marcellus/utica shale strategy - mplx.com€¦ · utica infrastructure investments l assets in...

TRANSCRIPT

Marcellus/Utica Shale StrategyJanuary 27, 2016

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of federal securities laws regarding MPLX LP ("MPLX"), Marathon Petroleum Corporation ("MPC"), and MarkWest Energy Partners, L.P. ("MarkWest"). These forward-looking statements relate to, among other things, expectations, estimates and projections concerning the business and operations of MPLX, MPC, and MWE. You can identify forward-looking statements by words such as "anticipate," "believe," "estimate," "expect," "forecast”, “goal," "guidance," "imply," "objective," “opportunity,” “outlook,” "plan," "project," "potential," “seek,” “target,” "could," "may," "should," "would," "will" or other similar expressions that convey the uncertainty of future events or outcomes. Such forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond the companies' control and are difficult to predict. In addition to other factors described herein that could cause MPLX's actual results to differ materially from those implied in these forward-looking statements, negative capital market conditions, including a persistence or increase of the current yield on common units, which is higher than historical yields, could adversely affect MPLX's ability to meet its distribution growth guidance, particularly with respect to the later years of such guidance. Factors that could cause MPLX's or MarkWest's actual results to differ materially from those implied in the forward-looking statements include: risk that the synergies from the MPLX/MarkWest transaction may not be fully realized or may take longer to realize than expected; disruption from the MPLX/MarkWest transaction making it more difficult to maintain relationships with customers, employees or suppliers; risks relating to any unforeseen liabilities of MarkWest; the adequacy of MPLX's and MarkWest's respective capital resources and liquidity, including, but not limited to, availability of sufficient cash flow to pay MPLX’s distributions, and the ability to successfully execute their business plans and implement their growth strategies; the timing and extent of changes in commodity prices and demand for crude oil, refined products, feedstocks or other hydrocarbon-based products; volatility in and/or degradation of market and industry conditions; completion of pipeline capacity by competitors; disruptions due to equipment interruption or failure, including electrical shortages and power grid failures; the suspension, reduction or termination of MPC's obligations under MPLX's commercial agreements; each company's ability to successfully implement its growth plan, whether through organic growth or acquisitions; modifications to earnings and distribution growth objectives; federal and state environmental, economic, health and safety, energy and other policies and regulations; changes to MPLX's capital budget; other risk factors inherent to MPLX or MarkWest's industry; and the factors set forth under the heading "Risk Factors" in MPLX's Annual Report on Form 10-K for the year ended Dec. 31, 2014, filed with the Securities and Exchange Commission (SEC); and the factors set forth under the heading "Risk Factors" in MarkWest's Annual Report on Form 10-K for the year ended Dec. 31, 2014, and Quarterly Report on Form 10-Q for the quarter ended Sept. 30, 2015, filed with the SEC (former ticker symbol: MWE). These risks, as well as other risks associated with MPLX, MarkWest and the transaction, are also more fully discussed in the joint proxy statement and prospectus included in the registration statement on Form S-4 filed by MPLX and declared effective by the SEC on Oct. 29, 2015, as supplemented. Factors that could cause MPC's actual results to differ materially from those implied in the forward-looking statements include: risks described above relating to MPLX and the MPLX/MarkWest transaction; changes to the expected construction costs and timing of pipeline projects; volatility in and/or degradation of market and industry conditions; the availability and pricing of crude oil and other feedstocks; slower growth in domestic and Canadian crude supply; the effects of the lifting of the U.S. crude oil export ban; completion of pipeline capacity to areas outside the U.S. Midwest; consumer demand for refined products; transportation logistics; the reliability of processing units and other equipment; MPC's ability to successfully implement growth opportunities; modifications to MPLX earnings and distribution growth objectives; federal and state environmental, economic, health and safety, energy and other policies and regulations; other risk factors inherent to MPC's industry; and the factors set forth under the heading "Risk Factors" in MPC's Annual Report on Form 10-K for the year ended Dec. 31, 2014, filed with SEC. In addition, the forward-looking statements included herein could be affected by general domestic and international economic and political conditions. Unpredictable or unknown factors not discussed here, in MPLX's Form 10-K, in MPC's Form 10-K, or in MarkWest's Form 10-K and Form 10-Qs could also have material adverse effects on forward-looking statements. Copies of MPLX's Form 10-K are available on the SEC website, MPLX's website at http://ir.mplx.com or by contacting MPLX's Investor Relations office. Copies of MPC's Form 10-K are available on the SEC website, MPC's website at http://ir.marathonpetrol eum.com or by contacting MPC's Investor Relations office. Copies of MarkWest's Form 10-K and Form 10-Qs are available on the SEC website (former ticker symbol: MWE), MarkWest's website at http://investor.markwest.com or by contacting MPLX's Investor Relations office.

