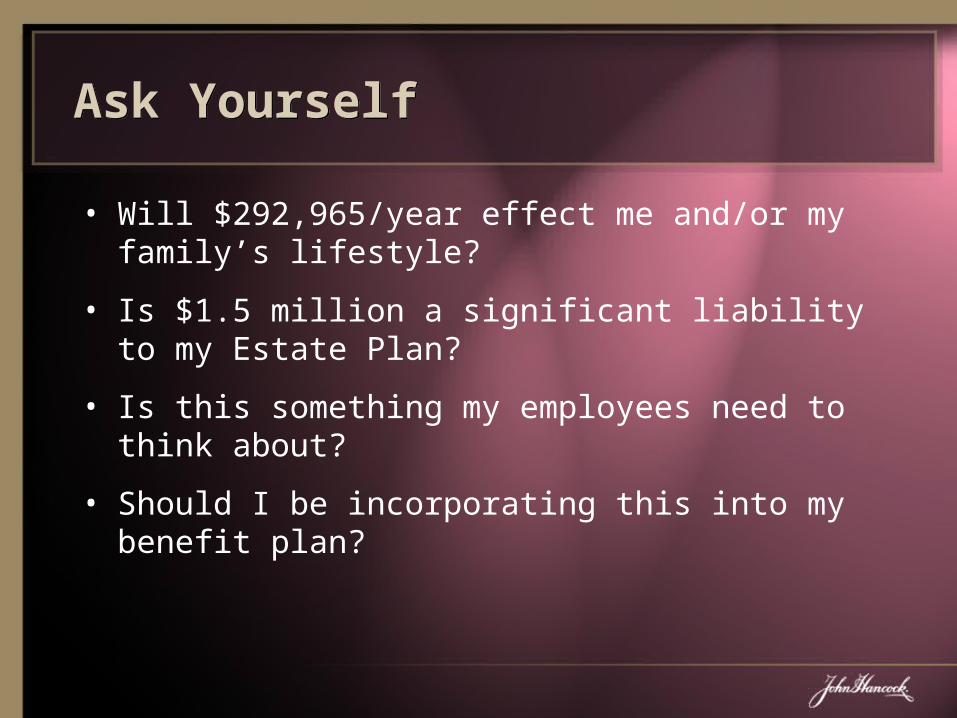

Ask YourselfAsk Yourself

• Will $292,965/year effect me and/or my family’s lifestyle?

• Is $1.5 million a significant liability to my Estate Plan?

• Is this something my employees need to think about?

• Should I be incorporating this into my benefit plan?

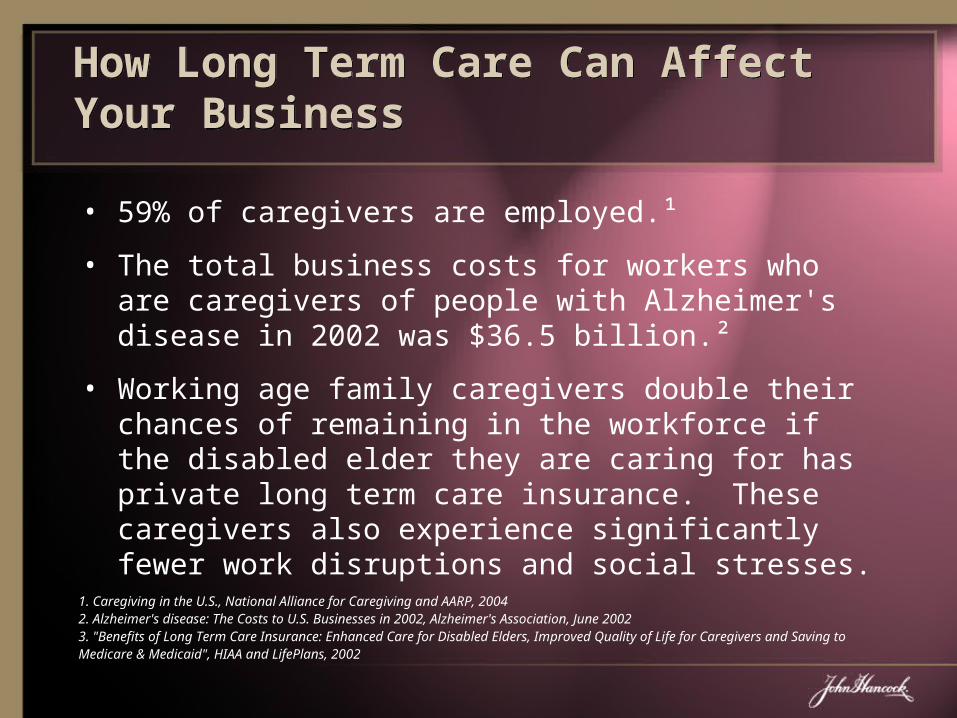

How Long Term Care Can Affect Your BusinessHow Long Term Care Can Affect Your Business

