managing complexity - investors – rbs/media/files/r/rbs-ir/archived... · managing complexity...

TRANSCRIPT

Managing ComplexityManaging ComplexityManaging Complexity

Sir Fred GoodwinSir Fred GoodwinGroup Chief ExecutiveGroup Chief Executive

Slide 2

Managing Complexity

1 Step Process

▮ Reduce complexity

Slide 3

Managing Complexity

Reduce Complexity

Step 1.i Limit business activity tocontiguous/complementary areas

▮ We haven’t diversified into– Equity trading and sales

– Mergers and acquisitions advisory services

– Institutional fund management

– Life assurance manufacturing

Slide 4

Managing Complexity

Reduce Complexity

Step 1.i Limit business activity to contiguous/complementary areas

▮ We have diversified– geographically:

Mellon, Charter One, other Citizens acquisitions, Bank vonErnst, First Active, People’s Bank, BIBIT, Lynk Systems

– Green Flag, Dixon Motors

Slide 5

Managing Complexity

Reduce Complexity

Step 1.ii Establish appropriate organisation structure

▮ Group similar activities together, creating– Centres of excellence

– Specialisation

– Economies of scale

▮ Maintain consistency

Slide 6

Group Structure

• Large Corporates - RBS• Mid Corporates and

Commercials-RBS/NW• Treasury - RBS• Greenwich Capital (US)• Lombard• Angel Trains• Specialist Businesses

WealthManagement

MANUFACTURING

CUSTOMERSCUSTOMERS

CitizensRBSInsurance

RetailDirect

RBS CBFMNatWest UlsterBank

• Coutts• Adam• NatWest Offshore• RBSI

• Direct Line• Churchill• NIG• International

• Personal• Small Business• RSA

• Personal• Small Business• NW Life

• Ulster Bank• First Active• Personal• Business• Corporate

• Personal• Business• Commercial

Technology Operations Services

• RBS Cards• NatWest Cards• MINT• One Account• Tesco PF• Lombard Direct• DLFS• International

Slide 7

Managing Complexity

Reduce Complexity

Step 1.iii Create appropriate operating model

▮ Featuring– Clear delegation of responsibility

– Clear reporting requirements

– Clear performance management regime

– Effective communication (bi-directional)

– Appropriate ‘clock speed’

▮ Must maintain consistency

Slide 8

Managing Complexity

Reduce Complexity

Step 1.iv Create clarity of objectives

▮ What are we trying to do?Objectives should be– Group wide– Aspirational– Achieveable– Not too detailed

▮ High level objective“We aim to deliver superior sustainable value for ourshareholders, customers and staff”

Slide 9

Managing Complexity

Reduce Complexity

Step 1.iv Create clarity of objectives

▮ More specific objectives– Achieve superior income growth

– Improve cost:income ratio

– Maintain/improve credit quality

– Increase customer numbers and satisfaction

– Improve employee opinion survey scores

▮ Must maintain consistency

Slide 10

Managing Complexity

Reduce Complexity

Step 1.v Create clarity of required outcome

▮ Disciplined approach to– Budgets– Action plans– Cost recharging (not favoured)– Project/transaction investment hurdles– Incentives and rewards

▮ Must maintain consistency

Slide 11

Managing Complexity

We have maintained consistency of our model since 1999

▮ But has it enabled us to cope with increasing complexity?

Slide 12

The Royal Bank of Scotland Group

Complexity Context 1999 2003 2004(pre-NatWest)

Employees 32,670 120,900 133,500

Income (£m) 4,138 19,229

US income (£m) 549 2,792

Operating profit (£m) 1,211 7,151

▮ Transformation of scope and scale of Group,through combination of

– Acquisitions

– Organic growth

– New businesses

Slide 13

Acquisitions 1999 – 2004

Date Acquisition Division Consideration (m)

1999 Oct State Street (commercial banking) Citizens $350Nov Green Flag Direct Line £223

2000 Jan UST Corporation Citizens $1,400Mar NatWest RBS £21,000

2001 Jul Balance of Virgin One Retail Direct £100Aug International Aviation Management CBFM £16Sep Euro Sales Finance CBFM £70Sep Allstate Corporation (motor insurance, Germany/Italy) Direct Line $20Dec Mellon Regional Franchise Citizens $2,200

