mauritius as an emerging location for delivery of offshore ... attractiveness.pdf · bpo services...

TRANSCRIPT

Mauritius as an Emerging Location for Delivery of Offshore Services

September 2009

Copyright © 2009, Everest Global, Inc.

Copyright © 2009, Everest Global, Inc.2

Table of contents (page 1 of 2)

Executive summary 4

Section I: Perspectives on global sourcing 9 Current state of play 10 Growth opportunity and outlook 15

Section II: A brief introduction to Mauritius 19 Key facts about the Island nation and its economy 20 ICT-sector – The Fifth pillar of the economy 23

Section III: Scope of current service delivery (IT-BPO) from Mauritius 29 Overall market size and growth 30 Key facts on current scope of services 33 Case studies that illustrate scope and maturity of services 40

Section IV: Comparison of Mauritius with other offshore locations 47 Costs 50 Talent pool 59 Structural factors and risks 69

Topic Page no.

Copyright © 2009, Everest Global, Inc.3

Table of contents (page 2 of 2)

Section V: Implications for investors 81 Roles that Mauritius can play for global investors and supporting rationale 84

Section VI: Appendix 89 Research methodology and list of participants 94 Glossary 98 Acknowledgements and Authors 103

Topic Page no.

Copyright © 2009, Everest Global, Inc.4

A. Introduction and context

Mauritius is emerging as an important offshore destination for IT/BPO. The industry currently employs ~10,500 people and has attracted a number of marquee global companies. Also, the industry has grown rapidly at a rate of ~45% per year.1

Mauritius is widely regarded as a relatively developed nation even though it is a part of the African continent. Its economy registered a healthy GDP growth (in excess of 5%) in recent years. Further, Mauritius witnessed a significant uptick in its services economy over the past decade. Though primarily driven by tourism, the services economy rapidly expanded into other sectors including offshore financial services and IT/BPO. Mauritius has identified IT/BPO as a key pillar for its economic growth and has put in place an ambitious vision for this sector. It targets to attract ~29,000 jobs by 2011 and also aspires to move towards “high value-added” niches. Further, Mauritius has put in place several enabling initiatives to support the growth of the sector. These include setting up infrastructure parks, talent development initiatives, and investor-friendly business policies.

This report presents a fact-based view of Mauritius’ current IT/BPO capabilities and highlights its key differentiators with respect to other offshore destinations. The reports also outlines potential ways investors could leverage Mauritius in offshore delivery ofIT/BPO services. As a starting point, the report outlines the significant growth opportunity in offshore IT/BPO and the opportunity for Mauritius to participate in this global sourcing phenomenon.

B. Global sourcing market: Opportunity and outlook

Global sourcing of services is a mature phenomenon, and the market represents US$90 billion in annual revenue across IT and BPO services. Over the last 10 years, this industry grew exponentially to employ over four million people across 150+ locations . While the industry is established, there remains significant untapped potential. Everest estimates put the addressable IT/BPOmarket opportunity at ~US$1 trillion, roughly 10 times the current market size.

The sector is currently witnessing slower growth (5-15%), given the recent economic crisis. However, the medium to long-term growth outlook is robust as firms will look to manage cost pressures by leveraging offshoring.

Further, as global firms expand their offshore footprint, they build global delivery networks. In doing so, they look beyond theestablished offshore locations (e.g., India, Philippines). This presents opportunities for Mauritius to participate in an increasing share of the global offshore market. Mauritius has established a good starting point, as described in the following section.

Executive summary (page 1 of 5)

1 Compounded Annual Growth Rate between 2004-08

Copyright © 2009, Everest Global, Inc.5

Exhibit 1

Exhibit 2

Executive summary (page 2 of 5)

C. Scope of current IT/BPO service delivery from Mauritius

The report examines the scope of current IT/BPO service delivery from the following perspectives: overall scale and growth of operations, types of functions delivered, languages, and client geographies served.

Overall scale and growth of operations

The IT/BPO industry in Mauritius currently employs ~10,500 people and has been growing at a rate of ~45% each year. A number of leading global suppliers (e.g., Accenture, Ceridian, Infosys) and offshore captives (e.g., Orange, DHL, Huawei) established operations in Mauritius. Further, some leading local suppliers (e.g., Rogers, Infinity BPO, Euro CRM) also built credible presence in this sector.

The offshore market size in Mauritius is comparable to many of its larger peer group countries, as indicated in Exhibit 1.

Types of functions served

The industry is successfully delivering a wide array of IT and BPO services to offshore clients. The majority of the service delivery (85%) is BPO focused, with a good mix of voice and non-voice BPO services. Exhibit 2 illustrates the split of the market across types of functions served.

ITO

35%

9%4%

11% 41%

100% = 10,400

Employee split by outsourcing services2009; Number of employees

Others1

Contact center

Non-voice BPO

KPO

Offshore-experienced IT/BPO talent pool by country2009; Number of employees in ‘000s

Has a large domestic market of over 100,000 jobs

Poland

Morocco

Egypt

South Africa

Mauritius

Tunisia

Senegal

Jamaica

Kenya 0.8-0.9

5-6

6-7

7-8

9-10

9-10

13-14

44-45

31-32

1 Include Multimedia, 3D/Graphic design, Engineering services, etc.

Copyright © 2009, Everest Global, Inc.6

Executive summary (page 3 of 5)

While there are some examples of relatively large centers (~1000 FTEs), the typical scale of operations is between 100-500 FTEs depending on functions served. Exhibit 3 provides a view of the typical scale of current delivery centers and also profiles the types of services delivered.

As shown in Exhibit 3, though most of the work delivered is transactional in nature, Mauritius is starting to move up the value chain with few instances of relatively higher-order work. There are emerging examples of success in areas such as customer surveys, reporting and compliance (F&A), and business research.

Languages and client geographies served

Mauritius has distinctive advantages in terms of its quality bilingual skills in both French and English. Given these strengths, Mauritius presents strong opportunities to serve French-speaking markets (e.g., France, Africa, parts of Canada) across both voice and non-voice functions. In addition, companies can leverage Mauritius to serve English-speaking markets in some areas (especially non-voice BPO).

As shown in Exhibit 4, while French and bi-lingual work constitute ~75% of the market, suppliers also delivermeaningful scale for English-speaking markets (e.g., US, UK). There are examples of global companies that have been successful serving English-speaking markets from Mauritius.

Exhibit 3

Exhibit 4

Typical processes deliveredTypical scale of large providers

Voice (French and English-language call center)

Inbound: Customer service, helpdesk, query resolution, bookings

Outbound: Campaigns, Customer surveys, telesales, collections

400-500 FTEs

Non-voice(Back-office BPO)

F&A and HRO (e.g., Account Payable, General Ledger, Accounts Receivable, Payroll, Employee benefits, Global mobility, Reporting and Compliance)

Insurance claims and policy administration Account servicing

250-350 FTEs

IT services Applications development and maintenance using Microsoft technologies, Java/J2EE, etc.

Technical service desk Datacenter operations and disaster recovery

100-150 FTEs

Knowledge services Business research Information services Data and document management Content management and publishing

50-100 FTEs

25%

40%34%

100% = 10,400

Employment distribution by language of service delivery2009; Number of employees

Only FrenchBi-lingual

(English & French)

Other languages1 – 1%

Pure English work is mostly non-voice BPO (e.g., payroll, claims processing)

Limited English voice work in Mauritius Only English

1 Spanish, Dutch, Italian and German

Copyright © 2009, Everest Global, Inc.7

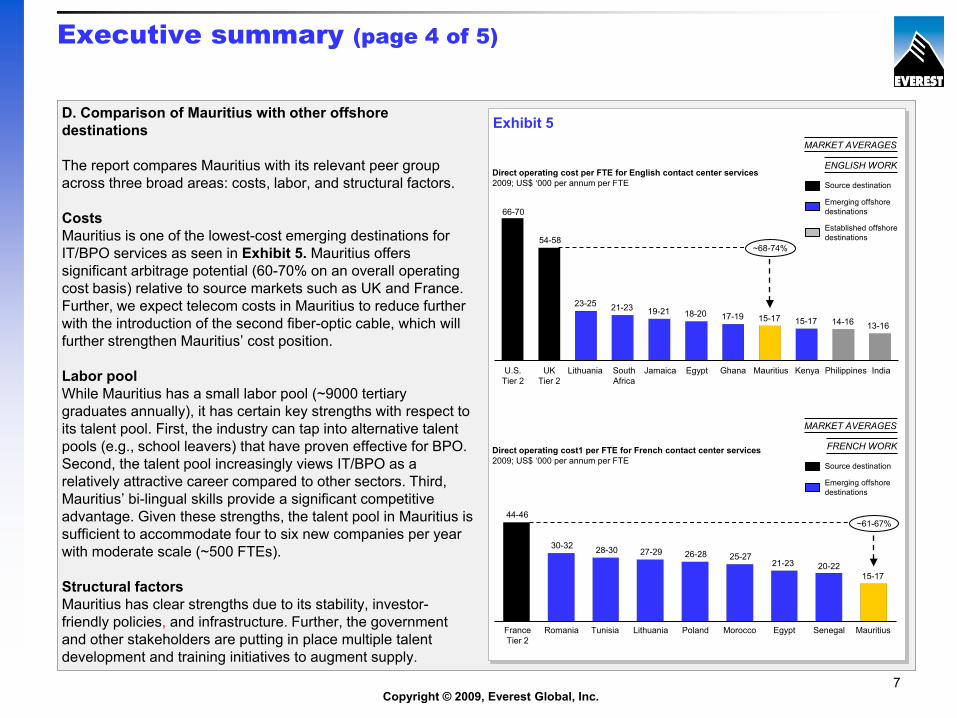

Exhibit 5

Executive summary (page 4 of 5)

D. Comparison of Mauritius with other offshore destinations

The report compares Mauritius with its relevant peer group across three broad areas: costs, labor, and structural factors.

CostsMauritius is one of the lowest-cost emerging destinations for IT/BPO services as seen in Exhibit 5. Mauritius offers significant arbitrage potential (60-70% on an overall operating cost basis) relative to source markets such as UK and France. Further, we expect telecom costs in Mauritius to reduce further with the introduction of the second fiber-optic cable, which will further strengthen Mauritius’ cost position.