• 59% of caregivers are employed.¹

• The total business costs for workers who are caregivers of people with Alzheimer's disease in 2002 was $36.5 billion.²

• Working age family caregivers double their chances of remaining in the workforce if the disabled elder they are caring for has private long term care insurance. These caregivers also experience significantly fewer work disruptions and social stresses.

1. Caregiving in the U.S., National Alliance for Caregiving and AARP, 20042. Alzheimer's disease: The Costs to U.S. Businesses in 2002, Alzheimer's Association, June 20023. "Benefits of Long Term Care Insurance: Enhanced Care for Disabled Elders, Improved Quality of Life for Caregivers and

Saving toMedicare & Medicaid", HIAA and LifePlans, 2002

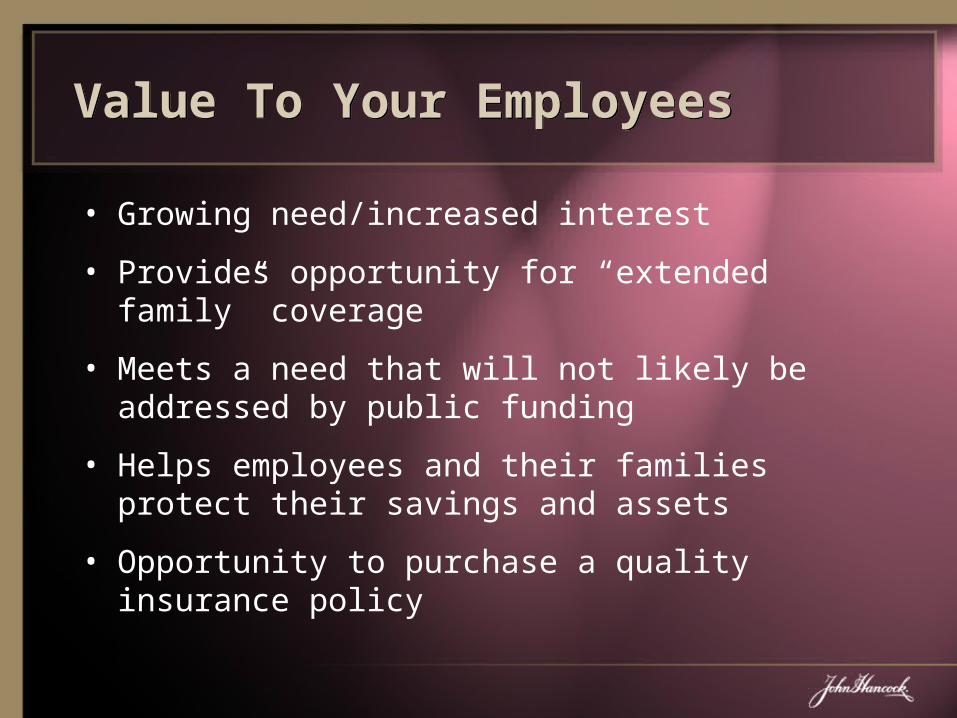

Value To Your EmployeesValue To Your Employees

• Growing need/increased interest

• Provides opportunity for “extended family” coverage

• Meets a need that will not likely be addressed by public funding

• Helps employees and their families protect their savings and assets

• Opportunity to purchase a quality insurance policy

Why John Hancock?Why John Hancock?

• Financial Stability

• Innovator in the Long Term Care Insurance Market

• Significant Role in Public Policy Development

• Experience in Providing High Quality Customer Service

• Ease of Implementation and Administration

John Hancock’s Financial StabilityJohn Hancock’s Financial Stability

• High Ratings for Financial strength and Stability as Judged by the Major Rating Agencies.

