microeco project grb2

TRANSCRIPT

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 1/26

9/14/2009

Study of the Indian Two Wheeler Industry and analyzing the Key Driving

Factors | Group B2

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 2/26

OVERVIEW

Indian automobile industry has grown leaps and bounds since 1898, a time when a car had touched the

Indian streets for the first time. At present it holds a promising tenth position in the entire world with

being # 1 in TwoWheelers and # 4 in commercial vehicles. Withstanding a growth rate of 18% per

annum and an annual production of more than 2 million units, it may not be an exaggeration to say

that this industry in the coming years will soon touch a figure of 10 million units per year.

The automobile industry in India — the ninth largest in the world with an annual production of over

2.3 million units in 2008 — is expected to become one of the major global automotive industries in the

coming years.

Segmentation of Automobile Industry

The automobile industry comprises of Heavy

vehicles (trucks, buses, tempos, tractors);

passenger cars; Two-wheelers; Commercial

Vehicles; and Three-

wheelers. Following is

the segmentation

that how much each

sector

Group B2 Page 2

INDIAN TWO WHEELER INDUSTRY

MICROECONOMICS PROJECT REPORT

Submitted To :Prof. DeviPrasad Bedari

Submitted By :Group B2

Subhashis Biswas

Anubhav KediaRahul Prakash Oswal

Priya Ramanthan

Sashank Shah

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 3/26

comprises of whole Indian Automobile Industry.

OBJECTIVE OF THE PROJECT

The main objectives of the Project study are:

• Study the growth pattern of the Two Wheeler Industry

• Analyze the Oligopolistic Indian Two Wheeler Industry and identify the key players

• Analyzing the Reasons/Factors affecting the Two Wheeler Industry.

METHODOLOGY

The data which is collected is mainly from the research on the internet. Data are collected from

various sources which archive such information. The data is archived in SIAM (Society of Indian

Automobile Manufacturers),India Stat. Apart from this related data is collected from auto magazines

like Top Gear, Overdrive, Autocar India ,CIAM India ,CMIE Prowess ,ACMA Buyers Guide EBSCO

Database , EIS, Crisil Research.

References :

www.indexmundi.com

www.tradingeconomics.com

Group B2 Page 3

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 4/26

www.indiastat.com

www.wikipedia.org

AutomobileIndia.com

ANALYSIS

A Growth Perspective

A major growth in the automobiles sales over the years can be noticed, however the composition of

the two-wheeler industry has witnessed sea changes in the post-reform period. In 1991, the share of

scooters was about 50 per cent of the total 2-wheeler demand in the Indian market. Motorcycle and

moped had been experiencing almost equal level of shares in the total number of two-wheelers. In

2003-04, the share of motorcycles increased to 78 per cent of the total two-wheelers while the shares

of scooters and mopeds declined to the level of 16 and 6 per cent respectively. A clear picture of the

motorcycle segmental share gaining importance during this period is exhibited by the figure given

below of segmental share of two-wheeler industry during the period 1993-94 through 2003-04.

Group B2 Page 4

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 5/26

Nature of Two-Wheeler Industry

The total size of the Indian two-wheeler industry stood at Rs 288 million in 2007-08, with total

volumes of around 80 million units. The industry, which is dominated by Hero Honda, Bajaj Auto

and TVS Motors, is divided into three segments - motorcycles, scooters and mopeds. Motorcycles

dominate the two-wheeler industry, both in terms of volume and value. In 2007-08, the share of

motorcycles in the domestic two-wheeler market was around 80 per cent while scooters and mopeds

accounted for 15 per cent and 5 per cent share, respectively.

Fig . Two-Wheeler : Player wise share in domestic sales

Segmental Market Domination

Motorcycle Segment

Group B2 Page 5

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 6/26

Hero Honda dominates the motorcycle segment, with nearly 50 per cent market share

followed by Bajaj Auto and TVS Motors. The segment also has players such as Yamaha and Suzuki.

However, they have not been able to grab significant market share in the Indian two-wheeler market.

Fig. Motorcycle: Player Wise share in domestic sales

Scooter

Bajaj Auto dominated the geared scooter segment, accounting for nearly 40-45 per cent of the scooter

market in 2002-03. However, the company began to lose market share with the decline in the geared

scooter segment, with its share in 2007-08 falling to a mere 2 per cent. Meanwhile, Honda Motorcycle

& Scooter India Ltd (HMSI) has become the dominant player in the scooter segment over the last 4-5

years with a market share in excess of 50 per cent followed by TVS Motors at 22-25 per cent.