Labor poolWhile Mauritius has a small labor pool (~9000 tertiary graduates annually), it has certain key strengths with respect to its talent pool. First, the industry can tap into alternative talent pools (e.g., school leavers) that have proven effective for BPO. Second, the talent pool increasingly views IT/BPO as a relatively attractive career compared to other sectors. Third, Mauritius’ bi-lingual skills provide a significant competitive advantage. Given these strengths, the talent pool in Mauritius is sufficient to accommodate four to six new companies per year with moderate scale (~500 FTEs).

Structural factorsMauritius has clear strengths due to its stability, investor-friendly policies, and infrastructure. Further, the government and other stakeholders are putting in place multiple talent development and training initiatives to augment supply.

ENGLISH WORK

Emerging offshore destinations

Established offshore destinations

Source destination

MARKET AVERAGES

13-1614-1615-1715-1717-1918-2019-2121-2323-25

54-58

66-70

U.S. Tier 2

UK Tier 2

Lithuania South Africa

Jamaica Egypt Ghana Mauritius Kenya Philippines India

Direct operating cost per FTE for English contact center services2009; US$ ‘000 per annum per FTE

~68-74%

FRENCH WORK

Emerging offshore destinations

Source destination

MARKET AVERAGES

44-46

30-32 28-30 27-29 26-28 25-2721-23 20-22

15-17

France Tier 2

Romania Tunisia Lithuania Poland Morocco Egypt Senegal Mauritius

Direct operating cost1 per FTE for French contact center services2009; US$ ‘000 per annum per FTE

~61-67%

Copyright © 2009, Everest Global, Inc.8

Executive summary (page 5 of 5)

Everest experience suggests that investors often evaluate cost-risk trade-offs in making location decisions. Exhibit 6 highlights these trade-offs between Mauritius and its peer group. Given Mauritius’ strengths in bilingual skills, low costs, and its conducive business environment, it emerges as an attractive location for moderate-scale (~500 FTEs) offshore services targeted at both French and English markets.

E. Roles that Mauritius can play for investors

Mauritius has a strong role to play in delivery networks of global investors. Based on Mauritius’ structural advantages and companies’ experiences to date, the report highlights some potential ways in which investors could consider leveraging Mauritius for offshore IT/BPO services. These include:

Offshore hub for French work Bilingual work for multinationals with a pan-European

presence Small-scale, relatively higher-order work in some IT/BPO

areas (e.g., software development, finance & accounting, business research)

Regional delivery hub for Africa (e.g., shared services) Risk diversification (e.g., disaster recovery) option for

established offshore locations (e.g., India, Philippines)

Exhibit 6

HighLow

Low

High

Cost

Risk

Ghana

MauritiusKenya

South Africa

Egypt

Jamaica

IndiaPhilippines

Established low cost, locations for mega scale (multiple ‘000 FTE) operations

Large English-speaking talent pool suited to support large-scale centers (1000-2000 FTE), but relatively higher cost

Low-cost, stable location suited to support moderate-scale centers (<500 FTE)

Low cost however, small talent pool and relatively less evolved infrastructure

Native English-speaking location; but relatively higher costs

Cost-risk comparison for potential countries serving English-speaking markets

ENGLISH LANGUAGE WORK

Cost-risk comparison for potential countries serving French-speaking market

FRENCH LANGUAGE WORK

High

Low

Low

High

Cost

Risk

Senegal

Mauritius

Egypt

Poland Tunisia

Morocco

LithuaniaRomania

Low cost but relatively less evolved infrastructure and small talent pool

Limited French skills and relatively higher costs

Scalable and stable locations, but relatively higher costs

Lowest cost, stable location, suited to support moderate-scale centers (~500 FTE)

Copyright © 2009, Everest Global, Inc.9

Table of contents

Section I: Perspectives on global sourcing Current state of play Growth opportunity and outlook

Section II: A brief introduction to Mauritius

Section III: Scope of current service delivery (IT-BPO) from Mauritius

Section IV: Comparison of Mauritius with other offshore locations

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.10

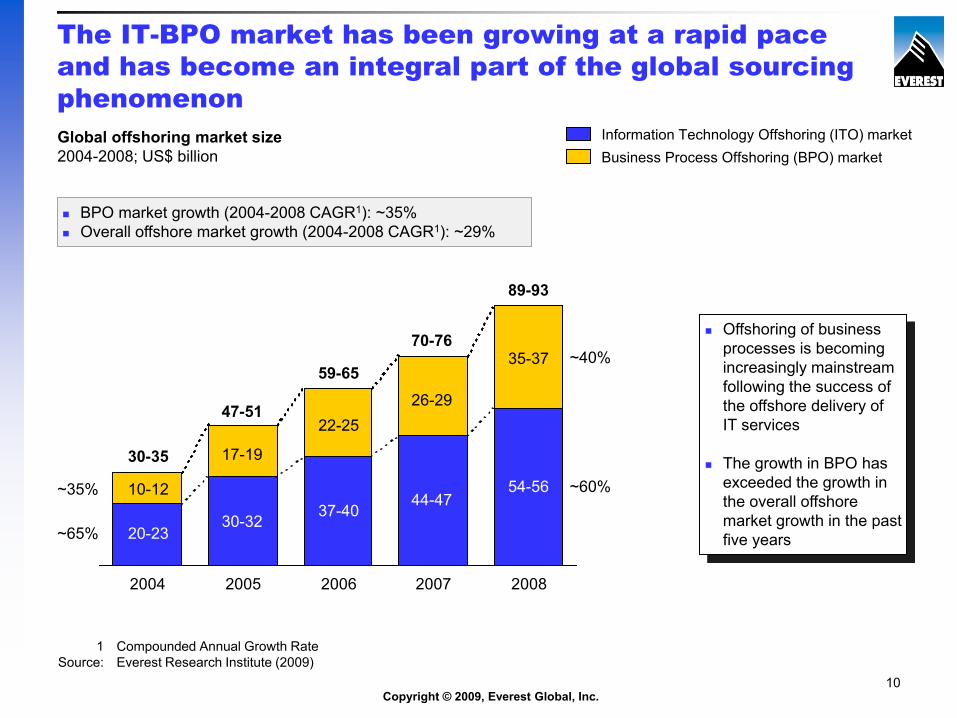

The IT-BPO market has been growing at a rapid pace and has become an integral part of the global sourcing phenomenonGlobal offshoring market size2004-2008; US$ billion Business Process Offshoring (BPO) market

Information Technology Offshoring (ITO) market

1 Compounded Annual Growth RateSource: Everest Research Institute (2009)

Offshoring of business processes is becoming increasingly mainstream following the success of the offshore delivery of IT services

The growth in BPO has exceeded the growth in the overall offshore market growth in the past five years

2004 2005 2006 2007 2008

~40%

~60%

20-23

10-1244-47

26-29

30-35

70-76

59-65

47-51

89-93

30-32

17-19

37-40

22-25

54-56

35-37

~35%

~65%

BPO market growth (2004-2008 CAGR1): ~35% Overall offshore market growth (2004-2008 CAGR1): ~29%

Copyright © 2009, Everest Global, Inc.11

Offshore BPO market captures a diverse set of services and processes across industry verticals

Revenue distribution by service offerings2008; US$ billion

Human Resources mgmt.

Industry-specific

BPO services

Customer Interaction & Support (call center)

Procurement services

Other BPO services

Finance & accounting

100% = 13

Customer Interaction & Support, which has historically been the leading segment, continues to account for close to 40% of the market

Overall, over a quarter of the market is now providing vertical-specific processes

Knowledge services

2%

13%

27%

9% 4%

42%

3%

Note: Revenues and employees for domestic BPO (Indian clients) excluded from the analysisSources: Everest analysis (2008); response from study participants; NASSCOM

INDIA EXAMPLE

Copyright © 2009, Everest Global, Inc.12

The global sourcing location landscape is evolving rapidly as investors have multiple options today

Eastern EuropeWestern

Europe

Egypt

South Africa

Caribbean

S.E. AsiaIndia

China

Canada

Nigeria

Kenya

Investors today have over 150+ credible offshore delivery options (cities); up from 50 four years ago

Source: Everest Research Institute (2009)

Philippines a key destination

Multiple emerging countries (e.g., Malaysia, Vietnam, Thailand)

Multiple Eastern European countries (e.g., Czech Republic, Poland, Hungary, Romania)

Number of options in North Africa

Multiple location options (e.g., Brazil, Mexico, Argentina, Chile)

Large domestic market, but nascent offshore experience

Mauritius

Copyright © 2009, Everest Global, Inc.13

As a result, multiple countries are competing to grab share in the offshore market

India and Philippines together constitute over half of the offshore BPO market

Market share is shifting towards emerging offshore locations, as they become increasingly significant

2004

52% 45%38% 32% 27%

41%46%

49%52%

50%

7% 9% 13% 16%23%

10-12 17-19 22-25 26-29

2005 2006 2007

Share of offshore BPO marketUS$ billion

100% =

Established offshore destinations

(India, Philippines)

Traditional sourcingdestinations

(Canada, Ireland)

Emerging offshore destinations1

2008

35-37

1 Includes Czech Republic, Romania, Poland, Hungary, South Africa, Mauritius, Egypt, Nigeria, Morocco, Mexico, Brazil, Argentina, Colombia, Chile, Costa Rica, Singapore, Malaysia, Jamaica, El Salvador, Peru, Panama, etc.

Source: Everest Research Institute (2009)

India dominant in IT

BPO EXAMPLE

Copyright © 2009, Everest Global, Inc.14

Mexico

Mexico city

Sao Paulo

Brazil

Santiago

Chile

Mumbai

Bangalore

India

China

Shanghai

Singapore

PolandKrakowBelfast

Ireland

DalianBeijingBudapest

Hungary

Warsaw

IT work for Latin America

Application Development and Maintenance for North America

F&A for Europe and Middle East markets

Loans processing, contact center, and analytics for global businesses

Customer care, transaction processing for U.S. and Asia-Pacific businesses

Application Development and Maintenance, data processing for global businesses

Regional delivery centers

Offshore delivery centers

Example: Global financial services major

Investors assess locations based on a combination of cost, risk and labor pool available.

