management accounting and organizational change : impact

TRANSCRIPT

Edith Cowan University Edith Cowan University

Research Online Research Online

Theses: Doctorates and Masters Theses

2010

Management accounting and organizational change : impact of Management accounting and organizational change : impact of

alignment of management accounting system, structure and alignment of management accounting system, structure and

strategy on performance strategy on performance

Tuan Tuan Mat Edith Cowan University

Follow this and additional works at: https://ro.ecu.edu.au/theses

Part of the Business Administration, Management, and Operations Commons

Recommended Citation Recommended Citation Tuan Mat, T. (2010). Management accounting and organizational change : impact of alignment of management accounting system, structure and strategy on performance. https://ro.ecu.edu.au/theses/149

This Thesis is posted at Research Online. https://ro.ecu.edu.au/theses/149

Edith Cowan University

Copyright Warning

You may print or download ONE copy of this document for the purpose

of your own research or study.

The University does not authorize you to copy, communicate or

otherwise make available electronically to any other person any

copyright material contained on this site.

You are reminded of the following:

Copyright owners are entitled to take legal action against persons who infringe their copyright.

A reproduction of material that is protected by copyright may be a

copyright infringement.

A court may impose penalties and award damages in relation to

offences and infringements relating to copyright material. Higher

penalties may apply, and higher damages may be awarded, for

offences and infringements involving the conversion of material

into digital or electronic form.

MANAGEMENT ACCOUNTING AND ORGANIZATIONAL CHANGE:

IMPACT OF ALIGNMENT OF MANAGEMENT ACCOUNTING SYSTEM,

STRUCTURE AND STRATEGY ON PERFORMANCE

TUAN ZAINUN TUAN MAT

A thesis submitted in partial fulfilment of the requirements for the degree of

Doctor of Philosophy

School of Accounting, Finance and Economics

Faculty of Business and Law

Edith Cowan University, Perth

Western Australia

December 2010

MANAGEMENT ACCOUNTING AND ORGANIZATIONAL CHANGE:

IMPACT OF ALIGNMENT OF MANAGEMENT ACCOUNTING SYSTEM,

STRUCTURE AND STRATEGY ON PERFORMANCE

School of Accounting, Finance and Economics

Faculty of Business and Law

Edith Cowan University, Perth

Western Australia

Principal Supervisor: Professor Malcolm Smith

Associate Supervisor: Dr Hadrian Djajadikerta

December 2010

USE OF THESIS

The Use of Thesis statement is not included in this version of the thesis.

ii

ABSTRACT

The business environment in Malaysia has changed rapidly over recent decades, and

continues to change. Globalization has brought new technology and made the

business environment in Malaysia open to greater competition. Central Government

economic policy relating to ‘knowledge economy (k-economy)’ and vision 2020

have also opened the market up for competition and certainly increased

technological development. These changes have impacted greatly on the business

environment in Malaysia, especially on manufacturing industry, which has been

identified as the most active and important contributor to the Malaysian economy.

Literature has identified that changes in both external and internal organizational

factors have influenced changes in management accounting practices in

organizations. When business organizations respond to challenges by embarking on

a change management path, they are faced with the choices of which ones of the

many management methods, techniques and systems would be most effective. This

is important as the management accounting system plays an important role in

providing useful information to management, especially in the decision making

process. Many researchers have shown an interest in understanding the way in which

management accounting and organizational changes respond to the changing

business environment. However, most of this research has to date been conducted in

a developed economy setting especially in Western countries.

This study aims to investigate the impact of alignment among the changes in external

and internal organizational factors, with the changes in management accounting

practice on performance. The framework has been developed based on the literature

from Western countries and Malaysia (as well as other less developed countries).

The six areas in the framework comprise changes in external organizational factors

(namely, competitive environment and advanced manufacturing technology),

internal factors (namely, structure and strategies), management accounting practices

and performance. To meet the research objectives, a quantitative research design was

iii

adopted involving the use of a mailed survey to collect data from various types of

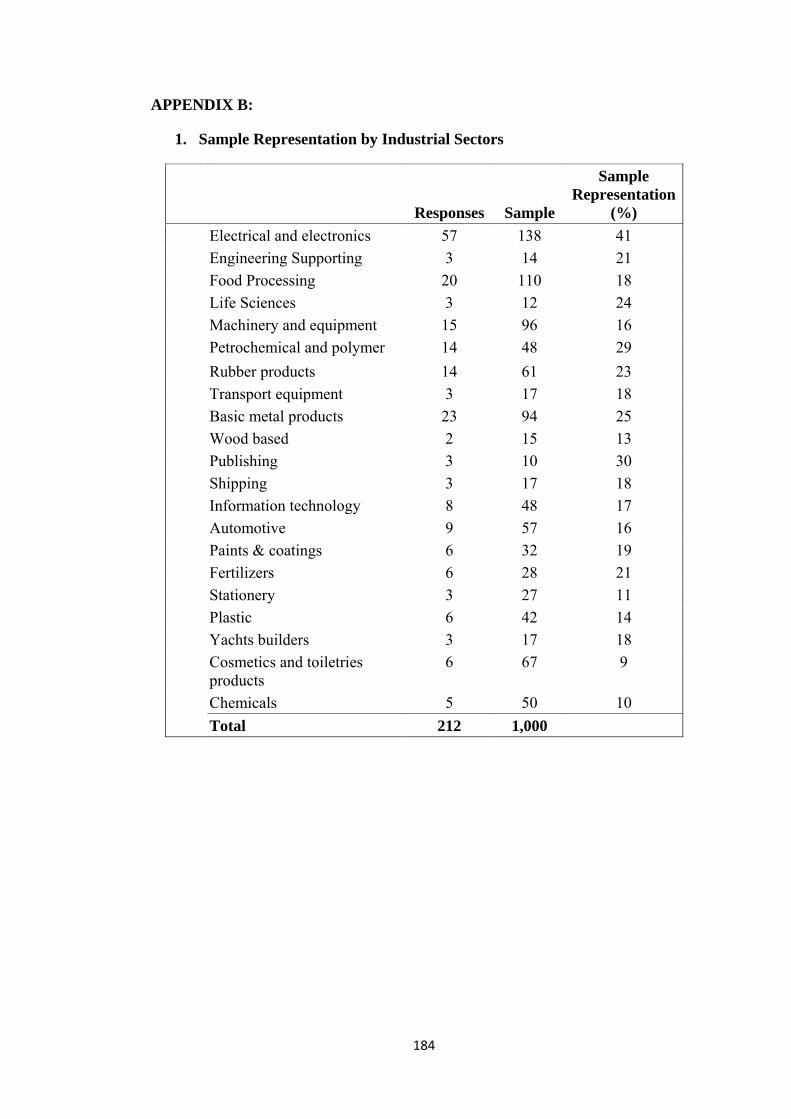

manufacturing companies in Malaysia. In total, 212 valid responses were obtained

and analysed. Structural equation modelling, using the CBSEM approach was

employed as the main statistical technique to test the hypothesized model. Non

parametric techniques were also employed to test the subsidiary hypothesis.

Interestingly, the findings of the study showed significantly different results from

those studies conducted in developed countries. It might be due to the government

policies which often favour firms in manufacturing industry (e.g., many incentives

are given to these firms). The results revealed a positive alignment among the

external environmental factors and organizational factors with management

accounting practices, which in turn positively impacted on organizational

performance. Surprisingly, the findings showed that changes in manufacturing

accounting practices and strategies were influenced by changes in advanced

manufacturing technology (AMT), but these changes were not influenced by changes

in market competition. Results also showed that neither market competition nor

AMT had influenced change in organizational structure.

This study also provides evidence of an interrelationship between management

accounting practices and structure, but with no evidence of a reciprocal relationship

between management accounting practices and strategy. Results from the subsidiary

hypotheses also support the main hypotheses. The distinctive findings obtained in

this study make a contribution to our knowledge of the relationship between

management accounting systems and organizational change, as well as providing

helpful insights to practitioners in making decisions in the face of a changing

business environment.

iv

DECLARATION

I certify that this thesis does not, to the best of my knowledge belief:

(i) incorporate without acknowledgement any material previously submitted

for a degree or diploma in any institution of higher education;

(ii) contain any material previously published or written by another person

except where due reference is made in text; or

(iii) contain any defamatory material.