Group B2 Page 6

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 7/26

Fig . Scooter: Player Wise share in domestic Sales

Mopeds

Mopeds are generally preferred in urban areas. Also, there are not many players in this segment with

TVS Motors accounting for more than 80 per cent market share over the past few years. With other

players gradually discontinuing operations in this segment, TVS Motors’s share grew to more than 95

per cent share in 2007-08.

Group B2 Page 7

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 8/26

Fig . Mopeds : Playerwise Share in Domestic Sales

Hero Honda is the leader with the maximum product launches and highest market share of around 42

per cent followed by Bajaj Auto. Though the number of launches for Yamaha has been high, the

company has not been able to grab significant market share. Further, players such as Suzuki and

Kinetic Motors have limited launches and marginal market share in the two-wheeler market.

Market Shares and Oligopolistic Nature

Group B2 Page 8

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 9/26

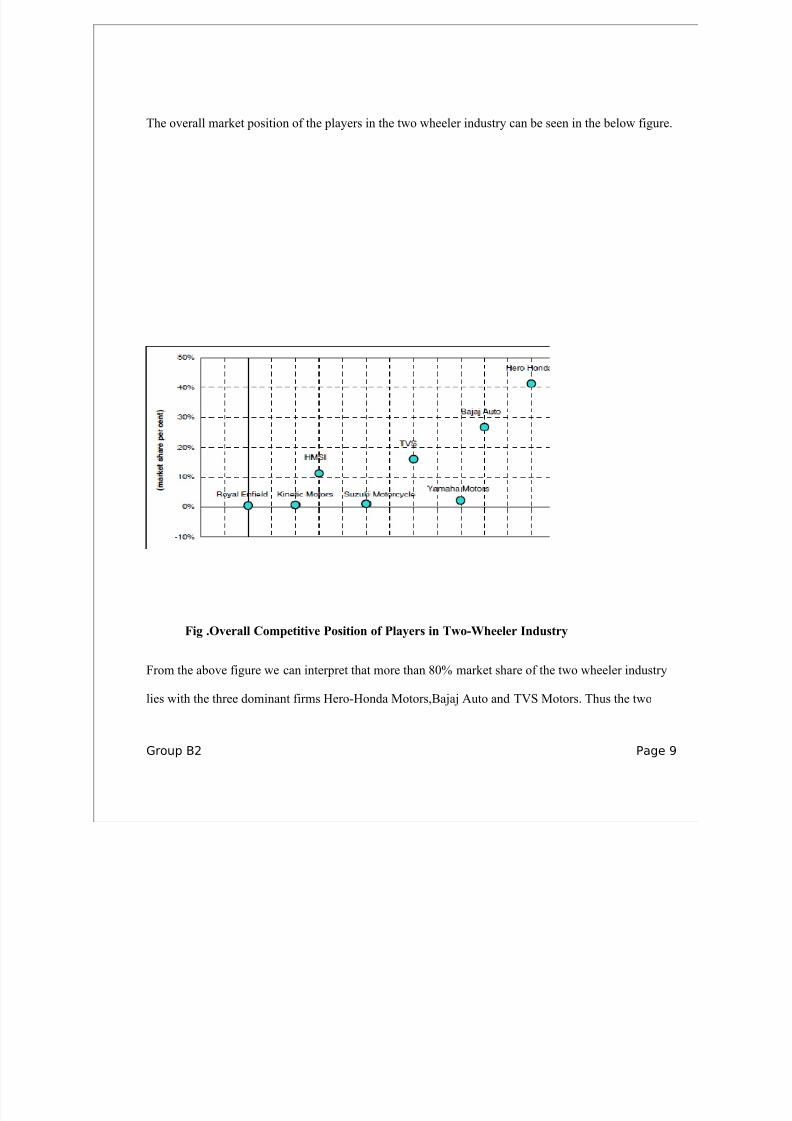

The overall market position of the players in the two wheeler industry can be seen in the below figure.

Fig .Overall Competitive Position of Players in Two-Wheeler Industry

From the above figure we can interpret that more than 80% market share of the two wheeler industry

lies with the three dominant firms Hero-Honda Motors,Bajaj Auto and TVS Motors. Thus the two

Group B2 Page 9

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 10/26

wheeler industry is a differentiated oligopoly with each player having differentiated products in the

market.