In addition, the role of each location in a network is determined based on fit across the following dimensions: Geographies Functions Industries Scale

Opportunity for Mauritius to participate in the growing offshore phenomenon

Source: Everest Research Institute (2009)

Metro ManilaPhilippines

Further, investors are building global delivery networks and in doing so, they are diversifying beyond the established locations (India, Philippines)

NOT EXHAUSTIVE

Copyright © 2009, Everest Global, Inc.15

Table of contents

Section I: Perspectives on global sourcing Current state of play Growth opportunity and outlook

Section II: A brief introduction to Mauritius

Section III: Scope of current service delivery (IT-BPO) from Mauritius

Section IV: Comparison of Mauritius with other offshore locations

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.16

The global sourcing opportunity is large and significant

60-61%

Global sourcing market size and opportunity2008; US$

Addressable offshore IT-BPO market opportunity

Current offshore IT-BPO market size (2008)

89-93 billion

1 trillion

Theoretical opportunity to grow market 10 times to

approximately US$1 trillion

42%

10%

58%

90%

Front-office

Back-office

13 220-280100% =

Offshore BPO market size by type of functionUS$ billion

India’s addressable offshore BPO market opportunity

Current offshore BPO market size (2008)

Within BPO, while voice work is likely to grow; non-voice is likely to become increasingly significant

Sources: Everest Research Institute (2009); NASSCOM

INDIA EXAMPLE

Copyright © 2009, Everest Global, Inc.17

However, the sector is witnessing some slowdown due to the global recession

ACV1 of outsourcing transactions signedUS$ million

Outsourcing transactions signedNumber of transactions

Average deal size has shrunk over the previous several quarters

4,0743,804

4,011

2,602

3,2073,553

2,972 2,989

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

The number of outsourcing transactions have remained flat and range bound

385333

403 417

481455

423467

Q32007

Q42007

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

1 Annualized Contract ValueSources: Everest Research Institute (2009); NASSCOM

Average

Copyright © 2009, Everest Global, Inc.18

While offshore market growth is likely to be tempered over the next 12-18 months, the medium-long term outlook remains robust

Offshore BPO industry

Factors likely to affect offshore BPO growth

Factors likely to drive offshore BPO growth

Firms facing survival pressures

Drop in underlying business volumes

Uncertainty driving slower decision making

Political sentiments against offshoring (job losses)

Offshoring a key lever to cut costs

Significant untapped opportunity

Mergers and acquisitions driving additional opportunities

Given these countervailing forces impacting growth, The Everest Research Institute expects the growth rate of the offshore BPO market to be tempered (between 5-15%) over next 12-18 months.However, the medium-outlook remains robust, with growth rate expected to pick up to 20-30% levels

Copyright © 2009, Everest Global, Inc.19

Table of contents

Section I: Perspectives on global sourcing

Section II: A brief introduction to Mauritius Key facts about the Island nation and its economy ICT sector – The fifth pillar

Section III: Scope of current service delivery (IT-BPO) from Mauritius

Section IV: Comparison of Mauritius with other offshore locations

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.20

Quick facts on Mauritius

Situated off the coast of African continent east of Madagascar, Mauritius is a small island nation in the southwest Indian Ocean with a population of 1.28 million people

History of colonialization by the Dutch, French and then by the British. Under the French rule, the island developed a prosperous economy based on sugar production and exports. Achieved independence from the British in 1968

Mauritians are bilingual (speak both English and French). Creole, the local language spoken by over 80% of the population, is similar to French. Some Indian languages (e.g., Bhojpuri, Hindi) also spoken

Ethnic groups comprise of Indo-Mauritian (68%), Creole (27%), Sino-Mauritian (3%), and Franco-Mauritian 2%. Majority are Hindu (48%) with the others being Roman Catholic (24%) and Muslim (17%)

Mauritius, an island nation, has strong cultural affinity with France, UK, and India due to its history…

…and is supported by a growing economy conducive for foreign investment

Key indicators 2005 2006 2007 2008

GDP growth (percentage) 2.3 5.1 5.4 5.3

Per capita GNI (US$) 4314 4810 5576 6157

Inflation FY (percentage) 5.6 5.1 10.7 8.8

Budget deficit FY, (percentage GDP) 5.0 5.3 4.3 3.3

Unemployment rate (percentage) 9.6 9.1 8.5 7.2

The Mauritian economy has registered a healthy average growth rate of 5.6% in recent years

Government has undertaken major economic reforms to facilitate business in Mauritius

These enable investors to set-up and operate in the country seamlessly

Mauritius

Africa Indian Ocean

Sources: CIA Factbook; US Department of State; World Economic Forum; World Bank, Board of Investment; Everest Research (2009)

Copyright © 2009, Everest Global, Inc.21

Even though a part of the African continent, Mauritius is widely regarded as a relatively “developed” nation

GDP per capita current prices US$ at PPP

Estimated at ~US$12,000 at PPP, Mauritius has the sixth highest GDP per capita in Africa, after Equatorial Guinea, Seychelles, Botswana, Gabon and Libya

Widely regarded as a developed country, Mauritius has a higher GDP per capita than several African countries that are emerging as offshore services locations

Mauritius has evolved from a low-income, agriculture-based economy to a growing middle-income economy reliant on sugar, textiles and apparel, financial services, and tourism

This has resulted in a more equitable income distribution and a much-improved infrastructure

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2007 2008 2009E

MauritusSenegalMoroccoTunisiaEgyptSouth AfricaGhanaKenya

Sources: CIA Factbook; US Department of State; World Economic Forum; World Bank; Everest Research (2009)

Copyright © 2009, Everest Global, Inc.22

14%

37%24%

5%14%

3%11%

38%

25%

17%

25%

38%

31%28%

48%38%

59%70%

48%

66% 61%

Egypt Ghana Kenya Mauritius Morocco SouthAfrica

Tunisia

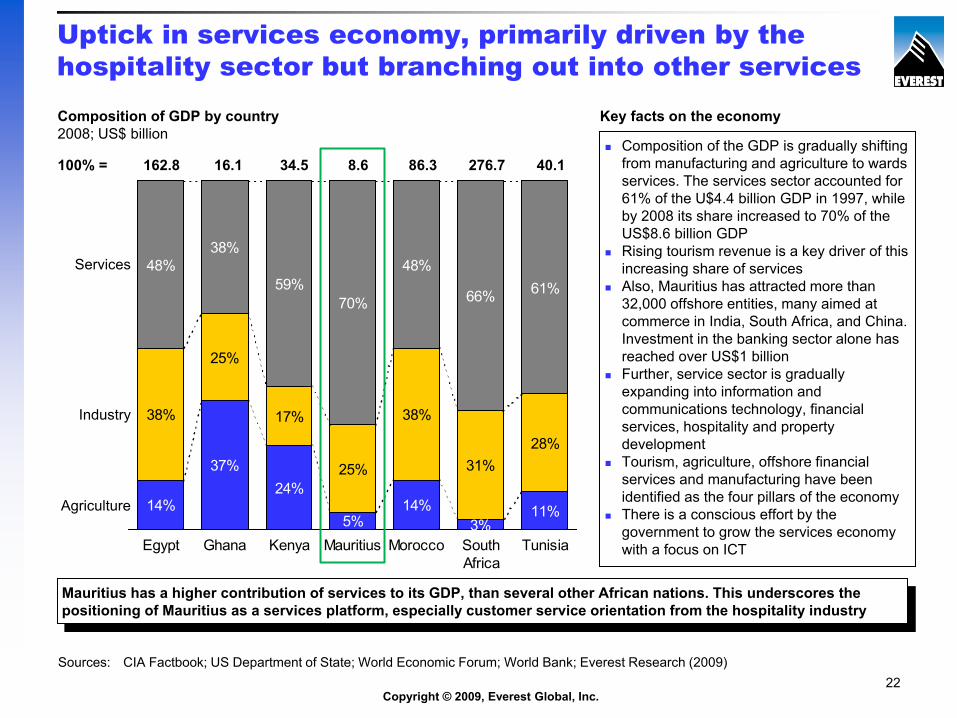

Uptick in services economy, primarily driven by the hospitality sector but branching out into other servicesComposition of GDP by country2008; US$ billion

Agriculture

Industry

Services

100% = 16.1 34.5 8.6 86.3 276.7 40.1 Composition of the GDP is gradually shifting

from manufacturing and agriculture to wards services. The services sector accounted for 61% of the U$4.4 billion GDP in 1997, while by 2008 its share increased to 70% of the US$8.6 billion GDP

Rising tourism revenue is a key driver of this increasing share of services

Also, Mauritius has attracted more than 32,000 offshore entities, many aimed at commerce in India, South Africa, and China. Investment in the banking sector alone has reached over US$1 billion

Further, service sector is gradually expanding into information and communications technology, financial services, hospitality and property development

Tourism, agriculture, offshore financial services and manufacturing have been identified as the four pillars of the economy

There is a conscious effort by the government to grow the services economy with a focus on ICT

Key facts on the economy

Mauritius has a higher contribution of services to its GDP, than several other African nations. This underscores the positioning of Mauritius as a services platform, especially customer service orientation from the hospitality industry

162.8

Sources: CIA Factbook; US Department of State; World Economic Forum; World Bank; Everest Research (2009)

Copyright © 2009, Everest Global, Inc.23

The ICT sector is being recognized as the ‘fifth pillar’ of Mauritius’ economy

It is forecasted that the IT-BPO sector will contribute up to 7% of the country’s GDP by 2011

Mauritius’ vision for ICTa. Enable the ICT sector to contribute into the GDP of Mauritiusb. Lead to the ICT sector employing more Mauritiansc. Make for sustained availability of skilled manpower to power the sector, and d. Facilitate contribution from the ICT sector into the Mauritian export basket, initiatives to create an

information society revolve around the instilling of a “technology temper” in Mauritians to bring about increased adoption, ICT-enabled knowledge networking among citizens, and generally accepting ICT as a stream of professional persuasion at par with others

National ICT strategic plan Target to create 29,000 jobs in the ICT sector by

2011 and contribute to 7% of GDP by 2011 Develop a sustainable ecosystem (i.e., talent pool,

physical infrastructure, policies, regulatory environment, etc.) and create an investor-friendly environment Increased adoption of ICT as a preferred career

choice Create an ICT-ready environment through increased

usage and adoption of ICT Inculcation of a ‘technology temper’ and

knowledge networking among citizens

Contribution of the IT-BPO sector to GDPPercentage

1

4

7

2005 2007 2011(E)

Sources: NICTSP; Everest Research (2009); Board of Investment

Copyright © 2009, Everest Global, Inc.24

Mauritius has made significant progress in putting the ecosystem in place from an ICT-readiness standpoint(page 1 of 2)

Developing an ICT conducive environment

Infrastructure development

Ebene Cybercity Well-developed digital network infrastructure and high-bandwidth international leased lines through the SAFE fiber optic cable

Advanced services include the introduction of WiMAX technology, HSDPA technology and 3G mobile networks

Furthermore, the second fiber optic will connect Mauritius to France and UK, amongst other destinations, in 2011 This is expected to further bring down costs and

increase availability Development of technology parks and free-trade

zones. For example, Ebene Cybercity, a state of the art cyber park, houses 52 IT/BPO companies

Additional technology parks under construction

Highest penetration of internet users in Africa (internet penetration estimated at 14.5% for 2008 with a total of 185,000 internet subscribers)

Post liberalization of the telecom sector, the number of connected lines has grown to over 364,500 in 2008 from 65,00 in 1991.

