modelling volatility: arch, garch and other modelsstats.lse.ac.uk/q.yao/talks/archgarch.pdf ·...

TRANSCRIPT

Modelling Volatility: ARCH, GARCH and

Other Models

Qiwei Yao

London School of Economics

• ARCH & GARCH models: properties, estimation and tests

• A numerical example with S&P 500 index returns

• Other univariate volatility models

Reference: Fan & Yao (2003/5). Nonlinear Time Series. Springer:

§4.2.

Standard time series models: model conditional means

Volatility models: model conditional variances — (conditional) het-

eroscedasticity

Goal: Explain and model risk and uncertainty

Background: It is often found in finance that the larger values of

time series also lead to larger instability (ie. larger variances)

1. Yields of Treasury

Bills from July 17, 1959

to September 24, 1999

(source: Federal Reserve):

(a) Yields of three-month

Treasury Bills; (b) yields of

six-month Treasury Bills; (c)

yields of twelve-month Trea-

sury Bills.

It is clear that the yields

of Treasury Bills exhibit the

largest variation around the

peaks.

(a)

0 500 1000 1500 2000

510

15

Yields of 3-month Treasury bills

(b)

0 500 1000 1500 2000

24

68

1012

1416

Yields of 6-month Treasury bills

(c)

0 500 1000 1500 2000

46

810

1214

Yields of 12-month Treasury bills

2. Annual sunspot data

••••

•

•

•••••••••

•

•

••

••••••

•

•

•

•

•

•

•

••

•

•

••

••

•

•

••

•••

•

•

••

••

•

•••

•

•••

•

•

••

••

•

•

••

•

•

••

•

•

•

•

•

•

•

•

•

•

•

•

••

•

•

••

••

••••••

•••••

•

••••••••

•••

••••••••

•

•

•••

•

•

••

•

•

•

•

•

•

•

•

••

•

•

•

•

•

•••

•

•

••

•

•

••

•

•

••

•

••

•

•

•

••

•

•

•••••

•

••••

•

•

••••

•

•

••

•

•

••

••••

•

•

•••

••

•

••••

••

•

•

•

•

•

•••

•

•••

•

•

••••

•

•

••

•

•

•

•

••

•

•

•

••

•

•

•

••

•

•

••

•

•

•

••

••

•

•

•••

••

••

••

•

•

••

•

•

•

•

••

•

•

•

••

•

•

•

time

1700 1750 1800 1850 1900 1950 2000

050

100

150

Number of Sunspots

Basic properties of ARCH models

Xt = σtεt, and σ2t = c0 + b1X2t−1 + · · ·+ bpX

2t−p,

where c0 ≥ 0, bj ≥ 0 are constants, {εt} ∼ IID(0,1), and εt is indepen-

dent of {Xt−k, k ≥ 1} for all t.

Theorem. (Chen & An 1998, Giraitis, Kokoszka & Leipus 2000)

(i) The necessary and sufficient condition for the above model defining

a unique strictly stationary process {Xt, t = 0,±1,±2, · · · } with EX2t <

∞ is∑p

j=1 bj < 1. Further,

EXt = 0 and EX2t = c0/{1−

p∑

j=1

bj},

and Xt ≡ 0 for all t if c0 = 0.

(ii) If Eε4t < ∞ and max{1, (Eε4t )1/2}∑p

j=1 bj < 1, the strictly station-

ary solution has the finite fourth moment, namely EX4t < ∞.

Remark. (i) Stationary ARCH process {Xt} is WN(0, c0/(1−∑p

j=1 bj)).

(ii) It follows from the model that

X2t = c0 + b1X

2t−1 + · · ·+ bpX

2t−p + et,

where

et = (ε2t − 1){c0 +p∑

j=1

bjX2t−p}.

Further,

E(et|Xt−k, Xt−k−1, · · · ) = 0, for any k ≥ 1.

Hence for any k > p,

Var(Xt+k|Xt−m, m ≥ 0) = c0 +

p∑

j=1

bjVar(Xt+k−j|Xt−m, m ≥ 0),

which reflects ‘volatility cluster’ in financial time series analysis.

(iii) Under the additional condition max{1, (Eε4t )1/2}∑p

j=1 bj < 1,

{et} ∼ WN(0, σ2e ) with

σ2e = Var(ε2t )E{c0 +p∑

j=1

bjX2t−p}2 < ∞.

Note that the condition∑p

j=1 bj < 1 implies that 1 − ∑pj=1 bjz

j 6= 0

for all |z| ≥ 1. Hence {X2t } is a causal AR(p) process. Therefore,

the ACF (also ACVF) of the process {X2t } can be easily calculated

in terms of its MA(∞)-representation, which implies the fact that for

all τ

Corr(X2t , X

2t+τ) > 0,

although Corr(Xt, Xt+τ) = 0.

(iv) The stationary ARCH process {Xt} has heavier tails than those

of the white noise {εt} based on which {Xt} is defined.

Let κε = E(ε4t )/(Eε2t )2 the kurtosis of the distribution of εt. Then

E(X4t |Xt−1, · · · , Xt−p) = σ4t Eε4t = κεσ

4t (Eε2t )

2

= κε{E(X2t |Xt−1, · · · , Xt−p)}2.

Now it follows from Jensen’s inequality that

E(X4t ) = κεE{E(X2

t |Xt−1, · · · , Xt−p)}2 ≥ κε(EX2t )

2.

Hence κx ≡ E(X4t )/(EX2

t )2 ≥ κε. In the case that εt is normal and

κx > κε = 3, Xt has leptokurtosis (i.e. fat tails).

Example. ARCH(1) model:

Xt = σtεt, and σ2t = c0 + b1X2t−1,

where {εt} ∼ IID(0,1), c0 > 0 and b1 ∈ (0,1). Then EX2t = c0/(1−b1),

and for k ≥ 1,

Var(Xt+k|Xt−j, j ≥ 0) = Var(Xt+k|Xt)

= c0 + b1Var(Xt+k−1|Xt) =c0(1− bk1)

1− b1+ bk1X

2t ,

which indicates that a large value of |Xt| will lead to large predictive

risk (i.e. conditional variance) in a sustained period in the immediate

future.

Suppose εt ∼ N(0,1). Under the condition 3b21 < 1, Corr(X2t , X

2t+τ) =

b|τ |1 , and {X2

t } follows a causal AR(1) equation

X2t = c0 + b1X

2t−1 + et,

where et = (ε2t − 1)(c0 + b1X2t−1). Hence,

EX4t = Eσ4t Eε4t = 3Eσ4t

= 3(c20 +2c0b1EX2t + b21EX4

t )

= 3(1− b1)2(EX2

t )2 +6(1− b1)b1(EX2

t )2 +3b21EX4

t

= 3(1− b21)(EX2t )

2 +3b21EX4t .

The last equality uses the fact that c0 = (1− b1)EX2t . Hence

EX4t

(EX2t )

2=

3(1− b21)

(1− 3b21)> 3.

Hence Xt has leptokurtosis (fat tails).

A sample of 1000

were generated from

the ARCH(1) model:

c0 = 1.5, b1 = 0.9,

and εt ∼ N(0,1)

