monetary theory: the basic new keynesian · pdf filerelated to output because an increase in...

TRANSCRIPT

Monetary Theory: The Basic New Keynesian Model

Behzad Diba

University of Bern

April 2011

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 1 / 12

Three Equations

The basic New Keynesian model with Calvo price setting simplifies toa system of three equations

1 The New Keynesian Phillips curve relating inflation to the output gap2 A "Dynamic IS Equation" linking the evolution of aggregate demand(and the output gap) to the nominal interest rate

3 A monetary-policy rule for setting the nominal interest rate (or, amoney-supply rule plus a money-demand specification)

These equations determine the real interest rate, inflation, and theoutput gap

We will derive the first two equations and put them together with apolicy rule below

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 2 / 12

Three Equations

The basic New Keynesian model with Calvo price setting simplifies toa system of three equations

1 The New Keynesian Phillips curve relating inflation to the output gap

2 A "Dynamic IS Equation" linking the evolution of aggregate demand(and the output gap) to the nominal interest rate

3 A monetary-policy rule for setting the nominal interest rate (or, amoney-supply rule plus a money-demand specification)

These equations determine the real interest rate, inflation, and theoutput gap

We will derive the first two equations and put them together with apolicy rule below

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 2 / 12

Three Equations

The basic New Keynesian model with Calvo price setting simplifies toa system of three equations

1 The New Keynesian Phillips curve relating inflation to the output gap2 A "Dynamic IS Equation" linking the evolution of aggregate demand(and the output gap) to the nominal interest rate

3 A monetary-policy rule for setting the nominal interest rate (or, amoney-supply rule plus a money-demand specification)

These equations determine the real interest rate, inflation, and theoutput gap

We will derive the first two equations and put them together with apolicy rule below

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 2 / 12

Three Equations

The basic New Keynesian model with Calvo price setting simplifies toa system of three equations

1 The New Keynesian Phillips curve relating inflation to the output gap2 A "Dynamic IS Equation" linking the evolution of aggregate demand(and the output gap) to the nominal interest rate

3 A monetary-policy rule for setting the nominal interest rate (or, amoney-supply rule plus a money-demand specification)

These equations determine the real interest rate, inflation, and theoutput gap

We will derive the first two equations and put them together with apolicy rule below

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 2 / 12

Three Equations

The basic New Keynesian model with Calvo price setting simplifies toa system of three equations

1 The New Keynesian Phillips curve relating inflation to the output gap2 A "Dynamic IS Equation" linking the evolution of aggregate demand(and the output gap) to the nominal interest rate

3 A monetary-policy rule for setting the nominal interest rate (or, amoney-supply rule plus a money-demand specification)

These equations determine the real interest rate, inflation, and theoutput gap

We will derive the first two equations and put them together with apolicy rule below

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 2 / 12

Three Equations

The basic New Keynesian model with Calvo price setting simplifies toa system of three equations

1 The New Keynesian Phillips curve relating inflation to the output gap2 A "Dynamic IS Equation" linking the evolution of aggregate demand(and the output gap) to the nominal interest rate

3 A monetary-policy rule for setting the nominal interest rate (or, amoney-supply rule plus a money-demand specification)

These equations determine the real interest rate, inflation, and theoutput gap

We will derive the first two equations and put them together with apolicy rule below

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 2 / 12

The Output Gap

Define the natural level of output as the level in the flexible-priceequilibrium, and let ynt denote the logarithm of natural output

For example, in our model with iso-elastic utility and the productionfunction

yt = at + (1− α)nt , (1)

0 < α < 1, we got

ynt =(1− α)[log(1− α)− µ]

ϕ+ α+ σ− ασ+

(ϕ+ 1

ϕ+ α+ σ− ασ

)at (2)

relating ynt to productivity shocksWe define the output gap as

∼yt = yt − ynt ,

and define recessions as periods with a negative output gapComparison to real-world measures, and the role of productivityshocks

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 3 / 12

The Output Gap

Define the natural level of output as the level in the flexible-priceequilibrium, and let ynt denote the logarithm of natural outputFor example, in our model with iso-elastic utility and the productionfunction

yt = at + (1− α)nt , (1)

0 < α < 1, we got

ynt =(1− α)[log(1− α)− µ]