Fixed line penetration of 28.7% for its 1.2 million population

Prevalence of e-banking and e-governance

Sources: Everest Research (2009); Board of Investment; NICT Survey, ICTA

14.513.1

10.910.3

6.35

2003 2004 2005 2006 2007 2008

Internet Penetration in MauritiusPercentage

Copyright © 2009, Everest Global, Inc.25

Mauritius has made significant progress in putting the ecosystem in place from an ICT-readiness standpoint(page 2 of 2)

Year Relevant legislation1998 Copyright Act (Amendment)2001 ICT Act2002 Electronic Transactions Act2003 Computer Misuse &

Cybercrime Act2006 Business Facilitation Act 2009 Data Protection Act

Talent development

Formal education Significant rise in secondary and tertiary education

enrolments Increase in adoption of knowledge-based

programs (e.g., information technology, engineering, finance and accounting, business management) among students

Training and skill-development programs HRDC: Administers training grants for employers Empowerment Foundation: Supports special

training and skill-development programs for unemployed people

ICT Academy: Soft skills and technical/domain training to industry workers and aspirants

Customized networking and telecom courses dispensed in French

PolicyDevelopment

Rise in tertiary enrolments‘000s

2629

33 35

2004 2005 2006 2007

Conducive business environment (e.g., low tax rates)

Streamlined process for investors to live and work in Mauritius (Occupation permit issued in ~3 working days)

Modern labour laws adopted to the needs of the ICT industry

Data Protection Act to comply with EU IP and data protection norms

Sources: Everest Research (2009); Education statistics department; Board of Investment

Copyright © 2009, Everest Global, Inc.26

Overview of the education system in Mauritius

Number of institutions

Type of institutions/ credentials awardedAnnual enrolments

~10,000 students in 2007/08; a 5.4% increase from the last year

6 public institutions

3 polytechnics

30 private institutions

~8,500 students appeared for HSC in 2007/08

~17,350 students examined for SC

180 schools

180 schools

University-level first stage (Diploma of 2 year duration)

University-level second stage (3-4 year Bachelor)

University-level third and fourth stages (Masters, M.Phil, PhD)

Upper secondary school

Length of program: 2 years

Primary and lower-secondary school

Length of program: 11 years including kinder garden

Universities, Institutes and colleges awarding Bachelor’s degrees, Diploma, Master’s Degree and PhDs

Tertiary level

Higher School Certificate (HSC) /

General Certificate of Education A-level

School Certificate (SC)/General Certificate of Education O-level

Education in Mauritius is provided free of cost till the senior secondary level and in government colleges till the tertiary level

Some SC qualified students may proceed directly for tertiary courses such as distance education, diplomas

Sources: Everest Research (2009); Education statistics department, Mauritius

Copyright © 2009, Everest Global, Inc.27

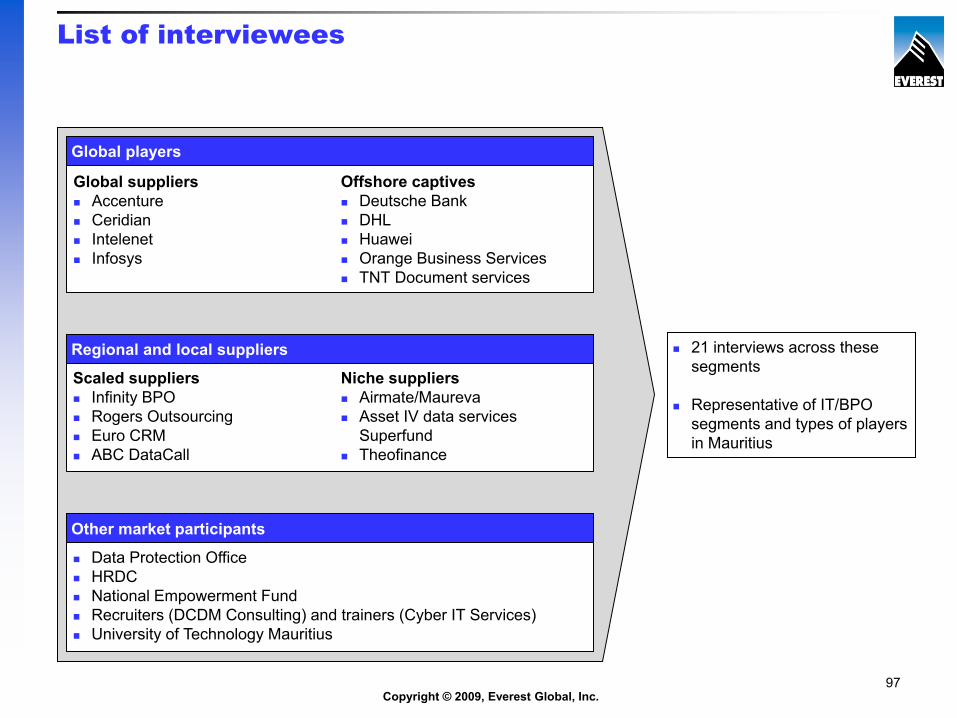

Key organizations involved in ICT development

The Board of Investment (BOI) is the official Investment Promotion Agency of the Government of Mauritius. It is viewed both locally and internationally as a strategic partner for any investor wishing to set up its operations in Mauritius.http://www.boimauritius.com

The National Computer Board (NCB) was set up by the National Board Act to promote the development of Information and Communication Technologies in Mauritius. It vision is to be the key enabler in transforming Mauritius into a Cyber Island and the regional ICT hub.http://www.ncb.intnet.mu/

Outsourcing & Telecommunications Association of Mauritius (OTAM) is an association of call centers/BPO’s, software developers, Internet Service Providers, International Long Distance operators established to promote the creation of an environment conductive to the growth of the ICT industry in Mauritius.http://www.otam.mu/

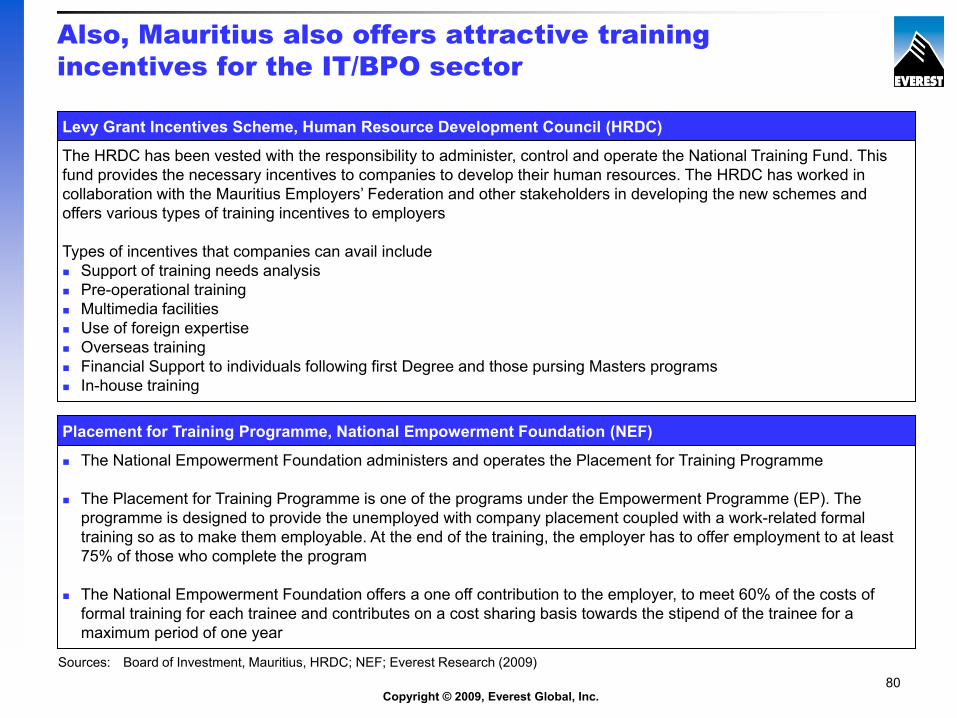

Human Resource Development Council was set up in accordance with the HRD Act with 27 members representing the different sectors of the economy. It’s aim is to promote human resource development in line with national economic and social objectives for successful transformation of the country into a Knowledge Economy. http://www.hrdc.mu/

The National Empowerment Foundation administers, controls and operates the Placement for Training Programme under the Empowerment Programme (EP). It attempts to address the problem of mismatch in the labor market, and the high rate of unemployment. The programme is designed to provide the unemployed with an in-company placement coupled with a work-related formal training so as to make them employable.