•

•

•••••

•••••

••

••

••••

•

•

••

•

••

••••••••

•

•

•

•

••••••

••••

•

••••

•••••••••••

•

•

••••••

•

•••

••

••

•••••••

•

•

•••

•

•••••••••

••

•••

•

••••••••

•

•

•

•

•

•

•

•

•••

•••

•

••••

•

•

••

•••••••••••

••••••••

••

••••••

•

•

••

•

•

••••

•

•

••

••••

•

•

•

•

•

•••

•

•

••

•

••

•

•••

••

•

••

•

••••

•

•

••

•••••••••

••

••

••••

•••

••••

•

•

•••

•

•

•

(a) ARCH(1) time series

t0 50 100 150 200 250

-10

-50

510

-15 -10 -5 0 5 10 15

0.0

0.05

0.10

0.15

0.20

0.25

(b) Histogram

•

•

•

••••••••••

••••••••

•

•••

•

•••••••••••

••

•••••••

•

••

•

•

••••

•••

•

••••••••••••••

••

••

•

••

••

•••••••

•

•

•••••••••••

••••

••

•

•••••••••

•

••

•

••

•

••••

•

•••••••

•

•

•

•

•••••••••••••••••••

••

••••••

••

••

•

•

••••••••••••••

•

••••

•

•

•••••••••••••••

•

•••••

•

••••••••••••

•

•

•

•••••

•

•

••••••

•••

•

•

(c) Conditional STD

t0 50 100 150 200 250

24

68

•

•

•••• •

• ••• •

• •••

• •••

•

•••

•

••

••

••••• •

•

•

•

•••• •

••

• •••

•

••••

•• ••

• •• •••••

••••••

•

••

• •

• •••

•••••••

•

•

• •••

•••••••

••

••• •

••

••••• • ••

•

•

•

•

•

•

•

•• ••

•••

••

• ••

•

•

••

••• •••

•••••

• •••• •

• •••

••

•• •••

•

••

••

•• ••

•

•

••• •

••

••

•

•

••

••

•

•••

•••

•

•••

• •

•••

•••

••

•

•

••• •••

•• •• •

••

••

•••

••

••

• ••••

••

• ••

•

•••

•

••••

•••

••

••

• •• ••

•••

••

••

•• •

• ••

• ••

•

••

••

• ••

• ••

••

••••

••

•

••

• •••

• ••

••

••••

•

•

•

•

•

•••

•••

•

••• • •

• • •

•

•

••

•

• ••• ••

••

•

••

••

•••

• ••

•• •••

•• •

•

•••

••

•• ••• •

••

••

•••

•

••

•

•

•

•

•

•

•

• •

• ••

••• ••••

••

•

•

•••••••

• •••••••

•

•

• •

•

•

•• • •

••

•••••

••••

••

•

•••

•

••

••• ••• • • •

••

•

•

•

••••

•

••

•

•••••

•

••

••

•

•

• ••••

•

•••

• ••

• •• •• ••

•••

••••••

••• • • ••••

•• • •••

••

••

•••••

•• •

••

•

•

•

•

•• •

••

••

•• ••• •

•••

•

•

•

•

•

•

••

•

• ••

•

•• •

•••••

••••

• •

•

•

••

•

•

•

•

•••

••••

• ••

••

• •• •••••

• •••

•

••• •••

• ••••

• ••

••

• •• •

•

• ••• • •

••

••

•••

••

• ••

•••

••

•

•

••••••

•• ••

••••

••

•••

•••••

•

•

••••• ••••• •

•

•

•••

•

•

•• •

••

•• • ••

••• • ••• •••

•••

••• •••

• • •••

•

•

•

••

•••

•

••

••

••

••

••

••

••

••

•

••

•• •••

•••••

••

••

••• •• •

• ••

•••••

••

••

•

•••

•••••

•••

••

•

•

•• ••••

••

•

••

•

••

•

••

• ••••

••

•

•

•

•

•• •

•

•••

• •• •

••••

•••• ••

• •

•

•••

••••••

••• ••

••• •••

•• •

•

•

•

•• ••

•••

•• •

•

•

••

••• • ••

• •

•••

••

•

•

• ••

•••

•

•••

••• • •• ••

••••• • •••

•••• •

•

••

•

•

•

•

••

•

•

•••

••

•

•

•• ••••

(d) QQ-plot

Normal quantile

AR

CH

qua

ntile

-2 0 2

-15

-10

-50

510

15

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(e) ACF

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(f) ACF of squared series

A sample of 1000

were generated from

the ARCH(1) model:

c0 = 1.5, b1 = 0.4,

and εt ∼ N(0,1)

•

•

•••••

•••

••

••

•

•

•

•••

•

•

••

•

•

•

•

•

•

••••

•

•

•

•

•

••••

•

•

•

••

•

•

•••

•

•••

•

•

•

•••••

•

•

•••

••

•

•

•

••

••

••

•••

•

••

•

•

•

•••

•

••

•

•

••

•

••

••

••

•

•

••••••••

•

•

•

•

•

•

•

•

••

•

•

••

•

•

•••

•

•

•

•

••

•

•••

••

••

•

••

•••

•

••

••

•

•

••••

•

•

•

•

•

•

•••

•

•

•

••

••

•

•

•

•

•

•

•

•

•

•

•

•

••

•

••

•

•

•

•

••

•

••

•

••

••

•

•

••

••••

•

•

•••

••

•

•

•

•

•

•

•

••

••••

•

•

•

••

•

•

•

(a) ARCH(1) time series

t0 50 100 150 200 250

-4-2

02

4

-6 -4 -2 0 2 4

0.0

0.1

0.2

0.3

(b) Histogram

•

•

•

••••••••

••

••

•

•

•

•••

•

•••

•

•

••

•••••••

•

•

•

•••••••

•

••

••

•••

•

•••

•

•••••••

•••••

•

•

•

•

•

•

•

••

••

•••••••

•

•

•••

•

•••••••

••••

••

•

•

•••••••

•

•

•

•

•••

•

•••

•

•

••

•••••

•

•

•

•

••

•

•••••••••

•••••••

••

•

•

••••

••

••

•

•

••••

••••••••

•

•

•

••••

••

•••

•

••

••

•••••••

•

••••

•

•

••••••••

••••

•

•

•

•

•

•

••

••

••••••

•

••

•

•

(c) Conditional STD

t0 50 100 150 200 250

1.0

1.5

2.0

2.5

3.0

•

•

••••

•

•••

• •

••

•

•

•

•••

•

•

••

•

•

•

•

•

•

••••

•

•

•

•

•

•••

•

•

•

•

••

•

•

•••

•

•• •

•

••

•••

••

•

•

••

•

••

•

•

•

••

••

••

•••

•

••

•

•

•

• ••

•

••

••

••

•

••

••

••

•

•

•••• • •

••

•

•

•

•

•

•

•

•

• ••

•

••

•

•

• ••

•

•

•

•

••

•

••

••

••

•

••

•••

•

• •

••

•

•

• • ••

•

•

•

•

•

•

••

•

•

•

•

••

• •

•

•

•

•

•

•

•

•

•

•

•

•

••

•

••

•

•

•

•

• •

•

••

•

••

••

•

•

••

••••

•

•

•• •

••

•

•

•

•

•

•

•

• •

••••

•

•

•

••

•

•

••

•

•

•••

•

••

•

•

•

•

•

••

••

•

•

••

•

•

•

•

•

••

• •

•

••

•

•

••

•

•

••

•

• •

•

••

•

•

••

••

•

•

•

••••

••

•

•

•

••

• •

•

•

•

•

•

••

•

•••

•

••••

••

• •

•

•

•

••

•

•••

•

••

•

•

•

• •

•

•

••

•

••

•

•

••••

•

••

•

•

••

•

•

••••

••

•

•

•

•

••

•

•

•

•

•

•

•

•

•

•

•

••

•

•

•

• ••

•••

•

••

•

•

•••

••

•

•

•

••

••••

•

•

•

••

•

•

•

•• •

•

•

•

••••

••

••

••

•

•

••

•

•

•

• •

••••

• • •

•

•

•

•

•

•

•••

•

••

•

•••

••

•

••

•

•

•

•

••

••

•

•

••

•

••

•

••

• ••

•

•

•

••

•••

••

•

•

••

•• •

••••

••

•••

•

•

•

•

••• •

•

•

••

•

•

•

•

•

•

•

••

••

•••

•

••

• ••

••

•

•

•

•

•

•

•

•

•

•

•

•

•

•••

••

•••

••

•••

••

•

•

•

•

•

•

•

•

• ••

••••

••

•

•

••

••

••••

•

• •••

•

•••

••

•

••

••

•

•

•

•

•

•

•

•

••

•

•

•

•••

•

•

•

•

•

•

••

•

•

••

••

••

••

•

•

•

•••• •

•

• ••

••

•

•

••

••

•

••

•

••

•

•

• •• ••

••

••••

•

•

•••

•

•

••

•

•

•

••

••

•

•

•••

••

••

••

•

•

•

•••••

•

••

••

•

•

•

•

•

••

••

•

•

•

•

•

••

•

••

•

•

•

•

•

•

•

•

•

••

•

•

•

•

•

••••

•

•

•

•

•

•••

•

•

••

••

•••

•

••

••

•

••

••••

••

•

••

•

•

•

•

••

••

••

•

••

•

•

•

•

•

•

••

••

••

•

•

•

•

•

•

•

•

•

•

•

•

••

••

••

•

•••

•

•••••

••

•

••

••

•

••••

••

••

•

•••

••

•

••

•

•

•

•

•

••••

••

•

•

••

•

•

•

•

••••

•

•

• •

••

•

••

•

•

••

•

•

••

•

•

••

••

•

••

••

•

••

••

••

••

•

•

• •

••

•

•

•

•

•

•

•

•••

•• ••

•

•

•

•

•

••••

•

(d) QQ-plot

Normal quantile

AR

CH

qua

ntile

-2 0 2

-4-2

02

4

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(e) ACF

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(f) ACF of squared series

(a) and (c) the time plots of the first 250 X ′ts and σ′

ts; (b) the normalized histogram,

and the normal density function with the same mean and variance; (d) the sample

quantiles are plotted against the quantiles of N(0,1); (e) and (f) the sample ACFs

of {Xt} and {X2t } respectively.

(i) Large values of |Xt| leads to large σt.

(ii) {Xt} ∼ WN.

(iii) Heavy tails: heavier for larger b1.

(iv) ρ(k) ≈ ρ(k) for b1 = 0.4 but not for b1 = 0.9.

Basic properties of GARCH processes

Extension of ARCH:

dictated by economic insight, or

broadly statistical ideas.

Most important extension: generalized ARCH (GARCH) due to Boller-

slev (1986) and Taylor (1986).

ARCH(p) is useful only with large p in practice. GARCH provides a

parsimonious representation for complex auto-dependence structure.

GARCH(1,1): a widely used benchmark model.

GARCH(p,q): Xt = σtεt, σ2t = c0 +∑p

i=1 biX2t−i +

∑qj=1 ajσ

2t−j,

where c0 ≥ 0, bj ≥ 0 and aj ≥ 0 , {εt} ∼ IID(0,1), and εt is independent

of {Xt−k, k ≥ 1} for all t.

Let

et = X2t − σ2t = (ε2t − 1)(c0 +

p∑

i=1

biX2t−i +

q∑

j=1

ajσ2t−j).

Then

X2t = c0 +

p∑

i=1

biX2t−i +

q∑

j=1

ajσ2t−j + et

= c0 +p∨q∑

i=1

(bi + ai)X2t−i + et −

q∑

j=1

ajet−j,

where bp+j = aq+j = 0 for j ≥ 1. Thus {X2t } follows an ARMA

equation.

