managing for growth - taking hsbc to the next level

TRANSCRIPT

Managing for growthTaking HSBC to the next levelPrepared for

Merrill Lynch Conference – London – October 2006

Michael GeogheganGroup Chief Executive Officer

Forward-looking statements

This presentation and subsequent discussion may contain certain forward-looking statements with respect to the financial condition, results of operations and business of the Group. These forward-looking statements represent the Group’s expectations or beliefs concerning future events and involve known and unknown risks and uncertainty that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Additional detailed information concerning important factors that could cause actual results to differ materially is available in our Annual Report.

Story so far… does it tell all?

0

500

1,000

1,500

2,000

2,500

3,000

Jun-91 Jun-94 Jun-97 Jun-00 Jun-03 Jun-06

Total shareholder return

90

100

110

120

130

140

Jul-04 Nov-04 Apr-05 Aug-05 Jan-06 Jun-06

HSBC TSR – two years, 13% CAGRHSBC TSR – 15 years, 25% CAGR

HSBC – record of growthDividends per share/earnings per share

0

20

40

60

80

100

120

140

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

DPS EPS

(US cents)

UK GAAP (excl goodwill amortisation) IFRS

Asian crisis Argentinean crisis

EPS + 25% CAGR

EPS + 15%

DPS1

16% CAGR 1995-2005

(1) DPS are in respect of periods shown above

HSBC half year results

9.48.7Tier 1 ratio (%)

+70.300.28Dividends per share (US$), first and second interim dividends

+130.780.69Earnings per share (US$)

+158,7297,596Profit attributable to shareholders

+1812,51710,640Profit before tax

+12(16,139)(14,420)Total operating expenses

+1428,29524,752Net operating income

+1532,18528,029Net operating income before loan impairment charges

% changeH106H105US$m

Has HSBC got too much capital and should it be returned to shareholders?

US$93bn

US$97bn

US$102bn

70

80

90

100

110

H104 H204 H105 H205 H1065

10

15

20

Average invested capital employed (US$bn) Return on invested capital (%) Tier 1 ratio (%)

24% annualised return fromadditional US$9bn of capital

(US$bn)

Improving capital efficiency

(%)

