matts valela - finance director etherton mpisaunga ...€¦ · ... finance director . etherton...

TRANSCRIPT

Imara Zimbabwe Investor Conference

Matts Valela - Finance Director Etherton Mpisaunga - Operations Director Meikles Hotel 28 May 2014

1. Delta Corporation Structure 2. Delta & Franchised Brands, Coke Portfolio 3. Market Share 4. Per Capita Consumption Lagers – Africa 5. Lagers Mix and Volume trends 6. Per Capita Consumption Sparkling Beverages– Africa 7. Sparkling Beverages Volumes & Mix 8. Per Capita Consumption Sorghum 9. Sorghum Volumes & Mix 10. Financials 11. Associates 12. The Future

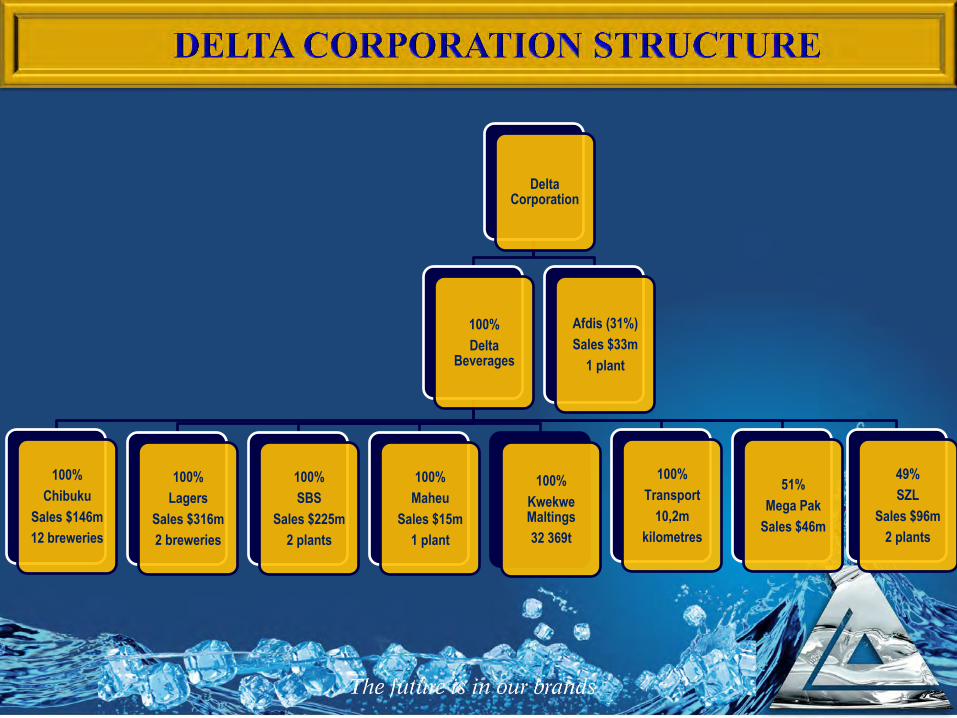

Delta Corporation

100%

Delta Beverages

100%

Chibuku

Sales $146m

12 breweries

100%

Lagers

Sales $316m

2 breweries

100%

SBS

Sales $225m

2 plants

100%

Maheu

Sales $15m

1 plant

100%

Kwekwe Maltings

32 369t

100%

Transport

10,2m

kilometres

51%

Mega Pak

Sales $46m

49%

SZL

Sales $96m

2 plants

Afdis (31%)

Sales $33m

1 plant

DRAUGHT SCUD CONIPACK PET

$0.35/Litre $0.50 / Litre $0.60/Litre $0.80 /Litre

MARKET SHARE

Focus was on market retention and building brand loyalty. Lager share largely driven by mainstream Sorghum beer demand reignited by Chibuku Super

DELTA

BEVERAGES

Lager Beer Sorghum Beer Soft Drinks

99

84

98

To focus on Value Creation through strengthening our Commercial Leadership in the long term by:

i. Deploying brands across price segments ii. Regular big hit innovations iii. Continuous improvement of brand health iv. In-trade captaincy to grow market size and

profit pools v. Investment in commercial capability of sales

force.