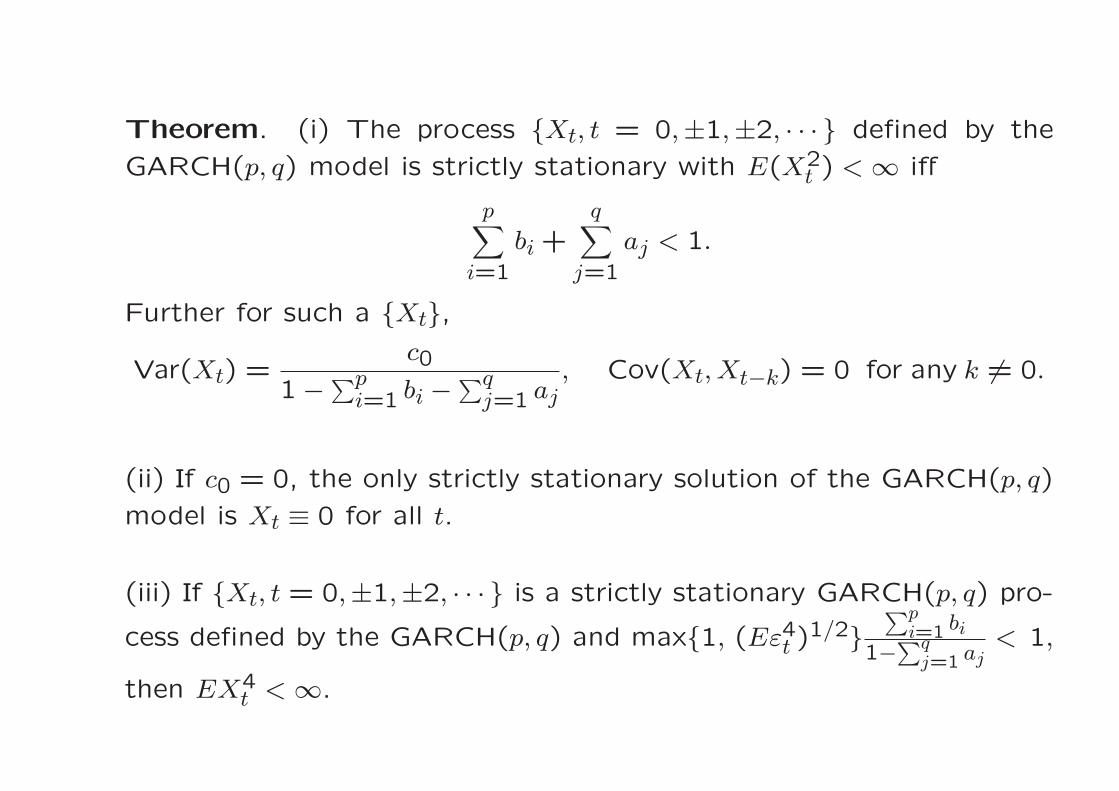

Theorem. (i) The process {Xt, t = 0,±1,±2, · · · } defined by the

GARCH(p, q) model is strictly stationary with E(X2t ) < ∞ iff

p∑

i=1

bi +q∑

j=1

aj < 1.

Further for such a {Xt},

Var(Xt) =c0

1− ∑pi=1 bi −

∑qj=1 aj

, Cov(Xt, Xt−k) = 0 for any k 6= 0.

(ii) If c0 = 0, the only strictly stationary solution of the GARCH(p, q)

model is Xt ≡ 0 for all t.

(iii) If {Xt, t = 0,±1,±2, · · · } is a strictly stationary GARCH(p, q) pro-

cess defined by the GARCH(p, q) and max{1, (Eε4t )1/2}

∑pi=1 bi

1−∑q

j=1 aj< 1,

then EX4t < ∞.

Note. Bougerol and Picard (1992) established a necessary and suf-

ficient condition for the existence of a strictly stationary solution of

the GARCH model, which may not have finite second moment. The

condition is defined in terms of Lyapunov exponents for some random

matrices associated with the model and is typically difficult to check

in practice.

Remark. (i) Stationary GARCH process is WN(0, c0(1 − ∑pi=1 bi −∑q

j=1 aj)).

(ii) The ARMA representation for X2t

X2t = c0 +

p∨q∑

i=1

(bi + ai)X2t−i + et −

q∑

j=1

ajet−j

is causal and invertible, where et = X2t − σ2t . Thus

(a) Formally {X2t } ∼ AR(∞)

(b) EX2t = Eε2t Eσ2t = Eσ2t , and E(Xt|Xt−1, Xt−2, · · · ) = 0.

(c) Eet = E(et|Xt−1, Xt−2, · · · ) = 0

(d) Var(Xt|Xt−1, Xt−2, · · · ) = E(X2t |Xt−1, Xt−2, · · · )

= c0 +∑p

i=1 biX2t−i +

∑qj=1 ajσ

2t−j = σ2t .

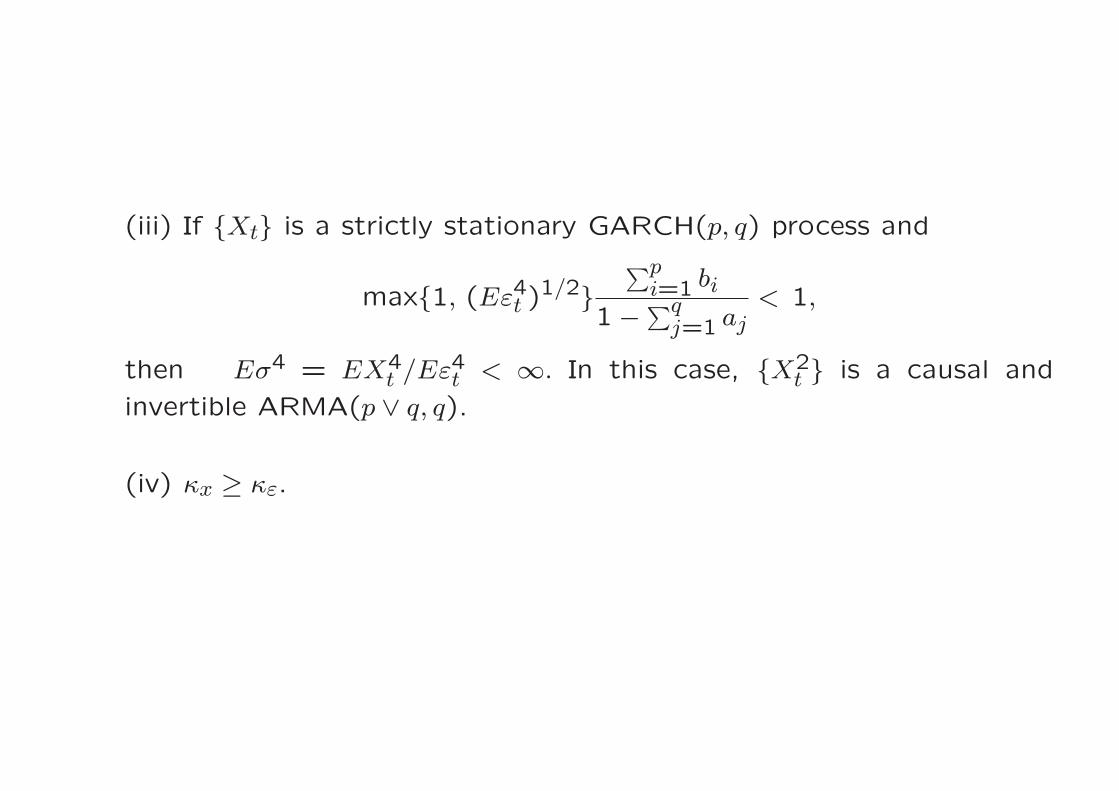

(iii) If {Xt} is a strictly stationary GARCH(p, q) process and

max{1, (Eε4t )1/2}

∑pi=1 bi

1− ∑qj=1 aj

< 1,

then Eσ4 = EX4t /Eε4t < ∞. In this case, {X2

t } is a causal and

invertible ARMA(p ∨ q, q).

(iv) κx ≥ κε.

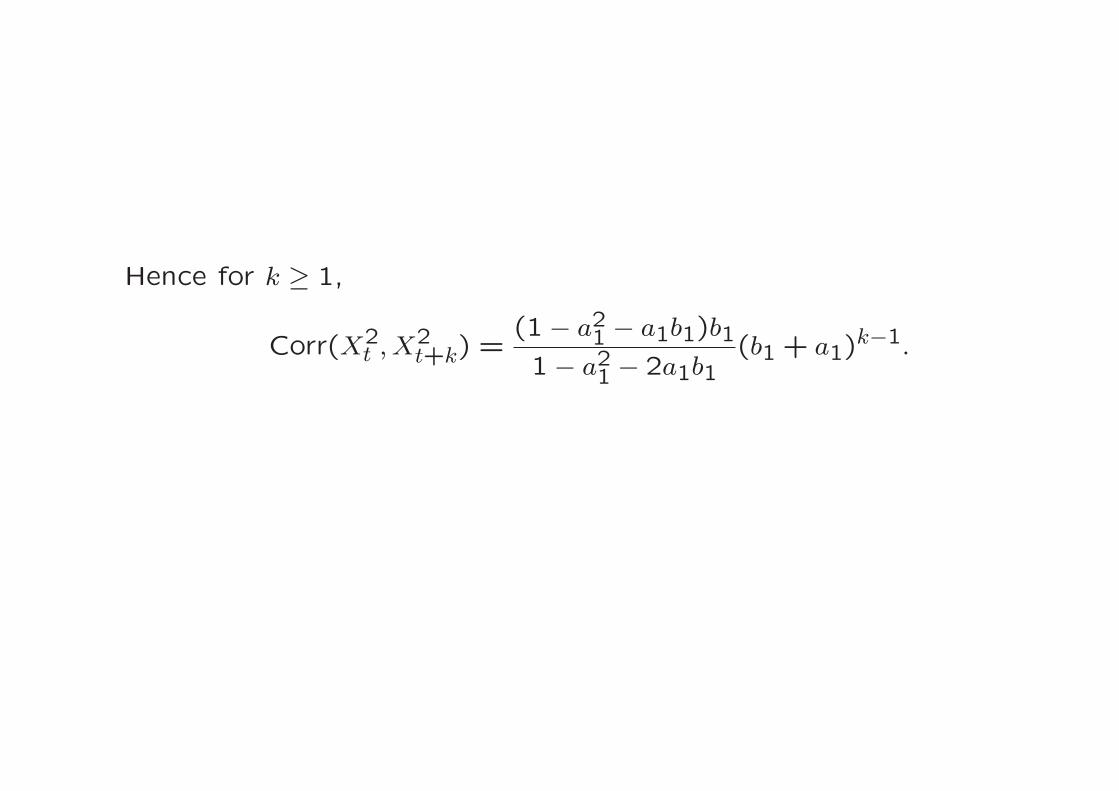

Example. GARCH(1,1) model: Xt = σtεt and

σ2t = c0 + b1X2t−1 + a1σ

2t−1,

where c0, b1 and a1 are positive, b1 + a1 < 1, and {εt} ∼ IID(0,1).

