modelling for provisioning of bad debt under ifrs 9

TRANSCRIPT

Prof. Arif Ahmed

Modelling For Provisioning

Of Bad Debt Under IFRS 9

South Asian Management Technologies Foundation

Housekeeping

• Slides will be available on our SlideShare page; the link will be emailed to you

• Recording of the webinar will be available to download; the link will be emailed to you

• Take the time to complete a post-webinar survey that will pop up at the end

• You can type your questions throughout the session

• Time will be allocated in the end for the speaker to address your questions

Your Speaker – Pro. Arif Ahmed

Prof. Arif Ahmed is a Chartered Accountant and MBA (Finance) and has more than 25 years of experience under his belt in the area of finance and risk management.

In addition to training, Prof. Ahmed has assisted many organisations to design and implement financial management and control systems across various industries including media, metals and minerals, logistics, banking, engineering, energy, hospitality, paper, etc. He is one of the most sought after speakers for his inimitable style of blending concepts with application in industry.

3

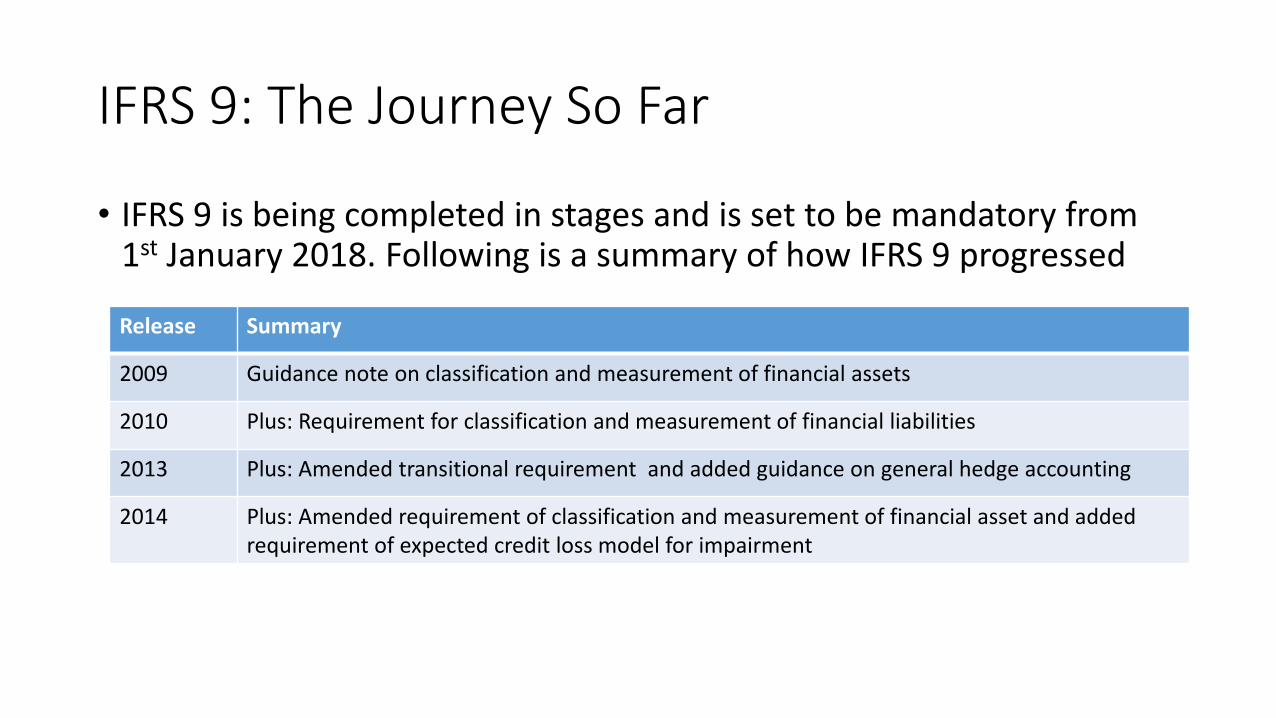

IFRS 9: The Journey So Far

• IFRS 9 is being completed in stages and is set to be mandatory from 1st January 2018. Following is a summary of how IFRS 9 progressed

