merrill lynch final -...

TRANSCRIPT

1

Douglas R. Wilburne Vice President, Investor Relations

Merrill Lynch 9th Annual Global Industries

May 9, 2007

Building and Growing

2

Forward-Looking Information

Certain statements in today’s discussion will be forward-looking statements, including those that discuss strategies, goals, outlook or other non-historical matters; or project revenues, income, returns or other financial measures. These forward-looking statements speak only as of the date on which they are made, and we undertake no obligation to update or revise any forward-looking statements.

These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materiallyfrom those contained in the statements, including the risks and uncertainties set forth under our full disclosure located at theend of this presentation.

3

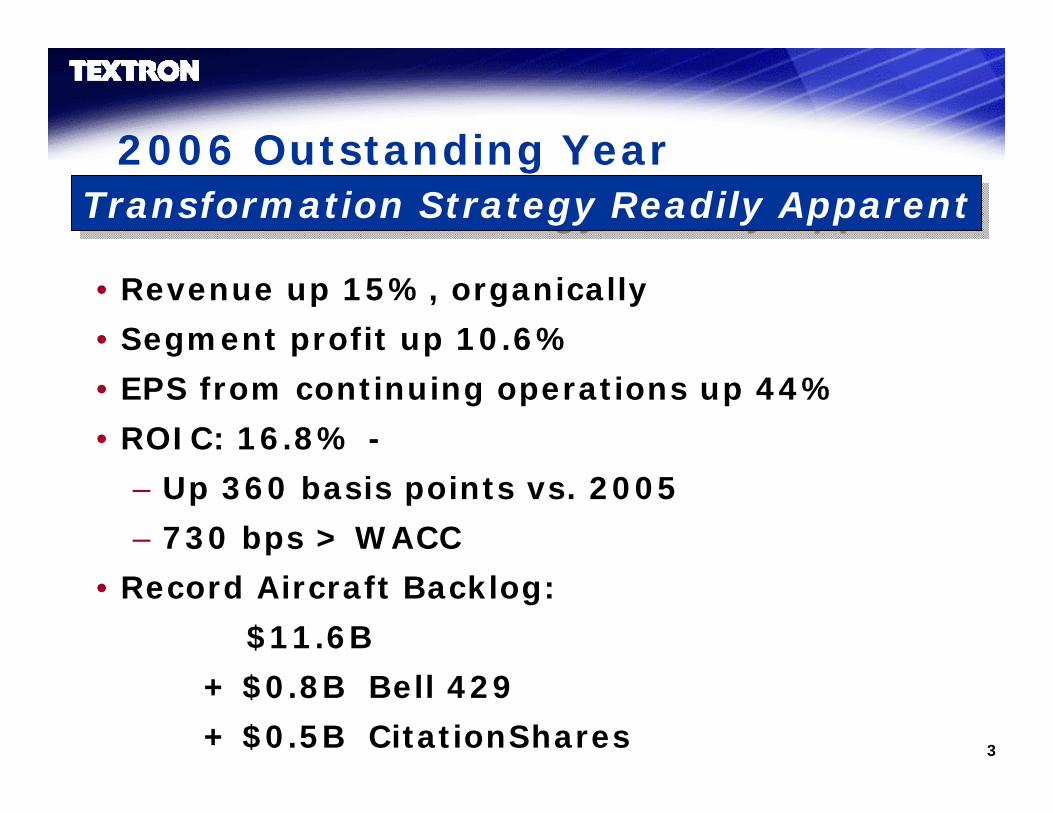

2006 Outstanding YearTransformation Strategy Readily ApparentTransformation Strategy Readily Apparent

• Revenue up 15%, organically

• Segment profit up 10.6%

• EPS from continuing operations up 44%

• ROIC: 16.8% -

– Up 360 basis points vs. 2005

– 730 bps > WACC

• Record Aircraft Backlog:

$11.6B

+ $0.8B Bell 429

+ $0.5B CitationShares

4

Q1 2007 Outstanding Quarter

Transformation Momentum ContinuesTransformation Momentum Continues

• Revenue up 12.6%

• Segment profit up 26.1%

• Manufacturing margins up 150 bps

• EPS from continuing operations up 30%

• Record Aircraft Backlog:

$12.9B

+ $0.8B Bell 429

+ $0.5B CitationShares

5

Transforming Textron Our Ongoing Journey to Premier

A Simpler, More Focused Portfolio of Leading, Branded Businesses in

Attractive Industries

A Simpler, More Focused Portfolio of Leading, Branded Businesses in

Attractive Industries

NETWORKED ENTERPRISE

EnterpriseManagementEnterprise

ManagementHow We Manage

What We Own

PortfolioManagement

PortfolioManagement

WhatWe Own

VISION:To be the premier multi-industry company, recognized for

our network of powerful brands, world-class enterprise processes and talented people