Then EX2t = c0/(1− b1 − a1). Note

(1− a1B)σ2t = c0 + b1X2t−1.

Thus

σ2t =∞∑

j=0

aj1B

j(c0 + b1X2t−1) =

c01− a1

+ b1

∞∑

j=0

aj1X

2t−j−1.

and

Var(Xt|Xt−k, k ≥ 1) =c0

1− a1+ b1

∞∑

j=0

aj1X

2t−j−1,

which is a marked difference from ARCH(1) process for which

Var(Xt|Xt−k, k ≥ 1) depends on Xt−1 only: volatility cluster is more

persistent in GARCHprocesses than in ARCHprocesses.

Nelson (1990) showed that the necessary and sufficient condition for

existence of a strictly stationary GARCH(1,1) process is

E{log(b1ε2t + a1)} < 0.

By Jensen’s inequality,

E{log(b1ε2t + a1)} ≤ logE(b1ε2t + a1) = log(b1 + a1).

Hence, the condition b1 + a1 < 1 is sufficient for the existence of a

strictly (also weakly) stationary solution. If εt is normal, and

1.732b1 < 1− a1,

EX4t < ∞. Then {X2

t } is a causal and invertible ARMA(1,1) process

X2t = c0 + (b1 + a1)X

2t−1 + et − a1et−1,

where

et = (ε2t − 1)(c0 + b1X2t−1 + a1σ

2t−1).

Hence for k ≥ 1,

Corr(X2t , X

2t+k) =

(1− a21 − a1b1)b1

1− a21 − 2a1b1(b1 + a1)

k−1.

A sample of 1000

were generated from

the GARCH(1,1)

model: c0 = 1.5,

b1 = 0.6, a1 = 0.3,

and εt ∼ N(0,1)

•

•••

••

•••

•

••••

•

•

•••••••••••

••

•

•

••

••

•••

••••

•

••••

•

•

••

•

•

•••

•

••••••••••••

••••

•

••

•••

•••

••

••

••

••

••

•

•••

••

••••

•

•

•

•

•

••

••

•••

•

•

••

•••

•

•

•

•

••

•

•••

•

••••••

•••

•

•

••

•

•••••••••

••

•

•

••

•••

•

••••••••

•

•••••

••••••

•

••

•

•••

•

••

•

•

•

•

•

•

•

••

•

•

•

•••••••

••

•

•

••••••••••

••••••

•

••

•

•

••••••

•••••

(a) GARCH(1,1) time series

t0 50 100 150 200 250

-15

-10

-50

510

15

-15 -10 -5 0 5 10 15

0.0

0.05

0.10

0.15

(b) Histogram

••••••••••••••••

•

••••••••••••

•

••

•••••

••

•••••••••

•

•••

••

•••

••••••••••••

••••

•

•••

•••

•••••••••••••

•

•••

••

••••

••

•

•

•

•

•

•••••••••

••

•

•

•

•

•••

•

•

••••••••••••

•

•••

••••••••••••

••

••

•••••••••••••••••

•

•••••••••••••

•

•••

•

•

•

•

•

•

••

••••••••••••••

•••••••••••••••

•••••

•••••••••••

(c) Conditional STD

t0 50 100 150 200 250

24

68

1012

•

••

•

• •

•••

•

••••

•

•

•••

••••

••• •

••

•

•

••

••

•• •

••••

•

••

• •

•

•

••

•

•

•••

•

•••

••

••

••••

•

•••

•

•

••

••

•

• ••

• •

••

• •

••

••

•

• ••

••

•••

•

•

•

•

•

•

••

••

••

•

•

•

••

•••

•

•

•

•

••

•

••

•

••••

••

• ••

•

•

••

•

•••

••

••

••

• •

•

•

••

•• •

•

•••••

••

•

•

•••

••

••••

• •

•

••

•

••

•

•

••

•

•

•

•

•

•

•

••

•

•

•

••• •••

•

••

•

•

•••

••

••

•••

••••

••

•

••

•

•

••

•••

•

•••••

••••

••

•

••

•

•

••

•••

••• • ••

••

•

•

•

•

•••

•

••

•

••••

•

•

••

•

•

•

•

•••

•

•

•

•••

•••

• •• •••

•

•••

•••••

•

•

•• •

• ••••

•

• • •••

••

•

•••••

•

••

•

•

•

•

•

•

•

•

••

•

•

•••

•• •• • •

••

•

•

•

•

•

•

•

•

•

•

•••

•

• ••

••

•••

• ••••

• •

•

•

• •

•

•

•

•

• ••

••••

••

•

•

••

•• •••••

••••

•

••• ••

•

• ••••

••

••

••

•

• ••

•

•

• • • ••

•

••

•••

••

• ••

•••

••

•

•

••••••

•• ••

••••

••

••

•

•••

••

•

•

• •••• ••

•••••

•

•• •

•

•

•••

•

•

••

••

•

••• •

•••

••••

••

•• • •••

• •••

•

•

•

•

••

•••

•

••

•

•

••

••

••

•

•

•

•

••

•

••

••

••

••

•••••

••

•

••• ••

•

• ••

•••••

••

••

•

•••

•••••

•••

•

•

•

•

••

••••

••

•

•

•

•

•

•

•

••

• ••

••

••

•

•

•

•

•

•

•

•

•

•

•

• •

••

•

•••

•

••• ••••

•

••

••

•••••••

• ••

••••

••

•••

•

•

•

•

••••

•••

•

• •

•

•

•

•

•••

• •

•

• •

••

•

••

•

•

••

•

•

••

•

•

••

•••

• ••

••

••••

• • ••

•

•

• ••

••

••

•

•

•

•

••

•

•

•••

•

•

•

•

•

•••••••

•••

••

•

••

•

••

•• ••

••

•

• •• ••

•• ••

••

•

••

••

•••

•• ••

•

••

• •

•

•••

•

•

••

•

••••

••

• ••

••••

• •••

••

•••

•

•

•

••

••

• •• •••

•••••

••

•

•••

•

••••

•

••••

••

••

••••

•• •

••

•

•

••••

••

• •

•••••

•

•

•

•

••••

••

••

•

•

•••••

•• •

•••

•

•••••

•••

••

• •••

•

•••• ••

••

• •• •

• ••

•

(d) QQ-plot

Normal quantile

GA

RC

H q

uant

ile

-2 0 2

-15

-10

-50

510

15

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(e) ACF

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(f) ACF of squared series

A sample of 1000

were generated from

the GARCH(1,1)

model: c0 = 1.5,

b1 = 0.3, a1 = 0.3,

and εt ∼ N(0,1)