2

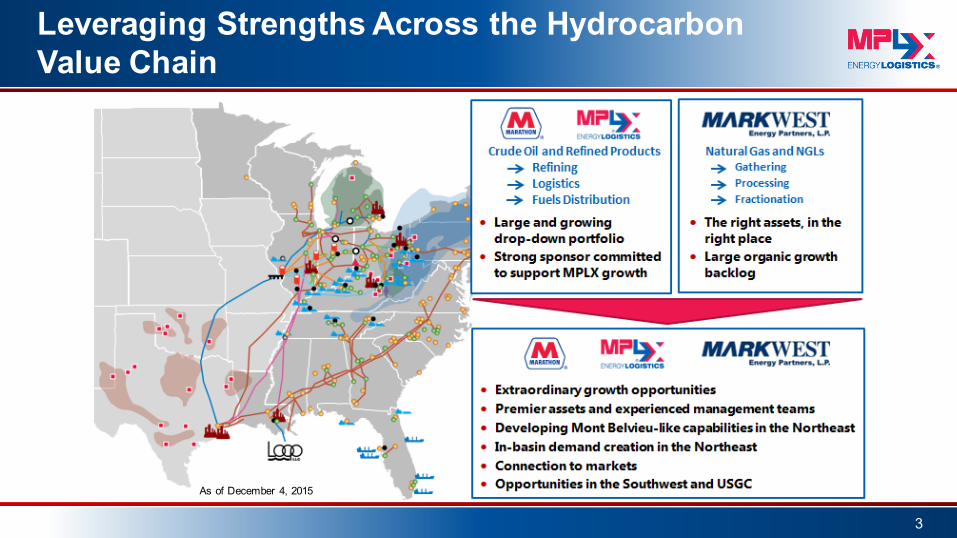

Leveraging Strengths Across the Hydrocarbon Value Chain

3

As of December 4, 2015

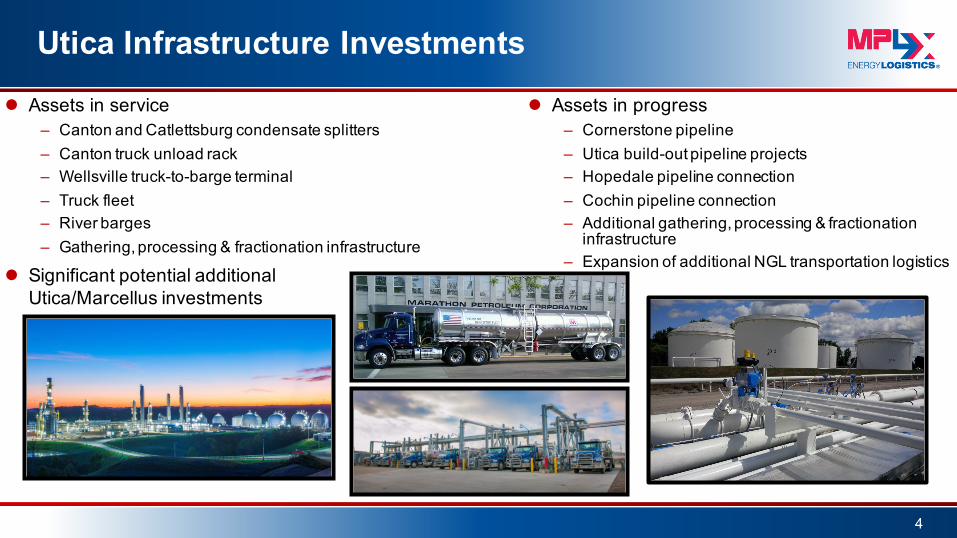

Utica Infrastructure Investments

l Assets in service– Canton and Catlettsburg condensate splitters– Canton truck unload rack– Wellsville truck-to-barge terminal– Truck fleet– River barges– Gathering, processing & fractionation infrastructure

