meeting the challenge of new banking - suruga · pdf filecustomer satisfaction. ... the nilson...

TRANSCRIPT

Meeting the Challenge ofNew Banking

Meeting the Challenge ofNew Banking

Competing on a different level with innovative financial services

Suruga Bank Ltd.May 30, 2006

Presentation to investors on fiscal year ended March 30, 2006

©2006 SURUGA bank, Ltd. All Rights Reserved. 1A

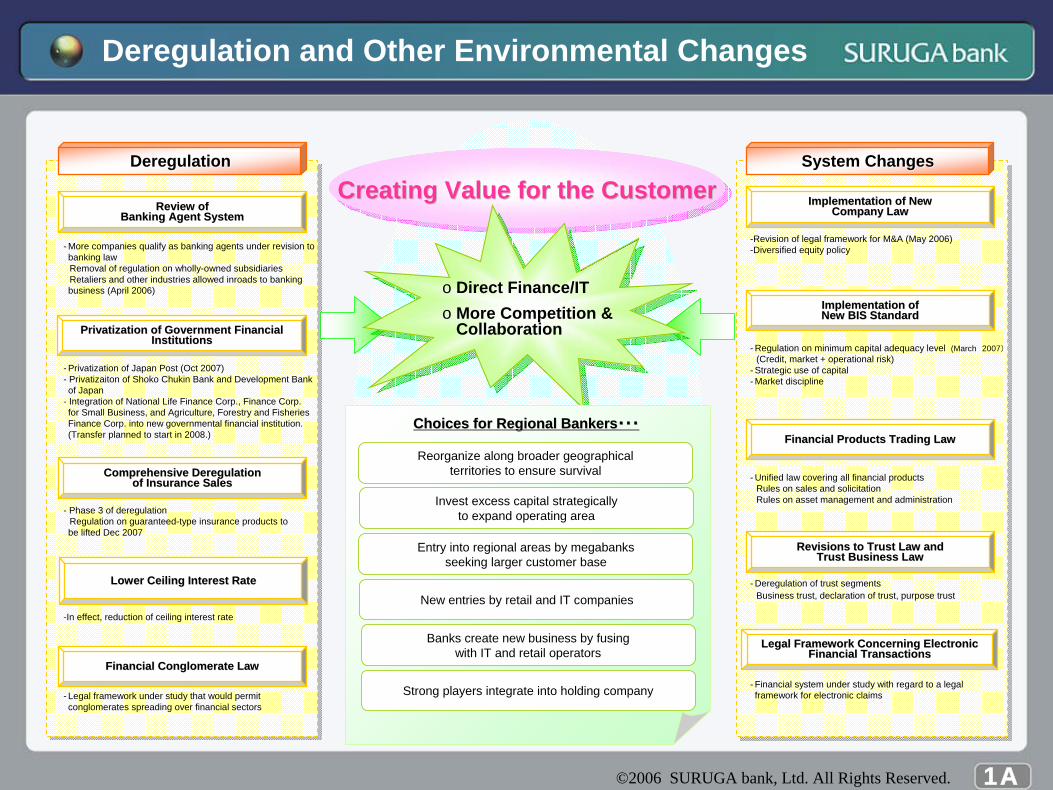

Deregulation and Other Environmental Changes

Legal Framework Concerning Electronic Legal Framework Concerning Electronic Financial TransactionsFinancial Transactions

Implementation of New Implementation of New Company LawCompany Law

-Revision of legal framework for M&A (May 2006)-Diversified equity policy

Revisions to Trust Law and Revisions to Trust Law and Trust Business LawTrust Business Law

- Deregulation of trust segmentsBusiness trust, declaration of trust, purpose trust

Financial Products Trading LawFinancial Products Trading Law

- Unified law covering all financial productsRules on sales and solicitationRules on asset management and administration

- Financial system under study with regard to a legal framework for electronic claims

System ChangesSystem Changes

Implementation of Implementation of New BIS StandardNew BIS Standard

- Regulation on minimum capital adequacy level (March 2007)(Credit, market + operational risk)

- Strategic use of capital- Market discipline

Review of Review of Banking Agent SystemBanking Agent System

- More companies qualify as banking agents under revision to banking lawRemoval of regulation on wholly-owned subsidiariesRetaliers and other industries allowed inroads to banking business (April 2006)

Comprehensive Deregulation Comprehensive Deregulation of Insurance Salesof Insurance Sales

- Phase 3 of deregulationRegulation on guaranteed-type insurance products to be lifted Dec 2007

Financial Conglomerate LawFinancial Conglomerate Law

- Legal framework under study that would permit conglomerates spreading over financial sectors

Privatization of Government Financial Privatization of Government Financial InstitutionsInstitutions

- Privatization of Japan Post (Oct 2007)- Privatizaiton of Shoko Chukin Bank and Development Bank of Japan

- Integration of National Life Finance Corp., Finance Corp. for Small Business, and Agriculture, Forestry and Fisheries Finance Corp. into new governmental financial institution. (Transfer planned to start in 2008.)

DeregulationDeregulation

Lower Ceiling Interest RateLower Ceiling Interest Rate

-In effect, reduction of ceiling interest rate

Creating Value for the CustomerCreating Value for the Customer

o Direct Finance/ITo More Competition &

Collaboration

Choices for Regional BankersChoices for Regional Bankers・・・・・・

Reorganize along broader geographical territories to ensure survival

Invest excess capital strategically to expand operating area

Strong players integrate into holding company

Entry into regional areas by megabanksseeking larger customer base

New entries by retail and IT companies

Banks create new business by fusing with IT and retail operators

©2006 SURUGA bank, Ltd. All Rights Reserved. 1B

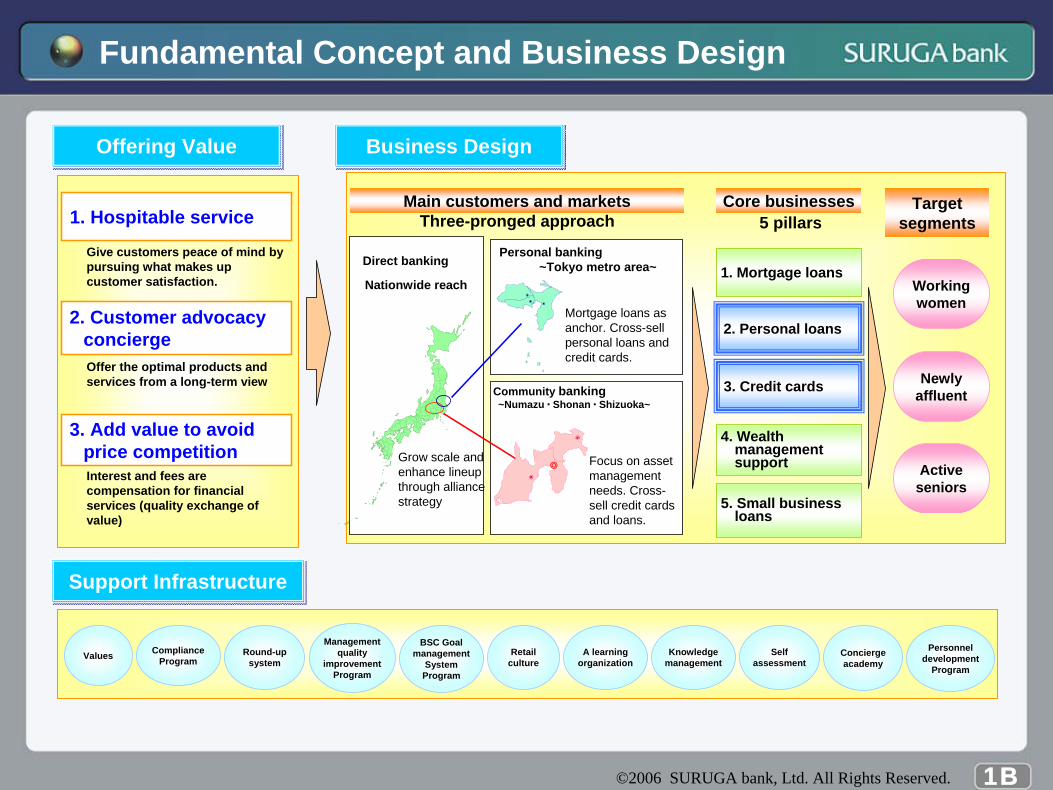

Fundamental Concept and Business Design

1. Hospitable service

2. Customer advocacy concierge

3. Add value to avoid price competition

Direct banking

Nationwide reach

Grow scale and enhance lineup through alliance strategy

Personal banking~Tokyo metro area~

Community banking~Numazu ▪ Shonan ▪ Shizuoka~

Mortgage loans as anchor. Cross-sell personal loans and credit cards.

Focus on asset management needs. Cross-sell credit cards and loans.

Core businesses

1. Mortgage loans

2. Personal loans

3. Credit cards

4. Wealth management support

5. Small business loans

5 pillarsTarget

segments

Working women

Active seniors

Newly affluent

Give customers peace of mind by pursuing what makes up customer satisfaction.

Offer the optimal products and services from a long-term view

Interest and fees are compensation for financial services (quality exchange of value)

Values Round-up system

Management quality

improvementProgram

BSC Goal management

SystemProgram

Retail culture

A learning organization

Knowledge management

Self assessment

Concierge academy

Personnel development

Program

Main customers and marketsThree-pronged approach

ComplianceProgram

Offering ValueOffering Value Business DesignBusiness Design

Support InfrastructureSupport Infrastructure

◎

©2006 SURUGA bank, Ltd. All Rights Reserved. 2A

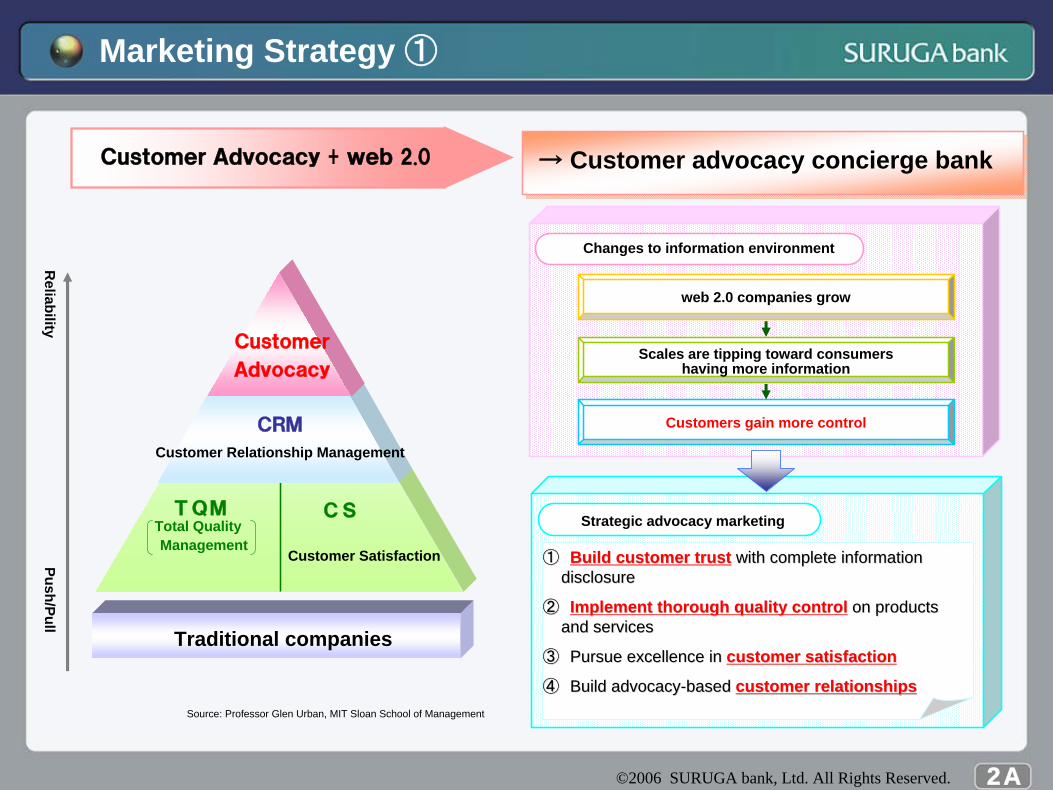

Marketing Strategy ①

Traditional companies

TQM CS

CRM

Customer Relationship Management

Source: Professor Glen Urban, MIT Sloan School of Management

Reliability

Push/Pull

web 2.0 companies grow

Scales are tipping toward consumers having more information

Customers gain more control

Customer

Advocacy

Customer Satisfaction

Customer Advocacy + web 2.0 → Customer advocacy concierge bank

Changes to information environment

Strategic advocacy marketing

①① Build customer trustBuild customer trust with complete information with complete information disclosuredisclosure

②② Implement thorough quality controlImplement thorough quality control on products on products and servicesand services

③③ Pursue excellence inPursue excellence in customer satisfactioncustomer satisfaction

④④ Build advocacyBuild advocacy--based based customer relationshipscustomer relationships

Total Quality Management

©2006 SURUGA bank, Ltd. All Rights Reserved. 2B

Marketing Strategy ②

Reliability

Two-way participationOne-way information flow

bank1.0Push/Pull

Marketing

World of web2.0World of web2.0 Strategic Direction Based on web2.0Strategic Direction Based on web2.0

What is web2.0?What is web2.0?

Three Things web2.0 Share in CommonThree Things web2.0 Share in Common

Information business

Platform is the Internet

Harnesses collective intelligence

Examples of web2.0 CompaniesExamples of web2.0 Companies

Advocated by Tim O’Reilly. Expresses ideals for the next generation for the Web.

A platform concept for coming up with new businesses that understand the rules and qualities inherent to the success of internet companies.