Release Summary

2009 Guidance note on classification and measurement of financial assets

2010 Plus: Requirement for classification and measurement of financial liabilities

2013 Plus: Amended transitional requirement and added guidance on general hedge accounting

2014 Plus: Amended requirement of classification and measurement of financial asset and added requirement of expected credit loss model for impairment

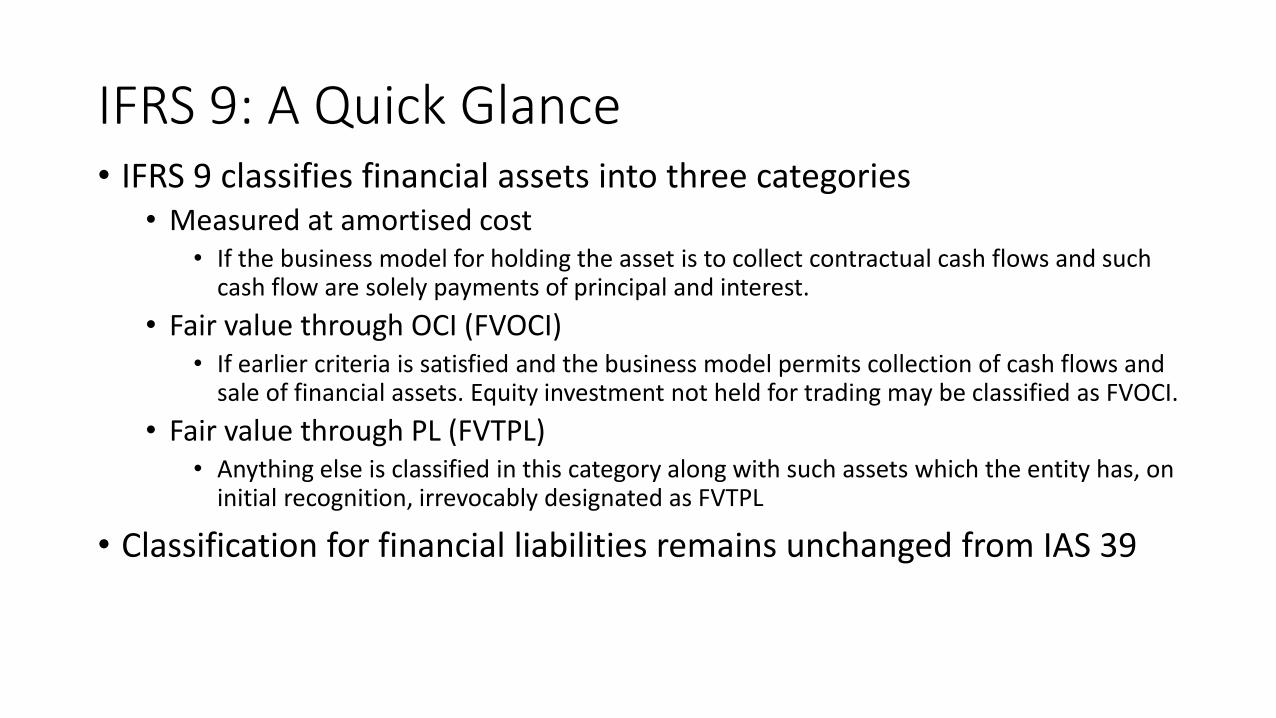

IFRS 9: A Quick Glance• IFRS 9 classifies financial assets into three categories

• Measured at amortised cost• If the business model for holding the asset is to collect contractual cash flows and such

cash flow are solely payments of principal and interest.

• Fair value through OCI (FVOCI)• If earlier criteria is satisfied and the business model permits collection of cash flows and

sale of financial assets. Equity investment not held for trading may be classified as FVOCI.

• Fair value through PL (FVTPL)• Anything else is classified in this category along with such assets which the entity has, on

initial recognition, irrevocably designated as FVTPL

• Classification for financial liabilities remains unchanged from IAS 39

Expected Credit Loss

• A major change is replacing “incurred” credit loss with “expected” credit loss.

