mandatory ifrs adoption and institutional investment decisions

TRANSCRIPT

THE ACCOUNTING REVIEW American Accounting AssociationVol. 87, No. 6 DOI: 10.2308/accr-502252012pp. 1993–2025

Mandatory IFRS Adoption and InstitutionalInvestment Decisions

Annita Florou

King’s College London

Peter F. Pope

City University London

ABSTRACT: We examine whether the mandatory introduction of International Financial

Reporting Standards leads to an increase in institutional investor demand for equities.

Using a large ownership database covering all types of institutional investors from

around the world, we find that institutional holdings increase for mandatory IFRS

adopters. Changes in holdings are concentrated around first-time annual reporting

events. Second, we document that the positive IFRS effects on institutional holdings are

concentrated among investors whose orientation and styles suggest they are most likely

to benefit from higher quality financial statements, including active, value, and growth

investors. These results are consistent with holdings changes being associated with the

financial reporting regime change. Finally, we show that increased institutional holdings

are concentrated in countries in which enforcement and reporting incentives are

strongest, and where the differences between local GAAP and IFRS are relatively high.

Overall, our study helps shed new light on the channels by which IFRS information

becomes impounded in market outcomes.

Keywords: accounting regulation; IFRS; standard-setting; accounting quality; compa-rability; institutional investment decisions.

JEL Classifications: G11; K22; M41; M42.

Data Availability: The data used in this study are available from the commercial

sources identified in the paper.

We thank Paulo Alves and Ulf Bruggeman for excellent research assistance. We are grateful to Wayne Thomas (editor)and John Harry Evans III (senior editor) and to two anonymous referees for their invaluable suggestions. We also thankHans Christensen, Mark DeFond, Miles Gietzmann, Fani Kalogirou, Sonia Konstantinidi, Scott Richardson, DanThornton, Stephen Young, Peter Wysocki, and participants at the 8th London Business School Accounting Symposiumand the 2009 AS-GAABR/IAAER Conference for their helpful comments on earlier drafts.

Editor’s note: Accepted by John Harry Evans III, with thanks to Wayne Thomas for serving as editor on a previousversion.

Submitted: March 2010Accepted: May 2012

Published Online: June 2012

1993

I. INTRODUCTION

Regulators have claimed that investors and issuers of securities will benefit from the

mandatory adoption of International Financial Reporting Standards (IFRS). They claim

that for many countries IFRS require higher quality measurement and recognition rules;

they are more transparent than local GAAP; and that common IFRS financial reporting across

countries will enhance comparability (EC Regulation No. 1606/2002, European Council 2002).

Theory predicts that the mandated introduction of higher quality financial reporting can improve

stock market liquidity and reduce the cost of capital (Leuz and Wysocki 2008), and empirical

evidence on the market outcomes of mandatory IFRS adoption generally supports these predictions

(Daske et al. 2008; Li 2010). An indirect implication of such findings is that market participants

find IFRS reporting to be incrementally informative. In this paper we test directly whether

mandated IFRS adoption affects institutional investor decisions. Institutional investors are an

interesting group of financial statement users because they are economically important and because

they are often regarded as sophisticated users who have the time, resources, and expertise to process

the information in complex financial statements. Establishing a causal link between mandatory

IFRS reporting and institutional investor decision outcomes helps to shed new light on the channels

by which IFRS information becomes impounded in market outcomes.

Using a global sample of 10,852 unique firms from 45 countries over the 2003–2006 period,

we report a number of results that are new to the literature. First, after controlling for standard

economic determinants of institutional holdings, we show that over the two-year period 2005–2006

institutional ownership increases by more than 4 percent and the number of institutional investors

increases by almost ten for mandatory IFRS adopters, relative to non-adopters. Results are

consistent for different analyses based on annual firm-level as well as quarterly firm-level and

country-level changes in institutional holdings. Second, we document that the positive IFRS effects

on institutional holdings are concentrated among investors whose orientation and styles suggest

they are most likely to benefit from higher quality financial statements. For example, institutional

holdings in mandatory IFRS adopters increase significantly for active investors, but changes are

much lower or insignificant for passive investors. Similarly, IFRS-related holdings increases are

substantially higher for value and growth investors than for index and income investors. Finally, we

document that the increases in institutional holdings associated with IFRS are not homogeneous

across countries. Our findings indicate that institutional holdings increase for first-time mandatory

adopters primarily in countries in which enforcement and reporting incentives are strongest, and

where the differences between local GAAP and IFRS are relatively high. Inferences are unaffected

by various sensitivity tests, including different sample definitions and additional control variables.

Our paper is most closely related to Bradshaw et al. (2004) and Covrig et al. (2007). Bradshaw

et al. (2004) is the first study to show that institutional stock ownership is related to firm-level

accounting choices, although they do not consider the role of accounting standards. Covrig et al.

(2007) show that stock ownership by foreign mutual funds increases with the voluntary adoption of

International Accounting Standards (IAS) by non-U.S. firms. Our paper extends this line of research

by investigating the effects of mandatory IFRS adoption on institutional holdings. Our paper is also

related to two concurrent studies reporting that foreign mutual fund ownership increases following

mandatory IFRS introduction (Yu 2010; DeFond et al. 2011). However, both of those studies focus

on the mechanisms through which IFRS attracts foreign investors. Yu (2010) examines the IFRS

effects of lower information asymmetry, measured primarily by the accounting distance between

the investees’ and investors’ accounting standards. DeFond et al. (2011) examine the IFRS effects

of increased comparability based on the similarity of accounting standards of investee firms within

industries and across different countries.

1994 Florou and Pope

The Accounting ReviewNovember 2012

We contribute to the literature in several ways. First, we provide evidence that institutional

investor decisions respond to IFRS reporting. This helps to explain the mechanism through which

the IFRS-related capital market outcomes reported in Daske et al. (2008) and Li (2010) occur.

Second, we employ a research design that enhances our ability to link the observed ownership

effects to the financial reporting regime change and helps rule out alternative explanations (Daske et

al. 2008, 1132) as follows: (1) we identify the timing of changes in institutional holdings relative to

first-time IFRS reporting events; (2) we examine the institutional holdings effects of mandatory

IFRS adoption with reference to differences in the predicted demand for and use of financial

reporting information by different investors; and (3) we focus on changes in holdings rather than

levels of holdings, thereby helping to control for firm- and country-level characteristics that

determine holdings independently of the financial reporting regime. Our focus on mandatory IFRS

adoption helps to mitigate potential issues of selection bias and omitted correlated factors in

voluntary adoption studies (Leuz and Wysocki 2008).

Finally, we introduce a new research design in examining the institutional context of IFRS

reporting effects. Our approach is different from that of prior work (Daske et al. 2008; Li 2010)

because we test the impact of complementary institutional features by using a single model based

on institutional ‘‘bundles’’ rather than several models focusing on different institutional

characteristics. Our findings on the role of institutions contribute to a growing literature

highlighting that the introduction of higher quality accounting standards is necessary, but not

sufficient, for higher quality financial reporting and associated benefits (Li 2010).

The remainder of the paper is organized as follows. In the next section we discuss prior related

studies and elaborate on the motivation of our study. In Section III we describe in detail the research

design and data. We discuss our findings in Section IV. Finally, in Section V we present our conclusions.

II. THEORETICAL BACKGROUND AND MOTIVATION

Proponents of IFRS claim that IFRS have advantages over local accounting standards in many

countries for several reasons. First, IFRS may be more capital-oriented and, therefore, more useful

to investors (Hail et al. 2010). Second, IFRS can reduce the choice of accounting methods, thus

constraining managerial discretion (International Accounting Standards Board [IASB] 1989;

Ashbaugh and Pincus 2001; Barth et al. 2008). Third, IFRS require accounting measurements and

recognition that better reflect a firm’s underlying economic position, hence providing more relevant

information for investment decisions (IASB 1989; Barth et al. 2008). Fourth, IFRS increase

required disclosures, thereby mitigating information asymmetries between firms and their

shareholders (Leuz and Verrecchia 2000; Ashbaugh and Pincus 2001). Aside from the higher

financial reporting quality argument, proponents of IFRS also claim that harmonization around

IFRS increases comparability of firms across markets and countries, hence facilitating cross-border

investment and integration of capital markets (Armstrong et al. 2010; DeFond et al. 2011).

