model for the swiss reserve market - eth z · the topic of this master thesis originates from the...

TRANSCRIPT

eeh power systemslaboratory

Haoyuan Qu

Three-Stage Stochastic Market-ClearingModel for the Swiss Reserve Market

Master ThesisPSL 1519

Department:EEH – Power Systems Laboratory, ETH Zurich

In collaboration with Swissgrid Ltd

Examiner:Prof. Dr. Goran Andersson, ETH Zurich

Supervisor:Farzaneh Abbaspourtorbati, Swissgrid

Line Roald, ETH ZurichDr. Marek Zima, Swissgrid

Zurich, December 16, 2015

ii

Abstract

The topic of this master thesis originates from the reserve procurement pro-cess in Switzerland. Currently, a two-stage reserve market has been oper-ated where secondary control reserves are procured in a weekly auction andtertiary control reserves are split between weekly and daily auctions. In or-der to make use of additional available power from producers and to allowthe participation of Renewable Energy Sources (RES), a third market stagewhich is closer to real-time operation is likely to be established in the future,converting the reserve procurement process into a three-stage problem.

The chief objective of this master thesis is to develop a three-stagestochastic market-clearing model for the Swiss reserve market. Within theframework of this thesis, scenarios for daily market are scrutinized and im-proved, which can be readily appended to the current two-stage stochasticmarket-clearing model. Scenarios for the third stage are generated based onreference data in the current market and various cases are simulated. Sim-ulation results show that both improvements on the two-stage model andthe incorporation of an additional third stage could lead to cost savings forTransmission System Operator (TSO).

iii

iv

Acknowledgements

This thesis is the outcome of research work done in cooperation betweenPower Systems Laboratory (PSL) at ETH and Swissgrid. After six monthsof efforts, it concludes my master’s studies in Energy Science and Technol-ogy at ETH and is one of the most important milestones in my life.

First, I would like to express my gratitude towards Prof. Dr. Goran Ander-sson for being my tutor and enabling this collaboration with Swissgrid.

My profound thanks go to Dr. Marek Zima, who has provided me withthe opportunity of conducting research at Swissgrid and introduced me tothe fascinating world of ancillary services market.

Furthermore, I would like to give my deepest appreciation to my supervisorat PSL, Line Roald and my supervisor at Swissgrid, Farzaneh Abbaspour-torbati. Without their continuous support and valuable input, I would nothave managed to come to this final stage.

I should not forget to thank my colleagues from Swissgrid who providedme with all sorts of support, be it technically or spiritually.

Last but not least, I would like to thank and share this piece of work withmy beloved family and friends for their lasting love, patience and support.

Zurich, December 2015

Haoyuan

v

vi

Contents

List of Figures x

List of Tables xi

List of Acronyms xiii

List of Symbols xv

1 Introduction 1

1.1 Balancing Reserves . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Reserve Market . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1.3 Stochastic Programming . . . . . . . . . . . . . . . . . . . . . 3

1.4 Structure of the Thesis . . . . . . . . . . . . . . . . . . . . . . 5

2 Reserve Market in Switzerland 7

2.1 Self-scheduling Market . . . . . . . . . . . . . . . . . . . . . . 7

2.2 Overview of Ancillary Services . . . . . . . . . . . . . . . . . 8

2.3 Structure of Reserve Market . . . . . . . . . . . . . . . . . . . 11

2.3.1 Primary Control Reserves . . . . . . . . . . . . . . . . 11

2.3.2 Secondary and Tertiary Control Reserves . . . . . . . 12

2.4 Bid Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

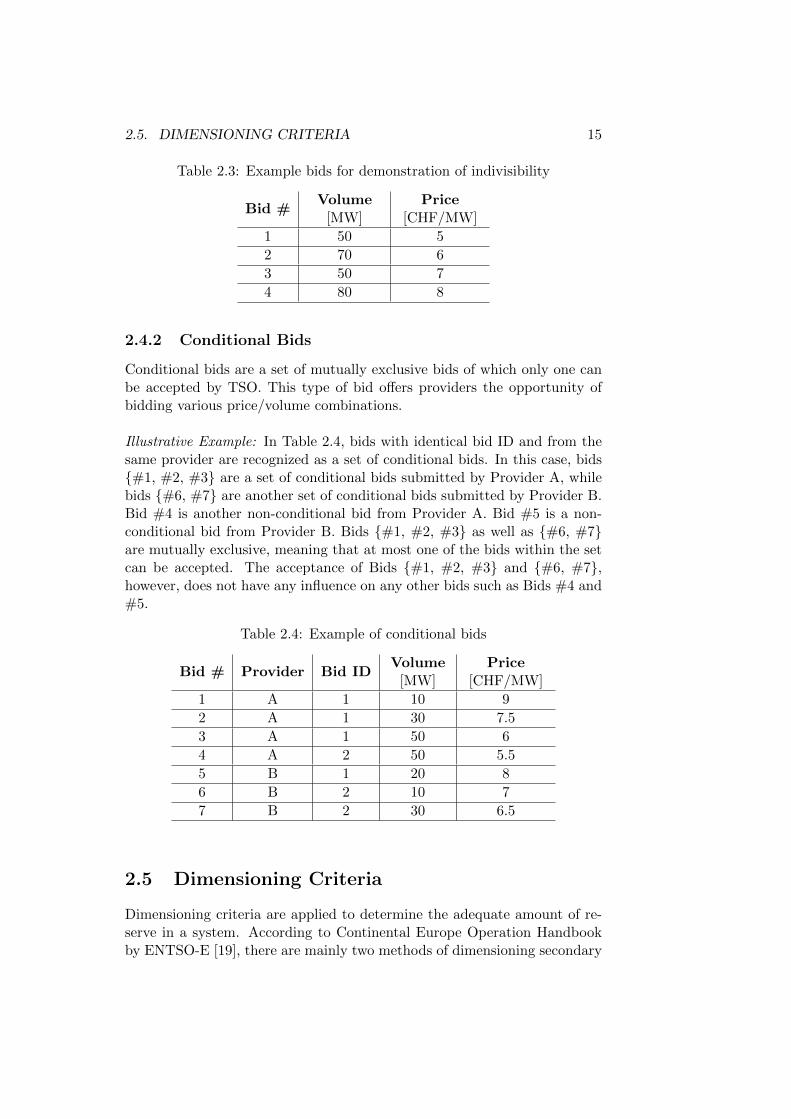

2.4.1 Indivisible Bids . . . . . . . . . . . . . . . . . . . . . . 14

2.4.2 Conditional Bids . . . . . . . . . . . . . . . . . . . . . 15

2.5 Dimensioning Criteria . . . . . . . . . . . . . . . . . . . . . . 15

2.5.1 Probabilistic Approach . . . . . . . . . . . . . . . . . . 16

2.5.2 Deterministic Approach . . . . . . . . . . . . . . . . . 17

2.6 Remuneration Scheme . . . . . . . . . . . . . . . . . . . . . . 17

2.6.1 Remuneration of Capacity . . . . . . . . . . . . . . . . 17

2.6.2 Remuneration of Energy . . . . . . . . . . . . . . . . . 17

3 Two-Stage Market-Clearing Model 19

3.1 Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.2 Stochastic Market-Clearing Model . . . . . . . . . . . . . . . 20

3.2.1 Decision Variables . . . . . . . . . . . . . . . . . . . . 21

vii

viii CONTENTS

3.2.2 Objective Function . . . . . . . . . . . . . . . . . . . . 223.2.3 Constraints . . . . . . . . . . . . . . . . . . . . . . . . 263.2.4 Formulation . . . . . . . . . . . . . . . . . . . . . . . . 31

3.3 Improvements of Two-Stage Model . . . . . . . . . . . . . . . 323.3.1 Linearization of Bid Curves . . . . . . . . . . . . . . . 323.3.2 Selection of Scenarios . . . . . . . . . . . . . . . . . . 37

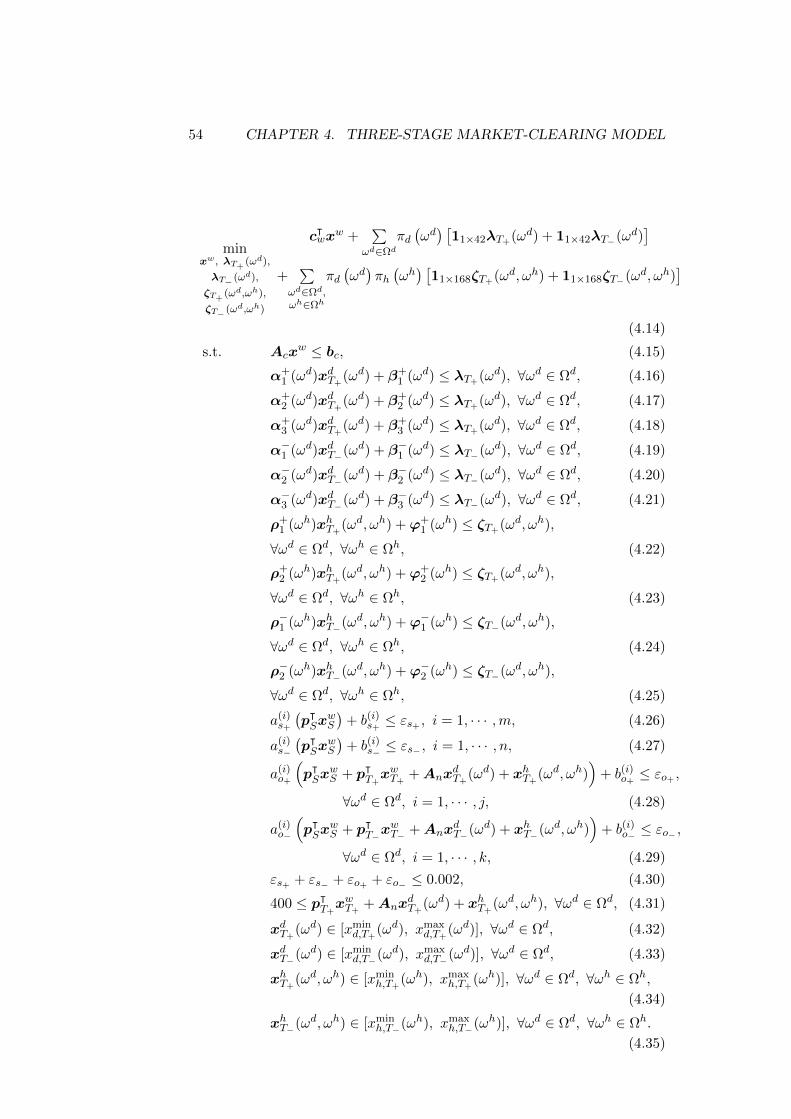

4 Three-Stage Market-Clearing Model 454.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 454.2 Stochastic Market-Clearing Model . . . . . . . . . . . . . . . 47

4.2.1 Decision Variables . . . . . . . . . . . . . . . . . . . . 474.2.2 Objective Function . . . . . . . . . . . . . . . . . . . . 474.2.3 Non-anticipativity Matrix . . . . . . . . . . . . . . . . 504.2.4 Constraints . . . . . . . . . . . . . . . . . . . . . . . . 524.2.5 Formulation . . . . . . . . . . . . . . . . . . . . . . . . 53

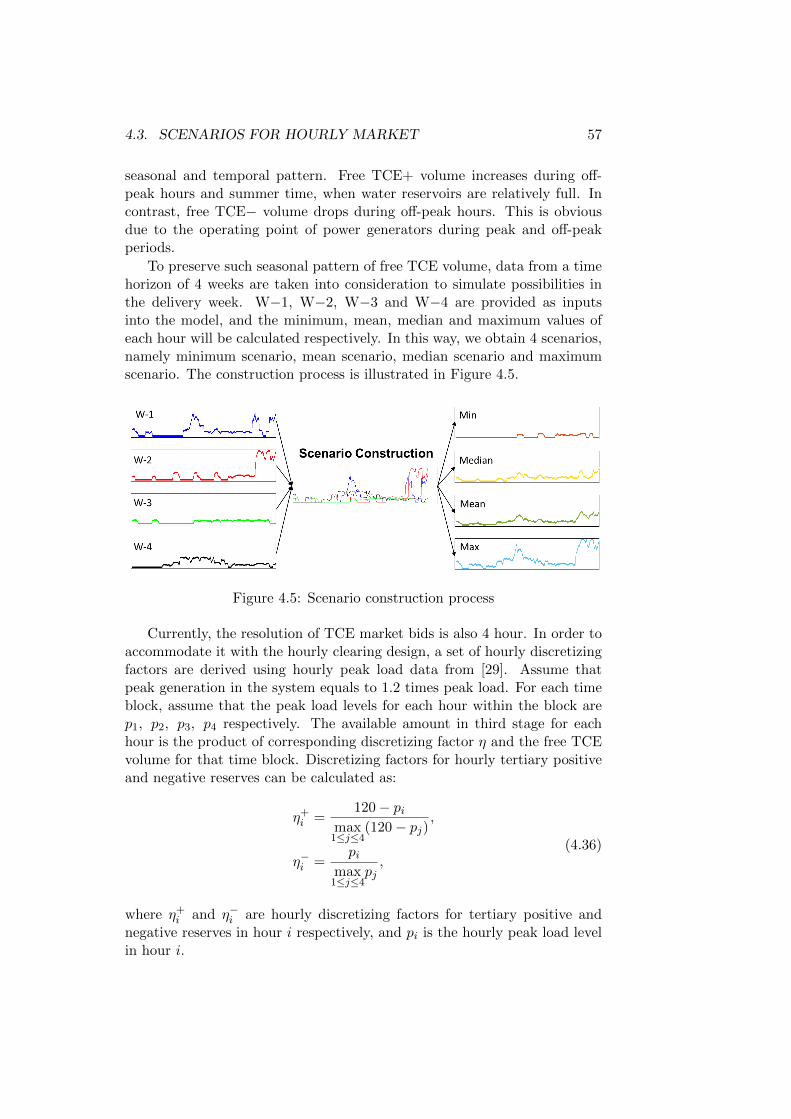

4.3 Scenarios for Hourly Market . . . . . . . . . . . . . . . . . . . 554.3.1 Modelling of Hourly Bid Curves . . . . . . . . . . . . 554.3.2 Scenario Construction . . . . . . . . . . . . . . . . . . 56

4.4 Simulation Results . . . . . . . . . . . . . . . . . . . . . . . . 584.4.1 Case Study: Impact of Hourly Market . . . . . . . . . 584.4.2 Complete Scenario Simulations . . . . . . . . . . . . . 61

5 Conclusions and Outlook 675.1 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 675.2 Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

A Hourly Discretizing Factors 69

Bibliography 71

List of Figures

1.1 Real-time electricity consumption and demand forecast ofNovember 16, 2015 [1] . . . . . . . . . . . . . . . . . . . . . . 2