ϕ+ α+ σ− ασ+

(ϕ+ 1

ϕ+ α+ σ− ασ

)at (2)

relating ynt to productivity shocks

We define the output gap as∼yt = yt − ynt ,

and define recessions as periods with a negative output gapComparison to real-world measures, and the role of productivityshocks

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 3 / 12

The Output Gap

Define the natural level of output as the level in the flexible-priceequilibrium, and let ynt denote the logarithm of natural outputFor example, in our model with iso-elastic utility and the productionfunction

yt = at + (1− α)nt , (1)

0 < α < 1, we got

ynt =(1− α)[log(1− α)− µ]

ϕ+ α+ σ− ασ+

(ϕ+ 1

ϕ+ α+ σ− ασ

)at (2)

relating ynt to productivity shocksWe define the output gap as

∼yt = yt − ynt ,

and define recessions as periods with a negative output gap

Comparison to real-world measures, and the role of productivityshocks

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 3 / 12

The Output Gap

Define the natural level of output as the level in the flexible-priceequilibrium, and let ynt denote the logarithm of natural outputFor example, in our model with iso-elastic utility and the productionfunction

yt = at + (1− α)nt , (1)

0 < α < 1, we got

ynt =(1− α)[log(1− α)− µ]

ϕ+ α+ σ− ασ+

(ϕ+ 1

ϕ+ α+ σ− ασ

)at (2)

relating ynt to productivity shocksWe define the output gap as

∼yt = yt − ynt ,

and define recessions as periods with a negative output gapComparison to real-world measures, and the role of productivityshocks

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 3 / 12

Real Marginal Cost

Recall that with flexible prices real marginal cost is constant at thesteady-state value

mc = log(

ε− 1ε

),

which is the inverse of the monopoly markup

Recall also that, with sticky prices, real marginal cost is positivelyrelated to output because an increase in output increases the realwage, and may also lead to diminishing marginal product of labor(mpn in the textbook) if we have a fixed factor in the productionfunction

For example, with our iso-elastic specification, with (1), we get

m̂c t =(

σ+α+ ϕ

1− α

)∼yt

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 4 / 12

Real Marginal Cost

Recall that with flexible prices real marginal cost is constant at thesteady-state value

mc = log(

ε− 1ε

),

which is the inverse of the monopoly markup

Recall also that, with sticky prices, real marginal cost is positivelyrelated to output because an increase in output increases the realwage, and may also lead to diminishing marginal product of labor(mpn in the textbook) if we have a fixed factor in the productionfunction

For example, with our iso-elastic specification, with (1), we get

m̂c t =(

σ+α+ ϕ

1− α

)∼yt

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 4 / 12

Real Marginal Cost

Recall that with flexible prices real marginal cost is constant at thesteady-state value

mc = log(

ε− 1ε

),

which is the inverse of the monopoly markup

Recall also that, with sticky prices, real marginal cost is positivelyrelated to output because an increase in output increases the realwage, and may also lead to diminishing marginal product of labor(mpn in the textbook) if we have a fixed factor in the productionfunction

For example, with our iso-elastic specification, with (1), we get

m̂c t =(

σ+α+ ϕ

1− α

)∼yt

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 4 / 12

Marginal Cost and Output

mct = (wt � pt)�mpnt= (� yt + ' nt)� (yt � nt)� log(1� �)

=

�� +

' + �

1� �

�yt �

1 + '

1� �at � log(1� �) (6)

Under �exible prices

mc =

�� +

' + �

1� �

�ynt �

1 + '

1� �at � log(1� �) (7)

=) ynt = ��y + ya atwhere �y � (��log(1��))(1��)

�+'+�(1��) > 0 and ya � 1+'�+'+�(1��).

=) cmct = �� + ' + �

1� �

�(yt � ynt ) (8)

where yt � ynt � eyt is the output gap

Real Marginal Cost and the Output Gap

Note that this equation,

m̂c t =(

σ+α+ ϕ

1− α

)∼yt ,

relates the proportional deviation of real marginal cost from itssteady-state value to the output gap

1 with α = 0, the connection involves the preference parameters σ andϕ, reflecting the effect of output on real wages

2 with 0 < α < 1, we have the additional effect of the diminishingmarginal product of labor

Either way, an expansion of output raises real marginal cost, and thiserodes the monopoly markup

New prices, in Calvo’s model, rise with real marginal cost (in responseto the erosion of the markup), and this leads to inflation