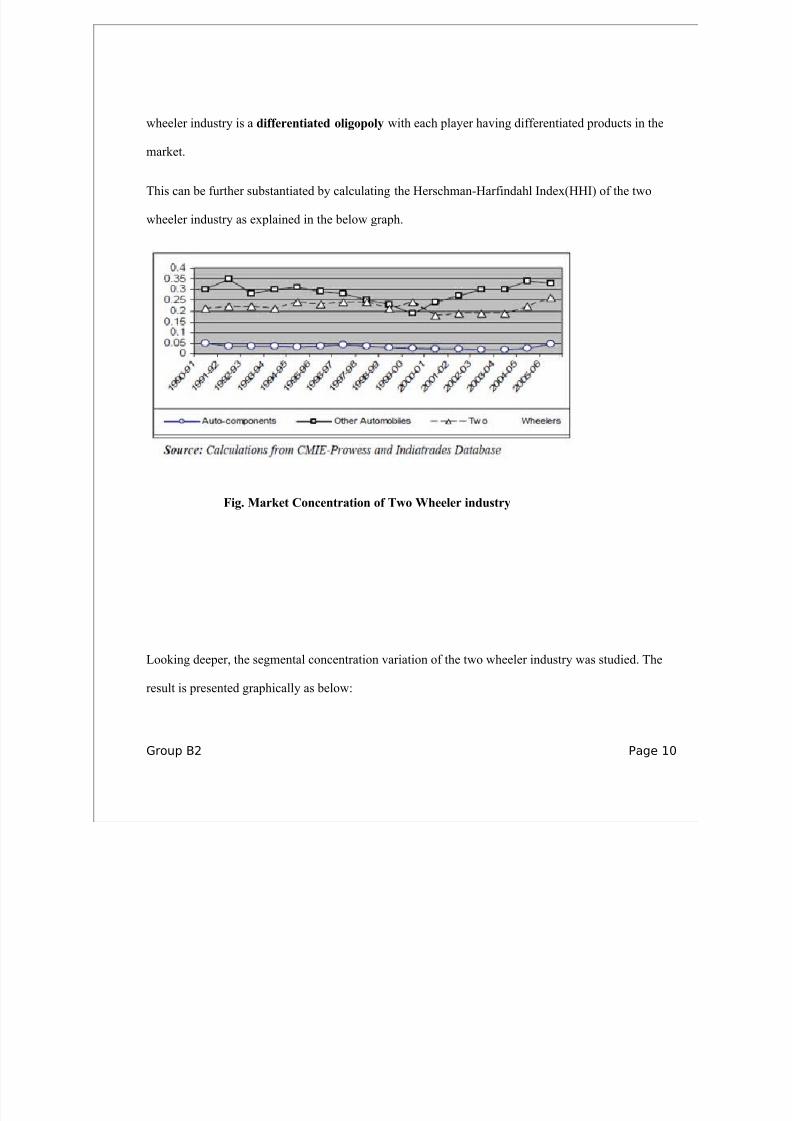

This can be further substantiated by calculating the Herschman-Harfindahl Index(HHI) of the two

wheeler industry as explained in the below graph.

Fig. Market Concentration of Two Wheeler industry

Looking deeper, the segmental concentration variation of the two wheeler industry was studied. The

result is presented graphically as below:

Group B2 Page 10

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 11/26

Fig. Harfindahl Index concentration of Different two –wheeler segments

We can now conclude that new firms like HMSI, TVS has entered into the scooter segment,

earlier dominated by Bajaj Auto and has captured significant market share. This has led to reduction in

the market concentration ratios of scooter which was, as revealed by declining Herfindahl Index of

Concentration as well. However in the motorcycle segment, the concentration increased for the

dominant players like Hero-Honda, TVS, Bajaj Auto inspite of the presence of few competetors the

market was widely governed by Hero-Honda Motors,Bajaj Auto,TVS Motors and HMSI having the

majority share.

Due to this oligopolistic nature in the two wheelers sector (HHI in the range 0.22->0.28),

which means that there have been 4-8 firms in this industry with an average individual market share in

the range of 10-25% each. The upward trend shows that few leading firms, through stiff non-price

competition, are virtually forcing the other firms out of this market. (Hero Honda, Bajaj, HMSI and

TVS together have grabbed a large market share from Yamaha, LML, Kinetic etc.).