VISION:To be the premier multi-industry company, recognized for

our network of powerful brands, world-class enterprise processes and talented people

6

Textron Financial

Cessna

2006 Revenue: $11.5 Billion2006 Revenue: $11.5 Billion2010 Revenue: $15 2010 Revenue: $15 -- $17 Billion$17 Billion

CessnaCessna

36%

IndustrialIndustrial

E-Z-GO

Fluid & Power

Greenlee

Jacobsen

Kautex

27%

FinanceFinance7%

BellBell

Bell Helicopter

Textron Systems

30%

Textron –Leading Branded Businesses &Attractive Growth Markets

7

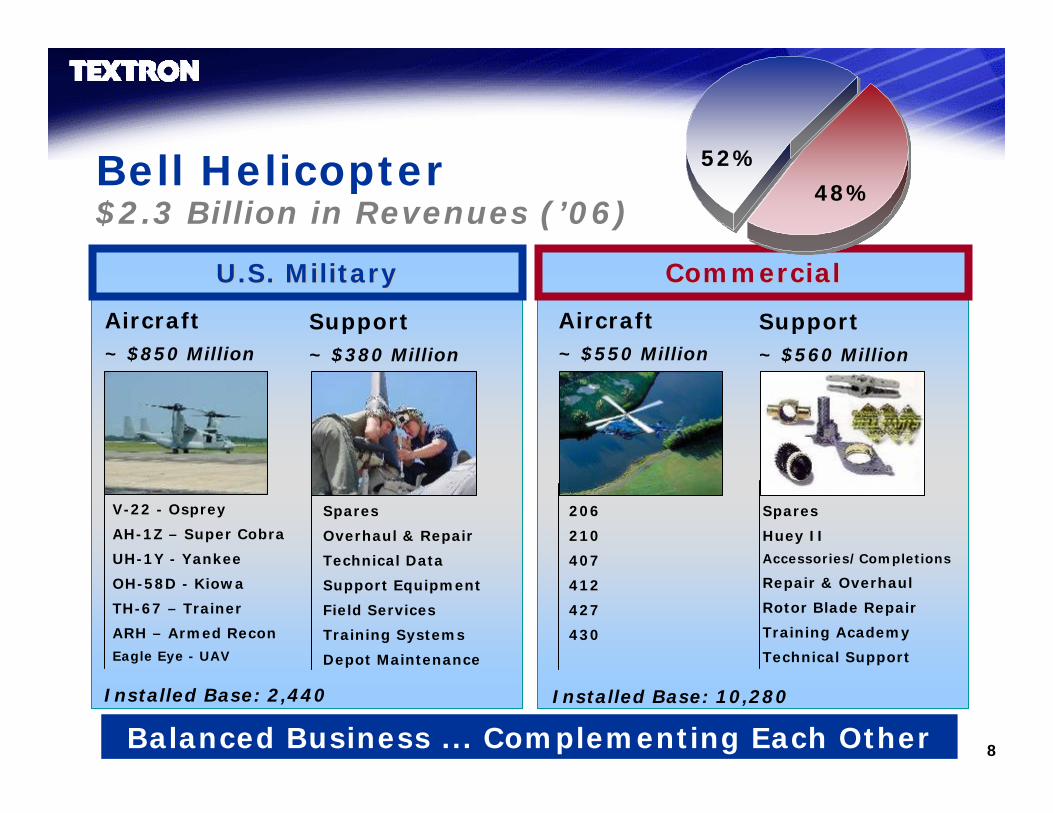

Bell Segment$3.4 Billion in Revenues (’06)

Bell Helicopter

Textron Systems

68% 32%

8

Spares

Overhaul & Repair

Technical Data

Support Equipment

Field Services

Training Systems

Depot Maintenance

Bell Helicopter$2.3 Billion in Revenues (’06)

Aircraft~ $850 Million

V-22 - Osprey

AH-1Z – Super Cobra

UH-1Y - Yankee

OH-58D - Kiowa

TH-67 – Trainer

ARH – Armed Recon

Eagle Eye - UAV

206

210

407

412

427

430

Support~ $380 Million

Spares

Huey II

Accessories/Completions

Repair & Overhaul

Rotor Blade Repair

Training Academy

Technical Support

U.S. MilitaryU.S. Military

Installed Base: 2,440 Installed Base: 10,280

Aircraft~ $550 Million

Support~ $560 Million

CommercialCommercial

52%

48%

52%

48%

Balanced Business ... Complementing Each Other

9

Aircraft

609

412407

206B3/L4

429427

430

210

Support

SparesRepair &OverhaulAircraft CompletionsRefurbishmentTraining SystemsField ServicesTechnical DataSupport Equipment