Dem

ocratization of D

emocratization of

information

information

Customer advocacy(Our Philosophy)

Service in other industries

(Enabler strategy)

Dream CRM(Customer advocacy

concierge)

webweb1.51.5

Dynamic Web

webweb2.02.0

Two-way network

webweb1.01.0Static Web with no renewal

Involve customers in product development

(tailor made)

Segment-specific branch strategy

Complete information including competition

(NEFSS)

bankbank2.02.0

©2006 SURUGA bank, Ltd. All Rights Reserved. 3A

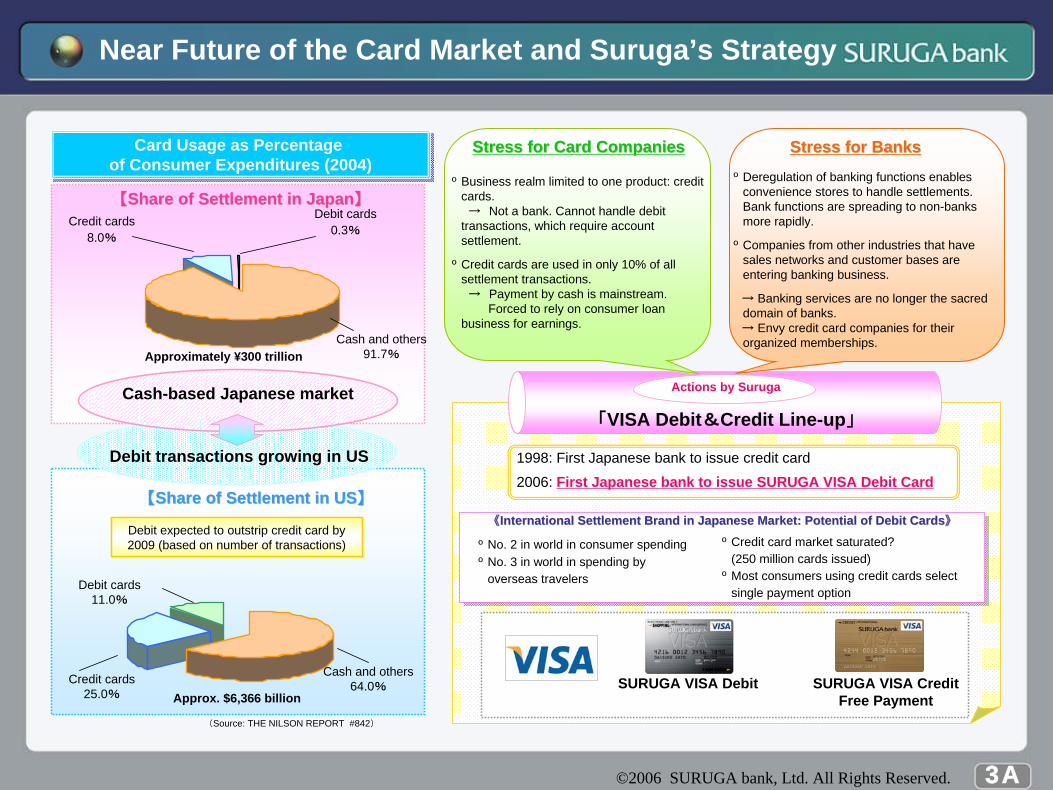

Near Future of the Card Market and Suruga’s Strategy

(Source: THE NILSON REPORT #842)

Approximately ¥300 trillion

Approx. $6,366 billion

Debit expected to outstrip credit card by 2009 (based on number of transactions)Debit expected to outstrip credit card by 2009 (based on number of transactions)

Card Usage as Percentage of Consumer Expenditures (2004)

Card Usage as Percentage of Consumer Expenditures (2004)

Cash-based Japanese market

Debit transactions growing in US

Cash and others 91.7%

Debit cards 0.3%

Credit cards 8.0%

【【Share of Settlement in JapanShare of Settlement in Japan】】

Cash and others 64.0%

Debit cards 11.0%

Credit cards 25.0%

【【Share of Settlement in USShare of Settlement in US】】

Stress for Card CompaniesStress for Card Companies

º Business realm limited to one product: credit cards.→ Not a bank. Cannot handle debit

transactions, which require account settlement.

º Credit cards are used in only 10% of all settlement transactions.→ Payment by cash is mainstream.

Forced to rely on consumer loan business for earnings.

Stress for BanksStress for Banks

º Deregulation of banking functions enables convenience stores to handle settlements. Bank functions are spreading to non-banks more rapidly.

º Companies from other industries that have sales networks and customer bases are entering banking business.

→ Banking services are no longer the sacred domain of banks.→ Envy credit card companies for their organized memberships.

Actions by Suruga

「VISA Debit&Credit Line-up」

1998: First Japanese bank to issue credit card

2006: First Japanese bank to issue SURUGA VISA Debit Card

SURUGA VISA Debit SURUGA VISA CreditFree Payment

《《International Settlement Brand in Japanese Market: Potential of International Settlement Brand in Japanese Market: Potential of Debit CardsDebit Cards》》

º No. 2 in world in consumer spendingº No. 3 in world in spending by

overseas travelers

º Credit card market saturated? (250 million cards issued)

º Most consumers using credit cards select single payment option

©2006 SURUGA bank, Ltd. All Rights Reserved. 3B

Compatibility With and Superiority Over New Settlement Methods

Edy Suica QUICPay SmartPlus iD DCMXmini

Cards Issued 17,000,000 12,240,000 30,000 10,000 20,000 ―

Merchant Stores 31,000 6,000 7,000 1,000 15,000 iD store compatible

Limit ¥50,000 ¥20,000 ¥20,000/transaction ¥30,000/transaction N/A ¥10,000/month

Applicant Requirements N/A

Mobile Suica: VIEW card (credit card) holders (18 years

or older)

JCB credit card holders (18 years or older)

UFJ Nikos credit card holders (18 years or older)

Mitsui Sumitomo credit card holders (18 years or older)

12 years or older (elementary school children excluded, parental consent required)

Major Merchant Stores

am/pm, Royal Host, Circle K Sunkus, Pronto, McDonalds

Family MartBic CameraJonathan, Three F

Royal HostKaraoke Kan, NakauKanachu Hire

Junkudo Book StoreSapporo Drug StoreSkylark Gardens

Bic CameraYodobashi CameraKinokuniya Book Store

―

Member store fee rates remain high

even though transactions are

for small amounts

Terminals (R/W)need to be

standardized ○ Use full account balance without limit

○ No credit screening. OK for 15 years and older.

○ Check balance online or at financial institution ATMs

○ Use at 2.6 million stores in Japan, 24 million worldwide.

○ Can get cash at conveience store and post office ATMs

Wallet Phones

Wallet Phones

Stress for Stress for MerchantMerchant

storesstoresStress for Stress for

usersusers

SOLU

TION

SOLU

TION

SURUGA VISA Debit

Plan to Use VISA Proximity IC Settlement ServicePlan to Use VISA Proximity IC Settlement Service

・iD (SMBC、UC、Seson & NTT Docomo)・QUICPay (JCB & Docomo、au、SB)・SmartPlus

(UFJNicos、DC、MUFG& Docomo、au、SB)・DCMXmini (NTT Docomo)

Credit = PostpaidCredit = Postpaid

・Suica (JR East & Docomo、au)

PrepaidPrepaid

・Edy (BitWallet & Docomo、au、SB) ・ New banking service by au & MUFG

Deposit TypeDeposit Type

(Excerpt from CardWave. Number of cards issued is card + mobile phones)

《《 Suruga Suruga VISAVISA Debit CardDebit Card 》》

Solutions by Suruga BankSolutions by Suruga Bank

Must have credit card to use

service (=credit product)

Limited number of

storesMust upgrade to compatible

phone

Charges are a

hassle

Limit on purchase

amount too low

Balance Concerns

Are Are ‘‘wallet phoneswallet phones’’ really user friendly?really user friendly?

©2006 SURUGA bank, Ltd. All Rights Reserved. 4A

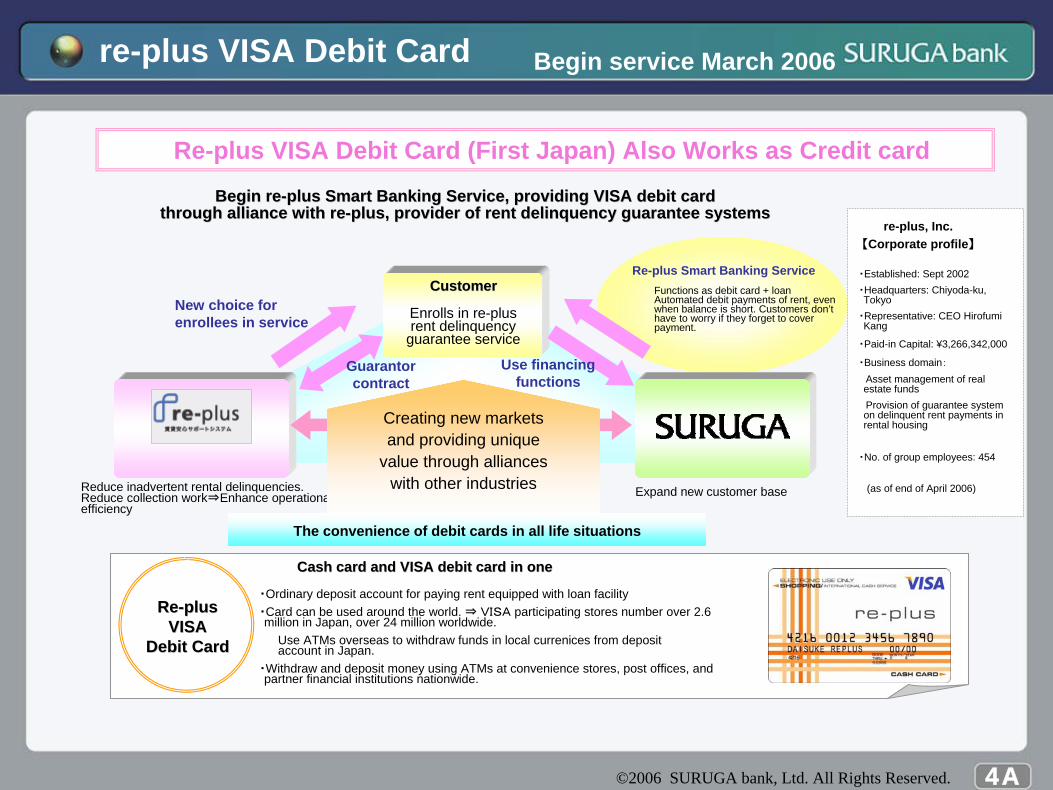

re-plus VISA Debit Card Begin service March 2006

Re-plus VISA Debit Card (First Japan) Also Works as Credit card

Begin reBegin re--plus Smart Banking Service, providing VISA debit cardplus Smart Banking Service, providing VISA debit cardthrough alliance with rethrough alliance with re--plus, provider of rent delinquency guarantee systemsplus, provider of rent delinquency guarantee systems

Reduce inadvertent rental delinquencies. Reduce collection work⇒Enhance operational efficiency

・Ordinary deposit account for paying rent equipped with loan facility・Card can be used around the world. ⇒ VISA participating stores number over 2.6 million in Japan, over 24 million worldwide.

Use ATMs overseas to withdraw funds in local currenices from deposit account in Japan.

・Withdraw and deposit money using ATMs at convenience stores, post offices, and partner financial institutions nationwide.

CustomerCustomer

Enrolls in re-plus rent delinquency

guarantee service

Cash card and VISA debit card in oneCash card and VISA debit card in one

ReRe--plusplusVISAVISA

Debit CardDebit Card

Guarantor contract

New choice for enrollees in service

Expand new customer base

Use financing functions

Re-plus Smart Banking ServiceFunctions as debit card + loanAutomated debit payments of rent, even when balance is short. Customers don’t have to worry if they forget to cover payment.

The convenience of debit cards in all life situations

Creating new markets and providing unique

value through alliances with other industries

re-plus, Inc.【Corporate profile】

・Established: Sept 2002・Headquarters: Chiyoda-ku, Tokyo・Representative: CEO Hirofumi Kang

・Paid-in Capital: ¥3,266,342,000

・Business domain:Asset management of real estate fundsProvision of guarantee system on delinquent rent payments in rental housing

・No. of group employees: 454

(as of end of April 2006)

©2006 SURUGA bank, Ltd. All Rights Reserved. 4B

Strategy for Targeting Lifestyles of Active SeniorsBegan Dream Life Series in February 2006

New business development in Kanagawa (existing service area), which holds a large wealthy market

New business development in Kanagawa (existing service area), which holds a large wealthy market

Change in lifestyle of senior age group

2005年 2010年 2020年 2030年

1. Multiple homes in different locations1. Multiple homes in different locations 2. Sentiment for nature and health (LOHAS)2. Sentiment for nature and health (LOHAS)

① Where they want to liveNear the sea 22.7%Near the mountains 19.5%Resort/holiday home 10.4%

② Reason for home site preferencePlenty of nature 49.8%Can enjoy hobbies 42.6%Mild climate 27.6%

10.8

1.9

6.8

1.0

Current trend and future image

(Source: MLIT)

Product Series Targeting Active SeniorsProduct Series Targeting Active Seniors

Phase 1 (On sale Feb 2006)Phase 1 (On sale Feb 2006)

Dream Life Mortgage Loan

Dream Life Plan 1 (collateralized personal loan)

Dream Life Asset (second mortgage)

Phase 2 (On sale Mar 2006)Phase 2 (On sale Mar 2006)

Dream Life Plan 2 (noncollateralized personal loan)

Phase 3 (Scheduled to begin Autumn 2006)Phase 3 (Scheduled to begin Autumn 2006)

Dream Life Support (reverse mortgage)

Buying a home

Utilizing assets

Resort, second home

Free

Utilizing assets

Grant based on Grant based on ‘‘life resumelife resume’’Suruga’s proprietary evaluation standard for assessing customer life achievements

Future Active Seniors ConceptFuture Active Seniors Concept

Strike the right balance between assets on hand and loans to enjoy a second life.

→ “Extended style”

Want to live a bright and active lifeFormer Senior ConceptFormer Senior Concept

Break into assets on hand. Use what is left over to enjoy a

second life.→ “Closed style”

【【SurugaSuruga’’s Wishs Wish】】

Make wise use of loan products to support a fulfilling and longevous

second life for our customers.