• This is applied on financial assets that are not measured at FVTPL including loans, financial guarantees, trade receivables, lease, etc. but not on equity instruments

• Loss allowance is measured for expected loss for next 12 months or for lifetime of the assets depending on whether there has been a significant increase of credit risk since first recognition.

• Simplified approach for trade receivable, contract assets, and lease receivables.

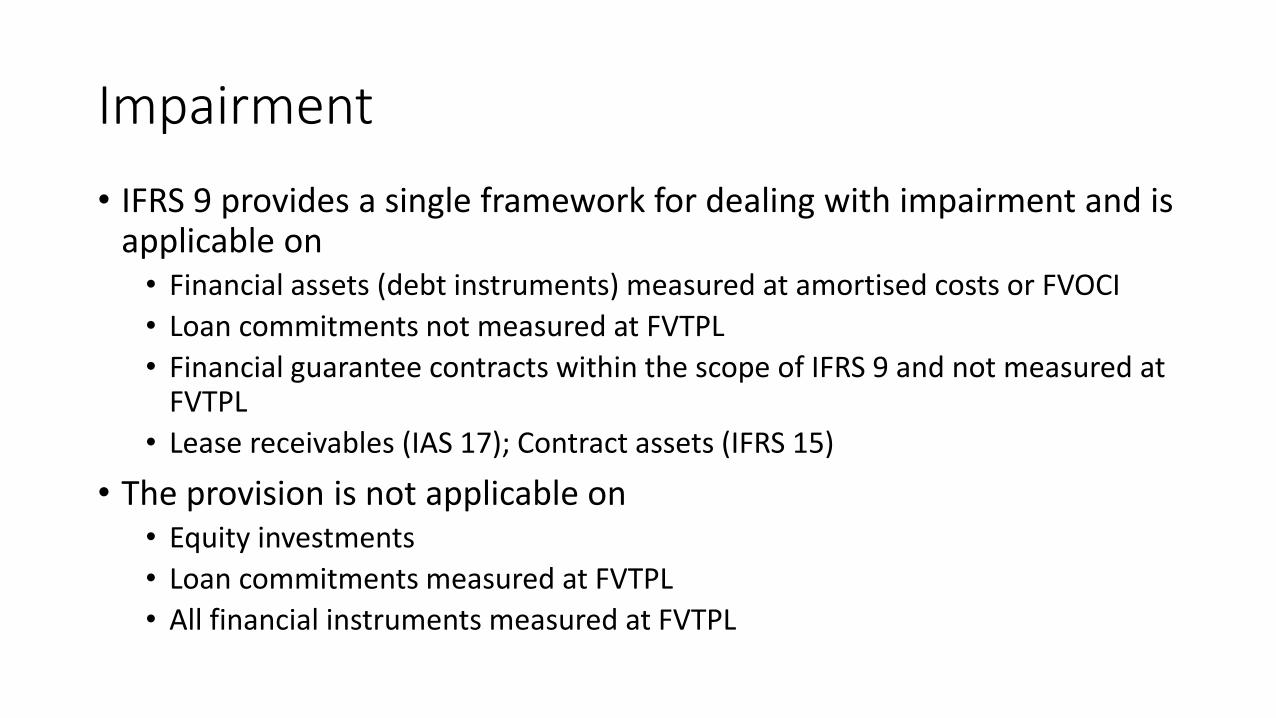

Impairment

• IFRS 9 provides a single framework for dealing with impairment and is applicable on• Financial assets (debt instruments) measured at amortised costs or FVOCI

• Loan commitments not measured at FVTPL

• Financial guarantee contracts within the scope of IFRS 9 and not measured at FVTPL

• Lease receivables (IAS 17); Contract assets (IFRS 15)

• The provision is not applicable on• Equity investments

• Loan commitments measured at FVTPL

• All financial instruments measured at FVTPL

The Impairment Flow ChartIs the asset credit impaired at initial recognition?

