metalloinvest jpmorgan 2011 · pdf filestrategic location of key production assets* 6 ... *...

TRANSCRIPT

METALLOINVEST

J.P. Morgan Annual Russia Credit Conference

Moscow November 2011

Corporate presentation

Disclaimer

1

Assumes the following RUB/USD FX rates for 2008, 2009, 2010, H1 2011 and 9M 2011: daily average over the period – 24.8553, 31.7231, 30.3692, 28.6242 and 28.7664 respectively;

at balance sheet dates – 29.3804, 30.2442, 30.4769, 28.0758 and 31.8751 respectively.

These materials contains certain forward-looking statements, particularly those relating to anticipated demand and consumption, global economic recovery,

commodity prices, management aims and objectives, strategy, production, anticipated investment and the anticipated completion of previously announced

transactions. Metalloinvest will not update these statements to reflect events and circumstances occurring after the date hereof. By their nature, forward-looking

statements involve risks and uncertainties because they relate to events and depend on circumstances that will or may occur in the future. Actual results may differ

from those expressed in such statements depending on a variety of factors, including future levels of industry product supply, demand and pricing, operational

problems, general economic conditions, political stability and economic growth in relevant areas of the world, changes in laws and governmental regulations,

exchange rate fluctuations, development and use of new technology, changes in public expectations and other changes in business conditions, the actions of

competitors, natural disasters and adverse weather conditions, wars and acts of terrorism or sabotage, other factors discussed elsewhere in this document, as well

as many other risks affecting Metalloinvest and its operations.

These materials does not constitute or form part of any advertisement of securities, any offer or invitation to sell or issue or any solicitation of any offer to purchase

or subscribe for, any securities of Metalloinvest in any jurisdiction, nor shall they or any part of them nor the fact of their presentation, communication or distribution

form the basis of, or be relied on in connection with, any contract or investment decision. No representation or warranty, express or implied, is given by

Metalloinvest, its affiliates or any of their respective advisers, officers, employees or agents, as to the accuracy of the information or opinions or for any loss

howsoever arising, directly or indirectly, from any use of these materials or their contents.

