marc schmittlein president & ceo – select accounts

TRANSCRIPT

Marc Marc SchmittleinSchmittlein

President & CEO President & CEO –– Select AccountsSelect Accounts

Keefe, Keefe, BruyetteBruyette & Woods & Woods Insurance ConferenceInsurance Conference

September 8, 2010September 8, 2010

1

This presentation contains, and management may make, certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical facts, may be forward-looking statements. Specifically, earnings guidance, statements about the Company’s share repurchase plans (which repurchase plans depend on a variety of factors, including the Company’s financial position, earnings, capital requirements of the Company’s operating subsidiaries, legal requirements, regulatory constraints. catastrophe losses, other investment opportunities (including mergers and acquisitions), market conditions and other factors) and statements about the potential impact of recent or future disruption in the investment markets and other economic conditions on the Company’s investment portfolio and underwriting results, among others, are forward looking, and the Company may make forward-looking statements about, among other things, its results of operations (including, among others, premium volume, premium rates (either for new or renewal business), net and operating income, investment income and performance, return on equity, expected current returns and combined ratio) and financial condition; the sufficiency of the Company’s asbestos and other reserves (including, among others, asbestosclaim payment patterns); the impact of emerging claims issues; the cost and availability of reinsurance coverage; catastrophe losses; the impact of investment, economic and underwriting marketconditions; and strategic initiatives. The Company cautions investors that such statements are subject to risks and uncertainties, many of which are difficult to predict and generally beyond the Company’s control, that could cause actual results to differ materially from those expressed in, or implied or projected by, the forward-looking information and statements.

Some of the factors that could cause actual results to differ include, but are not limited to, the following: catastrophe losses could materially and adversely affect the Company’s results of operations, its financial position and/or liquidity, and could adversely impact the Company’s ratings, the Company’s ability to raise capital and the availability and cost of reinsurance; during or following a period of financial market disruption or prolonged economic downturn, the Company’s business could be materially and adversely affected; the Company’s investment portfolio may suffer reduced returns or material losses, including as a result of a challenging economic environment that impacts the credit of municipal or other issuers in the company’s portfolio; if actual claims exceed the Company’s loss reserves, or if changes in the estimated level of loss reserves are necessary, the Company’s financial results could be materially and adversely affected; the Company’s business could be harmed because of its potential exposure to asbestos and environmental claims and related litigation; the Company is exposed to, and may face adverse developments involving, mass tort claims such as those relating to exposure to potentially harmful products or substances; the effects of emerging claim and coverage issues on the Company’s business are uncertain; the intense competition that the Company faces could harm its ability to maintain or increase its business volumes and profitability; the Company may not be able to collect all amounts due to it from reinsurers, and reinsurance coverage may not be available to the Company in the future at commercially reasonable rates or at all; the Company is exposed to credit risk in certain of its business operations; the Company’s businesses are heavily regulated and changes in regulation (including as a result of the adoption of financial services reform legislation) may reduce the Company’s profitability and limit its growth; a downgrade in the Company’s claims-paying and financial strength ratings could adversely impact the Company’s business volumes, adversely impact the Company’s ability to access the capital markets and increase the Company’s borrowing costs; the inability of the Company’s insurance subsidiaries to pay dividends to the Company’s holding company in sufficient amounts would harm the Company’s ability to meet its obligations and to pay future shareholder dividends; disruptions to the Company’s relationships with its independent agents and brokers could adversely affect the Company; the Company’s efforts to develop new products (including its direct to consumer initiative in Personal Insurance) or expand in targeted markets may not be successful, may create enhanced risks and may adversely impact results; the Company’s business success and profitability depend, in part, on effective information technology systems and on continuing to develop and implement improvements in technology; if the Company experiences difficulties with technology, data security and/or outsourcing relationships the Company’s ability to conduct its business could be negatively impacted; acquisitions and integration of acquired businesses may result in operating difficulties and other unintended consequences; the Company is subject to a number of risks associated with its business outside the United States; the Company could be adversely affected if its controls to ensure compliance with guidelines, policies and legal and regulatory standards are not effective; the Company’s businesses may be adversely affected if it is unable to hire and retain qualified employees; and loss of or significant restriction on the use of credit scoring in the pricing and underwriting of Personal Insurance products could reduce the Company’s future profitability.