I also grant permission for the Library at Edith Cowan University to make duplicate

copies of my thesis as required.

Signature: ..............................

Date: 6 December 2010

v

Some sections of this thesis have already been presented as conference paper or

conference proceedings, and have been published in an academic journal:

Conference paper and proceeding

Tuan Mat, T.Z., Smith, M., and Djajadikerta, H., 2009, Determinants of management

accounting change in Malaysian manufacturing companies. Proceedings of The 5th

International Management Accounting Conference, November, Kuala Lumpur,

Malaysia.

Paper published in academic journal

Tuan Mat, T.Z., Smith, M., and Djajadikerta, H., 2010, Determinants of management

accounting and control system in Malaysian manufacturing companies, Asian

Journal of Accounting & Governance, 1, 79-104.

vi

ACKNOWLEDGEMENT

I would like to acknowledge the foremost contribution provided by my Principal

Supervisor, Professor Malcolm Smith for his guidance throughout the completion

process of this thesis. He has made important comments and suggestions at every

stage of my learning process. The period of my study has been an opportunity for me

to learn from his experience and devotion to research. I would also like to thank Dr

Hadrian Djajadikerta for his association in supervising this project.

I wish to thank people who provided their academic knowledge to help me to

complete the thesis. I also wish to thank the University Teknologi MARA Malaysia

and Ministry of Higher Education Malaysia, for their financial support.

I am indebted to my family especially my husband, daughter and son for their

encouragement, support and love. They have been an inspiration to me. This

appreciation is also extended to my parents for their support and prayer for my

success. Without help from all of these people, it would have been difficult to

complete the study.

vii

TABLE OF CONTENTS

Use of Thesis................................................................................................................ i

Abstract ...................................................................................................................... ii

Declaration ................................................................................................................ iv

Acknowledgement .................................................................................................... vi

Table of Contents ..................................................................................................... vii

List of Tables ............................................................................................................ xii

List of Figures ......................................................................................................... xiv

CHAPTER ONE: INTRODUCTION AND OVERVIEW ..................................... 1

1.1 Introduction ........................................................................................................... 1

1.2 Background and Significance of the Study ........................................................... 3

1.3 Research Question................................................................................................. 6

1.4 Research Model..................................................................................................... 7

1.5 Study Design ......................................................................................................... 8

CHAPTER TWO: LITERATURE REVIEW ....................................................... 12

2.1 Introduction ......................................................................................................... 12

2.2 Management Accounting and Its Evolution........................................................ 12

2.3 Management Accounting Change ....................................................................... 15

2.3.1 Contingency Theory .................................................................................. 18

2.3.2 Institutional Perspectives ........................................................................... 21

2.4 Changes in Competitive Environment and Advanced Manufacturing

Technology.......................................................................................................... 23

2.5 Competitive Environment, Technology and Organizational Change ................. 26

2.5.1 Organizational Structure ............................................................................ 27

2.5.2 Organizational strategy .............................................................................. 29

2.6 Competitive environments, technology and management accounting

practices ............................................................................................................. 33

viii

2.7 Management Accounting and Organizational Change ....................................... 35

2.7.1 Management accounting and structural change ......................................... 38

2.7.2 Management accounting and strategic change .......................................... 41

2.8 Organizational Performance ............................................................................... 43

2.8.1 Management accounting practices and performance. ................................ 45

2.8.2 Organizational structure and performance. ............................................... 46

2.8.3 Organizational strategy and performance. ................................................. 47

2.9 Summary ............................................................................................................. 48

CHAPTER THREE: RESEARCH DESIGN ........................................................ 50

3.1 Introduction ......................................................................................................... 50

3.2 Background to the Survey ................................................................................... 50

3.2.1 Concept of Survey ..................................................................................... 52

3.2.2 Types of Survey ......................................................................................... 53

3.3 Questionnaire Design .......................................................................................... 55

3.3.1 Response Format and Scaling.................................................................... 56

3.3.2 Ethical Issues ............................................................................................. 57

3.3.3 Pre-Test ...................................................................................................... 57

3.4 Instrument Development ..................................................................................... 58

3.4.1 Section A ................................................................................................... 59

3.4.2 Section B.................................................................................................... 60

3.4.3 Section C.................................................................................................... 62

3.4.4 Section D ................................................................................................... 63

3.4.5 Section E .................................................................................................... 64

3.5 Sampling Procedures........................................................................................... 65

3.6 Data Collection Procedures ................................................................................. 68

3.7 Data Analysis ...................................................................................................... 70

3.7.1 Validity and Reliability of Measures ......................................................... 71

3.7.2 Structural Equation Modelling (SEM) ...................................................... 72

3.7.3 Data Distribution and Estimation Techniques ........................................... 75

3.7.4 Model’s Goodness-of-Fit (GOF) ............................................................... 77

3.8 Summary ............................................................................................................. 80

ix

CHAPTER FOUR: HYPOTHESES DEVELOPMENT ...................................... 82

4.1 Introduction ......................................................................................................... 82

4.2 Changes in Competitive Business Environment and Manufacturing

Technology.......................................................................................................... 84

4.2.1 Changes in Competitive Environments, Technology and Organizational

Structure..................................................................................................... 84

4.2.2 Changes in competitive environment, technology and organizational

strategy....................................................................................................... 85

4.2.3 Changes in competitive environment, technology and management

accounting practices .................................................................................. 86

4.3 Changes in Management Accounting Practices .................................................. 87

4.3.1 Changes in management accounting practices and organizational

structure ..................................................................................................... 88

4.3.2 Changes in management accounting practices and organizational

strategy....................................................................................................... 89

4.4 Impact on Performance ....................................................................................... 90

4.4.1 Effect of changes in management accounting practices on performance .. 90

4.4.2 Effect of changes in organizational structure on performance .................. 90

4.4.3 Effect of changes in organizational strategy on performance ................... 91

4.5 Subsidiary Hypotheses ........................................................................................ 92

4.6 Summary ............................................................................................................. 93