2002 Jan Royal Insurance (motor insurance, Italy) Direct Line €20May Dixon Motors CBFM £118Oct Medford Bancorp Citizens $273

2003 Jan Commonwealth Bancorp Citizens $450Jun Nordisk Renting CBFM €104Jul Port Financial Corporation Citizens $285Jul Santander Direkt Bank (credit cards, personal loans) Retail Direct €486Sep Churchill Insurance Group Direct Line £1,100Oct Community Bancorp Citizens $116Nov Bank von Ernst Wealth Management Swfr 500

2004 Jan Roxborough Manayunk Bank Citizens $136Jan First Active Ulster Bank €887Mar People’s Bank (credit cards) Retail Direct $360May Bibit Retail Direct €93Sep Charter One Citizens $10,500Sep Lynk Systems Inc Retail Direct $525

Slide 14

Income Growth 2000 – 2003

Pro forma1999 2003 Change over 4 Yrs

£m £m £m %

Total income 11,065 19,229 8,164 +74%

Components of Income Growth £m % Total

NatWest transaction benefits 872 11%

Other acquisitions 1,865 23%

Organic growth 5,427 66%

Total 8,164 100%

Slide 15

UK Financial Services New Entrants

Commenced Profit/(Loss) 2003

Scottish Widows Bank 1995 £17mGoldfish 1996 (£30m)The One account 1997 £27mSainsbury’s Bank 1997 £22mTesco Personal Finance 1997 £160mEgg 1998 (£34m)Standard Life Bank 1998 £5mDirect Line Rescue 1998 £31mMarbles 1999 not reportedSmile 1999 not reportedCahoot 2000 (£15m)Intelligent Finance 2000 (£53m)Zurich Bank 2001-03 closed Mar 03Profit/(loss) before exceptional items

Slide 16

Managing Complexity

Model has had to cope with increasing complexity

▮ But has it delivered results in line with our objectives?

Slide 17

Creating Value for Shareholders

▮ Grow income

▮ Improve efficiency

▮ Maintain credit quality

Slide 18

Grow Income

0

5

10

15

20

1999 2000 2001 2002 2003

RBS Income 1999 – 2003£bn

Pro forma

Slide 19

Grow Income

0 20 40 60 80 100

HSBC

RBS

Wells Fargo

Citigroup

Bank of America

JPM Chase

Income Growth 1999 – 2003

%Income as reported in US$, except RBS which reports in sterling

Slide 20

Grow Income

-20

0

20

40

60

80

100

1999 2000 2001 2002 2003

Percentage Growth in Income 1999 – 2003

Income as reported in US$, except RBS which reports in sterling

%

Wells Fargo

RBS

HSBC

Citigroup

Bank of America

JPM Chase

Slide 21

Grow Income

0 10 20 30 40

RBS

HSBC

Bank of America

Citigroup

Wells Fargo

JPM Chase

Half year income as reported in US$, except RBS whose sterling income has been converted into US$