Our forward-looking statements speak only as of the date of this presentation or as of the date they are made, and we undertake no obligation to update our forward-looking statements. For a more detailed discussion of these factors, see the information under the caption "Risk Factors" in our most recent annual report on Form 10-K filed with the Securities and Exchange Commission and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our most recent annual report on Form 10-K and our quarterly report on Form 10-Q filed with the Securities and Exchange Commission.

Explanatory NoteExplanatory Note

In this presentation, we may refer to some non-GAAP financial measures. For a reconciliation of these measures to the most comparable GAAP measures and a glossary of financial measures, we refer you to the most recent earnings press release and financial supplement which are available on the Travelers website under the investor section (www.travelers.com).

2

•• Overview Overview –– Select AccountsSelect Accounts

•• Formula for Success Formula for Success –– TravelersTravelersExpressExpressSMSM

•• Results Results –– TravelersTravelersExpressExpressSMSM

•• OnOn--going Initiativesgoing Initiatives

•• Q & AQ & A

3

Target Risk

Underwriting

Industry-Focused Underwriting

Spec. Dist.

Commercial Accounts

SelectAccounts

Nat'lAccts

Internat'l

Bond & FinancialProducts

Automobile

Homeowners & Other

OverviewOverview

Travelers Full Year 2009 Net Written Premiums: $21.3 BillionTravelers Full Year 2009 Net Written Premiums: $21.3 Billion

Personal InsurancePersonal Insurance$7.1 Billion$7.1 Billion

Business InsuranceBusiness Insurance$10.9 Billion$10.9 Billion

Financial, Professional & Financial, Professional & International InsuranceInternational Insurance

$3.3 Billion$3.3 Billion

4

Target Risk

Underwriting

Industry-Focused Underwriting

Spec. Dist.

Commercial Accounts

Nat'lAccts

Internat'l

Bond & FinancialProducts

Automobile

Homeowners & Other

Overview Overview -- Select AccountsSelect Accounts

Business Insurance Full Year 2009 Net Written Premiums: $10.9 BiBusiness Insurance Full Year 2009 Net Written Premiums: $10.9 Billionllion

Select AccountsSelect Accounts2009 NWP: $2.8 Billion2009 NWP: $2.8 Billion

• Serves businesses with generally fewer than 50 employees

• Average premium per policy: $3,400

• Primarily commercial multi-peril (CMP), workers’ compensation and commercial auto

• Distribution: 7,900 independent agents

SelectAccounts

5

13.8 Liberty Mutual Holding Co.3

1.7 Bank of America Corp.251.9 Progressive Corp.242.1 Allstate Corp.232.2 Auto-Owners Insurance Co.222.3 QBE Insurance Group Ltd.212.4 Tokio Marine Group202.4 Cincinnati Financial Corp.192.4 XL Capital Ltd182.5 Berkshire Hathaway Inc.172.7 FM Global162.8 Assurant Inc.152.8 Old Republic International143.2 W.R. Berkley Corp.133.4 American Financial Group Inc.124.4 State Farm Mutl Automobile Ins114.6 Allianz SE104.9 Nationwide Mutual Group96.7 Hartford Financial Services86.7 Chubb Corp.76.8 ACE Ltd.67.1 CNA Financial Corp.5

13.1 Zurich Financial Services Ltd4

14.5 Travelers Cos2$ 19.4 American International Group1

DWPDWPCompanyCompany

1.5 Wells Fargo & Co.28

0.8 Radian Group Inc.500.9 AmTrust Financial Services Inc490.9 Assured Guaranty Ltd.480.9 Endurance Specialty Holdings470.9 Swiss Reinsurance Co. Ltd460.9 CUNA Mutual Insurance Society450.9 Westfield Group440.9 Tower Group Inc.431.0 NAU Country Insurance Co.421.0 Employers Mutual Casualty Co.411.0 Harleysville Mutual Ins Co.401.1 Fairfax Financial Holdings Ltd391.1 Argo Group Intl Holdings381.1 Markel Corp.371.1 AXIS Capital Holdings Ltd.361.2 HCC Insurance Holdings Inc.351.2 Erie Insurance Group341.2 Alleghany Corp.331.3 MGIC Investment Corp.321.3 White Mountains Insurance311.4 Hanover Insurance Group Inc.301.4 Selective Insurance Group29