CHAPTER FIVE: PILOT STUDY ........................................................................ 94

5.1 Introduction and Background of Pilot Study ...................................................... 94

5.2 Research Method................................................................................................. 94

5.2.1 Sampling and Data Collection Procedures ................................................ 94

5.2.2 Research Instruments ................................................................................. 96

5.2.3 Data Analysis ............................................................................................. 98

5.3 Results and Discussion ....................................................................................... 98

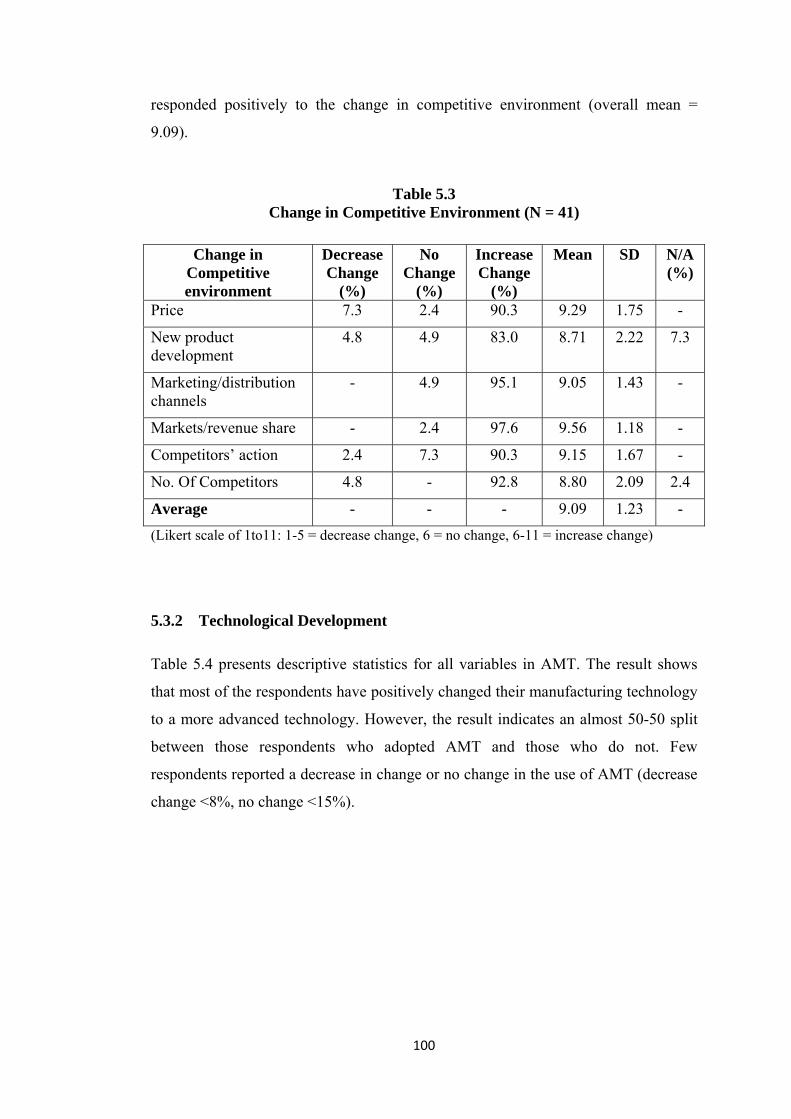

5.3.1 Competitive Environment ......................................................................... 99

5.3.2 Technological Development .................................................................... 100

5.3.3 Organizational Structure .......................................................................... 101

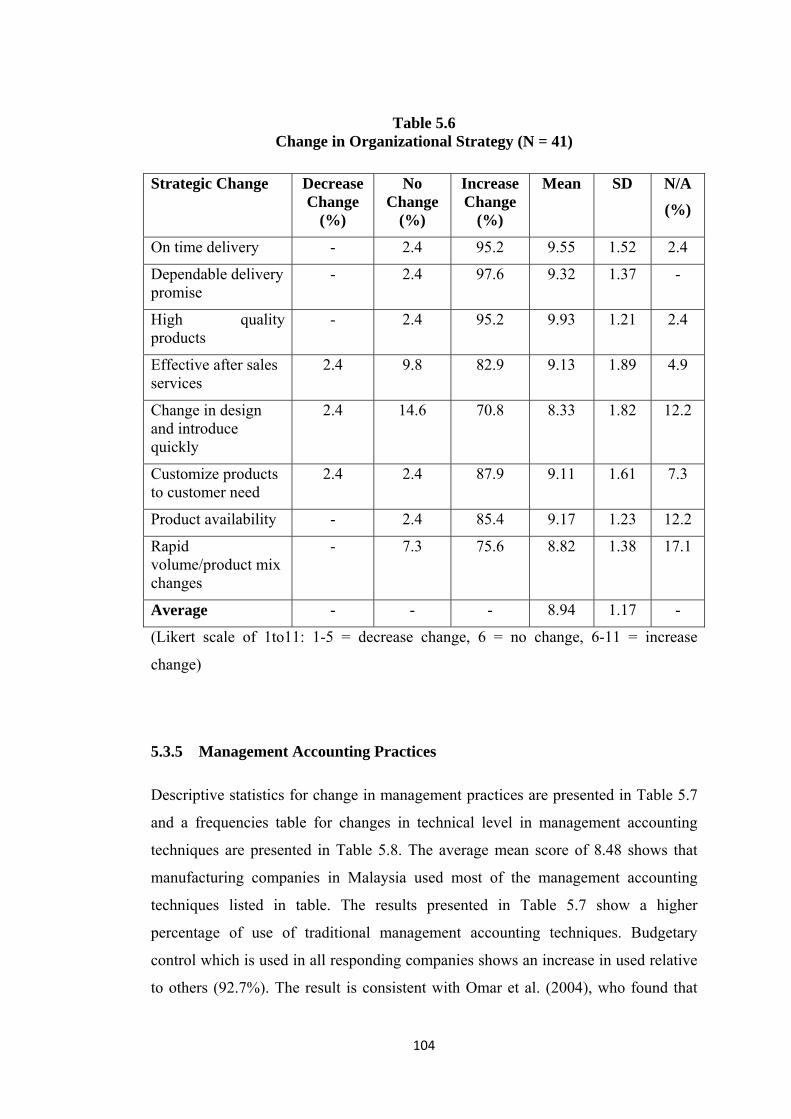

5.3.4 Organizational Strategy ........................................................................... 103

x

5.3.5 Management Accounting Practices ......................................................... 104

5.3.6 Organizational Performance .................................................................... 107

5.3.7 Correlation Matrix for Operational Measures ......................................... 108

5.4 Conclusions and Implications for the Main Study ............................................ 109

CHAPTER SIX: DATA ANALYSIS AND HYPOTHESES TESTING ........... 111

6.1 Introduction ....................................................................................................... 111

6.2 Response and Non-Response Bias .................................................................... 112

6.3 Profile of Responding Companies .................................................................... 113

6.3.1 Industry classification .............................................................................. 114

6.3.2 Company Size .......................................................................................... 114

6.4 Exploratory Data Analysis and Reliability and Validity of the

Measurements ................................................................................................... 116

6.4.1 Competitive Environment ....................................................................... 117

6.4.2 Advanced Manufacturing Technology (AMT) ........................................ 118

6.4.3 Organizational Structures ........................................................................ 119

6.4.4 Organizational Strategy ........................................................................... 119

6.4.5 Management Accounting Practices ......................................................... 120

6.4.6 Organizational Performance .................................................................... 121

6.4.7 Implications for SEM .............................................................................. 123

6.5 Correlations among the Hypothesized Variables .............................................. 124

6.6 Structural Equation Model Analysis and Hypotheses Testing.......................... 125

6.6.1 Hypothesized Model ................................................................................ 127

6.6.2 Model Re-Specification ........................................................................... 131

6.6.3 Assessment of Structural Model Validity ................................................ 135

6.6.4 Hypotheses Testing.................................................................................. 135

6.7 Subsidiary Hypotheses Testing ......................................................................... 138

6.8 Summary ........................................................................................................... 140

CHAPTER SEVEN: DISCUSSION AND CONCLUSIONS ............................. 142

7.1 Introduction ....................................................................................................... 142

7.2 Discussion of Findings ...................................................................................... 144

7.2.1 Changes in Competition, AMT and Structure (H1) ................................ 144

xi

7.2.2 Changes in Competition, AMT and Strategy (H2) ................................. 145

7.2.3 Changes in Competition, AMT and MAP (H3) ....................................... 146

7.2.4 Changes in MAP and Structure (H4) ....................................................... 147

7.2.5 Changes in MAP and Strategy (H5) ......................................................... 148

7.2.6 Impact of Management Accounting and Organizational Change on

Performance (H6-H8) ............................................................................... 148

7.2.7 Technical Level Changes in MAP (H9-H12) ............................................ 150

7.3 Conclusions and Implications ........................................................................... 151

7.4 Contributions to Knowledge ............................................................................. 154

7.4.1 Theoretical contributions ......................................................................... 154

7.4.2 Methodological contributions ................................................................. 155

7.4.3 Practical contributions ............................................................................. 156

7.5 Limitations ........................................................................................................ 156

7.6 Future Research................................................................................................. 157

7.7 Summary ........................................................................................................... 158

REFERENCES ....................................................................................................... 160

APPENDICES....................................................................................................... 175

Appendix A: Information Letter and Questionnaire .............................................. 175

Appendix B-1: Sample Representation .................................................................. 184

Appendix B-2: Demographic Statistics .................................................................. 185

Appendix C: Normality Test for Items of Main Variables ..................................... 186