Changes in lifetime expected credit loss to be

recognised

Is the asset trade receivable or contract asset with significant financing component, or Lease receivable against which lifetime expected credit

loss measurement has been selected

Is the asset trade receivable or contract asset with significant financing component

Has there been any significant increase in credit risk since initial recognition

Recognise 12-month expected credit loss

No

Provide lifetime expected credit loss

Yes

Yes

Yes

Yes

No

No

No

12 Month and Lifetime Expected Credit Loss

• This is a component of the lifetime expected credit loss which may be incurred because of default events on the financial instruments materialising within 12 months from the reporting date

• Major challenges• Differentiating between default event and significant increase in credit risk

• Segregate losses caused by a default event taking place within next 12 months from those taking place after 12 months

• Lifetime expected credit loss is the expected credit loss resulting from all possible default events over expected life of the instrument

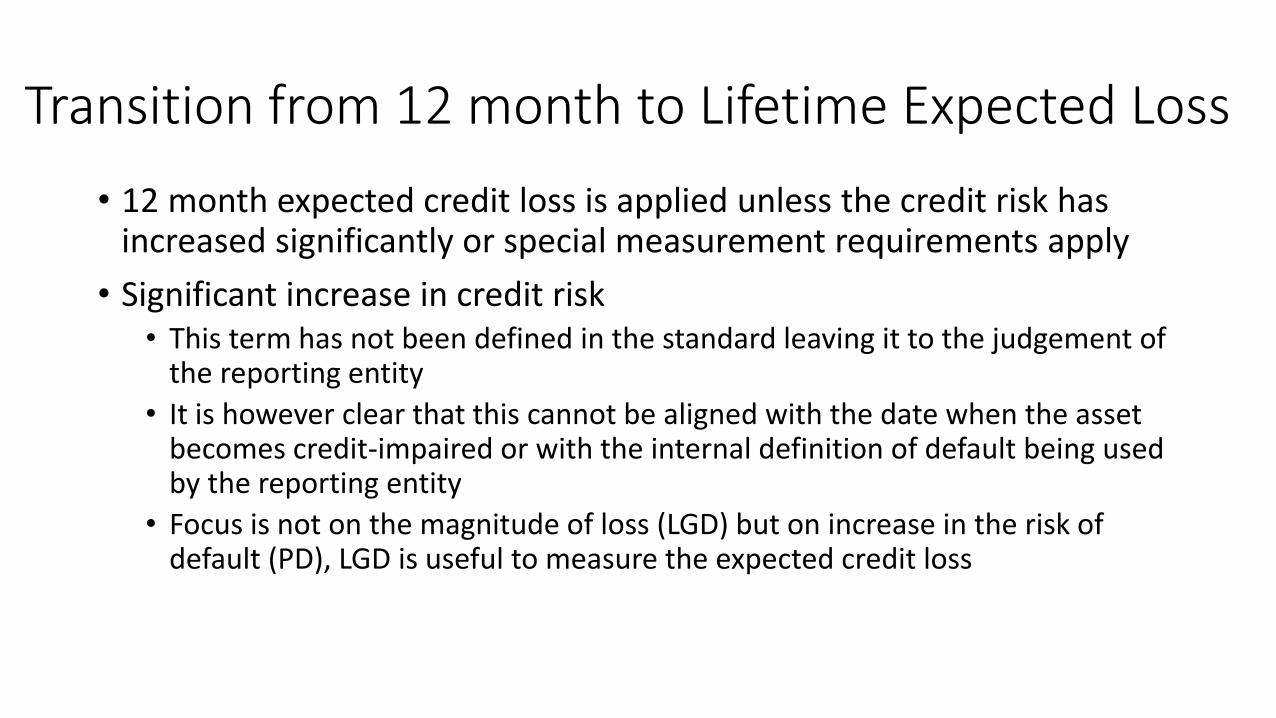

Transition from 12 month to Lifetime Expected Loss

• 12 month expected credit loss is applied unless the credit risk has increased significantly or special measurement requirements apply

• Significant increase in credit risk• This term has not been defined in the standard leaving it to the judgement of

the reporting entity

• It is however clear that this cannot be aligned with the date when the asset becomes credit-impaired or with the internal definition of default being used by the reporting entity