In light of these potential advantages, advocates of IFRS often argue that they can be beneficial

for investors, issuers, and economies because enhanced financial reporting can result in increased

investor demand for equities and lower cost of capital (European Council 2002). Theory suggests

that these outcomes will follow if (1) market liquidity increases and price protection falls due to

lower information asymmetries among investors (Baiman and Verrecchia 1996; Verrecchia 2001);

(2) risk sharing improves due to increased awareness of investment opportunities by investors

(Merton 1987; Easley and O’Hara 2004); or (3) the estimation risk facing investors falls (Jorgensen

and Kirschenheiter 2003; Lambert et al. 2007; Hughes et al. 2007). In each case investment and

portfolio decisions depend on financial reporting, and a change to a higher quality and

homogeneous financial reporting regime is predicted to result in an increase in demand for equities

and investment holdings.

Mandatory IFRS Adoption and Institutional Investment Decisions 1995

The Accounting ReviewNovember 2012

On the other hand, there are several reasons why the expected benefits of IFRS can be

questioned. First, reducing accounting alternatives may result in a less true and faithful

representation of the firm’s underlying economics (Barth et al. 2008). Second, increasing

managerial flexibility, because of the principles-based nature of IFRS, may augment the opportunity

for earnings management (Barth et al. 2008). Third, and perhaps most importantly, an increasing

number of scholars emphasize that dysfunctional reporting incentives combined with weak

enforcement mechanisms can reduce financial reporting quality, even when high-quality accounting

standards are implemented (Ball et al. 2003; Burgstahler et al. 2006; Ball 2006).

To the extent that financial reporting under IFRS enhances the quality and comparability of

accounting information provided by issuers, we predict that mandatory IFRS adoption is associated

with an increase in the demand for equity in IFRS adopting firms. We also predict that IFRS-related

changes in holdings are more likely to be observed for investors whose investment orientations and

styles rely most heavily on firm-specific financial information (Bushee and Goodman 2007).

The expected effects of mandatory IFRS adoption are likely to depend on the institutions of the

adopting country (Hail et al. 2010). In line with this argument, Daske et al. (2008) and Li (2010)

document that the capital market effects of IFRS are more pronounced in countries with stricter

enforcement regimes and therefore better IFRS implementation; stronger reporting incentives and

therefore higher quality financial reporting; and higher divergence between IFRS and local GAAP

and therefore a larger change of domestic accounting rules.1 Accordingly, we predict that the

IFRS-related effects on institutional holdings for first-time mandatory adopters are likely to be

greater in countries with higher quality institutions and countries with less conformity between

domestic GAAP and IFRS.

III. RESEARCH DESIGN AND DATA DESCRIPTION

Identification Strategies

An important concern in studies of the impact of institutional change is to provide evidence that

observed effects reflect causality and rule out alternative explanations. Our baseline results, using a

difference-in-differences research design similar to Daske et al. (2008), document increases in

institutional holdings after mandatory IFRS adoption. Our main challenge is to develop convincing

evidence that increases in institutional holdings result directly from the financial reporting regime

change and are not due to other contemporaneous regulatory or market changes affecting IFRS

countries. Our research design includes two strategies designed to address this challenge.

Our first strategy uses information on the timing of firm-specific IFRS reporting to infer

whether causality runs from financial reporting to institutional holdings changes. Therefore, we

examine changes in holdings for annual and quarterly periods relative to first-time IFRS reporting

events. Our tests include both firm-level as well as country-quarter analysis similar to the country-

month analysis of Daske et al. (2008).2

In the second set of tests, we use investor type and investor style as instruments reflecting

investor demand for, and use of, financial reporting information. Investor type is defined as active

or passive. Active investors often use firm-specific information, including financial reporting

1 We note, however, that Francis et al. (2009) provide evidence suggesting that an improved informationenvironment enhances asset allocation, irrespective of a country’s legal regime and enforcement mechanisms.Also, in a related study Daske et al. (2011) document that ‘‘serious’’ mandatory IFRS adopters experience higherliquidity and lower cost of capital compared to ‘‘label’’ adopters, providing evidence on the firm-levelheterogeneity in the capital market effects of IFRS adoption.

2 We conduct country-quarter analysis rather than country-month analysis because our institutional ownership datais published at the end of each calendar quarter.

1996 Florou and Pope

The Accounting ReviewNovember 2012

numbers and disclosures, to determine the portfolio weights of individual stocks. In contrast,

passive investors do not seek to take security-specific views and rely on decision rules that do not

depend on financial reporting information. Thus, we predict that institutional holdings changes will

be more significant for active investors than for passive investors if institutional holdings changes

are causally linked to the financial reporting regime change.

Similarly, within the subset of active investors, some investors have investment styles that are

more dependent on accounting numbers than others (Bushee and Goodman 2007). Our holdings

data allow us to identify several common stock-oriented investment styles including value, growth,

index, and income investing. Value investors seek to determine whether stock market values are

fairly priced relative to fundamental values estimated using firm-specific accounting numbers, and

take long (short) positions relative to their benchmark in under-valued (over-valued) stocks. Growth

investors seek to forecast future value-relevant outcomes that will determine future capital gains, for

example by identifying stocks with above-average earnings growth potential. Financial statements

and forward-looking disclosures are important inputs to the decision models of many such

investors. In contrast, income investors usually focus on short-term dividends and dividend yield,

while index investors invest in proportion to stock index weights. In the latter two investment

styles, financial statement information is less important in investment decisions. Therefore, we

predict that changes in institutional holdings attributable to the IFRS regime change are more likely

to be observed for value and growth investors than for income and index investors.

Our empirical tests progressively build evidence consistent with causality running from IFRS

adoption to changes in institutional holdings. First, we conduct firm-level analysis based on different

annual measurement periods relative to first-time IFRS reporting events. Then, we perform additional

firm-level analysis using quarterly changes in institutional holdings. Next, we conduct analysis at the

country-quarter level. Finally, we examine how annual changes in institutional holdings depend on

investor demand for financial reporting information, reflected in investor orientation and style.

Firm-Level Annual and Quarterly Analyses

The firm-level analyses employ a difference-in-differences design similar to Daske et al.

(2008), utilizing data on both voluntary and mandatory adopters of IFRS in countries where IFRS

are mandated (treatment sample firms) and non-IFRS adopters in other countries (benchmark

sample firms), and using versions of the following model:

DInstitutional Holdings ¼ d0 þ d1First-Time Mandatoryþ d2Voluntaryþ d3Voluntary�Mandatoryþ RcjDControlsj þ e: ð1Þ

For the annual firm-level analysis DInstitutional Holdings is the change in an institutional holdings

proxy over a year. The marginal effects of IFRS reporting on institutional holdings are captured by

three binary indicator variables First-Time Mandatory, Voluntary, and Mandatory � Voluntary,

coded based on the reporting standards used in each firm-year (Worldscope code WS07536). First-Time Mandatory refers to observations for firms that never reported under IFRS before mandatory

adoption and equals 1 for all firm-years with IFRS reporting periods ending on or after the local

mandated IFRS adoption date (i.e., December 31, 2005), and 0 otherwise. It captures the extent to

which institutional holdings of first-time mandatory adopters are different after IFRS adoption.

Voluntary relates to observations for firms that voluntarily switched to IFRS reporting before it was

mandated and equals 1 for all firm-years with IFRS reporting by voluntary adopters, and 0

otherwise. It captures the extent to which institutional holdings are different for firms that

voluntarily adopt IFRS. Voluntary �Mandatory equals 1 for all voluntary adopter firm-years ending

on or after the mandated local IFRS adoption date, and 0 otherwise. It captures the extent to which

institutional holdings of voluntary IFRS adopters are different in the mandatory IFRS period.

Mandatory IFRS Adoption and Institutional Investment Decisions 1997

The Accounting ReviewNovember 2012

Focusing on changes in institutional holdings in Equation (1) enables us to develop insights

about the timing of any changes in institutional ownership relative to firm-level IFRS adoption

events, as discussed below. The changes model also provides more powerful tests, given that a firm

serves as its own control because both current-year and prior-year levels data are required to be

included in the changes sample. This requirement helps alleviate concerns that unmodeled factors

other than IFRS adoption, including possible database selection biases, could explain differences in

the levels of institutional holdings between treatment and benchmark samples, and across time, thus

increasing confidence that documented results reflect causality running from the IFRS reporting

regime change.

Our baseline analysis of Equation (1) involves measuring changes in institutional holdings over

calendar-year intervals. In this case the IFRS indicator coefficient estimates capture the average

annual IFRS effects over the two-year period 2005–2006. Since holdings changes are measured

over identical periods for both treatment and benchmark samples, the calendar-year approach

controls effectively for unmodeled factors affecting both treatment and benchmark samples.