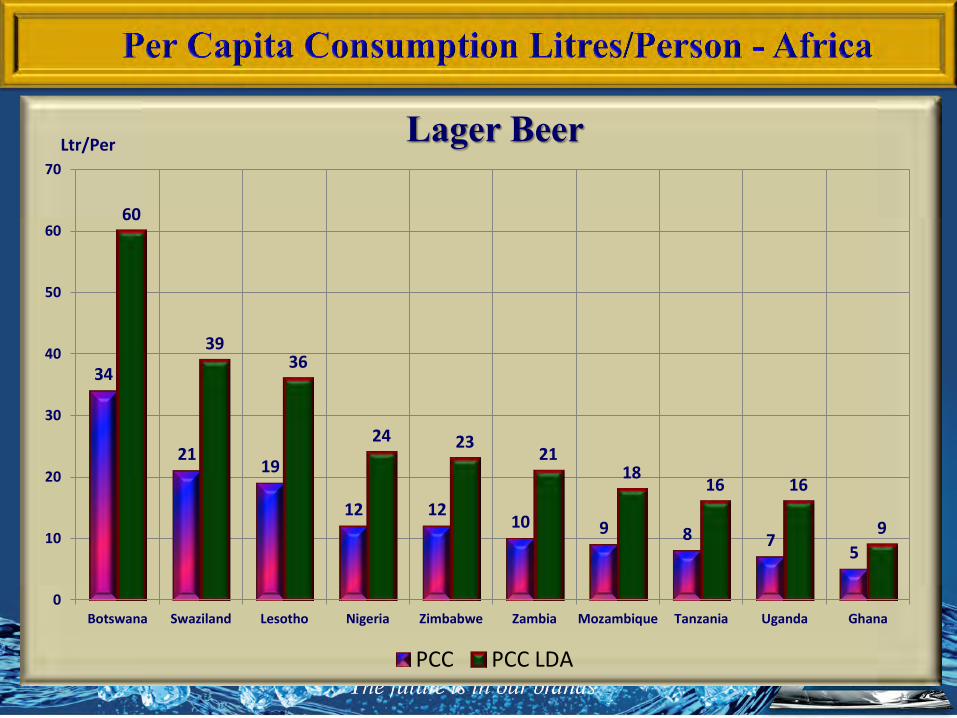

34

21 19

12 12 10 9 8 7

5

60

39 36

24 23 21

18 16 16

9

0

10

20

30

40

50

60

70

Botswana Swaziland Lesotho Nigeria Zimbabwe Zambia Mozambique Tanzania Uganda Ghana