Copyright © 2009, Everest Global, Inc.28

Key organizations involved in ICT development

Enterprise Mauritius is a collaborative partnership between industry and the government that aims to help businesses in Mauritius expand into regional and international markets, and at the same time develop their internal capability to meet the challenges of international competition. Focus areas would be to promote exports, support enterprise development and provide competitive intelligence.www.enterprisemauritius.biz

Founded in 2003 the Chambre de Commerce et d'Industrie France-Mauritius (CCIFM) comprises of 96 companies and entrepreneurs from France and Mauritius. The CCIFM aims at nurturing the commercial relationship that exists between the two countries and works in close collaboration with the French embassy, the French economic mission, the Board of Investment (BOI) and the Mauritius Employers Federation. www.ccifm.intnet.mu/

Founded in 2001, the Mauritius IT Industry Association (MITIA) represents the interests of the data processing industry near the government and contributes to the setting up of an environment which will support the prosperity and the competitiveness of the data processing industry at the international level and which is to strategic and commercial alliances. MITIA also nurtures the establishment of close connections with other regional and international ICT associations.http://www.mauritius-mitia.org/join.html

Copyright © 2009, Everest Global, Inc.29

Table of contents

Section I: Perspectives on global sourcing

Section II: A brief introduction to Mauritius

Section III: Scope of current service delivery (IT-BPO) from Mauritius Overall market size and growth Key facts on current scope of services Case studies that illustrate scope and maturity of services

Section IV: Comparison of Mauritius with other offshore locations

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.30

2,392 3,8015,513 6,960

10,440

29,000

2004 2005 2006 2007 2008 2011E

The IT-BPO industry in Mauritius has witnessed an impressive growth of 45% annually between 2004-2008

Evolution of employment opportunities in Mauritius2004-2008; Total employees in IT-BPO sector

The IT-BPO industry in Mauritius has experienced sustained growth from less than 100 companies in 2004 to 250+ companies in 2008. Employment opportunities have grown ~5 times since 2004 with several marquee players establishing operations

The IT-BPO sector generated revenues of ~US$200 million during FY 2008-09

Target to create 29,000 jobs in the ICT sector by 2011

Sources: Everest Analysis (2009); NICTSP, Questionnaire responses; Board of investment, Mauritius

Copyright © 2009, Everest Global, Inc.31

A numbers of suppliers and captives have established their operations in Mauritius

NOT EXHAUSTIVE

Source: Everest Research (2009)

Local/regional Mauritius suppliers

Captive operations

Global suppliers

Copyright © 2009, Everest Global, Inc.32

Offshore market size in Mauritius is comparable to that of other emerging destinations

Offshore-experienced IT/BPO talent pool by country2009; Number of employees in ‘000s

Source: Everest Research (2009)

0.8-0.9

5-6

6-7

7-8

9-10

9-10

13-14

31-32

44-45Poland

Morocco

Egypt

South Africa

Mauritius

Tunisia

Senegal

Jamaica

Kenya

Number of leading global suppliers and captives serving offshore markets 2009

Has a large domestic market of over 100,000 jobs

2-4

4-6

1-2

1-2

13-15

14-16

12-14

13-16

48-52Poland

Morocco

Egypt

South Africa

Mauritius

Tunisia

Senegal

Jamaica

Kenya

Offshore industry size in Mauritius is comparable to many of its larger peers (e.g., South Africa, Tunisia)

Copyright © 2009, Everest Global, Inc.33

11%

4%85%

Majority of the service delivery from Mauritius is BPO focused, with a fair mix of voice and non-voice BPO services

BPO ITO

100% = 10,400

Employee split by outsourcing services2009; Number of employees

Non-voice BPO (52% of

the market)

Corporate services (F&A, HR)

Voice BPO(front-office)

Industry specific- BPO(Insurance claims, account servicing)

Knowledge services (Data Mgmt., business research,

and information services)

Others1

BPO employees split by types of BPO functions served2009; Number of employees

1 Include Multimedia, 3D/Graphic design, Engineering services, etc.Note: The analysis is representative of ~70% of the market ( ~7,280 employees) extrapolated to cover the entire market (~10,400 employees)

Sources: Questionnaire responses; Interviews with leading service providers, Everest analysis

Mostly ADM

48%

28%

11%

13%

Number of employees

100% = 8,840

Voice BPO (48% of the

market)

Copyright © 2009, Everest Global, Inc.34

While diverse functions are currently being served from Mauritius, the scalability is limited

Typical processes deliveredTypical scale of large providers Player landscape

Voice (French and English-language call center)

Includes global and local/regional suppliers

Local/Regional suppliers have a larger average size of operations than their global counterparts

Inbound: Customer service, helpdesk, query resolution, bookings

Outbound: Campaigns, Customer surveys, telesales, collections

400-500 FTEs

Non-voice(Back-office BPO)

Numerous captives operating shared service centers

Significant presence of global suppliers running small scale transaction processing operations

F&A and HRO (e.g., Account Payable, General Ledger, Accounts Receivable, Payroll, Employee benefits, Global mobility, Reporting and Compliance)

Insurance claims and policy administration

Account servicing

250-350 FTEs

IT services Evidence of IT work, though small scale

Global suppliers more prominent in this space

Applications development and maintenance using Microsoft technologies, Java/J2EE, etc.

Technical service desk Datacenter operations and disaster

recovery

100-150 FTEs

Knowledge services Niche providers and global suppliers operating in this space

Business research Information services Data and document management Content management and publishing

50-100 FTEs

Sources: Everest Analysis (2009); Interviews with IT-BPO suppliers and captives in Mauritius

Copyright © 2009, Everest Global, Inc.35

Though most of the work delivered currently is transactional in nature, Mauritius is starting to move up the value-chain with few instances of higher-order work

Accounts payable | General accounting

Contact Center

Back-office BPO(F&A example)

Channel management

Lifecycle management

Customer data acquisitionCustomer service (simple queries)

Sales and marketing

Accounts receivableFixed assets | Tax

ReportingCompliance

Management reporting

Cross sellCustomer analyticsCustomer surveys

Treasury & risk

Audit

Capital budget

Knowledge services

Presentation supportData management and archiving

Information services

Business research

Investment research

Financial modelingRisk analytics

Legal process

Majority of current service delivery in Mauritius

Incr

easi

ng c

ompl

exity

and

val

ue d

eliv

ered

Increasing scope/diversification of service delivery

Customer survey, high-value customer service, etc.

Compliance, MIS and audit

Legal Process, Business Research

Early evidence of higher-order workRule-based/TransactionalJudgment orientedStrategic

BPO EXAMPLE

Source: Everest Analysis (2009)

Copyright © 2009, Everest Global, Inc.36

25%

40%

34%

Majority of service delivery is Bi-lingual with clear strengths in French-language delivery

Only French

Only English

Bi-lingual (English &

French)

Other languages1 - 1%

1 Spanish, Dutch, Italian and GermanNote: The analysis is representative of ~70% of the market ( ~7,280 employees ) extrapolated to cover the entire market (~10,400 employees)

Sources: Questionnaire responses; Interviews with leading service providers, Everest analysis

Employment distribution by language of service delivery2009; Number of employees

100% = 10,400

Pure English work is mostly non-voice BPO (e.g., payroll, claims processing)

Limited English voice work in Mauritius

Mauritius is one the few offshore locations that can support bilingual operations (French and English) in meaningful scale

Copyright © 2009, Everest Global, Inc.37

While France is the largest offshore market served, there is meaningful work delivered for English-speaking markets also

1 Includes Middle-East, Asia, Caribbean, Israel, RussiaNote: The analysis is representative of 70% of the market ( ~7,280 employees ) extrapolated to cover the entire market (~10,400 employees)

Sources: Questionnaire responses; Interviews with leading service providers, Everest analysis

Employment distribution by source geography served2009; Number of employees

7%

16%

3% 2%

10%

19%

43%

Domestic

U.S., Canada

UK

France

Benelux

Africa Others1

French-speaking population of Canada. However, there is evidence of U.S focused work as well

Key Anglo-Franco market

Largely non-voice work

Largest market served across Contact center, BPO and IT services

French-speaking population of North Africa and English speaking population of sub-Saharan Africa

100% = 10,400

Copyright © 2009, Everest Global, Inc.38

While local/regional service providers account for ~70% of the industry, global companies drive scale

Employment distribution by type of providerNumber of employees

17%

12%

71%

100% = 10,400

Global suppliers

Local/regional suppliers

Offshore captives

Average scale of operations by type of providerEmployees

250

150

50

800

350

650

Scale of largest provider Employees

Sources: Questionnaire responses; Interviews with leading service providers, Everest analysis

Multiple global suppliers and offshore captives in Mauritius (as illustrated on Page 26)

Global supplier

Offshore captive

Local/regional supplier

Copyright © 2009, Everest Global, Inc.39

22%8%

3%

26%

4%

14%

23%

A wide range of industry verticals are being supported, with some spikes in Telecoms and high-tech, BFSI

Employment distribution by vertical supportedNumber of employees

BFSITravel, hospitality,

and tourism

Telecom and Hi-tech

Other industries1

BFSI The evolved domestic offshore investments

industry potentially provides ‘transferable skills’ to the BPO industry

Tourism and Hospitality An incubator of foreign language skills (e.g.,

Spanish, Italian, German, Dutch), in addition to being fluent speakers of French and English

Customer service orientation helps in improved employability for the BPO sector

Logistics Several international logistics providers are

present in Mauritius given its geographical positioning to serve the African region

Examples of captives leveraging Mauritius as a shared services delivery location

Telecom Liberalization of the telecom sector has resulted in

availability of domain-specific skills within the domestic market. (e.g., Emtel, Orange)

Logistics

Manufacturing

E-commerce, media and entertainment

1 Others refer to all other client industry verticals (e.g., healthcare, pharmaceutical, retail, government etc.)Note: The analysis is representative of ~70% of the market ( ~7,280 employees ) extrapolated to cover the entire market (~10,400 employees)

Sources: Questionnaire responses; Interviews with leading service providers, Everest analysis

100% = 10,400

Copyright © 2009, Everest Global, Inc.40

Several examples and case studies demonstrate that service providers in Mauritius are successfully delivering a wide-array of services to offshore clients

Evidence of relatively niche/domain-specific work

IT and knowledge services

Contact center (French and bilingual)

Non-voice transactional BPO

1 2

34

Wide scope of services and multiple leverage models5

Copyright © 2009, Everest Global, Inc.41

Non-voice transactional BPO case studies1

Sources: Questionnaire responses; Interviews with leading service providers

1 2

345

Examples of non-voice BPO work delivered

The client is UK’s leading hospitality company that has outsourced its HR and payroll to the service provider as a part of a 5-year outsourcing deal