.

Porter’s Five Force Analysis of Indian Two Wheeler Industry:

Michael Porter identifies five forces that influence an industry. These forces are

• Degree of Rivalry

Group B2 Page 11

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 12/26

Despite the high concentration ratio seen in the two wheeler sector, rivalry is intense due to the

entry of foreign companies in the market. The industry rivalry is extremely high with any product

being matched in a few months by the competitors.

• Threat of Substitutes

The threat of substitutes to the two wheeler industry is fairly mild. Numerous other forms

of transportation are available, but none offer utility, convenience and value offered. The switching

cost associated with using a different mode of transportation, may be high in terms of personal

time, convenience and utility.

Group B2 Page 12

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 13/26

• Barriers to entry

Although the barriers to new companies are substantial, establishing companies are entering

the new markets through strategic partnerships or through buying out or merging with other

companies. However, a domestic company, with local knowledge and expertise, has the potential

to compete its home market against the global firms who are not well established there.

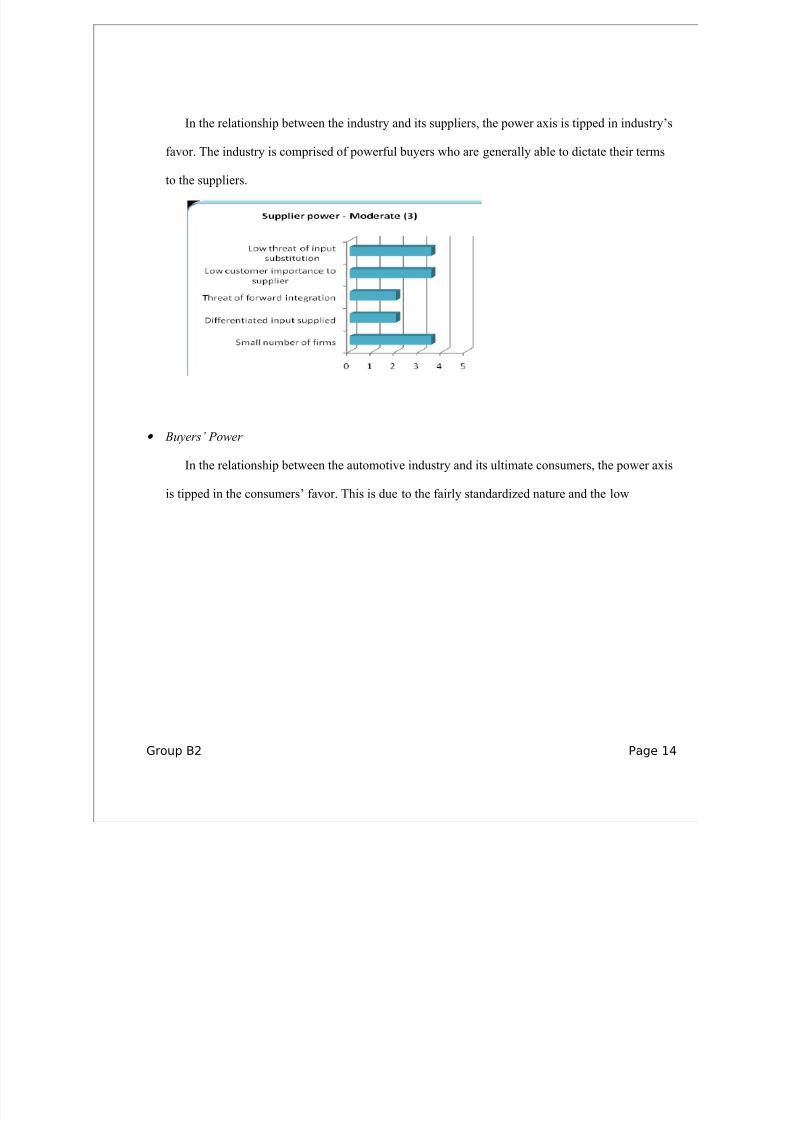

• Supplier’s power

Group B2 Page 13

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 14/26

In the relationship between the industry and its suppliers, the power axis is tipped in industry’s

favor. The industry is comprised of powerful buyers who are generally able to dictate their terms

to the suppliers.