l Significant potential additional Utica/Marcellus investments

4

l Assets in progress– Cornerstone pipeline– Utica build-out pipeline projects– Hopedale pipeline connection– Cochin pipeline connection– Additional gathering, processing & fractionation

infrastructure– Expansion of additional NGL transportation logistics

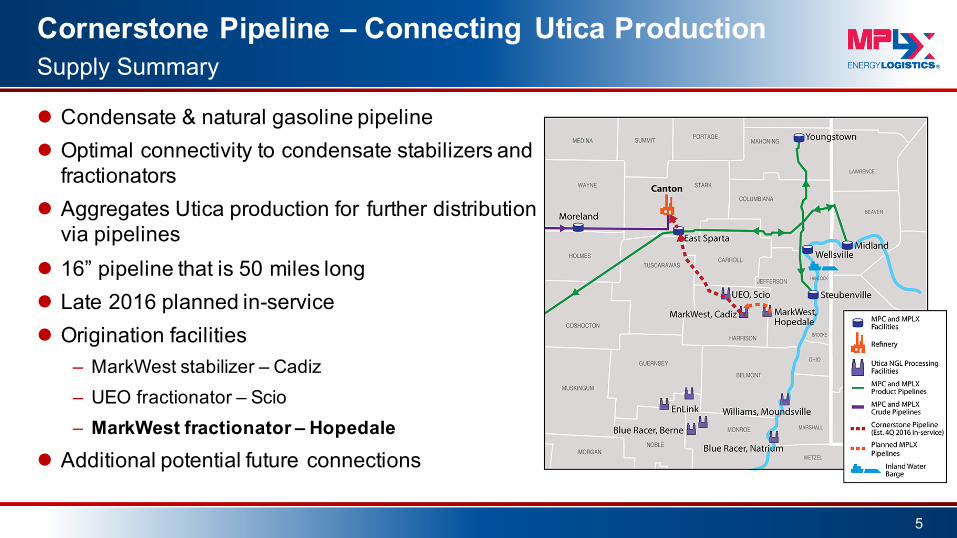

l Condensate & natural gasoline pipelinel Optimal connectivity to condensate stabilizers and

fractionatorsl Aggregates Utica production for further distribution

via pipelinesl 16” pipeline that is 50 miles longl Late 2016 planned in-servicel Origination facilities

– MarkWest stabilizer – Cadiz– UEO fractionator – Scio– MarkWest fractionator – Hopedale

l Additional potential future connections

5

Cornerstone Pipeline – Connecting Utica ProductionSupply Summary

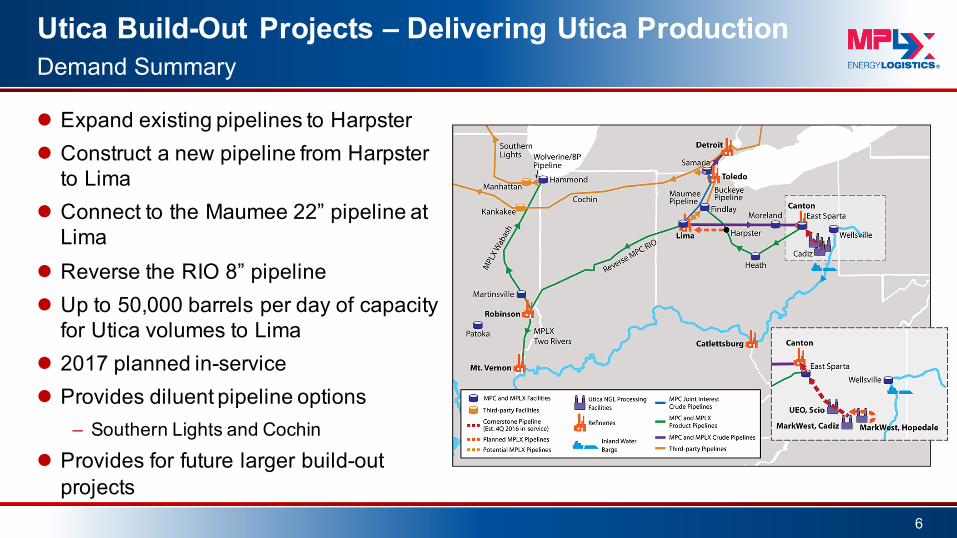

Utica Build-Out Projects – Delivering Utica Production

6

Demand Summary

l Expand existing pipelines to Harpsterl Construct a new pipeline from Harpster

to Limal Connect to the Maumee 22” pipeline at

Limal Reverse the RIO 8” pipelinel Up to 50,000 barrels per day of capacity

for Utica volumes to Limal 2017 planned in-servicel Provides diluent pipeline options