Agenda

2

o METALLOINVEST overview

o Market positions

o Debt profile

o Strategy

o Appendices

3

11

14

19

24

METALLOINVEST overview

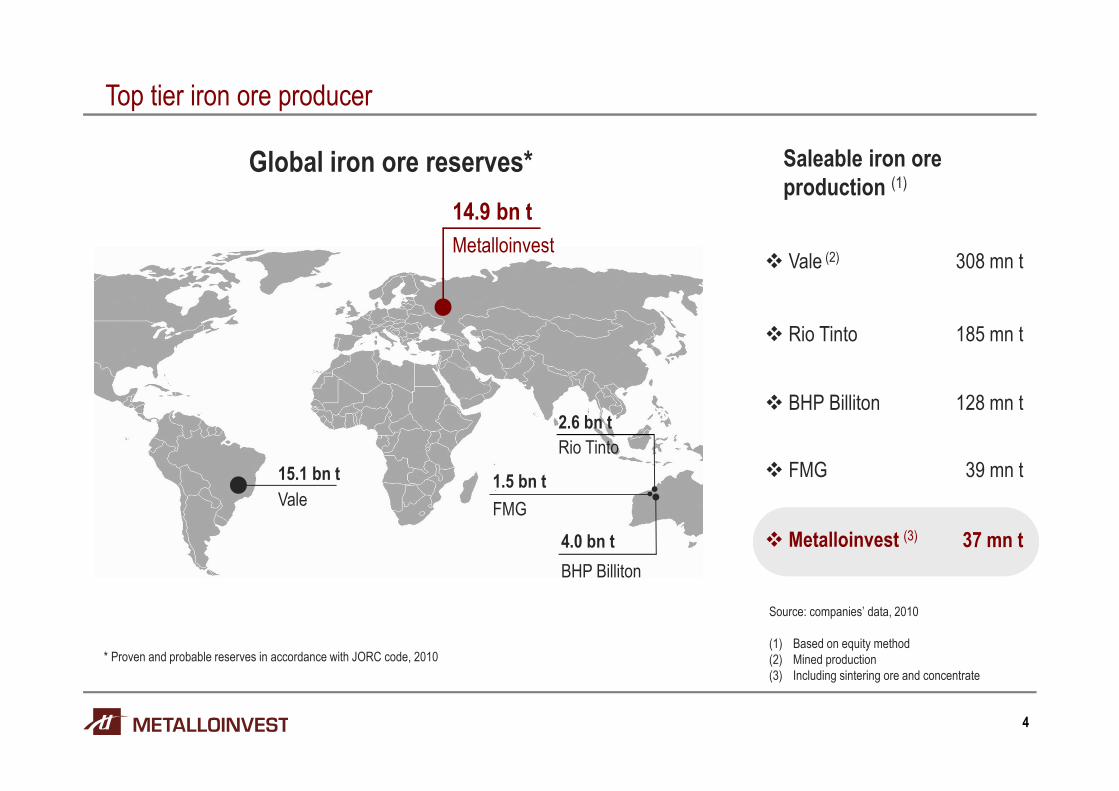

Top tier iron ore producer

4

� Metalloinvest (3) 37 mn t

14.9 bn t

Global iron ore reserves*

* Proven and probable reserves in accordance with JORC code, 2010

15.1 bn t

Vale

Metalloinvest

FMG

1.5 bn t

Saleable iron ore

production (1)

� Vale (2)