Mauritius offshore delivery center along with the service provider’s onshore facility in the UK, administers HR services, payroll and related technology services to more than 33,000 employees of the client worldwide

The Mauritius team has been set up with 50% of existing employees and 50% new graduates from universities and the domestic hospitality/tourism sector

The team operates 24/7 and provides non-voice and related-IT services in HRO

Software development using Microsoft technologies (e.g., .net, VB, C#)

HR transaction processing and payroll as per UK norms

Third-party administration of Payroll and related HR services for a UK client

Shared services unit of a large multinational delivers transactional F&A processes (e.g., invoice processing, claims) for its offshore operations in French-speaking countries

A global outsourcing services suppliers delivers F&A (AP, GL, AR, and business services (e.g., Visual aids) for its French-speaking customers in Europe

A leading global BPO supplier provides order management and transactional F&A to its French-clients

Qualified accountants of F&A shared service operations perform claims approval, payments, compliance and audit for the French-speaking African countries

Data capture, cleaning and data management services of media reports, press releases for a leading publication house in France

Case Vignettes: Back-office processing for the French market

Copyright © 2009, Everest Global, Inc.42

Contact center (French and bilingual) case studies2

Sources: Questionnaire responses; Interviews with leading service providers

1 2

345

Examples of contact center services delivered for French market

A global BPO supplier provides third-party sales support (e.g., quotations, follow-up, maintenance contracts) for the French operations of a leading high-tech and telecom MNC

Third party after-hours customer service for high-value French customers (corporate and platinum/priority) of a leading credit card company

Third Party campaigns on new product offering, sales support and post-sales customer service for a leading global media and publishing corporation

Third Party inbound customer service for France’s leading directory services/listing company focused on the French-market

Third-party outbound customer satisfaction surveys for the French customers of a leading auto manufacturer

Outbound fund-raising for the Art and donations for community service for a leading European insurer

Case vignettes: French Contact Center

The client is a leading player in the international assistance market operating in the vehicle, travel and lifestyle, medical, and home assistance space

The client sources inbound assistance services for France, Part of Europe and Canada and Southern African region, including transactional back-office services for the group company in UK

The inbound English call center team in Mauritius delivers hotline, emergency assistance, claims, helpdesk, concierge, and customer service for the client’s customers

On the non-voice side, the team in Mauritius provides claims processing, medical and legal transcriptions and software development services to its client’s group company in the UK

The center is complaint with the European Data Protection Act for processing sensitive financial information of its European clients

Administration of bilingual inbound assistance services for a leading assistance company

Copyright © 2009, Everest Global, Inc.43

Evidence of relatively niche/domain-specific work

Examples of relatively niche/domain-specific work delivered for offshore clients

3

Sources: Questionnaire responses; Interviews with leading service providers

1 2

345

With a team of over ~170 people, the offshore banking entity at Mauritius provides a range of offshore banking services to financial institutions, international business groups and its private clients

The Fiduciary team provides middle-office support services (e.g., accounting, administration) to the bank’s corporate trust structures and provides solutions for institutional clients

The private wealth management team provides custodian, investment, portfolio management services to high-net worth clients taking advantage of the extensive range of double taxation agreements available to the entity. Attractive concessions include reduction of withholding tax on bank interest in a number of DTA jurisdictions

The trust and securities team offers corporate services, Fund services and Trust Services backed by a supporting team providing Statutory and Fund Accounting support

The global transaction support team is responsible for the establishment and ongoing administration of capital markets special purpose entities through provision of management reporting, bookkeeping, accounting and accompanying administration services

Offshore financial services center of a leading European Bank

A leading European provider of worldwide business communication solutions operates its global service center from Mauritius

The team at Mauritius provides LI and L2 technical support for incident and problem management, service delivery coordination and project management for IT, Telecom and IP projects

~150 FTE managing service desk, ~50 engineers for network deployment, network optimization and IT security; ~50 FTEs performing IP telephony support, maintenance and upgrade functions

The talent pool employed are B.Sc graduates, engineers, A-levels with specialist networking certifications (e.g., CCNA, MCSE)

Managed services in communication network solutions

Copyright © 2009, Everest Global, Inc.44

IT and knowledge services case studies4

Sources: Questionnaire responses; Interviews with leading service providers

1 2

345

Examples of IT application outsourcing and knowledge services work delivered

A large global supplier provides Application development and outsourcing services to its French-speaking European clients using technologies such as Oracle family of applications, SAP, Java/J2EE and other Netcentric technologies, as well as dedicated testing services

Application development in Java/J2EE and Microsoft Technologies for supporting a large Anglo-Dutch bank’s applications

Application development and maintenance of document management and content management platforms for a leading publishing and document services supplier

Case Vignettes: IT Applications development

A leading provider of database and analytical tools providing investment research information to the investment industry/community, operates its delivery and research operations in India and Mauritius

The delivery centers create, manage and administer several platform-based product offerings around databases of environmental, social and governance information covering 2,500+ publicly listed companies

While the India team provides data mining and information gathering, the team at Mauritius verifies, cleans, tests and collates the information

~80 research analysts having backgrounds in Economics, Finance and Social sciences perform quantitative and judgment-based work from Mauritius

Delivery of platform-based business research and information services

Copyright © 2009, Everest Global, Inc.45

Investors leveraging Mauritius in multiple ways

Sources: Questionnaire responses; Interviews with leading service providers

1 2

345

5

Examples of distinctive role in global services supply chain

A leading global telecom equipment supplier operates its shared services center for the African region from Mauritius

Has selected Mauritius over other locations for bilingual skills, low cost structure, stable business environment, investor friendly policies, and favorable quality of life for its expatriates

The 170+ strong team delivers transactional F&A (AP, GL, AR). In addition, some higher-order processes such as compliance, closing of books, management reporting are also delivered from the operation

Leverages technology (ebanking, ERP platforms) to transmit high-volume of data/transactions

Employs B.Com graduates with ACCA/CIMA qualifications

Regional hub for the African region and parts of Europe

A couple of leading global suppliers of outsourcing services leverage Mauritius to support delivery of their projects for the European market or French Canada

While a typical ‘follow-the-sun’ approach is used to leverage Mauritius in certain projects, the French-skills of Mauritians proves to be a distinctive capability in several other projects

Reading technical specification documents, design documents, interacting with French-speaking client teams constitute areas in IT projects where Mauritius plays a distinctive role

Similarly, contact center (emails, chat) and processing invoices in French in BPO

Complementing supplier’s global delivery network in delivering IT projects

Copyright © 2009, Everest Global, Inc.46

Investor experiences have been positive

Sources: Questionnaire responses; Interviews with leading service providers

Investors express their satisfaction with Mauritius operations

Copyright © 2009, Everest Global, Inc.47

Table of contents

Section I: Perspectives on global sourcing

Section II: A brief introduction to Mauritius

Section III: Scope of current service delivery (IT-BPO) from Mauritius

Section IV: Comparison of Mauritius with other offshore locations Costs Talent pool Structural factors and risks

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.48

Costs

Fully loaded operating cost (including salaries, real estate, telecom, etc.)

Granular views to costs as applicable to the type of function Call center (French and English) F&A (transactional) IT ADM

Multiple views Entry-level pool Language skills Specialized skills Experienced pool

Telecom and other infrastructure

Connectivity/Accessibility Geo-political and

macroeconomic stability Safety and security Quality of Life Legal and regulatory

environment Business environment Incentives

The report compares Mauritius with other offshore destinations across three broad factors that most companies trade-off in making location decisions

Note: FS stands for Financial Services

Copyright © 2009, Everest Global, Inc.49

Mauritius has been compared with its relevant peers in this assessment

Examples of countries Key characteristics

India Philippines

Suited to support large scale centers (multiple ‘000 FTEs)

Account for >50% of the global offshore marketEstablished locations

Types of offshore locations

Emerging locations

French-speaking locations Morocco Tunisia Senegal Romania Poland Lithuania

English-speaking locations South Africa Kenya Ghana Jamaica Egypt Sri Lanka Vietnam

Suited to support medium scale (1000-2000 FTE) to limited scale (~500) centers

Increasingly being considered by investors as they seek to diversify beyond established locations and build a global delivery network

Relevant peer group for Mauritius

The report primarily compares Mauritius with its peer group of emerging locations as relevant by function

Source: Everest Analysis (2009)

Copyright © 2009, Everest Global, Inc.50

Table of contents

Section I: Perspectives on global sourcing

Section II: A brief introduction to Mauritius

Section III: Scope of current service delivery (IT-BPO) from Mauritius

Section IV: Comparison of Mauritius with other offshore locations Costs Talent pool Structural factors and risks

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.51

Total cost of operations has been assessed based on a bottom-up analysis of cost of delivery for a specific function at a city level

Agent salaries

Bonus Statutory

benefits Other

benefits: Transport, Meals

Supervisor and manager salaries

Bonus Statutory

benefits Other

benefits: Transport, Meals

Support staff (IT, HR, accounts) salaries

Statutory benefits

Training costs

Attrition-related costs

Real estate rentals

Fixtures and fit-outs

Utilities

Telecom Equipment

(servers, switches, networking, etc.)