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 5 / 12

Real Marginal Cost and the Output Gap

Note that this equation,

m̂c t =(

σ+α+ ϕ

1− α

)∼yt ,

relates the proportional deviation of real marginal cost from itssteady-state value to the output gap

1 with α = 0, the connection involves the preference parameters σ andϕ, reflecting the effect of output on real wages

2 with 0 < α < 1, we have the additional effect of the diminishingmarginal product of labor

Either way, an expansion of output raises real marginal cost, and thiserodes the monopoly markup

New prices, in Calvo’s model, rise with real marginal cost (in responseto the erosion of the markup), and this leads to inflation

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 5 / 12

Real Marginal Cost and the Output Gap

Note that this equation,

m̂c t =(

σ+α+ ϕ

1− α

)∼yt ,

relates the proportional deviation of real marginal cost from itssteady-state value to the output gap

1 with α = 0, the connection involves the preference parameters σ andϕ, reflecting the effect of output on real wages

2 with 0 < α < 1, we have the additional effect of the diminishingmarginal product of labor

Either way, an expansion of output raises real marginal cost, and thiserodes the monopoly markup

New prices, in Calvo’s model, rise with real marginal cost (in responseto the erosion of the markup), and this leads to inflation

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 5 / 12

Real Marginal Cost and the Output Gap

Note that this equation,

m̂c t =(

σ+α+ ϕ

1− α

)∼yt ,

relates the proportional deviation of real marginal cost from itssteady-state value to the output gap

1 with α = 0, the connection involves the preference parameters σ andϕ, reflecting the effect of output on real wages

2 with 0 < α < 1, we have the additional effect of the diminishingmarginal product of labor

Either way, an expansion of output raises real marginal cost, and thiserodes the monopoly markup

New prices, in Calvo’s model, rise with real marginal cost (in responseto the erosion of the markup), and this leads to inflation

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 5 / 12

Real Marginal Cost and the Output Gap

Note that this equation,

m̂c t =(

σ+α+ ϕ

1− α

)∼yt ,

relates the proportional deviation of real marginal cost from itssteady-state value to the output gap

1 with α = 0, the connection involves the preference parameters σ andϕ, reflecting the effect of output on real wages

2 with 0 < α < 1, we have the additional effect of the diminishingmarginal product of labor

Either way, an expansion of output raises real marginal cost, and thiserodes the monopoly markup

New prices, in Calvo’s model, rise with real marginal cost (in responseto the erosion of the markup), and this leads to inflation

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 5 / 12

The New Keynesian Phillips Curve (NKPC)

More precisely, we saw that (with Calvo price setting) inflationdynamics are governed by

πt = βEtπt+1 + λm̂c t

with a coeffi cient λ > 0 that is inversely related to the degree of pricerigidity θ

Combining this with

m̂c t =(

σ+α+ ϕ

1− α

)∼yt

we get the New Keynesian Phillips Curve

πt = βEtπt+1 + κ∼yt

with

κ = λ

(σ+

α+ ϕ

1− α

)> 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 6 / 12

The New Keynesian Phillips Curve (NKPC)

More precisely, we saw that (with Calvo price setting) inflationdynamics are governed by

πt = βEtπt+1 + λm̂c t

with a coeffi cient λ > 0 that is inversely related to the degree of pricerigidity θ

Combining this with

m̂c t =(

σ+α+ ϕ

1− α

)∼yt

we get the New Keynesian Phillips Curve

πt = βEtπt+1 + κ∼yt

with

κ = λ

(σ+

α+ ϕ

1− α

)> 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 6 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve

1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curve

the New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment

2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curve

the New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation

3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curve

the New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curve

the New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curve

the New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curvethe New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curvethe New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Digression: Phillips Curves, Old and New

The original Phillips Curve1 inverse relation, in the data, between inflation and unemployment2 the traditional Keynesian interpretation3 an inflation-unemployment (inflation-output) trade-off forpolicymakers?