– Southern Lights and Cochin

l Provides for future larger build-out projects

Cornerstone Pipeline and Utica Build-Out Projects

7

The Utica Pipeline Solution

l Provides optionality to multiple markets, maximizing producer netbacks

l Provides flexibility of commitment terms and seasonal shipper needs

l Allows MPLX to complete projects in phases as Utica production grows

l Maintains the option for future expansion volume and connectivity

l Adds superior safety, reliability and economics to existing alternatives

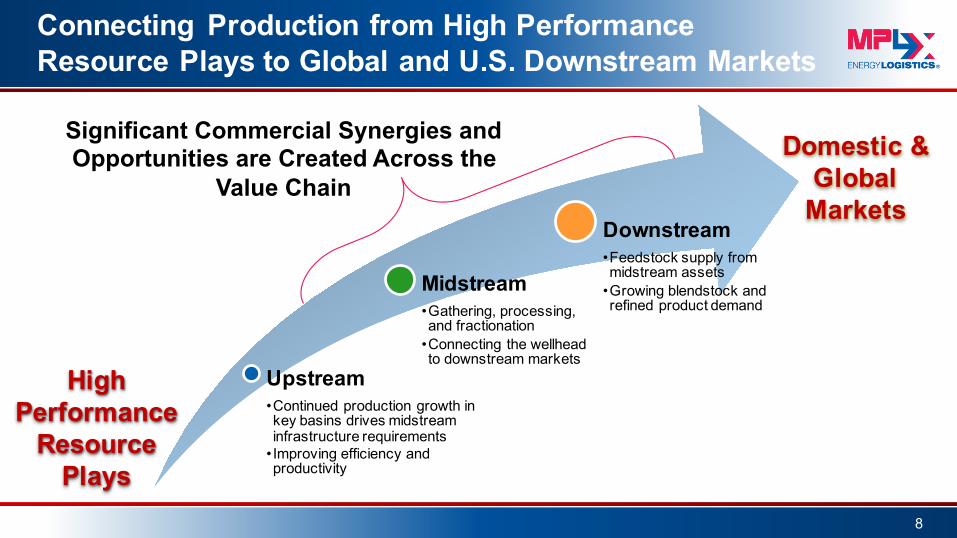

Connecting Production from High Performance Resource Plays to Global and U.S. Downstream Markets

8

Upstream•Continued production growth in key basins drives midstream infrastructure requirements

• Improving efficiency and productivity

Midstream•Gathering, processing, and fractionation

•Connecting the wellhead to downstream markets

Downstream•Feedstock supply from midstream assets

•Growing blendstock and refined product demand

Domestic & Global

Markets

High Performance

Resource Plays

Significant Commercial Synergies and Opportunities are Created Across the

Value Chain

MarkWest Strategy: Based on Service and Execution

PROVENCUSTOMER

SATISFACTION

• Leadingmidstreamproviderwithover7Bcf/dofprocessingcapacity,450MBbl/doffractionationcapacityandover5,000milesofpipeline

• Leadingpositionsinhighlyproductiveresourceplays• 11majorprocessingandfractionationprojectsunderconstruction

• Long-termagreementswithover160producercustomers• Receivedthe#1ratingforTotalMidstreamCustomerSatisfactionineveryEnergyPointResearchSurveysinceitsinceptionin2006

HIGH-QUALITYDIVERSIFIEDASSETS

CreatethetopperformingmidstreamMLPintheindustrybyconsistentlyprovidingbest-of-classserviceandrelentlesspursuitofsafe,efficient,andeffectivesolutionsforourcustomers