1.2 Example of a scenario tree for three-stage problems . . . . . . 4

2.1 Temporal structure of frequency control after a disturbance [2] 8

2.2 Simplified diagram of Swiss ancillary services market [3] . . . 11

2.3 Scheme of a two-stage reserve market in Switzerland [4] . . . 12

2.4 Example of SCR and TCR provision . . . . . . . . . . . . . . 14

2.5 Deficit curves for dimensioning reserves in Switzerland [4] . . 16

3.1 Two-stage stochastic market-clearing scheme . . . . . . . . . 20

3.2 Example of a bid curve (before and after linearization) . . . . 24

3.3 Example of piecewise linearized deficit curve . . . . . . . . . . 28

3.4 Overview of bid curve linearization methods . . . . . . . . . . 33

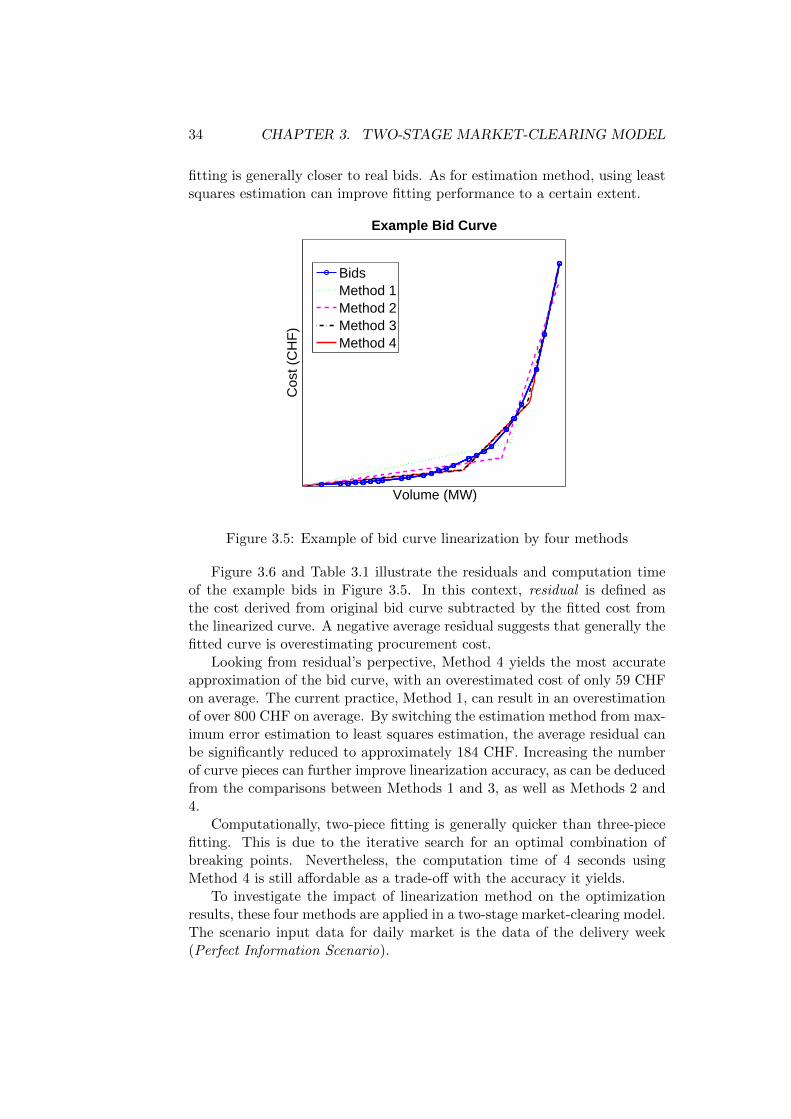

3.5 Example of bid curve linearization by four methods . . . . . . 34

3.6 Residual of fitted bid curve . . . . . . . . . . . . . . . . . . . 35

3.7 Amount of procured reserves using four fitting methods . . . 36

3.8 Total procurement cost of reserves using four fitting methods 36

3.9 Procurement cost in daily market using four fitting methodsafter fixing weekly decision . . . . . . . . . . . . . . . . . . . 36

3.10 Overview of scenario selection methods . . . . . . . . . . . . . 40

3.11 Cost difference w.r.t. perfect information scenario . . . . . . . 41

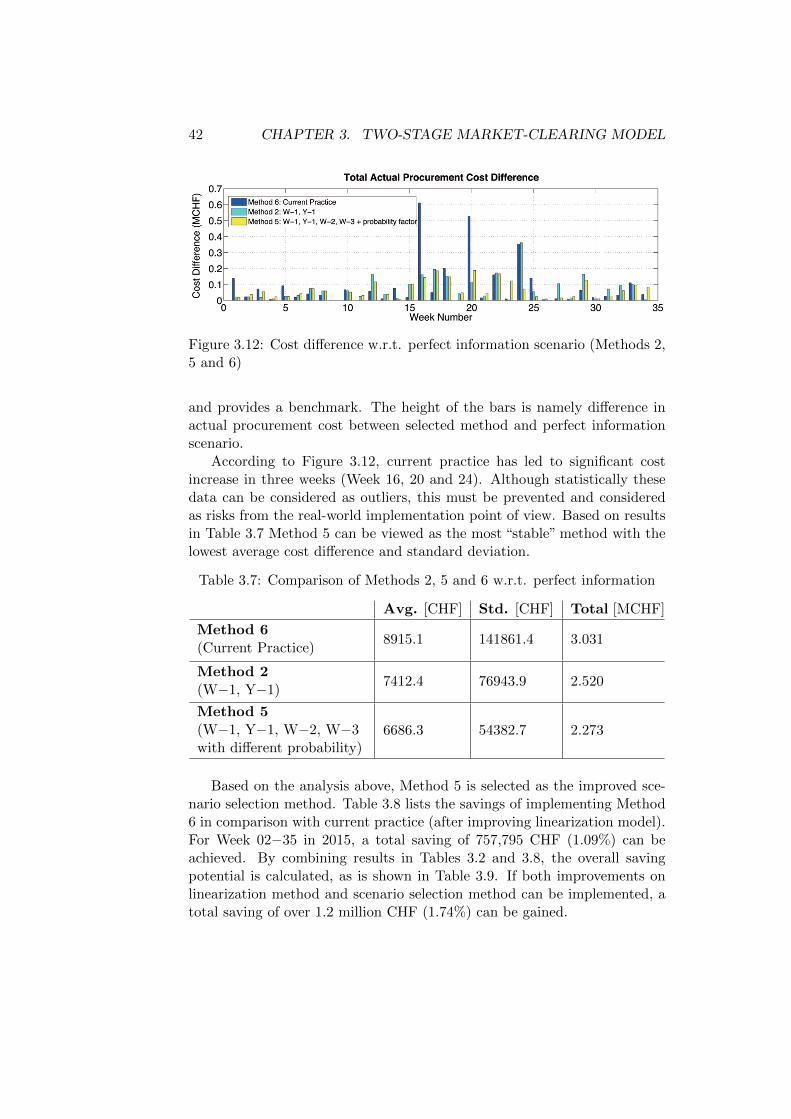

3.12 Cost difference w.r.t. perfect information scenario (Methods2, 5 and 6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.1 Three-stage stochastic market-clearing scheme . . . . . . . . . 46