Want to realize their own dreams

Choosy about the life style they lead

Active Seniors ConceptActive Seniors Concept

Product Lineup

Dream Life Series for making our customers’second dream’ a reality

~Evolve beyond sales activity in Tokyo metropolitan area onto the next stage~

Salon de Concierge

Shibuya

Salon de Concierge

Yokohama

Salon de Concierge

NihonbashiSalon de Concierge

Shinjuku

Base camp for realizing Base camp for realizing second life dreamssecond life dreams

In a society where the population is shrinking, this market forecasts population growth until 2015.

Mild climate by the sea. Residential area with unique life style with

“Shonan brand”

Located at entrance to Fuji Hakone National Park. Rich in nature and

history as castle town. Ideal location for second home.

Resort population in surrounding areas is growing

Potential for two Salons de Concierge

Salon de Concierge Salon de Concierge ChigasakiChigasaki

Salon de Concierge Salon de Concierge OdawaraOdawara

Entrance to resort lifeEntrance to resort life

Unit: million people

Providing an elegant day-to-day

©2006 SURUGA bank, Ltd. All Rights Reserved. 5A

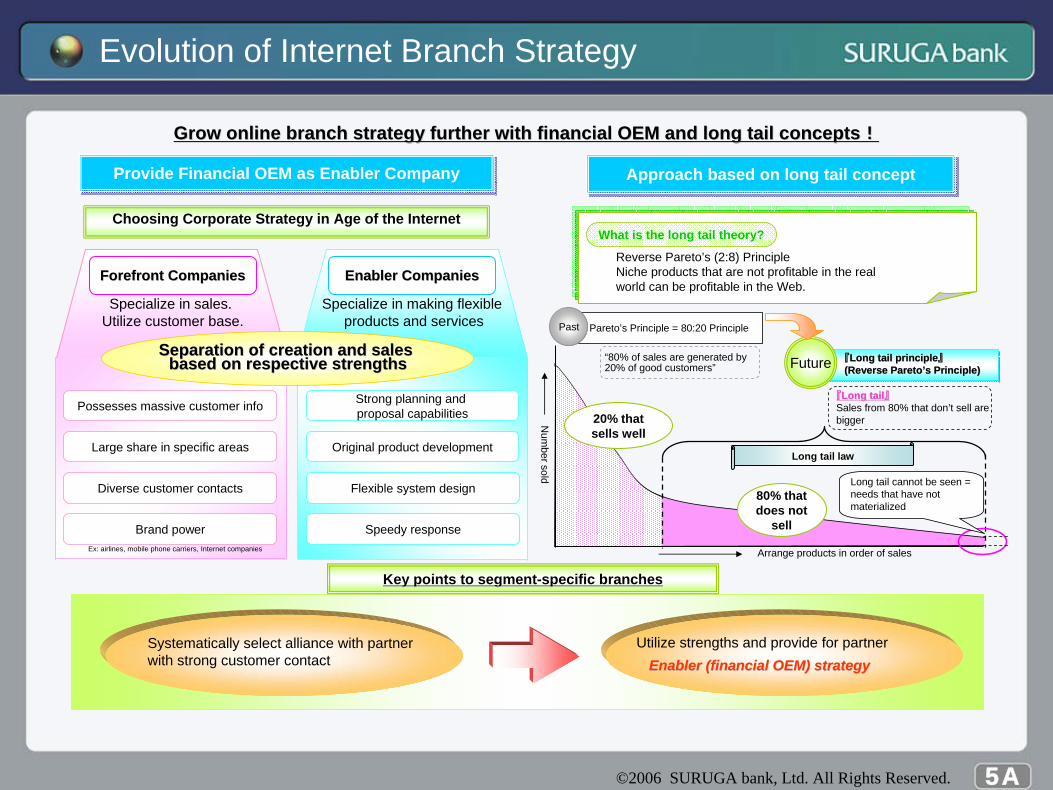

Evolution of Internet Branch Strategy

Key points to segmentKey points to segment--specific branchesspecific branches

Choosing Corporate Strategy in Age of the Internet

Grow online branch strategy further with financial OEM and long Grow online branch strategy further with financial OEM and long tail conceptstail concepts!!

Provide Financial OEM as Enabler CompanyProvide Financial OEM as Enabler Company Approach based on long tail conceptApproach based on long tail concept

Forefront CompaniesForefront Companies Enabler CompaniesEnabler Companies

Specialize in sales. Utilize customer base.

Specialize in making flexible products and services

Possesses massive customer info

Large share in specific areas

Diverse customer contacts

Brand powerEx: airlines, mobile phone carriers, Internet companies

Strong planning and proposal capabilities

Original product development

Flexible system design 80% that does not

sellN

umber sold

Arrange products in order of sales

Long tail law

20% that sells well

Past Pareto’s Principle = 80:20 Principle

Future 『Long tail principle』(Reverse Pareto’s Principle)『『Long tail principleLong tail principle』』(Reverse Pareto(Reverse Pareto’’s Principle)s Principle)

『『Long tailLong tail』』Sales from 80% that don’t sell are bigger

Long tail cannot be seen = needs that have not materialized

“80% of sales are generated by 20% of good customers”

What is the long tail theory?

Reverse Pareto’s (2:8) PrincipleNiche products that are not profitable in the real world can be profitable in the Web.

Separation of creation and sales Separation of creation and sales based on respective strengthsbased on respective strengths

Systematically select alliance with partner with strong customer contact

Utilize strengths and provide for partnerEnabler (financial OEM) strategyEnabler (financial OEM) strategy

Speedy response

©2006 SURUGA bank, Ltd. All Rights Reserved. 5B

Studying Creating New Value with OCN

2,000 2,500 3,000 3,500 4,000 4,500 5,000 5,500

OCN

@nifty

YAHOO!BB

BIGLOBE

DION

Business Development with OCN(OCN: NTT Communications’ ISP)

Customer

Proprietary financial services through Proprietary financial services through segmentsegment--specific branch businessspecific branch business

KnowKnow--how in online banking how in online banking branches + financial branches + financial

infrastructure (currently infrastructure (currently operating 9operating 9

branches and 4 clubs)branches and 4 clubs)

SynergiesTop Internet Service ProviderTop Internet Service Provider

Financial information service site Financial information service site Money Concierge opened Money Concierge opened

May 11, 2006May 11, 2006

◆◆OCN Users: 5.29 million OCN Users: 5.29 million (as of March 2006)

◆◆ Segments of ISPsSegments of ISPs

Merely migrating existing narrowband users to broadband

Promote attractive pricing

Acquiring new broadband users

Promote value added other than price

PuraraPurara

BIGBIGLOBELOBE

BB.BB.exciteexcite

@@niftynifty

YAHOOYAHOO!!BBBB

Currently succeeding in winning over existing and competitors’narrowband users as well as

new users

DIONDIONCreate new valueCreate new value

(Source: “What will happen in the future in the information and telecommunications market” Nomura Research Institute)

2.85 million2.85 million

5.29 million5.29 million

5.30 million*5.30 million*

5.05 million5.05 million

4.20 million*4.20 million*

※OCN・YAHOO・DION info based on March 06 releases. @nifty・BIGLOBE info are estimates.

ODNODN

SoSo--netnet

ASAHIASAHINetNet

SURUGA bank

SURUGA bank

©2006 SURUGA bank, Ltd. All Rights Reserved. 6A

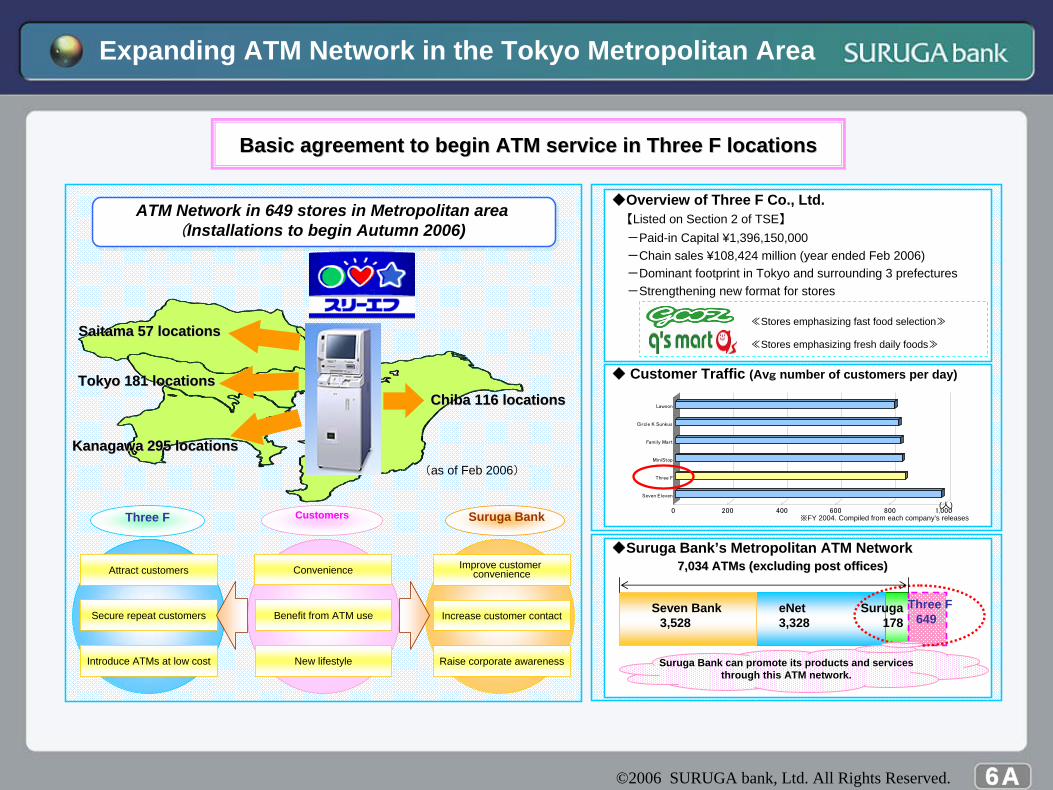

Expanding ATM Network in the Tokyo Metropolitan Area

Basic agreement to begin ATM service in Three F locationsBasic agreement to begin ATM service in Three F locations

Chiba 116 locationsChiba 116 locationsTokyo 181 locationsTokyo 181 locations

Kanagawa 295 locationsKanagawa 295 locations

Saitama 57 locationsSaitama 57 locations

Attract customers

Introduce ATMs at low cost

Convenience

Benefit from ATM use

New lifestyle

Improve customer convenience

Raise corporate awareness

Increase customer contactSecure repeat customers

◆Suruga Bank’s Metropolitan ATM Network

-Chain sales ¥108,424 million (year ended Feb 2006)

≪Stores emphasizing fresh daily foods≫

≪Stores emphasizing fast food selection≫

-Strengthening new format for stores

【Listed on Section 2 of TSE】

-Paid-in Capital ¥1,396,150,000

-Dominant footprint in Tokyo and surrounding 3 prefectures

◆Overview of Three F Co., Ltd.

0 200 400 600 800 1,000

Seven Eleven

Three F

MiniStop

Family Mart

Circle K Sunkus

Lawson

※FY 2004. Compiled from each company’s releases

◆ Customer Traffic (Avg number of customers per day)

7,034 ATMs (excluding post offices)7,034 ATMs (excluding post offices)

eNet3,328

Suruga178

Three F649

Seven Bank3,528

(人)

ATM Network in 649 stores in Metropolitan area(Installations to begin Autumn 2006)

Three F Customers Suruga Bank

(as of Feb 2006)

Suruga Bank can promote its products and services through this ATM network.

©2006 SURUGA bank, Ltd. All Rights Reserved. 6B

Introduction of New Management System

Employing IBM Japan’s Next Generation Financial Services System--NEFSS

(NEFSS:Next Evolution in Financial Services Systems)

More sophisticated customer serviceMore sophisticated customer service Original Products and ServicesOriginal Products and Services Safe and Reliable ServiceSafe and Reliable Service

○ Sophisticated consulting and simulation

○ More powerful solutions with customized products

○ Speedy provision of partner products and services

○ Customer-tailored products and services with CRM

○ Enhance marketing functions using integrated DWH

○ Ubiquitous financial services through channel alliances

○ Lower costs & speed that overwhelms the competition

○ Stable operation 365 days a year, 24 hours a day○ Sophisticated security management and enhanced

downtime resistance

「「System ReformSystem Reform」」 == 「「Management ReformManagement Reform」」

Product StrategyProduct Strategy

Loyalty program

More sophisticated channel strategy

Attract new customers with new products and services

Make decisions at branch locations

Stronger fee and rate functions

Strengthen loan repayment functions

Enable composite products and services

Strengthen alliances with external products

Increase ability to make customer

proposalsSpeedy

delivery of new products and

servicesImprove convenience for customers

Organizational settings make it possible to administer various parameters

Associate accounts with the organization and manage based on various parameters

Strengthen marketing capabilities with team sales management

Flexible response to mergers, spin-offs, and outsourcing

Single source control of diverse data

Expand types of data accumulated

Make effective use of information

Management quantifiers that are compatible with finance

information

More sophisticated campaign strategy

Management Information Management Information ControlControl

OrganizationOrganization

Marketing StrategyMarketing Strategy

Value Added by New Management SystemValue Added by New Management SystemValue Added by New Management System