• Buyers’ Power

In the relationship between the automotive industry and its ultimate consumers, the power axis

is tipped in the consumers’ favor. This is due to the fairly standardized nature and the low

Group B2 Page 14

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 15/26

switching costs associated with selecting from among competing brands.

Overall Evaluation : The Indian two wheeler industry is Moderately Attractive.

Group B2 Page 15

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 16/26

Demand and Supply of Two Wheelers:

Factors Affecting Two Wheeler Industry

Cost Analysis

Group B2 Page 16

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 17/26

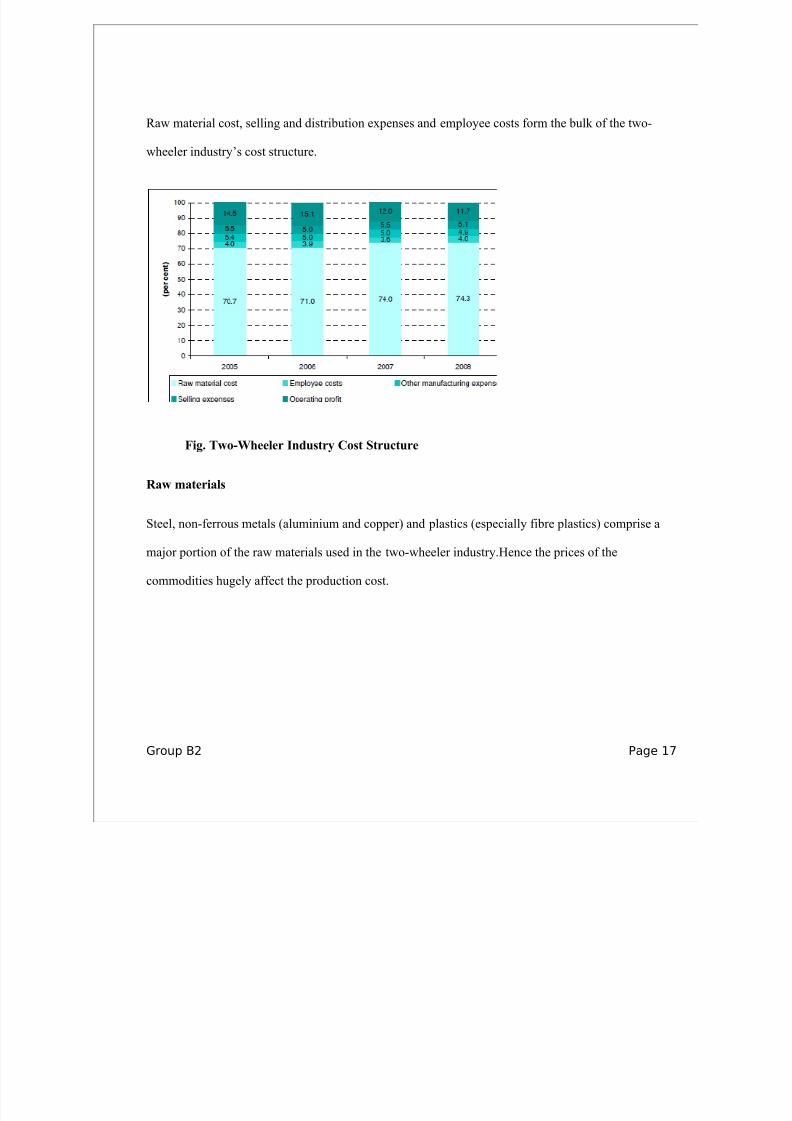

Raw material cost, selling and distribution expenses and employee costs form the bulk of the two-

wheeler industry’s cost structure.