However, to ensure that our inferences are not sensitive to the measurement interval for holdings

changes, we also report results based on two alternative annual windows spanning firms’ fiscal

year-ends. The window labeled �2/þ2 measures holdings changes over the last two quarters of a

fiscal year and the first two quarters of the next fiscal year, while the annual window labeled�1/þ3

measures changes over the last quarter of a fiscal year and the first three quarters of the next fiscal

year. A possible advantage of examining changes over these alternative windows is that IFRS

information contained in annual financial statements becomes available to investors during the

measurement interval. However, a significant disadvantage of the alternative windows is that

heterogeneity in fiscal year-end dates within and across the treatment and benchmark samples may

lead to weaker control for unmodeled factors. Hence, our baseline calendar-year results could be

viewed as more conservative estimates of overall IFRS effects that better control for unmodeled

global factors underlying holdings changes.

Having established our baseline results using annual windows, we use versions of Equation (1)

to address the identification problem by allowing the coefficients on First-Time Mandatory and

Voluntary � Mandatory to depend on the arrival of firm-specific IFRS information within the

mandated IFRS adoption period. Specifically, we conduct firm-quarter analysis by re-estimating

Equation (1) using institutional holdings changes measured over quarterly intervals. We supplement

Equation (1) by adding indicator variables that capture incremental reporting-time effects during the

mandated IFRS period 2005–2006. Incremental holdings changes for first-time mandatory adopters

are captured by indicator variables First-Time Mandatoryq (q¼�2,�1,þ1,þ2,þ3) set equal to 1 in

quarter q and 0 in other quarters, using the convention that q¼�1 is the quarter of the fiscal year-

end and q ¼ þ1 is the quarter following the fiscal year-end.3 The coefficients on Voluntary �Mandatoryq capture incremental reporting-time holdings changes for voluntary adopters in the

mandatory IFRS period in a similar manner.

While financial reporting lags vary across countries, we believe that it is reasonable to expect

that financial statements will usually be released late in quarter þ1 or early in quarter þ2.4

Therefore, we predict incremental investor reaction to financial statement information in quarterþ2

and significantly positive coefficients of First-Time Mandatoryþ2. Delayed response to financial

statement information will be indicated if the coefficients on First-Time Mandatoryþ3 are

3 For example, for firms where the first-time IFRS fiscal period ends in December 2005, First-Time Mandatoryþ1 isset equal to 1 for the first quarter of 2006, while First-Time Mandatory�1 equals 1 in the fourth quarter of 2005.

4 DeFond et al. (2007) report considerable variation in earnings announcement dates, with the median of country-level median earnings reporting lags being 83.25 days. Annual reports containing full financial statements arelikely to follow at least several weeks later, depending on statutory reporting rules.

1998 Florou and Pope

The Accounting ReviewNovember 2012

significant. We predict that incremental holdings changes in quarter þ3 (if any) will be lower in

magnitude than those in quarter þ2. If firms report earlier and investors react to information in

annual financial statements within quarterþ1, then First-Time Mandatoryþ1 will also be positive. If

firms do not report sufficiently early in quarter þ1 for investors to react in the same quarter, then

First-Time Mandatoryþ1 will capture any anticipation effects, as will the coefficients on First-TimeMandatoryq (q ¼ �2,�1). The interpretation of the coefficients on the reporting-time indicator

variables Voluntary � Mandatoryq is similar, with Voluntary � Mandatoryþ2 being most likely to

capture investor reaction to financial statement information.

Country-Quarter Analysis

We also conduct country-level analysis relating aggregate changes in institutional holdings to

changes in an index tracking the actual rate of reporting under IFRS in each country. The research

design follows closely the country-month analysis of Daske et al. (2008). We estimate the following

regression pooled over countries and quarters:

DInstitutional Holdings ¼ d0 þ d1DIFRS Adoption Rateþ RcjControlsj þ l: ð2Þ

In Equation (2) DInstitutional Holdings is the change in the median institutional holdings in a

country-quarter and DIFRS Adoption Rate is the change in an index of cumulative IFRS adoption

within a country based on the publication of mandatory IFRS financial statements and measured in

two ways described below. Consistent with the firm-quarter analysis, we predict that DIFRSAdoption Rate will be associated with changes in institutional holdings with a one-quarter lag,

reflecting the time taken for institutional investors to process information and rebalance portfolios.

We construct the IFRS adoption rate index for a country in two ways. First, we define IFRS

adoption with reference only to the reporting of first-time IFRS annual financial statements. In this

case and in line with the firm-quarter analysis, we assume that financial statement publication

occurs in the quarter following the fiscal year-end. We assign a firm-level adoption counter a value

of 1 starting in the quarter following the first-time IFRS fiscal year-end. In each calendar-quarter

IFRS Adoption Rate is the average value of the firm-level adoption counter for the set of mandatory

adopters in the country. The index has a maximum value of 1 in the quarter when the final firm in a

country reports under IFRS for the first time. Similar to Daske et al. (2008), we label the index

based on annual financial reporting as IFRS Adoption RateFYE.

If IFRS information arrives as a result of quarterly or interim announcements during the IFRS

adoption year, then IFRS Adoption RateFYE may understate the true rate of cumulative IFRS

information arrival in the first-time adoption year and overstate the true rate in the following year.

To address this possibility we also construct the IFRS Adoption Rate index with reference to

quarterly, interim, and annual earnings announcement dates (Worldscope item WS05905),

assuming that quarterly or interim financial reporting is under IFRS in the mandatory adoption year.

Under this definition of the IFRS Adoption Rate index, in the quarter of an announcement we

increase the firm-level adoption counter value by 1/n, where n equals 4, 2, or 1 for quarterly, semi-

annual interim, and annual announcements, respectively.5 In each calendar-quarter IFRS AdoptionRate is the average value of the firm-level adoption counter for the set of mandatory adopters in the

country. The index has a maximum value of 2 in the quarter when the final firm in a country reports

annual financial statements under IFRS for the first time, having previously reported quarterly or

5 In some countries firms vary in the frequency of reporting. For example, some U.K. firms voluntarily reportquarterly while being required to report semi-annual interim financial statements. Therefore, we define the firm-level reporting frequency for a given year (n) by counting the actual number of announcements reported by eachfirm in the year.

Mandatory IFRS Adoption and Institutional Investment Decisions 1999

The Accounting ReviewNovember 2012

interim statements. Similar to Daske et al. (2008), we label this variable IFRS AdoptionRATEINTERIM.

The Role of Institutions

We analyze the institutional context of IFRS financial reporting effects using a new approach.

Our approach is similar to Daske et al. (2008) and Li (2010) in that we model IFRS effects

conditional on proxies for the likelihood of high-quality enforcement and application of IFRS, and

measures of accounting difference between local GAAP and IFRS. Our approach is different

because we estimate the impact of complementary institutional features in a single model; we also

use measures of accounting difference capturing the changes in accounting that can be expected

when moving from an issuer’s local GAAP to IFRS.

Collinearity between institutional proxies may arise because different institutions in a country

do not develop independently and they can complement one another. This perspective predicts that

institutional ‘‘bundles’’ will emerge (Wysocki 2011). This is confirmed by Leuz et al. (2003) and

Leuz (2010) who apply cluster analysis to institutional proxies that capture the strength of securities

regulation, legal enforcement, investor protection, disclosure, and transparency of reporting

practices. We classify countries into three clusters defined in Leuz (2010) and characterized as

outsider economies with strong outsider protection and legal enforcement (Cluster 1); insider

economies with stronger rule enforcement (Cluster 2); and insider economies with weaker rule

enforcement (Cluster 3).6 We then allow the IFRS effects captured by First-Time Mandatory,

Voluntary, and Voluntary � Mandatory to vary across clusters. We predict that IFRS-related

holdings changes for first-time mandatory adopters are likely to be more pronounced in the cases of

Clusters 1 and 2 because reporting incentives and enforcement are predicted to lead to higher

quality reporting.

We consider whether IFRS-related changes in institutional holdings depend on the extent of

accounting change involved in moving from local GAAP to IFRS reporting. We do not model the

dependence of institutional holdings on country-pair differences between an investor’s home

country GAAP and an issuer’s home country GAAP (Yu 2010). Rather we examine how the

differences between local GAAP and IFRS influence changes in institutional holdings generally.

Holding reporting incentives and enforcement constant, the mandatory switch to IFRS in countries

with large differences between domestic accounting standards and IFRS should result in larger

improvements in financial reporting quality and in comparability, to the benefit of all institutional

investors irrespective of their location.

We estimate accounting differences using the two distinct measures proposed by Ding et al.