Points to ReformPoints to Reform

©2006 SURUGA bank, Ltd. All Rights Reserved. 7A

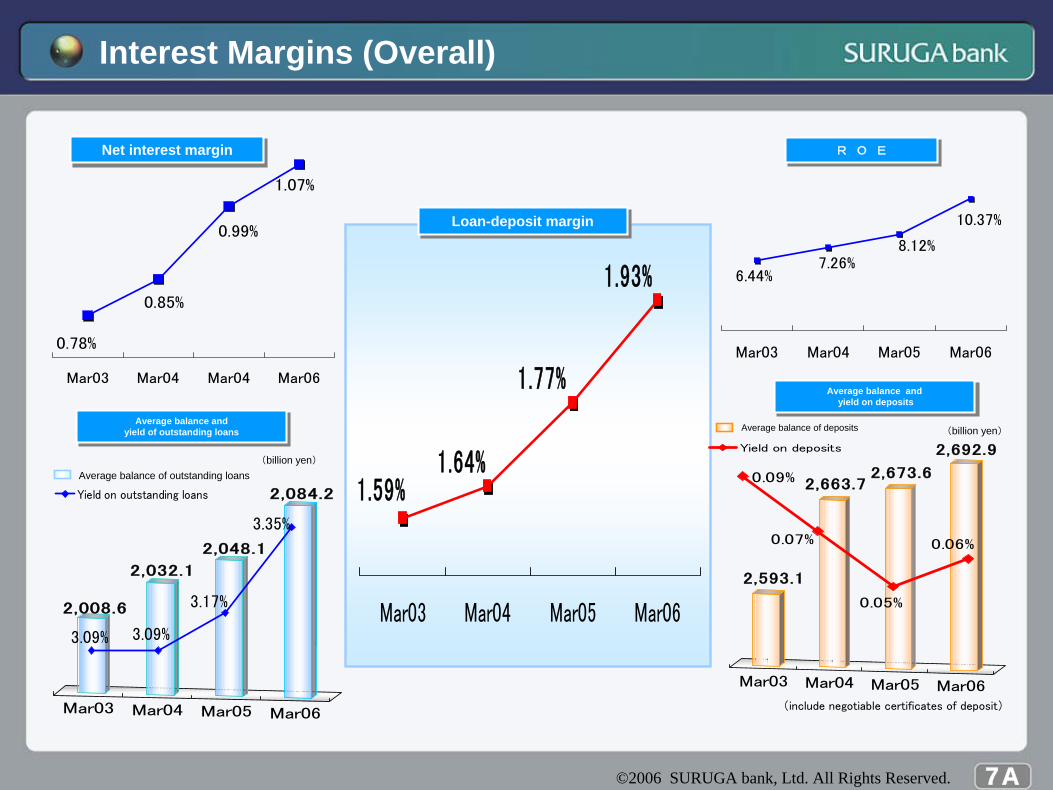

Interest Margins (Overall)

0.78%

0.85%

0.99%

1.07%

Mar03 Mar04 Mar04 Mar06

Mar03 Mar04 Mar05 Mar06

2,008.6

2,032.1

2,048.1

2,084.2

Loan-deposit marginLoan-deposit margin

1.59%1.64%

1.77%

1.93%

Mar03 Mar04 Mar05 Mar06

10.37%

8.12%7.26%

6.44%

Mar03 Mar04 Mar05 Mar06

R O ER O ENet interest marginNet interest margin

Mar03 Mar04 Mar05 Mar06

2,593.1

2,663.72,673.6

2,692.9

0.09%

0.06%

0.05%

0.07%

Yield on deposits

Average balance andyield on deposits

Average balance andyield on deposits

3.17%

3.35%

3.09%3.09%

Yield on outstanding loans

Average balance and yield of outstanding loans

Average balance and yield of outstanding loans

(include negotiable certificates of deposit)

Average balance of outstanding loans

Average balance of deposits

(billion yen)

(billion yen)

©2006 SURUGA bank, Ltd. All Rights Reserved. 7B

Interest Margins (Domestic) ①

Mar03 Mar04 Mar05 Mar06

0 .72%

0 .45%

0 .81%

0 .46%

0 .95%

0 .45%

1.04%

0 .42%

SURUGAAll Regional Banks

Mar03 Mar04 Mar05 Mar06

1 .66%

0 .81%

1 .77%

0 .85%

1 .84%

0 .84%

1.88%

0 .77%

SURUGAAll Regional Banks

loan-deposit marginloan-deposit margin Net Interest marginNet Interest margin

(Sep05)(Sep05)

©2006 SURUGA bank, Ltd. All Rights Reserved. 8A

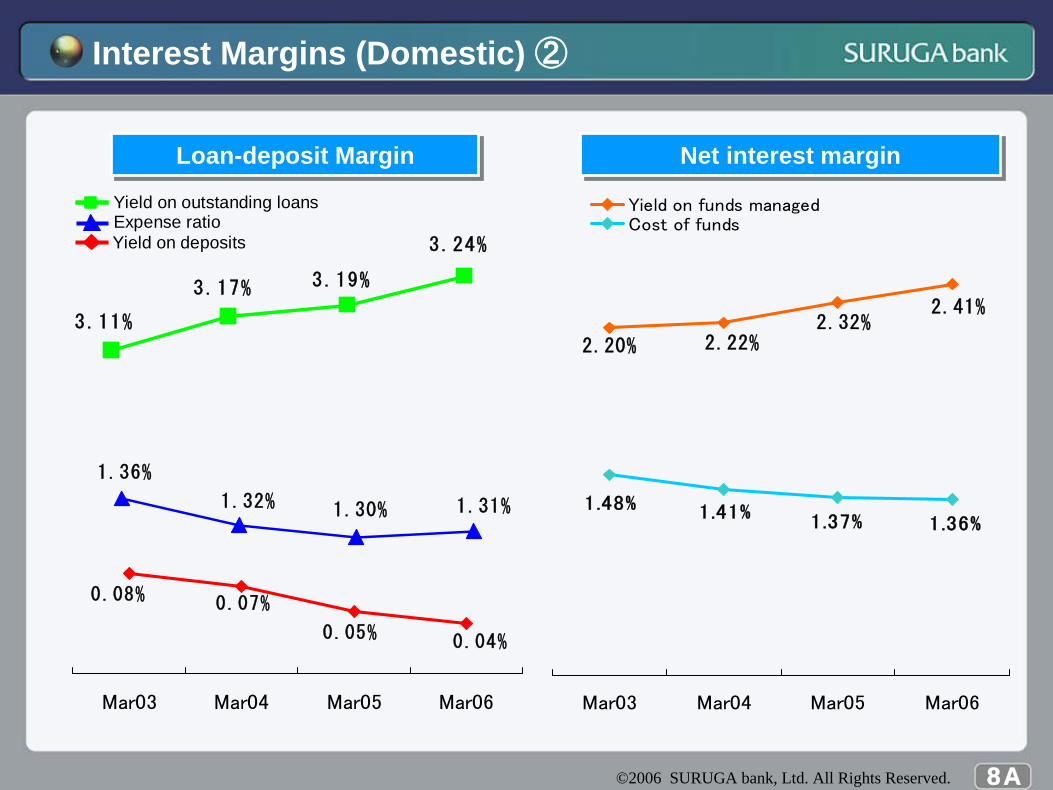

Interest Margins (Domestic) ②

3.24%

3.19%

3.11%

3.17%

1.36%

1.32% 1.30% 1.31%

0.04%0.05%

0.08% 0.07%

Mar03 Mar04 Mar05 Mar06

Loan-deposit MarginLoan-deposit Margin Net interest marginNet interest margin

Expense ratio

2.41%2.32%

2.20% 2.22%

1.36%1.37%1.41%1.48%

Mar03 Mar04 Mar05 Mar06

Yield on funds managedCost of funds

Yield on outstanding loans

Yield on deposits

©2006 SURUGA bank, Ltd. All Rights Reserved. 8B

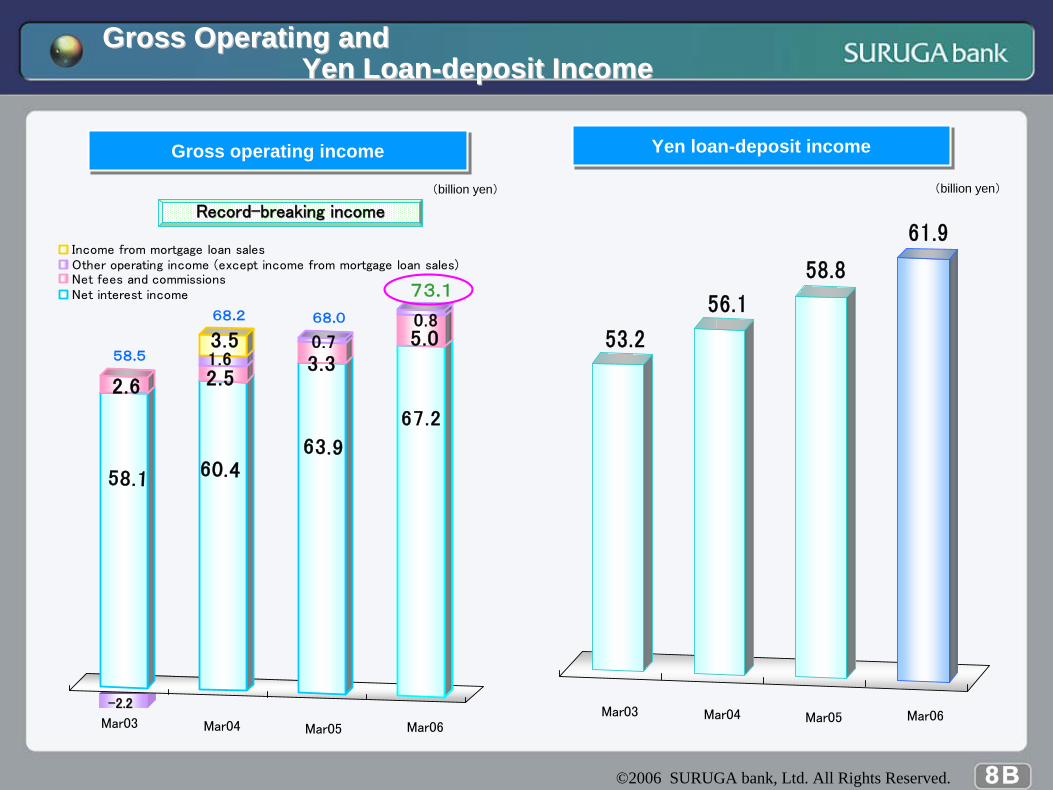

Gross Operating andGross Operating andYen LoanYen Loan--depositdeposit IncomeIncome

58.1

2.6

60.4

2.51.63.5

63.9

3.30.7

67.2

5.00.8

Income from mortgage loan salesOther operating income (except income from mortgage loan sales)Net fees and commissionsNet interest income

53.2

56.1

58.8

61.9

Gross operating incomeGross operating income

68.2

58.5

68.0

--2.22.2

73.1

Mar05Mar03 Mar04 Mar06

RecordRecord--breaking incomebreaking income

Yen loan-deposit incomeYen loan-deposit income

Mar05Mar03 Mar04 Mar06

(billion yen)(billion yen)

©2006 SURUGA bank, Ltd. All Rights Reserved. 9A

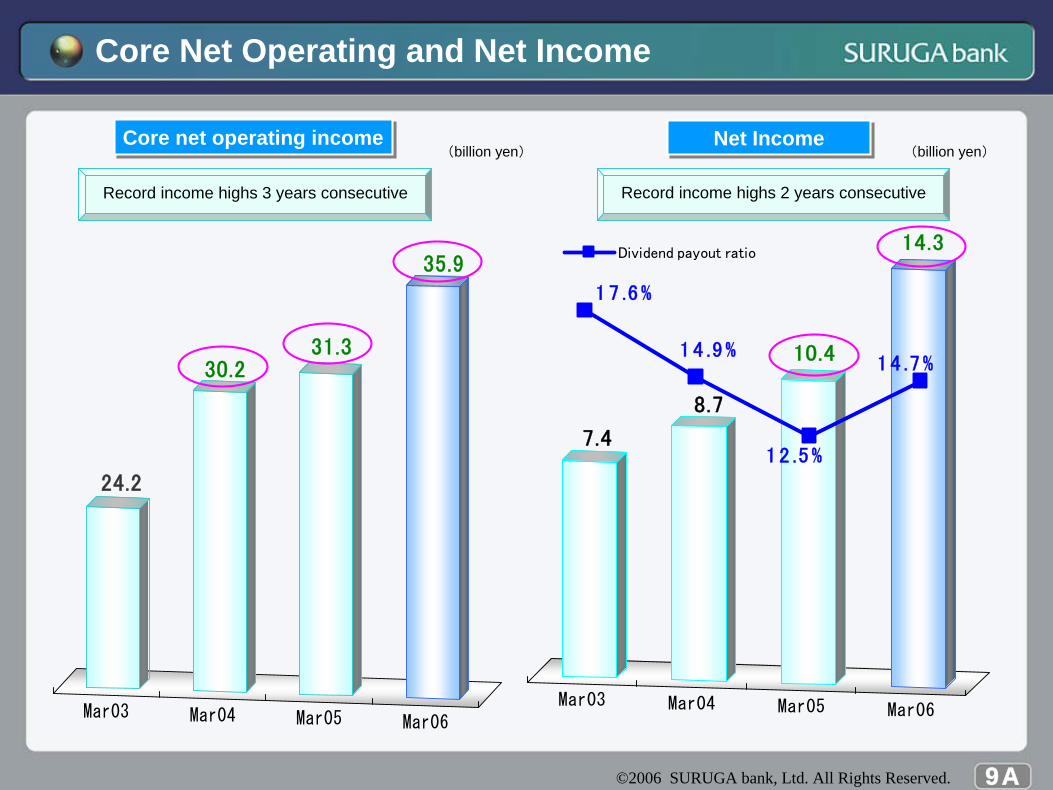

Core Net Operating and Net Income

Mar03 Mar04 Mar05 Mar06

7.4

8.7

10.4

14.3

14 .7%

17 .6%

12 .5%

14 .9%

Dividend payout ratio

Mar03 Mar04 Mar05 Mar06

24.2

30.231.3

35.9

Net IncomeNet IncomeCore net operating incomeCore net operating income(billion yen) (billion yen)