Commercial Business

Commercial Business Growing

Installed Base: 10,280

10

New Introduction from Bell

• “First-ever” Technologies from Bell’s Modular Affordable Product Line (MAPL)

– Unprecedented Cabin and Cockpit Features

– New High Performance Rotor Technology

• First Delivery – 2008/2009

Bell 429 Global Ranger Light Twin

Over 185 Orders

11

30

55

80

105

130

155

180

2002 2003 2004 2005 2006 2007

Commercial Business Growing

Commercial DeliveriesCommercial Deliveries

159

~180

123

111

92

105

12

Rotorcraft Industry -Strong Growth Outlook

Global War On Terrorism • DOD Rotorcraft Spend Increasing From 4.8% To 6.4% Of Procurement

Budget: FY05 To FY11

• Flight Hours Have Increased 2-4x Previous Levels

• Rotorcraft Survivability Essential To DOD

Homeland SecurityIncreasing Border Protection: Domestic And International

Offshore/Utility Segments80% Of Fleet: 20 Years Or Older

Regulatory/Insurance/Safety Issues Driving Fleet Replacement

High Oil Prices Driving Offshore Exploration

EMS & National Disaster EffortsAsia Tsunami Disaster; Pakistan Earthquake Relief

Hurricane Katrina / Rita / Wilma

Growing International DemandAsia-Pacific Significant Opportunity

Industry Growth Continues Across the Board

13

Aircraft Support

SparesOverhaul & RepairTechnical DataSupport EquipmentField ServicesTraining SystemsDepot Maintenance

Installed Base: 2,440

V-22Osprey

AH-1Z/ UH-1YSuperCobra/Huey

OH-58DKiowa Warrior

TH-67Creek II

USCGEagle Eye

VH-71Marine One

Government Business

ARH-70ABell 407

USAFCSAR-X Potential

Government Business Growing

14

V-22 Program

360 AircraftCombat AssaultAssault SupportExternal Load

Operations

Marine Corps

50 AircraftSpecial Operations

Insertion/ExtractionWMD Warfare

Air Force

48 AircraftCombat SAR

Fleet LogisticsSpecial WarfareAerial Tanker

Navy

$19BProgram

Twice the Speed . . . Five Times the Range

Total program: 458 unitsTotal program: 458 unitsAdditional future demandAdditional future demand

15

UH-1Y100 Units

AH-1Z180 Units

H-1 Upgrade ProgramLow Cost/High Performance

• Delivered first 3 Aircraft Q1 2007

• Improving line productivity

• Operational evaluation, phase II

• Resolve helmet issue

• Achieve full-rate decision

$5.6BProgram

Critically important to customer

16

• Militarized Commercial Derivative Of 407• 368 Units + 144 in President’s Budget Proposal• Initial Delivery – Under Review• Significant Future Foreign Military Potential

Armed Reconnaissance Helicopter

Completed Critical Design ReviewCompleted Critical Design Review

17

13%36% 13%

Textron Systems2006 Revenues: $1.1 Billion

Product Performance Driving GrowthProduct Performance Driving Growth

Intelligent Battlefield Sys

Air Launched Weapons

Aircraft Products

Aircraft Engines

Precision Engagement

38%

Combat Vehicles

Marine Systems

Marine & Land

18

Armed Vehicles – High Growth Opportunity

• U.S. Army Armed Security Vehicle requirement:

– Total Program of Record: 2,850

– Current contract: 1,350

• Additional requirements:

– Air Force: 95

– Army Convoy Protection: 700

– Army Knight: 381

– MRAP?

– Foreign Military?

– Aftermarket Support?

• Current ’07 production plan: ~530

19

CaravanSingle EngineCitations 6%

15%

3%

Used Aircraft

Parts, Service& Other

3%6% CitationShares

67%

Continued Growth Expected

Cessna2006 Revenues: $4.2 Billion

20

Corporate Profits A Key Driver of Jet Demand

$B Units

Source: Global Insight, Cessna estimates

0

200

400

600

800

1,000

1,200

1,400

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 20080

200

400

600

800

1,000

1,200

1,400Real Corporate Profits (8 Q Shift)