� Rio Tinto

� BHP Billiton

� FMG

308 mn t

185 mn t

128 mn t

39 mn t

BHP Billiton

Rio Tinto

4.0 bn t

2.6 bn t

Source: companies’ data, 2010

(1) Based on equity method

(2) Mined production

(3) Including sintering ore and concentrate

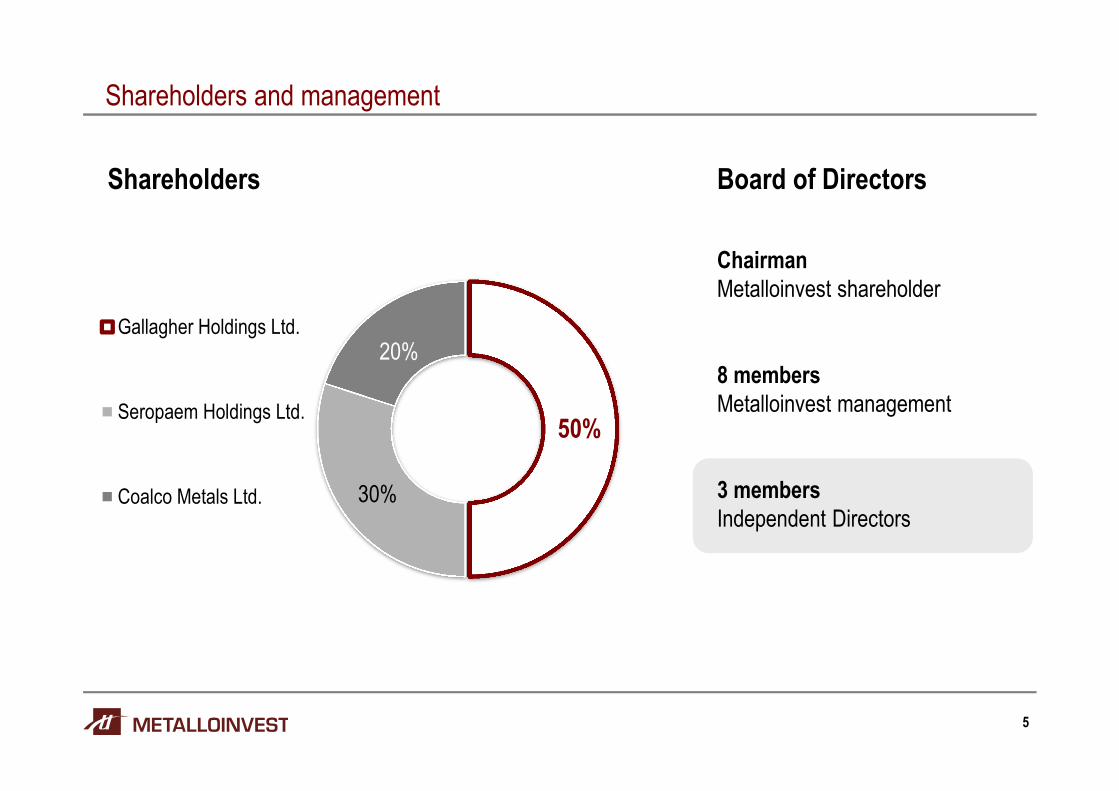

Shareholders and management

5

50%

30%

20%Gallagher Holdings Ltd.

Seropaem Holdings Ltd.

Coalco Metals Ltd.

Shareholders Board of Directors

Chairman

Metalloinvest shareholder

8 members

Metalloinvest management

3 members

Independent Directors

Strategic location of key production assets*

6

LGOK

• The largest iron ore producer in the CIS

• The highest quality among CIS peers

• The largest HBI producer in Europe and

CIS

Reserves 4.2 bn t

Concentrate

Pellets

HBI

19.8 mn t

8.8 mn t

2.3 mn t

MGOK

• The largest standalone iron ore reserves

in CIS

• 2nd largest Russian iron ore producer

• First to introduce flotation technology in

Russia

Reserves 10.7 bn t

Concentrate

Pellets

15.3 mn t

9.7 mn t

OEMK

• Unique coke-free technology

• Low-cost producer

• Maintained 100% capacity through crisis

Pellets

DRI

Crude steel

Steel products

3.5 mn t

2.4 mn t

3.3 mn t

3.1 mn t

Ural Steel

• High value-added niche steel products

• Large producer of merchant pig iron

• 50% self-sufficiency in electricity

Hot metal

Crude steel

Steel products

2.6 mn t

2.8 mn t

2.3 mn t

RUSSIA

MGOK

LGOK

OEMK Ural Steel

Open pit mining (project)Steelmaking

Open pit mining

Udokan

* Production figures in the charts stand for 2010

2.1 2.2 2.3 1.8

2.4 2.4 2.4

2.0

4.5 4.6 4.73.8

2008 2009 2010 9M 2011

LGOK (HBI) OEMK (DRI)

8.0 7.5 8.86.6

8.5 8.59.7

7.4

3.5 3.4

3.5

2.9

20.0 19.422.0

16.8

2008 2009 2010 9M 2011

LGOK MGOK OEMK

Key production figures

7

19.7

16.0

19.8

16.4

15.6

13.8

15.3

12.2

35.4

29.9

35.1

28.7

2008 2009 2010 9M 2011

LGOK MGOK

Pellets

HBI/DRI

Iron ore concentrate, mn t High value-added iron ore products, mn t

65-70%

Diversified customer base with focus on EM

8

Iron ore mining plants Key customers

RUSSIA & CIS

MMK

NLMK

Evraz

Mechel

China & South East Asia

Baosteel Group

Hebei Jingye I&S

Kobe Steel

Xilin Group

Europe & MENA

ArcelorMittal

Tata Corus

US Steel Kosice

Gulf Industrial Investment

30%

43%

27%

* Figures are based on the Company’s iron ore, pellets and HBI/DRI shipments in tonnes for 9M 2011