Record income highs 3 years consecutive Record income highs 2 years consecutive

©2006 SURUGA bank, Ltd. All Rights Reserved. 9B

Strong Focus on Retail

Mar03 Mar04 Mar05 Mar06

118.3

117.0

111.7

116.4

100.7

113.2

107.9

112.4

New loans second half

New loans first half

Mar03 Mar04 Mar05 Mar06

1,127.4

172.1

1,207.9

169.8

1,303.6

169.0

1,375.8

196.4

Personal loansMortgage loans

1,299.51,299.5 1,377.81,377.8

1,572.21,572.2

Consumer loan balance and ratioConsumer loan balance and ratio

+94.8+94.8

+78.2+78.2

235.3235.3228.2228.2

213.9213.9

63.8%

66.4%

69.1%

72.0%

+99.5+99.5

1,472.71,472.7 220.4220.4

New loansNew loans

(billion yen)(billion yen)

Consumer loan ratio

©2006 SURUGA bank, Ltd. All Rights Reserved. 10A

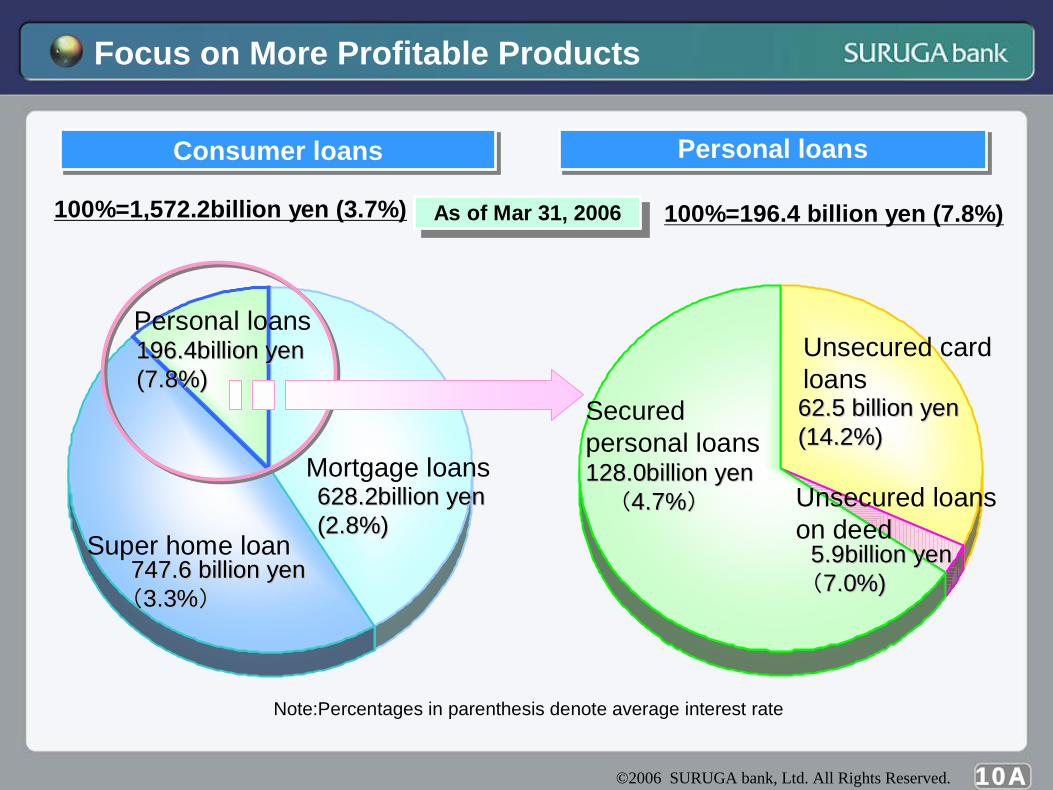

Focus on More Profitable Products

Personal loans

Consumer loansConsumer loans Personal loansPersonal loans

As of Mar 31, 2006As of Mar 31, 2006100%=1,572.2billion yen (3.7%) 100%=196.4 billion yen (7.8%)

196.4billion yen196.4billion yen(7.8%)(7.8%)

Super home loan747.6 billion yen747.6 billion yen((3.3%3.3%))

Mortgage loans628.2billion yen628.2billion yen(2.8%)(2.8%)

Secured personal loans128.0billion yen 128.0billion yen

((4.7%4.7%))

Unsecured card loans62.5 billion yen62.5 billion yen(14.2%)(14.2%)

Unsecured loans on deed

5.9billion yen 5.9billion yen ((7.0%)7.0%)

Note:Percentages in parenthesis denote average interest rate

©2006 SURUGA bank, Ltd. All Rights Reserved. 10B

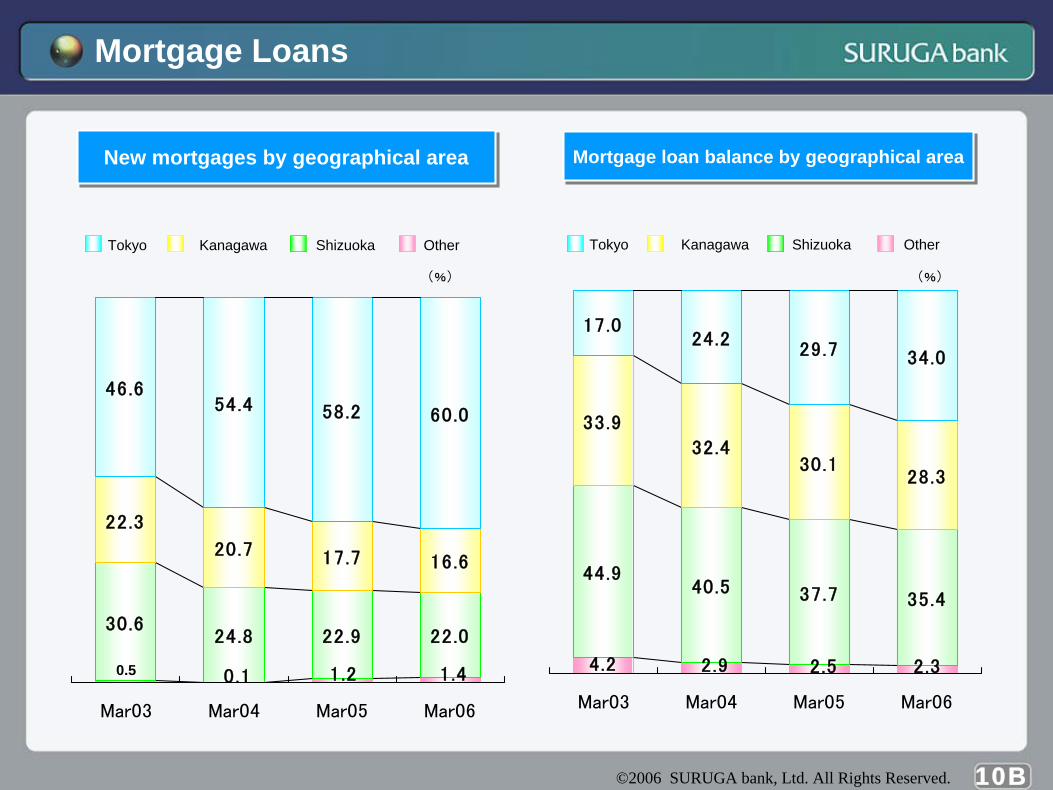

Mortgage Loans

Tokyo Kanagawa Shizuoka Other

2.32.52.94.2

44.940.5 37.7 35.4

28.330.1

32.4

33.9

34.029.724.2

17.0

Mar03 Mar04 Mar05 Mar06

Mortgage loan balance by geographical areaMortgage loan balance by geographical area

(%)

1.41.20.1

22.022.924.830.6

22.3

20.7 17.7 16.6

60.058.254.446.6

Mar03 Mar04 Mar05 Mar06

New mortgages by geographical areaNew mortgages by geographical area

0.5

Tokyo Kanagawa Shizuoka Other

(%)

©2006 SURUGA bank, Ltd. All Rights Reserved. 11A

Rates on New Mortgages/Mortgage Loans for Women

Mar03 Mar04 Mar05 Mar06

54.5

64.1

72.2

79.23,700

3,293

4,080

4,384

Balance (billion yen)

No. of borrowers

Mortgage loans for womenMortgage loans for women

Started in Aug 2000

2.01.10.30.3

14.715.416.317.1

26.328.030.032.1

12.713.314.014.1

23.022.822.5

21.3

16.614.9

12.3

10.6

4.4

4.2

4.2

4.2

0.3

0.4

0.4

0.3

Mar03 Mar04 Mar05 Mar06

5.0% or higher

4.5% to under 5.0%4.0% to under 4.5%

3.5% to under 4.0%

3.0% to under 3.5%2.5% to under 3.0%

2.0% to under 2.5%Under 2.0%

(%)

Distribution of new mortgage rates (cumulative)

Distribution of new mortgage rates (cumulative)

Based on number of new mortgages

©2006 SURUGA bank, Ltd. All Rights Reserved. 11B

Family Value Chain Loan

0.5

1.1

1.7

3.3

192

107

68

30

1.1

3.2

5.4

8.8

328

211

123

46

Sep05 Mar06Mar05Dec04

Balanced packageBalanced package Parent-help loanParent-help loan

Jun05 Sep05 Dec05 Mar06

from Mar 2005from Oct 2004

Balance (billion yen) Balance (billion yen)

● No. of loans● No. of loans

©2006 SURUGA bank, Ltd. All Rights Reserved. 12A

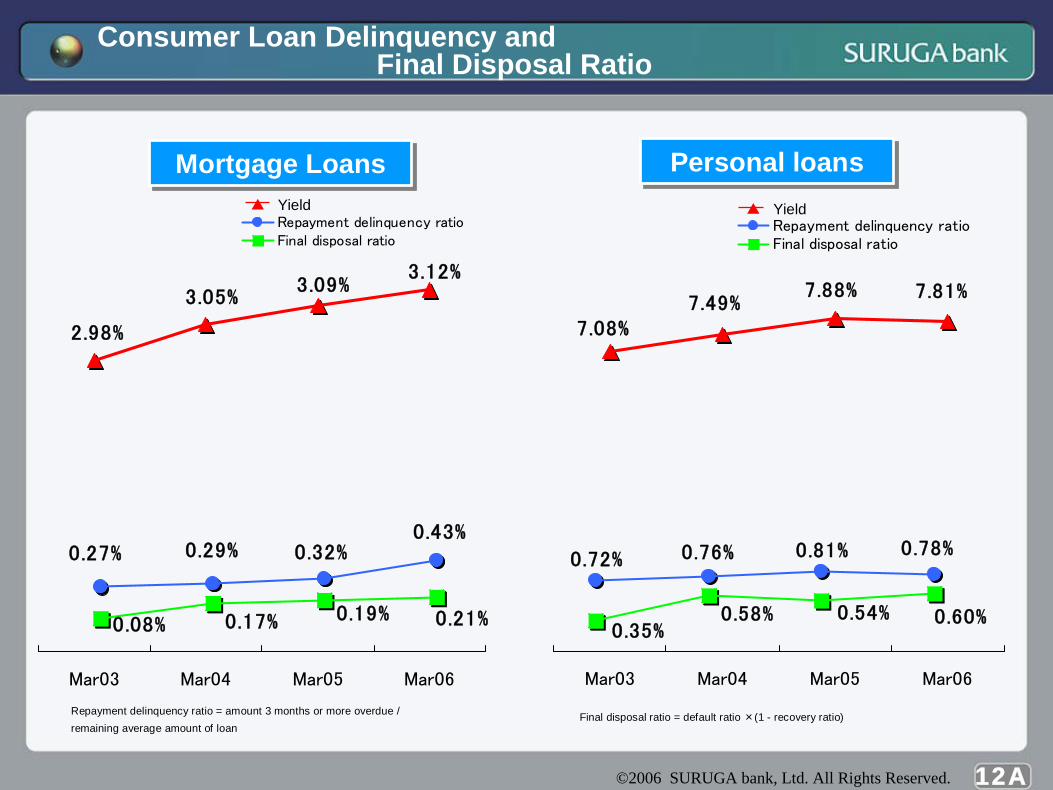

Consumer Loan Delinquency andFinal Disposal Ratio

0.27% 0.29% 0.32%0.43%

0.21%0.19%0.17%0.08%

Repayment delinquency ratioFinal disposal ratio

0.72% 0.76% 0.81% 0.78%

0.35%0.58% 0.54% 0.60%

Repayment delinquency ratioFinal disposal ratio

7.08%7.49%

7.88% 7.81%

Mar03 Mar04 Mar05 Mar06

Personal loansPersonal loansMortgage LoansMortgage Loans

2.98%

3.05%3.09%

3.12%

Mar03 Mar04 Mar05 Mar06

Repayment delinquency ratio = amount 3 months or more overdue /remaining average amount of loan

Final disposal ratio = default ratio ×(1 - recovery ratio)

▲ Yield▲ Yield

©2006 SURUGA bank, Ltd. All Rights Reserved.