Miscellaneous bucket

Captures 40+ data elements

Does not include supplier margins, travel, and one-time expenses

Elements included in above heads

Direct operating cost per FTE per annumUS$ per FTE

Salaries and benefits

Management Administration Facilities and real estate

Technology Other direct operating expenses

Total direct operating cost per FTE

ILLUSTRATIVE

Costs benchmarked across functions: Call Center (French and English), F&A and IT

Source: Everest Research Institute (2009)

Copyright © 2009, Everest Global, Inc.52

13-1614-1615-1715-1717-1918-2019-2121-2323-25

54-58

66-70

U.S. Tier 2 UK Tier 2 Lithuania SouthAfrica

Jamaica Egypt Ghana Mauritius Kenya Philippines India

For English language work, Mauritius offers a cost advantage over multiple emerging locations

Direct operating cost1 per FTE for English contact center services2009; US$ ‘000 per annum per FTE

Emerging offshore destinations

Established offshore destinations

1 Ongoing costs only; excludes margins/mark-ups, centralized corporate overheads, initial investment, set-up costs, and travel costs2 For Philippines and India, their respective capital cities Manila and New Delhi have been considered

Note: Exchange rates for local currencies with respect to the U.S. Dollar have been averaged for 7 months from 1-Nov-2008 to 30-June-2009Source: Everest Research Institute (2009)

2 2

~68-74%

ENGLISH WORK

MARKET AVERAGES

Mauritius presents significant arbitrage opportunity (~70% on operating cost basis) over the UK

Source destination

Copyright © 2009, Everest Global, Inc.53

44-46

30-3228-30 27-29 26-28 25-27

21-23 20-2215-17

France Tier 2 Romania Tunisia Lithuania Poland Morocco Egypt Senegal Mauritius

Further, for French language work, Mauritius is the lowest cost offshore delivery location

Direct operating cost1 per FTE for French contact center services2009; US$ ‘000 per annum per FTE

1 Ongoing costs only; excludes margins/markups, centralized corporate overheads, initial investment, set-up costs, and travel costsNote: Exchange rates for local currencies with respect to the U.S. Dollar have been averaged for 7 months from 1-Nov-2008 to 30-June-2009

Source: Everest Research Institute (2009)

MARKET AVERAGES

FRENCH WORK

~61-67%

Source destination

Mauritius presents significant arbitrage opportunity (~65% on operating cost basis) over France

Emerging offshore destinations

Copyright © 2009, Everest Global, Inc.54

Similarly, for F&A and IT, costs in Mauritius are lower than most other emerging destinations (page 1 of 2)F&A cost comparisonDirect operating cost1 per FTE for transactional F&A services2009; US$ ‘000 per annum per FTE

15-17

34-36 33-3530-32

27-29 26-2823-25 22-24

19-21 18-20 18-20

Poland Tunisia Morocco Romania Lithuania SouthAfrica

Jamaica Egypt Mauritius Kenya India

1 Ongoing costs only; excludes margins/markups, centralized corporate overheads, initial investment, set-up costs, and travel costs2 New Delhi has been used as a proxy for India to get the F&A cost

Note: Exchange rates for local currencies with respect to the U.S. Dollar have been averaged for 7 months from 1-Nov-2008 to 30-June-2009Source: Everest Research Institute (2009)

MARKET AVERAGES

Emerging offshore destinationsEstablished offshore destinations

2

Copyright © 2009, Everest Global, Inc.55

Direct operating cost1 per FTE for IT Applications Development and Maintenance2009; US$ ‘000 per annum per FTE

41-43 41-43 40-42 37-3933-35

30-3225-27

22-2421-23

Poland Morocco Tunisia Romania Egypt Lithuania Mauritius Vietnam India

Similarly, for F&A and IT, costs in Mauritius are lower than most other emerging destinations (page 2 of 2)IT cost comparison

1 Ongoing costs only; excludes margins/markups, centralized corporate overheads, initial investment, set-up costs, and travel costs2 New Delhi has been used as a proxy for India to get the IT cost

Note: Exchange rates for local currencies with respect to the U.S. Dollar have been averaged for 7 months from 1-Nov-2008 to 30-June-2009Source: Everest Research Institute (2009)

MARKET AVERAGES

Emerging offshore destinationsEstablished offshore destinations

2

Copyright © 2009, Everest Global, Inc.56

Romania Tunisia Lithuania Poland Morocco Egypt Senegal Mauritius

Key drivers are the lower salaries in Mauritius and in some cases, lower telecom costs relative to peers

30-3228-30 27-29 26-28 25-27

21-23 20-22

15-17

Salaries,Management,

andAdministration

Facilities

Telecom

Breakup of direct operating cost per FTE per annum2009; US$ ‘000 per FTE per annum

Miscellaneous1

Cos

t hea

ds

1 Miscellaneous costs include training, attrition cost etc.Note: Exchange rates for local currencies with respect to the Euro have been averaged for 7 months from 1-Nov-08 to 30-June-09

Source: Everest Research Institute (2009)

MARKET AVERAGES

FRENCH CALL CENTER

Entry-level salaries are lower in Mauritius compared to its peers for French call center work School-leavers (SC and HSC) typically employed in Mauritius, compared to tertiary graduates in many other countries However, school leavers have proven quite effective for call center work. Reasonably good employability of school leavers (20-25%), comparable to that of tertiary graduates in other countries

Salaries for experienced roles are higher given the relatively small pool of middle-senior management talent

Copyright © 2009, Everest Global, Inc.57

While there are opportunities for reduction in Mauritius’ telecommunication costs, they are lower than North African countries even at current levelsAnnual rental tariffs for IPLC (telecom)1

2009; US$ per E1 connection

1,63,200

1,36,800

1,33,200

1,26,000

93,600

79,080

72,000

67,200

66,737

60,000

58,800

46,691

13,325

Tunisia

Senegal

Romania

Jamaica

Morocco

Lithuania

Kenya

Egypt

Vietnam

Ghana

Mauritius

South Africa

India

Telecom costs in Mauritius have been falling significantly over the years (~30% each year) Costs expected to reduce further through connection to the fiber optic cable (expected in 2010) This is likely to strengthen Mauritius’ overall cost position

12,600

10,500

7,900

6,300

4,900

3,000

2003 Feb 2006 Jul 2006 Sep 2006 Jan 2009 2010(E)

Telecom rentals / license (IPLC 2 Mbps)MUR per annum

Trends in Mauritius’ telecom tariffs

Target

Note: Exchange rates for local currencies with respect to the U.S. Dollar have been averaged for 7 months from 1-Nov-08 to 30-June-09 Sources: Everest Research Institute (2009); Real estate reports, BOI

Copyright © 2009, Everest Global, Inc.58

Telecom costs in Mauritius are expected to decline further with the advent of the second fiber-optic cable

Planned initiative A high-capacity undersea

fiber-optic cable linking Africa to Asia and Europe via the Middle East

Expected capacity of 1.28Tb/s enabling high-speed services

Cable expected to provide Mauritius, and South and East African countries with access to major business centers globally, and support the growing demand for broadband

Current status Cable went live in July 2009

at a landing station in South Africa to meet the bandwidth needs of the Africa continent

Additional, landing stations have been planned at Mauritius, Kenya, Madagascar and other points along the east coast of Africa

Security teams have been beefed up at various places to protect the slow moving cable layers

Impact and implications The fiber optic is expected

to bring down international bandwidth costs substantially

Significant increase in bandwidth, ~ 10 times current capacity

Multiple telecom operators expected to become tenants on the cable and pass on its benefits to consumers

Higher availability and better SLAs are expected to be offered

Source: Service Provider Executive Interviews

Copyright © 2009, Everest Global, Inc.59

Table of contents

Section I: Perspectives on global sourcing

Section II: A brief introduction to Mauritius

Section III: Scope of current service delivery (IT-BPO) from Mauritius

Section IV: Comparison of Mauritius with other offshore locations Costs Talent pool Structural factors and risks

Section V: Implications for investors

Section VI: Appendix

Copyright © 2009, Everest Global, Inc.60

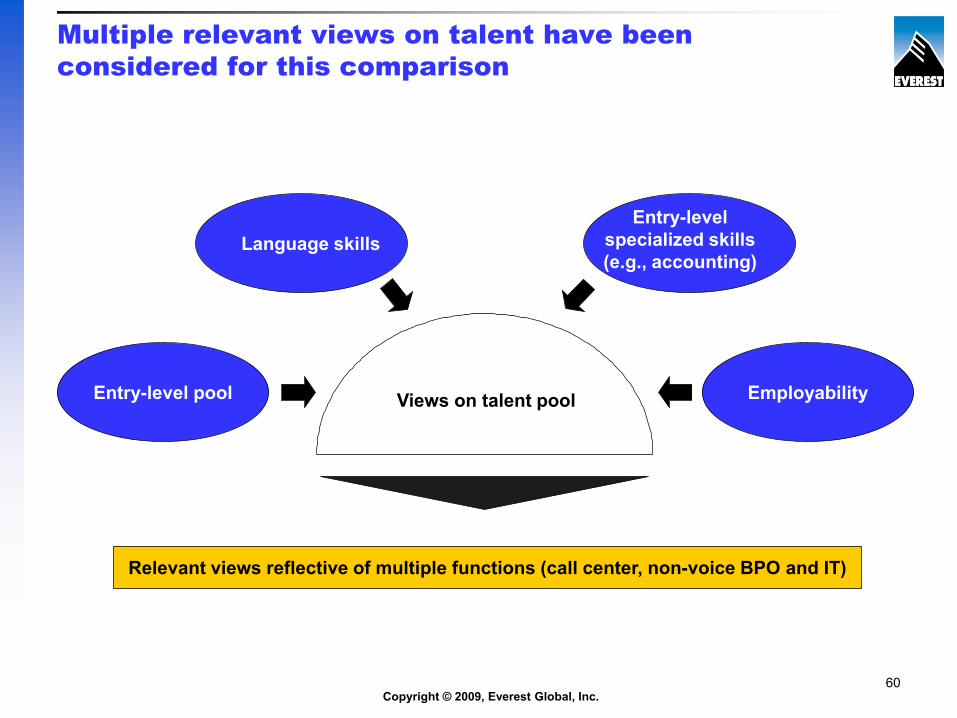

Relevant views reflective of multiple functions (call center, non-voice BPO and IT)

Views on talent pool

Multiple relevant views on talent have been considered for this comparison

EmployabilityEntry-level pool

Entry-level specialized skills(e.g., accounting)

Language skills

Copyright © 2009, Everest Global, Inc.61

7-9

10-12

11-13

34-36

42-44

58-60

62-64

126-128

160-162

274-276

328-330

500-502

30-32

13-15

Poland

Egypt

Vietnam

South Africa

Romania

Morocco

Tunisia

Lithuania

Ghana

Kenya

Jamaica

Estonia

Sri Lanka

Mauritius

Mauritius has a relatively small talent pool

Annual tertiary education labor pool estimates1 by country2008; ‘000s

1 Estimated based on assessment of total enrolments annualized over past 3 years and the structure of the education system Note: Tertiary graduates in Mauritius refer to graduates from government universities, private education and distance mode

Sources: Everest Research Institute (2009); Country-specific education statistics