SUBSTANTIALGROWTH

OPPORTUNITIES

9

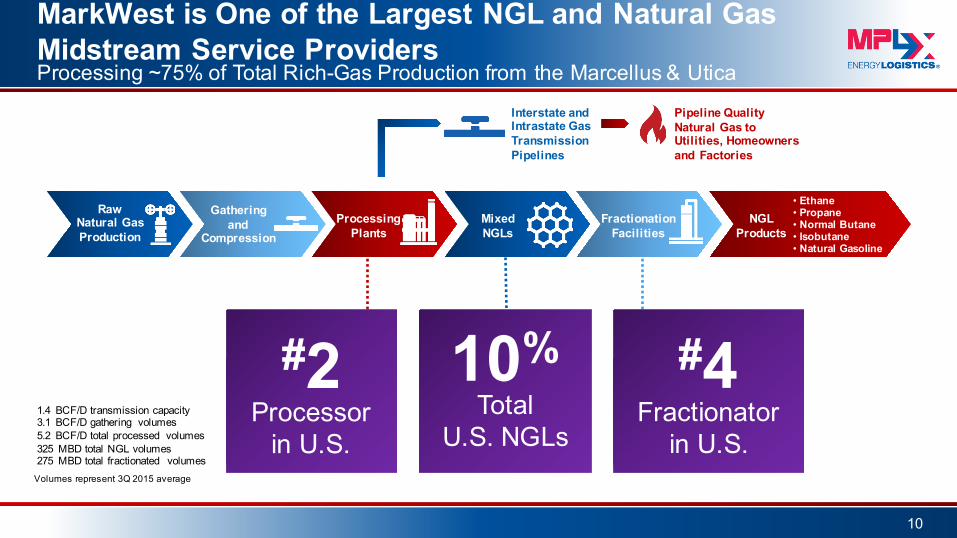

MarkWest is One of the Largest NGL and Natural Gas Midstream Service Providers

10

Processing ~75% of Total Rich-Gas Production from the Marcellus & Utica

RawNatural GasProduction

ProcessingPlants

MixedNGLs

FractionationFacilities

NGLProducts

• Ethane• Propane• Normal Butane• Isobutane• Natural Gasoline

Gatheringand

Compression

Interstate and Intrastate Gas Transmission Pipelines

Pipeline QualityNatural Gas toUtilities, Homeownersand Factories

#2Processor

in U.S.

#4Fractionator

in U.S.

10%Total

U.S. NGLsVolumes represent 3Q 2015 average

1.4 BCF/D transmission capacity3.1 BCF/D gathering volumes 5.2 BCF/D total processed volumes325 MBD total NGL volumes 275 MBD total fractionated volumes

Growth Driven by Customer Satisfaction

11

MarkWest has received the No.1 rating for total customer satisfaction in every EnergyPoint Research survey since its inception in 2006

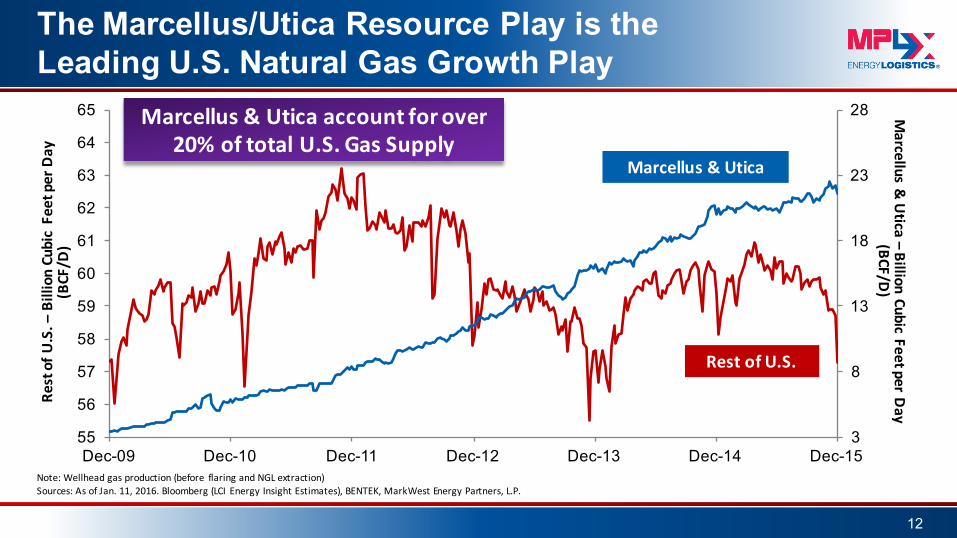

3

8

13

18

23

28

55

56

57

58

59

60

61

62

63

64

65

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

The Marcellus/Utica Resource Play is the Leading U.S. Natural Gas Growth Play

RestofU

.S.–

BillionCubicFeetperDay

(BCF/D

)

Note:Wellheadgasproduction(before flaringandNGLextraction)Sources:AsofJan.11,2016.Bloomberg(LCI EnergyInsightEstimates),BENTEK,MarkWestEnergyPartners,L.P.