2.7%

4.3%

6.7%

10.1%

12B

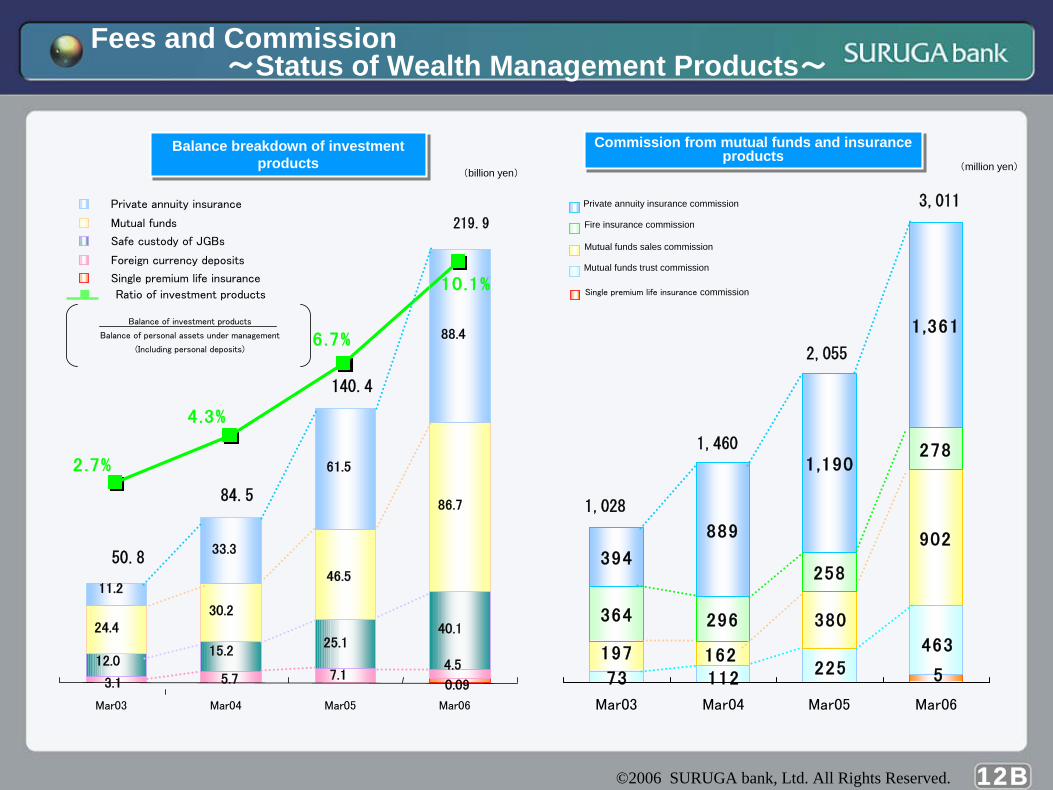

Fees and Commission~Status of Wealth Management Products~

■ Ratio of investment products

Single premium life insurance

4.5

0.097.15.73.1

25.140.1

15.212.0

24.430.2

46.5

86.7

61.5

88.4

11.2

33.3

Mar03 Mar04 Mar05 Mar06

Private annuity insurance

Mutual funds

Safe custody of JGBs

Foreign currency deposits

5

463225

73 112

902

380

162197

278

258

296364

1,361

1,190

889

394

Mar03 Mar04 Mar05 Mar06

1,460

2,055

84.5

140.4

Commission from mutual funds and insurance products

Commission from mutual funds and insurance productsBalance breakdown of investment

productsBalance breakdown of investment

products

219.9

50.8

1,028

3,011Private annuity insurance commission

Fire insurance commission

Mutual funds sales commission

Mutual funds trust commission

(million yen)(billion yen)

Balance of investment products

Balance of personal assets under management

(Including personal deposits)

Single premium life insurance commission

©2006 SURUGA bank, Ltd. All Rights Reserved. 13A

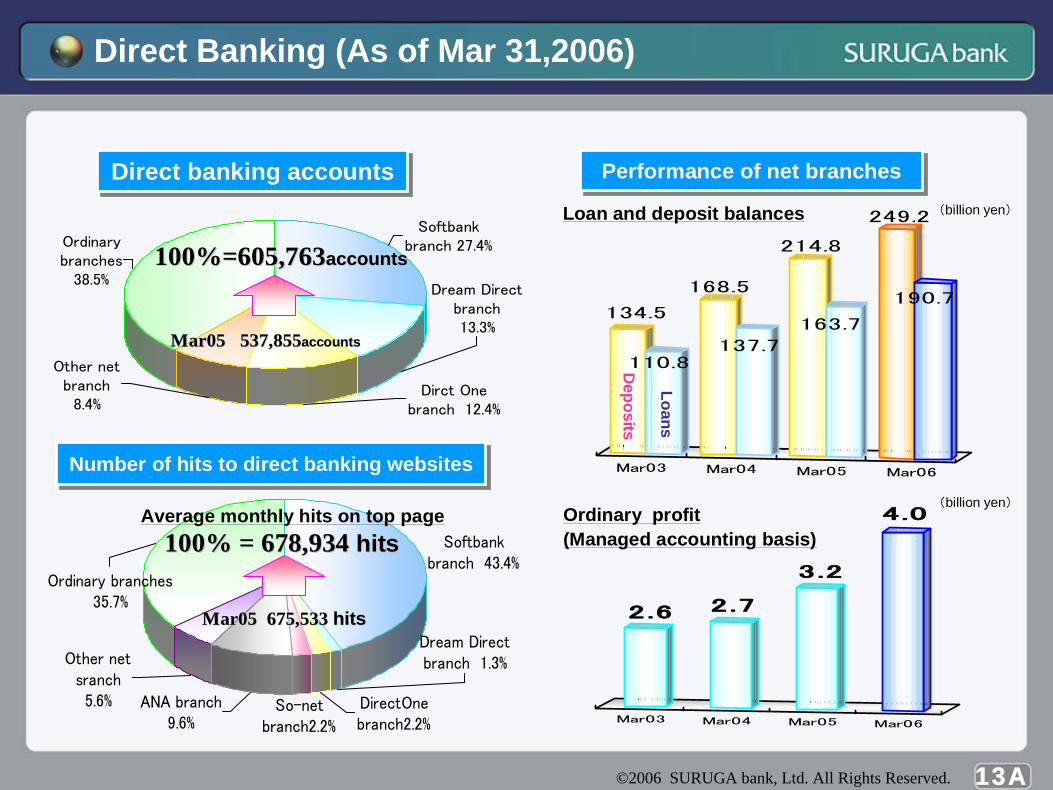

Direct Banking (As of Mar 31,2006)

Mar03 Mar04 Mar05 Mar06

134.5

110.8

168.5

137.7

214.8

163.7

249.2

190.7

Mar03 Mar04 Mar05 Mar06

2.6 2.7

3.2

4.0

Other netbranch

8.4%Dirct One

branch 12.4%

Softbankbranch 27.4%

Dream Directbranch13.3%

Ordinarybranches

38.5%

Ordinary branches35.7%

So-netbranch2.2%

ANA branch9.6%

Other netsranch5.6%

Dream Directbranch 1.3%

DirectOnebranch2.2%

Softbankbranch 43.4%

Direct banking accountsDirect banking accounts

100%=605,763100%=605,763accountsaccounts

Mar05 537,855Mar05 537,855accountsaccounts

100% = 678,934 100% = 678,934 hitshits

Mar05 675,533 Mar05 675,533 hitshits

Performance of net branchesPerformance of net branches

Loans

Deposits

(billion yen)

(billion yen)

Loan and deposit balances

Ordinary profit (Managed accounting basis)

Number of hits to direct banking websitesNumber of hits to direct banking websites

Average monthly hits on top page

©2006 SURUGA bank, Ltd. All Rights Reserved. 13B

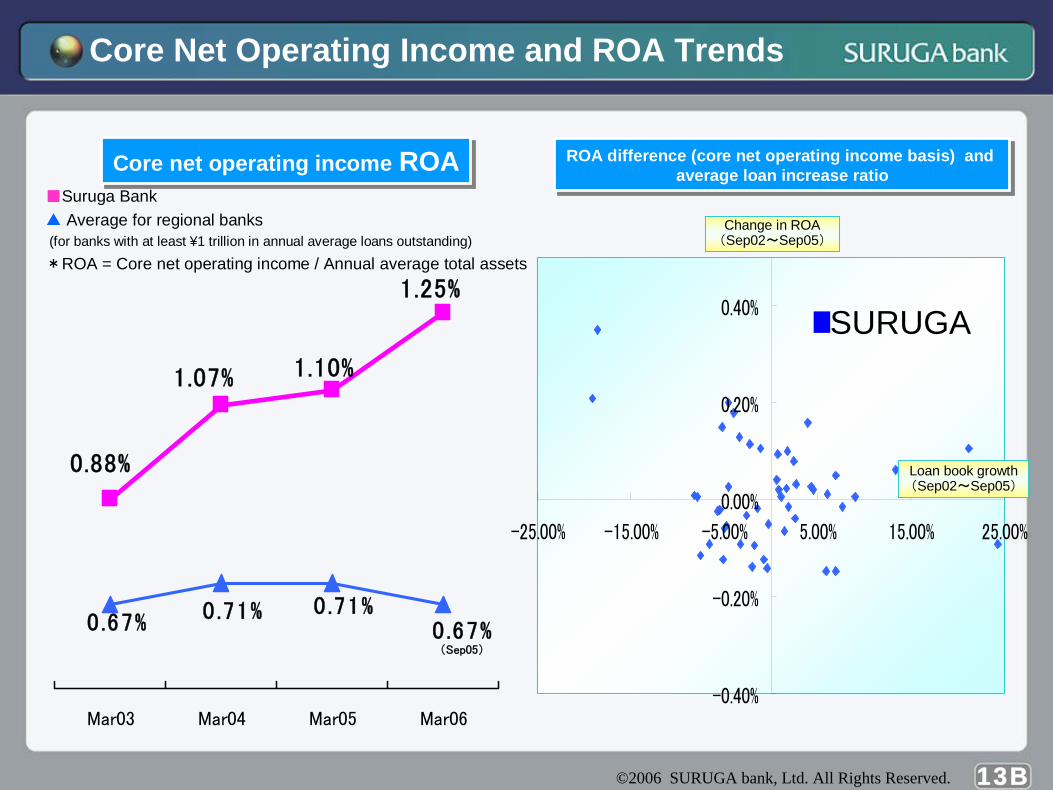

Core Net Operating Income and ROA Trends

1.25%

1.07% 1.10%

0.88%

0.67% 0.71%0.67%

0.71%

Mar03 Mar04 Mar05 Mar06

ROA difference (core net operating income basis) and average loan increase ratio

ROA difference (core net operating income basis) and average loan increase ratioCore net operating income ROACore net operating income ROA

-0.40%

-0.20%

0.00%

0.20%

0.40%

-25.00% -15.00% -5.00% 5.00% 15.00% 25.00%

(Sep05)

SURUGA

Loan book growth(Sep02~Sep05)

Change in ROA(Sep02~Sep05)

■Suruga Bank▲ Average for regional banks(for banks with at least ¥1 trillion in annual average loans outstanding)

*ROA = Core net operating income / Annual average total assets

©2006 SURUGA bank, Ltd. All Rights Reserved.

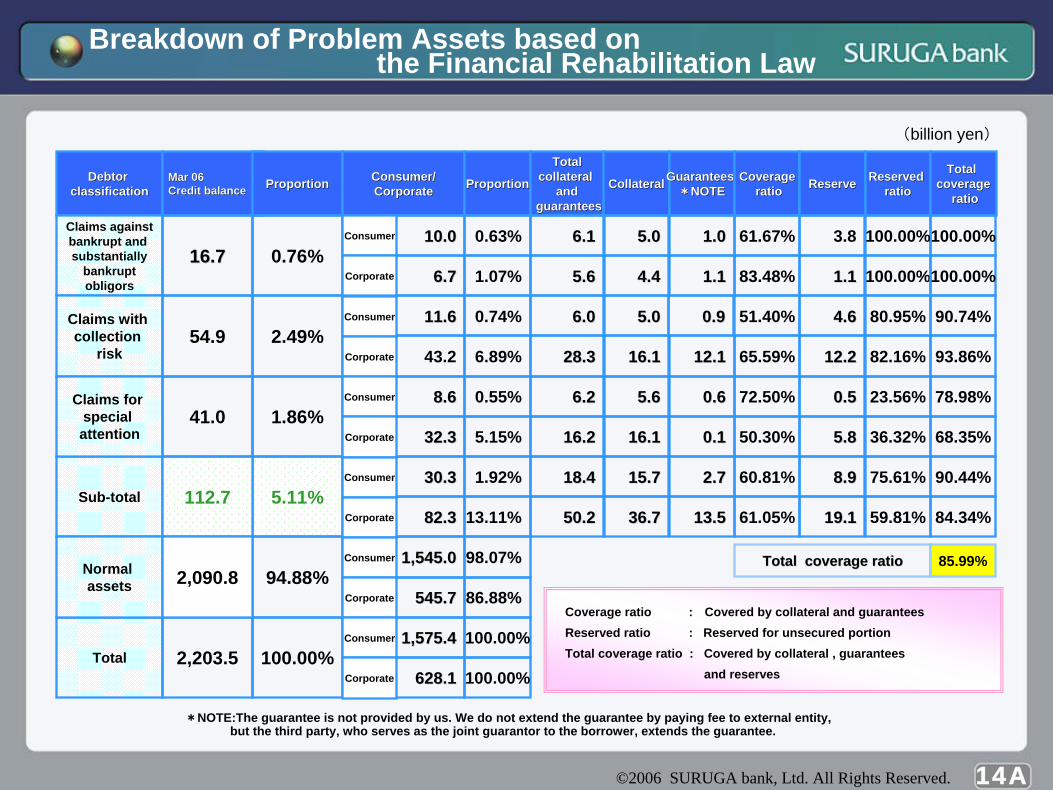

Breakdown of Problem Assets based on the Financial Rehabilitation Law

100.00%Total 2,203.5

Debtor Debtor classificationclassification

Mar 06Mar 06Credit balanceCredit balance ProportionProportion Consumer/Consumer/

CorporateCorporate ProportionProportion

TotalTotalcollateral collateral

andandguaranteesguarantees

CollateralCollateral Guarantees Guarantees **NOTENOTE

CoverageCoverageratioratio ReserveReserve Reserved Reserved

ratioratio

Total Total coveragecoverage

ratioratio

30.330.3 1.92% 18.418.4 15.715.7 2.72.7 60.81%

82.382.3 13.11% 50.250.2 36.736.7 13.513.5 61.05%

1,545.01,545.0 98.07%

545.7545.7 86.88%

1,575.41,575.4 100.00%

5.11%

94.88%

628.1628.1 100.00%

Sub-total 112.7

Normal assets 2,090.8

8.98.9

19.119.1

75.61%

59.81%

90.44%

84.34%

Claims againstbankrupt and substantially

bankrupt obligors

16.716.7 0.76%0.63% 6.16.1 5.05.0 1.01.0 61.67%

1.07% 5.65.6 4.44.4 1.11.1 83.48%

3.8

1.11.1 100.00%

100.00%

100.00%

11.611.6 0.74% 6.06.0 5.05.0 51.40%

43.2 6.89% 28.328.3 16.116.1 12.112.1 65.59%

8.68.6 0.55% 6.26.2 5.65.6 0.60.6 72.50%

32.332.3 5.15% 16.216.2 16.116.1 0.10.1 50.30%

2.49%

1.86%

Claims with collection

risk54.9

Claims for special attention

41.0

4.64.6

12.212.2

0.50.5

5.85.8

80.95%

82.16%

23.56%

36.32%

90.74%

93.86%

78.98%

68.35%

6.76.7

10.010.0

0.90.9

85.99%

100.00%

Coverage ratio : Covered by collateral and guaranteesReserved ratio : Reserved for unsecured portionTotal coverage ratio : Covered by collateral , guarantees

and reserves

Total coverage ratioTotal coverage ratio

(billion yen)

*NOTE:The guarantee is not provided by us. We do not extend the guarantee by paying fee to external entity,but the third party, who serves as the joint guarantor to the borrower, extends the guarantee.

