microinsurance seminar, karachi 28 nov 2011 eamon kelly

TRANSCRIPT

Microinsurance

Client Value - Case studies

Microinsurance Seminar, Karachi 28 Nov 2011

Eamon Kelly

Microinsurance is...?

Client Value is ...?1. What is client value and ways to assess it2. Value creation examples3. Conclusion

What about the Business Case ...?

Contents

Based on work completed by the Microinsurance Innovation Facility and my own experience

No perfect answer, most MI operators are still learning...

Background

Microinsurance vs Conv Insurance

Key Aspect Conventional insurance Microinsurance

Clients •Relatively low risk environment •Reasonable insurance culture

•Higher risk exposure/high vulnerability •Weak or no insurance culture

Distribution Channel

•Sold by licenced intermediaries directly to high/middle income or corporate clients

•Sold by non-traditional intermediaries to clients with little experience of insurance

Policy Features •Complex policy documents •Many exclusions

•Simple language •Few, if any, exclusions •Group policies

Premium Calculation & collection

•Often good statistical data •Pricing often based on individual risk characteristics •Monthly to yearly payments

•Little or no historical data •Group pricing •Very price sensitive market •Frequent and irregular payments

Enrolment process

•Often Voluntary •Enrolment via brokers, sales agents

•Mix of mandatory or voluntary sometimes with government involvement •Direct face to face enrolment

Risk control •Limited eligibility •Significant documentation required •Screenings, such as medical tests, may be required

•Broad eligibility or mandatory enrolment •Limited but specific controls are in place •Insurance risk included in premiums, rather than exclusions

Claims process •Complicated processes •Extensive verification documentation

•Simple and fast procedures for small sums •Efficient fraud control

1Assessing client value

Product and process design

How do products meet client needs in relation

to alternatives?

DemandWhat factors influence

the choices of low-income households?

Product useWhat is client

satisfaction, loyalty and feedback to improve

products?

ImpactTo what extent and how

microinsurance improves risk-

management and reduces vulnerability?

6

What is “Client Value”?

accessiblesimple

affordable

responsive

7

appropriate

Building on risk management preferences

PRODUCT• Coverage & sum assured• Exclusions & waiting periods• Eligibility criteria• Value-added services

ACCESS• Choice and enrolment• Information & understanding• Premium payment method• Proximity

COST• Premium to client income• Premium to benefit/cost• Other fees & costs• Cost structure and controls

EXPERIENCE• Policy administration & tangibility• Claims procedures• Claims processing time• Customer care

8

Client value assessment tool - PACE

1.1 Coverage, quality of service, exclusions and waiting periods

0.35

Covers appropriate risks from a client perspectiveIntegrates appropriate riders to main coverProvides adequate service quality (for health)Offers simple cover without many exclusionsProvides limited waiting period

1.2 Sum insured in relation to cost of risk

0.35Pays out adequate amount in relation to cost of riskDoes not put many sub-limits on specific covers

1.3 Eligibility criteria 0.15Is inclusive, does not exclude groups of people unintended...

1.4 Value-added services

0.15

Offers non-insurance benefits Offers preventive health services (for health)Offers value-added agriculture servicesTriggers positive behaviour changes

9

Unpacking one dimension - Product

10

Spectrum of Client Value tools

KPIs

PACE

Client Satisfaction Study

Market Study

Impact Study

MILK Client Math

11

2Value creation examples

12

PACE pilot testing

Kenya composite

• CIC• Pioneer• Britak• Jamii Bora• NHIF

India health

• ICICI Lombard – MG Swath Bima Yojna

• Yeshasvini• Bharti/AXA -

PWDS• VimoSEWA• Uplift• RSBY

Philippineslife

• FICCO• CARD MBA• CLIMBS• TSKI -

Microensure

13

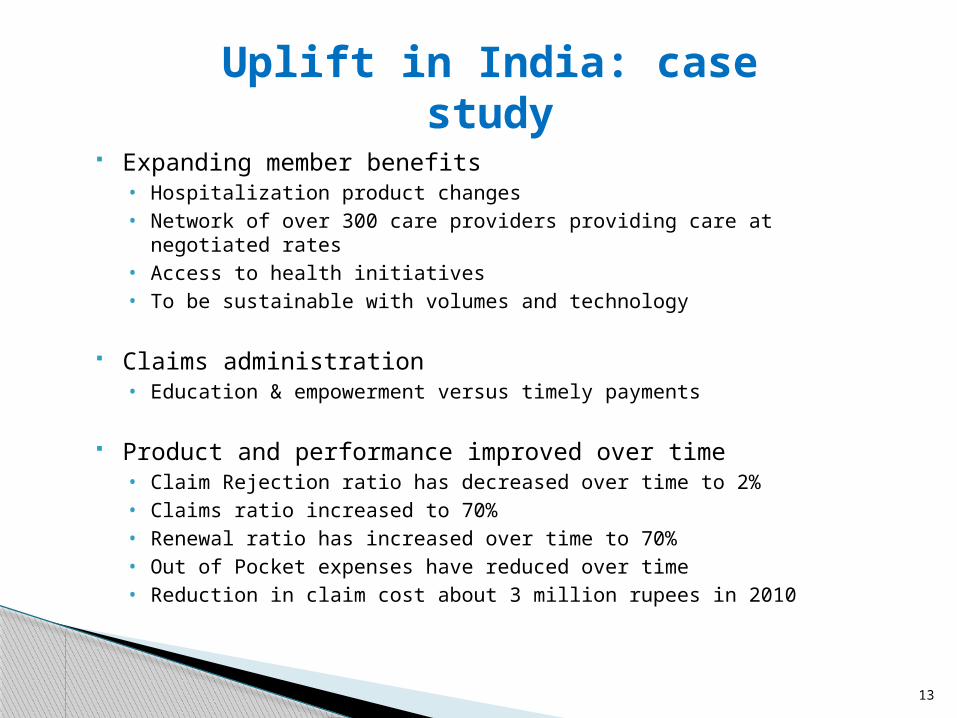

Uplift in India: case study

Expanding member benefits • Hospitalization product changes• Network of over 300 care providers providing care at negotiated rates• Access to health initiatives• To be sustainable with volumes and technology

Claims administration• Education & empowerment versus timely payments

Product and performance improved over time• Claim Rejection ratio has decreased over time to 2% • Claims ratio increased to 70%• Renewal ratio has increased over time to 70%• Out of Pocket expenses have reduced over time • Reduction in claim cost about 3 million rupees in 2010

14

Philippines: case study

TSKI Product

Cover Amount Raised

Community Pricing

Includes borrower and

spouseDefinition of dependents extended

Exclusions => Increasing benefits

Documents Required

Improved product

Opportunities and trade-offs Many value creation opportunities, small

improvements that can make a difference

Balancing trade offs in a continuous improvement process◦ Cost vs Product, Access and Experience

Contextualizing client value

Product and/or market maturity matters!

15