Appendix D: SEM Output ...................................................................................... 188

xii

LIST OF TABLES

Page

Table 3.1: Summary of Data Collection Procedure 70

Table 3.2: Summary of the Findings of Normality Issue 76

Table 3.3: Guidelines of Establishing Acceptable and Unacceptable Fit 81

Table 5.1: Items Asked in Questionnaire 96

Table 5.2: Descriptive Statistics for Main Variables 99

Table 5.3: Change in Competitive Environment 100

Table 5.4: Change in AMT 101

Table 5.5: Change in Structure 102

Table 5.6: Change in Strategy 104

Table 5.7: Change in MAP 105

Table 5.8: Management Accounting Change Dimensions 106

Table 5.9: Change in Organizational Performance 107

Table 5.10: Correlation Matrix 109

Table 6.1: Descriptive Statistics for Early and Late Respondents 113

Table 6.2: Industry Classification 114

Table 6.3: Results of Descriptive Statistics, Reliability and Validity

(Competitive Environment) 117

Table 6.4: Results of Descriptive Statistics, Reliability and Validity

(AMT) 118

Table 6.5: Results of Descriptive Statistics, Reliability and Validity

(Organizational Structure) 119

Table 6.6: Results of Descriptive Statistics, Reliability and Validity

(Organizational Strategy) 120

Table 6.7: Results of Descriptive Statistics, Reliability and Validity

xiii

(MAP) 121

Table 6.8: Results of Descriptive Statistics, Reliability and Validity

(Performance) 122

Table 6.9: Correlation Matrix among the Constructs 124

Table 6.10: Pearson Correlation Matrix among Hypothesized Variables 125

Table 6.11: Descriptive Statistics for Final Variables 126

Table 6.12: Goodness of Fit Statistics for Hypothesized Model (MLE) 130

Table 6.13: Goodness of Fit Statistics for Modified Model 132

Table 6.14: Goodness of Fit Statistics for Re-Modified Model 134

Table 6.15: Result of Hypothesis Testing 136

Table 6.16: Spearman Correlation Coefficients 139

Table 7.1: Summary of Hypothesis Testing 143

xiv

LIST OF FIGURES

Page

Figure 1.1: Basic Research Model 7

Figure 1.2: Conceptual Model 8

Figure 2.1: Gordon and Miller’s Framework 19

Figure 2.2: A Simplified Model of Contingency Theory 21

Figure 3.1: Basic Survey Process 51

Figure 3.2: Six-Stage Decision Process in SEM 73

Figure 4.1: Hypothesized Model 93

Figure 5.1: Steps Involved in Pilot Study 95

Figure 6.1: Company Size 115

Figure 6.2: Hypothesized Model (WLS) 127

Figure 6.3: Hypothesized Model (MLE) 128

Figure 6.4: Modified Model (Over Fit) 131

Figure 6.5: Re-Modified Model (Good Fit) 133

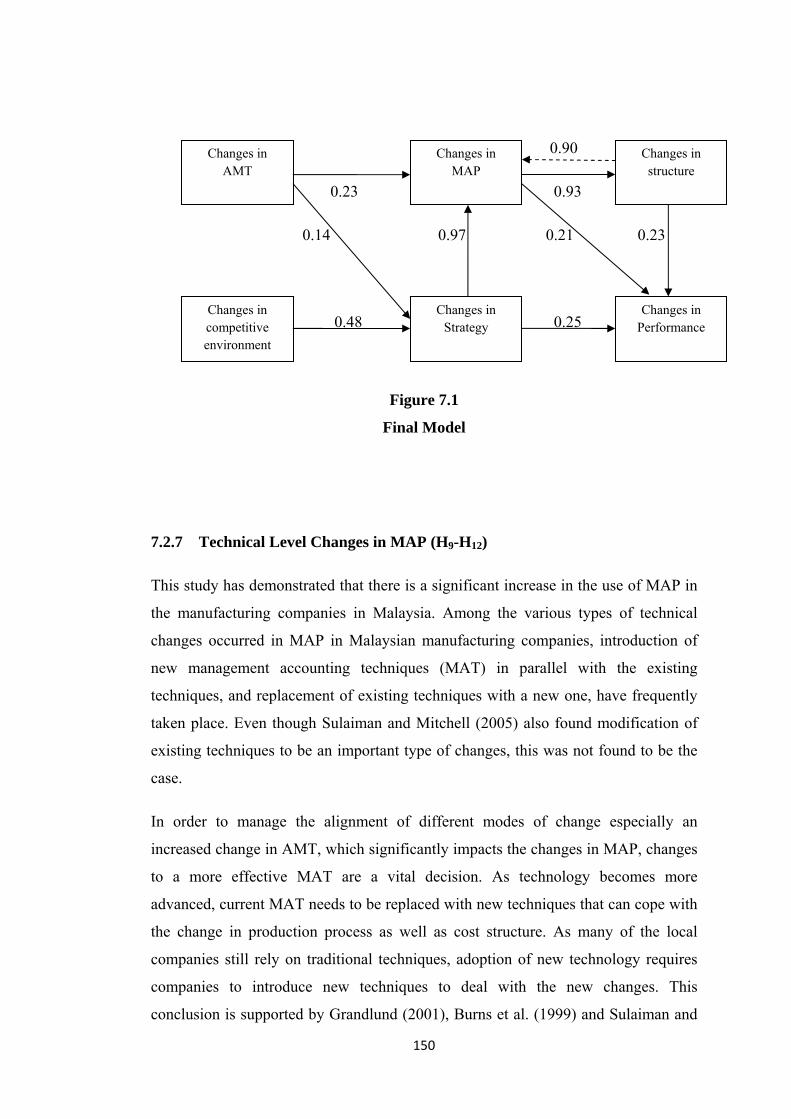

Figure 7.1: Final Model 150

1

CHAPTER ONE

INTRODUCTION AND OVERVIEW

1.1 Introduction

In the search to understand management accounting in competitive environments and

advance technologies, change has increasingly become a focus for research. Many

firms have experienced significant changes in their organizational design,

competitive environments and technologies. Business environments exhibit a variety

of structures and processes, including flat and horizontal organizational forms,

multidimensional matrix structures, networks of “virtual organizations” and self-

directed work teams. When business organizations respond to challenges by

embarking on a change management path, they are faced with choices of which one

of the management methods, techniques, and systems would be most effective

(Waldron, 2005).

Every organization is located within a particular configuration of contingencies. It is

dependent on the market and technological environment in which it operates its scale

and diversity of operations, the technology applied to its work, and the type of

personnel it employs. To achieve congruence, an appropriate design is the one which

best suits its contextual and operational contingencies. According to Moores and

Yuen (2001, p.352), “to be internally consistent, organizations must have tightly

independent and mutually supportive parts in terms of strategies, structures and

2

process”. The management of organizations faces a challenge to reinforce the

management accounting system, strategies and structures together in order to achieve

competitive advantage and enhance performance. Thus, research needs to be carried

out to help management make appropriate decisions in order to achieve this

congruence.

This study examines companies in Malaysia’s manufacturing industry in responding

to the rapid changes in technological and competitive environment in Malaysia as a

result of globalization. Globalization has changed the environment surrounding

organizations operating in developing countries with an increase in uncertainty,

intensified industry competition and advanced technology. According to Kassim,

Md-Mansur and Idris (2003) globalization brings in new technology and makes a

developing country open to greater competition. These changes may affect the choice

of management accounting practice (MAP) in an organization and may also result in

the need for the firm to reconsider its existing organizational design and strategies in

order to fit with the changing environment. This argument is supported by Burns and

Scapens (2000) and Shields (1997), who suggest that changes in environment cause

changes in organizations, which in turn cause changes in MAP.

As the firm strives to achieve a better fit with its environment, and to be more

successful; sustaining and improving current performance will become critical.

However, very limited research has taken place into how changes in technological

and competitive business environments have caused management accounting and

organizational change in developing countries. Most empirical evidence in this area

originates from research in developed countries (Baines & Langfield-Smith, 2003;

Burns, Ezzamel, & Scapens, 1999; Chenhall & Euske, 2007; DeLisi, 1990; Innes &

Mitchell, 1990; Libby & Waterhouse, 1996; Lucas & Baroudi, 1994; J. A. Smith,

Morris, & Ezzamel, 2005).

The next section presents the background and significance of the study, followed by

the research question, research model and research design.

3

1.2 Background and Significance of the Study

The business environment in a developing country differs from that within a

developed country with regards to market size, access to manufactured inputs, human

capital, infrastructure, volatility and governance. According to Tybout (2000),

although some developing economies are quite large, most are not; the menu of

domestically produced intermediate inputs and capital equipment is often limited; a

scarcity of technicians and scientists also affects flexibility in the production process

and the ability to absorb new technologies; infrastructure is relatively limited;

macroeconomic and relative price volatility is typically more extreme; legal systems

and crime prevention are also relatively poor; and corruption is often a serious

problem.