Lager Beer

PCC PCC LDA

Ltr/Per

0

500

1 000

1 500

2 000

2 500

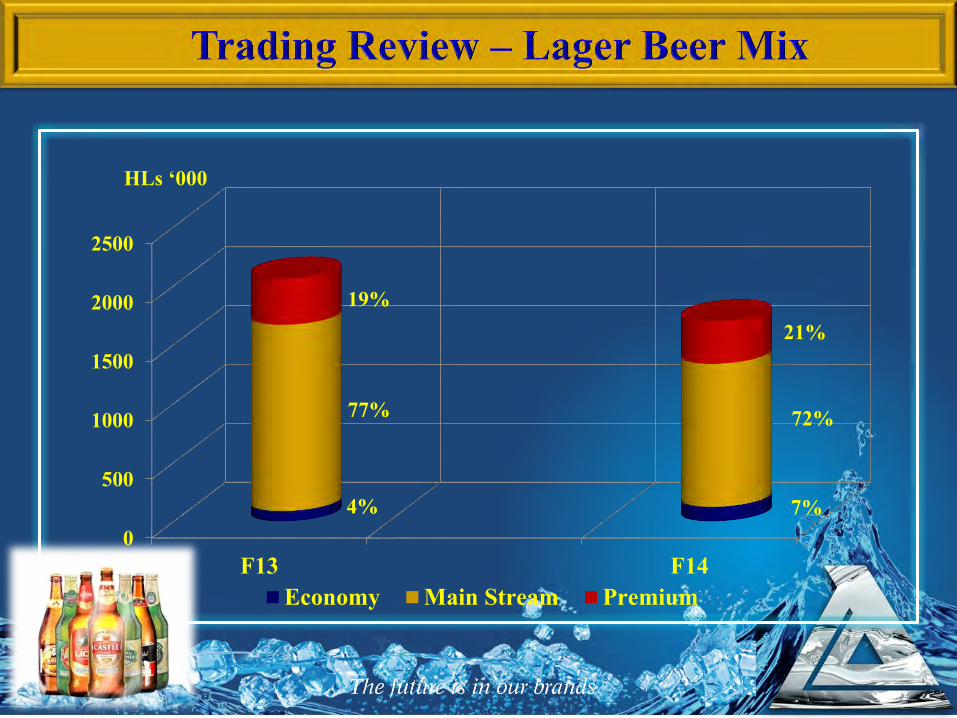

F10 F11 F12 F13 F14

1 148

1 608

1 981 2 060

1 697

HLs ‘000

0

500

1000

1500

2000

2500

F13 F14

4% 7%

77% 72%

19% 21%

Economy Main Stream Premium

HLs ‘000

0

10

20

30

40

50

60

70 62 60

42

34

19 16 15 14

9 6

Soft Drinks Ltr/Per

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