Consumer

Corporate

Consumer

Corporate

Consumer

Corporate

Consumer

Corporate

Consumer

Corporate

Consumer

Corporate

14A

©2006 SURUGA bank, Ltd. All Rights Reserved. 14B

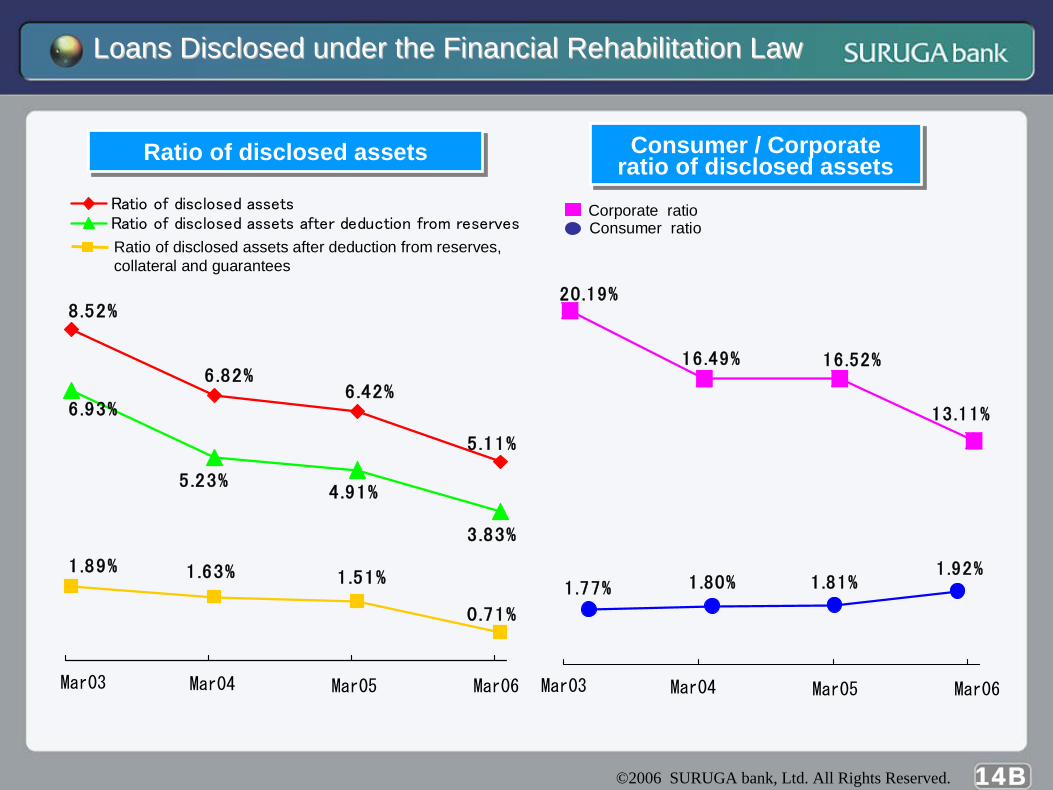

Loans Disclosed under the Financial Rehabilitation LawLoans Disclosed under the Financial Rehabilitation Law

13.11%

16.52%16.49%

20.19%

1.81%1.80%1.92%

1.77%

5.11%

6.42%6.82%

8.52%

1.89%

0.71%

1.63% 1.51%

3.83%

6.93%

5.23%4.91%

Ratio of disclosed assetsRatio of disclosed assets after deduction from reserves

Ratio of disclosed assetsRatio of disclosed assets Consumer / Corporate ratio of disclosed assetsConsumer / Corporate

ratio of disclosed assets

Mar03 Mar04 Mar05 Mar06

Ratio of disclosed assets after deduction from reserves,collateral and guarantees

Mar03 Mar04 Mar05 Mar06

Corporate ratioConsumer ratio

©2006 SURUGA bank, Ltd. All Rights Reserved. 15A

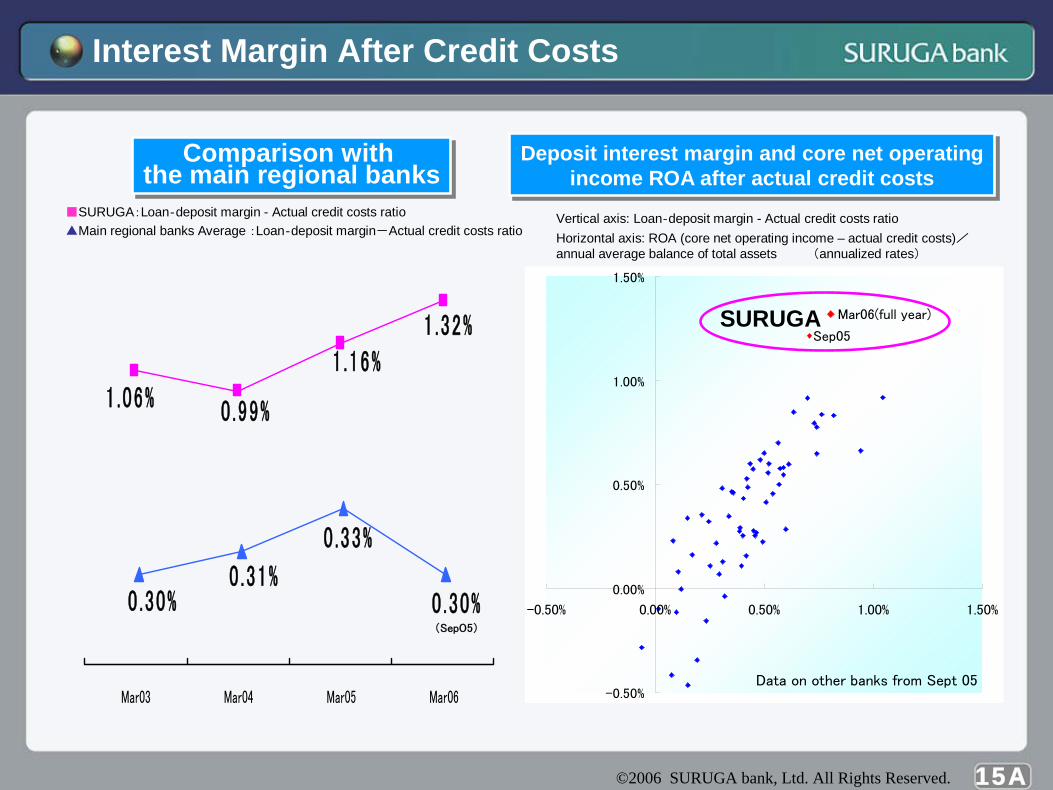

Interest Margin After Credit Costs

-0.50%

0.00%

0.50%

1.00%

1.50%

-0.50% 0.00% 0.50% 1.00% 1.50%

1 .32%

0 .99%

1 .16%1 .06%

Mar03 Mar04 Mar05 Mar06

0 .30%0 .31%

0 .30%

0 .33%

(Sep05)

Sep05

Comparison with the main regional banks

Comparison with the main regional banks

■SURUGA:Loan‐deposit margin - Actual credit costs ratio▲Main regional banks Average :Loan‐deposit margin-Actual credit costs ratio

SURUGA

Deposit interest margin and core net operating income ROA after actual credit costs

Deposit interest margin and core net operating income ROA after actual credit costs

Vertical axis: Loan‐deposit margin - Actual credit costs ratioHorizontal axis: ROA (core net operating income – actual credit costs)/annual average balance of total assets (annualized rates)

Data on other banks from Sept 05

Mar06(full year)

©2006 SURUGA bank, Ltd. All Rights Reserved. 15B

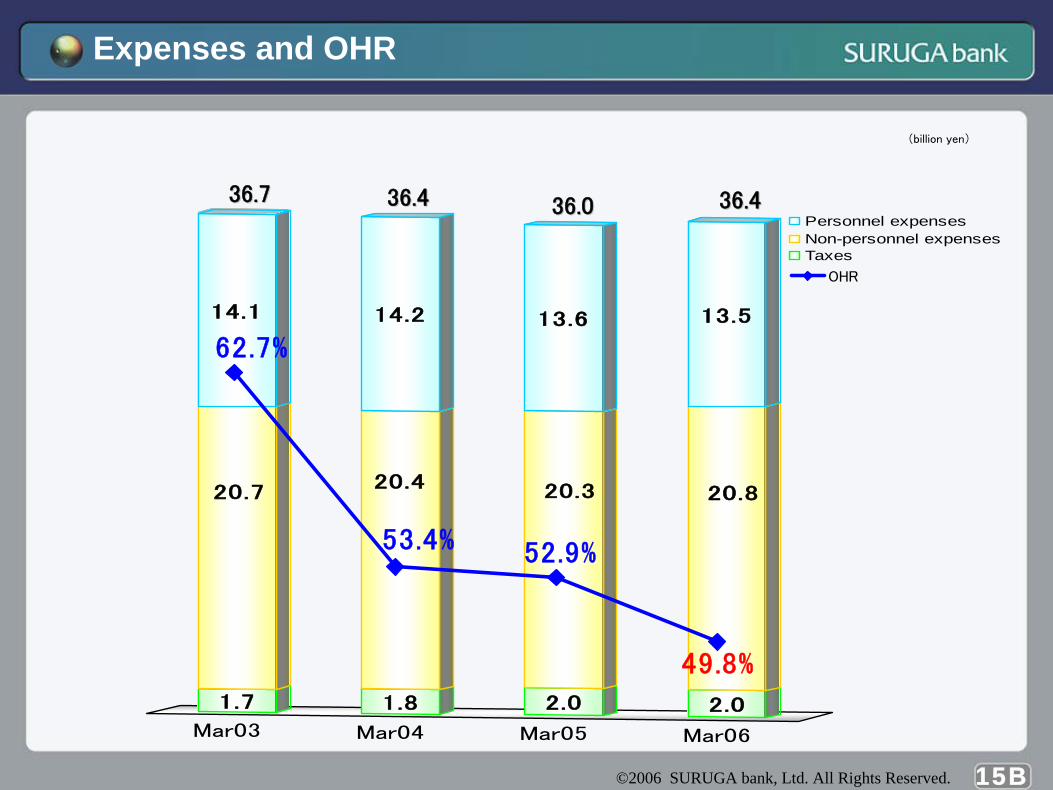

Expenses and OHR

Mar03 Mar04 Mar05 Mar06

1.7

20.7

14.1

1.8

20.4

14.2

2.0

20.3

13.6

2.0

20.8

13.5

Personnel expensesNon-personnel expensesTaxes

49.8%

52.9%53.4%

62.7%

OHR

36.736.7 36.436.4 36.036.0 36.436.4

(billion yen)

©2006 SURUGA bank, Ltd. All Rights Reserved. 16A

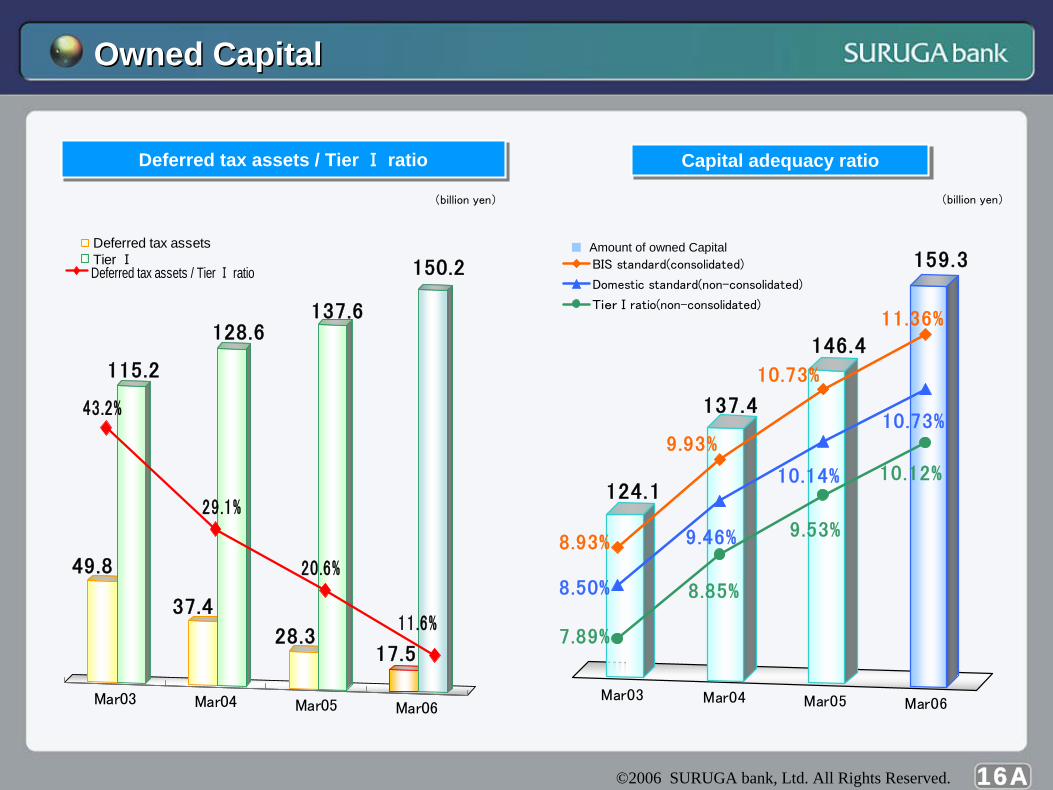

Owned CapitalOwned Capital

Mar03 Mar04 Mar05 Mar06

49.8

115.2

37.4

128.6

28.3

137.6

17.5

150.2Deferred tax assets Tier Ⅰ

43.2%

29.1%

20.6%

11.6%

Deferred tax assets / Tier Ⅰ ratio

Mar03 Mar04 Mar05 Mar06

124.1

137.4

146.4

159.3

Capital adequacy ratioCapital adequacy ratio

8.93%

9.93%

10.73%

11.36%

10.73%

10.14%

9.46%

8.50%

10.12%

7.89%

9.53%

8.85%

BIS standard(consolidated)

Domestic standard(non-consolidated)

TierⅠratio(non-consolidated)

Deferred tax assets / Tier Ⅰ ratioDeferred tax assets / Tier Ⅰ ratio

(billion yen)

■ Amount of owned Capital

(billion yen)

©2006 SURUGA bank, Ltd. All Rights Reserved.