Malaysia is categorised as the developing country, however it has more advanced

infrastructure and technology compared to most other developing countries.

Malaysian manufacturing industries are also more concentrated than those of most

developed countries (Bhattacharya, 2002). With globalization, the application of

technology in Malaysia has increased, especially through foreign investment (Kassim

et al., 2003). Changes in business environment in Malaysia arising from a market-

oriented economy and government policies that provide businesses with the

opportunity for growth and profits, have made Malaysia a highly competitive

manufacturing and export base.

On the whole, manufacturing industries are the most active and important

contributors to the Malaysian economy after the services sector. In 2006 the

manufacturing sector contributed 31.1% of the total GDP, and 29.1% of total

employment1. In addition, Malaysia’s rapid move from a production-based economy

(p-economy) towards a knowledge-based economy (k-economy) allows companies

to do business in an environment that is geared towards information technology2. The

advance of technology through ICT and computerization has also made management

accounting information flow within organizations in this country more useful, timely,

accurate, and relevant (Omar, Abd-Rahman, & Sulaiman, 2004).

1 Source: FMM directory 2008 Malaysian Industries. 2 Source: Malaysia Industrial Development Authority (MIDA), http://www.mida.gov.my.

4

In developing countries, the manufacturing sector often receives preferential

treatment from policy makers. According to Tybout (2000), most developing

countries’ government promote manufacturing with special tax concessions and

relatively low tariff rates for importers of manufacturing machinery and equipment.

It is also argued that government policies often favour large firms; even when

policies do not explicitly favour large firms, these firms may enjoy de facto

advantages, because sectors with large capital-intensive firms lobby the government

more effectively (Tybout, 2000). Malaysia has industrialized rapidly in the last 20

years, and the confidence gained from this experience has led its leader to formulate

Vision 2020 and k-economy. However, Malaysia’s path to being an industrialized

country has not been based on strong domestic producers but has instead relied on

foreign multinationals to produce for export (Rasiah, 1995).

Based on the distinctive features of market size, access to manufactured inputs,

human capital, infrastructure, volatility and governance, as discussed above, it can be

concluded that the business environment in Malaysia is quite volatile from both

regulatory and macroeconomic perspectives as compared to developed countries,

especially Western countries like U.K., U.S. and Australia. Moreover, as

organizations grow through expanding their range of products or services in response

to more mature and saturated markets, they inevitably confront an increasingly

hostile environment (Moores & Yuen, 2001). But, if there is substantial uncertainty

about future demand conditions for these products, it often makes sense to choose

production techniques that do not lock one into a specific technology; that is, to rely

more heavily on labour (Tybout, 2000). This is because investment in fixed capital

involves long-term commitments to particular products and production volume.

Therefore, manufacturing firms in Malaysia may respond to the changes in

environment in different ways than firms in those countries. Even though much

research on management accounting and organizational change has been carried out

in Western countries like U.K, U.S and Australia, because of these differences,

empirical evidence obtained from research in these countries cannot necessarily be

generalized to the Malaysian environment.

Moreover, the introduction of fast information technology within which firms in

manufacturing industries in Malaysia operate has greatly affected the technological

5

environment. Much literature has identified technological advancement, active

competitors and demanding customers as potential predictors of organizational and

management accounting change (Baines & Langfield-Smith, 2003; Dibrell & Miller,

2002; Innes & Mitchell, 1990; Kaplan & Norton, 1996; Shields, 1997; Waweru,

Hoque, & Uliana, 2004). This aspect is important because the management

accounting system (MAS) requirement can vary significantly depending on how well

known the causes of change in the external environment and their indicators are to

the organization. This argument is supported by Waweru et al. (2004), who found

that an increase in global competition and changes in technology were the two main

contingent factors affecting management accounting change in South Africa. Apart

from these external organizational factors, previous studies also found that contextual

variable factors inside the organizations also have a connection to management

accounting change. As suggested by Moores and Yuen (2001), support from

strategies and structures are important to ensure a consistency in an organization.

Strategy and structure have also been identified in the previous literature as the most

important factors in management accounting change process. Thus, this study is

conducted to further investigate these relationships.

Unlike developed countries, MAP in developing countries may be gained through

“importing” management accounting systems in the manner adopted by foreign

companies establishing operations in developing countries (Abdul-Rahman, Omar, &

Taylor, 2002; Chow, Shields, & Wu, 1999). For example in Malaysia, local

manufacturing companies are still using traditional methods compared to

multinational corporations such as Japanese-owned companies, which mainly use

new management accounting techniques (Abdul-Rahman et al., 2002). Furthermore,

little research has been done in developing countries (see for example, Hoque &

Hopper, 1994; Waweru et al., 2004) and even fewer studies in Asian countries like

Malaysia (e.g., Abdul-Rahman, 1993; Nor-Aziah & Scapens, 2007). These factors

provide further motivation to carry out this research in Malaysia so that it can

contribute to a better understanding of the adoption of changes in organizational and

MAS in a developing country context.

Further, this study attempts to provide incremental contributions to the management

accounting change literature by explaining how organizations implement

6

management accounting innovations, or how redesign of their existing MAS can

improve organizational performance3 (Baines & Langfield-Smith, 2003; Chenhall,

2003; Hyvönen, 2007; Libby & Waterhouse, 1996; Mia & Clarke, 1999; Otley,

1980). Therefore, by looking into the performance implications of the possible

alignment between change in MAS and organizational factors within environmental

uncertainty, the findings of this study will make a significant contribution to

management accounting theory and literature as well as providing guidance for

decision makers, professionals and practitioners.

1.3 Research Question

In its broadest form, the proposed research will address this overall research

question:

“How does the alignment of the management accounting system with

organizational factors improve performance?”

In addressing this primary question, the study will concentrate on the influences of

technology and the competitive business environment on MAP, organization

structure, strategy and the impact of these changes on performance. More

specifically, this study addresses the following research questions:

1. What is the level of changes that have taken place in competitive

environment, manufacturing technology, MAP, structure and strategy in

Malaysian manufacturing companies?

2. How do changes in the competitive business environment and manufacturing

technology in Malaysia manufacturing companies influence the changes in

MAP, organizational structure and strategy?

3. In what ways do changes in MAP, organizational structure and strategy relate

to each other and to what extent will these changes take place?

4. What changes have been made to MAP in organizations facing changes in

3 Detail on this topic is discussed in the literature review chapter.

7

their configurations?

5. In what ways do the alignment among MAS and other organizational factors

influence performance?

1.4 Research Model

The literature review on management accounting and organizational change

presented in Chapter Two suggests the basic framework as presented in Figure 1.1.

Figure 1.1

Basic Research Model

Taking into account different factors which influence organizational and

management accounting change (as explained in Chapter 2), the basic model can be

refined and developed to fit the current study by focusing on the specific

environmental and organizational factors that can influence changes and performance

of an organization, as follows:

ORGANIZATIONAL

CHANGE

MANAGEMENT

ACCOUNTING CHANGE

CHANGES IN

ENVRONMENT

ORGANIZATIONAL

PERFORMANCE

8

Figure 1.2

Conceptual Model

1.5 Study Design

A review on management accounting and organizational change literature shows

some relatively neglected areas. For example the study by Baines and Langfield-

Smith (2003) examined the relationships between the changing competitive

environment, and a range of organizational variables as antecedents to management

accounting change. However, their study was based on the assumption of

unidirectional relationships between the variables. The literature review suggests that

some relationships are in the opposite direction, or even have reciprocal or reverse

causation, which will be further tested by this research. Some new relationships, not

tested by Baines and Langfield-Smith (2003), will also be tested in this study: the

cause of changes in competitive environment with management accounting practices,

changes in technology on organizational strategy, changes in organizational structure

on MAP and the impact of changes in management accounting practices,

organizational structure and strategy on performance. Although Baines and

Changes in

Manufacturing

Technology

Changes in

competitive

environment

Changes in

Organizational

Strategy

Changes in

organizational

structure

Changes in

MAP

Changes in

Organizational

Performance

9

Langfield-Smith (2003) examined the relationships amongst competitive

environment, technology, organizational design, advanced management accounting

practice, and change in reliance on non-financial management accounting

information, they only consider the direct relationship between greater reliance on

non-financial management accounting information and organizational performance.