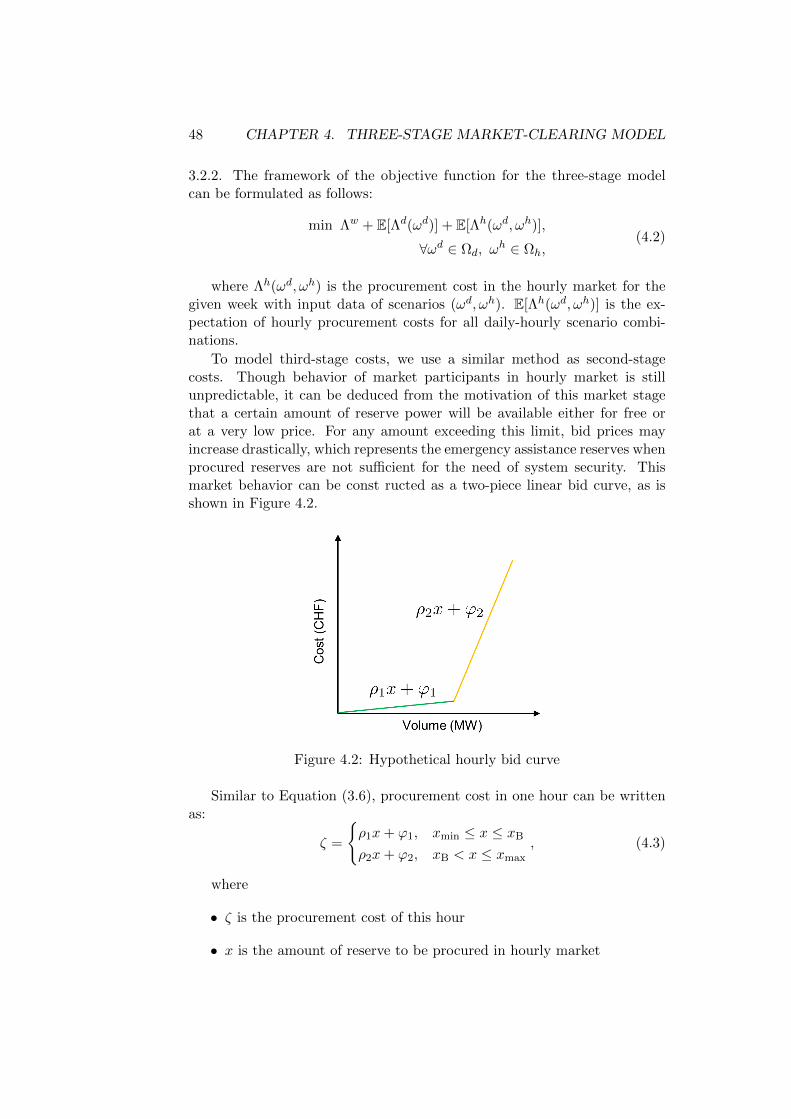

4.2 Hypothetical hourly bid curve . . . . . . . . . . . . . . . . . . 48

4.3 Free TCE+ volume in 2015 (Week 01−35) . . . . . . . . . . . 56

4.4 Free TCE− volume in 2015 (Week 01−35) . . . . . . . . . . . 56

4.5 Scenario construction process . . . . . . . . . . . . . . . . . . 57

4.6 Definition of cases . . . . . . . . . . . . . . . . . . . . . . . . 59

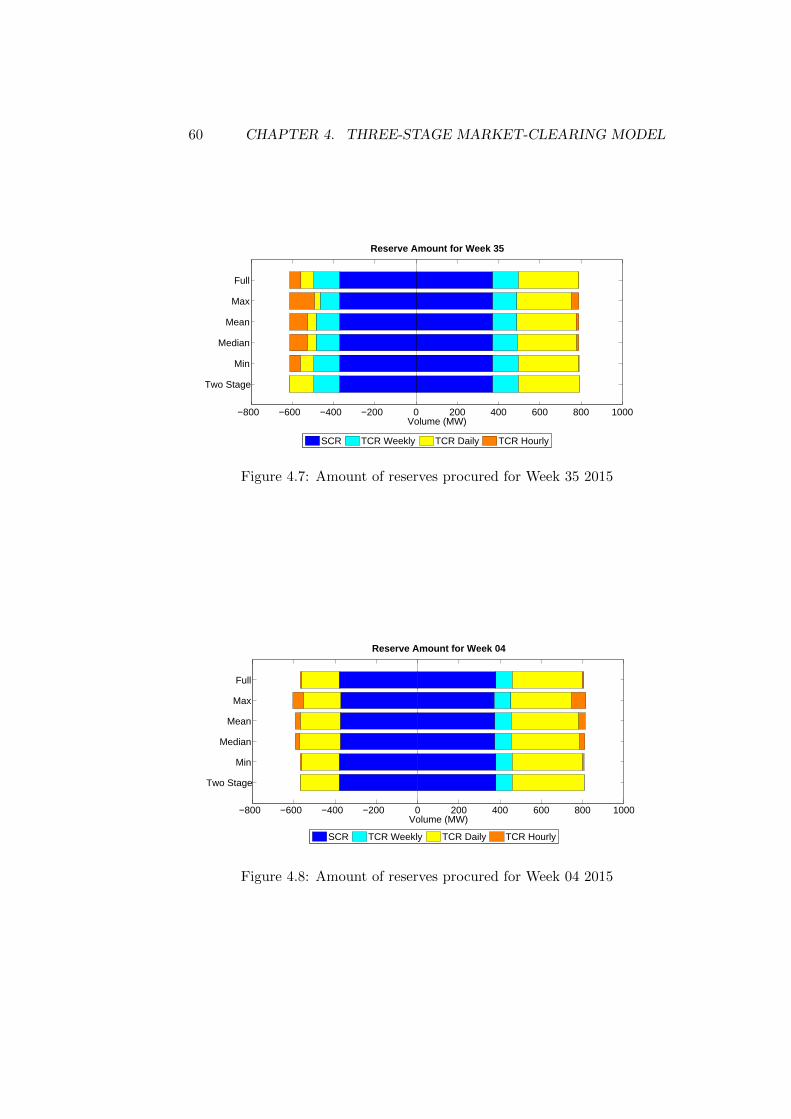

4.7 Amount of reserves procured for Week 35 2015 . . . . . . . . 60

4.8 Amount of reserves procured for Week 04 2015 . . . . . . . . 60

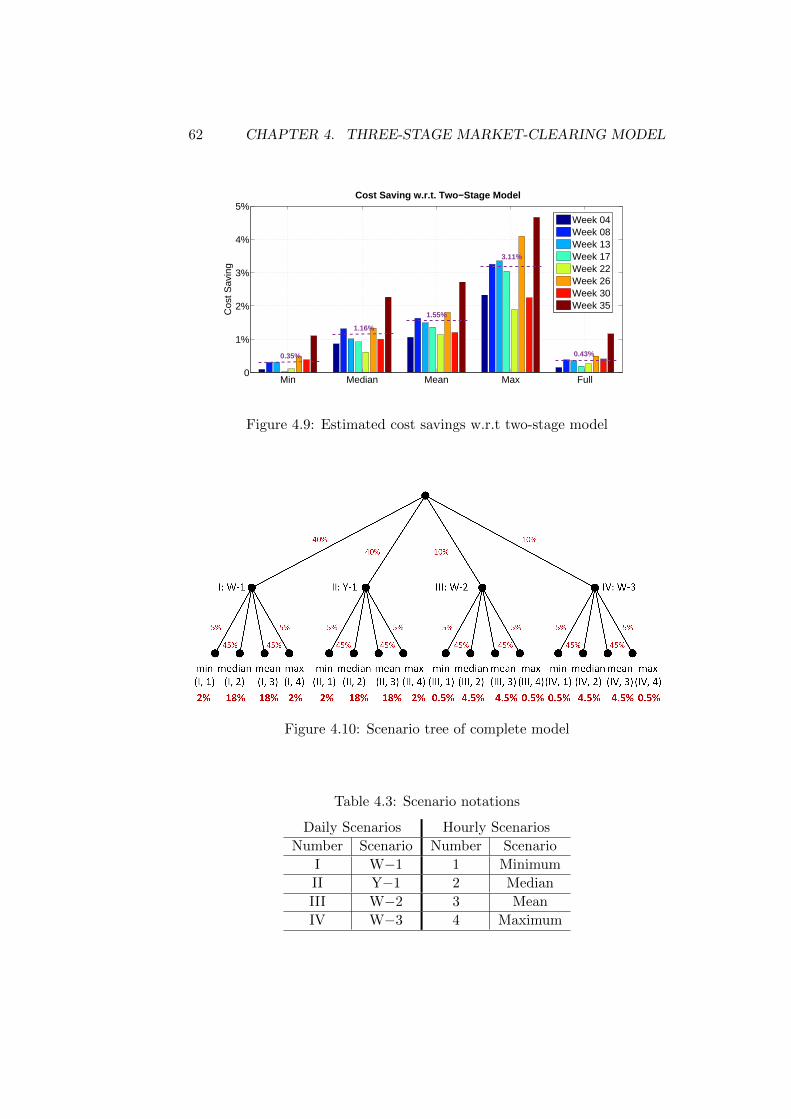

4.9 Estimated cost savings w.r.t two-stage model . . . . . . . . . 62

ix

x LIST OF FIGURES

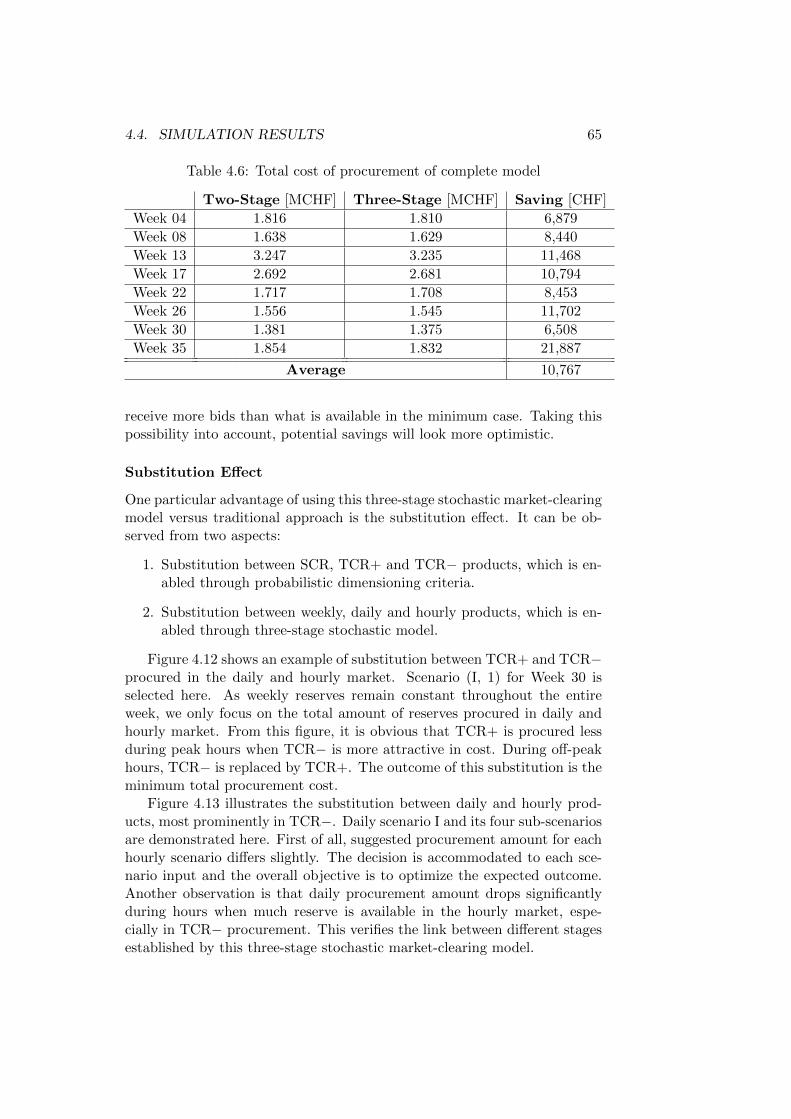

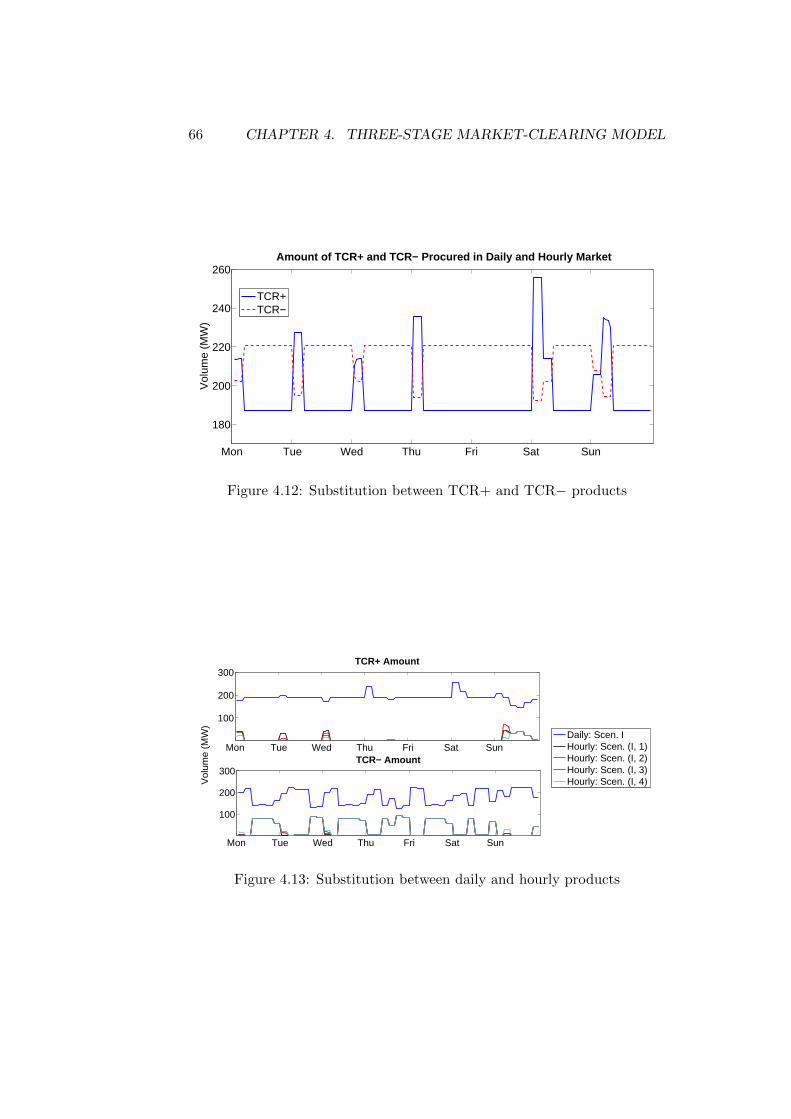

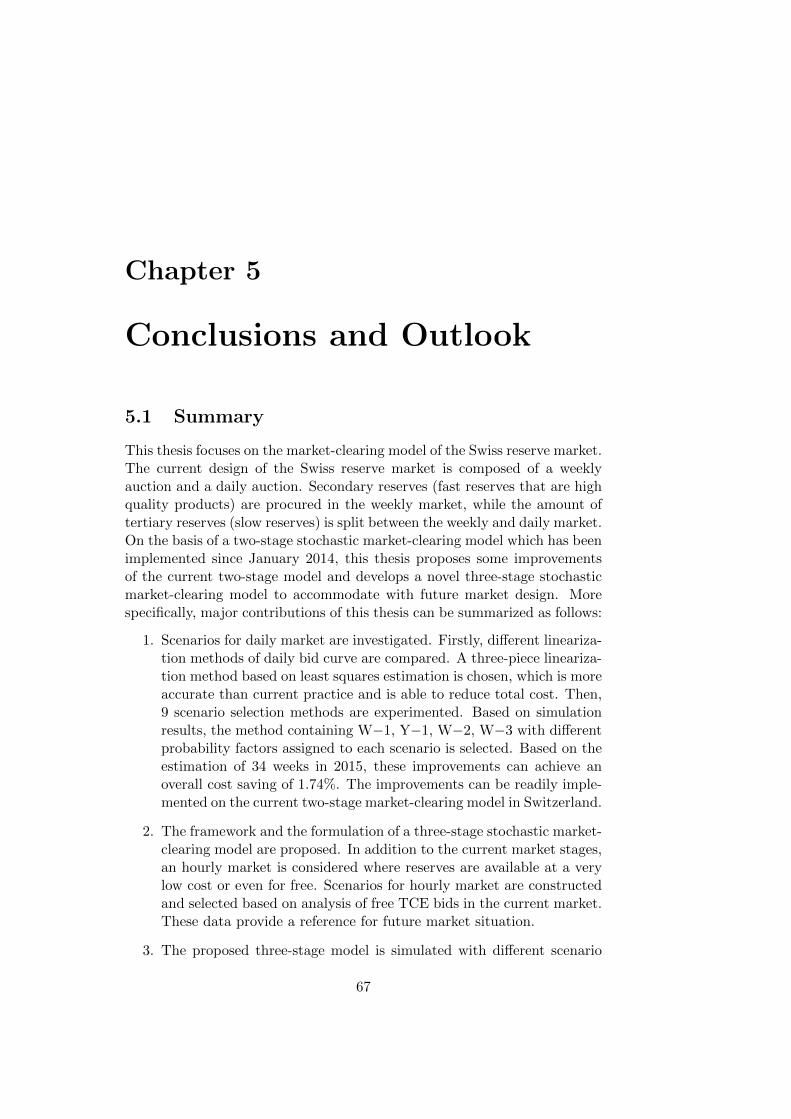

4.10 Scenario tree of complete model . . . . . . . . . . . . . . . . . 624.11 Reserve amount of complete model . . . . . . . . . . . . . . . 644.12 Substitution between TCR+ and TCR− products . . . . . . 664.13 Substitution between daily and hourly products . . . . . . . . 66

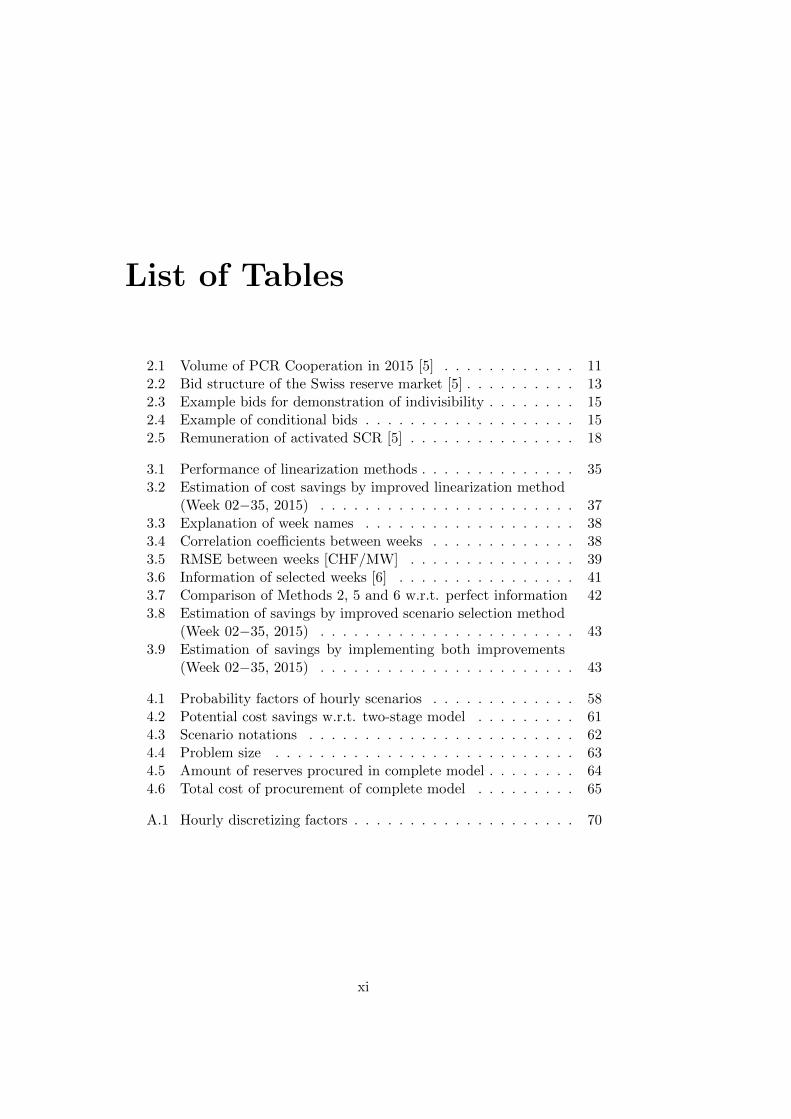

List of Tables

2.1 Volume of PCR Cooperation in 2015 [5] . . . . . . . . . . . . 112.2 Bid structure of the Swiss reserve market [5] . . . . . . . . . . 132.3 Example bids for demonstration of indivisibility . . . . . . . . 152.4 Example of conditional bids . . . . . . . . . . . . . . . . . . . 152.5 Remuneration of activated SCR [5] . . . . . . . . . . . . . . . 18

3.1 Performance of linearization methods . . . . . . . . . . . . . . 353.2 Estimation of cost savings by improved linearization method

(Week 02−35, 2015) . . . . . . . . . . . . . . . . . . . . . . . 373.3 Explanation of week names . . . . . . . . . . . . . . . . . . . 383.4 Correlation coefficients between weeks . . . . . . . . . . . . . 383.5 RMSE between weeks [CHF/MW] . . . . . . . . . . . . . . . 393.6 Information of selected weeks [6] . . . . . . . . . . . . . . . . 413.7 Comparison of Methods 2, 5 and 6 w.r.t. perfect information 423.8 Estimation of savings by improved scenario selection method

(Week 02−35, 2015) . . . . . . . . . . . . . . . . . . . . . . . 433.9 Estimation of savings by implementing both improvements

(Week 02−35, 2015) . . . . . . . . . . . . . . . . . . . . . . . 43

4.1 Probability factors of hourly scenarios . . . . . . . . . . . . . 584.2 Potential cost savings w.r.t. two-stage model . . . . . . . . . 614.3 Scenario notations . . . . . . . . . . . . . . . . . . . . . . . . 624.4 Problem size . . . . . . . . . . . . . . . . . . . . . . . . . . . 634.5 Amount of reserves procured in complete model . . . . . . . . 644.6 Total cost of procurement of complete model . . . . . . . . . 65

A.1 Hourly discretizing factors . . . . . . . . . . . . . . . . . . . . 70

xi

xii LIST OF TABLES

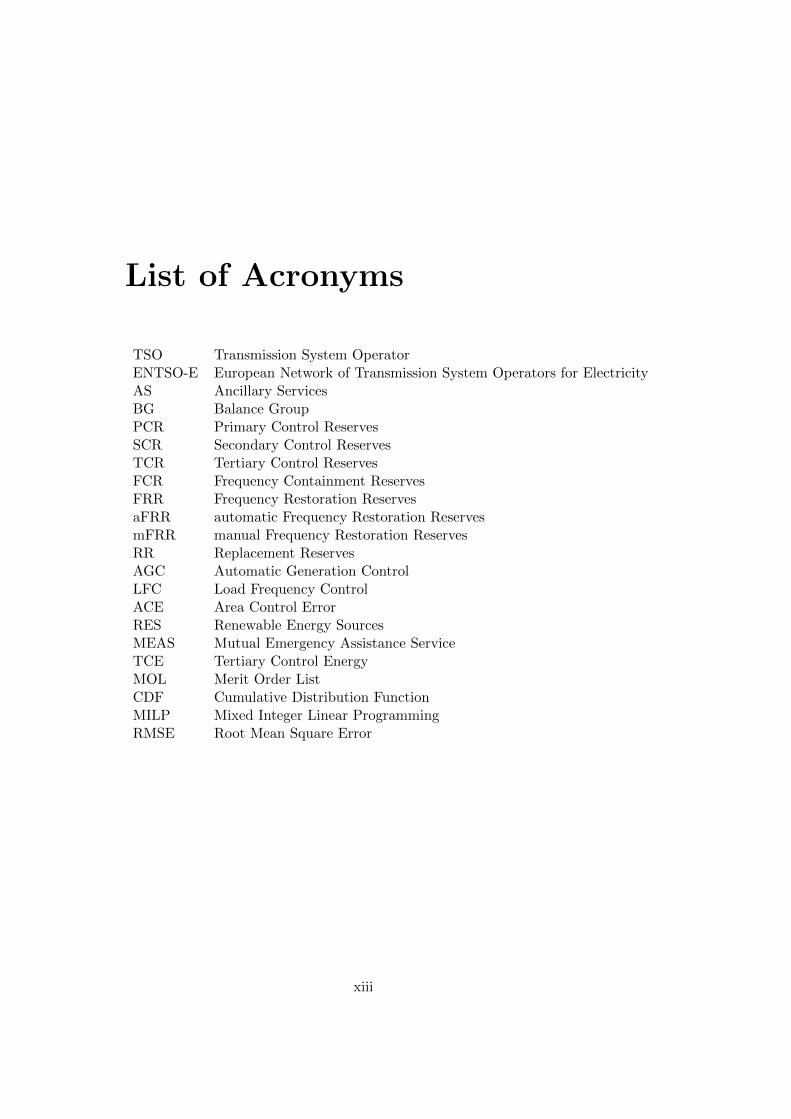

List of Acronyms

TSO Transmission System OperatorENTSO-E European Network of Transmission System Operators for ElectricityAS Ancillary ServicesBG Balance GroupPCR Primary Control ReservesSCR Secondary Control ReservesTCR Tertiary Control ReservesFCR Frequency Containment ReservesFRR Frequency Restoration ReservesaFRR automatic Frequency Restoration ReservesmFRR manual Frequency Restoration ReservesRR Replacement ReservesAGC Automatic Generation ControlLFC Load Frequency ControlACE Area Control ErrorRES Renewable Energy SourcesMEAS Mutual Emergency Assistance ServiceTCE Tertiary Control EnergyMOL Merit Order ListCDF Cumulative Distribution FunctionMILP Mixed Integer Linear ProgrammingRMSE Root Mean Square Error

xiii

xiv LIST OF ACRONYMS

List of Symbols

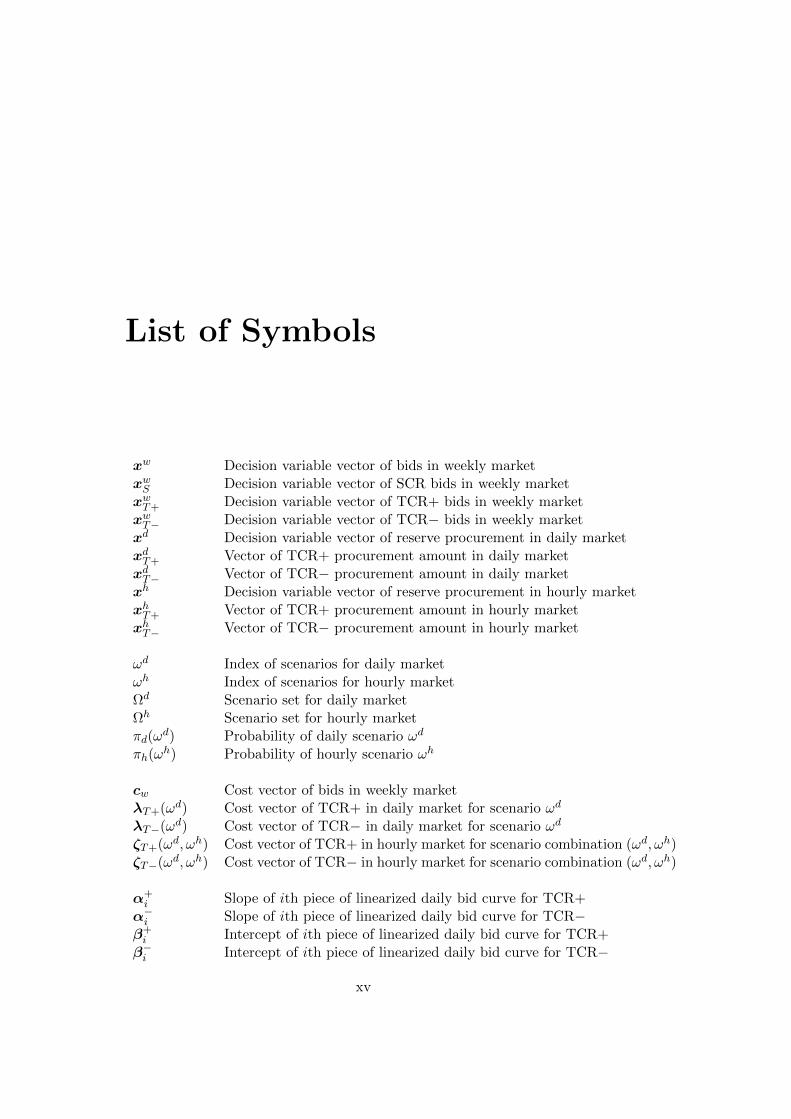

xw Decision variable vector of bids in weekly marketxwS Decision variable vector of SCR bids in weekly marketxwT+ Decision variable vector of TCR+ bids in weekly marketxwT− Decision variable vector of TCR− bids in weekly marketxd Decision variable vector of reserve procurement in daily marketxdT+ Vector of TCR+ procurement amount in daily marketxdT− Vector of TCR− procurement amount in daily marketxh Decision variable vector of reserve procurement in hourly marketxhT+ Vector of TCR+ procurement amount in hourly marketxhT− Vector of TCR− procurement amount in hourly market