Jet Shipments

21

New Products Drive GrowthCertified in 2004 - 2006

Citation CJ3$6.7M

Backlog: ~$950M

Citation CJ2+$5.7M

Backlog: ~$525M

Citation CJ1+$4.2M

Backlog: ~$230M

Citation Mustang$2.5M

Backlog: ~$750M

Citation XLS$11.6M

Backlog: ~$2.2B

Citation Sovereign$15.5M

Backlog: ~$2.1B Backlog: ~$150M

Citation Encore+$8.1M

22

Citation CJ4

• Fully integrated Collins Pro Line 21 avionics

• Advanced avionics diagnostic system

• New standard integrated cabin management system

• Newly engineered, moderately swept wing

• New Williams International FJ44-4A electronically controlled (FADEC) engines

• Over 120 orders as of Q1 2007

Upward Extension to the Single-pilot-certified Citation Family

$7.995 million

First Flight: 1H08

Deliveries: 1H10

23

Growth Drivers – Cessna• International Markets Expanding

• Current Demand:– 496 Orders in 2006

– 122 Orders in Q1 2007

– Sold out for 375 deliveries in ’07

– >400 orders for ’08 delivery

– $9.0B backlog + $0.5B CitationShares

– Order activity remains strong

48%

’06

41%35%35%19%

International Citation Orders’05 ’04’03’02

24

Aftermarket Services

10.4% CAGR10.4% CAGR

$0

$100

$200

$300

$400

$500

$600

$700

Reven

ues

(in

mil

lion

s)

1999 2000 2001 2002 2003 2004 2005 2006

25

Value Drivers – Cessna Segment•Leveraging demand through operational

excellence

•Productivity strides

•Lean (e.g. combined CJ production line)

Combined CJ1+, CJ2+ and CJ3 Production Line

26

15.5%

8.4%

10.7%

13.1%

9.3%

10.5%11.1%

11.8%

7%8%9%

10%11%12%13%14%15%16%

'99 '00 '01 '02 '03 '04 '05 '06 '07E

NO

P M

argi

n

150

200

250

300

350

400

Unit D

eliveries

Jet Deliveries

49%33%17%13%23%22%19%14%ROIC 49%33%17%13%23%22%19%14%ROIC

~16%

Cessna Jet Deliveries and MarginsLeveraging Top Line Growth

~50%

27

Industrial

Revenues (Revenues (’’06)06)$3.1 Billion$3.1 Billion

E-Z-GO~$395 million

Fluid & Power~$520 million

Greenlee~$375 million

Jacobsen~$300 million

Kautex~$1.5 billion

Low-Mid Single Digit Organic GrowthContinual Margin Improvement

28

Value Drivers - Industrial Segment

• Steady operational improvements across the segment

• Lean implementation continuing

• Good growth; China expansion

• Significant new product introductions

29

Liquidating

Textron Financial Corporation2006 Managed Finance Receivables: $10.2B

Asset-BasedLending

8%

DistributionFinance

AviationFinance

Golf Finance

ResortFinance

StructuredCapital

19% 15%

13% 7%Non-Core1%

Growing ~10%/Year

37%

(% of Managed Finance Receivables as of 12/31/06)

30

Textron Financial Corporation

• Strategic to aircraft, golf & turf

• Excellent core business

– Good growth

– Strength in underwriting

• Leveraging assets and capabilities

31

Textron - Strong Organic GrowthInvesting in ER&D and CAPEX to SupportAbove-Average Growth

2005 - 2009 Investments -• Engineering,

Research & Development:

$2.2 Billion

• CAPEX: $2.0 Billion

Creating Value

32

$11.0

$13.0

$15.0

$17.0

2006 2007 2008 2009 2010

Strong Organic GrowthInvesting in ER&D and CAPEX to SupportAbove-Average Growth

10% CAGR – Optimistic

7% CAGR – Probable

$, Billions

33

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009(15.00)