Fig. Two-Wheeler Industry Cost Structure

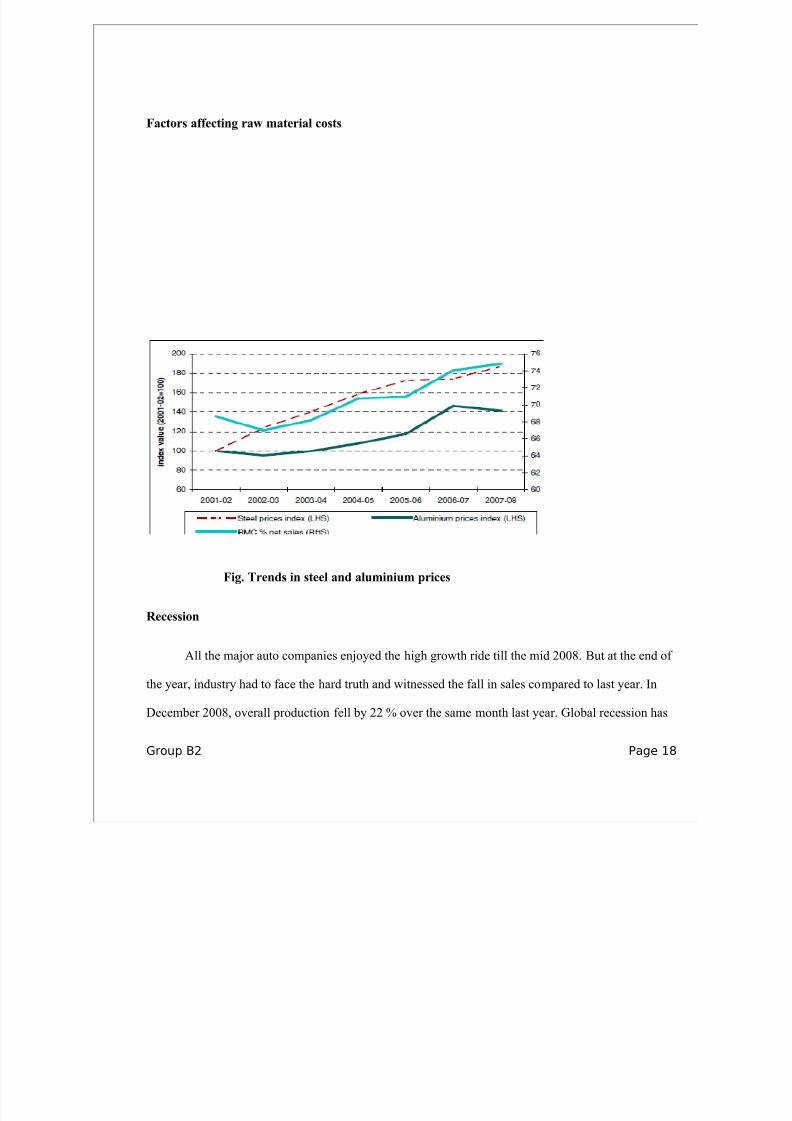

Raw materials

Steel, non-ferrous metals (aluminium and copper) and plastics (especially fibre plastics) comprise a

major portion of the raw materials used in the two-wheeler industry.Hence the prices of the

commodities hugely affect the production cost.

Group B2 Page 17

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 18/26

Factors affecting raw material costs

Fig. Trends in steel and aluminium prices

Recession

All the major auto companies enjoyed the high growth ride till the mid 2008. But at the end of

the year, industry had to face the hard truth and witnessed the fall in sales compared to last year. In

December 2008, overall production fell by 22 % over the same month last year. Global recession has

Group B2 Page 18

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 19/26

hit the Indian auto industry, India has a strong and growing industry but the impact of recession is

evident now on industry as sales & growth of two wheeler companies have declined.

Two Wheelers registered minor growth of 1.85 % during April – December 2008. However, Two

Wheelers sales recorded 15.43 percent fall in December 2008 over the same month last year. Although

the sector was hit by economic slowdown, overall production (passenger vehicles, commercial

vehicles, two wheelers and three wheelers) increased from 10.85 million vehicles in 2007-08 to 11.17

million vehicles in 2008-09.

.

Inflation

In last FY despite of skyrocketing oil prices had affected every sector which is related to car

manufacturing and production. The increase in the price of fuel and the steel due to inflation has led to

a decline in two wheeler domestic sales and exports.

Fig. Growth Trend in Two-Wheeler Exports in 2008-09

Group B2 Page 19

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 20/26

Fig. Growth Trend in Two-Wheeler Domestic sale in 2008-09

FDI’s

In India FDI up to 100 percent, has been permitted under automatic route to this sector, which has led

to a turnover of USD 12 billion in the Indian auto industry and USD 3 billion in the auto parts

industry. India enjoys a cost advantage with respect to casting and forging as manufacturing costs in

India are 25 to 30 per cent lower than their western counterparts the Investment Commission has set a

target of attracting foreign investment worth US$ 5 billion for the next seven years to increase India's

share in the global auto components market from the existing 0.9 per cent to 2.5 per cent by 2015. FDI

inflows in Automobile Industry 2008-09 was Rs.5,212 Cr an increase of 47.25% compare to 2007-08,

while in April-May 2009 it was around Rs.497 Cr.