%

Income Growth 1H03 - 1H04 in US Dollars

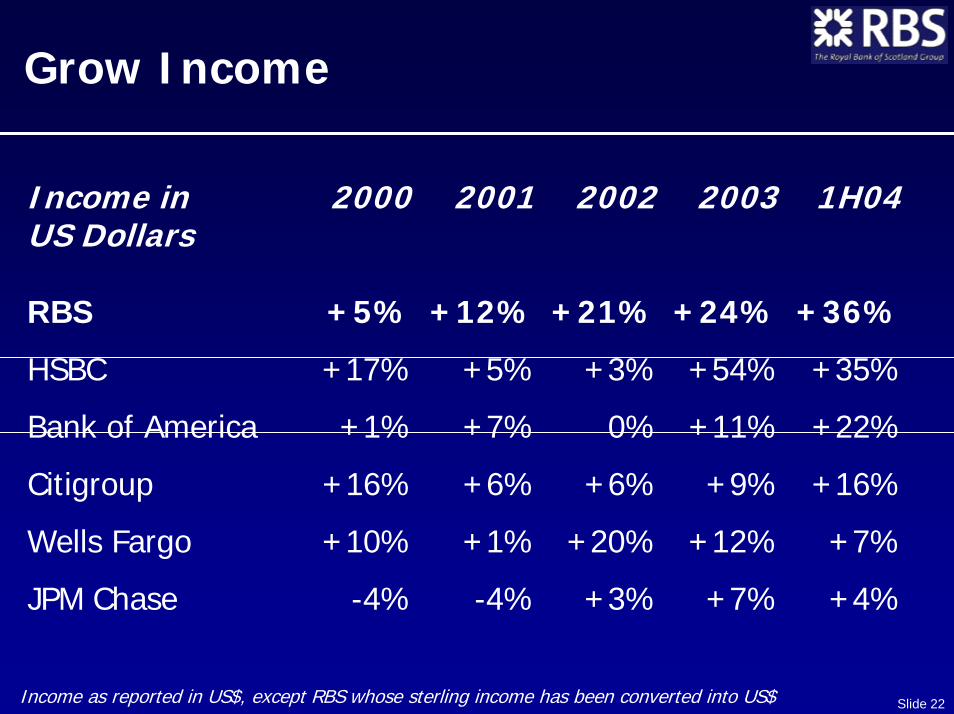

Slide 22

Grow Income

Income in 2000 2001 2002 2003 1H04US Dollars

RBS +5% +12% +21% +24% +36%

HSBC +17% +5% +3% +54% +35%

Bank of America +1% +7% 0% +11% +22%

Citigroup +16% +6% +6% +9% +16%

Wells Fargo +10% +1% +20% +12% +7%

JPM Chase -4% -4% +3% +7% +4%

Income as reported in US$, except RBS whose sterling income has been converted into US$

Slide 23

Improve Efficiency

35

40

45

50

55

60

65

70

1999 2000 2001 2002 2003 1H04

RBS Cost:Income Ratio 1999 – 1H04%

RBS: netting operating lease depreciation against rental income

Slide 24

Improve Efficiency

35

40

45

50

55

60

65

70

Citigroup B of A HSBC JPM Chase Wells Fargo RBSCost:income ratios as reported by banks, or based on income and costs reported by banksRBS: netting operating lease depreciation against rental income

Cost:Income Ratios 1999 – 1H04%

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

Slide 25

Maintain Credit Quality

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Citigroup B of A HBSC JPM Chase Wells Fargo RBS

%

99 00 0102 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

99 00 01 02 03 1H04

P&L Account Provisions:Customer Loans + Advances

Slide 26

Maintain Credit Quality

0

20

40

60

80

100

1999 2000 2001 2002 2003 1H04

RBS Balance Sheet Provisions as a Percentage ofRisk Elements in Lending and Potential Problem Loans%

Slide 27

Creating Value for Shareholders

▮ Grow income

▮ Improve efficiency

▮ Maintain credit quality

Slide 28

Strategy

What is our goal?