Financials performance

9

9.3

4.7

7.2

5.1

3.6

0.8

2.62.0

0.3 0.4

1.21.0

0

1

2

3

4

5

6

7

8

9

10

2008 2009 2010 H1 2011

Revenue

EBITDA

Net Income

USD bn

Key strengths

10

Best-in-class profitability metrics

#2iron ore reserve base

in the world

#5global iron ore player

& regional champion

#1supplier of merchant HBI

in the world

#1cost curve ranking

in pellets & HBI

Market positions

A leading supplier of high value-added iron ore products*

12

64%

36%

HBI

World Metalloinvest

89%

11%

Pellets

World Metalloinvest

Source: AME, Company data, 2010 Source: CRU, Company data, 2010

* Charts provide the data on the Company’s market share in global shipments

The highest performance among Russian peers

13

21%

6%

18% 17%

39%

25%

28%27%

39%

18%

36%39%

0%

10%

20%

30%

40%

50%

2008 2009 2010 H1 2011

EBITDA EBITDAmarginUSD mn

2,204

687

1,606

783

6,206

1,444

3,263

2,043

3,564

838

2,588

1,982

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2008 2009 2010 H1 2011

Russian peers*

Metalloinvest

* Severstal, NLMK, MMK, Mechel, Evraz

Debt profile

Credit portfolio performance

15

6.1

5.4

4.1

6.2

5.5

0.2 0.4 0.2 0.4 0.4

1.7

6.5

1.6

1.81.5

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

2008 2009 2010 H1 2011 Q3 2011

Total Debt Cash & equivalents Total Debt/EBITDA LTM* (rhs)

USD bn Rx

* Last twelve-months period

Credit portfolio structure

16

56%

13%

18%

13%

Breakdown by type of source

PXF

Eurobonds

Sberbank

Others 73%

24%

3%

Breakdown by currency

USD

RUR

EUR

* Data as of October 1, 2011

Credit portfolio performance

17

21.6 23.019.6

29.5

33.6

7.8% 7.8%

6.6%

4.8% 4.8%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

5

10

15

20

25

30

35

40

2008 2009 2010 H1 2011 Q3 2011

Weighted Average Life Interest rate (RHS)