ωd Index of scenarios for daily marketωh Index of scenarios for hourly marketΩd Scenario set for daily marketΩh Scenario set for hourly marketπd(ωd) Probability of daily scenario ωd

πh(ωh) Probability of hourly scenario ωh

cw Cost vector of bids in weekly marketλT+(ωd) Cost vector of TCR+ in daily market for scenario ωd

λT−(ωd) Cost vector of TCR− in daily market for scenario ωd

ζT+(ωd, ωh) Cost vector of TCR+ in hourly market for scenario combination (ωd, ωh)ζT−(ωd, ωh) Cost vector of TCR− in hourly market for scenario combination (ωd, ωh)

α+i Slope of ith piece of linearized daily bid curve for TCR+

α−i Slope of ith piece of linearized daily bid curve for TCR−β+i Intercept of ith piece of linearized daily bid curve for TCR+β−i Intercept of ith piece of linearized daily bid curve for TCR−

xv

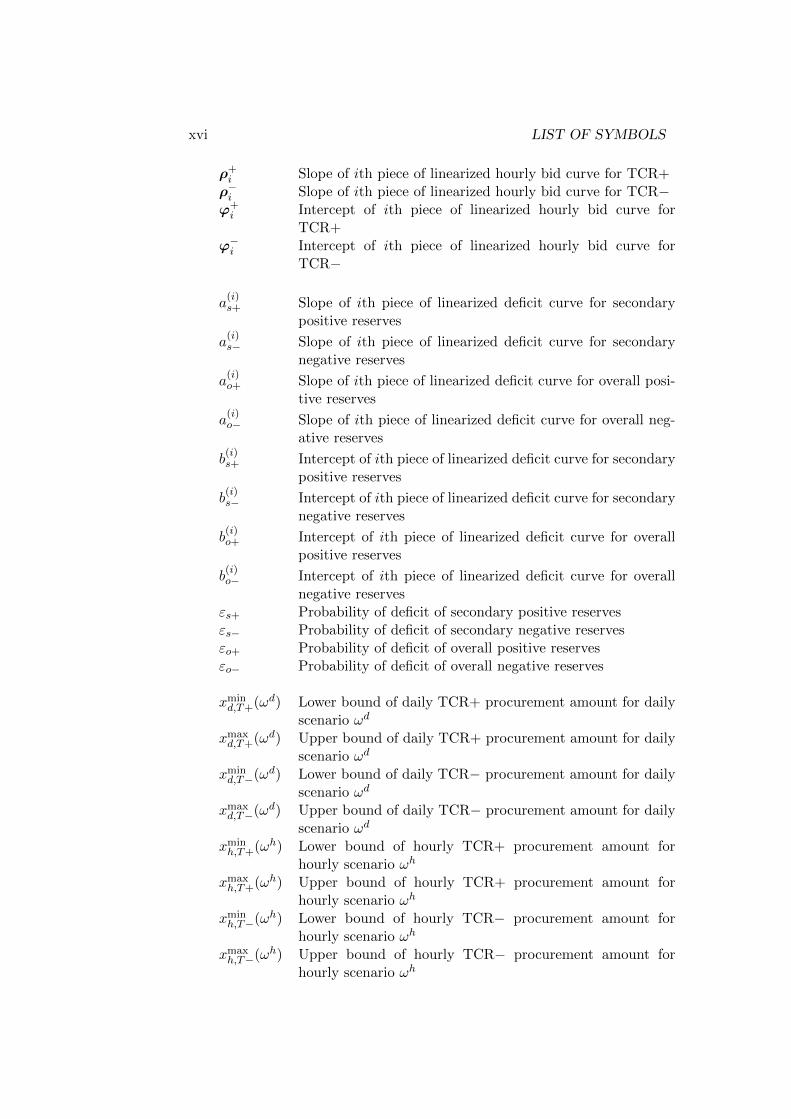

xvi LIST OF SYMBOLS

ρ+i Slope of ith piece of linearized hourly bid curve for TCR+ρ−i Slope of ith piece of linearized hourly bid curve for TCR−ϕ+

i Intercept of ith piece of linearized hourly bid curve forTCR+

ϕ−i Intercept of ith piece of linearized hourly bid curve forTCR−

a(i)s+ Slope of ith piece of linearized deficit curve for secondary

positive reserves

a(i)s− Slope of ith piece of linearized deficit curve for secondary

negative reserves

a(i)o+ Slope of ith piece of linearized deficit curve for overall posi-

tive reserves

a(i)o− Slope of ith piece of linearized deficit curve for overall neg-

ative reserves

b(i)s+ Intercept of ith piece of linearized deficit curve for secondary

positive reserves

b(i)s− Intercept of ith piece of linearized deficit curve for secondary

negative reserves

b(i)o+ Intercept of ith piece of linearized deficit curve for overall

positive reserves

b(i)o− Intercept of ith piece of linearized deficit curve for overall

negative reservesεs+ Probability of deficit of secondary positive reservesεs− Probability of deficit of secondary negative reservesεo+ Probability of deficit of overall positive reservesεo− Probability of deficit of overall negative reserves

xmind,T+(ωd) Lower bound of daily TCR+ procurement amount for daily

scenario ωd

xmaxd,T+(ωd) Upper bound of daily TCR+ procurement amount for daily

scenario ωd

xmind,T−(ωd) Lower bound of daily TCR− procurement amount for daily

scenario ωd

xmaxd,T−(ωd) Upper bound of daily TCR− procurement amount for daily

scenario ωd

xminh,T+(ωh) Lower bound of hourly TCR+ procurement amount for

hourly scenario ωh

xmaxh,T+(ωh) Upper bound of hourly TCR+ procurement amount for

hourly scenario ωh

xminh,T−(ωh) Lower bound of hourly TCR− procurement amount for

hourly scenario ωh

xmaxh,T−(ωh) Upper bound of hourly TCR− procurement amount for

hourly scenario ωh

Chapter 1

Introduction

This chapter unveils the background of this thesis. Key concepts involved arebalancing reserves and market for reserve procurement. Stochastic program-ming, the core methodology applied in this thesis, will be briefly introducedin Section 1.3. The framework of this thesis is then exhibited in Section 1.4.

1.1 Balancing Reserves

Power systems operate at a certain frequency, e.g. 50 Hz in Europe and amajority of countries in the world, and 60 Hz in the Americas and part ofAsia. It is important to maintain system frequency within a small range ofdeviation. On the one hand, large frequency deviations can damage equip-ment and affect load performance. On the other hand, if frequency dropstoo much, generation units might be disconnected from the grid by protec-tion devices, further enlarging frequency deviation. In worst cases, largefrequency fluctuations could possibly lead to interruption of power supplyand system collapse [7].

In most European countries, Transmission System Operators (TSOs)are responsible for the security of transmission system and coordinating thesupply of and demand for electrical energy to avoid frequency deviations.Generally, a surplus in generation shifts system frequency upwards, whilea deficit depresses it [7]. Therefore, in order to maintain constant systemfrequency, production and consumption of electricity have to be balancedinstantaneously and continuously.

However, demand forecast can never yield 100% precision. Forecast er-rors, sudden load changes and unforeseen generation incidents can causepower imbalances between supply and demand in the system. Under thecircumstances, TSOs have to deploy balancing energy to “fill the gap” be-tween supply and demand. Yet one of the most unique features of electricalenergy is that it cannot be stored. In order to ensure that there is sufficientenergy in real-time operation for the purpose of balancing, TSOs usually

1

2 CHAPTER 1. INTRODUCTION

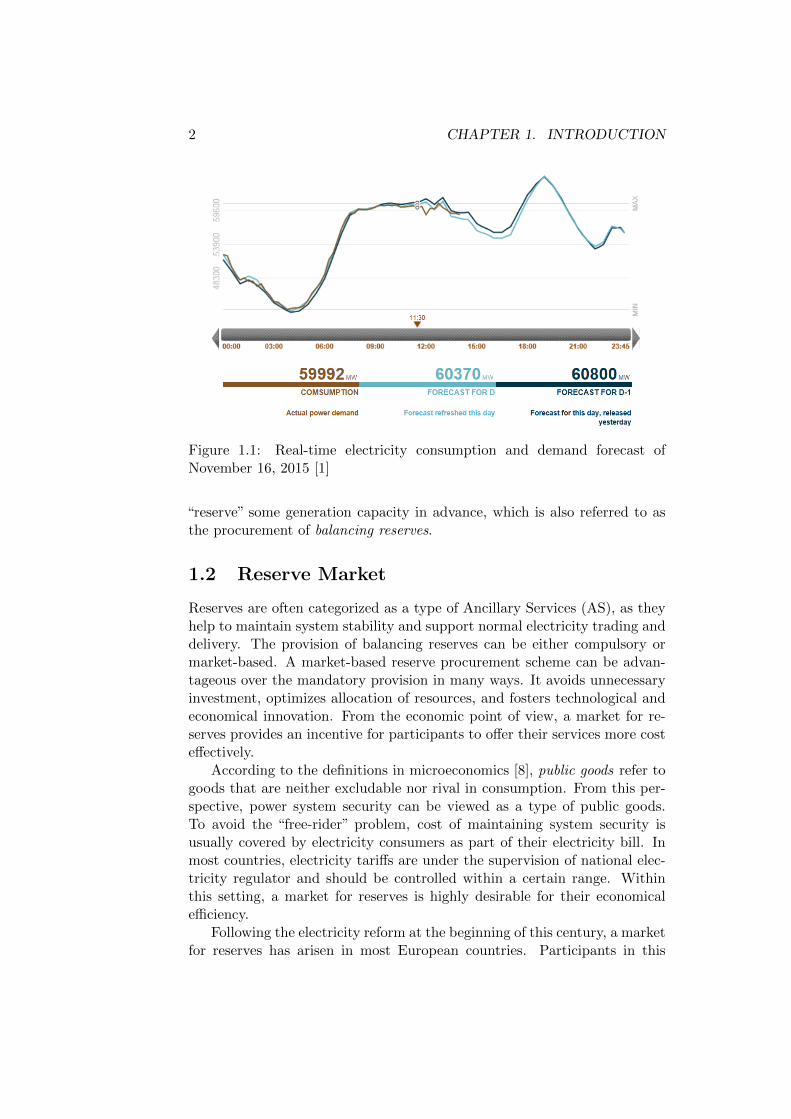

Figure 1.1: Real-time electricity consumption and demand forecast ofNovember 16, 2015 [1]

“reserve” some generation capacity in advance, which is also referred to asthe procurement of balancing reserves.

1.2 Reserve Market

Reserves are often categorized as a type of Ancillary Services (AS), as theyhelp to maintain system stability and support normal electricity trading anddelivery. The provision of balancing reserves can be either compulsory ormarket-based. A market-based reserve procurement scheme can be advan-tageous over the mandatory provision in many ways. It avoids unnecessaryinvestment, optimizes allocation of resources, and fosters technological andeconomical innovation. From the economic point of view, a market for re-serves provides an incentive for participants to offer their services more costeffectively.

According to the definitions in microeconomics [8], public goods refer togoods that are neither excludable nor rival in consumption. From this per-spective, power system security can be viewed as a type of public goods.To avoid the “free-rider” problem, cost of maintaining system security isusually covered by electricity consumers as part of their electricity bill. Inmost countries, electricity tariffs are under the supervision of national elec-tricity regulator and should be controlled within a certain range. Withinthis setting, a market for reserves is highly desirable for their economicalefficiency.

Following the electricity reform at the beginning of this century, a marketfor reserves has arisen in most European countries. Participants in this

1.3. STOCHASTIC PROGRAMMING 3

market can be pre-qualified power plants, industrial consumers or possiblysomeone providing demand side response. TSOs are normally the sole buyerin this market. The demand is determined by dimensioning criteria set byENTSO-E and TSO. Depending on different market setup, providers withaccepted bids are reimbursed either at their bid price (pay-as-bid) or theprice of the last accepted bid (market-clearing price).

The operation of reserve market is usually separated into two steps: di-mensioning and procurement. Traditionally, TSOs complete these two stepsin a sequential order, i.e. first determine the demand using dimensioningcriteria and then procure the fixed amount in the market. In Germany,for example, reserves are dimensioned using probabilistic criteria and thenecessary amount is published every three months for the next quarter [9].Afterwards, a tender auction process for the fixed demand will take place,in which bids with the most attractive offering price will be awarded.

While this traditional approach obeys the security criteria, it neglectsthe temporal coupling between different market stages and potential sub-stitution between different types of reserves by unlinking dimensioning andprocurement [4], which results in overly conservative procurement decisions.In [4], a new market-clearing approach for reserve market is proposed. Thisnew approach is a two-stage stochastic market-clearing model based on thestructure of the Swiss reserve market and has been implemented since Jan-uary 2014. The economic saving of this new approach is estimated to bearound 12 million Swiss francs (CHF) in 2014.

1.3 Stochastic Programming

Stochastic programming is a model for optimization under uncertainty. Ingeneral, stochastic programming incorporates a wide range of problems: two-stage recourse problems, multi-stage stochastic problems, stochastic integerprograms, chance-constrained programs, etc. [10], of which the first one ismost widely studied and applied. This thesis is based on a two-stage recourseproblem, and extends it to a three-stage stochastic problem.

In a two-stage or three-stage stochastic programming problem, multipledecisions are made as we progress in time, with more information on theunknown parameter being disclosed. Here, uncertainty is represented by afinite number of input data, which can be random variables or stochasticprocesses. The objective function is formulated as the sum of individualsolutions of each set of input data weighted by the corresponding probabilityfactor. Hence, instead of optimizing deterministic objective functions, theexpected value of objective function (if not risk-averse) is optimized. Thefinal solution is therefore the best solution for all sets of input data, but notfor each individual scenario particularly [11].

Some common terminologies in stochastic programming are explained

4 CHAPTER 1. INTRODUCTION

below [10,11]:

• Stage: a point in time where a new decision has to be made with achange in uncertainty.

• Here-and-now decisions: decisions made without any realization ofuncertain information.

• Wait-and-see decisions: decisions made after uncertainty has totallyor partially unfolded.

• Recourse action: additional actions possible in second or further stageswhen uncertainty reveals.

• Scenarios: a set of data representing stochastic processes spanninga given time horizon. For instance, if λ is the hourly electricityprice of next week (168 hours), λ can be represented by NΩ scenariosλ(1), · · · ,λ(ω), · · · ,λ(NΩ), each with a length of 168×1 and occurringwith a probability of π(ω), where ω is the scenario index.

• Scenario tree: a graphical demonstration of scenarios. A node is apoint where a decision has to be made. A node can be succeeded bymultiple nodes and can be traced back to only one node. The numberof nodes at each stage is equal to the number of scenarios at this stage.There is only one node at first stage, which is named root. A branchcorresponds to a “path” from the first-stage node to a final-stage node,which represents a realization of the random variables.