• Focus is not on the magnitude of loss (LGD) but on increase in the risk of default (PD), LGD is useful to measure the expected credit loss

The Movement

12 months expected credit loss provision

Lifetime expected credit loss provision

Significant increase in credit risk

Reversal of transfer conditions

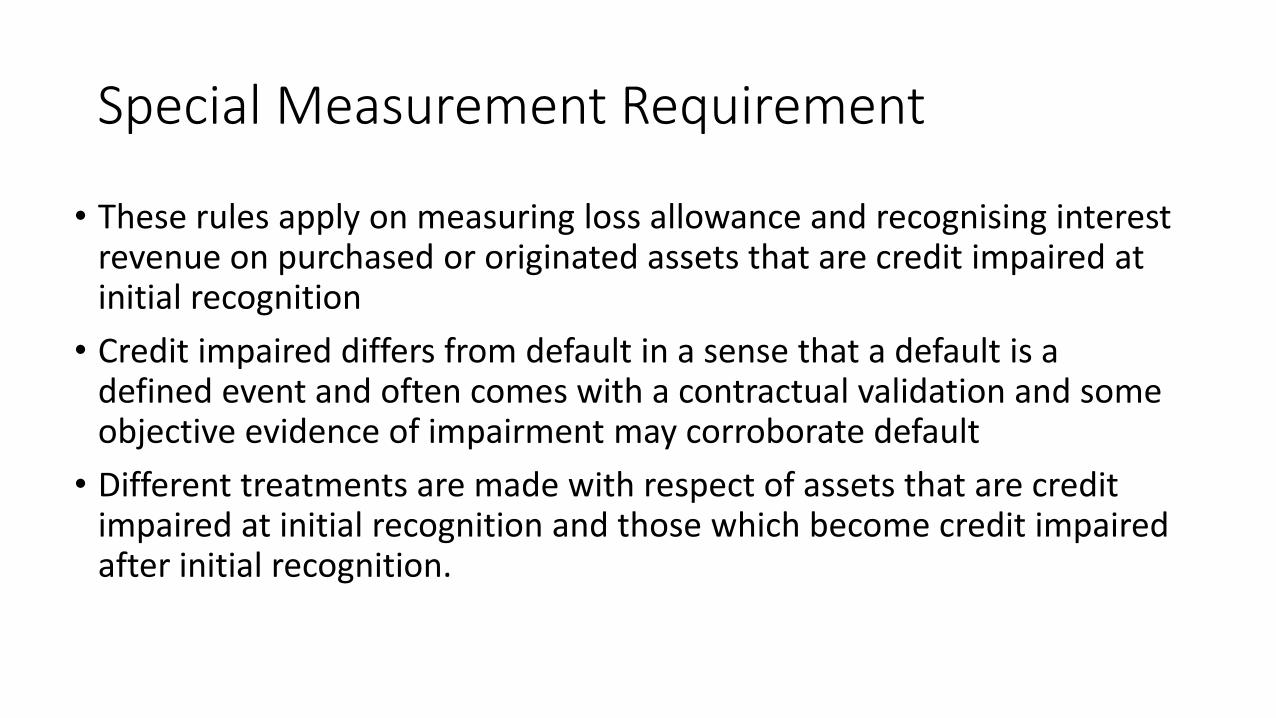

Special Measurement Requirement

• These rules apply on measuring loss allowance and recognising interest revenue on purchased or originated assets that are credit impaired at initial recognition

• Credit impaired differs from default in a sense that a default is a defined event and often comes with a contractual validation and some objective evidence of impairment may corroborate default

• Different treatments are made with respect of assets that are credit impaired at initial recognition and those which become credit impaired after initial recognition.

Purchased or Originated Credit Impaired Assets

• At initial recognition find out the IRR based on the cash price paid and expected cash inflow. Debit loan asset and credit cash

• On interest application period apply interest at IRR. Debit loan asset and credit interest revenue. If cash is received debit Cash and credit Loan asset.