▮ Generating superior sustainable value forour shareholders

▮ To achieve this we need to add value for– Our customers

– Our people

Slide 29

Our Customers

1999 – 2003 Increase Increase000s %

Retail BankingPersonal customers 1,900 +16%

Retail DirectUK credit card accounts 3,600 +55%

RBS InsuranceUK motor in-force policies 5,400 +203%

Ulster BankPersonal customers 500 +68%

CitizensPersonal customers 1,400 +136%

Slide 30

CBFMCustomer Satisfaction

Service Quality Index

Impo

rtan

t B

ank

Overall Relationship Performance

RBS

0%

15%

30%

45%

60%

75%

350 500 650

Slide 31

Retail BankingCustomer Satisfaction

50 60 70 80

RBS

NatWest

GB Q2 average, extremely and very satisfiedSource: NOP FRS, quarterly rolling

Telephony Satisfaction

%

Slide 32

RBS InsuranceCustomer Satisfaction

Direct Line Motor

Motor quotes

Motor renewers

Motor purchasers

Source: RBS Insurance, August 2004

0 20 40 60 80 100

Extremely/very satisfied

%

Slide 33

Tesco Personal FinanceCustomer Satisfaction

Customer Satisfaction – Motor Insurance%

0102030405060708090

TPF

% customers very satisfied% customers extremely satisfied

Source: NOP FRSBase: 6 months to end of June 2004

Other Providers

Slide 34

CitizensCustomer Satisfaction

Customer Satisfaction Ratings%

70

75

80

85

90

Q202 Q302 Q403 Q103 Q203 Q303 Q403 Q104 Q204

Source: Citizens

New England

Mid Atlantic

Completely or very satisfied

Slide 35

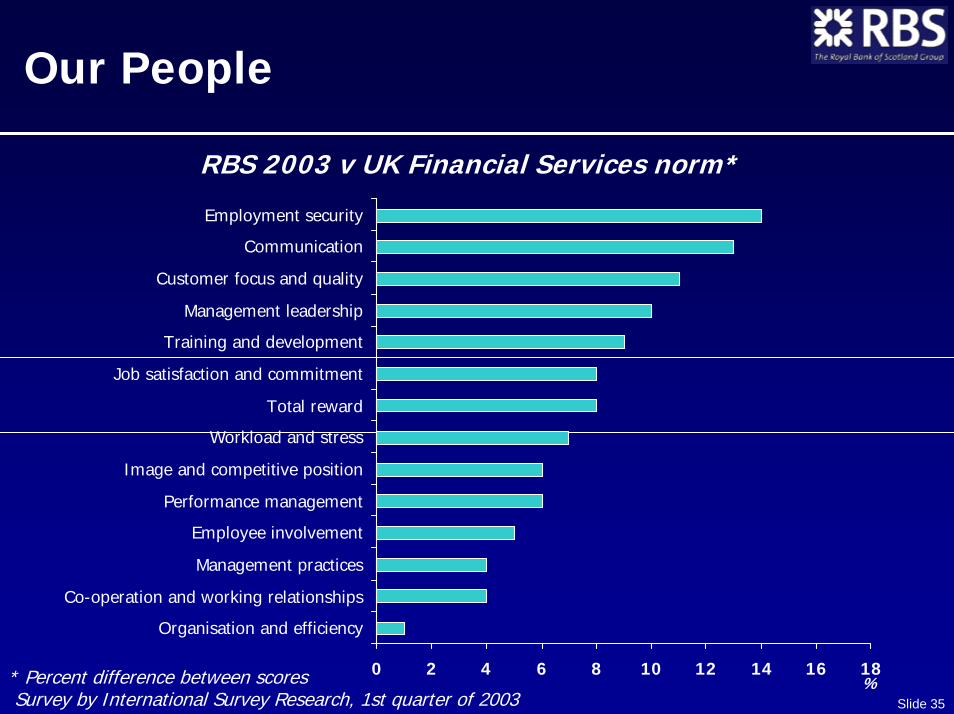

Our People

RBS 2003 v UK Financial Services norm*

* Percent difference between scores Survey by International Survey Research, 1st quarter of 2003

%0 2 4 6 8 10 12 14 16 18

Organisation and efficiency

Co-operation and working relationships

Management practices

Employee involvement

Performance management

Image and competitive position

Workload and stress

Total reward

Job satisfaction and commitment

Training and development

Management leadership

Customer focus and quality

Communication

Employment security

Slide 36

Our People

2003 Employee Opinion Survey

I have a clear understanding of the goalsand objectives of our business 86%

Slide 37

Our Shareholders

-40 -20 0 20 40 60 80 100 120 140

Bank of America

RBS

Wells Fargo

HSBC

Citigroup

JPM Chase

Source: Merrill Lynch

Total Shareholder Return 6 Mar 2000 – 1 Oct 2004

%

Slide 38

Strategy

What is our goal?

▮ Generating superior sustainable value forour shareholders

▮ To achieve this we need to add value for:– Our customers

– Our people

Slide 39

Managing Complexity

Conclusion

▮ RBS model works

▮ Has helped to reduce complexity

▮ Remains relevant and viable

Slide 40

Charter One Update

▮ Transaction completed 1 September 2004,ahead of schedule

▮ Management transition completed

▮ Balance sheet positioning implemented

▮ Integration underway

▮ So far, so good

Slide 41

Other Recent Acquisitions

▮ Churchill integration fully on track

▮ First Active integration fully on track

▮ IT migration completed for– People’s Bank credit card business

– Bank von Ernst

Managing ComplexityManaging ComplexityManaging Complexity

Sir Fred GoodwinSir Fred GoodwinGroup Chief ExecutiveGroup Chief Executive