• Established in 1862

• Diversified Financial Services Company

• Recognized Leader in Insurance Products and Quality Service

Flexible Product DesignFlexible Product Design

• Reimbursement Model

• Comprehensive Benefits

• “Pool of Dollars” Approach

John Hancock’s Long Term Care Insurance PoliciesJohn Hancock’s Long Term Care Insurance Policies

• Custom Care II* Policy - This long term care insurance policy covers all levels of care in your home, an adult day care center, an assisted living facility or a nursing home. This policy provides comprehensive coverage with several optional features and benefits

*Custom Care I available in CA and FL

Covered ServicesCovered Services

• All levels of nursing home care

• Home health care

• Adult day care

• Care in Assisted Care Living

• Respite Care

Benefit Selections*Benefit Selections*

• LTCI Benefit Amount

• Monthly Benefit: $1,500-$15,000 (In $100 increments)

• Daily Benefit: $50-$500 (In $10 increments)

• Benefit Periods - 2, 3, 4, 5, 6, 10 Years or Lifetime

• Elimination Period: 30, 60, 90,180, or 365 Days

• Inflation Protection – GPO, 5% Simple, 5%/3% Compound or 5%/5% Compound

• Payment Options

• 10-Pay

• Paid-up at age 65*Benefits vary depending upon age and state where purchased.

Additional Benefits¹Additional Benefits¹

• Respite Care

• Care Advisory Services (CAS)

• Stay-at-home Benefit

• Bed Hold Benefit

• International Coverage

• Advantage Provider Program

1. Benefits vary by state

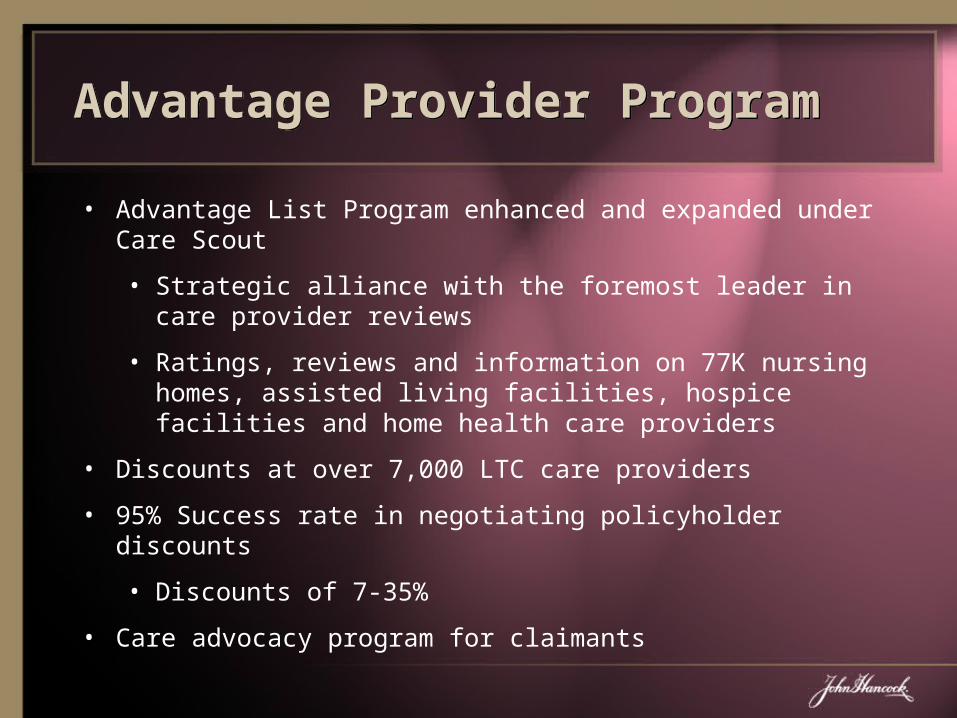

Advantage Provider ProgramAdvantage Provider Program

• Advantage List Program enhanced and expanded under Care Scout

• Strategic alliance with the foremost leader in care provider reviews

• Ratings, reviews and information on 77K nursing homes, assisted living facilities, hospice facilities and home health care providers

• Discounts at over 7,000 LTC care providers

• 95% Success rate in negotiating policyholder discounts

• Discounts of 7-35%

• Care advocacy program for claimants

Built In Benefits for Under Age 65*Built In Benefits for Under Age 65*

• Double Coverage for Accidents Benefit¹

• Return of Premium²

*Benefits vary by state1.This benefit is not available with FamilyCare Benefit or Lifetime Benefit Periods2.This benefit is not available with FamilyCare Benefit