They did not explore an interaction effect of this relationship on firm performance. A

study by Mia and Clarke (1999) also only indicates the moderating role of the use of

management accounting information on the relationship between the intensity of

market competition and business unit performance, and not the effect on firm

performance.

Based on the contingency fit argument, it can be argued that organizations are likely

to perform effectively if they implement MAS that suit their organization’s

situational factors in an uncertain environment. This suggests a two-way interaction

effect on firm performance between the change in MAS and organizational factors.

Thus, a reverse causation relationship between MAP and organizational factors is

tested in this study. In their study, Baines and Langfield-Smith (2003) also measured

organizational change by means of managers’ perception over a three-year period.

However, it may take organizations more than three years to make substantial

changes in investments in advanced manufacturing technology, or change their use

of MAP, in response to changes in the competitive environment. This study provides

a more detailed survey to capture the time lag between various organizational

changes, which is five years.

Kober, Ng and Paul (2007) studied the interrelationship between management

control systems and strategy in Australian organizations. Their analysis confirmed

the existence of a two way relationship between management control systems and

strategy, whereas, Chenhall and Langfield-Smith (1998b) examined how

combinations of management techniques and MAP enhance the performance of

organizations, under particular strategic priorities. This study extends these

contributions by investigating how the alignment between MAP, organization’s

strategy and structure can improve performance. The extension adds several

refinements to earlier studies, designed to add to the explanatory power of the prior

research. Therefore, a theoretical advance in knowledge can be achieved.

10

Using both contingency and institutional theory, this study contributes to an

elaboration of how the alignment of the MAS with organizational structure and

strategy can contribute to performance improvement in manufacturing firms in

Malaysia. Through providing a better understanding of these relationships, the study

can help practitioners to make better decisions in the face of a changing environment,

as well as helping the organization to overcome barriers to change. Moreover, it also

contributes to the improvement in organizational performance and competitive

advantage. Besides providing more helpful insights to practitioners, the theoretical

framework developed and tested in this study contributes to the organizational and

management accounting change literature.

This is an empirical research study. It is noted that few empirical research studies

have been conducted on this topic (Baines & Langfield-Smith, 2003; Libby &

Waterhouse, 1996; Sulaiman & Mitchell, 2005). Baines and Langfield-Smith (2003,

p. 675) noted that “there has been limited empirical research examining the nature of

the changes in MAS and organizational variables in response to environmental

changes, and whether or not these changes improve performance.” The current study

represents an attempt to fill such an apparent gap in prior research.

This study used a mailed survey of manufacturing companies registered with the

Federation of Malaysian Manufacturers (FMM). The selection of the manufacturing

industry for this study was due to the fact that this industry is known to have rapid

changes in technological and competitive environment. A survey questionnaire is

used as the main method of data collection to examine how changes in competitive

environment and advanced technology cause changes in organization’s design,

strategy and MAP, and how alignment among these variables impacts on

performance. This is a causal study and it attempts to examine how one variable

affects changes in other variables and how these variables are responsible for

changes in organizational performance. The design of the questionnaire for the

study will cover six major areas within the conceptual model and hypotheses, i.e.

competitive environment, advanced manufacturing technology, MAP, organization

structure, strategy, and performance.

The remainder of the thesis is organized as follows. Chapter 2 draws on previous

research to identify the different dimensions of change, causal factors and change

11

process. The adoption of the survey research method and research instruments are

explained and justified in Chapter 3, whereas the hypotheses for this study are

elaborated in Chapter 4. The discussion of findings for the pilot test is provided in

Chapter 5. Data analysis and hypotheses testing for this study are presented in

Chapter 6. Finally, the detailed discussion of the findings is presented in Chapter 7,

together with the conclusions and implications of the findings, its contribution to the

body of knowledge in this area, limitations, and also some recommendations for

future research.

12

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter reviews the research literature on management accounting and

organizational change. It provides the basis for the design of the research conducted

both in terms of research methods used and the aspects of change upon the study.

This chapter is divided into nine sections. The first section discusses management

accounting and organizational change dimensions. This is followed by a discussion

of management accounting change process, the external environment and

technology, as well as a discussion of the relationship among competitive

environment, technology, organizational and management accounting change. The

final sections discuss aspects of performance with management accounting and

organizational change, together with a summary.

2.2 Management Accounting and Its Evolution

The basic purpose of accounting information is to help users make decisions.

Management accounting is branch of accounting that produces information for

managers and forms an important integral part of the strategic process within an

organization. It involves the process of identifying, measuring, accumulating,

13

analysing, preparing, interpreting, and communicating information that helps

managers fulfil organizational objectives (Horngren, Sundem, Stratton, Burgstahler,

& Schatzberg, 2007). Chartered Institute of Management Accountants (UK) views

management accounting as an integral part of management which requires the

identification, generation, presentation, interpretation and use of information relevant

to:

- formulating business strategy;

- planning and controlling activities;

- decision-making;

- efficient resource usage;

- performance improvement and value enhancement.

Johnson and Kaplan (1987) argued for a ‘relevance lost’ in management accounting.

They pointed the issue of inappropriateness of conventional management accounting

techniques which offered little capacity for providing useful and timely information

for better decision and control in the contemporary environment of rapid

technological change and vigorous competition. Following Johnson and Kaplan

(1987), management accounting techniques had rapidly developed for better

decision-making and management control.

To promote a better understanding of the changes in management accounting

practices, the International Federation of Accountants (IFAC) (1998) provides a

framework explaining the development of management accounting. This framework

explains the evolution in management accounting through four recognisable stages.

As explained by Omar et al. (2004, p. 27), the primary focus of each stage are:

Stage 1 (prior 1950)

During this period, most companies were focusing on cost determination, which was

related to stock valuation and the allocation of overheads. Some of the management

accounting techniques that were developed for cost estimation were Last In First Out

(LIFO) and First In First Out (FIFO). Cost estimation was justifiably emphasized

because by estimating the cost, managers were able to control their financial

position.

14

Stage 2 (1965-1985)

By 1965, companies had moved into generating information for the purpose of

management planning and control. This was important because only valuable

information could induce managers to make correct decisions. Management

accounting techniques such as marginal costing and responsibility accounting were

introduced during this stage to help managers to choose the correct course of action

or create strategic business units respectively.

Stage 3 (1985-1995)

Increased global competition accompanied by rapid technological development in the

early 1980s affected many aspects of the industrial sector. During this stage, the

management focus remained on cost reduction, but more process analysis was made

possible by cost management technologies. The aim was basically to reduce waste

when processing the product because this could reduce the expenses incurred, thus

increasing expected profit. Some of the techniques popularly practiced by companies

at this stage include Just in Time (JIT) and Activity-Based Costing (ABC).

Stage 4 (1995 onwards)

In the 1990s world-wide industry continued to face considerable uncertainty and

unprecedented advances in manufacturing technologies, which further increased and

emphasised the challenge of global competition (Abdel-Kader & Luther, 2008). In

this stage, companies focused on enhancing the creation of value through the

effective use of resources. Basically, managers tried to identify factors of drivers that

could potentially increase shareholder value. As such, non-value added activities

were deliberately eliminated. Among the popular techniques introduced during this

stage were Total Quality Management (TQM), Activity-Based Management (ABM),

Benchmarking and Reengineering.

Even though the management accounting evolution can thus be distinguished into

four stages, it is important to note that the techniques used in previous phases

continued to be used in subsequent stages. This is consistent with a view that

traditional and advanced management accounting practices tend to complement each

other (Chenhall & Langfield-Smith, 1998b).

15

2.3 Management Accounting Change

Management accounting change is not a uniform phenomenon. Consequently one

might expect the causal factors of change to be varied and this has indeed been

confirmed by management accounting researchers. It is evident that both the external

factors (environmental) and internal factors (relating to the organization concerned)

have influenced the recent development of new management accounting systems and

techniques. According to Shields (1997), the potential change drivers are

competition, technologies, organizational design and strategies. These drivers of

change also indicate the differing roles which causal factors can have in the process

of change. Change in environment also implies uncertainty and risk which create a

demand for further management accounting change in the form of ‘non-financial’

measures (Vaivio, 1999). Less attention has been given by researchers to the

management accounting change process. Burns and Scapens (2000, p. 4) observed

that, “little research attention has been given to understanding the processes through

which new management accounting systems and practices have emerged (or failed to

merge) through time”.