5.00

25.00

45.00

65.00

85.00

105.00

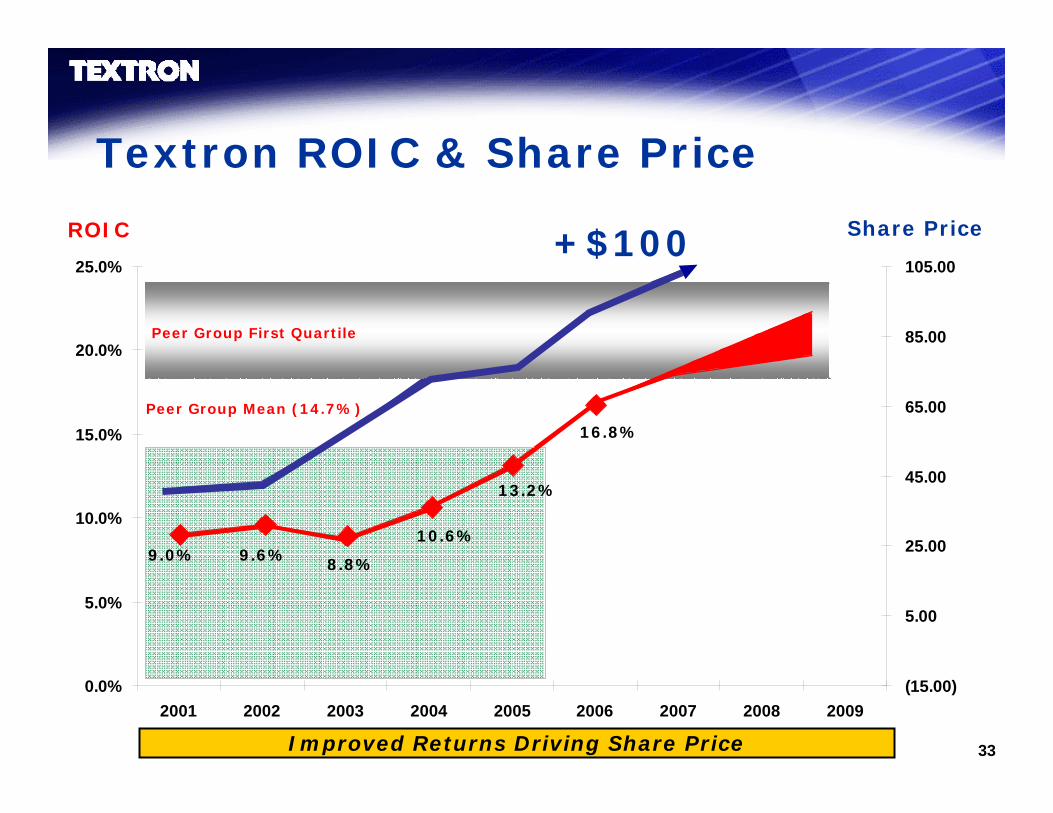

13.2%

8.8%

10.6%9.6%9.0%

Peer Group First Quartile

Textron ROIC & Share Price

Improved Returns Driving Share Price

Peer Group Mean (14.7%)

16.8%

ROIC Share Price+$100

34

Textron Transformation Strategy Driving & Leveraging Growth

•Strong organic growth

•Double digit earnings growth

•Expanding ROIC

•Premier growth of shareholder value

EliminateWaste

ReduceVariability

Grow & Innovate

35

Forward Looking InformationForward-looking Information: Certain statements in this report and other oral and written statements made by Textron from time to time are forward-looking statements, including those that discuss strategies, goals, outlook or other non-historical matters; or project revenues, income, returns or other financial measures. These forward-looking statements speak only as of the date on which they are made, and we undertake no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements, including the following: [a] changes in worldwide economic and political conditions that impact demand for our products, interest rates and foreign exchange rates; [b] the interruption of production at Textron facilities or Textron’s customers or suppliers; [c] Textron's ability to perform as anticipated and to control costs under contracts with the U.S. Government; [d] the U.S. Government's ability to unilaterally modify or terminate its contracts with Textron for the Government's convenience or for Textron's failure to perform, to change applicable procurement and accounting policies, and, under certain circumstances, to suspend or debar Textron as a contractor eligible to receive future contract awards; [e] changes in national or international funding priorities and government policies on the export and import of military and commercial products; [f] the ability to control costs and successful implementation of various cost reduction programs; [g] the timing of new product launches and certifications of new aircraft products; [h] the occurrence of slowdowns or downturns in customer markets in which Textron products are sold or supplied or where Textron Financial offers financing; [i] changes in aircraft delivery schedules or cancellation of orders; [j] the impact of changes in tax legislation; [k] the extent to which Textron is able to pass raw material price increases through to customers or offset such price increases by reducing other costs; [l] Textron’s ability to offset, through cost reductions, pricing pressure brought by original equipment manufacturer customers; [m] Textron's ability to realize full value of receivables; [n] the availability and cost of insurance; [o] increases in pension expenses and other post-retirement employee costs; [p] Textron Financial’s ability to maintain portfolio credit quality; [q] Textron Financial’s access to debt financing at competitive rates; [r] uncertainty in estimating contingent liabilities and establishing reserves to address such contingencies; [s] performance of acquisitions; [t] the efficacy of research and development investments to develop new products; [u] the launching of significant new products or programs which could result in unanticipated expenses; and [v] bankruptcy or other financial problems at major suppliers or customers that could cause disruptions in Textron’s supply chain or difficulty in collecting amounts owed by such customers.