The Phelps-Friedman "Expectations-augmented" Phillips Curvethe New Classical rendition (with Rational Expectations)

πt = Et−1πt + κ∗ (yt − ynt ) , κ∗ > 0

may arise from the Lucas aggregate-supply curve

yt = ynt + φ (pt − Et−1pt ) , φ > 0

(setting κ∗ = 1/φ)

Contrast with the forward-looking NKPC

πt = βEtπt+1 + κ (yt − ynt ) , κ > 0

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 7 / 12

Dynamic IS Equation

The consumers’Euler equation governs the evolution of aggregatedemand, given our market-clearing condition Ct = Yt

Define the natural real interest rate rnt as the real rate in theflexible-price equilibrium

Recall that rnt depends on productivity, but not on the prevailingnominal interest rate (nor anything else that monetary policy canaffect)

For example, in our iso-elastic specification leading to (2), we have

ynt = −1σ(rnt − ρ) + Etynt+1

and

rnt = ρ+ σ

(ϕ+ 1

ϕ+ α+ σ− ασ

)Et (∆at+1)

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 8 / 12

Equilibrium

Goods markets clearing

Yt(i) = Ct(i)

for all i 2 [0; 1] and all t.

Letting Yt ��R 1

0 Yt(i)1�1

� di� ���1,

Yt = Ct

for all t. Combined with the consumer�s Euler equation:

yt = Etfyt+1g �1

�(it � Etf�t+1g � �) (5)

Dynamic IS Equation

The consumers’Euler equation governs the evolution of aggregatedemand, given our market-clearing condition Ct = YtDefine the natural real interest rate rnt as the real rate in theflexible-price equilibrium

Recall that rnt depends on productivity, but not on the prevailingnominal interest rate (nor anything else that monetary policy canaffect)

For example, in our iso-elastic specification leading to (2), we have

ynt = −1σ(rnt − ρ) + Etynt+1

and

rnt = ρ+ σ

(ϕ+ 1

ϕ+ α+ σ− ασ

)Et (∆at+1)

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 8 / 12

Dynamic IS Equation

The consumers’Euler equation governs the evolution of aggregatedemand, given our market-clearing condition Ct = YtDefine the natural real interest rate rnt as the real rate in theflexible-price equilibrium

Recall that rnt depends on productivity, but not on the prevailingnominal interest rate (nor anything else that monetary policy canaffect)

For example, in our iso-elastic specification leading to (2), we have

ynt = −1σ(rnt − ρ) + Etynt+1

and

rnt = ρ+ σ

(ϕ+ 1

ϕ+ α+ σ− ασ

)Et (∆at+1)

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 8 / 12

Dynamic IS Equation

The consumers’Euler equation governs the evolution of aggregatedemand, given our market-clearing condition Ct = YtDefine the natural real interest rate rnt as the real rate in theflexible-price equilibrium

Recall that rnt depends on productivity, but not on the prevailingnominal interest rate (nor anything else that monetary policy canaffect)

For example, in our iso-elastic specification leading to (2), we have

ynt = −1σ(rnt − ρ) + Etynt+1

and

rnt = ρ+ σ

(ϕ+ 1

ϕ+ α+ σ− ασ

)Et (∆at+1)

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 8 / 12

IS Equation and the Output Gap

Combining the Euler equations in the two equilibria (with flexible andsticky prices), we can relate the evolution of the output gap to theinterest-rate gap rt − rnt

Monetary policy affects the output gap through its effect on theinterest-rate gap:

yt − ynt = Et (yt+1 − ynt+1)−1σ[it − Et (πt+1)− rnt ] ,

i.e.∼yt = Et (

∼yt+1)−

1σ[rt − rnt ]

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 9 / 12

New Keynesian Phillips Curve

�t = � Etf�t+1g + � eyt (9)

where � � ��� + '+�

1���.

Dynamic IS equation

eyt = Etfeyt+1g � 1�(it � Etf�t+1g � rnt ) (10)

where rnt is the natural rate of interest, given by

rnt � � + � Etf�ynt+1g= � + � ya Etf�at+1g

Missing block: description of monetary policy (determination of it).