• If there is a reversal of impairment and larger cash flow is expected, debit Loss Allowance and credit Impairment Gain for the value of increase discounted at original IRR.

Simplified Measure for Trade/ Lease Receivables

• Lifetime expected loss can be provided for trade receivables and contract assets without a significant financing component. These assets would usually have a short duration – generally of less than 12 months

• In case of trade receivables and contract assets with a significant financing component, the reporting entity may opt to use the general approach or provide lifetime expected loss

• One can use a provision matrix for short term trade receivables

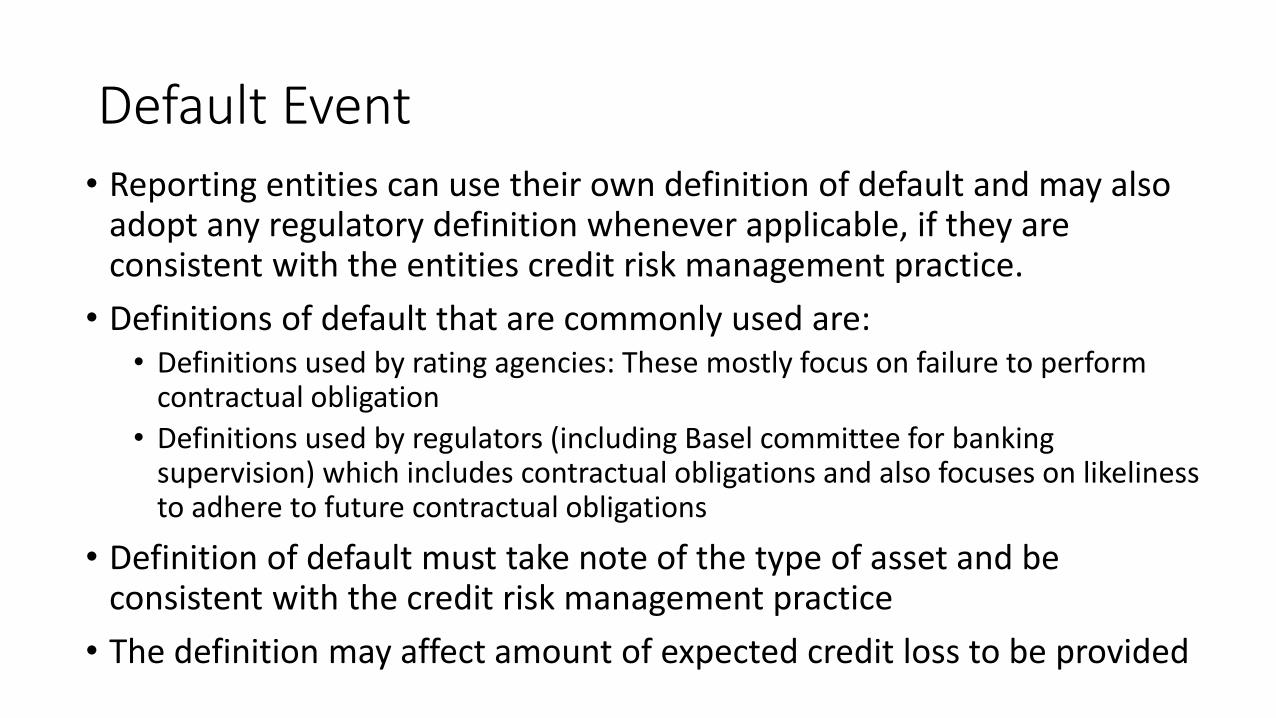

Default Event• Reporting entities can use their own definition of default and may also

adopt any regulatory definition whenever applicable, if they are consistent with the entities credit risk management practice.

• Definitions of default that are commonly used are:• Definitions used by rating agencies: These mostly focus on failure to perform

contractual obligation

• Definitions used by regulators (including Basel committee for banking supervision) which includes contractual obligations and also focuses on likeliness to adhere to future contractual obligations

• Definition of default must take note of the type of asset and be consistent with the credit risk management practice

• The definition may affect amount of expected credit loss to be provided

Challenge to Infrastructure

• There will be no “one size fits all” definition of critical terms like credit risk, significant increase, or default.