1.5 Munich-American Holding Corp.27$ 1.7 Arch Capital Group Ltd.26

DWPDWPCompanyCompany

0.8 Everest Re Group Ltd.53

0.5 West Bend Mutual Insurance Co.750.5 Utica Mutual Insurance Co.740.5 Amerisure Mutual Insurance Co.730.5 Navigators Group Inc.720.5 ACUITY A Mutual Insurance Co.710.5 American National Insurance700.5 PMA Capital Corp.690.6 Church Mutual Insurance Co.680.6 ProAssurance Corp.670.6 State National Companies Inc.660.6 RLI Corp.650.6 Doctors Co. An Interinsurance640.6 Federated Mutual Insurance Co.630.6 Texas Mutual Insurance Co.620.6 American Family Mutual Ins Co.610.7 Allied World Assurance Co.600.7 Meadowbrook Insurance Group590.7 Genworth Financial Inc.580.7 USAA Insurance Group570.7 State Auto Insurance Cos560.8 Sentry Insurance a Mutual Co.550.8 Medical Liability Mutl Ins Co.54

0.8 Accident Fund Group52$ 0.8 PMI Group Inc.51

DWPDWPCompanyCompany

1Source: SNL Financial (2009 Direct Written Premium data)

14. Travelers Select Accounts 2.8

Overview Overview -- Select AccountsSelect Accounts

Top 75 U.S. Commercial Lines InsurersTop 75 U.S. Commercial Lines Insurers11

Specialization in small commercial - scale mattersSpecialization in small commercial Specialization in small commercial -- scale mattersscale matters

($ in billions)

6

Building competitive advantage for high volume / smaller premium business

Building competitive advantage for high volume / Building competitive advantage for high volume / smaller premium businesssmaller premium business

2009 Net Written Premium

Average PremiumPer Policy

$2.8 Billion$2.8 Billion

$3,400$3,400

TotalTotal Low Low –– TouchTouch(Plus)(Plus)

$1.4 Billion$1.4 Billion

23%23%

$7,400$7,400

No No –– TouchTouch(Express)(Express)

$1.4 Billion$1.4 Billion

77%77%

$2,200 $2,200

• Express success driven by:

– Automated business and underwriting rules

– Pricing and rating sophistication

– Low/no underwriter intervention (straight thru processing)

% of Policies

Overview Overview -- Select AccountsSelect AccountsTravelers Excels at Both Travelers Excels at Both ““EndsEnds”” of the Small Commercial Marketof the Small Commercial Market

7

$67 Billion$67 Billion11

““In AppetiteIn Appetite””

Travelers is the Travelers is the Market Leader Market Leader

With $2.8 Billion With $2.8 Billion of Businessof Business……

……But With But With Significant Significant HeadroomHeadroom

Overview Overview -- Select AccountsSelect Accounts

Small Commercial Small Commercial –– Why Invest?Why Invest?

1Source: Market Stance: commercial multi-peril, commercial auto, workers’ compensation.

8

Overview Overview -- Select AccountsSelect Accounts

Delivering the Small Commercial Value PropositionDelivering the Small Commercial Value Proposition

Solving for Inefficiencies in the Small Commercial MarketplaceSolving for Inefficiencies in the Small Commercial Marketplace

EfficiencyEfficiency

BroadenedBroadenedRiskRisk

AppetiteAppetiteEase of UseEase of Use Consistent Consistent

UnderwritingUnderwriting

9

•• Overview Overview –– Select AccountsSelect Accounts

•• Formula for Success Formula for Success –– TravelersTravelersExpressExpressSMSM

•• Results Results –– TravelersTravelersExpressExpressSMSM

•• OnOn--going Initiativesgoing Initiatives

•• Q & AQ & A

10

Product and Pricing Sophistication

Platform

Class Breadth

Line of Business Breadth

Distribution

A “simple” formula, but all five components are needed and working effectively

A A ““simplesimple”” formula, but all five components are formula, but all five components are needed and working effectivelyneeded and working effectively

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

11

Decline3%

Decline3%

Policy IssuancePolicy

Issuance

Refer to Underwriter

23%

Refer to Underwriter

23%

Automated Bindable Quote (AFI)