IS Equation and the Output Gap

Combining the Euler equations in the two equilibria (with flexible andsticky prices), we can relate the evolution of the output gap to theinterest-rate gap rt − rntMonetary policy affects the output gap through its effect on theinterest-rate gap:

yt − ynt = Et (yt+1 − ynt+1)−1σ[it − Et (πt+1)− rnt ] ,

i.e.∼yt = Et (

∼yt+1)−

1σ[rt − rnt ]

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 9 / 12

Interest-rate Rules

We can close the model by specifying an interest-rate rule formonetary policy

For example, near the steady state with zero inflation, a Taylor Rule

it = ρ+ φππt + φy∼yt + υt

delivers determinacy if it satisfies the Taylor Principle, φπ > 1, andφy ≥ 0 (the necessary condition for determinacy, presented in thetextbook, is a bit weaker)

Here, υt represents a "monetary-policy shock" and may, for example,follow an exogenous AR(1) process

Although we can solve this simple model analytically, we usually relyon a calibration and stochastic simulations to assess the quantitativeimplications of our models

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 10 / 12

New Keynesian Phillips Curve

�t = � Etf�t+1g + � eyt (9)

where � � ��� + '+�

1���.

Dynamic IS equation

eyt = Etfeyt+1g � 1�(it � Etf�t+1g � rnt ) (10)

where rnt is the natural rate of interest, given by

rnt � � + � Etf�ynt+1g= � + � ya Etf�at+1g

Missing block: description of monetary policy (determination of it).

Interest-rate Rules

We can close the model by specifying an interest-rate rule formonetary policy

For example, near the steady state with zero inflation, a Taylor Rule

it = ρ+ φππt + φy∼yt + υt

delivers determinacy if it satisfies the Taylor Principle, φπ > 1, andφy ≥ 0 (the necessary condition for determinacy, presented in thetextbook, is a bit weaker)

Here, υt represents a "monetary-policy shock" and may, for example,follow an exogenous AR(1) process

Although we can solve this simple model analytically, we usually relyon a calibration and stochastic simulations to assess the quantitativeimplications of our models

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 10 / 12

Equilibrium under a Simple Interest Rate Rule

it = � + �� �t + �y eyt + vt (11)

where vt is exogenous (possibly stochastic) with zero mean.

Equilibrium Dynamics: combining (9), (10), and (11)� eyt�t

�= AT

�Etfeyt+1gEtf�t+1g

�+BT (brnt � vt) (12)

where

AT � �� 1� ����� � + �(� + �y)

�; BT �

�1�

�and � 1

�+�y+���

Uniqueness () AT has both eigenvalues within the unit circle

Given �� � 0 and �y � 0, (Bullard and Mitra (2002)):

� (�� � 1) + (1� �) �y > 0

is necessary and su¢ cient.

Interest-rate Rules

We can close the model by specifying an interest-rate rule formonetary policy

For example, near the steady state with zero inflation, a Taylor Rule

it = ρ+ φππt + φy∼yt + υt

delivers determinacy if it satisfies the Taylor Principle, φπ > 1, andφy ≥ 0 (the necessary condition for determinacy, presented in thetextbook, is a bit weaker)

Here, υt represents a "monetary-policy shock" and may, for example,follow an exogenous AR(1) process

Although we can solve this simple model analytically, we usually relyon a calibration and stochastic simulations to assess the quantitativeimplications of our models

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 10 / 12

Interest-rate Rules

We can close the model by specifying an interest-rate rule formonetary policy

For example, near the steady state with zero inflation, a Taylor Rule

it = ρ+ φππt + φy∼yt + υt

delivers determinacy if it satisfies the Taylor Principle, φπ > 1, andφy ≥ 0 (the necessary condition for determinacy, presented in thetextbook, is a bit weaker)

Here, υt represents a "monetary-policy shock" and may, for example,follow an exogenous AR(1) process

Although we can solve this simple model analytically, we usually relyon a calibration and stochastic simulations to assess the quantitativeimplications of our models

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 10 / 12

E¤ects of a Monetary Policy Shock

Set brnt = 0 (no real shocks).Let vt follow an AR(1) process

vt = �v vt�1 + "vt

Calibration:

�v = 0:5, �� = 1:5, �y = 0:5=4, � = 0:99, � = ' = 1, � = 2=3, � = 4.