(2005, 2007), who analyze a comprehensive set of 111 accounting items reported in the GAAP2001 survey of national accounting rules conducted by seven large auditing firms. Absence captures

missing local GAAP financial reporting rules relative to IFRS. Divergence captures inconsistencies

between local GAAP and IFRS treatments. Ding et al. (2007) show that these two dimensions are

uncorrelated and argue that they cannot be considered as substitutes or complements. Absenceimplies an accounting issue is not important enough in a specific jurisdiction and/or is beyond the

standard-setter’s competence, while Divergence means the issue is important in the country and the

standard-setter is competent and confident enough to adopt a non-IAS approach (Ding et al. 2009,

160).7 We believe that the Ding et al. (2005, 2007) measures are appropriate in our research setting

for four main reasons. First, our focus is on the IFRS-related ownership effects across institutional

6 Consistent with institutions being associated with financial reporting quality, Leuz (2010) reports higherdisclosure and more informative earnings in Cluster 1 relative to Cluster 2, and in Cluster 2 relative to Cluster 3.

7 Divergence may also indicate that the national GAAP covered a particular issue before it was covered by IAS.

2000 Florou and Pope

The Accounting ReviewNovember 2012

investors irrespective of their location. The Absence and Divergence measures capture the potential

accounting changes that can benefit investors generally. Second, the Ding et al. (2005, 2007)

measures are based on a comprehensive list of potential discrepancies. Third, the distinction

between absence and divergence could be important.8 Fourth, empirical evidence in Garcia Osma

and Pope (2011) indicates that Divergence explains country-level adjustments to local GAAP

numbers on first-time IFRS adoption, whereas alternative measures of accounting difference do not

or they have the wrong sign.

We predict that IFRS-related changes in institutional holdings for first-time mandatory adopters

will be positively related to Divergence and Absence if differences between alternative accounting

regimes are important to investors. To implement these measures in empirical tests we generate

binary indicators from the Divergence and Absence continuous variables using the medians across

IFRS adoption countries as the classification cut-off.

Empirical Proxies

Institutional Holdings

In contrast to previous and concurrent research that focuses on the ownership of mutual funds

(Covrig et al. 2007; Yu 2010; DeFond et al. 2011), this is the first study to examine the links

between IFRS reporting and global institutional ownership including investors other than mutual

funds. Our institutional holdings data are drawn from the Thomson Financial Ownership (TFO)

quarterly data feed and include domestic and foreign holdings of mutual funds, pension funds,

insurance companies, hedge funds, private equity funds, and venture capital funds from 45

countries.9 An advantage of our data is that the data capture a much higher proportion of total

institutional ownership. For example, we document average ownership of almost 22 percent, in

contrast to Covrig et al. (2007), Yu (2010), and DeFond et al. (2011) who report a mean value of

mutual fund ownership between 2 percent and 10 percent. Under the assumption that decisions by

non-mutual fund institutional owners reflect informed investor opinion, the expanded scope of

8 Based on the same data source, Bae et al. (2008) propose two measures (gaapdif1 and gaapdif2) of differences inaccounting standards at the country-pair level. Moreover, these measures are a blend of absence of local GAAPrules and divergence between local GAAP and IAS and they are not intended to provide a comprehensivecatalogue of country-level differences from IAS. Bae et al. (2008) construct country scores based on differencesrelating to 21 (gaapdiff1) or 52 (gaapdiff2) ‘‘key’’ accounting items, selected because they appear in the pastresearch literature (gaapdiff1) and because they appear frequently in the survey. The focus on country-pairsrestricts the set of accounting rules considered because countries that differ from IFRS are also required to havesimilar GAAP. As a consequence, relative to Absence and Divergence, the Bae et al. (2008) measures areexpected to be noisy measures of the distance between local GAAP and IAS for two reasons. First, they excludesome important sources of differences. For example, gaapdiff1excludes 12 standards in IAS, 11 of which affectrecognition and measurement, including IAS 39 (Financial Instruments), where Divergence is often high andaccounts for 6 out of the 111 items considered by Ding et al. (2005, 2007). Second, gaapdiff1 also covers twostandards (IAS 1, Presentation of Financial Statements, and IAS 24, Related Party Disclosures) where there is ahigh degree of local GAAP conformity with IAS (81 percent and 73 percent, respectively). The gaapdiff1measure with respect to these two items captures Absence only. We thank an anonymous reviewer for helpfulcomments on the relative merits of the alternative measures of accounting difference.

9 Thomson Reuters state that the database includes holdings on more than 44,000 global equity issues. The sourceof the data depends on the region. Specifically, in the case of Europe, Middle East, Africa, South/CentralAmerica, and Asia, information on equity holdings is processed primarily from Shareholder, Trade, and MutualFund Portfolio Reports, which gather data from annual and interim reports, stock exchanges, regulatory bodies,investor relations departments, and third-party vendors. In the case of U.K. and Ireland holdings, data above a0.015 percent threshold is sourced from inspection of firms’ registers of shareholders. In the case of the U.S.,security information is gathered from SEC 13D, 13G, 10K, 20F, and 13F filings and from mutual fund andpension fund portfolio reports.

Mandatory IFRS Adoption and Institutional Investment Decisions 2001

The Accounting ReviewNovember 2012

our institutional investor universe enhances the power of our tests to detect IFRS-related

effects.10

To obtain our holdings proxies we employ the following procedures. First, we retrieve

disaggregated holdings data on the number and value of institutional shares from the Historical

Holdings Files for each quarter in the period 2003–2007. Second, using the Historical Security File

we identify all types of common and registered equity securities owned by institutional investors for

each firm. ADR holdings are converted to the equivalent number of shares of the underlying equity

class by multiplying ADR holdings by the ADR-underlying conversion ratio. From this file we also

collect data on various items including share price, outstanding shares, and security identifiers.

Finally, we retrieve data on investor orientation (active or passive) and investor style (value,

growth, income, and index) from the Historical Owner File.

In line with prior studies of institutional ownership we consider the aggregate percentage

ownership of institutional shareholders (Covrig et al. 2007; DeFond et al. 2011) and the total

number of institutional investors (O’Brien and Bhushan 1990; Walther 1997; Bradshaw et al.

2004). Percentage ownership is calculated as the total market value of shares owned by institutional

investors (or investors having particular orientations or style) divided by the total market value of

the firm at the end of a quarter. The number of institutional investors is the count of investors with

recorded holdings at the end of a quarter.

Control Variables

Following prior literature (Leuz et al. 2010; DeFond et al. 2011), we include control variables

documented to be associated with institutional holdings: Nanalysts (the number of analysts at the

fiscal year-end from I/B/E/S) to proxy for richness of the information environment; Market Index

(Worldscope item WS05661), a dummy variable that equals 1 if the firm is included in any national

stock market index and MSCI Index, a binary variable set equal to 1 if the firm is included in the

MSCI World Index, to control for the firm’s visibility to investors;11 ADR (WS11496), a dummy

that takes the value of 1 if the firm has an ADR listed on a U.S. exchange, to proxy for the degree of

visibility and information environment richness of non-U.S. firms; Big4 (WS07800), a

dichotomous variable equal to 1 if the firm is audited by a Big 4 firm or their predecessors, to

control for investor preferences for auditors with a strong reputation; Size (WS07210), defined as

the natural logarithm of market value of equity in U.S. dollars at year-end, to proxy for liquidity,

information environment, and fiduciary concerns; ROE, measured as net income before

extraordinary items (WS01551) divided by total assets at the beginning of the year (WS02999),

to control for accounting performance; RET, calculated as log of (RItþ1/RIt), where RI is the

DataStream Total Return Index on first January, to capture the effect of stock market performance

over the fiscal year; RetVar, measured as the standard deviation of monthly stock returns over the

fiscal year, to control for firm risk.

In addition, we include in our set of controls a number of proxies for firm fundamentals that are

potentially related to institutional holdings, namely Dividend Yield, computed as total dividends

10 Further, mutual fund investment decisions are partially driven by (retail) customer funds flows and, therefore,mutual fund ownership changes reflect effects related to private investor sentiment and liquidity needs. Incontrast, many of the non-mutual fund investors in our database are longer-term investors, e.g., pension fundsand insurance companies, whose investment decisions are less susceptible to swings in private investor sentimentand liquidity.

11 Market Index is available as a Worldscope data item, but is time-invariant and available for the most recent yearof our study, i.e., 2006. MSCI Index is available on a time-varying basis. We thank Old Mutual AssetManagement for providing these data.

2002 Florou and Pope

The Accounting ReviewNovember 2012

(WS05376) divided by market value of equity at year-end (WS08001); Book-Market, defined as

book value of equity (WS03501) divided by market value of equity at year-end (WS08001);

Earnings-Price, calculated as net income (WS01551) divided by market value of equity at year-end

(WS08001); and Leverage, defined as total liabilities (WS03351) divided by total assets at year-end

(WS02999). Following Daske et al. (2008), we also include US GAAP (WS07536), a dummy

variable equal to 1 if a non-U.S. firm prepares its financial statements according to U.S. financial

reporting rules, and Market Benchmark, calculated as the yearly mean of the dependent variable

from all observations in the benchmark sample. The latter variable is used to help us disentangle the

IFRS effects from effects due to changes in the general economic conditions or changes in

institutional holdings unrelated to IFRS reporting. All continuous variables are winsorized at the

extreme 1 percentiles.