•

•

•

•

••

•

••

•

••

••

•

•

••

•

•••

•

•

•••

••

•

•

•

•

•

•

•

••

••••

•

•

•

••

•

•

••

•

•

•••

•

••

•

•

•

•

•

•

••

•

•

•

••

•

•

•

•

•

•

•

••

•

••

•

•

••

•

•

•

•

•

••

•

••

•

•••

•

•

•

•

•

••

••

••

•

•

•

•

•

••

•

•

•

•

•

••

•

•••

•

•••

•

••

••

•

•

•

••

•

•••

•

•

•

•

•

•

••

•

•

••

•

••

•

•

••••

•

•

•

•

•

••

•

•

••

••

••

•

•

•

•

••

•

•

•

•

•

•

•

•

•

•

•

••

•

•

•

••

•••

•

•

••

•

•

•••

••

•

•

•

••

•••

•

•

•

•

•

•

•

•

•

•••

•

•

•

••••

(a) GARCH(1,1) time series

t0 50 100 150 200 250

-6-4

-20

24

-6 -4 -2 0 2 4

0.0

0.05

0.15

0.25

(b) Histogram

•

•••••••••

•

•••••

•

•

•••••••

••••

•

•

•

••

•••

••

••••••

•••

•

•••

•

•

•••

•

•••••••••••

•

•••

•

•••

•

••

••

•

•••

•••

••

••

•

•

••

••

•

•

••

••

••

•

••••••

•

••••

••

•

•

•

•

•••

•

•

••

••••••••••

•

•••

•

••••••••

•

••

•

•

••

•

•

•

••

•••••••

•

••••

•

••••••

•

••

••••

•

•

••

•

•

•

••

•

•

•

•••••••••

•

••••

•••••••

•

••••••

•

••

•••

•

•

••••

•••••

(c) Conditional STD

t0 50 100 150 200 250

1.5

2.0

2.5

3.0

3.5

•

•

•

•

••

•

••

•

••

••

•

•

••

•

•••

•

•

••

•

••

•

•

•

•

•

•

•

••

••••

•

•

•

••

•

•

••

•

•

•••

•

••

•

•

•

•

•

•

••

•

•

•

••

•

•

•

•

•

•

•

••

•

••

•

•

•

•

•

•

•

•

••

•

••

•

••

•

•

•

•

•

•

••

••

••

•

•

•

•

•

••

•

•

•

•

•

••

•

•••

•

•••

•

••

••

•

•

•

••

•

•••

•

•

•

•

•

•

••

•

•

••

•

••

•

•

••••

•

•

•

•

•

••

•

•

••

••

••

•

•

•

•

••

•

•

•

•

•

•

•

•

•

•

•

••

•

•

•

• •

•••

•

•

••

•

•

•••

••

•

•

•

••

•••

•

•

•

•

•

•

•

•

•

••

•

•

•

•

••••

••

•

•

••

•

•

••

•

•

•

• •

••••

•• •

•

•

•

•

•

•

• ••

•

••

•

••

••

•

•

••

•

•

•

•

••

••

•

•

••

•

•

•

••

•••

•

•

•

••

•••

•

••

•

•

••

••

•••

•

••

••

•

•

•

•

•

••• •

•

•

•

•

•

•

•

•

•

•

•

••

•

•

•••

•

••

••

•

•

•

•

•

•

•

•

•

•

•

•

•

•

••

•

• ••

••

•••

••

•••

••

•

•

•

•

•

•

•

•

• ••

••••

••

•

•

•

•

••

•••

•

•

••••

•

•

• ••

•

•

•

•

••

•

•

•

•

•

•

•

•

••

•

•

•

•••

•

•

•

•

•

•

••

•

•

• •

••

••

••

•

•

•

•••• •

•

• ••

••

•

•

••

••

•

••

•

••

•

•

••• •

•••

••••

•

•

•

••

•

•

••

•

•

•

••

••

•

•

•••

••

•

••

•

•

•

•

•• •

••

•

••

••

•

•

•

•

•

•

•

••

•

•

•

•

•

•

••

••

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

••••

•

•

•

•

•

•••

•

•

•

•

•

•••

••

••

••

•

••

•

•••

••

•

••

•

•

•

•

•

•

••

••

•

•

•

•

•

•

•

•

•

••

••

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

••

••

•

•••

•

•••••

••

•

••

•

••

••

••

••

••

•

•••

•

•

•

••

•

•

•

•

•

••••

•

••

•

••

•

•

•

•

••••

•

•

••

•

•

•

••

•

•

••

•

•

••

•

•

••

••

•

••

•

•

•

••

••

••

•

•

•

•

••

••

•

•

•

•

•

•

•

••

•

•

•••

•

•

•

•

•

•

•••• ••

••

••

•

•

•

•

•

•

••

•••

•

•

•

•

• ••

•

•

••

•

•

•

•

•

••

•

•

••

•

•

• ••

•

•

••

•

•

•

••

•

•

• •

•

•

•••

•

•

••

•

••

•

•

••

••

••

••

••

•

•

••

•

••

•••

•

•

•••

••

•

•

•

•

••

••

•

•••

•

•••

•

••

•

•

•

•••

••

•

•

•

•

•

•••

•

•

•

••

•• •

••

•

•

•

•

••

••

••

•

•

•

•

••

•••

•

••

••

•

•

•

••• •

•

••

•

•

••

••

•

•

••••

•

•

•

••

••

••

•

•

(d) QQ-plot

Normal quantile

GA

RC

H q

uant

ile

-2 0 2

-6-4

-20

24

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(e) ACF

Lag

AC

F

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

(f) ACF of squared series

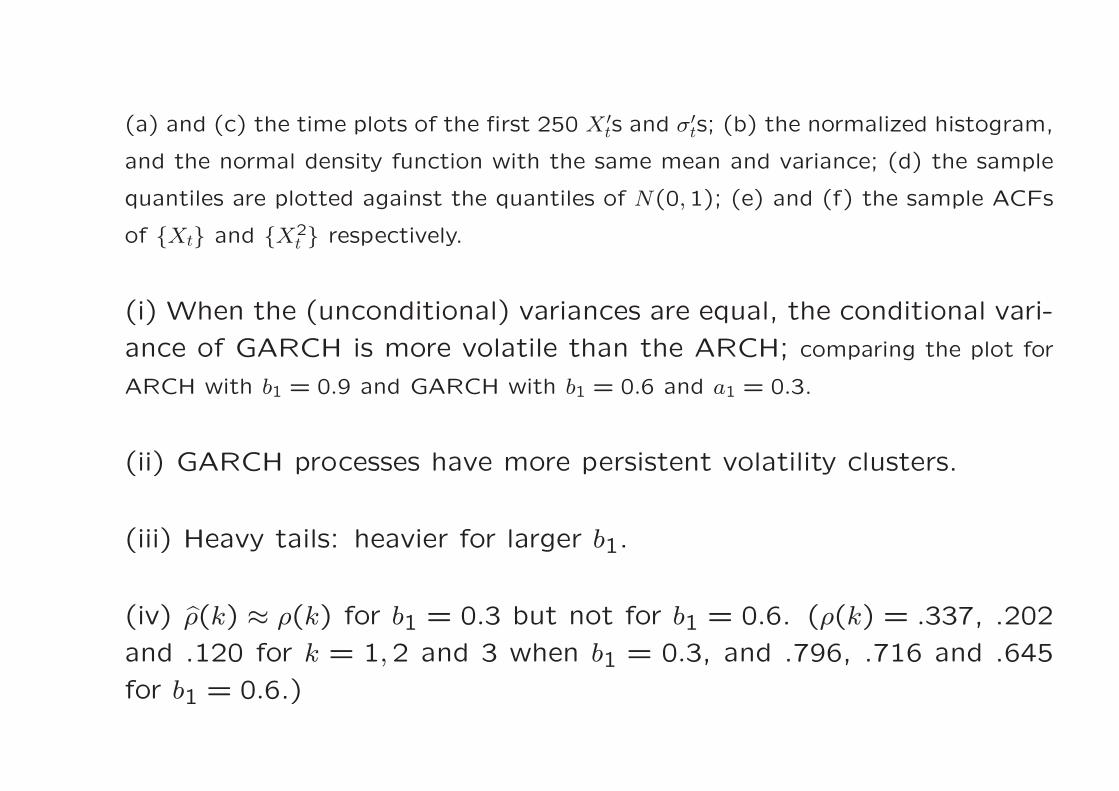

(a) and (c) the time plots of the first 250 X ′ts and σ′

ts; (b) the normalized histogram,

and the normal density function with the same mean and variance; (d) the sample

quantiles are plotted against the quantiles of N(0,1); (e) and (f) the sample ACFs

of {Xt} and {X2t } respectively.

(i) When the (unconditional) variances are equal, the conditional vari-

ance of GARCH is more volatile than the ARCH; comparing the plot for

ARCH with b1 = 0.9 and GARCH with b1 = 0.6 and a1 = 0.3.

(ii) GARCH processes have more persistent volatility clusters.

(iii) Heavy tails: heavier for larger b1.

(iv) ρ(k) ≈ ρ(k) for b1 = 0.3 but not for b1 = 0.6. (ρ(k) = .337, .202

and .120 for k = 1,2 and 3 when b1 = 0.3, and .796, .716 and .645

for b1 = 0.6.)

Bougerol and Picard (1992) proved: the GARCH(p, q) model admits

a strictly stationary solution {Xt} with EX2t = ∞ if

p∑

i=1

bi +q∑

j=1

aj = 1,

and the distribution of εt has unbounded support and has no atom at

zero.

The GARCH processes fulfilled the above equation has been unfor-

tunately called integrated GARCH(p, q) (IGARCH) processes, in anal-

ogy to integrated ARMA (ARIMA) processes (i.e. processes with unit

roots).

Note. ARIMA processes are always non-stationary while an IGARCH

process may be strictly stationary.

Estimation

Observations: X1, · · · , XT be observations for a (G)ARCH process.

Goal: to estimate the parameters in the model.

5.1 Conditional MLE.

For ARCH(p) model

Xt = σtεt, and σ2t = c0 + b1X2t−1 + · · ·+ bpX

2t−p,

if we know the pdf p(·) of εt, the (conditional) log-likelihood function

is

l({bj}, c0, σ2) =T∑

t=p+1

{log p(Xt/σt)− logσt}.

The MLEs for c0, b′js and σ2 could be obtained by maximising the

above function.

Often we use qMLE resulted from assuming εt ∼ N(0,1),

l({bj}, c0, σ2) = −1

2

T∑

t=p+1

{X2t

σ2t+ logσ2t }

Note. (i) Under some mild regularity conditions, the qMLE is con-sistent. The asymptotic normality requires more conditions such asEε4t < ∞ (which may be questionable in financial application).

(ii) For a GARCH model with

σ2t = c0 +p∑

i=1

biX2t−i +

q∑

j=1

ajσ2t−j,

it can be shown that

σ2t =c0

1− ∑qj=1 aj

+p∑

i=1

biX2t−i

+p∑

i=1

bi

∞∑

k=1

q∑

j1=1

· · ·q∑

jk=1

aj1 · · · ajkX2t−i−j1−···−jk

.

Apply truncation: define for t > p

σ2t =c0

1− ∑qj=1 aj

+p∑

i=1

biX2t−i

+p∑

i=1

bi

∞∑

k=1

q∑

j1=1

· · ·q∑

jk=1

aj1 · · · ajkX2t−i−j1−···−jk

I(t− i− j1 − · · · − jk ≥ 1).

The conditional MLE (b, a, c0) minimises

T∑

t=ν

{log σt − log f(Xt/σt)} ,

where ν > p+1.

(iii) The estimation for conditional second moments is more difficult

than that for conditional mean; the likelihood functions tend to be

rather flat (unless T is very large).

Simulation with 1000 replications for ARCH(1) with b1 = 0.9, c0 = 0.2

and εt ∼ N(0,1)

T Eb1 MSE(b1) P (b1 ≥ 1)

100 .8522 .2574 .266250 .8839 .1636 .239500 .8927 .1066 .1521000 .8980 .0814 .100

Simulation with 1000 replications for GARCH(1,1) with b1 = c0 = 0.2,

a1 = 0.7 and εt ∼ N(0,1)

T E(b1 + a1) MSE(b1 + a1) P (b1 + a1 ≥ 1)

100 .8787 .1467 .206250 .8868 .1025 .143500 .8968 .0658 .0601000 .8991 .0489 .019

(vi) To increase the fatness of tails, we may let εt have one of the

following distributions (all with tails heavier than normal):

(a) t(k): fk(x) =Γ((k+1)/2)

(πk)1/2Γ(k/2)1

(1+x2/k)(k+1)/2.

(b) Double exponential distribution:

f(x) = 2−1/2 exp{−√2|x|}.