77%

Automated Bindable Quote (AFI)

77%

QuoteQuote

Available for Issue (AFI) =Available for Issue (AFI) = Automated Automated bindablebindable quote without underwriter interventionquote without underwriter intervention

Policy IssuancePolicy

Issuance

Note: All percentages as of June 2010

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

Product and Pricing Sophistication / PlatformProduct and Pricing Sophistication / Platform

Automated Decline11%

Automated Decline11%

Predictive Model

(Pricing)

Predictive Model

(Pricing)

Business Rules

Product / EligibilityUnderwriting /

Coverage

Business Rules

Product / EligibilityUnderwriting /

Coverage

Agent Portal

Continue89%

Continue89%

12

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 June 2010

78%78%

CMP CMP

Workers Compensation

Workers Compensation

AutoAuto

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

Product and Pricing Sophistication / PlatformProduct and Pricing Sophistication / Platform

Strategic investment in automated underwriting and pricing driving dramatic increase in “Available for Issue” (AFI)

Strategic investment in automated underwriting and pricing Strategic investment in automated underwriting and pricing driving dramatic increase in driving dramatic increase in ““Available for IssueAvailable for Issue”” (AFI)(AFI)

Percentage of Available for Issue FlowPercentage of Available for Issue FlowAvailable for Issue (AFI) = Automated Available for Issue (AFI) = Automated bindablebindable quote without underwriter interventionquote without underwriter intervention

Commercial MultiCommercial Multi--Peril (CMP) AFIPeril (CMP) AFI WorkersWorkers’’ Compensation AFICompensation AFI Auto AFIAuto AFI Total Policy AFITotal Policy AFI

86%86%

77%77%

56%56%

13

B.O.B.S28%

All Other 72%

1Industry data from Market Stance

B.O.B.S.70%

All Other 30%

IndustryIndustry11

Note: B.O.B.S = Buildings, Office, Business, Stores. All Other = Apartments, Condominiums, Contractors, Garage, Manufacturers, Religious,Restaurants, Technology, Wholesalers.

Mix of New BusinessMix of New Business

TravelersTravelersExpressExpressSMSM ResultsResults

PostPost--Launch Launch (2009)(2009)

PrePre--Launch Launch (2006)(2006)

B.O.B.S.45%

All Other 55%

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

Class BreadthClass Breadth

Broadening reach while growing productionBroadening reach while growing productionBroadening reach while growing production