To perform the firm-quarter analysis, we incorporate in Equation (1) only those control

variables that can be measured at the end of a quarter, i.e., Size, Ret, RetVar, and Market

Benchmark. In the country-quarter analysis based on Equation (2) we include the natural logarithm

of Market Value (WS08001), measured as stock price times the number of shares outstanding (in

U.S. dollars) at the end of quarter q�3; Return Variability, defined as the standard deviation of the

previous 12 monthly stock returns measured at time q�3; Market Benchmark, defined as the mean

dependent value from all observations in the benchmark sample; and the level and the change in the

dependent variables measured at time q�3.

Sample and Descriptive Statistics

We include all listed firms in the Worldscope database in the period 2003–2006 with

complete data for the independent variables and for which ownership data are available in the

TFO database.12 For firms that adopt IFRS for fiscal years ending December 2005, this sample

period allows us to compare changes in institutional holdings in the year prior to mandatory

IFRS adoption, the transition year, and the year after first-time adoption. Applying these criteria

yields a sample of 35,160 firm-years for 10,852 unique firms and 45 countries. Table 1 describes

the sample composition across years and countries. Panel A indicates that 9.61 percent (4.92

percent) of firm-years in the overall sample are mandatory (voluntary) IFRS adopters.

Mandatory IFRS reporters represent 14.15 percent (21.93 percent) of sample observations for

fiscal years ending in 2005 (2006), indicating that a substantial number of firms adopt IFRS for

the first time for fiscal years ending in 2006 rather than 2005. Panel B of Table 1 shows the

country composition of the IFRS treatment sample, which includes 11,926 observations from

3,865 firms and 24 countries, and the benchmark sample, which comprises 23,234 firm-year

observations from 6,987 firms and 21 countries.13 As in prior studies adopting a similar

sampling frame, the U.S. accounts for approximately 43 percent of benchmark sample

observations. We test whether our main results are sensitive to the weight of the U.S. in the

benchmark sample in robustness checks.

Table 2 describes the institutional holdings variables. Panel A reveals that over the full

12 We constrain the sample to end in 2006 because extending the sample period beyond 2006 would increase therisk that any observed changes in institutional holdings in treatment firms relative to benchmark firms are due tofactors other than IFRS adoption.

13 The apparent discrepancy between the 3,380 total IFRS mandatory adopters reported in Panel A and the 3,865total treatment firms reported in Panel B is due to some treatment countries not requiring IFRS reporting by alllisted companies, e.g., because, the firms do not report consolidated financial statements. Singapore is excludedfrom our sample because it mandated adoption of IFRS in 2003, in contrast to all other countries in our treatmentsample where the adoption date was 2005.

Mandatory IFRS Adoption and Institutional Investment Decisions 2003

The Accounting ReviewNovember 2012

TABLE 1

IFRS Adoption by Year and Sample Composition by Country

Panel A: IFRS Adoption for Full Sample by Year

Year Total Firm-Years

First-Time Mandatory Adopters Voluntary Adopters

Firm-Years Percent Firm-Years Percent

2003 8,385 0 0.00 458 5.46

2004 8,364 0 0.00 468 5.60

2005 8,450 1,196 14.15 399 4.72

2006 9,961 2,184 21.93 406 4.08

Total 35,160 3,380 9.61 1,731 4.92

Panel B: Sample Composition by Country

Treatment Firms Firm-Years Benchmark Firms Firm-Years

Australia 482 1,271 Argentina 36 121

Austria 42 138 Bermuda 10 26

Belgium 63 226 Brazil 76 240

Czech Republic 9 26 Canada 459 1,530

Denmark 99 300 Chile 72 145

Finland 90 304 China 33 95

France 395 1,377 Colombia 10 22

Germany 282 953 Egypt 15 40

Greece 94 262 India 64 175

Hong Kong 529 1,451 Indonesia 95 261

Hungary 19 61 Israel 62 197

Ireland 41 143 Japan 2,097 6,838

Italy 160 546 Korea (South) 246 602

Luxemburg 14 53 Malaysia 372 1,018

The Netherlands 95 316 Mexico 50 142

Norway 72 235 New Zealand 27 72

Philippines 66 163 Russia 12 34

Poland 72 215 Taiwan 418 1,141

Portugal 27 101 Thailand 133 357

South Africa 113 405 Turkey 41 77

Spain 96 342 United States 2,659 10,101

Sweden 112 238

Switzerland 150 376

U.K. 743 2,424

Total 3,865 11,926 Total 6,987 23,234

The complete sample consists of a maximum 35,160 firm-year observations from 45 countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data from Worldscope to perform the regressionanalysis. We exclude countries with less than 20 firm-year observations.Panel A reports descriptive information for the following indicators: (1) First-Time Mandatory that refers to observationsof firms that never reported under IFRS before mandatory adoption and equals 1 for all firm-years with IFRS reportingperiods ending on or after the local mandated IFRS adoption date (i.e., December 31, 2005), and 0 otherwise; and (2)Voluntary that relates to observations of firms that voluntarily switched to IFRS reporting before it was mandated andequals 1 for all firm-years with IFRS reporting by voluntary adopters, and 0 otherwise.Panel B reports the number of firms and firm-years for: (1) the treatment sample, i.e., countries that mandated IFRSreporting and (2) the benchmark sample, i.e., countries that do not allow or do not require IFRS reporting.

2004 Florou and Pope

The Accounting ReviewNovember 2012

sample mean (median) institutional ownership is 21.69 percent (6.93 percent) of issued equity

and the mean (median) number of institutional shareholders is 74.88 (18.00). The changes in

both institutional holdings proxies are, on average, positive over the sample period. Panels B and

C provide insights to the importance of different investor types in our data. Most firms have

active institutional investors—on average there are 63.72 active investors owning 18.62 percent

of equity. In contrast, passive investors have lower overall equity stakes than active investors

and are fewer in number—on average 11.16 passive investors own equity stakes totaling 3.22

percent of equity. Analysis of investment styles reveals that growth and value investors hold

stakes in a large proportion of sample firm-years and holdings are economically significant. For

example, value investors hold mean equity stakes of 5.94 percent.

TABLE 2

Descriptive Statistics for Institutional Holdings

Panel A: Full Sample

Variable Obs. Mean Median Std. Dev.

Percentage Ownership 33,131 21.69 6.93 0.291

DPercentage Ownership 21,726 2.67 0.87 0.079

Number of Investors 34,330 74.88 18.00 150.100

DNumber of Investors 22,826 10.38 3.00 28.130

Panel B: Percentage Ownership for Full Sample by Investor Type

Investor Type Obs. Mean Median Std. Dev.

Active 33,131 18.62 6.63 0.245

Passive 33,131 3.22 0.00 0.062

Growth 33,131 5.40 1.75 0.083

Value 33,131 5.94 1.22 0.095

Income 33,131 0.55 0.00 0.019

Index 33,131 2.67 0.00 0.052

Panel C: Number of Investors for Full Sample by Investor Type

Investor Obs. Mean Median Std. Dev.

Active 34,330 63.72 16.00 133.47

Passive 34,330 11.16 1.00 19.77

Growth 34,330 23.35 7.00 49.32

Value 34,330 18.30 4.00 39.44

Income 34,330 2.38 0.00 7.67

Index 34,330 6.53 0.00 11.03

The complete sample consists of a maximum 35,160 firm-year observations from 45 countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data from Worldscope to perform the regressionanalysis. Percentage Ownership is defined as the total market value of shares owned by institutions divided by the totalmarket value of the firm at year-end, where both items are measured in U.S. dollars. Number of Investors refers to thetotal number of institutional investors of the firm at year-end. D denotes changes in variables computed over year t�1 to t.Additional descriptive information is provided conditioning on: (1) Investment Orientation, i.e., active versus passiveinvestors and (2) Investment Style, i.e., value/growth versus index/income investors.

Mandatory IFRS Adoption and Institutional Investment Decisions 2005

The Accounting ReviewNovember 2012

Table 3 describes the control variables used in our regression tests and Table 4 shows the

correlations between the independent variables. Descriptive statistics are pooled over the full

sample. The data do not suggest any unusual behavior.14

IV. EMPIRICAL RESULTS

In this section we discuss our empirical findings. First, we report univariate difference-

in-differences results, followed by baseline regression results capturing the average effects of

TABLE 3

Descriptive Statistics of Independent Variables

Variable (n = 35,160) Mean Median Std. Dev.