Copyright © 2009, Everest Global, Inc.62

2-4

13-15

14-16

15-17

15-17

18-20

31-33

60-62

62-64

147-49

3.5-4.5

2-4

Poland

Egypt

South Africa

Romania

Morocco

Lithuania

Tunisia

Ghana

Kenya

Mauritius

Estonia

Sri Lanka

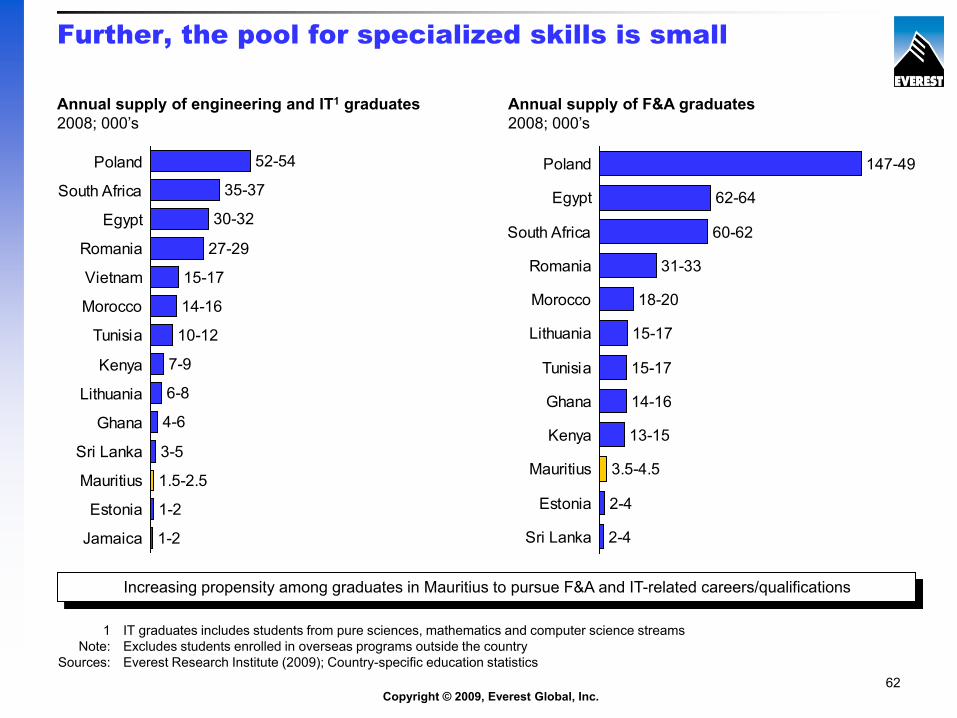

Further, the pool for specialized skills is small

Annual supply of engineering and IT1 graduates2008; 000’s

Annual supply of F&A graduates2008; 000’s

3-5

4-6

52-54

35-37

30-32

27-29

15-17

14-16

10-12

7-9

6-8

1.5-2.5

1-2

1-2

Poland

South Africa

Egypt

Romania

Vietnam

Morocco

Tunisia

Kenya

Lithuania

Ghana

Sri Lanka

Mauritius

Estonia

Jamaica

Increasing propensity among graduates in Mauritius to pursue F&A and IT-related careers/qualifications

1 IT graduates includes students from pure sciences, mathematics and computer science streams Note: Excludes students enrolled in overseas programs outside the country

Sources: Everest Research Institute (2009); Country-specific education statistics

Copyright © 2009, Everest Global, Inc.63

While the scale is relatively small, Mauritius has certain strengths in terms of its talent pool

The labor pool in Mauritius is sufficient to support 4-5 additional centers annually with an average center scale of 400-500 seats

High employability of entry-level talent

Alternative pools available to augment supply

Mauritius’ strengths in talent pool

Willingness to work in IT-BPO

Competitive advantage in

Bilingual skills

1

2

3

4

School-leavers (HSC and SC) in addition to tertiary graduates

IT-BPO is a relatively attractive career option, compared to other sectors (e.g., manufacturing)

Ability to support both French and English

Copyright © 2009, Everest Global, Inc.64

While the tertiary educated pool is small, providers are leveraging high-school and school leavers for transactional and call center work in Mauritius

Mauritius: Total annual addressable1 entry level pool2008; ‘000s

Tertiary graduates2

SC qualified but not pursuing HSC

Total addressable entry level annual pool

2-3

7

12-13.5

3-3.5

HSC qualified but not pursuing tertiary education

Suitability for function / role in IT-BPO sector

Judgment-based back-office processes

IT outsourcing

Call centers Rule-based back-

office transaction processing

Contact center (Inbound/Outbound) French and English

High school leavers and school leavers are typically employed as entry level talent for call center and transactional back-office work in Mauritius

Profile of talent pool being employed in Mauritius for transactional BPO and contact center work2008; ‘000s

1

1 Estimated based on assessment of total enrolments annualized over past 3 years and the structure of the education system2 Tertiary graduates in Mauritius refer to graduates from government universities, private education and distance mode

Sources: Everest Research Institute (2009); Country-specific education statistics

Tertiary level

Higher School Certificate/

General Certificate of

Education A-level

School Certificate/ General Certificate of Education

O-level

Alternative pool

Copyright © 2009, Everest Global, Inc.65

However, the unique strength of Mauritius lies in its bi-lingual skills…

Mauritius offers robust capabilities in both French and English language skills

French is widely spoken in Mauritius Commonly used in day-to day communication Creole, the native language is very similar to French

and it typically requires 2-3 weeks of training time to convert Creole speakers to French

French spoken skills leveraged for call center work

English is the medium of instruction in schools and universities English is also the official language for conducting

business As a result, the quality of written English tends to be

better than that of spoken English Written English skills are widely leveraged for non-

voice operations Some challenges with spoken English skills,

evidence of a ‘French accent’ that needs to be neutralized

2

Source: Everest Research Institute (2009)

Copyright © 2009, Everest Global, Inc.66

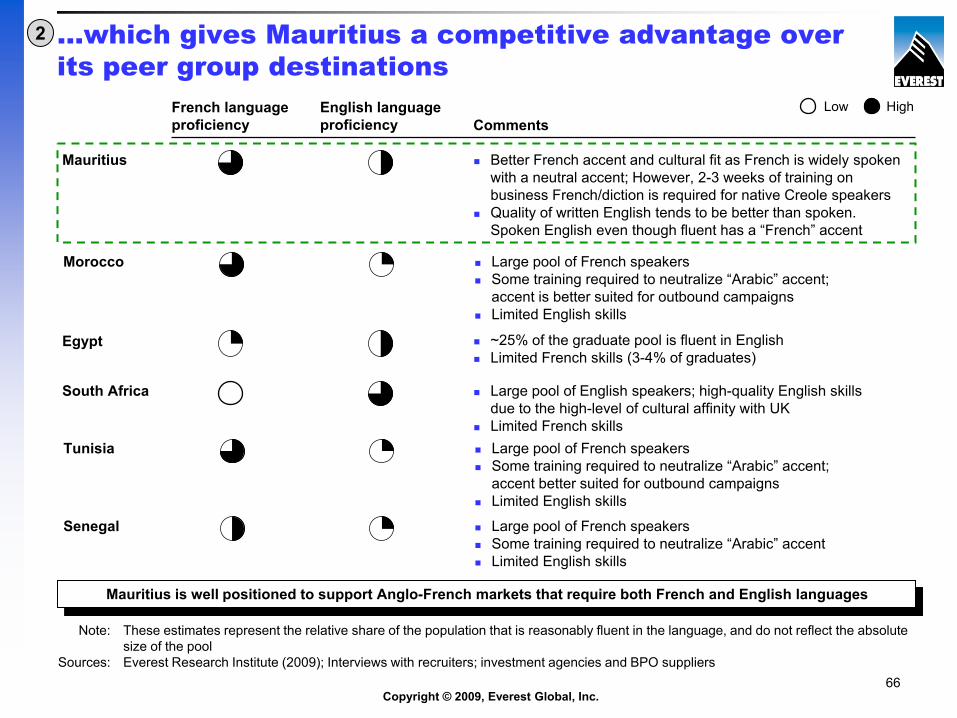

…which gives Mauritius a competitive advantage over its peer group destinations

CommentsLow HighEnglish language

proficiencyFrench language proficiency

Mauritius Better French accent and cultural fit as French is widely spoken with a neutral accent; However, 2-3 weeks of training on business French/diction is required for native Creole speakers

Quality of written English tends to be better than spoken. Spoken English even though fluent has a “French” accent

Morocco Large pool of French speakers Some training required to neutralize “Arabic” accent;

accent is better suited for outbound campaigns Limited English skills

Egypt ~25% of the graduate pool is fluent in English Limited French skills (3-4% of graduates)

South Africa Large pool of English speakers; high-quality English skills due to the high-level of cultural affinity with UK

Limited French skills

Mauritius is well positioned to support Anglo-French markets that require both French and English languages

Tunisia Large pool of French speakers Some training required to neutralize “Arabic” accent;

accent better suited for outbound campaigns Limited English skills

Senegal Large pool of French speakers Some training required to neutralize “Arabic” accent Limited English skills

2

Note: These estimates represent the relative share of the population that is reasonably fluent in the language, and do not reflect the absolute size of the pool

Sources: Everest Research Institute (2009); Interviews with recruiters; investment agencies and BPO suppliers

Copyright © 2009, Everest Global, Inc.67

In addition, the talent pool has reasonably good employability for IT/BPO

30-35%

25-30%

20-25%Call Center(French)

F&A

IT

Typical employability percentage of entry level talent pool in Mauritius Typical profile employed Comments

Employability is comparable to other locations (e.g., Morocco, Tunisia, Egypt) that mostly employ tertiary educated or equivalent profiles for similar roles

F&A courses are modelled on the British system and impart industry-standard practices

Good written English skills Students opting for certification courses

(e.g., ACCA) have better employability

Suited to perform software development work on relatively common programming languages

Some pressures on talent due to relatively small pool

A-levels O-levels Diplomas

University graduates (e.g., Accounting, Economics, Finance, Management)

A-levels pursuing accounting specializations (e.g., ACCA, CIMA)

Engineering graduates Technical diplomas with

certifications (e.g., CCNA, MCSE)

3

Sources: Everest Analysis (2009); Interviews with recruiters and service providers

Copyright © 2009, Everest Global, Inc.68