Figure 1.2: Example of a scenario tree for three-stage problems

1.4. STRUCTURE OF THE THESIS 5

In recent years, there has been a growing trend of real-world applicationsof stochastic programming. Examples are especially concentrated in thefields of finance and energy [12]. The application of three-stage stochasticprogramming in electricity market is generally focused on maximizing theprofits of power producers in multi-stage trading activities [13–15]. Researchon reserve market-clearing using stochastic programming models is mostlyconducted under the setting of a centralized market where reserve and energyare jointly cleared [16,17]. These approaches are, however, not applicable forthe market design in Europe, where energy trading is separated from reservemarket operation. To our knowledge, Swiss reserve market is one of the onlyreal-world implementations of a stochastic market-clearing model reportedso far [4]. The idea of further extending it to a three-stage stochastic market-clearing model is thus novel as well.

1.4 Structure of the Thesis

The main objective of this thesis is to develop a three-stage stochasticmarket-clearing model for the Swiss reserve market. This market-clearingmodel can be adapted to future reserve market design in Switzerland, wherepower plants may be requested to offer all or part of their remaining genera-tion capacity close to real-time for the purpose of balancing. An alternativeapplication can be based on current market design in situations where plentyof balancing energy bids are received without a priori accepted reserve bids.

The contributions of this thesis are twofold:

1. Scenarios for current two-stage stochastic market-clearing model areinvestigated and improved, mainly from the aspects of scenario mod-elling and scenario selection method. The improvements are simulatedwith real market data and can be readily implemented in current Swissreserve market.

2. A three-stage stochastic market-clearing model for Swiss reserve mar-ket is proposed, which is so far novel in applications of stochasticprogramming. Based on analysis of current market reference data,scenarios for third stage are created in order to simulate possibilitiesin future Swiss reserve market.

Therefore, the thesis is organized as follows:Chapter 2 opens with an overview of ancillary services in Switzerland

and the organization of their procurement. The focus is then shifted to themarket design of secondary and tertiary control reserves. Explanations onbid structure, dimensioning criteria and remuneration scheme follow.

Chapter 3 presents the current two-stage stochastic market-clearing model.Formulation of the model is depicted in Section 3.2, while Section 3.3 ex-hibits improvements on scenarios used in the two-stage model.

6 CHAPTER 1. INTRODUCTION

In Chapter 4, formulation of the three-stage stochastic market-clearingmodel is illustrated, followed by explanations on modelling and selectionmethod of third-stage scenarios in Section 4.3. Then, simulations regardingthe three-stage model are run and results are presented.

Chapter 5 covers the conclusion and the outlook of this project.

Chapter 2

Reserve Market inSwitzerland

In this chapter, the Swiss ancillary services market is presented. The focuswill be specially on the procurement of frequency control reserves. Marketstructure, bid structure, dimensioning criteria and remuneration scheme ofreserve market will be explained in Sections 2.3, 2.4, 2.5 and 2.6 respectively.

2.1 Self-scheduling Market

In most European countries, wholesale trading of electricity is separatedfrom dispatch by TSOs. This type of market design is named self-schedulingmarket, or decentralized market, as opposed to centralized market in NorthAmerica. Switzerland belongs to one of these countries.

In a self-scheduling market, generation schedule of each power plant isdetermined on their own based on their economic interest. In most cases,these schedules are based on results from bilateral, day-ahead and intradaypower trading. Schedules are submitted to TSOs after trading closes. TSOswill only intervene when there is a need for balancing or when securitycriteria are violated. In such cases, TSO will deploy Ancillary Services (AS)to ensure system security and reliability.

In Switzerland, connection between energy markets and TSO (Swissgrid)is established through Balance Group (BG) model [18]. A balance group isa virtual aggregation of several feed-in and feed-out points. Energy transac-tions are carried out by each BG as an entity. After transaction closes, BGsare obliged to deliver their schedules to Swissgrid. Meanwhile, Swissgridbalances the production and consumption within the entire Swiss network.However, due to forecast errors and inexacts, actual delivery of energy islikely to deviate from schedules, creating imbalances in the system (a.k.a.balance energy). The settlement of balance energy is a two-price systemdepending on the direction of discrepancy. The prices are usually unfavor-

7

8 CHAPTER 2. RESERVE MARKET IN SWITZERLAND

able to BGs as a measure to discourage such discrepancies. Formula forcalculating imbalance settlement price can be found in [18]. The prices arecalculated by Swissgrid and posted on Swissgrid’s website every month.

2.2 Overview of Ancillary Services

As national TSO, Swissgrid guarantees the secure and reliable operation ofpower system with the help of ancillary services from providers. Ancillaryservices organized by Swissgrid primarily include frequency control, volt-age support, compensation of active power losses and black start [3], whichare explained below. The main focus of this thesis is on frequency controlreserves.

Frequency Control

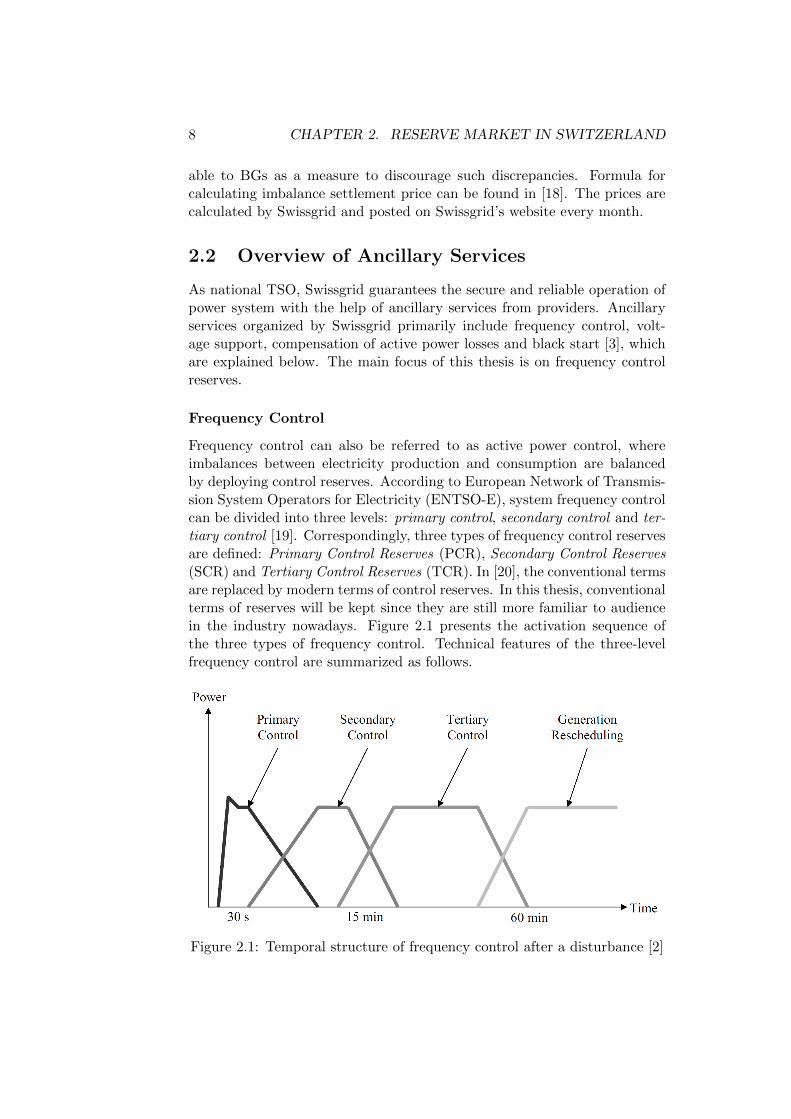

Frequency control can also be referred to as active power control, whereimbalances between electricity production and consumption are balancedby deploying control reserves. According to European Network of Transmis-sion System Operators for Electricity (ENTSO-E), system frequency controlcan be divided into three levels: primary control, secondary control and ter-tiary control [19]. Correspondingly, three types of frequency control reservesare defined: Primary Control Reserves (PCR), Secondary Control Reserves(SCR) and Tertiary Control Reserves (TCR). In [20], the conventional termsare replaced by modern terms of control reserves. In this thesis, conventionalterms of reserves will be kept since they are still more familiar to audiencein the industry nowadays. Figure 2.1 presents the activation sequence ofthe three types of frequency control. Technical features of the three-levelfrequency control are summarized as follows.

Figure 2.1: Temporal structure of frequency control after a disturbance [2]

2.2. OVERVIEW OF ANCILLARY SERVICES 9

1. Primary Frequency ControlThe purpose of primary frequency control is mainly to stabilize systemfrequency after a disturbance at steady state. Full activation time isusually 30 seconds after disturbance in Continental Europe [21]. Pri-mary frequency control is activated through automatically adjustingsetpoints for frequency and power at a local generator and is thereforedecentralized control. Since this type of control is purely proportional,it merely prevents system frequency from further deviating, but can-not restore frequency to normal value. All online generators shouldbe technically available for the provision of primary frequency controlthrough installation of speed governors [2]. Some frequency sensitiveloads such as induction motors also participate in this control by coun-teracting frequency deviations [22,23].Primary control reserves are also known as Frequency ContainmentReserves (FCR). In the synchronous area of Continental Europe, theoverall amount of primary control reserve is 3000 MW [19]. Thisamount is shared between member states and the demand in eachcountry is designated by European Network of Transmission SystemOperators for Electricity (ENTSO-E) every year.

2. Secondary Frequency ControlSecondary frequency control is also referred to as Automatic Gener-ation Control (AGC) or Load Frequency Control (LFC). Secondarycontrol is activated to restore system frequency and power exchangesbetween areas in case of frequency noises under normal operation or af-ter a large incident. The activation of secondary control usually starts30 seconds after the disturbance and is completed within 15 minutesat the latest [19]. In contrast with primary control, secondary controlcan be regarded as a type of centralized control. However, only gen-erators in the control area where frequency disturbance occurred willparticipate in this control.In modern terms of ENTSO-E, secondary control reserves are cate-gorized into Frequency Restoration Reserves (FRR), or more specif-ically, automatic Frequency Replacement Reserves (aFRR), as somedocuments indicate [24]. Secondary control reserves can also releaseprimary control reserves as they can sustain for longer periods.

3. Tertiary Control ReservesThe purpose of tertiary control is usually twofold: to assist secondarycontrol reserve to recover system frequency and to replace primaryand secondary control reserves. The activation of tertiary frequencycontrol is manual, in the forms of calls from local TSO. After receiving

10 CHAPTER 2. RESERVE MARKET IN SWITZERLAND

the activation signal, power plant operators will adjust the setpointvalues of power output manually. In some countries, tertiary controlis also activated for the purpose of managing congested lines, which isoften referred to as re-dispatch.According to modern ENTSO-E definitions, fast tertiary control re-serves (those can be fully activated within 15 minutes) are groupedinto Frequency Restoration Reserves (FRR), or more specifically man-ual Frequency Restoration Reserves (mFRR), while slower units par-ticipate as Replacement Reserves (RR) (activation time can be from15 minutes up to 1 hour).

Voltage Support

In power systems analysis, voltage at each node is usually coupled with theexchange of reactive power. Maintaining certain voltage level is also crucialin system operation, since large deviations will cause damages to electri-cal equipment and further jeopardize system security. Therefore, as TSO,Swissgrid should ensure that voltage at each node remains in an acceptablerange.

Voltage support is mainly realized by reactive power control. Unlikeactive power, reactive power cannot be transmitted. Thus, reactive powercontrol is rather local [2].

So far, there is no tendering process for reactive power in Switzerland.All power stations online must provide a certain volume of reactive powerin order to keep the voltage within the range indicated by Swissgrid. Theexchanged reactive energy is remunerated at a fixed rate (CHF/Mvarh) [25].

Compensation of Active Power Losses

Resistance in power transmission lines inevitably leads to losses of activepower. These energy losses must be compensated in the network in order todeliver the desired amount of energy to end-consumers. In Switzerland, thetendering process for active power losses and inadvertent deviations takesplace once per month. Any balance group in the Swiss control area can par-ticipate and compensated energy will be remunerated at its bid price basedon exchange schedules [5].

Black Start and Island Operation

Black start refers to the ability of power generators to start operating with-out the need for power injection from the grid. Island operation is thecapability of a power station to operate continuously without requiring anyconnection to the synchronous grid. Both services are guarantees for the

2.3. STRUCTURE OF RESERVE MARKET 11

restoration of power grid after large incidents. Currently, the provision ofblack start and island operation services is secured via bilateral agreementbetween the provider and Swissgrid [25].

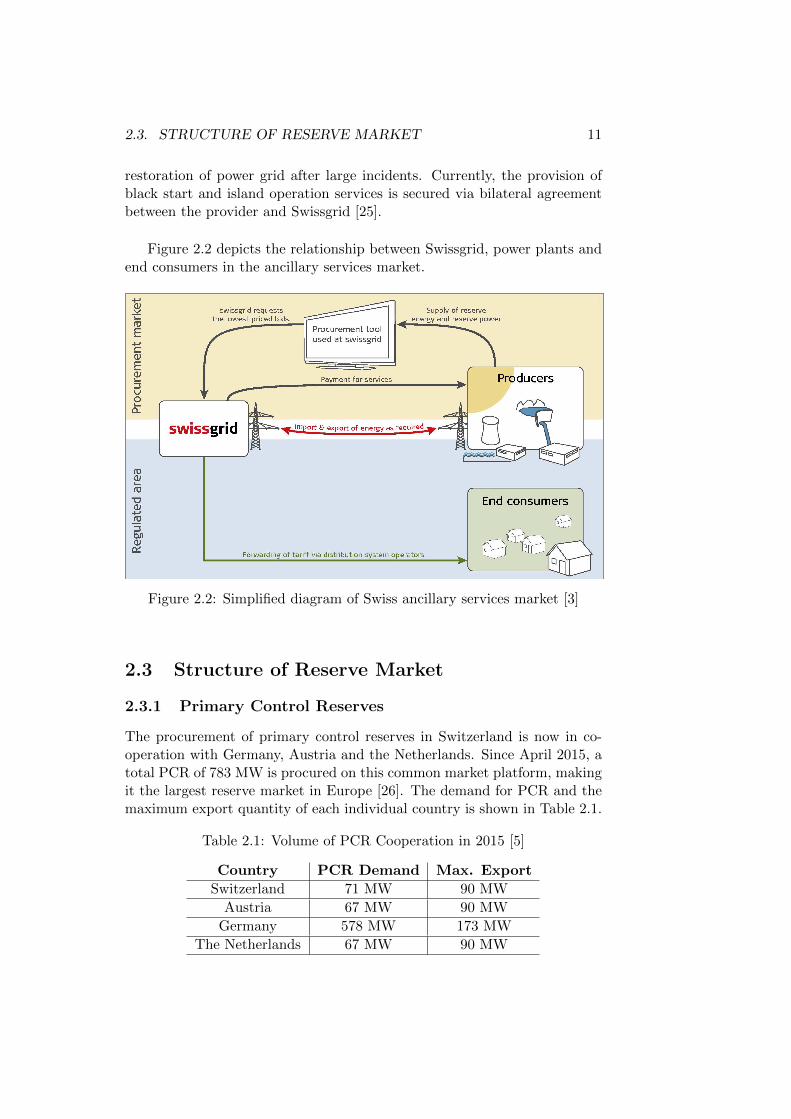

Figure 2.2 depicts the relationship between Swissgrid, power plants andend consumers in the ancillary services market.

Figure 2.2: Simplified diagram of Swiss ancillary services market [3]

2.3 Structure of Reserve Market

2.3.1 Primary Control Reserves

The procurement of primary control reserves in Switzerland is now in co-operation with Germany, Austria and the Netherlands. Since April 2015, atotal PCR of 783 MW is procured on this common market platform, makingit the largest reserve market in Europe [26]. The demand for PCR and themaximum export quantity of each individual country is shown in Table 2.1.

Table 2.1: Volume of PCR Cooperation in 2015 [5]

Country PCR Demand Max. Export

Switzerland 71 MW 90 MW

Austria 67 MW 90 MW

Germany 578 MW 173 MW

The Netherlands 67 MW 90 MW

12 CHAPTER 2. RESERVE MARKET IN SWITZERLAND

In this common market, power plants from all four countries can submittheir bids into the pool. The tender call takes place every Tuesday afternoon[26]. After gate closure, the market will be cleared and those bids with lowestprice will be accepted, regardless of their geographical location (providedthat the maximum export quantity of each country is not exceeded). Theprocured PCR will be utilized across the four participating countries.

2.3.2 Secondary and Tertiary Control Reserves

SCR and TCR are procured together in a national reserve market in Switzer-land. This reserve market is the main focus of this thesis.