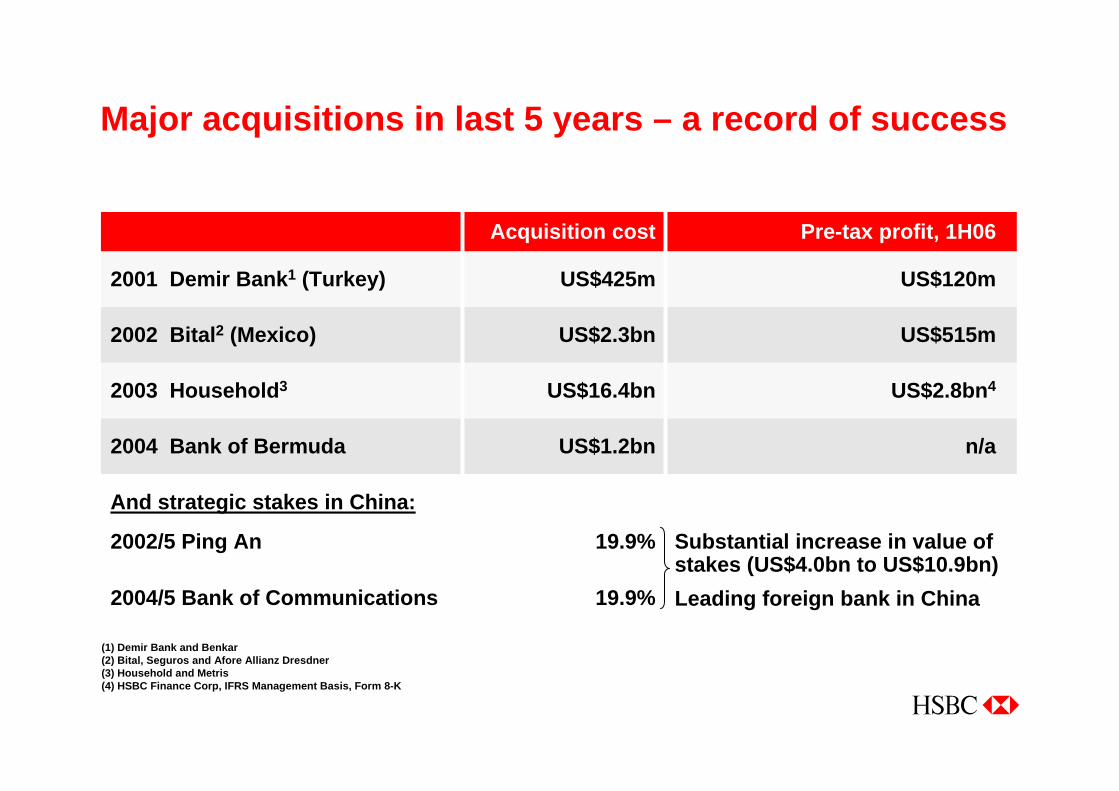

Major acquisitions in last 5 years – a record of success

n/aUS$1.2bn2004 Bank of Bermuda

US$2.8bn4US$16.4bn2003 Household3

US$515mUS$2.3bn2002 Bital2 (Mexico)

US$120mUS$425m2001 Demir Bank1 (Turkey)

Leading foreign bank in China19.9%2004/5 Bank of Communications

Substantial increase in value of stakes (US$4.0bn to US$10.9bn)

19.9%2002/5 Ping An

And strategic stakes in China:

Pre-tax profit, 1H06Acquisition cost

(1) Demir Bank and Benkar(2) Bital, Seguros and Afore Allianz Dresdner(3) Household and Metris(4) HSBC Finance Corp, IFRS Management Basis, Form 8-K

Has HSBC become too big to manage?

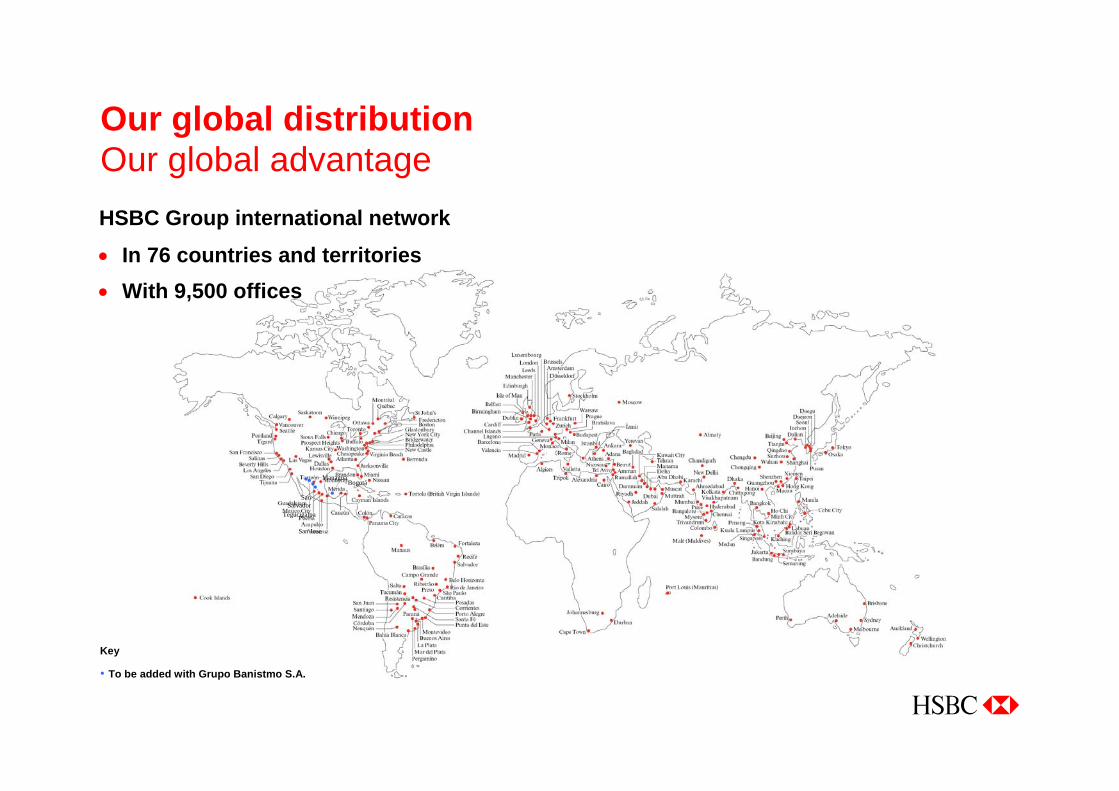

Tegucigalpa

Bogotá

SanSalvador

San Jose

Managua

To be added with Grupo Banistmo S.A.