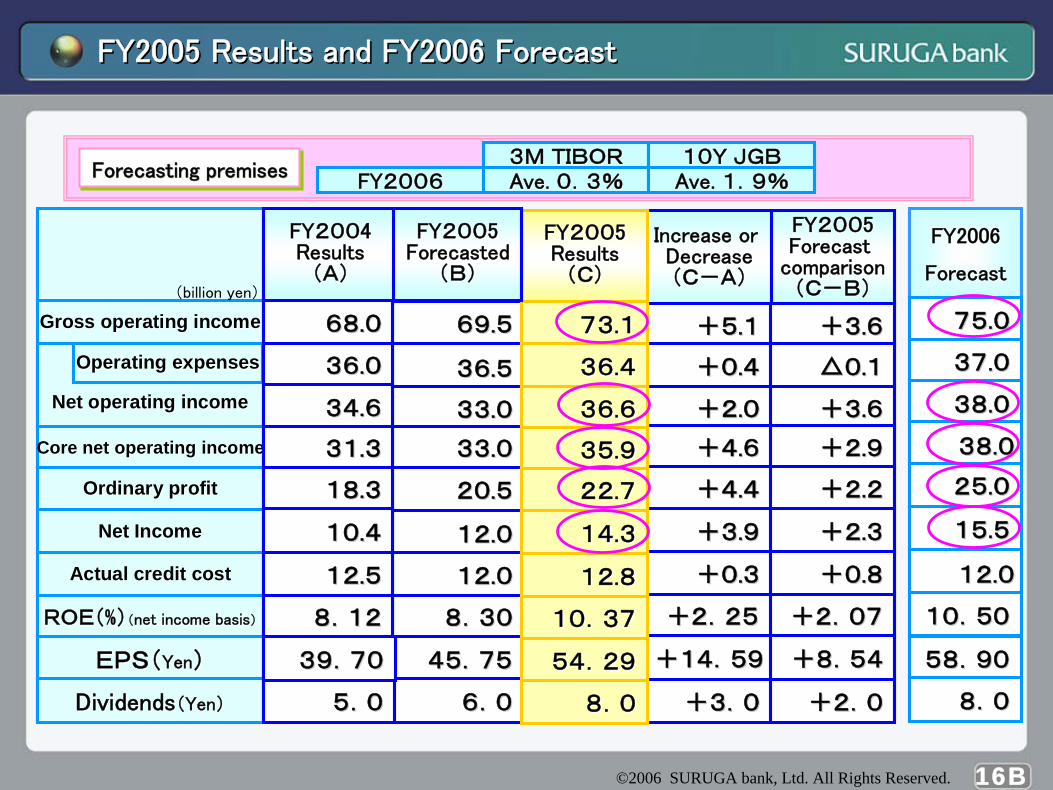

FY2005 Results and FY2006 ForecastFY2005 Results and FY2006 Forecast

FYFY20020055Forecast Forecast

comparisoncomparison(C-B)(C-B)

3M3M TIBORTIBOR 10Y10Y JGBJGBFYFY20062006 Ave. Ave. 0.3%0.3% Ave. Ave. 1.9%1.9%

Net operating incomeNet operating income

Operating expensesOperating expenses

Increase or Increase or DecreaseDecrease(C-A)(C-A)

6969..55

3636..55

3333..00

+5+5..11

+0+0..44

+2+2..00

3636..00

3434..66

+3+3..66

△△00..11

+3+3..66

ROE(ROE(%%))((net income basisnet income basis))

EPS(EPS(YenYen))

DividendsDividends((YenYen))

8.308.30

45.7545.75

+2.25+2.25

+14.59+14.59

8.128.12 +2.07+2.07

+8.54+8.54

6.06.0 +3.0+3.0 +2.0+2.05.05.0

39.7039.70

Core net operating incomeCore net operating income 3333..00 +4+4..663131..33 +2+2..99

Ordinary profitOrdinary profit

Net IncomeNet Income

Actual credit costActual credit cost

2020..55

1212..00

1212..00

+4+4..44

+3+3..99

+0+0..33

1818..33

1010..44

1212..55

+2+2..22

+2+2..33

+0+0..88

FY2006FY2006

ForecastForecast

7575..00

3737..00

3838..00

10.5010.50

58.9058.90

8.08.0

2525..00

1515..55

1212..00

3838..00

Forecasting premisesForecasting premisesForecasting premises

FYFY20020055ResultsResults

(C)(C)

7373..11

3636..44

3636..66

10.3710.37

54.2954.29

8.08.0

3535..99

2222..77

1414..33

1212..88

Gross operating incomeGross operating income(billion yen)

6868..00

FYFY20020044ResultsResults

(A)(A)

FYFY20020055ForecastedForecasted

(B)(B)

16B

©2006 SURUGA bank, Ltd. All Rights Reserved.

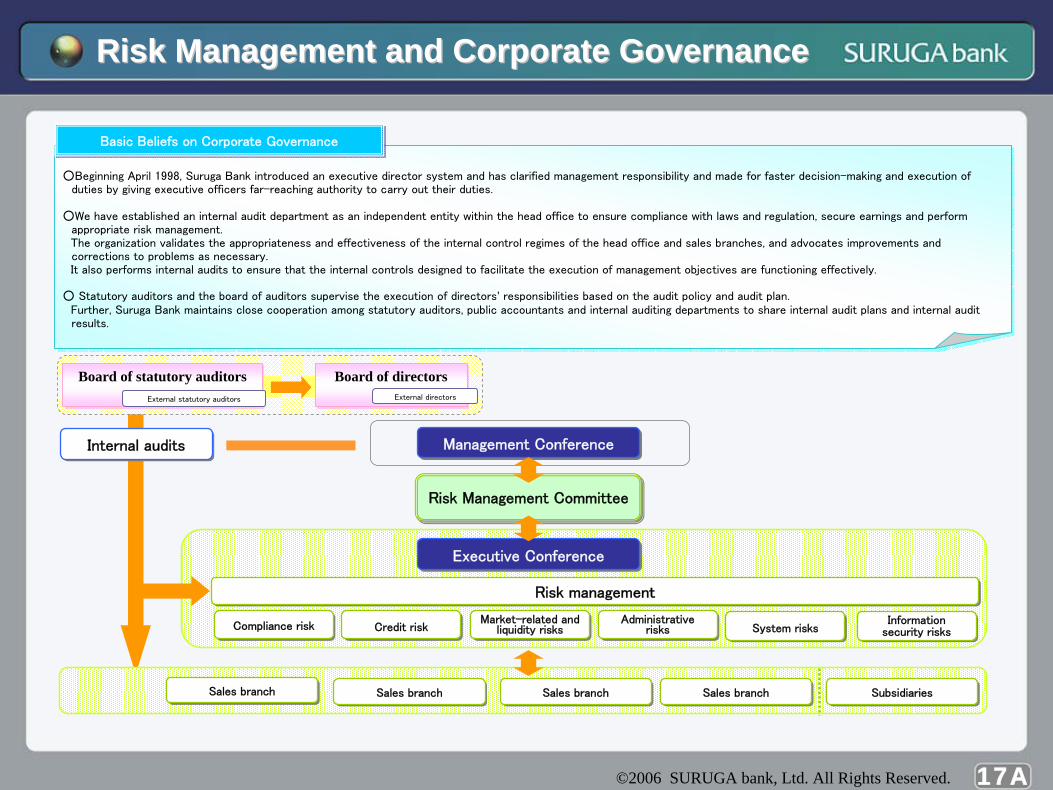

Risk Management and Corporate GovernanceRisk Management and Corporate Governance

17A

Board of directorsBoard of directorsBoard of statutory auditorsBoard of statutory auditorsExternal directorsExternal statutory auditors

Executive ConferenceExecutive Conference

Risk Management CommitteeRisk Management Committee

Risk managementRisk management

Management ConferenceManagement Conference

Market-related and liquidity risks

Market-related and liquidity risksCompliance riskCompliance risk System risksSystem risksCredit riskCredit risk Administrative

risksAdministrative

risks

SubsidiariesSubsidiariesSales branchSales branch Sales branchSales branch Sales branchSales branch Sales branchSales branch

Basic Beliefs on Corporate GovernanceBasic Beliefs on Corporate Governance

Internal auditsInternal audits

○Beginning April 1998, Suruga Bank introduced an executive director system and has clarified management responsibility and made for faster decision-making and execution of duties by giving executive officers far-reaching authority to carry out their duties.

○We have established an internal audit department as an independent entity within the head office to ensure compliance with laws and regulation, secure earnings and perform appropriate risk management.The organization validates the appropriateness and effectiveness of the internal control regimes of the head office and sales branches, and advocates improvements and corrections to problems as necessary.It also performs internal audits to ensure that the internal controls designed to facilitate the execution of management objectives are functioning effectively.

○ Statutory auditors and the board of auditors supervise the execution of directors’ responsibilities based on the audit policy and audit plan.Further, Suruga Bank maintains close cooperation among statutory auditors, public accountants and internal auditing departments to share internal audit plans and internal audit results.

Information security risksInformation

security risks

©2006 SURUGA bank, Ltd. All Rights Reserved. 17B

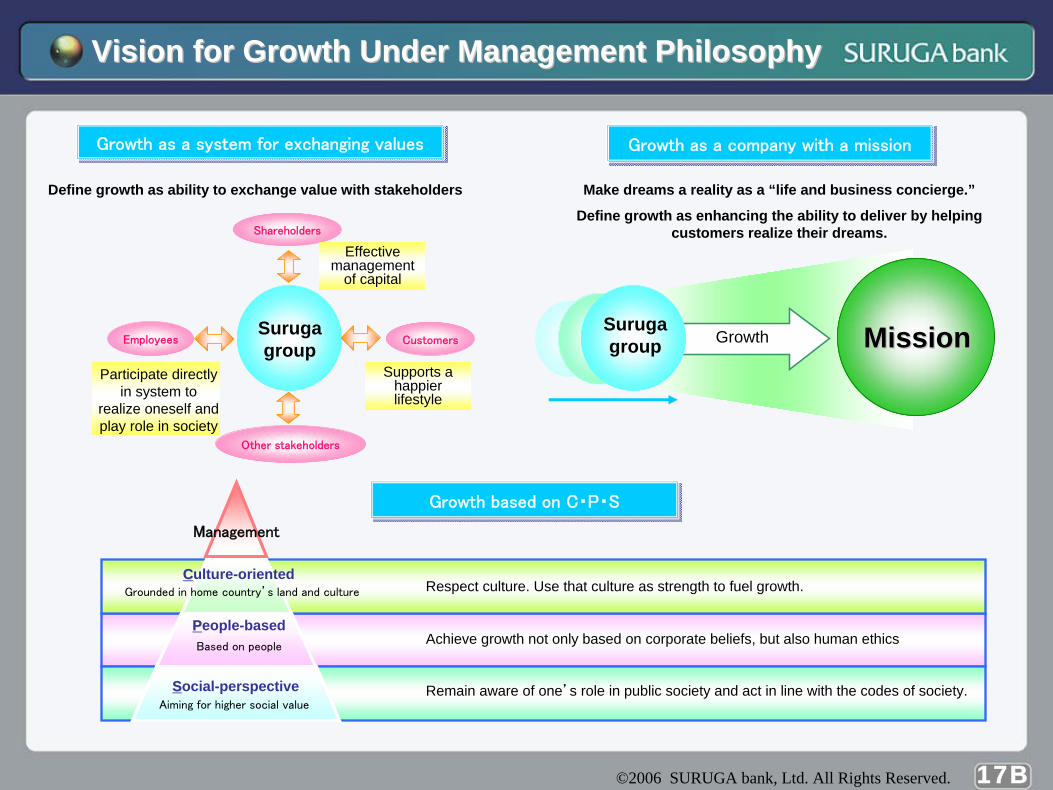

Vision for Growth Under Management PhilosophyVision for Growth Under Management Philosophy

Growth as a system for exchanging valuesGrowth as a system for exchanging values Growth as a company with a missionGrowth as a company with a mission

Growth based on C・P・SGrowth based on C・P・S

Shareholders

Other stakeholders

CustomersEmployees

Effective management

of capital

Supports a happier lifestyle

Participate directly in system to

realize oneself and play role in society

Define growth as ability to exchange value with stakeholders

Growth MissionMission

Make dreams a reality as a “life and business concierge.”

Define growth as enhancing the ability to deliver by helping customers realize their dreams.

Management

Grounded in home country’s land and culture

Based on people

Aiming for higher social value

CCulture-oriented

PPeople-based

SSocial-perspective

Respect culture. Use that culture as strength to fuel growth.

Achieve growth not only based on corporate beliefs, but also human ethics

Remain aware of one’s role in public society and act in line with the codes of society.

Suruga group

Suruga group

For further details regarding the above, please contact

IR & PR Office, Suruga Bank Tel: +81-3-3279-5536

e-mail: [email protected]