Dynamic e¤ects of an exogenous increase in the nominal rate (Figure 1):

Exercise: analytical solution

Figure 3.1: Effects of a Monetary Policy Shock (Interest Rate Rule))

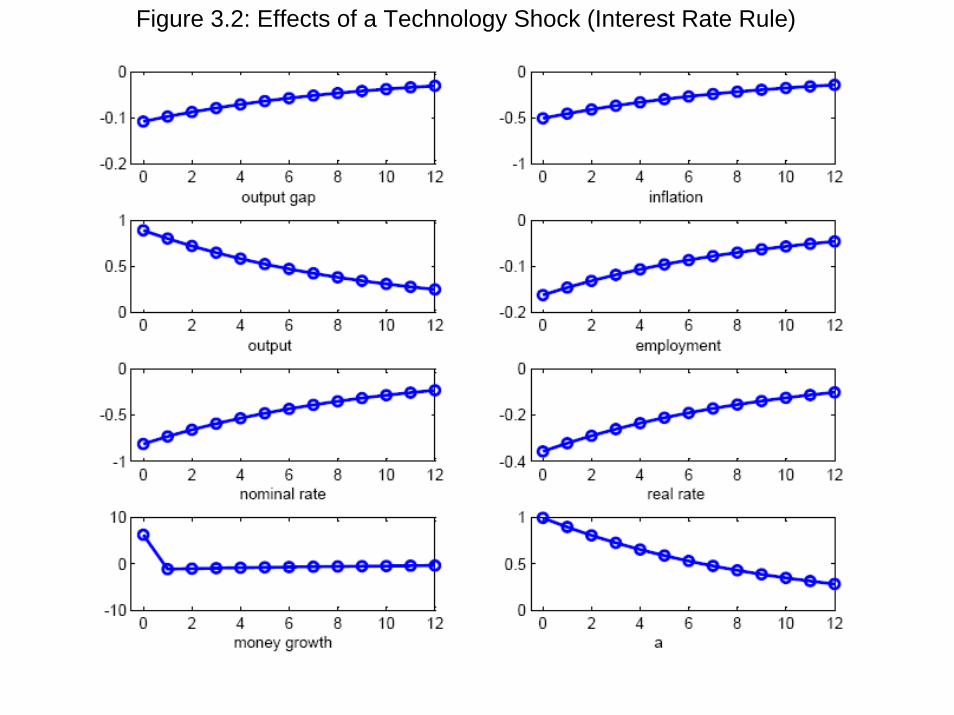

E¤ects of a Technology Shock

Set vt = 0 (no monetary shocks).

Technology process:at = �a at�1 + "

at :

Implied natural rate: brnt = �� ya(1� �a) at

Dynamic e¤ects of a technology shock (�a = 0:9) (Figure 2)

Exercise: AR(1) process for �at

Figure 3.2: Effects of a Technology Shock (Interest Rate Rule)

Money-supply Rule

Alternatively, we may specify a policy rule that sets the moneysupply—e.g., an AR(1) process for money growth—and solve the(simple) model or simulate (richer) models

The practical motivation for this specification is weaker because majorcentral banks use the nominal interest rate as their policy instrument

But the ability of various models to generate liquidity effects, undermoney-supply rules, has motivated some academic researchers

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 11 / 12

Money-supply Rule

Alternatively, we may specify a policy rule that sets the moneysupply—e.g., an AR(1) process for money growth—and solve the(simple) model or simulate (richer) models

The practical motivation for this specification is weaker because majorcentral banks use the nominal interest rate as their policy instrument

But the ability of various models to generate liquidity effects, undermoney-supply rules, has motivated some academic researchers

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 11 / 12

Equilibrium under an Exogenous Money Growth Process

�mt = �m �mt�1 + "mt (13)

Money market clearing

blt = byt � � bit (14)= eyt + bynt � � bit (15)

where lt � mt � pt denotes (log) real money balances.

Substituting (14) into (10):

(1 + ��) eyt = �� Etfeyt+1g + blt + � Etf�t+1g + � brnt � bynt (16)

Furthermore, we have blt�1 = blt + �t ��mt (17)

Equilibrium dynamics

AM;0

24 eyt�tblt�135 = AM;1

24 Etfeyt+1gEtf�t+1gblt�1

35 +BM24 brntbynt�mt

35 (18)

where

AM;0 �

24 1 + �� 0 0�� 1 00 �1 1

35 ; AM;1 �

24 �� � 10 � 00 0 1

35 ; BM �

24 � �1 00 0 00 0 �1

35Uniqueness () AM � A�1

M;0AM;1 has two eigenvalues inside and oneoutside the unit circle.

E¤ects of a Monetary Policy Shock

Set brnt = ynt = 0 (no real shocks).

Money growth process

�mt = �m �mt�1 + "mt (19)

where �m 2 [0; 1)Figure 3 (based on �m = 0:5)

E¤ects of a Technology Shock

Set �mt = 0 (no monetary shocks).