Our global distributionOur global advantageHSBC Group international network

• In 76 countries and territories• With 9,500 offices

Key

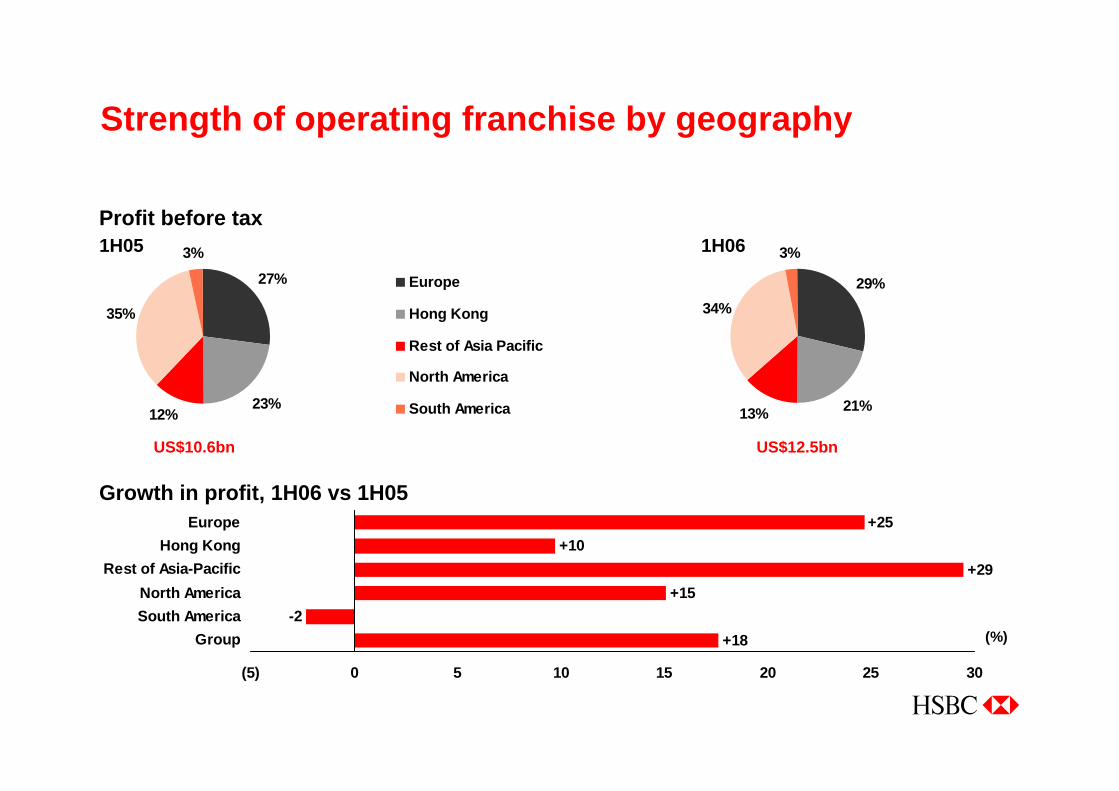

27%

23%12%

35%

3%

Europe

Hong Kong

Rest of Asia Pacific

North America

South America

Strength of operating franchise by geography

29%

21%13%

34%

3%

US$12.5bn

1H06

US$10.6bn

1H05Profit before tax

+18-2

+15+29

+10+25

(5) 0 5 10 15 20 25 30

GroupSouth AmericaNorth America

Rest of Asia-PacificHong Kong

Europe

(%)

Growth in profit, 1H06 vs 1H05

Strength of operating franchise by customer group

22%

22%

4% 3%

49%

Personal Financial Services

Corporate, Investment Banking and Markets

Commercial Banking

Private Banking

Other

US$10.6bn

1H05

47%

25%

23%

5%

US$12.5bn

1H06Pre-tax profits

Growth in profit, 1H06 vs 1H05

+18+33

+21+37

+13

0 5 10 15 20 25 30 35 40

GroupPrivate Banking

Commercial BankingCorporate, Investment Banking and Markets

Personal Financial Services

(%)

Why invest in HSBC rather than good regional players?

0

20

40

60

80

100(40) (20) 0 20 40 60 80

Cos

t effi

cien

cy ra

tio

Revenue growth

Prioritisation of Investment

50.1%

14.8%

US

UK

HongKong

Mainland ChinaFrance

Argentina

Brazil

UAE

India

MexicoMalaysia

Malta

Germany

SingaporeBermuda

Turkey

Canada

Re-engineer

Harvest

Invest

Grow

Our businesses – building for sustained growth

Europe Private Banking

What are the next things to look for from HSBC?