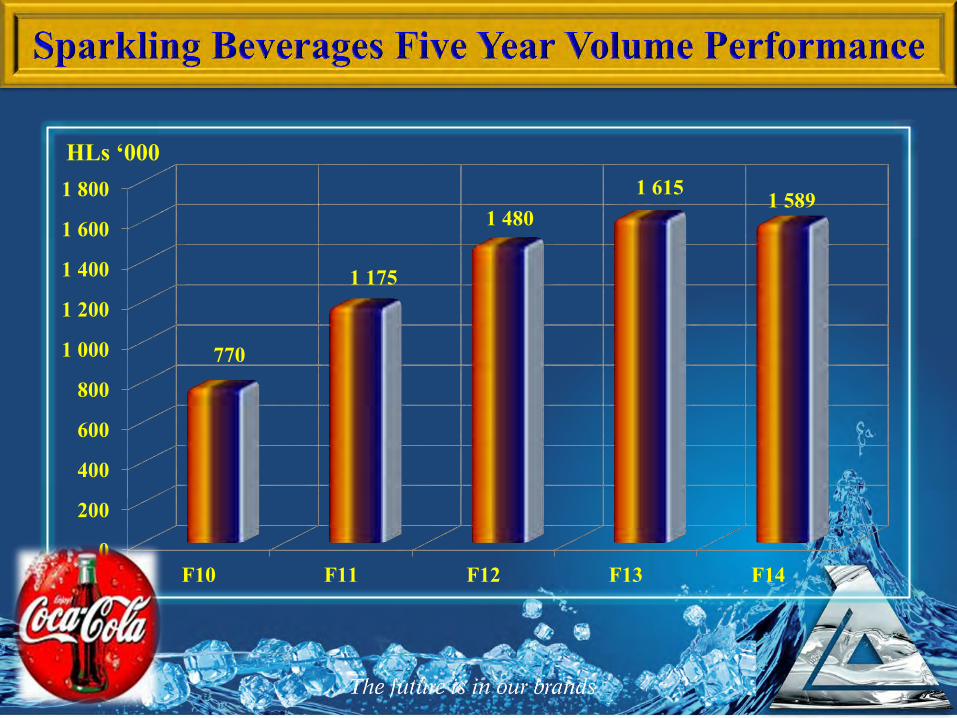

F10 F11 F12 F13 F14

770

1 175

1 480 1 615 1 589

HLs ‘000

0

500

1000

1500

2000

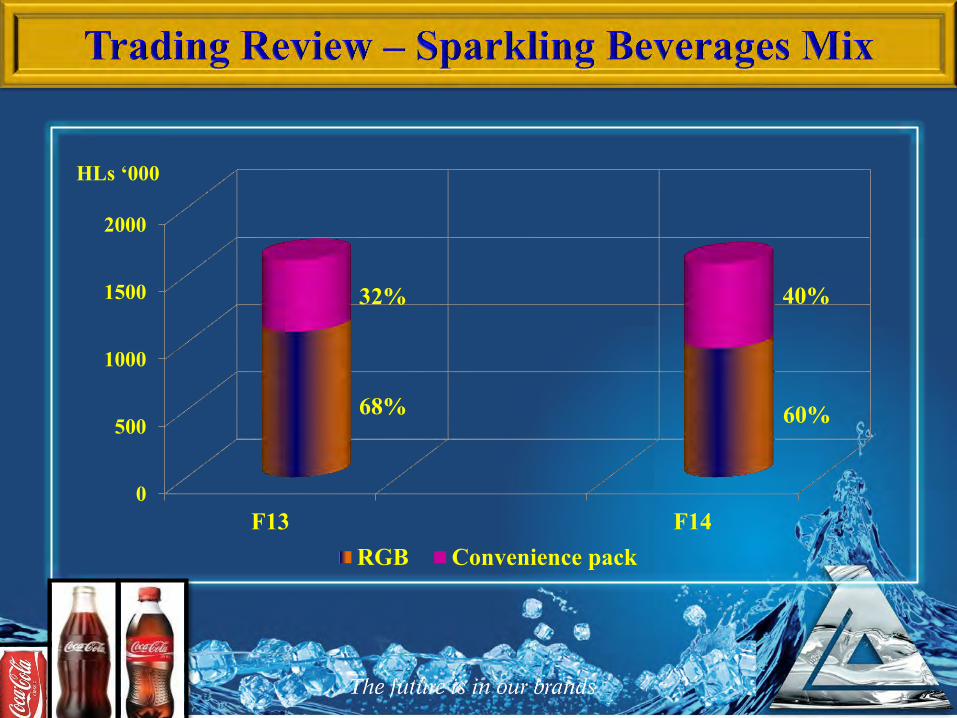

F13 F14

68% 60%

32% 40%

RGB Convenience pack

HLs ‘000

0

50

100

150

200

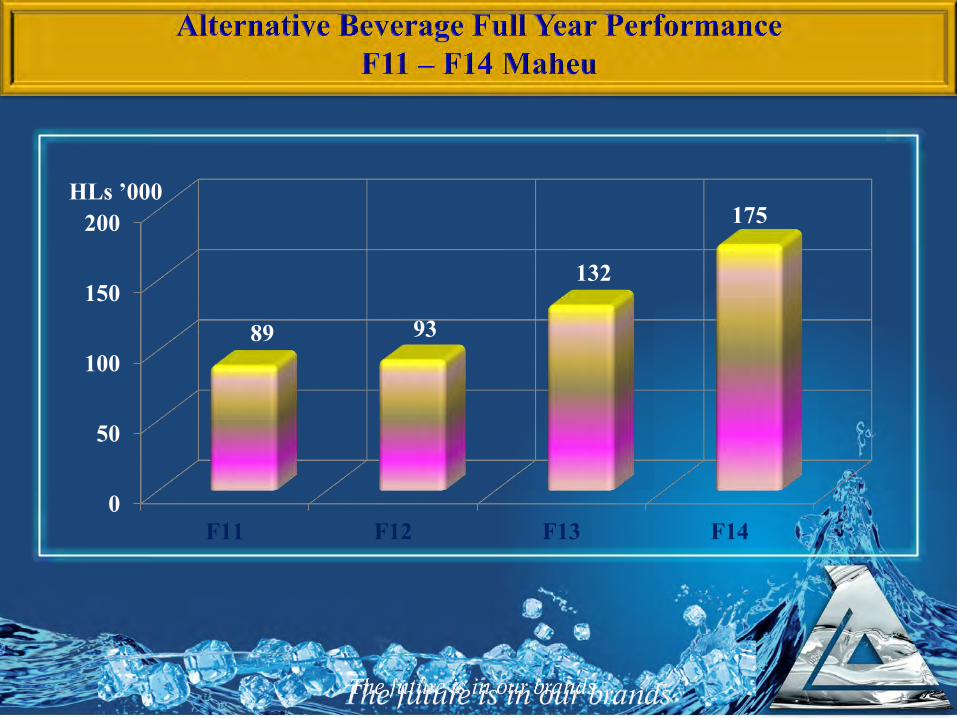

F11 F12 F13 F14

89 93

132

175 HLs ’000

0

10

20

30

40

50

60

70

Botswana Zimbabwe Zambia Mozambique

38

30

25

0

66

57 55

0

PCC PCC LDA

Ltr/Per