Marcellus&

Utica–

BillionCubicFeetperDay

(BCF/D)

Marcellus&Uticaaccountforover20%oftotalU.S.GasSupply

Marcellus&Utica

RestofU.S.

12

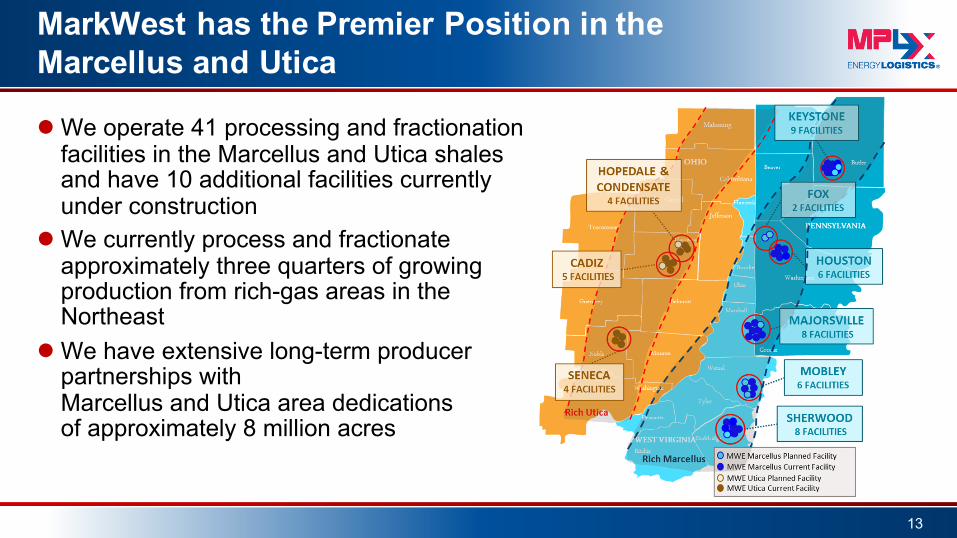

MarkWest has the Premier Position in the Marcellus and Utica

l We operate 41 processing and fractionation facilities in the Marcellus and Utica shalesand have 10 additional facilities currently under construction

l We currently process and fractionate approximately three quarters of growing production from rich-gas areas in the Northeast

l We have extensive long-term producer partnerships with Marcellus and Utica area dedications of approximately 8 million acres

13

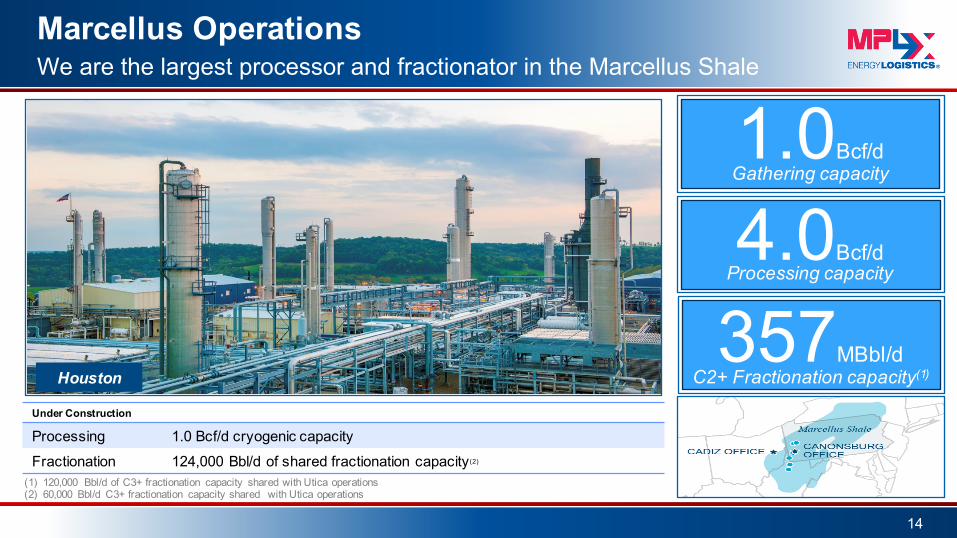

Marcellus Operations

14

We are the largest processor and fractionator in the Marcellus Shale

01.0Bcf/dGathering capacity

4.0Bcf/dProcessing capacity

357MBbl/dC2+ Fractionation capacity(1)