Currently, SCR is procured on a weekly basis, whereas the procurementof TCR is split between a weekly auction and daily auction. Figure 2.3illustrates the scheme of the two-stage Swiss reserve market.

Figure 2.3: Scheme of a two-stage reserve market in Switzerland [4]

Weekly Market

The weekly auction for SCR and TCR is closed every Tuesday afternoonat 13:00 [27], before the gate closure of PCR market. At this stage, ASproviders who are willing to participate in this market will submit their bidsfor SCR and/or TCR into system. The bids in the weekly market must bevalid for a horizon of the whole week, i.e. 168 hours.

2.4. BID STRUCTURE 13

Daily Market

TCR can also be procured from a daily market, which provides power plantswith more flexibility. In a daily market, there are six auctions, each of themcomprising a 4-hour block. Power plants can bid for any of these blocks.Accepted bids must be available for a duration of 4 hours.

Traditionally, the share of reserves in the weekly and daily market is de-termined prior to the tender call. However, this approach does not allow anyflexibility in the amount procured in weekly and daily market, hence leadingto higher procurement costs. The stochastic approach, on the other hand,takes into account options from both markets and finds the optimal solution,i.e. the procurement combination with the lowest cost. This approach willbe elaborated in Section 3.2.

2.4 Bid Structure

In weekly and daily market, bidding rules are listed in Table 2.2. Someexplanations of Table 2.2 are also listed below.

Table 2.2: Bid structure of the Swiss reserve market [5]

Type of Control SCR TCR

Symmetry Symmetrical Asymmetrical

Offer Size 50 MW/Bid 100 MW/Bid

Min. Output Window ±5 MW +5 MW or -5 MW

Conditional Bids Allowed, min. volume increment is ±1 MW

• Symmetry refers to the symmetry of provided control power bands.For the time being, SCR is a symmetrical product, which requires an-cillary services provider to hold the reserved capacity available for bothupward and downward regulation. TCR, however, is non-symmetrical.Ancillary services providers will have to specify whether they bid forupward or downward regulating capacity. TCR+ refers to upwardtertiary control reserve, whereas TCR− refers to downward tertiarycontrol reserve thereafter.

Illustrative Example: Figure 2.4 shows two options of a generator withmaximum generation capacity Pmax = 100 MW and technical mini-mum Pmin = 10 MW. The planned production is Pplan = 60 MW. Ifthe generator participates in SCR provision (left bar), it has to pro-vide a power band of ±40 MW, which means it is capable of adjustingits power output by max. 40 MW both upwards and downwards uponcall. If it plans to offer all its remaining capacity to TCR market (rightbar), it will be able to bid for 40 MW TCR+ and an additional 60MW of TCR−.

14 CHAPTER 2. RESERVE MARKET IN SWITZERLAND

Figure 2.4: Example of SCR and TCR provision

• Offer Size means the maximum volume of a bid.

• Minimum Output Window is namely the minimum volume of each bid.

• Conditional Bids are bids which allow different price/volume combi-nations. Minimum volume increment is the resolution of these combi-nations. More details will be explained in Section 2.4.2.

2.4.1 Indivisible Bids

In current design of Swiss reserve market, bids are not divisible. This meansthat a bid can either be rejected or accepted. There is no such result thata bid is partially accepted or split. As a result, decision variables for eachindividual bid are binary variables as such:

ξ(i) =

1, bid i is accepted

0, bid i is rejected

Illustrative Example: Assume that there are four bids in the pool and totaldemand for reserve capacity is 100 MW.

In this illustrative example, if we select bids purely based on the meritorder of bid prices, Bids #1 and #2 will be selected. Since Bid #2 cannotbe split to match the total demand, the total cost in this case will be:50 × 5 + 70 × 6 = 670 CHF. Instead, if bids #1 and #3 are accepted, thetotal cost will be: 50× 5 + 50× 7 = 600 CHF.

Therefore, from the perspective of minimizing total cost, the secondcombination of Bids (#1 and #3) is more favorable than the first (#1 and#2), although the unit price of Bid #2 is lower than Bid #3.

2.5. DIMENSIONING CRITERIA 15

Table 2.3: Example bids for demonstration of indivisibility

Bid #Volume

[MW]Price

[CHF/MW]

1 50 5

2 70 6

3 50 7

4 80 8

2.4.2 Conditional Bids

Conditional bids are a set of mutually exclusive bids of which only one canbe accepted by TSO. This type of bid offers providers the opportunity ofbidding various price/volume combinations.

Illustrative Example: In Table 2.4, bids with identical bid ID and from thesame provider are recognized as a set of conditional bids. In this case, bids#1, #2, #3 are a set of conditional bids submitted by Provider A, whilebids #6, #7 are another set of conditional bids submitted by Provider B.Bid #4 is another non-conditional bid from Provider A. Bid #5 is a non-conditional bid from Provider B. Bids #1, #2, #3 as well as #6, #7are mutually exclusive, meaning that at most one of the bids within the setcan be accepted. The acceptance of Bids #1, #2, #3 and #6, #7,however, does not have any influence on any other bids such as Bids #4 and#5.

Table 2.4: Example of conditional bids

Bid # Provider Bid IDVolume

[MW]Price

[CHF/MW]

1 A 1 10 9

2 A 1 30 7.5

3 A 1 50 6

4 A 2 50 5.5

5 B 1 20 8

6 B 2 10 7

7 B 2 30 6.5

2.5 Dimensioning Criteria

Dimensioning criteria are applied to determine the adequate amount of re-serve in a system. According to Continental Europe Operation Handbookby ENTSO-E [19], there are mainly two methods of dimensioning secondary

16 CHAPTER 2. RESERVE MARKET IN SWITZERLAND

and tertiary control reserves: probabilistic approach and deterministic ap-proach. In Switzerland, criteria for dimensioning reserves are a hybrid ofprobabilistic and deterministic approach [4].

2.5.1 Probabilistic Approach

The probabilistic approach of dimensioning reserves is based on the rec-ommendation by ENTSO-E that the Area Control Error (ACE) has to beregulated to zero in a certain amount of hours within a year [19]. The per-centage of hours is not strictly specified by ENTSO-E and can be determinedby each TSO individually. Switzerland, for example, requires that ACE shallbe smoothened to zero in 99.8% of all hours during a year. In other words,the deficit of reserves should not occur with a probability of more than0.2% [4], which can also be interpreted as the deficit rate of reserves.

To determine the deficit rate of reserves, cumulative probability distribu-tion curves of power imbalances (deficit curve) are used. The deficit curvenormally takes into account all possible causes of failures, forecast errorsand fluctuations of Renewable Energy Sources (RES).

In Switzerland, two sets of deficit curves are built with respect to thedimensioning of secondary reserves solely and total amount of secondaryand tertiary reserves respectively. For the former curve, AGC signals andremaining ACE are aggregated to form spontaneous power imbalance ∆Ps,which is expected to be compensated by secondary reserves. The latter curveconsiders AGC signals, remaining ACE as well as activated tertiary reserves,which yields to the so-called open-loop ACE, or overall power imbalance ∆Po.This open-loop ACE will be covered by the sum of secondary and tertiarycontrol reserves. Figure 2.5 demonstrates the deficit curves for dimensioningsecondary and overall reserve amount in Switzerland.

Figure 2.5: Deficit curves for dimensioning reserves in Switzerland [4]

2.6. REMUNERATION SCHEME 17

2.5.2 Deterministic Approach

The deterministic approach of sizing reserves recommended by ENTSO-Eis based on the largest possible generation incident, which includes powerplant outage, tripping of power lines, and so on [19]. In Switzerland, thelargest power generation incident is the outage of the nuclear power plantLeibstadt, whose installed capacity is 1250 MW [4]. Hence, the total amountof reserves to prevent further incident under this circumstance should be atleast 1250 MW.

Meanwhile, Switzerland also has contractual Mutual Emergency Assis-tance Service (MEAS) with neighboring countries. This type of contractguarantees the availability of maximum 400 MW reserve given that Switzer-land holds the same amount of reserve ready at the same time, which adds upto 800 MW positive reserves. Since the amount of SCR procured is empiri-cally around 400 MW, the deterministic criteria of securing supply in case oflargest power plant outage and MEAS contract can be altogether convertedto procuring 400 MW of TCR+ for MEAS contract at the moment [4].

2.6 Remuneration Scheme

2.6.1 Remuneration of Capacity

After bids are accepted in the reserve market, corresponding ancillary ser-vice providers will be remunerated for holding the accepted reserve capacity.This remuneration is based on the bid price of the capacity (pay-as-bid). Es-sentially, bid price should reflect the opportunity cost of holding the reservesinstead of selling the produced electricity on the spot market. Since the ma-jority of ancillary services providers in Switzerland is hydro power plantowners, this payment also implies the value of water in the reservoir [28].

2.6.2 Remuneration of Energy

The remuneration scheme of activated secondary and tertiary energy can bedifferent, due to the way they are deployed and some historical reasons.

Secondary Control

The activation of SCR is triggered automatically and centrally after ACEexceeds a certain limit. The amount of activated SCR in each balance groupis calculated ex post and is usually proportional to the amount of reservecapacity it has been accepted in the reserve market. Since activation ofSCR does not require any manual dispatch from TSO, it is remunerated ata flat rate coupled with spot market price. Detailed remuneration rate canbe found in Table 2.5.

18 CHAPTER 2. RESERVE MARKET IN SWITZERLAND

Table 2.5: Remuneration of activated SCR [5]

Direction Upward Downward

Price SwissIXa +20%b SwissIX −20%c

Cash Flow Swissgrid → Bidder Bidder → Swissgrid

Energy Flow Bidder → Swissgrid Swissgrid → Bidder

aHourly price index for Swiss day-ahead auction in EPEX Spot Marketbat least weekly basecat most weekly base

Tertiary Control

In contrast with SCR, TCR is deployed manually. When a dispatcher in shiftobserves continuous power imbalance that needs to be balanced, he/she willmanually call ancillary services providers to activate their tertiary control.The lead time is currently 15 minutes in Switzerland.

For this reason, an separate market for Tertiary Control Energy (TCE)arises to allow ancillary services providers to bid for the regulating energythey provide. Providers with TCR bids accepted in the reserve market mustsubmit energy bids to TCE market. Apart from compulsory bids, additionalenergy can also be offered voluntarily without previously accepted reservebids [5]. Dispatchers will activate TCE based on demand and Merit OrderList (MOL). Bids with lowest price will be activated first. Currently, pay-ment of activated tertiary energy is calculated based on activated amountand bid price.

Chapter 3

Two-Stage Market-ClearingModel

This chapter focuses on the current two-stage stochastic market-clearingmodel and the formulation of the model. Contributions of this thesis areinvestigation and improvement of second-stage scenarios used in this two-stage model. These improvements result in higher accuracy of predictingbidding behavior in daily market using historical data and thus decrease to-tal procurement cost.

3.1 Background

As is briefly stated in Sections 1.2 and 2.3, traditional reserve procure-ment process decouples dimensioning from procurement and neglects thelink between weekly and daily market. By introducing a two-stage stochas-tic market-clearing model, dimensioning and procurement are coupled, andsubstitution between weekly and daily products is also enabled. The chiefobjective is to minimize total expected procurement cost while respectingall constraints.

Figure 3.1 illustrates the decision-making model of this two-stage mar-ket. Weekly market is cleared once per week. At this point in time, adecision on the procurement in weekly market has to be made with onlyweekly bids available. It is still uncertain how market participants will bidin daily market. Unknown daily bids are therefore modelled by a finitenumber of scenarios, each representing a possible set of inputs with a givenprobability. Based on these daily scenarios and known bids from the weeklyauction, weekly procurement decision is made with regard to weekly bids tobe accepted and suggested amount of reserve to be procured in daily mar-ket. After the two-stage clearing of weekly market, results are then passedonto the daily market, where daily bids are received. At this stage, a de-terministic market-clearing process is carried out with actual daily bids and

19

20 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

Figure 3.1: Two-stage stochastic market-clearing scheme

procurement results from previous stage.In the context of this thesis, first stage refers to weekly market, and

second stage refers to daily market. In this chapter, only the two-stagestochastic model for weekly market clearing will be elaborated. The deter-ministic clearing model for daily market is a simple optimization problembased on given bids.

3.2 Stochastic Market-Clearing Model

This section will introduce the formulation of the two-stage stochastic pro-gramming model for current reserve market. The objective of this opti-mization problem is to minimize expected total cost of procurement of allscenarios. Constraints include bidding behavior of known market stages,probabilistic and deterministic dimensioning criteria, etc. An overview ofthe optimization model is presented in Equation (3.1).

min expected total procurement cost

s.t. conditional bids in weekly marketprobabilistic dimensioning criteriadeterministic dimensioning criteria

(3.1)

Please note that bids are usually submitted by BGs (portfolio-based)instead of a specific power plant (unit-based). Thus, this model does notinclude any power flow and power balance equations. The selection of bidsis purely based on bid price and bid volume.

Components of this optimization problem will be built step by step inSections 3.2.1, 3.2.2 and 3.2.3. The complete model will be presented againas a whole in Section 3.2.4.

3.2. STOCHASTIC MARKET-CLEARING MODEL 21

3.2.1 Decision Variables

In this two-stage stochastic programming problem, there are two differentdecision variable vectors, each representing a stage.

First-Stage Decision Variables

Considering different products in the weekly reserve market, the decisionvariable vector of first stage consists of three components:

xw = [xwS ,x

wT+,xw

T− ], (3.2)

where

• xw ∈ ΥNw×1 is the decision variable vector of bids in weekly market

• xwS ∈ ΥNw

S ×1 is the decision variable vector of SCR bids in weeklymarket

• xwT+∈ Υ

NwT+×1

is the decision variable vector of TCR+ bids in weeklymarket

• xwT−∈ ΥNw

T−×1 is the decision variable vector of TCR− bids in weeklymarket

• Υ = 0, 1 is the set of binary variables indicating acceptance andrejection of a bid

• NwS is the number of SCR weekly bids

• NwT+

is the number of TCR+ weekly bids

• NwT−

is the number of TCR− weekly bids

• Nw = NwS + Nw

T++ Nw

T−is the total number of bids in the weekly

market (including SCR, TCR+ and TCR−)

As real bids from the weekly market are considered in this model, theindivisibility of bids should preserved in the decision-making process. Thisfeature can be interpreted as binary decision variables for weekly bids, as isalready discussed in Section 2.4.1.

In case of conditional bids, each single bid within the set of conditionalbids will still be counted as one bid and is assigned with a binary variable.An additional constraint is added to ensure the property of conditional bids,which will be explained in Section 3.2.3.

22 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

Second-Stage Decision Variables

In the second stage, a finite number of scenarios are constructed in orderto model the uncertainty. For each daily scenario ωd, an individual second-stage decision variable vector xd(ωd) is assigned:

xd(ωd) = [xdT+

(ωd),xdT−(ωd)], (3.3)

where

• ωd ∈ Ωd is the index of scenarios for daily market

• Ωd contains NdΩ scenarios for daily market

• xdT+

(ωd) ∈ R42×1 is the amount of TCR+ to be procured in daily

market in each 4-hour time block for scenario ωd

• xdT−

(ωd) ∈ R42×1 is the amount of TCR− to be procured in the daily

market in each 4-hour time block for scenario ωd

In the second stage, TCR market is cleared for each 4-hour time block.Since the results from two-stage market clearing are valid for one week (24×7 = 168 hours), length of second-stage parameters and variables is often168/4 = 42, which corresponds to 42 time blocks in a week.

3.2.2 Objective Function

The objective of this optimization model is to minimize expected procure-ment cost. The total cost can be calculated as the sum of first-stage cost(deterministic cost of weekly market) and second-stage cost (expected valueof daily costs with respect to different scenarios):

min Λw + E[Λd(ωd)],

∀ωd ∈ Ωd,(3.4)

where Λw is the total procurement cost in the weekly market and Λd(ωd)is the total procurement cost in the daily market for the given week withinput data of scenario ωd. E[Λd(ωd)] is the expectation of daily procurementcosts in all scenarios.