(c) Generalized Gaussian distribution:

f(x) =k

λ21+1/kΓ(1/k)exp{−1

2|x/λ|k},

where λ = {2−2/kΓ(1/k)/Γ(3/k)}1/2.

Note. All above distributions have been normalised with variance 1.

(v) Model selection: We may use AIC or BIC to determine the orders

of model.

AIC = −2(maximised log likelihood)

+ 2(No. of estimated parameters)

BIC = −2(maximised log likelihood)

+ logT (No. of estimated parameters)

Let θ = (c0, b1, · · · , bp, a1, · · · , aq)τ , Ut =∂σ2t∂θ . Then Ut/σ

2t has all its

moments finite. Suppose M ≡ E(UtU

τt /σ

4t

)> 0.

Asymptotic properties. Suppose

(i)∑

i bi +∑

j aj < 1,

(ii) all bi and aj are positive.

Then

(i) If E(ε4t ) < ∞, T1/2

{E(ε4t )−1}1/2(θ − θ)D−→ N(0,M−1).

(ii) If E(|εt|4−η) < ∞ for any η > 0 and E(ε4t ) = ∞, θ is

asympotically normal with a convergnece rate slower than T1/2

(iii) If E(|εt|α) = ∞, for some α ∈ (0,4), θ is no longer asymp-

totically normal.

L1-estimation

Model: Xt = σtεt, εt ∼ (0,1), and

σ2t ≡ σt(θ)2 = c0 +

p∑

i=1

biX2t−i +

q∑

j=1

ajσ2t−j,

where θ = (c0, b1, · · · , bp, a1, · · · , aq)τ .

Reparametrisation: Eεt = 0, Median(ε2t ) = 1.

Note. Under the new parametrisation, c0 and bi’s differ by a common positive

constant factor while aj’s unchanged

Now

X2t /σ

2t = 1+ (ε2t − 1).

This leads to

θ1 = argminθ

T∑

t=ν+1

|X2t /σt(θ)

2 − 1|.

Note: Median(ε2t ) = 1 iff Median{log(ε2t )} = 0. Write

log(X2t ) = log{σt(θ)}2 + log(ε2t ).

This leads to

θ2 = argminθ

T∑

t=ν+1

| log(X2t )− log{σt(θ)2}|.

It we write

X2t = σ2t + et,

where et = σ2t (ε2t − 1) has median 0. This leads to

θ3 = argminθ

T∑

t=ν+1

|X2t − σt(θ)

2|.

Asymptotic normality. Suppose

(i)∑

i “bi”+∑

j aj < 1,

(ii) all bi and aj positive,

(iii) log ε2t has the unique median zero, and its density function

f is continuous at zero.

Then,

(i) T1/2(θ2 − θ) is asymptotically normal with mean 0

(ii) T1/2(θ1−θ) is also asymptotically normal with a non-zero

mean (i.e. bias).

(iii) The asymptotic normality for T1/2(θ3 − θ) requires more

conditions such as Eε4t < ∞.

Simulation comparison of conditional MLE and LADE

ARCH(2): σ2t = c0 + b1X2t−1 + b2X

2t−2

GARCH(1,1): σ2t = c0 + b1X2t−1 + a1σ

2t−1

with c0 = 3, b1 = 0.5 and b2 = a1 = 0.4

εt ∼ N(0,1), t3 or t4. (E|εt|d = ∞ if εt ∼ td.)

Sample size: 300 Simulation replications: 500

The average absolute error (AAE):

(|b1/c0 − b1/c0|+ |b2/c0 − b2/c0|)/2 (for ARCH(2)),

(|b1/c0 − b1/c0|+ |a1 − a1|)/2 (for GARCH(1,1)),

Estimates were obtained through exhausting search.

0.0

0.2

0.4

0.6

0.8

t(3)MLE

t(3)LADE1

t(3)LADE2

t(3)LADE3

t(4)MLE

t(4)LADE1

t(4)LADE2

t(4)LADE3

NormMLE

NormLADE1

NormLADE2

NormLADE3

(a)

0.0

0.4

0.8

1.2

t(3)MLE

t(3)LADE1

t(3)LADE2

t(3)LADE3

t(4)MLE

t(4)LADE1

t(4)LADE2

t(4)LADE3

NormMLE

NormLADE1

NormLADE2

NormLADE3

(b)

Tests for ARCH effect

Tests on GARCH models can be divided into two categories:

1. The LR tests can be constructed in the standard manner.

2. Apply the standard tests for ARMA models to the process {X2t }.

Suppose that {Xt} is a strictly stationary process defined by

Xt = σtεt, σ2t = c0 +p∑

i=1

bjX2t−i,

where c0 > 0 and aj ≥ 0.

We are interested in testing

H0 : b1 = · · · bp = 0

against

H1 : bj 6= 0 for at least one j.

Suppose the density function f(·) of εt in is known, the (conditional)

likelihood ratio test based on the test statistic

T∏

t=p+1

σt(c0, b)−1f{Xt/σt(c0, b)}

σt(c0,0)−1f{Xt/σt(c0,0)},

where (c0, b) is the (conditional) MLE for an ARCH(p) model, and c0is the constrained (conditional) MLE under H0.

Under the null hypothesis H0

2 log(ST,1)D−→ χ2

p

provided that the density function f(·) is enough smooth, and theFisher information matrix

I(c0,b) ≡(

I11(c0,b) I12(c0,b)I21(c0,b) I22(c0,b)

)= E{ℓ(Xt; c0,b)ℓ(Xt; c0,b)}τ .

exists and is positive-definite; see §4.4.4 of Serfling (1980). (Those

conditions are fulfilled for GARCH models with εt ∼ N(0,1).) In the

above expression, ℓ(Xt; c0,b) denotes the derivative of log[σ−1t f(Xt/σt)]

with respect to (c0,b).

The above asymptotic distribution under the null hypothesis is also

shared by both score test and Wald test.

The score test is also called the Lagrange multiplier test by econome-

tricians. It is based on the fact that the gradient of a log-likelihood

function should be close to 0 under a null hypothesis. More precisely,

it can be shown that under H0,

1√T − p

T∑

t=p+1

ℓ2(Xt; c0, 0)D−→ N(0, I22(c0, 0)),

where

ℓ2(Xt; c0,b) =∂

∂blog[σ−1

t f(Xt/σt)],

and I22 is defined in the above Fisher information matrix.

The score statistic is defined as

ST,2 =1

T − p{

∑

t=p+1

ℓ2(Xt; c0, 0)}τ{I22(c0, 0)}−1

×∑

t=p+1

ℓ2(Xt; c0, 0).

If εt is normal, Engle (1982) shown that the score test may be per-

formed in terms of the statistic TR2 which is asymptotically equiva-

lent to ST,2, where R2 is the multiple correlation coefficient of Xt and

(Xt−1, · · · , Xt−p), namely

R2 = Xτp+1X (X τX )−1X τ

Xp+1/(Xτp+1Xp+1),

where Xk = (X2k , X

2k+1, · · · , X2

T−p−1+k)τ , X = (1,Xp,Xp−1, · · · ,X1),

and 1 is a vector with all components 1.

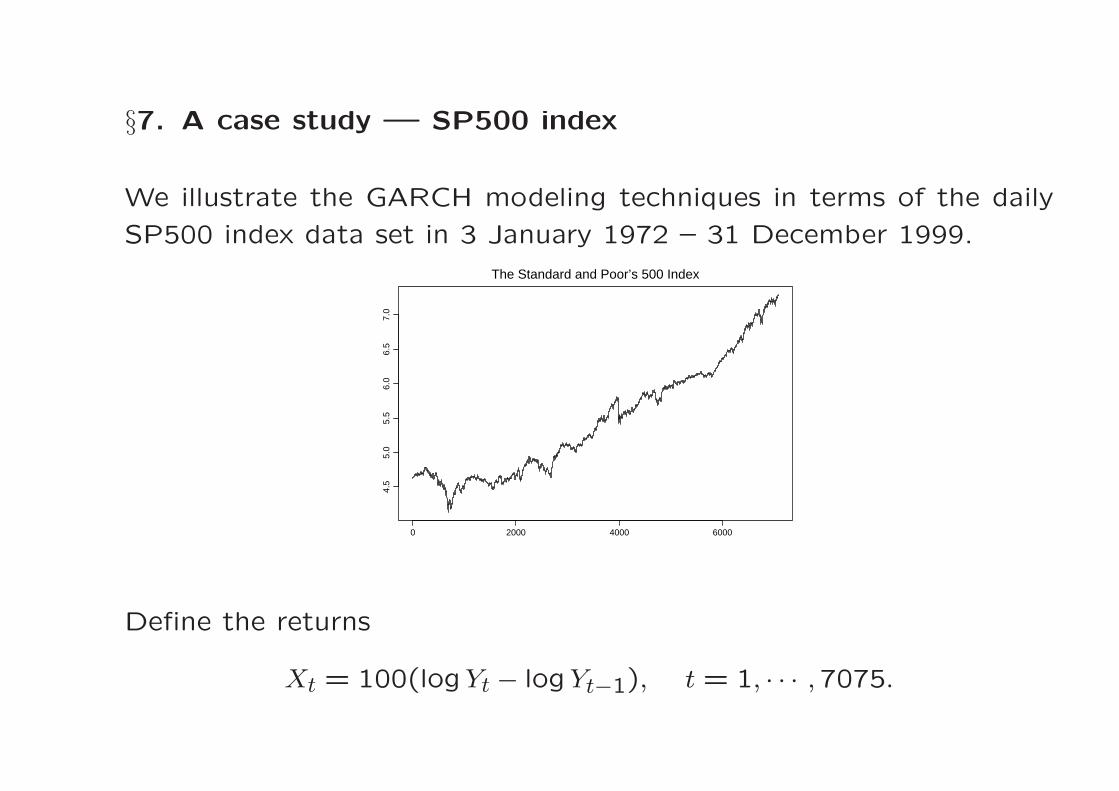

§7. A case study — SP500 index

We illustrate the GARCH modeling techniques in terms of the daily

SP500 index data set in 3 January 1972 – 31 December 1999.