The Brand

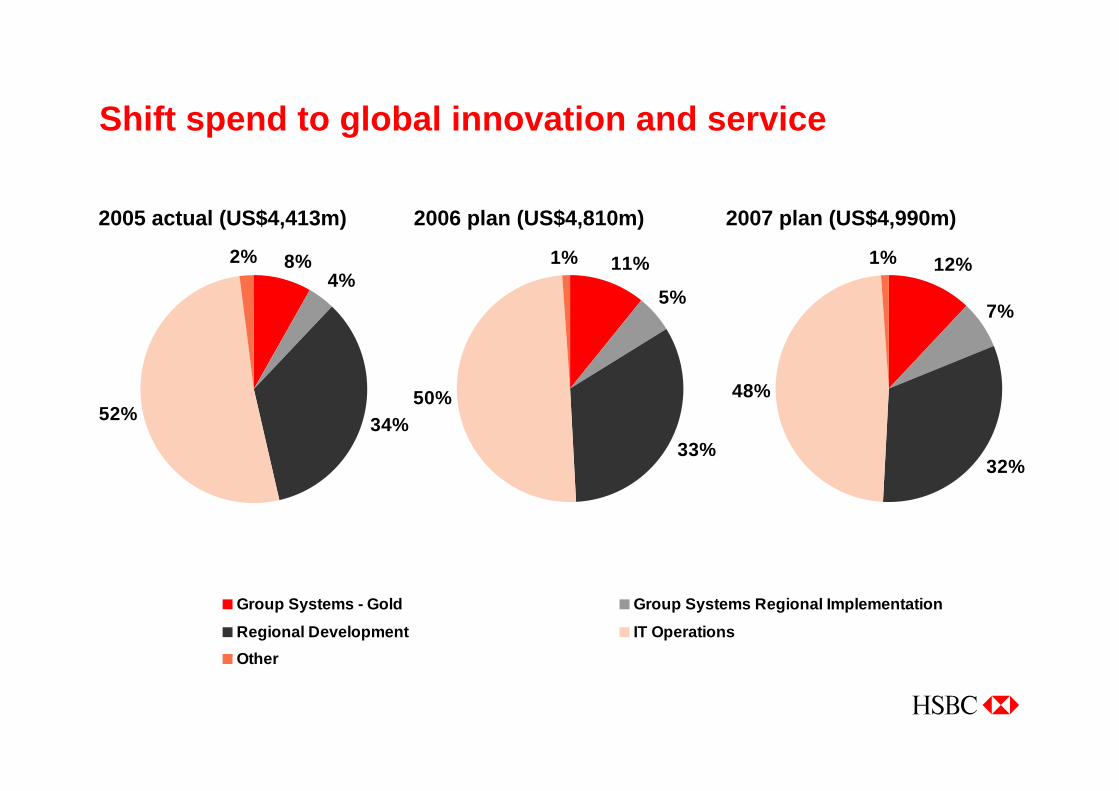

Shift spend to global innovation and service

2005 actual (US$4,413m) 2006 plan (US$4,810m) 2007 plan (US$4,990m)

8%4%

34%52%

2% 11%

5%

33%

50%

1% 12%

7%

32%

48%

1%

Group Systems - Gold Group Systems Regional Implementation

Regional Development IT OperationsOther

Our people, our culture – the best place to work

Insurance and retirement businessThe opportunityPeople aged 60 years and over: 1950–2050 (millions)

Source: United Nations World Population Prospects, 2004 Revision

2,000

1,500

1,000

500

0 1950 1980 2000 2025 2050

What are the potential challenges?

HSBC exposure to US residential lending

112118

126

100105110115120125130

1H05 2H05 1H06

US residential mortgages (US$bn)

US consumer finance (1H06)

82%

18%

First lien

Second lien

73%

27%

Fixed rate

ARMs

US$89bn US$89bn

US$73bn

US$16bn US$24bn

US$65bn

(1)

(1)

(1) 1st mortgage and 2nd lien lending

HSBC exposure to UK consumer

36%

64%

Residential mortgages

Other personalunsecured

26%

74%

UK

Rest ofGroup

UK Personal Lending (US$118bn)

HSBC Group Personal Lending (US$448bn)

Distrib

ution

TechnologyBrand

Businesses

Cultur

e

Organisation

Our main focusJoining up the company for our customers

Now you know

Who is Michael Geoghegan?