2006 2006 –– 2009 CAGR2009 CAGR

New business: B.O.B.S. = 9% / All Other = 34%

14

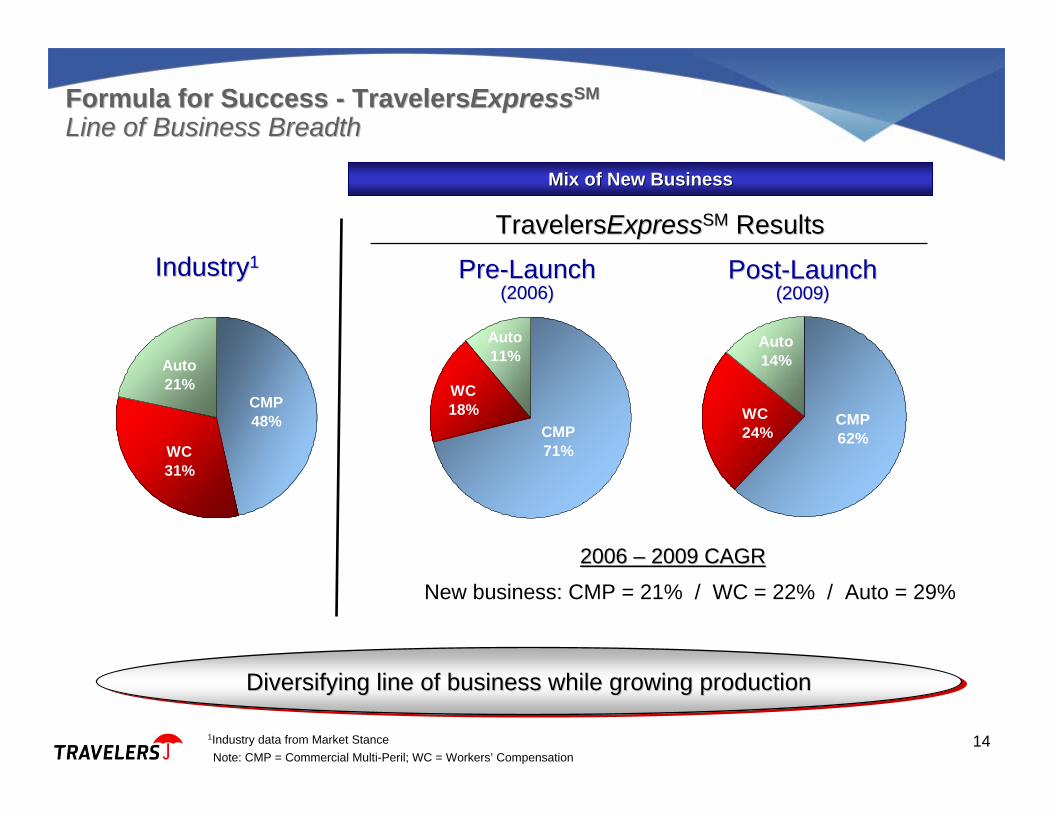

CMP48%

Auto 21%

WC31%

CMP71%

Auto 11%

WC18%

IndustryIndustry11

Note: CMP = Commercial Multi-Peril; WC = Workers’ Compensation

CMP62%

Auto 14%

WC 24%

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

Line of Business BreadthLine of Business Breadth

1Industry data from Market Stance

Mix of New BusinessMix of New Business

TravelersTravelersExpressExpressSMSM ResultsResults

PostPost--Launch Launch (2009)(2009)

PrePre--Launch Launch (2006)(2006)

Diversifying line of business while growing productionDiversifying line of business while growing productionDiversifying line of business while growing production

2006 2006 –– 2009 CAGR2009 CAGR

New business: CMP = 21% / WC = 22% / Auto = 29%

15

The TravelersExpressSM platform is attracting productive new agents

The TravelersExpressSM platform is attracting productive new agents

New Agent Appointments

Total Agents

Total Agents & New Agent AppointmentsTotal Agents & New Agent Appointments

7,900

2006 2007 2008 2009 2005 YE% of New BusinessBy New Appointments 3% 7% 16% 22%

4,800

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

DistributionDistribution

Additional 1,275 agents appointed in

2010 thru end of June

1616

1 Market Opportunity: High Medium Low

1 Source: MarketStance 2007

Formula for Success Formula for Success -- TravelersTravelersExpressExpressSMSM

DistributionDistribution• Systematic strategy of agency appointments

– 7,900 agents appointed at year-end 2009 compared to 4,800 at year-end 2005

• Optimized distribution in areas of market opportunity – Central, West

• Enhanced geographic diversification strategy

New agents appointed nationwide since 2006 contributed 22% of new business in 2009

New agents appointed nationwide since 2006 New agents appointed nationwide since 2006 contributed 22% of new business in 2009contributed 22% of new business in 2009

June 2010June 2010NonNon--East Coast East Coast

AgentsAgents

PrePre--20062006NonNon--East Coast East Coast

AgentsAgents

17

•• Overview Overview –– Select AccountsSelect Accounts

•• Formula for Success Formula for Success –– TravelersTravelersExpressExpressSMSM