0 2000 4000 6000

4.5

5.0

5.5

6.0

6.5

7.0

The Standard and Poor’s 500 Index

Define the returns

Xt = 100(logYt − logYt−1), t = 1, · · · ,7075.

Graphical investigation

-20 -15 -10 -5 0 5 10

0.0

0.1

0.2

0.3

0.4

0.5

Histogram of the SP500 returns and a normal density function with the

same mean and variance.

The histogram has a long stretch on its left due to the single large

negative return — the stock market crash of October 1987. However

if we discard this single ‘outlier’, the marginal distribution seems fairly

symmetric but not normal.

Lag

AC

F

0 20 40 60 80 100

0.0

0.2

0.4

0.6

0.8

1.0

(a) ACF of returns

Lag

AC

F

0 20 40 60 80 100

0.0

0.2

0.4

0.6

0.8

1.0

(b) ACF of squared returns

The correlogram of (a) the SP500 returns, and (b) the squared returns.

There is almost no significant autocorrelation in the return series {Xt}itself, but such a autocorrelation does exist in the squared series {X2

t }.

The sample quantiles of the

SP500 returns are plotted

against, respectively, the

quantiles of N(0,1) and

t-distributions with degrees

of freedom between 7 and

3.

Both tails the empirical dis-

tribution of the returns are

heavier than those of N(0,1)

and tk for k = 6 and 7, is

considerably lighter than t3.

Therefore,

E(X6t ) = ∞, E(|Xt|3−ǫ) < ∞

for any ǫ > 0.