Months %

Debt maturity profile

18

0.1 0.8

1.2

1.0

1.0

1.4

5.5

0

1

2

3

4

5

6

Q4 2011 2012 2013 2014 2015 2015+ Total Debt*

* Data as of October 1, 2011

USD bn

Strategy

Strategy highlights

20

Iron ore HVA*

production increase

HBI/DRI & Pellets

Maintaining global leadership on HBI market

Steel segment

profitability growth

Product mix widening & focus on niche markets

Installation of new high-efficiency equipment

M&A activityFinancial investments in Metals & Mining industry

Diversification of commodity portfolio

Iron ore reserve base

development

Exposure to Emerging markets

Focus on new customers & Logistics

Cost efficiency

improvements

Application of new technologies

Production facilities improvements & economy of scale

* HVA means high value-added products

Focus on value-added iron ore products

21

4.8

6.6

1.8

2010 After new HBI-3construction

22

27

5

2010 After new pellet plantconstruction

Pellets capacity, mta HBI/DRI capacity, mta

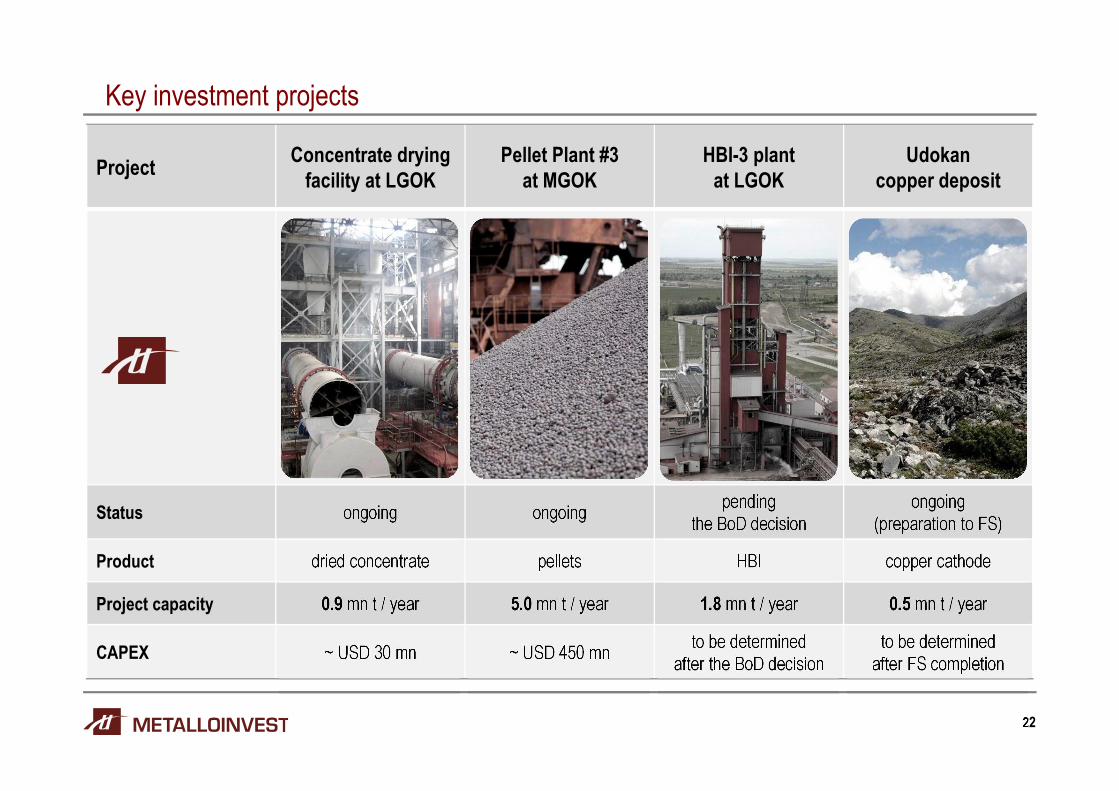

Key investment projects

22

ProjectConcentrate drying

facility at LGOK

Pellet Plant #3

at MGOK

HBI-3 plant

at LGOK

Udokan

copper deposit

Status ongoing ongoingpending

the BoD decision

ongoing

(preparation to FS)

Product dried concentrate pellets HBI copper cathode

Project capacity 0.9 mn t / year 5.0 mn t / year 1.8 mn t / year 0.5 mn t / year

CAPEX ~ USD 30 mn ~ USD 450 mnto be determined

after the BoD decision

to be determined

after FS completion

Rating agencies

Financial

institutions

Investors

Independent reserves

auditors

International insurance

companies

Sep-Dec 2011Jan-Aug 201120102007 2008

Integration in Global Economy

23

Increase in iron ore P&P

reserves up to 14.9 bn tonnes

by IMC

New PXF USD 3.1 bn

loan obtained

USD 1.6 bn

syndicated loan by

Deutsche Bank

USD 0.7 bn

syndicated loan

by ABN / BNPP

USD 750 mn

Eurobonds issue (LSE)

Web-site improvements

13.8 bn tonnes of

P&P* reserves by IMC

Ba3, positive by Moody’s

BB-, stable by Fitch

Ba3, stable

by Moody’s

Business partners 2009

IR dep. establishment

Debut Disclosure

Broader coverage by

international insurance

companies

* P&P – proved and probable reserves based on JORC code

Appendices

HBI – unique HVA product

25

Supply side

Constrained supply (high quality iron ore and abundance of natural gas required)

HBI produced only in handful of countries(India, Mexico, Russia, Venezuela, etc.)

Demand side

Growing number of mini-mills and scrap shortage

Technological shift to EAF steelmaking

Scrap shortage & scrap quality decrease in CIS

Market position

The only HBI producer in Russia and CIS

The largest commercial HBI supplier globallywith 36% market share

Efficiency and environment33% - energy savings over traditional pig iron production

44% - greenhouse gas emission reduction over traditional steelmaking route (sinter&coke & BF&BOF)

High-quality material (low non-ferrous metals content)

HBI -direct substitute of scrap

METALLOINVEST & Capital Markets

26

70

80

90

100

110

July August September October

Eurobonds issue

Buy-back

Key parameters

Date

July 2011

Maturity

5 years

Value

USD 750 mn

Coupon rate

6.5%

* In August-September the Company repurchased its Eurobonds at the total amount of USD 52 mn (par value)

For more details:

Artem Lavrischev

Head of Investor Relations

T: +7 (495) 981 55 55, ext. 7243

Thank You