Change can be addressed in a variety of dimensions. According to The American

Heritage Dictionary, 4th Edition, change includes all of the following aspects:

becoming different or undergo alteration; transformation or transition; going from

one phase to another; making an exchange; modifying; substitution; giving and

receiving reciprocally; replace with another; abandon. This definition illustrates

different types of change and shows that, in general, it is not a uniform phenomenon.

Wickramasinghe and Alawattage (2007) suggest change in management accounting

as a learning methodology to understand how environmental factors shape internal

process within organization. According to them, the process of change reflects on the

question of how management accounting techniques emerged, evolved and were

transformed when new demands from the changing environment are in place.

From a management accounting perspectives, different types of change can be

researched upon. For example Sisaye (2003) study change with respect to the

integration of Activity Based Costing (ABC) into strategy to manage organization’s

16

operating activities. It is suggested that ABC can contribute to improve

organizational performance if implemented as part of the overall organizational

change strategy. Perera, McKinnon and Harrison (2003), examined changes in term

of introduction, abandonment and reintroduction of transfer pricing in government

trading enterprise as it moved from protected monopolistic status to

commercialization.

Many researchers have shown an interest in understanding management accounting

change (Baines & Langfield-Smith, 2003; Chenhall & Langfield-Smith, 1998b; Innes

& Mitchell, 1990; Libby & Waterhouse, 1996). For example Chenhall and

Langfield-Smith (1998b) have explored the benefit of management accounting

change, but less is known about the forces that induce this change (Laitinen, 2006).

The reasons for management accounting to change are termed “motivational factors”

(Laitinen, 2006). Many researchers have suggested a substantial list of motivational

factors (Baines & Langfield-Smith, 2003; Laitinen, 2001; Libby & Waterhouse,

1996). For example, Innes and Mitchell (1990) found a different set of circumstances

linked with management accounting change, which they termed as follows:

- Motivators (e.g., competitive market, organizational structure, and product

technology)

- Catalyst (e.g., poor financial performance, loss of market share,

organizational change)

- Facilitators (e.g., accounting staff resources, degree of autonomy, accounting

requirements)

The interaction between these variables promotes change not only in management

accounting but also other related disciplines4 (Innes & Mitchell, 1990; Laitinen,

2006). Laitinen (2001) classified these factors in six groups: information needs;

changes in technology and environment; willingness to change; resources for change;

objectives for change; and external requirements. Laitinen (2006), on the other hand,

used four categories of factors to explain management accounting change:

organizational factors; financial factors; motivational factors; management tools.

While, various factors have been associated with management accounting change,

4 For example in organizational study related to structure and strategy.

17

this study considers three factors, i.e., motivational factors, organizational factors and

financial factors. Changes in environment and technology are used as motivational

factors in explaining management accounting change and changes in organizational

factors (i.e., structure and strategy). Besides that, organizational structure and

strategy (organizational factors) are considered as contextual factors inside the firm

that may have a connection to change in management accounting (Moores & Yuen,

2001). Financial factors are used as outcomes of management accounting and

organizational change. Grandlund (2001) suggested that low financial performance

may put economic pressure on the firm to change its MAS to increase performance.

Baines and Langfield-Smith (2003) suggested that if management accounting change

is accompanied with a greater reliance on accounting information, it may result in

improved performance. Thus, financial performance may be an antecedent or an

outcome factor of management accounting change.

Many firms have experienced significant changes in their business environment with

advances in information technology, highly competitive environments, new

management strategies, and a greater focus on quality and customer services. Many

relevant management accounting studies have highlighted the significant changes in

these operating environments (e.g., Burns & Vaivio, 2001; Choe, 2004; Gomes,

Yasin, & Lisboa, 2007; Haldma & Laats, 2002; Hopwood, 1990; Hussain & Hoque,

2002; Innes & Mitchell, 1995; Kaplan & Norton, 1996; Libby & Waterhouse, 1996;

Scapens, 1999; Vamosi, 2003) which have influenced the choice of which

management accounting systems and techniques would be most effective (Waldron,

2005) and engendered the organization to reconsider its design and strategy (Baines

& Langfield-Smith, 2003) in maintaining and/or improving performance (Chenhall

& Langfield-Smith, 1998a; Choe, 2004).

Organizational change is a central issue within organizational theory, management

and accounting. Hopwood (1987, p. 207) claimed that ‘very little is known of the

processes of accounting change’. This has provoked controversy over the theory of

why and how changes are occurring. As argued by Quattrone and Hopper (2001, p.

404), ‘what the concept of change means, whether it can be conceptualized

independently from its process and how these factors relate to the practice of

accounting is taken for granted and is poorly understood. Researchers have

18

commended various theoretical frameworks to explain these accounting changes, e.g.

Gordon and Miller (1976) commend contingency theory whereas Burns and Scapens

(2000) proffer old institutional economic theory (OIE). Contingency theory

explained how changes in an environment surround organization causes changes in

organizational factor as well as its accounting practice and decision making process.

Whereas old institutional economic theory suggest how accounting and organization

can change through the process of institutionalization.

Management accounting research has used a variety of theoretical frameworks to

explain the changes. This study uses both contingency and institutional theory to

explain a need for a good fit between the MAS, external environment and

organizational aspects, to improve performance. This is similar to other studies on

management accounting and organizational change which also use contingency

theory (for example, Baines & Langfield-Smith, 2003; Haldma & Laats, 2002;

Hyvönen, 2007). The following sub-sections summarise the process of management

accounting change from each perspective.

2.3.1 Contingency Theory

Contingency theory is paramount to explain how accounting systems might be

affected by the fit between environmental and organizational factors. Central to the

contingency approach in examining these relationships is the notion of fitness.

Contingency is defined by the Oxford dictionary as:

“The relationship between behaviour and the consequences that is dependent

on that behaviour”.

Contingency theory posits that an appropriate match between organizational

characteristics to contingencies will improve organizational effectiveness (Morton &

Hu, 2008). Donaldson (2001, p. 7) defined “Contingency” as “any variable that

moderates the effect of organizational characteristics on organizational

performance”.

19

In the contingency theory of organizations, there is no universally acceptable model

of the organization that explains the diversity of organizational systems design.

Gordon and Miller (1976) suggested the usefulness of contingency theory for

developing effective management accounting systems. Gordon and Miller (1976)

proposed that the design of accounting information systems should be dependent on

firm-specific contingencies where environmental, organizational and decision style

variables could contribute to understanding such systems (see Figure 2.1).

Figure 2.1

Gordon & Miller’s Framework

Gordon and Miller (1976) also suggested operational measures for each component

of the model. The environmental measures include dynamism, heterogeneity and

degree of differentiation, bureaucratization, available resources, and integration

through committees, rules or policies.

A contingency perspective suggests that effective management accounting systems

should align with both internal and external factors. Depending on the match

between management accounting system characteristics and these various factors

affecting the organization, different levels of effectiveness might be witnessed.

Waterhouse and Tiessen (1978) expanded the organizational context to include both

environmental and technological factors, while Simons (1987) incorporated business

strategy into these measures.

Environment

Accounting Information

System

Organization

Decision

making

style

20

The identification of contextual variables in this study is traced from the original

structural contingency frameworks developed within organizational theory. Early

accounting researchers focused on the impact of environment and technology on

organizational structure (Otley, 1980; Waterhouse & Tiessen, 1978). According to

Chenhall (2007), a new research stream is related to the role of strategy. It has been

incorporated in the traditional organizational model which suggests important links

with environment, technology, organizational structure and MCS.