Size 5.99 5.86 1.853

ROE (%) 6.34 9.68 0.414

RET (%) 19.38 18.29 0.429

RetVar 0.102 0.086 0.062

Leverage 0.521 0.515 0.262

Dividend Yield 0.016 0.009 0.022

Book-Market 0.669 0.539 0.608

Earnings-Price 0.004 0.047 0.219

Nanalysts 4.426 2.000 6.064

Big4 0.855 1.000 0.351

MSCI Index 0.103 0.000 0.304

Market Index 0.527 1.000 4.999

ADR 0.067 0.000 0.251

US GAAP 0.018 0.000 0.133

The complete sample consists of a maximum 35,160 firm-year observations from 45 countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data from Worldscope to perform the regressionanalysis.All financial variables are winsorized at the 1st and 99th percentiles.

Variable Definitions:Size¼ the natural logarithm of market value of equity in U.S. dollars;ROE ¼ net income before extraordinary items divided by total assets at the beginning of the year;RET ¼ log of (RItþ1/RIt), where RI stands for Return Index on January 1st;RetVar ¼ standard deviation of monthly stock returns over the fiscal year;Leverage ¼ total liabilities divided by total assets;Dividend Yield ¼ total dividends divided by market value of equity;Book-Market ¼ book value of equity divided by market value of equity;Earnings-Price ¼ net income divided by market value of equity;Nanalysts ¼ number of analysts;Big4 ¼ dichotomous variable equal to 1 if the firm is audited by a Big 4 auditing firm or their predecessors, and 0

otherwise;MSCI Index ¼ binary variable equals 1 if the firm is included in the MSCI World Index, and 0 otherwise;Market Index ¼ dummy variable equals 1 if the firm is part of any stock market index, and 0 otherwise;ADR ¼ dummy that takes the value of 1 if the firm has an ADR listed on a U.S. exchange, and 0 otherwise; andUS GAAP¼dummy variable equal to 1 if a non-U.S. firm prepares its financial statements according to the U.S. financial

reporting rules, and 0 otherwise.

14 Untabulated findings document low correlations among the institutional factors employed in our cross-sectionanalysis, Absence, Divergence, and Cluster 1 and Cluster 2 indicators.

2006 Florou and Pope

The Accounting ReviewNovember 2012

IFRS adoption on holdings changes measured over different annual windows. Second, we

provide further analysis showing that changes in institutional holdings are concentrated in the first

quarter after first-time mandatory IFRS reporting. Third, we present results of the country-quarter

analysis. Fourth, we report additional findings on the IFRS-related ownership effects across

different types of investors. Fifth, we discuss results on the dependence between IFRS-related

holdings changes and country-level institutional factors capturing reporting incentives,

compliance, and accounting differences. Finally, we describe a series of additional tests and

robustness checks.

TABLE 4

Correlations between Independent Variables

Panel A: Correlations of Variables First-Time Mandatory to Book-Market

First-TimeMandatory Voluntary RET ROE Leverage

DividendYield

Book-Market

Voluntary �0.074

RET 0.034 0.013

ROE 0.045 �0.001 0.135

Leverage 0.051 0.045 �0.009 �0.001

Dividend Yield 0.063 0.002 �0.028 0.147 0.023

Book-Market �0.070 �0.008 �0.053 �0.019 �0.190 0.139

Price-Earnings 0.028 �0.004 0.220 0.394 �0.152 0.177 0.084

Size 0.013 0.047 0.144 0.216 0.130 0.063 �0.246

RetVar �0.069 �0.053 0.104 �0.237 �0.042 �0.270 �0.106

Nanalysts 0.034 0.077 �0.005 0.120 0.065 0.002 �0.227

Market Index �0.005 �0.000 0.032 0.107 0.109 0.070 �0.017

Big5 �0.068 0.010 0.011 0.035 0.039 0.046 �0.057

ADR 0.061 0.065 0.021 0.024 0.036 0.064 �0.026

MSCI Index 0.041 0.033 �0.000 0.058 0.071 0.018 �0.090

US GAAP �0.044 �0.013 �0.002 �0.008 �0.024 �0.029 �0.017

Panel B: Correlations of Variables Price-Earnings to MSCI Index

Price-Earnings Size RetVar Nanalysts

MarketIndex Big5 ADR

MSCIIndex

Size 0.270

RetVar �0.351 �0.354

Nanalysts 0.101 0.701 �0.197

Market Index 0.125 0.532 �0.230 0.359

Big5 0.060 0.264 �0.080 0.179 0.139

ADR 0.018 0.251 �0.051 0.245 0.132 0.068

MSCI Index 0.049 0.413 �0.146 0.403 0.252 0.065 0.166

US GAAP �0.021 0.074 0.025 0.099 �0.009 0.029 0.195 0.067

The complete sample consists of a maximum 35,160 firm-year observations from 45 countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data from Worldscope to perform the regressionanalysis.Pearson’s correlation coefficients between independent variables are reported. All financial variables are winsorized atthe 1st and 99th percentiles. For variable definitions see Tables 1 and 3.

Mandatory IFRS Adoption and Institutional Investment Decisions 2007

The Accounting ReviewNovember 2012

Difference-in-Differences Analysis

Table 5 presents difference-in-differences analyses showing the contrast between institutional

holdings changes for the treatment and benchmark samples over the pre-IFRS period (2004), the

IFRS adoption year (2005) and the post-IFRS period (2006). We report results for changes in our

two institutional holdings proxies, Percentage Ownership and Number of Investors.

The differences between treatment sample and benchmark sample holdings changes in the

bottom row of each panel indicate that changes in institutional holdings are significantly higher in

the benchmark sample in the pre-IFRS year and the transition year for both holdings proxies. In

contrast, institutional holdings changes in the post-IFRS year are significantly higher in the

treatment sample. Both panels reveal that institutional holdings grow over the sample period for

TABLE 5

Difference-in-Differences Analyses of Ownership

Panel A: Difference-in-Differences Analysis for DPercentage Ownership

SamplePre-IFRS

(a)

TransitionPeriod

(b)Post-IFRS

(c) (b) � (a) (c) � (a)

Benchmark (i ) 2.14 2.20 3.95 0.06 1.81

(n ¼ 4,614) (n ¼ 4,759) (n ¼ 5,050) (0.699) (0.000)

Treatment (ii ) 0.27 0.30 6.31 0.03 6.04

(n ¼ 2,358) (n ¼ 2,339) (n ¼ 2,606) (0.845) (0.000)

(ii ) � (i ) �1.87 �1.90 2.36 �0.03 4.23

(0.000) (0.000) (0.000) (0.647) (0.000)

Panel B: Difference-in-Differences Analysis for DNumber of Investors

SamplePre-IFRS

(a)

TransitionPeriod

(b)Post-IFRS

(c) (b) � (a) (c) � (a)

Benchmark (i ) 7.21 7.17 18.53 �0.04 11.32

(n ¼ 5,017) (n ¼ 5,043) (n ¼ 5,294) (0.936) (0.000)

Treatment (ii ) 0.64 1.81 23.10 1.17 22.46

(n ¼ 2,459) (n ¼ 2,393) (n ¼ 2,620) (0.001) (0.000)

(ii ) � (i ) �6.57 �5.36 4.57 1.21 11.14

(0.000) (0.000) (0.000) (0.038) (0.000)

The complete sample consists of a maximum 35,160 firm-year observations from 45 countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data from Worldscope to perform the regressionanalysis.Panels A and B report results from difference-in-differences analysis of the IFRS-related ownership effects; p-values inparentheses.Percentage Ownership is defined as the total market value of shares owned by institutions divided by the total marketvalue of the firm at year-end, where both items are measured in U.S. dollars. Number of Investors refers to the totalnumber of institutional investors of the firm at year-end. D denotes changes in variables computed over year t�1 to t. Thetreatment sample consists of countries that mandated IFRS reporting and the benchmark sample includes countries thatdo not allow or do not require IFRS reporting. The pre-IFRS period refers to changes in 2004, while the transition periodand the post-IFRS period relate to changes over 2005 and 2006, respectively.

2008 Florou and Pope

The Accounting ReviewNovember 2012

both the treatment and the benchmark samples. Mean changes in percentage ownership and

number of investors are uniformly positive for all sample periods. However, the final two

columns indicate that differences in percentage ownership changes are significant only in the

post-IFRS period. Results for the change in the number of investors indicate relatively large

increases in the post-IFRS period and a small increase in the IFRS implementation year relative to

the pre-IFRS year. The observation that benchmark sample holdings also increase in the post-

IFRS period emphasizes the importance of controlling for common global factors underpinning

institutional holdings changes.

