mosquito consolidated gold mines ltd. (tsxv: msq

TRANSCRIPT

Investment Analysis for Intelligent Investors

Siddharth Rajeev, B.Tech, MBA Analyst

Vincent Weber, B.Sc

Research Associate-Mining

Randall Hsu, BBA Research Associate

June 15, 2010

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Coverage; Continued resource

development at one of the world's largest undeveloped molybdenum deposits

Sector/Industry: Junior Exploration/Mining www.mosquitogold.com

Market Data (as of June 15, 2010)

Current Price C$1.18

Fair Value C$2.67

Rating* BUY

Risk* 5 (Highly Spec)

52 Week Range C$0.33 - C$1.69

Shares O/S 68.93 mm

Market Cap C$81.34 mm

Current Yield N/A

P/E (forward) N/A

P/B 3.25

YoY Return 218.9%

YoY TSXV 29.0%

*see back of report for rating and risk definitions

-

300,000

600,000

900,000

1,200,000

1,500,000

16-Jun-09 15-Oct-09 13-Feb-10 14-Jun-10

0.00

0.60

1.20

1.80

2.40

3.00

Investment Highlights

• Mosquito Consolidated Gold Mines Ltd. (“Mosquito”, “MSQ”, “the company”) is a Vancouver, British Columbia based exploration company focused on development of the CUMO molybdenum-copper deposit located in the US state of Idaho.

• The CUMO project has an indicated resource of 1.44 billion tons containing 1.84 billion pounds of molybdenum, and 2.21 billion pounds of copper. Inferred resources are 2.52 billion tons containing 2.29 billion pounds of molybdenum, and 3.66 billion pounds of copper.

• Substantial quantities of silver and tungsten are also present and their recovery will reduce the overall cash cost of molybdenum production.

• The company has a strong management team and the chairman of the board of directors is Hongxue Fu, a professional expert in energy and mining and also president of the International Energy and Mineral Resources Investment Company Limited (HK).

Risks

• The value of the company is dependant on commodity prices

• At this time, the company does not own a producing mineral property.

• Development of a project the size of CUMO requires extensive capital investment.

Key Financial Data (FYE - June 30)

(C $) 2009 Q3-2010

(9mo)

Cash 1,733,738 4,605,615

Working Capital 1,084,009 4,150,739

Mineral Assets 14,808,088 17,429,654

Total Assets 21,108,604 25,722,790

Net Loss (4,506,480) (2,869,130)

Loss per Share (0.11) (0.05)

Sensitivity Of Fair Value to Changes in Moly Price Assumptions

M o P r ic e (U S $ ) V P S (C $ )

3

$ 6 .0 0 ( $ 2 .5 0 )

$ 8 .0 0 $ 0 .0 8

$ 1 0 .0 0 $ 2 .6 7

$ 1 2 .0 0 $ 5 .2 6

$ 1 4 .0 0 $ 7 .8 6

$ 1 6 .0 0 $ 1 0 .4 5

$ 1 8 .0 0 $ 1 3 .0 5

$ 2 0 .0 0 $ 1 5 .6 5

Mosquito Consolidated Gold Mines Ltd. is working to develop the CUMO project located near Boise, Idaho. The project

hosts what is considered the largest un-mined open pit molybdenum deposit in the world.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 2

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Company

Overview

Company

History

CUMO

Mosquito Consolidated Gold Mines Ltd. is a Vancouver based company focused on development of the CUMO project located just north of Boise, Idaho. The project contains what is billed as the largest un-mined open pit molybdenum deposit in the world. A recent independent preliminary economic assessment proposed production schemes at various levels of mill throughput with the following results:

Throughput Option (short tons)

50 kt/d 100 kt/d 150 kt/d 200 kt/d

NPV (US$ Billion @ 5%) 4 10 16 21

IRR% 19 29 36 39

Simple Payback Period 4.9 3 2.3 2

Discounted Payback Period (years @5%) 6.1 3.6 2.7 2.3

Total Operating Costs (per lb of Molybdenum Oxide Equivalent) 5.5 4.3 3.9 3.8

(Source: Mosquito Consolidated Gold Mines Ltd.)