(1) 120,000 Bbl/d of C3+ fractionation capacity shared with Utica operations(2) 60,000 Bbl/d C3+ fractionation capacity shared with Utica operations

Under Construction

Processing 1.0 Bcf/d cryogenic capacity

Fractionation 124,000 Bbl/d of shared fractionation capacity(2)

Houston

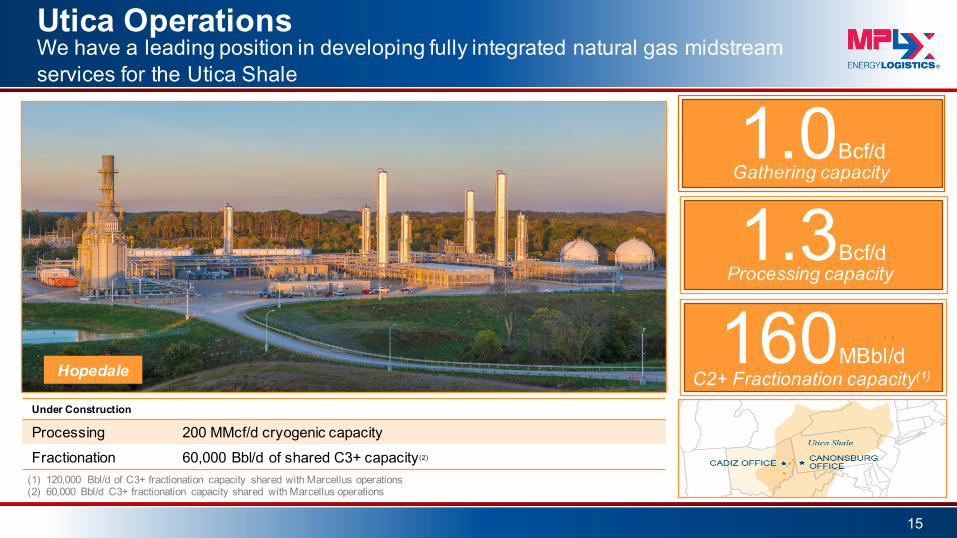

Utica Operations

15

We have a leading position in developing fully integrated natural gas midstream services for the Utica Shale

Under Construction

Processing 200 MMcf/d cryogenic capacity

Fractionation 60,000 Bbl/d of shared C3+ capacity(2)

1.0Bcf/dGathering capacity

1.3Bcf/dProcessing capacity

160MBbl/dC2+ Fractionation capacity(1) Hopedale

(1) 120,000 Bbl/d of C3+ fractionation capacity shared with Marcellus operations(2) 60,000 Bbl/d C3+ fractionation capacity shared with Marcellus operations