Optional Benefits¹Optional Benefits¹

• Waiver of Home Care Elimination Period

• Additional Cash Benefit

• Restoration of Benefits

• Nonforfeiture

1. Choice of benefits will require additional premium 2. Not available with 180- or 365- Day Elimination Period. This benefit is not payable under International Coverage3.This benefit may trigger a taxable event. Not available in CT, OR or the IN Partnership plan.4. Not Available ages 80-84 or with 2 year, 10 year or Lifetime Benefit Periods

4

2

3

Additional Optional BenefitsAdditional Optional Benefits

• Survivor and Waiver of Premium Benefit

• SharedCare

• Enhanced Return of Premium

1. Choice of benefits will require additional premium 2. Not available with Limited Pay Options or Guaranteed Purchase Option. Not available in WA. 3.Not available ages 80-84 or Lifetime Benefits Period. In AZ and NH, available only with the 4-, 5-, 6- or 10-year

Benefit Period. In PA, available only with the 3-, 4-, 5-, or 6-year Benefit Period. 4.Not available with SharedCare of FamilyCare or to ages 80-84. Not available in all states.

¹¹

2

3

4

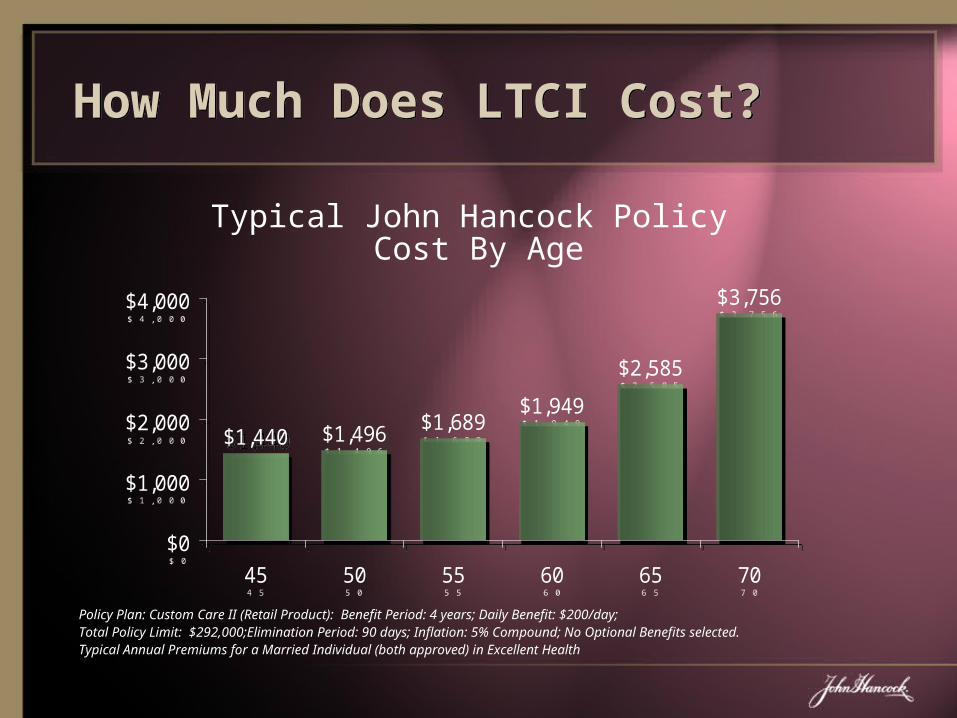

$1,440 $1,496 $1,689$1,949

$2,585

$3,756

$0

$1,000

$2,000

$3,000

$4,000

45 50 55 60 65 70

$1,440 $1,496 $1,689$1,949

$2,585

$3,756

$0

$1,000

$2,000

$3,000

$4,000

45 50 55 60 65 70

Policy Plan: Custom Care II (Retail Product): Benefit Period: 4 years; Daily Benefit: $200/day; Total Policy Limit: $292,000;Elimination Period: 90 days; Inflation: 5% Compound; No Optional Benefits selected. Typical Annual Premiums for a Married Individual (both approved) in Excellent Health

Typical John Hancock Policy Cost By Age

How Much Does LTCI Cost?How Much Does LTCI Cost?

Underwriting FlexibilityUnderwriting Flexibility

• Various health ratings to meet a wide range of health situations

• Prequalification Hotline 1-888-604-7296 Option #3

Claims Case Management UnitClaims Case Management Unit

• Staffed by experienced case managers and social workers

• Eligibility certification

• Information counseling

Client ServiceClient Service

• Client Service Hotline

• 1-800-377-7311

Thank You Thank You