The company is planning on completing approximately 30,000 meters of drilling on the project in 2010. The program will have several purposes including delineation of the final outline of the deposit for reserve calculation/final pit designs, geotechnical drilling to determine pit wall stabilities and metallurgical holes for bulk sampling. The company will pursue a pre-feasibility study in 2010 and feasibility in 2011. Should the company maintain its projected optimal timeline, construction on the project will begin in 2014. The company holds varying interests in a number of other exploration projects throughout North America. At the current time however, expenditures on these properties are at a minimum or have been written off. As a result, we have chosen to focus this initiating report solely on the company’s high priority CUMO project. All of the company’s projects are located in politically stable countries and many projects, including CUMO, are in mining friendly regions. The company was originally formed on June 8, 1971. In 1987, the company assumed control of Mosquito Creek Gold Mining Limited and the Mosquito Creek claim group leading to the current name Mosquito Consolidated Gold Mines Limited. The company acquired the rights to the CUMO deposit in 2004. Overview: The 100% MSQ owned CUMO project in Idaho, USA is billed as the largest un-mined open pit molybdenum deposit in the world. The project lies in the Idaho-Montana porphyry belt and is situated on trend, approximately 80 kilometers from Thompson Creek Metals Company Inc.’s (“Thompson Creek” TSX: TCM) Thompson Creek molybdenum mine also located in Idaho. The current resource states 1.44 billion tons indicated and 2.52 billion tons inferred. Contained metals include 1.84 billion pounds of molybdenum oxide (MoO3) indicated and 2.29 billion pounds inferred, as well as 2.21 billion pounds and 3.66 billion pounds of copper indicated and inferred respectively. There is also a significant component of silver and tungsten.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 3

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

A recently completed independent preliminary economic assessment studied various production scenarios using all indicated and inferred resources. At a production rate of

100,000 t/day, the project has an NPV of U$10 billion (at a 5% discount rate) and an

IRR of 29%. At a production rate of 150,000 t/day the project has an NPV of U$16

billion (at a 5% discount rate) and IRR of 36%.

Sensitivity analysis show that the project value is based primarily on molybdenum and copper recovery and that recovery of accessory metals will contribute to reduced cash costs in the production of molybdenum and copper. Despite its already massive size, the company believes that only about a quarter of the deposit has been drilled to date and significant expansion potential still exists. The company also has the opportunity to explore for at (or very near) surface high grade resources that could be used in initial production. Ownership: The company holds 100% ownership in the CUMO property which totals 345 unpatented claims and covers an area of 7,100 acres (2,873 hectares). The company originally acquired the property in 2004. On January 21, 2005, the company granted Kobex Resources Ltd. (Now Kobex Minerals Inc. – “Kobex” TSXV: KXM) the right to acquire a 100% interest in the property in 2005. However on October 6, 2006, Kobex chose not to meet its required commitments and surrendered all rights relating to the CUMO property, returning 100% ownership to MSQ. Location/Accessibility/Infrastructure: The property is located in the US state of Idaho approximately 37 air miles (approximately 60 kilometers) northeast of the city of Boise. The property has excellent access from Boise, which is serviced by both domestic and international air travel. The area is serviced by the Idaho Power Company and the nearest rail line is the Idaho Northern & Pacific line which runs through the town of Banks approximately 32 kilometres to the west. We anticipate a sufficient water supply will be obtainable with appropriate permits and a power line sits seven miles from the property. Despite receiving moderate amounts of snowfall in the winter, the property can be explored year round due to the established roads and infrastructure.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 4

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Figure 1: CUMO property location in Idaho. (Source: Mosquito Consolidated Gold Mines Ltd.)