• •••• ••••••• •••

••••• • •• •• • ••••

•••• ••• •• • •• • •••••••• •••

• •••••

•• • •••• ••• •• •• •••• • • •• • • ••••

•• ••• • •••• •••••••• •• •• • • •••• ••••• •• • •• • •

••• •••

• • ••• •

• •• •••••••••• ••

••• •• ••• •• •• •••• ••••

•••• ••• •• ••••• ••

•••••• •••••

•••• •• •••• •

•• ••• ••

••• ••• • •• ••• ••••• •• •• •••

••• •••• •••••

•• • •••• ••

•• • •• • • •

• ••••

••

••• •

• •••

••••

••• • ••• ••

•••

• • ••

••• • • •

• •••••••••

•••

••

• •• •

••

•••••

•••• •••

••

•• •••

••

•••

•••••

•••

••

•• ••

• •••

• • •

••

•• •• •• • ••••••

•• ••••

••••

• ••• ••

••• •

• ••• ••• • • • •••

•••• •••• • •••

••••

••

••• • •

•••• •

•• • •••

•• •

• • ••

••

••

••

••

•

•••

••

•••

•••

••

•••• •

••

• •••

••••

•

••

• ••

••

••••• ••

•••

• ••••

••••

••••

••••• •

••

•• •• •••

• ••• • ••

••••

••

•• •

••• ••

••• •

•• ••

• ••

•• • •••

• ••••

•• •

••

••

•

•••

••

•••

• • ••• ••••

••

••• •

•••

•

•

••

•

••

••• • ••

••••

• • •• •

•

• •••••••

•

•••

•

•••

•

••

•

•

•••

• •

•••

•

••

••

•••• •

••

•

•

••

• •

• •

• •••

••

••

••

• ••

•

••

• •

•••

••

•• • •

••••

••

•

••

••

••••

•••••

••• •

• ••••

•

• •

••••

•••

•• •

•

• •

•

•••

•• •• •

••••

• •••

•

•• • ••••••

•••

• •

••• ••

••

••• •• ••

••

••••• •

••

••

• •••

•• ••

••• •

•••

•••••

••

•• •••

•• ••• •

••• •

• ••

• ••••• ••••

• ••

•• •••• ••••

•• •••••••

•••••

••

••

•••

•••

••

••

••••

• • • ••••

••

• ••

• ••••

••

••

••••

• • ••••• •

••

••

•••• ••• • •

••• •

•• • • ••

•••••

••

•• •• • • •••

••••••• • •

••• •••

•

••

•••

• •••

••••• • •

• •• •••••

• •••

•••

• • •••

•••• •

•••

•• •••

• ••••

• ••

•• •• •

••

• • •••• •• •••••

•• • •

•••• • •••

••

•• • •• ••

• • •• • •••

••

• •• • ••• •••

•• •• ••

• •• ••• ••••• • • ••

••• •••

• •• • •••• ••

•• • • • •

• • ••• •• • ••••

•• • •• • ••

•• • ••••

•

•• •• •

••• •••

••

••

• •••

••

•• • •• •

•• •

• • ••••• •••• ••••••••

•••

•••• •

•• •• •

••••

••

•••• • •• ••• ••••••

•• ••• ••• • • •

• ••••••• •••••• •• •• • •

••

•• •• •• •

• •••• •••

••• ••••• • •

• • ••• •••

• •••

• ••

••

•••• •• •

• •• ••• • ••• • •• •• ••• • • • •••• •• •

••• •

• • ••• • •• • •• ••• ••••

••

••• •••

•• • • •••• •• •• •• • •••• • ••••• • •••

•••••

••••• • • ••• •

•••

•• • ••

•••••

•••••

• • ••• •• •• • • •••• ••

••••• •• ••• • •

• •• • ••

• •• ••• •

••• •• •• •• ••

•••

••••••

•• •• • ••

• • •••••••

• •• •••••

••

•• •

••••

•••

•• ••

•• ••••••

• ••

•• •• ••• ••

•• ••• ••• •

•• • ••

•••••••

• •• ••••

••

••• • ••• ••

•••• ••

•••• ••••• •••• • •• • •••

••••• •• ••••• •

•• ••• ••• •

••

• •• • •••

•• •

•••

•

•

••

•••• •

••

• •••• •••

••

• ••

••••

••• ••

•

•••••

• • • • •••• •

•• ••

•• ••• •

•••

•••••

••

•••• ••••

••• • •

•• ••

•• • •• ••• • ••

•••••

•• •••

•• ••• •

• ••• •

• • • ••• • ••••••

• ••

•• • ••

• • •• • •••

••••••• • •

• ••• •• ••••

••••

• • ••••• • •

• •• •• • •••• •••• •

•••

••• •• • ••• • ••• •• •

• •••

•• ••••

••• • ••

•••

• • •

••

••••• ••

•• • ••

•••

••••••

• • •

•• •

• •• • •

•

• ••• ••• •

• •• ••••

• • •• •••• ••

••

••

• •• • ••• • ••

•••

••

••

••

• •••

•••

• • •

•

• ••

••

••

••

•• ••

•••

•

•

••

• •

•

•••

••

• ••

•

••

••• •• •••

•

• •••• ••

• ••

•••

••

•• ••• •• •••

•

•• •

•• •• • •

• ••• •• •

• • •• •

•••

••• •

••

•

••

•••••••• •

••• •• • •• •

• ••

•

••

• ••

• •••• • •

••••••• • • •

•• •

••

•••

••• • •

••

•••

••

• ••

• ••

••

•••

• • •

•••

••

•••

••

•• •

•••

•

•••••

••

••

• • •• •

•• ••

••••

••

• •••• • •••

••• ••

•• ••

•

•• ••

••• • •

•••

• •• • ••••

•• •

•••

•

••

• ••• •

•

•

•••

•••••• •••

• ••• •

• ••••

•• •••

• • •••

•• •••• •••

•••• •

••• ••• • •

• ••

••

•••

• ••••• •••• •• •• •• •

•••

• • •• • ••

• • •••

• •• ••••

•••

•

• ••

••

• •• ••

•••

•••• ••

•• ••

••• •

•••

••• ••

•

•• •

•••• •

•••

••••

• ••

• ••••

••

• ••

•• ••

••

• •• • •••

•••

••• •• •••

•••

•• • •

•••

•••• •

•• •• •

••

•

••

• •

••

•• ••• ••

••

•• • ••

• • ••

•••••

••••

••

• ••

•••••

• •• •• •• ••••

••••

• •••• •• ••

••

•• •• •• • •••• •• • ••

••••

••

•••• • •

• •••

••••• • • •

••••

• •••• •••••

••

•

•• •• • •••

•

•

••

••

•

••

••

•

•

• •

••

•••• •

•••

•

• •• ••• •

•• •

••• •

••

• •

•

••

••

•

•••

•••

•

••

•

•

••

•• •

••

••

•••

•

•

•••

••

••• •

• ••

•

•

•• •

•

••

••

•

••

•

••

••

••••••

••

••

•• •

•• • ••

• ••

• ••• • •

•

••

••

•••••

•

•• •• •

•• • •

••

••• ••

• •••• • •• • •• •

••

• ••

••

••

•• •• •

• •• • ••

••• • • •••••• •••

• •• • •• • •

••••• •

••

••••

•• •

••

• •• • •

•

•• • •

• ••• •

••

••

• •• • ••

••

•••• •

•• ••

• ••

•••• • ••

••••

•• •

• ••• • • • •• •

•• •• •

•• •• • •• ••

•• •• • • •

••

••

•••••••••

••

•• •• •• • •••••••

•••

••• ••••

••• ••• • ••••••

• • •••• •

•••

•• •

••

• ••• • ••

•

•• ••

••••

••

•• • ••

•••

•• ••

••• • ••

•• ••

••

••• ••

•• •• •

•••

•• •

• •• •••

• ••••••

•••

••

••

• •• • •• •

•• •

• ••••••• •

• ••

••

••••

••••••••

••

•••

•••

•

•••••• •

•• • •

•••• •

• ••

• • •••

••• • •• • • ••

•• •••••• •• ••

• •

•

•• • ••• ••

••

• • •• •• •• ••

• •••

•

••

•• •• ••

•• ••••••

•

••••

•• • •• ••

•• ••

••

••• ••

••

• ••••••••• ••

••

••• •••• •

•• •

•• •

• • •• •• ••

••

• ••• • •• •••• •• • ••••••• •• •• ••• ••

• •• •• • ••• • • • •

•••••• •

•• •• •

• •••••

• •• ••

• •• ••••••

••••••

•••

••• • •••

• •••••

• ••• • ••• • ••

• • • •••••• • •••• • • ••• •

••

••••

•• ••• • •• • •

••

•• • •••• • •••

•• ••• •

••

••

• •• ••

•• • •••

••

•••• ••

••• • • •

• •• •••

•••

•

•• • •• ••••••

• •• •••

••• • • • •

• • • ••

•

•••• •

••• • • •• •

•••

•

••• •

•

••

••••

•••

••

••

• •••

•••

• • • ••

••

•••

•••••

• ••

••

•• •••••

••••

•• ••

••

•••

•

•••• • ••••

••

•••••

•••• ••••

••

•••

••• •••••••••

•• •

•

••• •

•

• •

• • ••

•

•

••• •••••

••

•• ••• ••

•• • ••

•••

•• •

•• •• • •

• •••• • • •••

••

•

•••

••••••

••• •••

• • • •• •

•••

••• ••

• •• •••••

••• •••

•

••

••

• ••

•••

••••

•• •

••••

• •• •• ••

••••

• ••••

• ••••• •

••

•• ••

•

••

••

••

••

•

•

••

•• • • •

• ••

•••••••

••

••

••

• •• ••

••

••

•• • •••• •• •••

•• •

••

••

••• •••

• ••••

•• ••• •••••• ••

•••

•• •

••

••

••

••••

•••••

•• •

•• •

•••

•

•• • •• •

•••

•

•• • •

•

• •

•

•

•

•

•

•

•

•

••

•

••

•

••

•

••

••

•

•

•

•••

••

•

••

•

•

• ••

•

••

••

•

•

•••

••

••

•

•

•• •

•

•

•••

•

••

•

••

•

••

••

••

••••

••

•• •

••••

••••

•

• ••• • ••

•

•••••

••••

•••

••

••

••

••

• ••

•

•••• ••••••• • •

• ••••

••

••••

•••

•• ••

••

•••

•

•

•••

••

••

•• •

•••

••

••

•

••• •

••• •

•••

••••

•

••

•• ••••••••

•••••

••

•

•• •

•••

•••• •• • •

••

•••• ••• •

•••• ••

•••

••• • •

•

••• ••

••••••

•••

• •

•• •

•• •• • •

•• • •

• ••••• •••••

• •• •• •• • •••

••••• •••••

••••

•• ••• •

•• •••

•••••

•• ••

••

••••

•• •• •••

•• • •

••

••••••• ••

• •••• ••

•

••

•••

••• • •••• •••• • • •

••

•••

•••

•• ••

•• ••

•••••• ••

•••• ••

••

••

•••• ••••• •••

••

•• •

•••

•• •••

•••

•• •

••• ••

••

•• •

••• •

•• • •• •• •

••••• •• • • •

• • ••• •••••

•

•

• ••

•• ••• •

••

•• •

•• •

•••••• •

• • •••••• •

•• •• ••••• •

•• • • •

• •• ••

••••

• ••

••

••

••

•

••••••

•• ••

••

• ••

•• •••

••••

•• ••

••

••

••

••••

•••••

•••••

•• •• ••• •••

• •••• ••

••• •• •••••

••

•• •••••••

••• • •

••••• •

•• ••

•• •• • •

••• •••

•••

•••••••

••• •••

•••••

•

•••

•

•••

••

•

• ••

••

••

•

•• •

••

• • •• •

•••

••

•

•

••

••

••

•••

•••

••

••

•••

• ••• •

••• ••

••

•••

••

•• •

••• ••••

••• •

•• ••

••• •

••• •

• ••

• •••

••

••

•••

• •

•

•••

• ••••

•••

•••

••

•

••

•

••

•• • •

•

••

••

••••••

•• ••

••• • •

•• •

•

•

• ••

••

••••

••

•• •••

••

•• •

•••••

•

•

•• •

••• •••

• •• ••

• •• ••• •

••

•• ••

• •

•• • •

•

••

•• •

• • • •••••

••• • •• • ••• •••

••• • •••••

••

• ••••

••• • • •••

• ••

•• •••••••• ••••• • •

•••

•••• ••• •• •••••••• • •

• • •••

•

••

• •• •

•••

••••

•••••••• •••

•• •

••

•• •• • ••• ••

•• ••••

••••

••

•• •

••••• •

• ••

••

• •••

•• • ••• • • •• • •• •

• • •••• ••

• •••

• •

••

•••••

••

•• •• • • ••

••• • •

• •••• •

•••

• ••

• ••

•• ••••••••

••

•• ••• ••

••

• ••

• ••• •• ••• ••

••••••• ••••• ••• • •••

• •••• •• •• •••••

• ••

•

••• •

••

• ••

•• ••• • ••

••

•••• • ••••••

• ••••

••• •• •••••

•• ••

•••••• • • ••••• ••• •

••• ••• •• •• •

• • •• • ••••••• •

•• •• ••••••• ••

••

•• ••••

••••

•• ••

• •••

••••

•• •• ••

•••••

•• •••

••• ••• •• •••

• •• ••••• • •••

••••

••

•• •••

•••••••• ••• ••

••••

•• •• ••••

••

• •• ••• • ••••••••

••••• • •• •• • •• ••••

•••• •••• •• • • ••• •• •• •

••••

••• ••••• •••••••• ••• ••• •• ••

••••• •

• ••

•• •••

•••• •• •••••• • •• • • •• •• ••••• • ••• • •

• •••• ••••• • • •• •

•••

•

•• ••

•• •••••

••

••• •• ••• ••

••• •••• •••• •••

••

•• •

••

• • ••• •••

••

•••••• •••

••

••••••

•• ••••• •• •• •• •• •• •

••••

••

•• •

•••• ••• • • ••••• •• ••• • ••• •• • •• ••

••••• •• • •

••

• •••• •• •• • •

•• •

•• •• •• •

• •••

•• • • •• •••• •

• •••• •

••• • •

•• ••••

•• ••••

•• •••••

•••••

• •••

• ••• ••• •

• •• • •• •• ••••••••• •• •• •• •• • ••• •• •• • ••• • •••

••

• • •••••

•• ••

•••• •••••••• • •••••• ••

• •• • • •• •••• •

••• •• •• • •••

••

•••••

••

•• ••• ••• •

•• • •••

••• • •• • ••

•••••

•• •••

•• • •• •• •• • •• •••••

•• •• •• •• • •• •• • ••• •• •• ••• • •

• • ••••

•• •• ••• • • ••••• •

•• •••

••• • ••••••••

••••

•• •• ••• • •••

• ••• •• •

•

••

•• ••• • ••• • •••

••••

• • ••••

••• ••••••• •

• ••••••

• ••

• •••• ••

• •

•

•• •••

••• • •• •

• •••

••••

••

••••

• •• ••• ••••••

• •••

•• •••• •••

•• •

• ••

• •••

• •••••• •• •• •••••• •

• ••

•••

••

•

•• •

•••• ••

••• • •

• ••• • ••

•• •••••

••••• •••

•• •

• •• •••• • ••• ••••• ••

•••• •

••• •• ••• •• •••• •• • • •

•••• • ••• •••• •

•• ••• • ••

••••

••

•••

•• •••••

••

• ••

••••

• • •• ••• • • •

• ••• •

••

••

•••

••

•••

•••• •

••

••

• •••

•

••• •• • •

• •

••

••

••••

• •

•

• ••• •

•

••••

••

••

• •

••

•••

•• •

•• •

•••

••• •••••

••• •

•••••

••

•

•

• •••

• •••

••

••• • ••

••

•••••

• •••

•• ••

•

•• • •

•

•••

•••• •

• •

•

• •• ••• •

••

•

• •• ••••

•••

••• • •• •• •••••

• ••

••

•

•

••

••

•••• ••

•

•• •

•• •

••

•• ••

• ••

••••

••

••••••

• ••

••• ••

• •••

••••

• •

•• • ••••

•

••••

••

•• •• • ••

•••

•••• •••

•

•••••

•• •• ••

•• •• •

•• •••• •

•• ••

•

•• ••

•••

•• ••••••

••

•••• • • •••

•• •

• • ••

• ••••

••

•

• ••• •

••• •••

••

••

••

•••

••••

••

•• •

••

•

••

•

•••••

•

••

•••••

•••

•

•

•

•

•••

•

••

••••

•

• • •

•

•

• ••

••

•

••

• •

••

••

•

••• • •• ••

•••

• • ••• •• •

• •• • • ••

• ••

•

••

•

••

• ••

•

•

••

•• ••

•

•••

• ••• •

• ••

••

•

•••

••

• ••

••••

•

••

•

•

••

•

•

•

••

•

•• •• ••

•• •

•• • ••

•••

•

••

•

••

•

•

•••

•

•• •

• ••

•••

•

•••

• ••• ••

•

•

•

••

••••

•

•••

••••

•

•

•• • •

••

••

• • • ••

•• •• •

••

• ••••• •• •

•• • •••

•

••

•••

•• •

••••

• ••

••

•• •

••• •

••

• •••

••

•

•• •• •••••

••

•

•

•• ••

•

••

••

•

••

•••

•

•

•••

••

•••

••

• •••••

••• •

••

••

• ••

••••

• ••

•• • • •••••••

••

••• •• •

(a) Returns vs Normal

normal quantile

quan

tile

of r

etur

ns

-4 -2 0 2 4

-15

-10

-50

510

•••••

•••••••••••

••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••

••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••

•••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••

••••••••••••••••••••••••••••••••••••••••••••••••••••••••

••••••• •

•

(b) Returns vs t(7)

quantile of t(7)

quan

tile

of r

etur

ns

-5 0 5

-15

-10

-50

510

•••••

•••••••••••