•• Results Results –– TravelersTravelersExpressExpressSMSM

•• OnOn--going Initiativesgoing Initiatives

•• Q & AQ & A

18

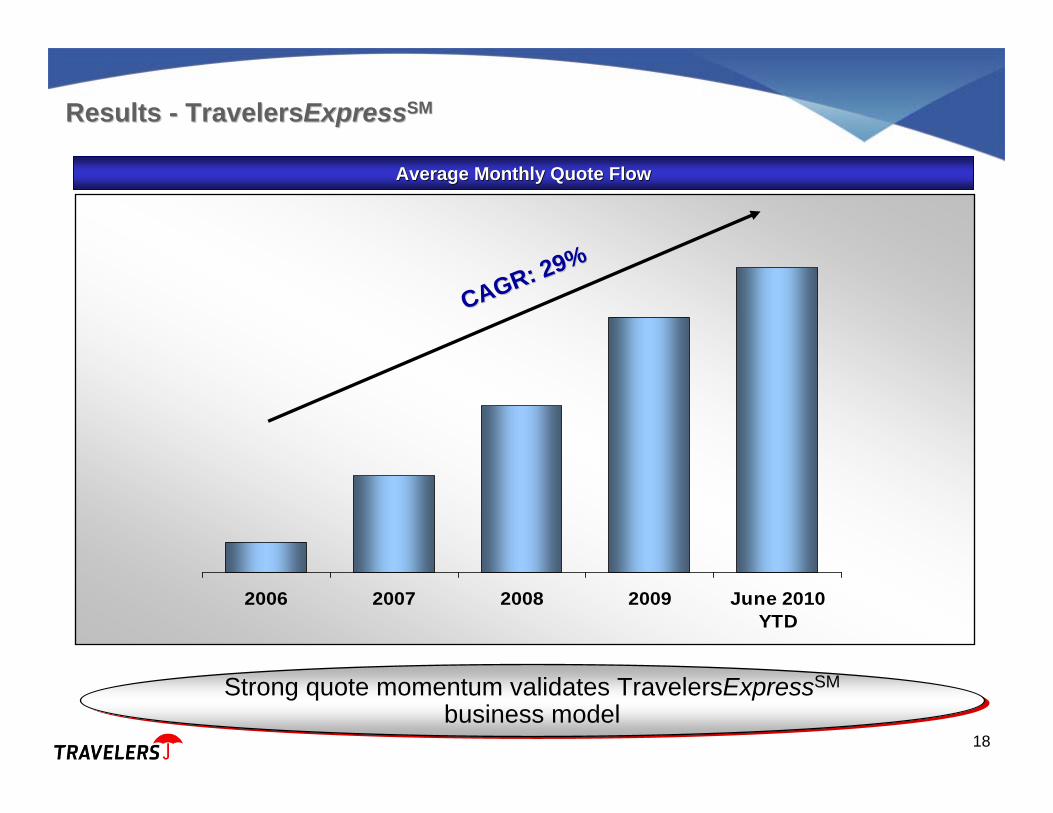

Strong quote momentum validates TravelersExpressSM

business modelStrong quote momentum validates TravelersExpressSM

business model

2006 2007 2008 2009 June 2010YTD

CAGR: 29%CAGR: 29%

Results Results -- TravelersTravelersExpressExpressSMSM

Average Monthly Quote FlowAverage Monthly Quote Flow

19

Generating more opportunities, while continuing to apply discipline

Generating more opportunities, while continuing to apply discipline

Results Results -- TravelersTravelersExpressExpressSMSM

2006 2007 2008 2009 June 2010YTD

Decrease of 8.3 pointsDecrease of 8.3 points

Hit Ratio PercentageHit Ratio Percentage

Stabilizing to a level

reflecting maturation of model as all

lines of business rolled in

20

Policies in ForcePolicies in Force

+32%

+31%

Policies in force continue to achieve new highs each monthPolicies in force continue to achieve new highs each month

2006 2007 2008 2009 June 2010YTD

Results Results -- TravelersTravelersExpressExpressSMSM

CAGR: 9%CAGR: 9%

21

•• Overview Overview –– Select AccountsSelect Accounts

•• Formula for Success Formula for Success –– TravelersTravelersExpressExpressSMSM

•• Results Results –– TravelersTravelersExpressExpressSMSM

•• OnOn--going Initiativesgoing Initiatives

•• Q & AQ & A

22

ProductProductTravelersExpressTravelersExpressSMSM

20102006 2007 2008 2009

PlatformPlatform 750 New Classes750 New Classes

Technology SegmentTechnology Segment

Automobile ExpressAutomobile Express

Umbrella ExpressUmbrella Express

WorkersWorkers’’ Comp. ExpressComp. Express

CMP ExpressCMP Express

2005

Add New AgentsAdd New Agents

Significant investment - long-term barrier to competitors’ success

Significant investment - long-term barrier to competitors’ success

OnOn--going Initiativesgoing InitiativesSignificant InvestmentSignificant Investment

2nd Gen2nd Gen UmbrellaUmbrella

2nd Gen2nd Gen CMPCMP

2011

23

Available for Issue

Pre-Merger

Advantage

PortfolioExpress

CMP

Plus

2005-2009 2010-2012

AFI:AFI:

AutoAuto

CMPCMP

WCWC

UMBUMB

LowLow--TouchTouch

(Refer)(Refer)

NoNo--Touch Touch IssueIssue

AFI:AFI:

CMPCMP

WCWC

LowLow--TouchTouch

(Refer)(Refer)

LowLow--TouchTouch

(Refer)(Refer)

Continually drive efficiencies into the small commercial space

Continually drive efficiencies into the small commercial space

Note: AFI= Available for Issue; CMP = Commercial Multi-Peril; WC = Workers’ Compensation; UMB = Umbrella.

OnOn--going Initiativesgoing InitiativesAdvancing Product & Pricing SophisticationAdvancing Product & Pricing Sophistication

24

OnOn--going Initiativesgoing InitiativesManaging ResultsManaging Results

Powerful analytics driving decision-making and accountability down to the front line

Powerful analytics driving decision-making and accountability down to the front line

• Rolled out in 2010

• Interactive, real-time capability

• Ability to drill down to granular level i.e. region, office, account

• Ability to model impact of potential actions

25

““Mom & PopMom & Pop””

Local communityLocal community

Commercial lines Commercial lines producersproducers

Wide geographyWide geography

Dedicated small Dedicated small commercial lines commercial lines producer(sproducer(s))

Targeted sectors Targeted sectors (e.g., Tech or (e.g., Tech or Medical)Medical)

Small commercial Small commercial lines departmentlines department

Phone & web basedPhone & web based

Volume drivenVolume driven

Agency segmentation - focusing resources to optimize distribution channel

Agency segmentation - focusing resources to optimize distribution channel

Commitment to Producing Small CommercialLOW HIGH

OnOn--going Initiativesgoing InitiativesAgency Segmentation for a More Sophisticated View of DistributioAgency Segmentation for a More Sophisticated View of Distributionn

Main StreetMain Street GeneralistGeneralist EngagedEngaged CommittedCommitted

• Voice of the agent – what is driving behavior and why?

• Learning more about agents to help them optimize value within Travelers platform

26

OnOn--going Initiativesgoing InitiativesRedeploying Savings from Platform Efficiency into Sales & DistriRedeploying Savings from Platform Efficiency into Sales & Distributionbution

• Serve as an extension of the traditional regional sales teams

• Handle agents that are Express-driven, a geographic challenge, and/or new appointments

• Provide high frequency, focused interactions as requested by some agents

• Drive flow through high frequency of agent interactions

Created New Role Created New Role –– Inside Sales ExecutiveInside Sales Executive

Creating insights on how to get new agents productive and improve same-store sales from existing agents

Creating insights on how to get new agents productive and improve same-store sales from existing agents

Measure Inside Sales Executive Outside Sales Executive

Agents Assigned 100 40

Quality, Daily Contacts 15 Calls 3-4 Visits

Interaction Virtual – Phone, Email In Person

Illustrative data

27

• Scale matters for success

• Having a winning formula is critical

• All elements need to be there and work together

• Achieving strong results in a challenging environment

• Long-term view of strategic investments

• Well positioned for the future with continued evolution of Travelers winning formula

Increasing Travelers lead in the small commercial marketplace

Increasing Travelers lead in the small commercial marketplace

Select AccountsSelect AccountsGrowing Market Share Profitably Growing Market Share Profitably

28

•• Overview Overview –– Select AccountsSelect Accounts

•• Formula for Success Formula for Success –– TravelersTravelersExpressExpressSMSM

•• Results Results –– TravelersTravelersExpressExpressSMSM

•• OnOn--going Initiativesgoing Initiatives

•• Q & AQ & A

2929

• For further information, please see Travelers reports filed with the SEC pursuant to the Securities Exchange Act of 1934 which are available at the SEC’s website (www.sec.gov).

• This presentation should be read with accompanying discussion and Travelers SEC filings.

• From time to time, Travelers may use its website as a channel of distribution of material company information. Financial and other material information regarding the company is routinely posted on and accessible at http://investor.travelers.com. In addition, you may automatically receive email alerts and other information about Travelers by enrolling your email by visiting the “E-mail Alert Service” section at http://investor.travelers.com.

DisclosureDisclosure

30