First-Stage Cost Function

Since the first stage of this problem is deterministic, cost incurred in theweekly market is calculated as the cumulative cost of accepted bids:

Λw = cᵀwxw = (κ · p)ᵀxw (3.5)

where

3.2. STOCHASTIC MARKET-CLEARING MODEL 23

• cw ∈ RNw×1 is the cost vector of all weekly bids

• κ ∈ RNw×1 is a vector containing unit prices (CHF/MW) of each bid

• p ∈ RNw×1 = [pS ,pT+ ,pT− ] is a vector consisting of volume (MW) ofeach bid

• pS is a vector consisting of volume (MW) of each SCR bid

• pT+ is a vector consisting of volume (MW) of each TCR+ bid

• pT− is a vector consisting of volume (MW) of each TCR− bid

Second-Stage Cost Function

To render the computation time affordable for real market clearing, thisstochastic programming problem is limited to a Mixed Integer Linear Pro-gramming (MILP) problem. Therefore, all components are to be linearized.To model daily costs, bid curves are derived from actual bids and then lin-earized via the following steps:

1. For each 4-hour time block, bids are obtained for TCR+ and TCR−respectively.

2. As for conditional bids, the bid with minimum price within the set isselected to represent this set. If there are multiple bids with the sameminimum price, the one with the largest quantity is chosen.

3. Bids are sorted in ascending order according to their bid prices.

4. Cumulative volume and cost are calculated respectively.

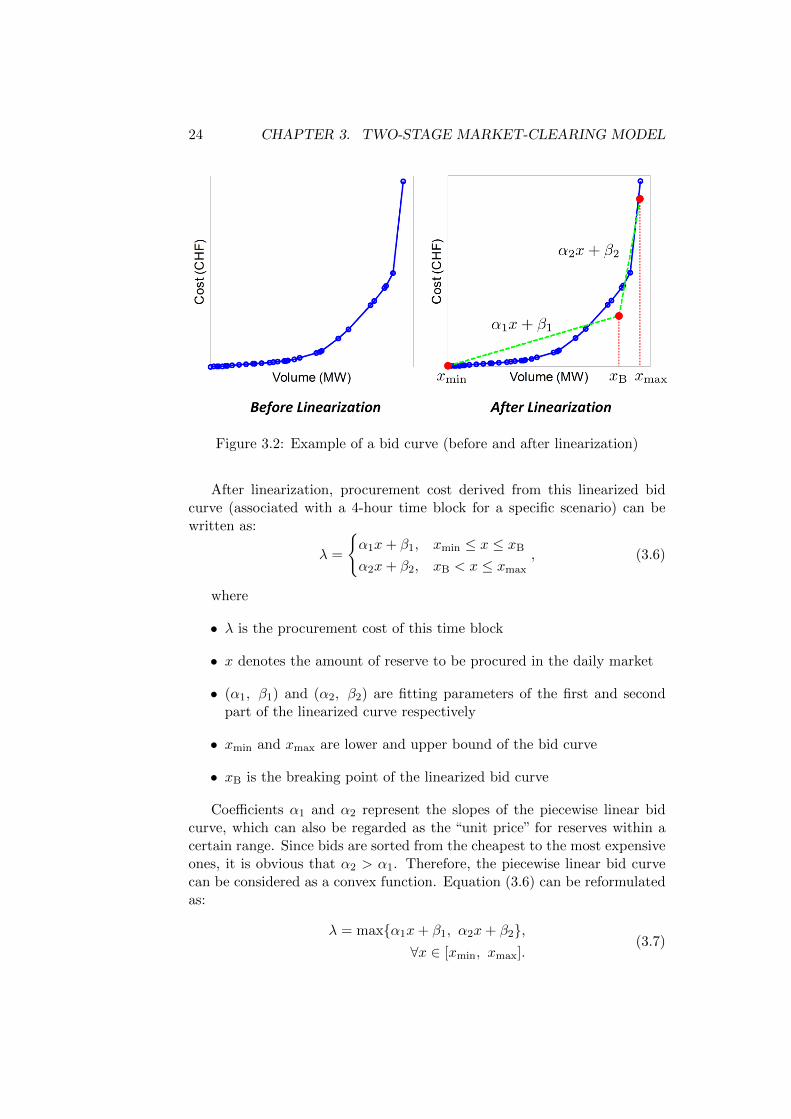

5. A bid curve is drawn based on cumulative volume and cost. Theleft curve in Figure 3.2 shows an example of bid curve. Each bluecircle represents a bid. The x-coordinate corresponds to the cumulativevolume up to this bid, whereas the y-coordinate is the cumulative costfor such volume.

6. To incorporate daily bids into the linear model, bid curves are lin-earized. The curve on the right in Figure 3.2 depicts how a bid curve(blue line) can be approximated by two straight lines (green dashedlines).

Two-piece linearization is selected by the current market-clearing algo-rithm, since it represents bidding behavior in a most efficient manner.

24 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

Figure 3.2: Example of a bid curve (before and after linearization)

After linearization, procurement cost derived from this linearized bidcurve (associated with a 4-hour time block for a specific scenario) can bewritten as:

λ =

α1x+ β1, xmin ≤ x ≤ xB

α2x+ β2, xB < x ≤ xmax

, (3.6)

where

• λ is the procurement cost of this time block

• x denotes the amount of reserve to be procured in the daily market

• (α1, β1) and (α2, β2) are fitting parameters of the first and secondpart of the linearized curve respectively

• xmin and xmax are lower and upper bound of the bid curve

• xB is the breaking point of the linearized bid curve

Coefficients α1 and α2 represent the slopes of the piecewise linear bidcurve, which can also be regarded as the “unit price” for reserves within acertain range. Since bids are sorted from the cheapest to the most expensiveones, it is obvious that α2 > α1. Therefore, the piecewise linear bid curvecan be considered as a convex function. Equation (3.6) can be reformulatedas:

λ = maxα1x+ β1, α2x+ β2,∀x ∈ [xmin, xmax].

(3.7)

3.2. STOCHASTIC MARKET-CLEARING MODEL 25

Equation (3.7) can be written as an optimization problem:

minx

λ

s.t. α1x+ β1 ≤ λ,α2x+ β2 ≤ λ,

xmin ≤ x ≤ xmax.

(3.8)

In reality, daily procurement costs are calculated for each 4-hour timeblock and summed up. Fitting parameters α1, α2, β1 and β2 vary accord-ing to each piecewise linear bid curve derived for each time block and areconstructed for each scenario. Therefore, Equation (3.8) can be extended tothe full week horizon and all scenarios in the daily market:

minxdT+

(ωd), xdT−

(ωd)λT+(ωd) + λT−(ωd)

s.t. α+1 (ωd)xd

T+(ωd) + β+

1 (ωd) ≤ λT+(ωd),

α+2 (ωd)xd

T+(ωd) + β+

2 (ωd) ≤ λT+(ωd),

α−1 (ωd)xdT−

(ωd) + β−1 (ωd) ≤ λT−(ωd),

α−2 (ωd)xdT−

(ωd) + β−2 (ωd) ≤ λT−(ωd),

xdT+

(ωd) ∈ [xmind,T+

(ωd), xmaxd,T+

(ωd)],

xdT−

(ωd) ∈ [xmind,T−

(ωd), xmaxd,T−

(ωd)],

∀ωd ∈ Ωd,

(3.9)

where

• λT+(ωd) ∈ R42×1 is the cost vector of TCR+

• λT−(ωd) ∈ R42×1 is the cost vector of TCR−

• α+1 (ωd), β+

1 (ωd), α+2 (ωd), β+

2 (ωd) ∈ R42×1 are fitting parameters ofTCR+ bid curves

• α−1 (ωd), β−1 (ωd), α−2 (ωd), β−2 (ωd) ∈ R42×1 are fitting parameters ofTCR− bid curves

• xmind,T+

(ωd), xmaxd,T+

(ωd) are lower and upper bound of TCR+ bid curve

• xmind,T−

(ωd), xmaxd,T−

(ωd) are lower and upper bound of TCR− bid curve

Therefore, the term E[Λd(ωd)] in the Equation (3.4) can be reformulatedas:

E[Λd(ωd)] =∑

ωd∈Ωd

πd

(ωd) [

11×42λT+(ωd) + 11×42λT−(ωd)],

∀ωd ∈ Ωd,

(3.10)

where πd(ωd)

is the probability of scenario ωd and 11×42 is the summa-tion vector whose elements are all 1.

26 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

3.2.3 Constraints

The constraints considered in the stochastic market-clearing model primarilyencompass three aspects:

1. Conditional bids in weekly market

2. Probabilistic dimensioning criterion

3. Deterministic dimensioning criterion

The mathematical formulation of three types of constraints will be ex-plained individually in this section.

Conditional Bids in Weekly Market

According to current bidding rules in the Swiss reserve market, providersare allowed to submit a set of conditional bids. Definition and example ofconditional bids are given in Section 2.4.2.

To guarantee that this rule will not be violated in the optimization prob-lem, it is translated into the following constraint:

Acxw ≤ bc, (3.11)

where

• Ac ∈ RNwc ×Nw

is a matrix whose element is either 1 or 0 dependingon whether the corresponding bid is within the set of conditional bidsor not

• bc ∈ RNwc ×1 is a vector whose elements are all 1

• Nwc is the number of conditional bid sets amongst all bids in the weekly

market (including SCR, TCR+ and TCR−)

Illustrative Example: Consider the bids in Table 2.4. Bids #1, #2, #3and #6, #7 are two sets of conditional bids. The decision vector for theseseven bids is:

x = [x1, x2, · · · , x7]ᵀ,

where xi ∈ 0, 1 is the binary decision variable for Bid #i.According to the definition of conditional bids, at most one of x1, x2 and

x3 can have a value of 1. The rest should be 0. This is also applicable forx6 and x7. The rule of conditional bids can thus be written as:

x1 + x2 + x3 ≤ 1

x6 + x7 ≤ 1.

In this case, Ac =

[1 1 1 0 0 0 00 0 0 0 0 1 1

], and bc =

[11

].

3.2. STOCHASTIC MARKET-CLEARING MODEL 27

Probabilistic Dimensioning Criterion

The probabilistic criterion for dimensioning reserves states that the portionof time within a year when secondary control reserve alone is not able tocover spontaneous power imbalances and when secondary and tertiary con-trol reserve together are not able to cover overall power imbalances shouldnot exceed 0.2% [4]. This percentage can be translated as the probability ofpower imbalances being greater than the amount of reserves procured:

P (∆Ps ≥ Rs) + P (∆Po ≥ Ro) ≤ 0.2%, (3.12)

where ∆Ps and ∆Po are spontaneous and overall power imbalances re-spectively, Rs and Ro are the amount of secondary and overall reserves(including SCR and TCR).

Considering both positive and negative power imbalances, Equation (3.12)can be rewritten as:

P(∆Ps+ ≥ Rs+

)+ P

(∆Ps− ≤ −Rs−

)+ P

(∆Po+ ≥ Ro+

)+P(∆Po− ≤ −Ro−

)≤ 0.2%,

(3.13)

where

• ∆Ps+ > 0 and ∆Ps− < 0 are positive and negative spontaneous powerimbalances respectively

• ∆Po+ > 0 and ∆Po− < 0 are positive and negative overall powerimbalances respectively

• Rs+ and Rs− refer to positive and negative SCR (currently in Switzer-land Rs+ = Rs−)

• Ro+ and Ro− refer to overall positive and negative control reserves

If we define cumulative distribution functions of power imbalances assuch:

Fs+(p) = P(∆Ps+ ≥ p

)Fs−(p) = P

(∆Ps− ≤ −p

)Fo+(p) = P

(∆Po+ ≥ p

)Fo−(p) = P

(∆Po− ≤ −p

) , (3.14)

then Equation (3.15) can be reformulated as:

Fs+(Rs+) + Fs−(Rs−) + Fo+(Ro+) + Fo−(Ro−) ≤ 0.002. (3.15)

28 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

The amount of procured reserve Rs+ , Rs− , Ro+ and Ro− can be replacedby decision variables in the following terms:

Rs+ = Rs− = pᵀSxwS ,

Ro+ = pᵀSxwS + pᵀT+

xwT+

+ xdT+

(ωd),

Ro− = pᵀSxwS + pᵀT−

xwT−

+ xdT−

(ωd),

∀ωd ∈ Ωd.

(3.16)

Inserting Equation (3.16) into (3.15), Equation (3.15) becomes:

Fs+(pᵀSxwS ) + Fs−(pᵀSx

wS ) + Fo+

(pᵀSx

wS + pᵀT+

xwT+

+ xdT+

(ωd))

+Fo−

(pᵀSx

wS + pᵀT−

xwT− + xd

T−(ωd))≤ 0.002, ∀ωd ∈ Ωd.

(3.17)

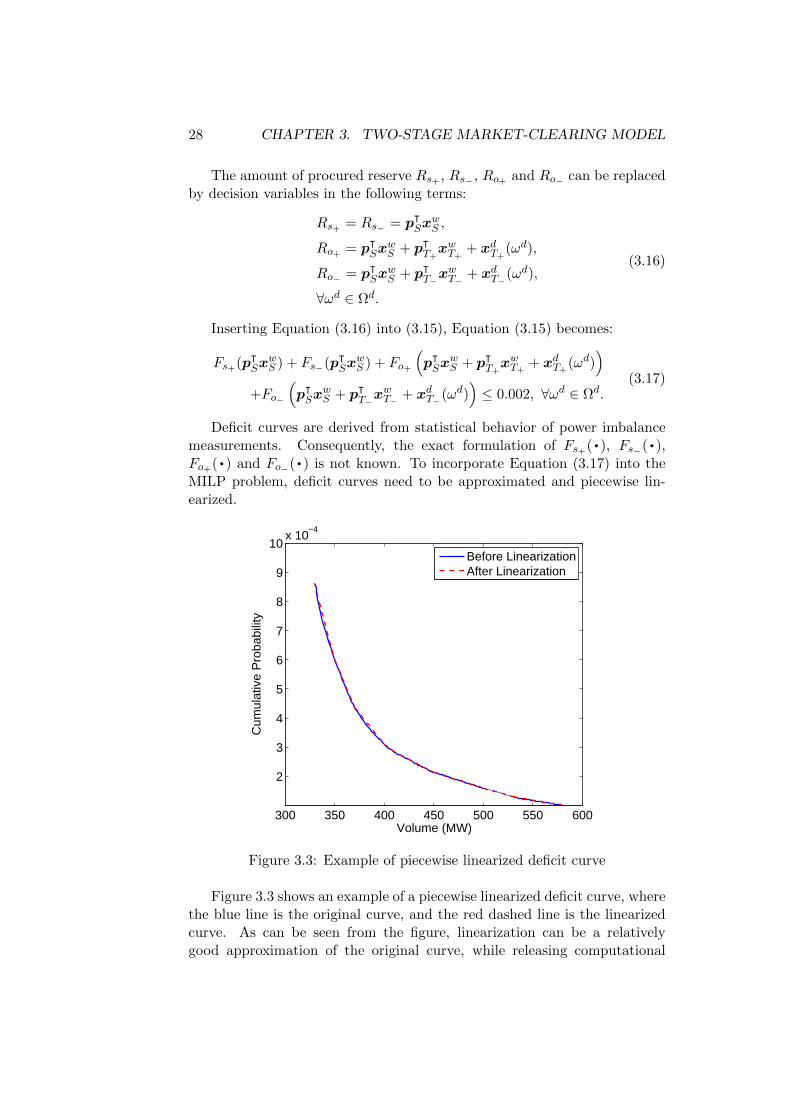

Deficit curves are derived from statistical behavior of power imbalancemeasurements. Consequently, the exact formulation of Fs+(·), Fs−(·),Fo+(·) and Fo−(·) is not known. To incorporate Equation (3.17) into theMILP problem, deficit curves need to be approximated and piecewise lin-earized.

300 350 400 450 500 550 600

2

3

4

5

6

7

8

9

10x 10

−4

Volume (MW)

Cum

ulat

ive

Pro

babi

lity

Before LinearizationAfter Linearization

Figure 3.3: Example of piecewise linearized deficit curve

Figure 3.3 shows an example of a piecewise linearized deficit curve, wherethe blue line is the original curve, and the red dashed line is the linearizedcurve. As can be seen from the figure, linearization can be a relativelygood approximation of the original curve, while releasing computational

3.2. STOCHASTIC MARKET-CLEARING MODEL 29

burden of the problem. The linearization process takes place once per halfa year along with the update of original deficit curve based on the mostrecent measurement data. After linearization, parameters are obtained andinserted into constraints:

εs+ =

a(1)s+Rs+ + b

(1)s+ , Rs+ ∈

[r

(0)s+ , r

(1)s+

]a

(2)s+Rs+ + b

(2)s+ , Rs+ ∈

[r

(1)s+ , r

(2)s+

]...

...

a(m)s+ Rs+ + b

(m)s+ , Rs+ ∈

[r

(m−1)s+ , r

(m)s+

](3.18)

εs− =

a(1)s−Rs− + b

(1)s− , Rs− ∈

[r

(0)s− , r

(1)s−

]a

(2)s−Rs− + b

(2)s− , Rs− ∈

[r

(1)s− , r

(2)s−

]...