• In addition to definition, relevance of the definition to the reporting entity will have to be established.

• Provisioning for bad debt is to be computed based on rigorous analysis of past data

• There will be a tough balancing act between the measurement requirement and corresponding cost

• Entities with simpler computation mechanism will also be affected, though at a lower magnitude.

Impact

• Reporting entities, particularly those with regulatory capital requirement may face a negative impact since now the expected loss will also have to be provided as against the current practice of providing for only incurred credit loss.

• Transition from 12 month to lifetime provision is likely to cause an enhanced provision which will have an adverse impact on the capital adequacy.

Impact on Financial Sector

• Financial sector have additional regulatory requirement of providing for credit risk under various versions of Basel accord.

• The major points to be considered are as follows:• In case of Basel, credit risk can be seen at any “point in time” or “through the

cycle”, whereas under IFRS 9 it is a “point in time” view

• IFRS 9 does not mandate any minimum data requirement for LGD and EAD computation unlike Basel where minim data requirement is 5 years for retail and 7 years for corporate, sovereign, and others.

• “Default” is defined under Basel but not under IFRS 9

• There is no minimum floor for expected credit loss in IFRS 9 unlike Basel

• Discounting rate is essentially EIR under IFRS 9 and WACC under Basel 2

• IFRS 9 uses cash shortfall to compute expected loss; Basel uses PD x EAD x LGD

Impact: Case Study by IASB• IASB conducted a study between April and June 2013 to understand

potential impact of the provisioning model. Most of the respondents reported that amount of credit loss allowance will increase significantly across the life cycle of the asset. • Mortgage portfolio:

• On transition total allowance is likely to increase between 30-260% (80-400% in case of worst economic scenario)

• On transition if lifetime expected credit loss is to be provided the increase will be between 130-730% (400-540% in case of worst economic scenario)

• Other portfolio• On transition total allowance is likely to increase between 25-60% (50-150% in case of

worst economic scenario)

• On transition if lifetime expected credit loss is to be provided the increase will be between 50-140% (110-210% in case of worst economic scenario)

Using the Framework

• Step 1: • Estimate 12-month expected credit loss

• Step 2• Estimate lifetime expected credit loss

• Step 3• Use available macro-economic and firm level information to assess whether

any significant increase in credit risk has occurred or reversed

• The last step requires reporting entity to use a model to measure the credit risk at an account (or group) level unless external credit rating information is available.

Measuring Expected Credit Loss

• Expected credit loss are probability weighted estimate of credit losses over the expected life of the financial instrument. Credit losses include present value of expected cash shortfall over the estimation period

• Expected credit loss measurement should consider• An unbiased and probability-weighted amount

• Time value of money

• Information that are reliable, supportable. and available without undue effort

• Cash shortfall is the difference between contractual cash flow and cash flow that the entity expects to receive

Developing Credit Risk Assessment Models

• Past performance of specific assets or cohort of specific asset

• Classifying past performance into behaviour groups – what is the percentage of loss on retails loans that are overdue by 60 days?

• Develop a probability of default and loss given default reference table for various kinds of assets and at various points of default

Loss Provision Examples

• A company originates a 10 year loan of MU1,000,000 with 5% interest paid annually. 12 month PD and LGD is 0.5% and 25% respectively. Lifetime PD and LGD is 20% and 25% respectively and default is expected at the end of 2 years.

• 12 month expected credit loss• MU1,050,000 x 0.5% x 25% discounted at 5%: MU1250

• Lifetime expected credit loss• MU (1,050,000 /1,052) x 20% x 25%: 47619

• Assumption: First year interest was paid fully

Building In-house Loss Estimation Models

• One major challenge for small and medium size business is to have a mechanism in place to make assessment of credit loss provision

• In addition to using the simplified provision norms for trade and lease rent receivables, a SME can build in-house model for assessment of PD using common spreadsheet packages like Excel

• Using past transaction data and relating them to behaviour pattern, the financial instruments can be grouped into various risk classes with associated PD or linked with provision matrix.

Thank You