Over the last few decades, a number of innovative management accounting

techniques have been developed. This innovation is needed to support modern

technologies and new management process. As noted by Abdel-Kader and Luther

(2008, p. 3), “the new techniques have affected the whole process of management

accounting (planning, controlling, decision making and communication) and have

shifted its focus from a ‘simple’ role of cost determination and financial control, to a

‘sophisticated’ role of creating value through the deployment of resources”. It also

has been argued that these ‘new’ accounting techniques are important in the search

for a competitive advantage to meet the challenge of global competition. Thus, to

adapt to these technological development and competitive environment, firms must

design a MAS that is congruent with the new requirements (Gerdin, 2005). However,

it is also noted that few organizations have adopted these new techniques. As cited

by Abdel-Kader and Luther (2008), Tillema (2005) explain the appropriateness of

using advanced techniques is dependent on the circumstances in which these

techniques are being used and this gives rise to the need for a contingency theory

perspective.

Many researchers suggest that an appropriate accounting system depends upon

organizational contextual variables (Gordon & Miller, 1976; Otley, 1980;

Waterhouse & Tiessen, 1978). For example, Otley (1980) proposed the need to

identify specific aspects of an accounting system associated with certain defined

circumstances and demonstrate an appropriate matching. The contingency approach

to management accounting is based on the premise that, there is no universally

appropriate MAS that applies equally to all organizations in all circumstances

(Waterhouse & Tiessen, 1978). Thus, the complex relationship between MAS, its

contextual variables and its impact on organizational performance has attracted

21

numerous researchers to investigate this issue (Baines & Langfield-Smith, 2003;

Jermias & Gani, 2002; Laitinen, 2006). Figure 2.2 shows a simplified contingency

model by Weill and Olson (1989) which could be used to explain this contingent

relationship.

Drawing upon a structural contingency theory of management accounting, this study

examines how technology and environmental factors determine the degree of

changes in MAS and organizational factors (strategy and structure). Further, this

study examines whether firm performance is contingent on the alignment of

management accounting change with the organizational factor in technological

development and competitive environment.

Figure 2.2 A Simplified Model of Contingency Theory

in Organizational Research

2.3.2 Institutional Perspectives

Institutional theory is an adaptive change process framework. It examines the impact

of external environment factors and market conditions on organizational change and

development (Barnett & Caroll, 1995). Using institutional theory, Burns and Scapens

(2000) have conceptualized management accounting change as change in

organizational rules and routines. Under old institutional economic (OIE) theory,

management accounting is conceived as a routine, and potentially institutionalized,

ENVRONMENT PERFORMANCE

ORGANIZATIONAL SUBUNIT

ORGANIZATIONAL SUBUNIT

22

organizational practice. By being institutionalized, management accounting practices

can both shape and be shaped by institutions which govern organizational activity.

Within OIE theory, institution is defined as:

“a way of thought or action of some prevalence and permanence, which is

embedded in the habits of a group or the customs of a people” (Burns &

Scapens, 2000, p.5).

In OIE there are three dichotomies which offer insights into the process of

management accounting change. They are: (1) formal versus informal change;

revolutionary versus evolutionary change; and (3) regressive versus progressive

change (Burns & Scapens, 2000). The formal versus informal change dichotomy will

be used in this study as it is the most appropriate for explaining the reciprocal

relationship between management accounting and organizational change. Formal and

informal management accounting change is used to imply that change is not

specifically directed (formal change), but may evolve out of the intended actions of

the individuals who are enacting and reproducing organizational routines (informal

change). In this study, organizational routines are referred to as organizational

structure and strategy. On the other hand, the other two dichotomies, i.e.,

revolutionary versus evolutionary change, and regressive versus progressive change,

involve a disruption to existing routines and institutions, and focus on a value system

in management accounting changes process, which will not be examined in this

study.

Formal change occurs through the introduction of new management accounting

systems and techniques, which in turn, engender the organization to change. In

contrast, informal change occurs when change in an organization’s operation

condition (i.e. organizational activity such as ownership structure or production

technology) creates the need for change in management accounting practice. Hassan

(2005) provides evidence on formal change. He shows how management accounting

is acted upon to disrupt the hospital’s micro institutions and routines, challenge

physicians’ professional and bureaucratic power and therefore bring change to a

public hospital. J. A. Smith et al. (2005) show the occurrence of informal change

where, organizational change, as effected by the use of outsourcing, causes specific

changes to take place in the organizations' management accounting systems. Both

23

findings provide evidence of a reciprocal relationship between management

accounting and organizational change, where change in management accounting

practices can influence the organization to change (formal change) and change in

organizational activity also can influence management accounting practices to

change (informal change).

The management of change suggests how management accounting change is

intertwined with a changing organizational design and strategy; these have been the

most consistently used organization characteristic and variable in past research (e.g.,

Chenhall, 2003; Lapsley & Pallot, 2000). According to Sisaye (2003), the

institutional approach to organizational change which suggests that organizational

structures, that affect an organization’s learning strategy and ability to adapt changes

in the external environment, provide the context for at least two types of

organizational change strategies: gradual-incremental and revolutionary-radical. In

this case, the institutional framework maintains the view that organizations

irrespective of their structural arrangements, can successfully change if they

implement adaptive strategies of either incremental or radical change to bring about

process innovation changes. Ma and Tayles (2009) in their case study of the

emergence of strategic management accounting is also used institutional framework

to interpret the external and internal influences on the change in management

accounting techniques in their studied organization.

2.4 Changes in Competitive Environment and Advanced

Manufacturing Technology

Environment can be broadly characterized as phenomena that are external to the

organization and which have either potential or actual influence on the organization

(Macy & Arunachalam, 1995, p.67). The external environment may thus relate to

technology, law, politics, economics, culture and demographics. According to

Chenhall (2007, p. 172), environment refers to “ particular attributes such as intense

price competition from existing or potential competitors”. Uncertain environment,

which is impacted from high competition, is an important contextual variable in

contingency-based research.

24

Globalization has changed external environmental factors in developing countries,

which in turn affect the internal operations of organizations as well as their

management accounting practices. This relationship is explained using contingent

theoretic arguments that changes in management accounting practices and internal

operations of organizations are contingent on the “fit” with changes in the external

environment that surrounds them (for a review, see Abdel-Kader & Luther, 2008;

Haldma & Laats, 2002; Macy & Arunachalam, 1995). Competitive environment and

technology advancement have generally been assumed in the literature, to influence

the manufacturing company to change its management accounting practices, as well

as its organizational design and strategies. However, there is little empirical research

to support such relationships and little, if any, research has been conducted in the

context of developing countries.

This study investigates how the alignment between the adoptions of management

accounting practices with organizational structure and strategy in a competitive

environment with advanced technology, influence performance. As compared to a

developed country, Malaysia is categorized as an ‘uncertain’ country, with rapid pace

of change and which has the opportunity for economic growth. Fluctuating interest

rates, inflation, exchange rate and stock exchange indices, are evidence of a business

environment in Malaysia which is volatile. Increased economic uncertainty is an

important cause of changes in management accounting practices5 (Luther &

Longden, 2001). Mia and Clarke (1999) found a positive relationship between the

intensity of market competition and the usefulness of management accounting

information.

The pressure of management accounting and organizational change may come from

the environment of the firm. The most obvious environmental factor is market

competition (Hoque, Mia, & Alam, 2001; Libby & Waterhouse, 1996; Mia & Clarke,

1999). Literature has identified that organizations which operate in competitive

business environment tend to change their management accounting practices,

organizational structures and strategy in order to succeed (e.g., Baines & Langfield-

Smith, 2003; Chenhall & Morris, 1986; Chong & Chong, 1997; Libby &

5 Luther and Longden found that the mean response to the importance of increased uncertainty of the economic environment as a cause of changing management accounting practices in South Africa (high economic uncertainty) is higher than in the UK (more certain economic).

25

Waterhouse, 1996; Luther & Longden, 2001; Mia & Clarke, 1999; Pratt, 2004;

Waweru et al., 2004). For example, Luther and Longden (2001) found evidence that

the organization’s ability to sell abroad and to compete against imports changed

managerial and business practices, forcing change in management accounting.

Technology also becomes an important aspect of management accounting and

organization research drawing on the manufacturing sector. Previously, issues

concerning the role of MAS within advanced manufacturing settings such as Just-In-

Time (JIT), Total Quality Management (TQM) and Flexible Manufacturing (FM)

have been explored. According to Emmanuel, Otley and Merchant (1990),