microfinance: learning what works, what does not, and why

TRANSCRIPT

Microfinance: Learning What Works,

What Does Not, And Why

How do we Reach 1 Billion?

• Is it flexibility?• Is it price?• Is it institutional?

Massive untapped market: Why are so many yet to be reached?

What’s the Secret?How do we Design Effective Microfinance?

How do we:

• Create the most impact?– increase incomes, improve

health, education• Reach more clients?• Reach poorer clients?• Increase savings balances?• Improve client retention?• Improve profitability?

The answer is:

We Don’t Really Know

Yet

We Have a Lot to Learn• Example: Interest rates are very high– In the US, we call this usury and regulate it. – Abroad, we call this charity and donate to it.

• Impact:• How do interest rates affect impact?

• Outreach:• Can we target only those clients who are likely to

benefit (likely to earn high returns)?• Business:• Can we lower interest rates and make more profit?

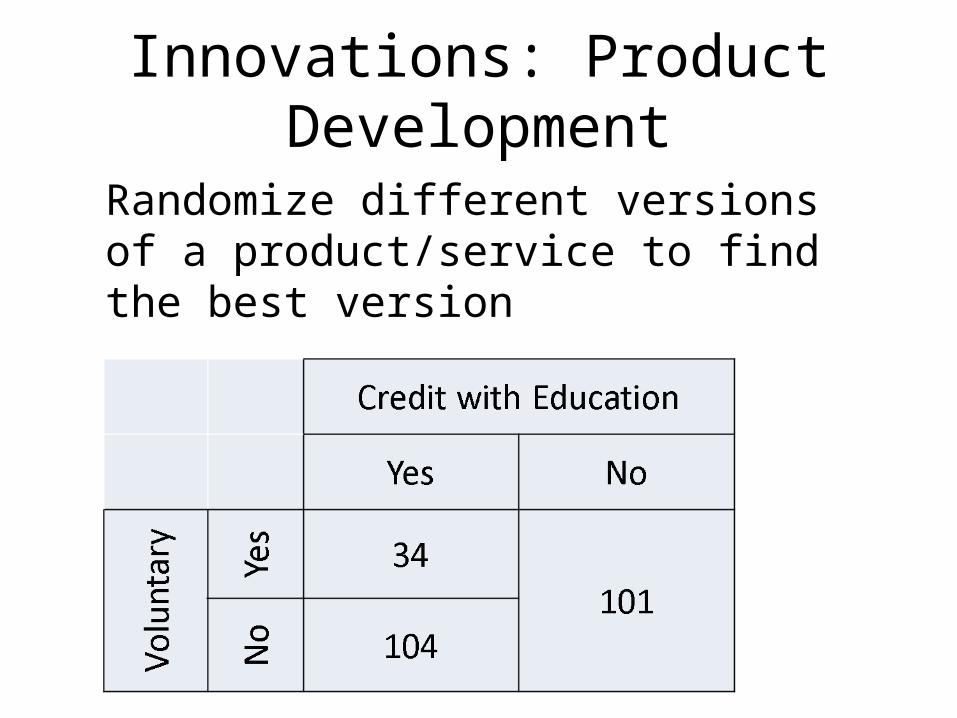

Example: Credit with Education

• Why do many microenterprises plateau? How can we help them grow?

Is credit with education a solution?

Who do You Trust?

• Well-known microfinance leader A: – “The poor do not need us to teach them how to

survive; they already know. So rather than waste our time teaching them new skills, we try to make maximum use of their existing skills.”

• Well-known microfinance leader B: – “Group-based lending/saving services provide an

unusual opportunity to provide transformative educational experiences along with financial services.”

There is No Magic Solution

• Learning what works in microfinance requires methodical experimentation across settings• Not guesswork based on anecdotes

• We need high-quality research methods to produce reliable results

• Randomized controlled trials are the most reliable research methodology.

Evaluation is for Managers!

• Evaluation is for microfinance programs, not annual reports

• Evaluation is much more than “does the program help people?”

• We use rigorous evaluations to learn which products and services work best by trying out different versions and seeing which are most effective– most impact, most profitable, etc.

R&D

Key question for donors/investors:• How do we leverage our

investments to maximize social welfare, while maintaining private returns?

• R&D can help figure out how to tap that market profitably.

• Make sure the approach, if successful, gets replicated and scaled.

Why Randomize: Example from Get out the Vote

Method Estimated Impact

Reached vs. Not Reached 10.8 pp

Why Randomize: Example from Get out the Vote

Method Estimated Impact

Reached vs. Not Reached 10.8 pp

Regression: Control for differences between the groups

6.1 pp

Why Randomize: Example from Get out the Vote

Method Estimated Impact

Reached vs. Not Reached 10.8 pp

Regression: Control for differences between the groups

6.1 pp

Also control for voting history 4.5 pp

Why Randomize: Example from Get out the Vote

Method Estimated Impact

Reached vs. Not Reached 10.8 pp

Regression: Control for differences between the groups

6.1 pp

Also control for voting history 4.5 pp

Matching similar voters 2.8 pp

Why Randomize: Example from Get out the Vote

Method Estimated Impact

Reached vs. Not Reached 10.8 pp

Regression: Control for differences between the groups

6.1 pp

Also control for voting history 4.5 pp

Matching similar voters 2.8 pp

Randomized Experiment 0.4 pp,statistically insignificant

How to Randomize:Experimental Credit Scoring

?

x

applicants scored 0-100

0

100

T C

0

100

Credit Scoring: Findings

• What is the impact of consumer credit?– Positive effect on employment, wages and hunger– 7 percentage-point reduction in poverty level

• Marginal loans are profitable for the lender

How to Randomize: Group vs. Individual Liability

Group vs. Individual Liability: Findings

• 150 joint-liability centers:– 75 randomly assigned to convert to individual

liability– 75 randomly assigned to remain as-is

• Outcomes:– No change in repayment– No change in savings– Higher client retention– More new members joined

Innovations: Product Development

Randomize different versions of a product/service to find the best version

Peru: Teaching Entrepreneurship

Teaching Entrepreneurship: Findings

• Strong benefits for both the client and the institution.

• Repayment higher• Client retention up• Clients’ sales higher• Profitable to offer free

education

Current Work

• Replication• Price• Behavioral Savings: using psychology to help

clients save more• Insurance– Health insurance– Crop price insurance

• Targeting the Ultra Poor