The difference-in-differences results at the bottom right-hand side of each panel indicate that

treatment sample firms have statistically and economically significantly higher holdings changes in

the post-IFRS period compared to benchmark sample firms. These results provide the first evidence

that mandatory IFRS reporting has a positive impact on institutional holdings. We now examine

whether coincident changes in other determinants of institutional holdings can explain the IFRS

reporting effects.

Baseline Findings

Table 6 presents the results of estimating Equation (1) for the full sample. These and

subsequent regression results are estimated with industry-year fixed effects captured by indicator

variables using the industry classifications in Campbell (1996), country dummy variables based on

Worldscope nation code (WS06027), and White standard errors adjusted to account for correlation

within firm clusters (Rogers 1994; Petersen 2009).

In Table 6, Panel A the changes in institutional holdings proxies are measured over calendar-

year intervals, where the mandatory IFRS period is defined as 2005 and 2006. Hence, the estimated

coefficients on First-Time Mandatory and Voluntary � Mandatory capture average effects over the

two-year period. Empirical findings indicate that there is an increase in average institutional

ownership of 2.2 percent per annum for first-time mandatory IFRS adopters, after controlling for

global changes affecting benchmark sample firms and changes in other firm-level determinants of

institutional ownership. Similarly, the number of investors in mandatory IFRS adopters increases by

nearly five relative to benchmark firms in the IFRS adoption period. The positive coefficient on

Voluntary � Mandatory suggests that voluntary adopters also experience an increase in institutional

holdings at the time of mandated adoption. This result is in line with Yu (2010) and with the

liquidity effects for voluntary adopters at the time of mandated adoption reported by Daske et al.

(2008). A possible explanation is that voluntary adopters also benefit from increased comparability

when IFRS is mandated (Daske et al. 2008; DeFond et al. 2011).

In Table 6, Panel B the changes in institutional holdings are measured over different annual

intervals ordered relative to the fiscal year-end of each firm. Results for both alternative windows

�2/þ2 and �1/þ3 are consistent with those in Panel A, indicating statistically and economically

significant ownership effects for first-time mandatory IFRS adopters. First-Time Mandatory and

Voluntary � Mandatory coefficient estimates for both holdings proxies are higher for the �2/þ2

interval than for the calendar-year intervals. However, the R2 statistics are considerably lower for

both alternative windows, suggesting that this research design does not control as effectively for

unmodeled factors.

Firm-Quarter Analysis

The results in Table 6 capture the average institutional holdings effects associated with IFRS

reporting measured over annual intervals. To alleviate concerns that these results could reflect

factors other than IFRS reporting, we now examine the timing of institutional ownership changes

Mandatory IFRS Adoption and Institutional Investment Decisions 2009

The Accounting ReviewNovember 2012

TABLE 6

Changes in Institutional Holdings and IFRS Mandatory AdoptionFirm-Annual Analysis

Panel A: Base Model

Independent Variables

DPercentageOwnership

(1)

DNumber ofInvestors

(2)

First-Time Mandatory 0.022 4.938

(0.000) (0.000)

Voluntary 0.008 1.970

(0.002) (0.091)

Voluntary � Mandatory 0.006 4.027

(0.034) (0.003)

DSize 0.046 18.38

(0.000) (0.000)

DROE �0.002 0.134

(0.162) (0.718)

DRET �0.013 �3.929

(0.000) (0.000)

DRetVar �0.051 �0.087

(0.000) (0.976)

DLeverage �0.013 �6.636

(0.079) (0.000)

DDividend Yield �0.039 0.658

(0.224) (0.934)

DBook-Market 0.006 1.753

(0.001) (0.000)

DEarnings-Price 0.000 �3.352

(0.925) (0.000)

DNanalysts 0.002 1.623

(0.000) (0.000)

DBig4 �0.042 5.112

(0.000) (0.000)

DMSCI Index �0.008 0.304

(0.000) (0.683)

DUS GAAP 0.004 2.094

(0.450) (0.475)

DMarket Benchmark 2.327 1.760

(0.000) (0.000)

Intercept �0.088 �31.22

(0.000) (0.000)

Country Dummies Yes Yes

Industry-Year Dummies Yes Yes

No. Observations 21,726 22,826

No. Countries 45 45

Adj. R2 12.5% 18.5%

(continued on next page)

2010 Florou and Pope

The Accounting ReviewNovember 2012

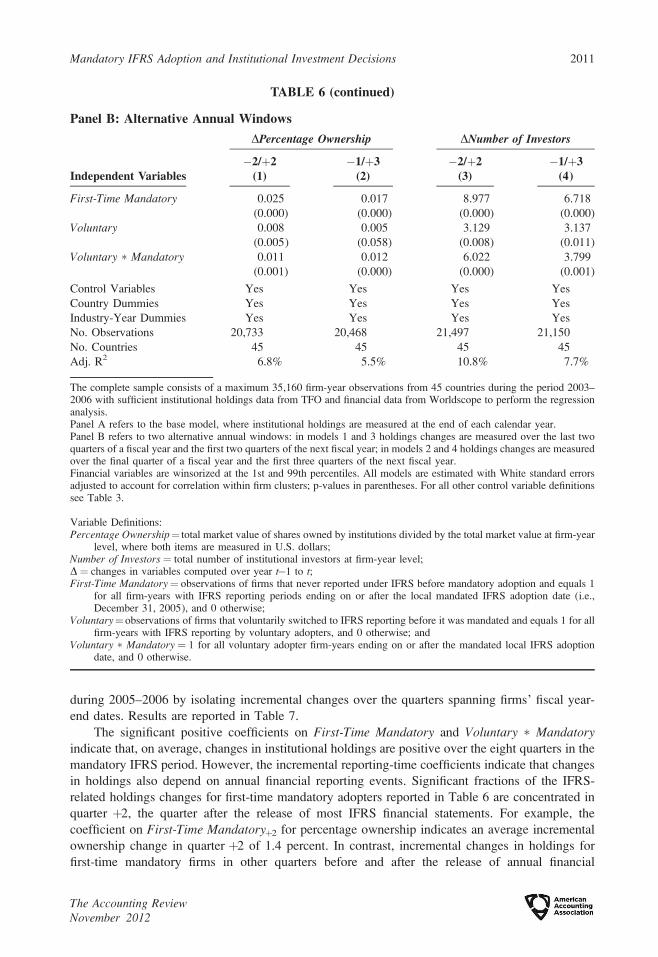

during 2005–2006 by isolating incremental changes over the quarters spanning firms’ fiscal year-

end dates. Results are reported in Table 7.

The significant positive coefficients on First-Time Mandatory and Voluntary � Mandatoryindicate that, on average, changes in institutional holdings are positive over the eight quarters in the

mandatory IFRS period. However, the incremental reporting-time coefficients indicate that changes

in holdings also depend on annual financial reporting events. Significant fractions of the IFRS-

related holdings changes for first-time mandatory adopters reported in Table 6 are concentrated in

quarter þ2, the quarter after the release of most IFRS financial statements. For example, the

coefficient on First-Time Mandatoryþ2 for percentage ownership indicates an average incremental

ownership change in quarter þ2 of 1.4 percent. In contrast, incremental changes in holdings for

first-time mandatory firms in other quarters before and after the release of annual financial

TABLE 6 (continued)

Panel B: Alternative Annual Windows

Independent Variables

DPercentage Ownership DNumber of Investors

�2/þ2(1)

�1/þ3(2)

�2/þ2(3)

�1/þ3(4)

First-Time Mandatory 0.025 0.017 8.977 6.718

(0.000) (0.000) (0.000) (0.000)

Voluntary 0.008 0.005 3.129 3.137

(0.005) (0.058) (0.008) (0.011)

Voluntary � Mandatory 0.011 0.012 6.022 3.799

(0.001) (0.000) (0.000) (0.001)

Control Variables Yes Yes Yes Yes

Country Dummies Yes Yes Yes Yes

Industry-Year Dummies Yes Yes Yes Yes

No. Observations 20,733 20,468 21,497 21,150

No. Countries 45 45 45 45

Adj. R2 6.8% 5.5% 10.8% 7.7%

The complete sample consists of a maximum 35,160 firm-year observations from 45 countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data from Worldscope to perform the regressionanalysis.Panel A refers to the base model, where institutional holdings are measured at the end of each calendar year.Panel B refers to two alternative annual windows: in models 1 and 3 holdings changes are measured over the last twoquarters of a fiscal year and the first two quarters of the next fiscal year; in models 2 and 4 holdings changes are measuredover the final quarter of a fiscal year and the first three quarters of the next fiscal year.Financial variables are winsorized at the 1st and 99th percentiles. All models are estimated with White standard errorsadjusted to account for correlation within firm clusters; p-values in parentheses. For all other control variable definitionssee Table 3.