Technology process:at = �a at�1 + "

at :

Figure 4 (based on �a = 0:9).

Empirical Evidence

Figure 3.3: Effects of a Monetary Policy Shock (Money Growth Rule)

Figure 3.4: Effects of a Technology Shock (Money Growth Rule)

Money-supply Rule

Alternatively, we may specify a policy rule that sets the moneysupply—e.g., an AR(1) process for money growth—and solve the(simple) model or simulate (richer) models

The practical motivation for this specification is weaker because majorcentral banks use the nominal interest rate as their policy instrument

But the ability of various models to generate liquidity effects, undermoney-supply rules, has motivated some academic researchers

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 11 / 12

New Keynesian (NK) Insights

The core RBC framework plays an important role in the NK model,and in its implications for the effects of productivity (and fiscal)shocks

The NK model’s household block (maximizing utility over time)makes it very different from traditional Keynesian models

The NK concept of stabilization policy is fundamentally different fromthe traditional notion of stabilizing (de-trended) output

the output target ynt depends on productivityas an illustration, consider the effects of a productivity shock in thesimple model with one-period price rigidity

The NK model offers fundamentally new insights about theoutput-inflation "trade-off" facing the central bank, as we will see inChapter 4

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 12 / 12

New Keynesian (NK) Insights

The core RBC framework plays an important role in the NK model,and in its implications for the effects of productivity (and fiscal)shocks

The NK model’s household block (maximizing utility over time)makes it very different from traditional Keynesian models

The NK concept of stabilization policy is fundamentally different fromthe traditional notion of stabilizing (de-trended) output

the output target ynt depends on productivityas an illustration, consider the effects of a productivity shock in thesimple model with one-period price rigidity

The NK model offers fundamentally new insights about theoutput-inflation "trade-off" facing the central bank, as we will see inChapter 4

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 12 / 12

New Keynesian (NK) Insights

The core RBC framework plays an important role in the NK model,and in its implications for the effects of productivity (and fiscal)shocks

The NK model’s household block (maximizing utility over time)makes it very different from traditional Keynesian models

The NK concept of stabilization policy is fundamentally different fromthe traditional notion of stabilizing (de-trended) output

the output target ynt depends on productivityas an illustration, consider the effects of a productivity shock in thesimple model with one-period price rigidity

The NK model offers fundamentally new insights about theoutput-inflation "trade-off" facing the central bank, as we will see inChapter 4

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 12 / 12

New Keynesian (NK) Insights

The core RBC framework plays an important role in the NK model,and in its implications for the effects of productivity (and fiscal)shocks

The NK model’s household block (maximizing utility over time)makes it very different from traditional Keynesian models

The NK concept of stabilization policy is fundamentally different fromthe traditional notion of stabilizing (de-trended) output

the output target ynt depends on productivity

as an illustration, consider the effects of a productivity shock in thesimple model with one-period price rigidity

The NK model offers fundamentally new insights about theoutput-inflation "trade-off" facing the central bank, as we will see inChapter 4

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 12 / 12

New Keynesian (NK) Insights

The core RBC framework plays an important role in the NK model,and in its implications for the effects of productivity (and fiscal)shocks

The NK model’s household block (maximizing utility over time)makes it very different from traditional Keynesian models

The NK concept of stabilization policy is fundamentally different fromthe traditional notion of stabilizing (de-trended) output

the output target ynt depends on productivityas an illustration, consider the effects of a productivity shock in thesimple model with one-period price rigidity

The NK model offers fundamentally new insights about theoutput-inflation "trade-off" facing the central bank, as we will see inChapter 4

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 12 / 12

New Keynesian (NK) Insights

The core RBC framework plays an important role in the NK model,and in its implications for the effects of productivity (and fiscal)shocks

The NK model’s household block (maximizing utility over time)makes it very different from traditional Keynesian models

The NK concept of stabilization policy is fundamentally different fromthe traditional notion of stabilizing (de-trended) output

the output target ynt depends on productivityas an illustration, consider the effects of a productivity shock in thesimple model with one-period price rigidity

The NK model offers fundamentally new insights about theoutput-inflation "trade-off" facing the central bank, as we will see inChapter 4

(Institute) Monetary Theory: The Basic New Keynesian Model April 2011 12 / 12