HLs ‘000

1 200

1 700

2 200

2 700

3 200

3 700

F10 F11 F12 F13 F14

3 114 2 908

3 354

3 080

3 442

200

700

1200

1700

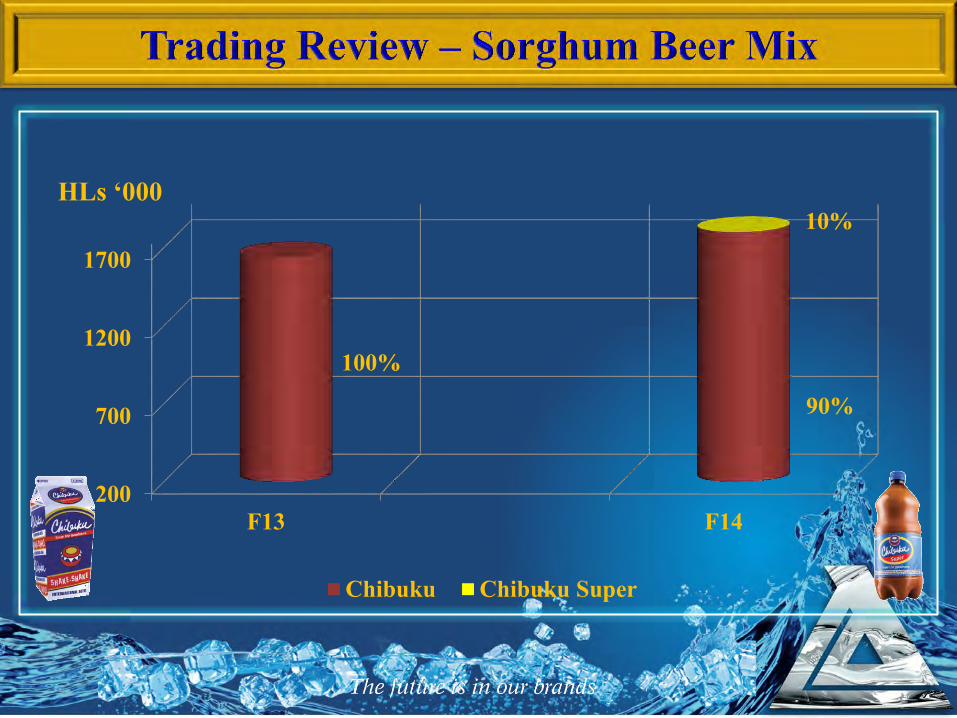

F13 F14

100%

90%

10%

Chibuku Chibuku Super

HLs ‘000

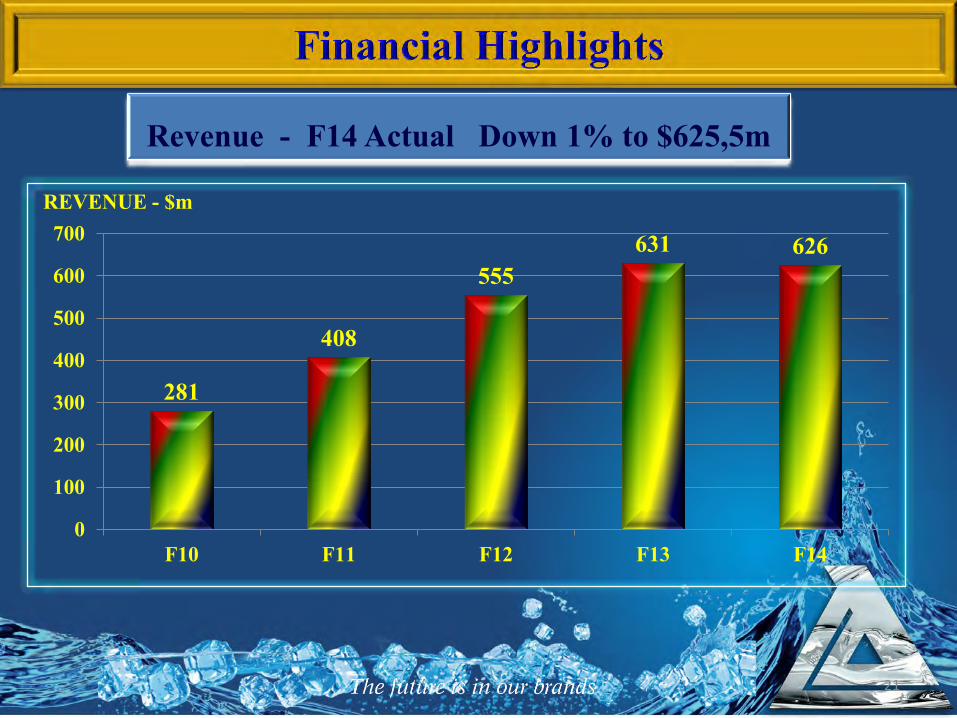

281

408

555 631 626

0

100

200

300

400

500

600

700

F10 F11 F12 F13 F14

REVENUE - $m

Revenue - F14 Actual Down 1% to $625,5m

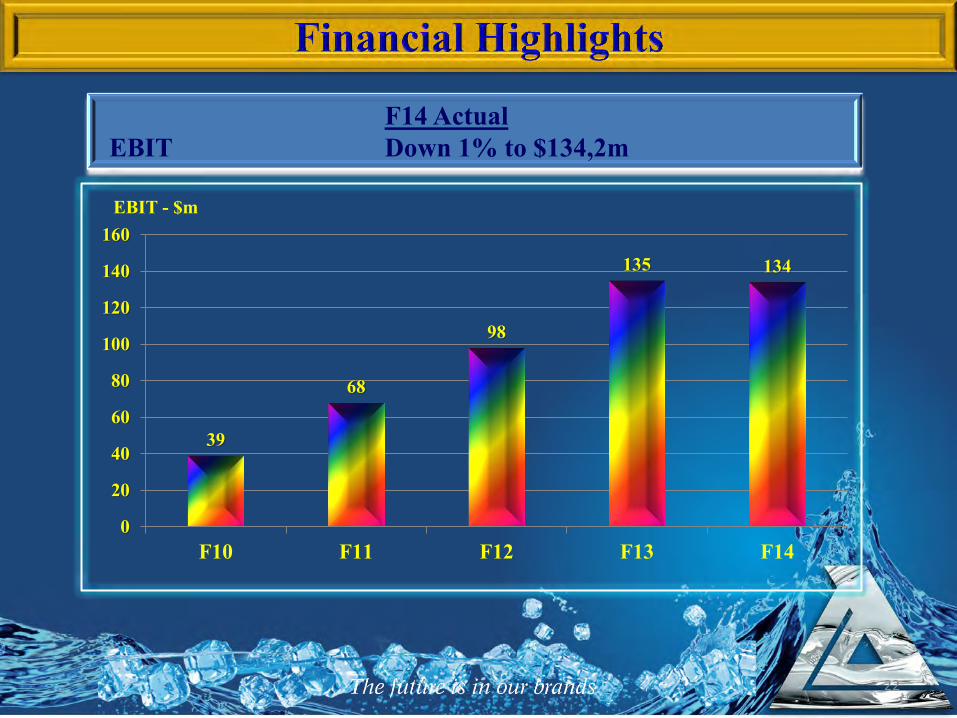