Variable Definitions:Percentage Ownership¼ total market value of shares owned by institutions divided by the total market value at firm-year

level, where both items are measured in U.S. dollars;Number of Investors ¼ total number of institutional investors at firm-year level;D¼ changes in variables computed over year t�1 to t;First-Time Mandatory¼ observations of firms that never reported under IFRS before mandatory adoption and equals 1

for all firm-years with IFRS reporting periods ending on or after the local mandated IFRS adoption date (i.e.,December 31, 2005), and 0 otherwise;

Voluntary¼observations of firms that voluntarily switched to IFRS reporting before it was mandated and equals 1 for allfirm-years with IFRS reporting by voluntary adopters, and 0 otherwise; and

Voluntary � Mandatory ¼ 1 for all voluntary adopter firm-years ending on or after the mandated local IFRS adoptiondate, and 0 otherwise.

Mandatory IFRS Adoption and Institutional Investment Decisions 2011

The Accounting ReviewNovember 2012

TABLE 7

Changes in Institutional Holdings and IFRS Mandatory AdoptionFirm-Quarter Analysis

Independent Variables

DPercentageOwnership

(1)

DNumber ofInvestors

(2)

First-Time Mandatory 0.003 0.535

(0.000) (0.000)

Voluntary 0.002 0.435

(0.006) (0.021)

Voluntary � Mandatory 0.002 0.501

(0.025) (0.013)

First-Time Mandatory�2 �0.000 �0.322

(0.914) (0.057)

First-Time Mandatory�1 0.001 0.544

(0.358) (0.007)

First-Time Mandatoryþ1 �0.000 0.188

(0.886) (0.347)

First-Time Mandatoryþ2 0.014 4.302

(0.000) (0.000)

First-Time Mandatoryþ3 �0.002 1.081

(0.001) (0.000)

Voluntary � Mandatory�2 �0.003 �1.128

(0.004) (0.000)

Voluntary � Mandatory�1 �0.003 �0.437

(0.005) (0.104)

Voluntary � Mandatoryþ1 �0.004 �1.062

(0.001) (0.000)

Voluntary � Mandatoryþ2 0.017 6.850

(0.000) (0.000)

Voluntary � Mandatoryþ3 0.000 1.238

(0.903) (0.000)

DSize 0.015 8.696

(0.000) (0.000)

DRET �0.009 �6.328

(0.000) (0.000)

DRetVar �0.023 �2.590

(0.000) (0.013)

DMarket Benchmark 1.390 1.112

(0.000) (0.000)

Intercept �0.012 �3.484

(0.000) (0.000)

Country Dummies Yes Yes

Industry-Year Dummies Yes Yes

No. Observations 85,741 89,368

No. Countries 45 45

Adj. R2 9.5% 15.5%

The sample in models 1 and 2 consists of a maximum 85,741 and 89,368 firm-quarter observations, respectively, from 45countries during the period 2003–2006 with sufficient institutional holdings data from TFO and financial data fromWorldscope to perform the regression analysis.

(continued on next page)

2012 Florou and Pope

The Accounting ReviewNovember 2012

statements are generally small in economic terms, and with three exceptions, statistically

insignificant.15

The coefficients on Voluntary � Mandatoryþ2 indicate that the incremental holding changes for

voluntary adopters in quarter þ2 are also positive and significant in economic terms, again

accounting for a large fraction of the overall change documented for voluntary adopters in the

mandated IFRS period. However, in contrast to the results for mandatory adopters, incremental

holdings changes for voluntary adopters in the three prior quarters�2,�1, andþ1 are significantly

negative, implying that institutional holdings in these firms fall in the quarters leading up to the

mandating of IFRS for other firms and suggesting that holdings changes follow different dynamics

for voluntary compared to first-time adopters. Overall, the results in Table 7 provide reassurance

that the main results reported in Table 6 are associated with financial reporting events in the

mandatory IFRS period.

Country-Quarter Analysis

We now report the results of the country-quarter analysis, based on Equation (2). In this

analysis we run regressions of the quarterly aggregate change in median institutional holdings in a

country on the change in the adoption rate in that country in the previous quarter. In the first

analysis we estimate the adoption rate index assuming that first-time adoption occurs by the end of

the quarter following the fiscal year-end of first-time adoption (IFRS Adoption RateFYE). We can

measure changes in this variable over five quarters (four quarters in 2006 and the first quarter in

2007), yielding 120 country-quarter observations over the 24 treatment countries. In the second

analysis we base the adoption rate index on actual annual, interim, and quarterly announcement

dates (IFRS Adoption RateINTERIM). We can measure changes in this variable over nine quarters

(four quarters in each of 2005 and 2006 and the first quarter of 2007) yielding 216 country-quarter

observations over the 24 treatment countries. Panel A of Table 8 reports descriptive statistics for

TABLE 7 (continued)

Financial variables are winsorized at the 1st and 99th percentiles. All models are estimated with White standard errorsadjusted to account for correlation within firm clusters; p-values in parentheses. For all other control variable definitionssee Table 3.

Variable Definitions:Percentage Ownership¼ total market value of shares owned by institutions divided by the total market value of the firm

at the end of a quarter, where both items are measured in U.S. dollars;Number of Investors ¼ total number of institutional investors at firm-quarter level;D¼ changes in variables computed over quarter q�1 to q;First-Time Mandatory¼ observations of firms that never reported under IFRS before mandatory adoption and equals 1

for all firm-years with IFRS reporting periods ending on or after the local mandated IFRS adoption date (i.e.,December 31, 2005), and 0 otherwise;

Voluntary¼observations of firms that voluntarily switched to IFRS reporting before it was mandated and equals 1 for allfirm-years with IFRS reporting by voluntary adopters, and 0 otherwise;

Voluntary � Mandatory ¼ 1 for all voluntary adopter firm-years ending on or after the mandated local IFRS adoptiondate, and 0 otherwise; and

First-Time Mandatoryq (q¼�2,�1,þ1,þ2,þ3)¼1 in quarter q and 0 in other quarters, using the convention that q¼�1is the quarter of the fiscal year-end and q¼þ1 is the quarter following the fiscal year-end. The indicator variablesVoluntary � Mandatoryq are defined in an exactly analogous manner to First-Time Mandatoryq.

15 The sum of the First-Time Mandatoryq coefficients in Table 7 closely reconcile with the First-Time Mandatorycoefficient in Table 6. From Table 7 the estimated total holdings change over the two-year period 2005–2006 is 83 First-Time MandatoryþRqFirst-Time Mandatoryq, giving 0.037 (10.07) for percentage ownership (number ofinvestors). The equivalent estimated changes from Table 6 over the two years equal to 2 3 First-TimeMandatory, giving 0.044 (9.876) for the above two holdings proxies, respectively.

Mandatory IFRS Adoption and Institutional Investment Decisions 2013

The Accounting ReviewNovember 2012

TABLE 8

Country-Quarter Analysis of the Effects of Mandatory IFRS Adoption on InstitutionalHoldings

Panel A: Descriptive Statistics of Dependent and Independent Variables Used in theCountry-Quarter Analysis

Variable Obs. Mean Median Std. Dev

DPercentage Ownership 120 0.42 0.00 0.038

216 0.25 �0.00 0.031

DNumber of Investors 120 0.85 0.00 5.732

216 0.53 0.00 5.254

DIFRS Adoption RateFYE (%) 120 18.13 6.76 0.253

DIFRS Adoption RateINTERIM (%) 216 19.66 14.14 0.168

Market Value 120 592.2 377.2 900.700

216 517.6 329.1 779.000

Return Variability 120 0.076 0.075 0.016

216 0.078 0.076 0.017

DMarket BenchmarkPercentageOwnership 120 �0.21 0.00 0.008

216 0.07 0.02 0.012

DMarket BenchmarkNumber of Investors 120 �0.03 0.03 1.466

216 0.16 0.03 2.352

Panel B: Regression Analysis

Independent Variables

DPercentage OwnershipQþ1 DNumber of InvestorsQþ1

AnnualReports

(1)

Interim andAnnualReports

(2)

AnnualReports

(3)

Interim andAnnualReports

(4)

DIFRS Adoption RateFYE,Q 0.042 — 7.354 —

(0.002) (0.002)

DIFRS Adoption RATEINTERIM,Q — 0.050 — 12.58

(0.002) (0.000)

Log (Market ValueQ�3) �0.025 �0.010 �6.332 1.345

(0.309) (0.154) (0.222) (0.579)

Return VariabilityQ�3 0.075 �0.327 9.750 �34.49

(0.889) (0.117) (0.927) (0.376)

Dependent VariableQ�3 �2.040 �1.048 0.070 �0.343

(0.000) (0.000) (0.907) (0.455)

DDependent VariableQ�3 2.111 1.326 �0.106 0.056