monmouth county 1st quarter real estate report

DESCRIPTION

Colleen Tobin's quarterly review of real estate market activity and trends.TRANSCRIPT

M O N M O U T H C O U N T Y

BRIELLE | WALL | SEA GIRT | SPRING LAKE | SPRING LAKE HEIGHTS | AVON-BY-THE-SEA

BELMAR | MANASQUAN

R E A L E S T A T E 2 0 1 4 1ST Q U A R T E R R E P O R T

2013 COMPANY-WIDE TOP PRODUCER

Courtesy of

C O L L E E N T O B I N

SPRING LAKE BRIELLE

WALL SPRING LAKE BRIELLE

WALL BELMAR BRIELLE

Hello Neighbors,

I am pleased to present my analysis of the real estate market for the 1st Quarter of 2014. The

recovery that began last year has continued to take hold during the first three months of

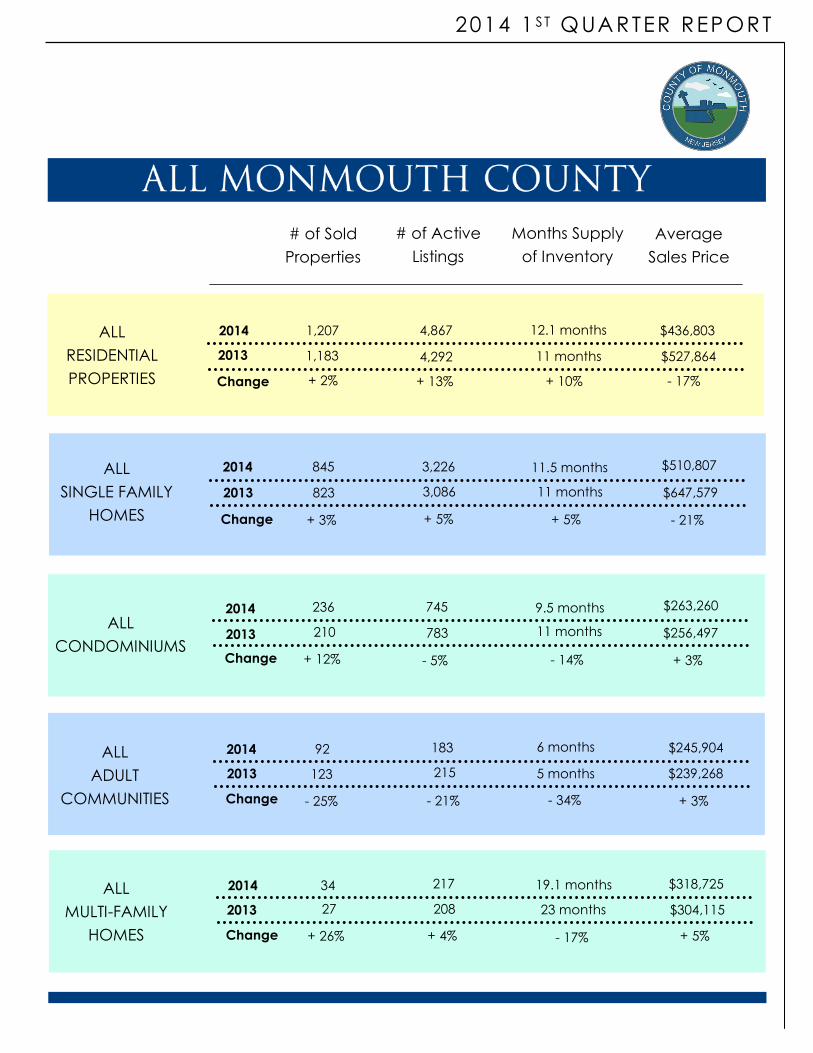

2014. Overall, Monmouth County sales increased slightly but the supply of homes also increased,

leading to more homes on the market now when compared to last year. This may explain the 17%

decline in the average sales price of homes in the county.

Another interesting trend developed in comparing the single-family market with the condominium

and adult community markets. The condominium market experienced a 5% drop in the number of

units for sale, while the supply of single-family homes for sale increased by 10%. Despite the drop in

condominium inventory and increase in the number of sales in both categories, there is still room for

improvement before both single-family and condominium markets fully recover.

There were several positive developments in the real estate market that should be noted.

Adult Communities - The real estate market in adult communities is fully recovered. Inventory

levels are normal and average prices are continuing to increase.

Luxury Market - A recovery in the luxury market is well underway. Sales of properties valued over

$1 million increased by 78% during the first quarter, and the average sales price in this category

was up 9% year-over-year. This is the second year of continuous improvement in the luxury

market.

Wall Township, Belmar & Spring Lake Heights - These three communities posted strong gains in

the number of sales and the increase in average sales prices. Higher than average inventory levels

should continue to drop during the remainder of this year.

Spring Lake & Sea Girt - Sales activity posted strong gains and the average sales price also

increased dramatically in both communities. With inventory levels below normal, it is likely that

the Spring Lake and Sea Girt real estate markets will remain strong throughout 2014.

Homeowners who are thinking about selling should find the upcoming months to be an ideal time to

list and sell their property. Interest rates remain low and buyer demand should remain strong.

Realtor-Associate®

732-213-5166

ALL

RESIDENTIAL

PROPERTIES

2014

2013

Change

1,183

1,207

+ 2% - 17%

4,867

$527,864

12.1 months $436,803

4,292

+ 13% + 10%

11 months

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

823

845

+ 3% - 21%

3,226

$647,579

11.5 months $510,807

3,086

+ 5% + 5%

11 months

ALL

CONDOMINIUMS

2014

2013

Change

210

236

+ 12% + 3%

745

$256,497

9.5 months $263,260

- 5% - 14%

11 months 783

ALL

ADULT

COMMUNITIES

2014

2013

Change

123

92

- 25% + 3%

183

$239,268

6 months $245,904

- 21% - 34%

5 months 215

2014

2013

Change

27

34

+ 26% + 5%

217

$304,115

19.1 months $318,725

+ 4% - 17%

23 months 208

ALL

MULTI-FAMILY

HOMES

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

2014 1 ST QUA RTER REPORT

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

33

36

+ 9% + 45%

156

$384,179

13 months $557,533

150

+ 4% - 7%

14 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

5

10

+ 100% + 4%

41

$593,560

12.3 months $616,200

38

+ 8% - 47%

23 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

9

21

+ 133% + 26%

55

$1,749,889

7.9 months $2,209,059

55

0% - 56%

18 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

4

12

+ 200% + 81%

21

$1,099,750

5.3 months $1,991,500

22

- 5% - 69%

17 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

2014 1 ST QUA RTER REPORT

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

0

2

N/A N/A

19

N/A

28.5 months $861,250

20

- 5% N/A

N/A

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

13

10

- 23% - 20%

65

$666,835

19.5 months $533,819

64

+ 2% + 30%

15 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

8

11

+ 38% + 84%

51

$363,750

13.9 months $668,330

55

- 7% - 34%

21 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

ALL

SINGLE FAMILY

HOMES

2014

2013

Change

5

7

+ 40% + 18%

26

$498,200

11.1 months $588,428

22

+ 18% - 15%

13 months

Average

Sales Price

Months Supply

of Inventory

# of Active

Listings

# of Sold

Properties

2014 1 ST QUA RTER REPORT

2 0 1 4