21

39

68

98

135 134

0

20

40

60

80

100

120

140

160

F10 F11 F12 F13 F14

EBIT - $m

22

F14 Actual EBIT Down 1% to $134,2m

0

5

10

15

20

25

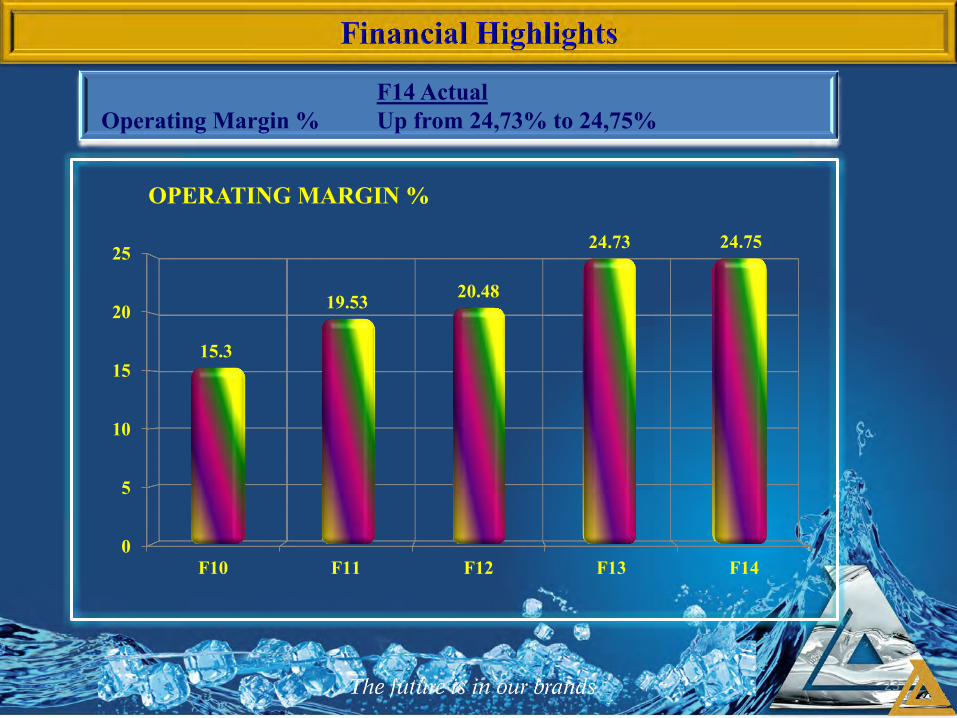

F10 F11 F12 F13 F14

15.3

19.53 20.48

24.73 24.75

OPERATING MARGIN %

23

F14 Actual Operating Margin % Up from 24,73% to 24,75%

0

20

40

60

80

100

120

140

160

180

F10 F11 F12 F13 F14

49

82

119

162 165

EBITDA - $m

F14 Actual EBITDA Up 2% to $165,3m

24

Challenges • Politics • Utilities :- Water, road network,

electricity • Labour law reform • Liquidity/disposable income

Opportunities • Deflation/Price Correction – Consumer Disposable

Income • Lobby for Excise reduction • Country Debt/Funding management • Mining FDI / Employment levels • Agriculture • Infrastructure Spend • Expand & Innovate the Beverage portfolio • Margin expansion and cash