Source- FDI Statistics Govt. of India

Group B2 Page 20

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 21/26

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 22/26

Fig, Two Wheeler financing

Government Fiscal Policy

The Union Budget for 2001-02 had lowered the excise duty on two-wheelers (with engine

capacity in excess of 75 cc) from 24% to 16%. The manufacturers responded to this by passing on a

relatively large part of the excise cut to customers. The Union Budget thereafter have left the excise

duty on two-wheelers unchanged. But the Union Budget 2004-05 provides for a weighted deduction of

150% for investments in R&D. This may facilitate increasing R&D allocations and allow for

improvement in the technical as well as product development skills of the Indian companies.

• Indian Auto Policy 2002

The Government of India approved a comprehensive automotive policy in March 2002, the main

proposals of which are as under:

○ Import tariff: Import tariffs are proposed to be fixed at a level such that they facilitate the

development of manufacturing capabilities as opposed to mere assembly.

Group B2 Page 22

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 23/26

Fig. Decrease in Customs Duty and increase in Production of Two Wheeler.

○ Incentives for R&D: The weighted average tax deduction under the Income Tax

Act, 1961 for automotive companies is proposed to be increased from current level of

125% (The weighted average deduction for R&D was increased to 150% in the Union

Budget 2004-05). Further, the policy proposes to include vehicle manufacturers for a rebate

on the applicable excise duty for every 1% of the gross turnover of the company expended

during the year on R&D.

Group B2 Page 23

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 24/26

Fig. Yearly Estimate of R&D Allocation by Major Players (Rs. Crores)

Future Prospects of Two Wheeler Industry

The two wheeler industry has grown in leaps and bounds since after removal of MRTP and FERA.

According to analysis, rural India would drive the growth, whereas the opportunity in urban India,

especially bigger cities, is limited. Abundant and low cost labor coupled with local availability of raw

materials like steel, aluminium and natural rubber has placed India amongst the low cost producing

centres of two-wheelers. Consequently buoyant growth in two-wheeler exports is anticipated as well.

Global demand to rise 7.6% annually through 2013

Global demand for motorcycles is forecast to rise 7.6 percent per year through 2013 to 114 million

units, spurred by rising standards of living in poorer developing parts of the world, which are making

motorcycles a more affordable alternative to walking, bicycling or using mass transit. Higher energy

prices, along with a rebound in economic growth after a recessionary period that began in a number of

nations in 2008, will also contribute to motorcycle market gains in both developing and developed

Group B2 Page 24

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 25/26

areas. Product sales will expand at a slower pace in value terms, climbing 7.2 percent annually to

$66.6 billion in 2013, because of an expected decline in sales-weighted prices. Some offsetting

support will be provided by the introduction of new models equipped with sophisticated emissions

control systems and increased sales of machines with more features, boosting motorcycle dollar

demand.

Conclusion

The oligopolistic nature of the Two Wheeler industry had not changed from the pre-reforms

time in 1988-1990 to the post reform period ie, after 1996, infact the degree of concentration has

increased making it difficult for new players to enter into the market. The established players are being

able to drive away new competitors. This implies that the deregulation of the industry has not led to

substantially higher competition. This may reflect the inadequacy of regulatory policy and/or the

nature of the technology of the industry wherein an oligopolistic structure is natural.

The values of the HHI also indicate that the three segments of the industry have responded in

different ways to changes in the forces of competition. This is an outcome of liberalization which led

to an unequal number of entrants in each segment. Thus, it is quite possible that when competition-

inducing policies are introduced, there could be an unequal number of entrants in each segment, which

would then further increase oligopoly in some segments and for the industry as a whole. Oligopoly

could also result from the fact that it is existing firms that are introducing new brands rather than new

firms entering the industry – thus making the industry a differentiated oligopoly. When the

movement of prices in the three segments is considered, it is seen that prices (net of inflation) have not

Group B2 Page 25

8/9/2019 Microeco Project Grb2

http://slidepdf.com/reader/full/microeco-project-grb2 26/26

decreased though the number of brands has increased. This is indicative of oligopoly(non-price

competition). Therefore, future reforms in the industrial policy covering the twowheeler industry will

probably need to incorporate some mechanism to induce new firms to enter the industry.

Group B2 Page 26