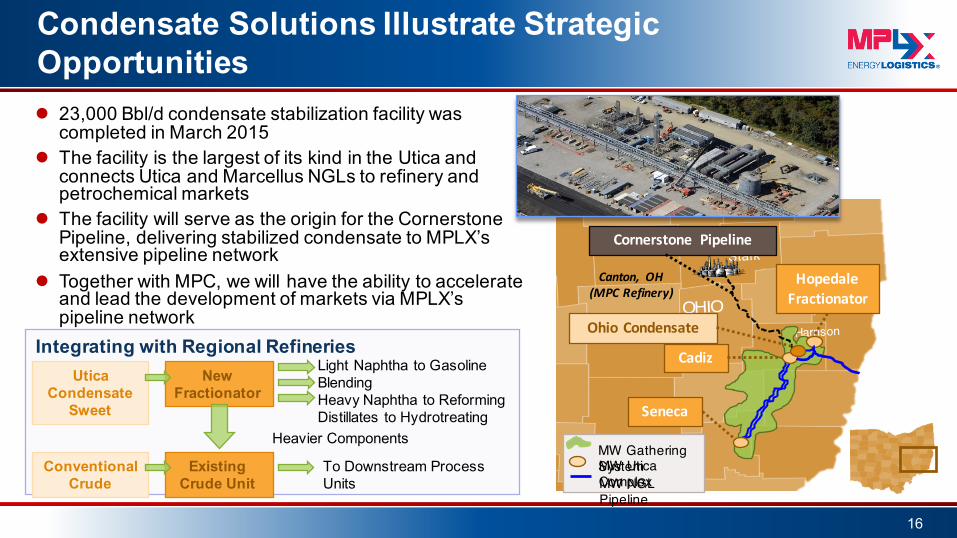

Condensate Solutions Illustrate Strategic Opportunitiesl 23,000 Bbl/d condensate stabilization facility was

completed in March 2015 l The facility is the largest of its kind in the Utica and

connects Utica and Marcellus NGLs to refinery and petrochemical markets

l The facility will serve as the origin for the Cornerstone Pipeline, delivering stabilized condensate to MPLX’s extensive pipeline network

l Together with MPC, we will have the ability to accelerate and lead the development of markets via MPLX’s pipeline network

16

Cornerstone Pipeline

OhioCondensate

Cadiz

Seneca

HopedaleFractionator

MW Utica ComplexMW NGL Pipeline

MW Gathering System

Canton, OH(MPCRefinery)

Utica Condensate

Sweet

Conventional Crude

New Fractionator

Existing Crude Unit

To Downstream Process Units

Heavier Components

Integrating with Regional RefineriesLight Naphtha to Gasoline BlendingHeavy Naphtha to ReformingDistillates to Hydrotreating

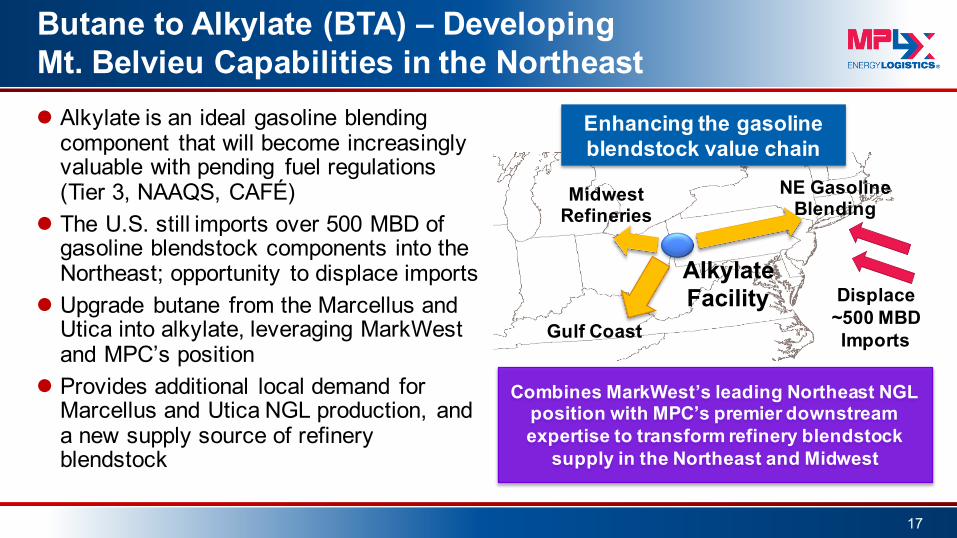

Displace~500 MBDImports

AlkylateFacility

NE Gasoline Blending

Midwest Refineries

Gulf Coast

Butane to Alkylate (BTA) – DevelopingMt. Belvieu Capabilities in the Northeast

Combines MarkWest’s leading Northeast NGL position with MPC’s premier downstream expertise to transform refinery blendstock

supply in the Northeast and Midwest

Enhancing the gasoline blendstock value chain

l Alkylate is an ideal gasoline blending component that will become increasingly valuable with pending fuel regulations (Tier 3, NAAQS, CAFÉ)

l The U.S. still imports over 500 MBD of gasoline blendstock components into the Northeast; opportunity to displace imports

l Upgrade butane from the Marcellus and Utica into alkylate, leveraging MarkWest and MPC’s position

l Provides additional local demand for Marcellus and Utica NGL production, and a new supply source of refinery blendstock

17

18