...

a(n)s− Rs− + b

(n)s− , Rs− ∈

[r

(n−1)s− , r

(n)s−

](3.19)

εo+ =

a(1)o+Ro+ + b

(1)o+ , Ro+ ∈

[r

(0)o+ , r

(1)o+

]a

(2)o+Ro+ + b

(2)o+ , Ro+ ∈

[r

(1)o+ , r

(2)o+

]...

...

a(j)o+Ro+ + b

(j)o+ , Ro+ ∈

[r

(j−1)o+ , r

(j)o+

](3.20)

εo− =

a(1)o−Ro− + b

(1)o− , Ro− ∈

[r

(0)o− , r

(1)o−

]a

(2)o−Ro− + b

(2)o− , Ro− ∈

[r

(1)o− , r

(2)o−

]...

...

a(k)o−Ro− + b

(k)o− , Ro− ∈

[r

(k−1)o− , r

(k)o−

](3.21)

where

• subscripts s+, s−, o+, o− denote variables/parameters of secondarypositive, secondary negative, overall positive and overall negative re-serves

• ε·(R) is the probability of deficit with a reserve amount of R accordingto the corresponding deficit curve

• a(i)· and b(i)· are linearization parameters of piece i of the corresponding

deficit curve

30 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

• m, n, j, k are the total number of pieces for each linearized deficitcurve

•[r

(i−1)· , r(i)·]

is the range of reserve volume in which linear piece i is

valid

Theoretically, deficit curves should be close to convex functions. Underthis assumption, Equations (3.18)−(3.21) can be treated similarly as thelinearized bid curves in Section 3.2.2. Thus, constraints with respect to theprobabilistic dimensioning criterion can be formulated as:

a(i)s+

(Rs+

)+ b

(i)s+ ≤ εs+ , i = 1, · · · ,m,

a(i)s−

(Rs−

)+ b

(i)s− ≤ εs− , i = 1, · · · , n,

a(i)o+

(Ro+

)+ b

(i)o+ ≤ εo+ , i = 1, · · · , j,

a(i)o−

(Ro−

)+ b

(i)o− ≤ εo− , i = 1, · · · , k,

Rmins+ ≤ Rs+ ≤ Rmax

s+ ,

Rmins− ≤ Rs− ≤ Rmax

s− ,

Rmino+ ≤ Ro+ ≤ Rmax

o+ ,

Rmino− ≤ Ro− ≤ Rmax

o− ,

εs+ + εs− + εo+ + εo− ≤ 0.002.

(3.22)

In this set of constraints, εs+ , εs− , εo+ and εo− are regarded as “deci-sion variables” and appended to those described in Section 3.2.1. They donot appear in objective function, though. Rs+ , Rs− , Ro+ and Ro− can beexpressed by decision variables according to Equation (3.16).

Deterministic Dimensioning Criterion

According to Section 2.5.2, the deterministic criterion of sizing reserves inSwitzerland can be described as a minimum TCR+ of 400 MW according toMEAS contract. This criterion can thus be written with weekly and dailydecision variables as follows:

400 ≤ pᵀT+xwT+

+ xdT+

(ωd),

∀ωd ∈ Ωd.(3.23)

3.2. STOCHASTIC MARKET-CLEARING MODEL 31

3.2.4 Formulation

The complete mathematical formulation of the current two-stage stochasticmarket-clearing model is presented as follows:

minxw, λT+

(ωd), λT− (ωd)cᵀwx

w +∑

ωd∈Ωd

πd

(ωd) [

11×42λT+(ωd) + 11×42λT−(ωd)]

(3.24)

s.t. Acxw ≤ bc, (3.25)

α+1 (ωd)xd

T+(ωd) + β+

1 (ωd) ≤ λT+(ωd), ∀ωd ∈ Ωd,

(3.26)

α+2 (ωd)xd

T+(ωd) + β+

2 (ωd) ≤ λT+(ωd), ∀ωd ∈ Ωd,

(3.27)

α−1 (ωd)xdT−(ωd) + β−1 (ωd) ≤ λT−(ωd), ∀ωd ∈ Ωd,

(3.28)

α−2 (ωd)xdT−(ωd) + β−2 (ωd) ≤ λT−(ωd), ∀ωd ∈ Ωd,

(3.29)

a(i)s+

(pᵀSx

wS

)+ b(i)s+ ≤ εs+ , i = 1, · · · ,m, (3.30)

a(i)s−

(pᵀSx

wS

)+ b(i)s− ≤ εs− , i = 1, · · · , n, (3.31)

a(i)o+

(pᵀSx

wS + pᵀT+

xwT+

+ xdT+

(ωd))

+ b(i)o+ ≤ εo+ ,

∀ωd ∈ Ωd, i = 1, · · · , j, (3.32)

a(i)o−

(pᵀSx

wS + pᵀT−

xwT− + xd

T−(ωd))

+ b(i)o− ≤ εo− ,

∀ωd ∈ Ωd, i = 1, · · · , k, (3.33)

εs+ + εs− + εo+ + εo− ≤ 0.002, (3.34)

400 ≤ pᵀT+xwT+

+ xdT+

(ωd), ∀ωd ∈ Ωd, (3.35)

xdT+

(ωd) ∈ [xmind,T+

(ωd), xmaxd,T+

(ωd)], ∀ωd ∈ Ωd, (3.36)

xdT−(ωd) ∈ [xmin

d,T−(ωd), xmaxd,T−(ωd)], ∀ωd ∈ Ωd. (3.37)

Constraint (3.25) corresponds to the conditional bids received in weeklymarket. Constraints (3.26)−(3.29) are related to piecewise linearized dailybid curves. (3.30)−(3.34) are associated with probabilistic dimensioning cri-terion. Constraint (3.35) is for deterministic dimensioning criterion (MEASconstraint). Last but not least, constraints (3.36) and (3.37) define feasibleranges for daily procurement amounts.

32 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

3.3 Improvements of Two-Stage Model

This section presents two major improvements made to the current two-stage market-clearing model: linearization of bid curves and selection ofdaily scenarios. Different methods are investigated and compared. Resultsshow that cost savings can be achieved with these improvements, which canbe readily implemented in Swissgrid.

3.3.1 Linearization of Bid Curves

The linearization method of bid curves refers to how the piecewise linearizedbid curve in Figure 3.2 is obtained. It encompasses two aspects: the numberof curve pieces and the method of obtaining linearization parameters.

In [4], a two-piece linearization method is applied and this method hasbeen implemented since the launch of two-stage stochastic market-clearingmodel in Switzerland. This linearization method is based on minimizing themaximum fitting error on a curve, which is referred to as maximum errorestimation hereafter.

The process of searching for optimal fitting parameters using maximumerror estimation can be described as:

min γs.t. |yi − yi| ≤ γ,

yi =

α1xi + β1, xi ∈ [x(0)B , x

(1)B ]

...

αjxi + βj , xi ∈ [x(j−1)B , x

(j)B ]

...

αMxi + βM , xi ∈ [x(M−1)B , x

(M)B ]

,

∀i = 1, · · · , N,

(3.38)

where

• (xi, yi) represents an individual bid on bid curve, and xi, yi denotecumulative volume and cost at this point respectively

• yi is the estimated cost after linearization at xi

• N is the total number of data points to be fitted on the bid curve

• γ denotes the maximum error between fitted curve and original curve

• αj and βj are linearization parameters of piece j

• x(j−1)B and x

(j)B indicate the lower and upper bound of piece j

• M is the total number of pieces of the linearized curve

3.3. IMPROVEMENTS OF TWO-STAGE MODEL 33

Another commonly used method in curve fitting is least squares estima-tion. It can be described via the following formulation:

min

N∑i=1

(yi − yi)2

s.t. yi =

α1xi + β1, xi ∈ [x(0)B , x

(1)B ]

...

αjxi + βj , xi ∈ [x(j−1)B , x

(j)B ]

...

αMxi + βM , xi ∈ [x(M−1)B , x

(M)B ]

,

∀i = 1, · · · , N,

(3.39)

Notations in Equation (3.39) follow those in Equation (3.38).

In the linearization process, optimizations based on Equation (3.38) or(3.39) are repeated for each combination of bids taken as breaking point. Theoptimal solution is then the minimum value of objective functions among alliterations.

Sometimes a two-piece linearization of the bid curve can result in in-accurate estimation of daily procurement cost. This usually occurs whenthe shape of bid curve is close to quadratic, for example the one in Figure3.2. In such cases, more pieces should be considered while linearizing thebid curve. However, too many pieces will significantly increase the num-ber of iterations due to more combinations of breaking points. Consideringthe computational burden, the maximum number of curve pieces consideredhere is three.

Therefore, four linearization methods (Figure 3.4) concerning two dimen-sions (number of pieces and estimation method) are analyzed and compared.The number of pieces refer to the value of M in Equations (3.38) and (3.39).

Figure 3.4: Overview of bid curve linearization methods

Figure 3.5 shows an example of bid curve linearization using the above-mentioned four different methods. As can be seen from the figure, three-piece

34 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

fitting is generally closer to real bids. As for estimation method, using leastsquares estimation can improve fitting performance to a certain extent.

Volume (MW)

Cos

t (C

HF

)

Example Bid Curve

BidsMethod 1Method 2Method 3Method 4

Figure 3.5: Example of bid curve linearization by four methods

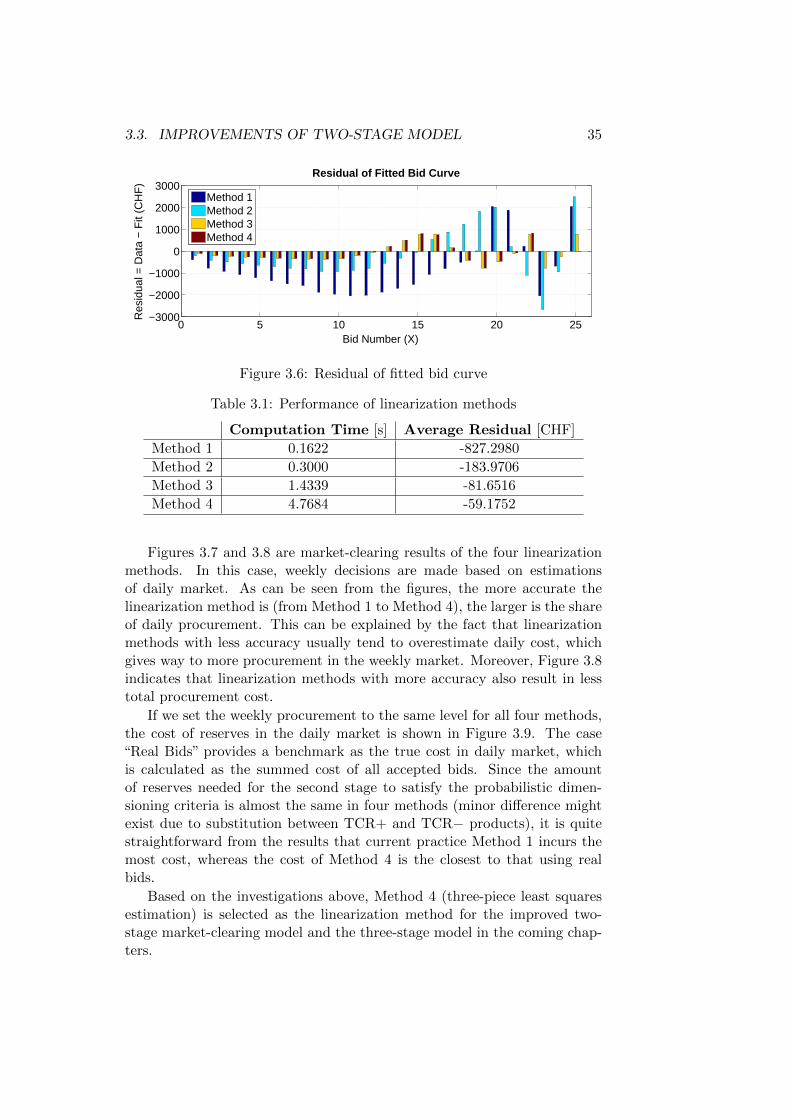

Figure 3.6 and Table 3.1 illustrate the residuals and computation timeof the example bids in Figure 3.5. In this context, residual is defined asthe cost derived from original bid curve subtracted by the fitted cost fromthe linearized curve. A negative average residual suggests that generally thefitted curve is overestimating procurement cost.

Looking from residual’s perpective, Method 4 yields the most accurateapproximation of the bid curve, with an overestimated cost of only 59 CHFon average. The current practice, Method 1, can result in an overestimationof over 800 CHF on average. By switching the estimation method from max-imum error estimation to least squares estimation, the average residual canbe significantly reduced to approximately 184 CHF. Increasing the numberof curve pieces can further improve linearization accuracy, as can be deducedfrom the comparisons between Methods 1 and 3, as well as Methods 2 and4.

Computationally, two-piece fitting is generally quicker than three-piecefitting. This is due to the iterative search for an optimal combination ofbreaking points. Nevertheless, the computation time of 4 seconds usingMethod 4 is still affordable as a trade-off with the accuracy it yields.

To investigate the impact of linearization method on the optimizationresults, these four methods are applied in a two-stage market-clearing model.The scenario input data for daily market is the data of the delivery week(Perfect Information Scenario).

3.3. IMPROVEMENTS OF TWO-STAGE MODEL 35

0 5 10 15 20 25−3000

−2000

−1000

0

1000

2000

3000Residual of Fitted Bid Curve

Bid Number (X)

Res

idua

l = D

ata

− F

it (C

HF

)

Method 1Method 2Method 3Method 4

Figure 3.6: Residual of fitted bid curve

Table 3.1: Performance of linearization methods

Computation Time [s] Average Residual [CHF]

Method 1 0.1622 -827.2980

Method 2 0.3000 -183.9706

Method 3 1.4339 -81.6516

Method 4 4.7684 -59.1752

Figures 3.7 and 3.8 are market-clearing results of the four linearizationmethods. In this case, weekly decisions are made based on estimationsof daily market. As can be seen from the figures, the more accurate thelinearization method is (from Method 1 to Method 4), the larger is the shareof daily procurement. This can be explained by the fact that linearizationmethods with less accuracy usually tend to overestimate daily cost, whichgives way to more procurement in the weekly market. Moreover, Figure 3.8indicates that linearization methods with more accuracy also result in lesstotal procurement cost.

If we set the weekly procurement to the same level for all four methods,the cost of reserves in the daily market is shown in Figure 3.9. The case“Real Bids” provides a benchmark as the true cost in daily market, whichis calculated as the summed cost of all accepted bids. Since the amountof reserves needed for the second stage to satisfy the probabilistic dimen-sioning criteria is almost the same in four methods (minor difference mightexist due to substitution between TCR+ and TCR− products), it is quitestraightforward from the results that current practice Method 1 incurs themost cost, whereas the cost of Method 4 is the closest to that using realbids.

Based on the investigations above, Method 4 (three-piece least squaresestimation) is selected as the linearization method for the improved two-stage market-clearing model and the three-stage model in the coming chap-ters.

36 CHAPTER 3. TWO-STAGE MARKET-CLEARING MODEL

−600 −400 −200 0 200 400 600 800

Method 1

Method 2

Method 3

Method 4

Amount of Procured Reserves

Volume (MW)

SCR TCR Weekly TCR Daily

Figure 3.7: Amount of procured reserves using four fitting methods

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

Method 1

Method 2

Method 3

Method 4

Cost (MCHF)

Total Cost of Reserves

Weekly Daily

4.197

4.216

4.231

4.237

Figure 3.8: Total procurement cost of reserves using four fitting methods

Method 1 Method 2 Method 3 Method 4 Real Bids0

0.1

0.2

0.3

0.4

0.5Cost of Reserves in Daily Market

Cos

t (M

CH

F)

0.348

0.403

0.2870.257

0.233

Figure 3.9: Procurement cost in daily market using four fitting methodsafter fixing weekly decision

3.3. IMPROVEMENTS OF TWO-STAGE MODEL 37

By applying the improved linearization method on 34 weeks in 2015(Week 02−35), a total cost saving of 455,372 CHF can be gained, as isshown in Table 3.2. This corresponds to 0.65% and an average saving of13,393 CHF per week.

Table 3.2: Estimation of cost savings by improved linearization method(Week 02−35, 2015)

Total Savings in CHF 455,372

Total Savings in % 0.65

Average Savings per Week in CHF 13,393

3.3.2 Selection of Scenarios

In stochastic programming, scenarios are crucial in obtaining an optimalsolution to the problem. Therefore, various data analyses and simulationshave been carried out within the framework of this thesis in order to improvethe performance of scenarios in the current model.