Historic Exploration/Production: Between 1969 and 1981, prior to acquisition by the company, 26 drill holes – 3 air rotary, 23 DDH – were completed on the property for a total of 10,971 meters. In 1982, a historical resource was calculated for the project. The computer generated kriged block model estimated geological reserves of 1.387 billion tons of 0.093% MoS2 at a cut-off grade of 0.05% MoS2. A higher-grade core zone of 444 million tons of 0.135% MoS2 at a 0.10% MoS2 cut-off was also included in the estimate. This high-grade core is

incorporated in the current NI 43-101 resource estimate and comprises a part of the

resource blocks with a Gross Recoverable Value of over US$20/ton (see Resource

Estimate). There has been no historic production from the CUMO property. MSQ Exploration: In the three drilling programs from 2006 to 2008, subsequent to resuming control of the property in late 2006, the company completed 19 diamond drill holes

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 5

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

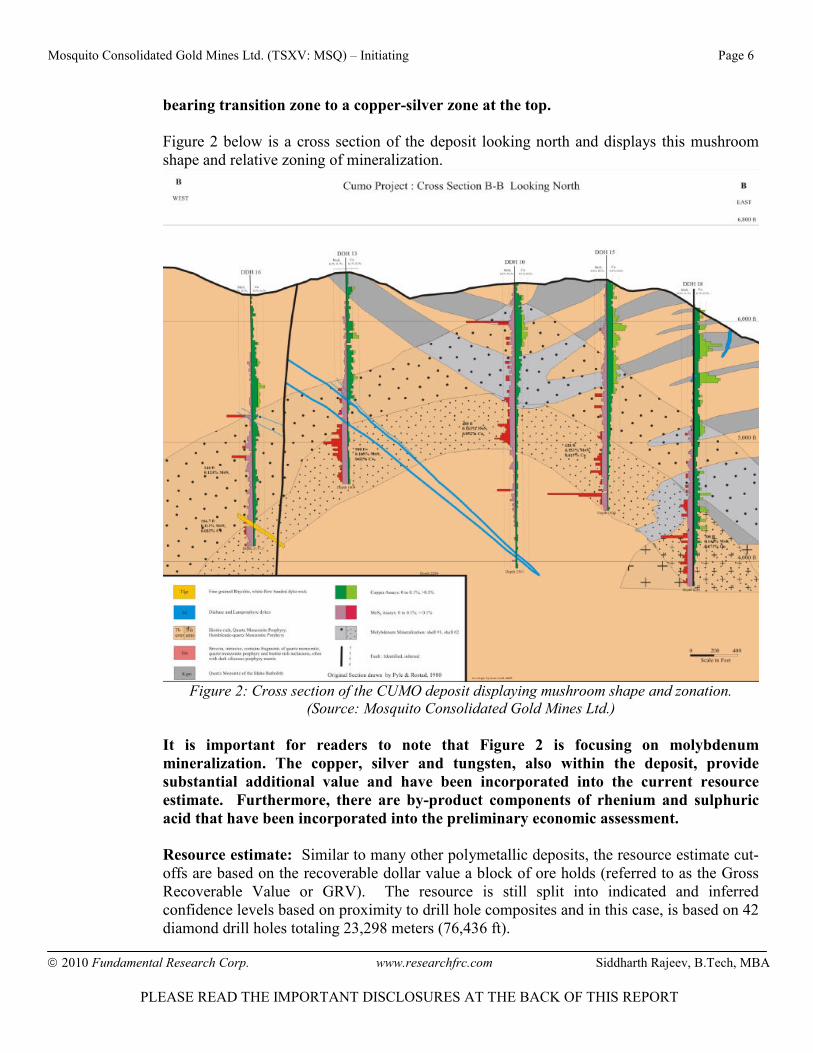

totaling 14,729 meters (44,188 feet). The 2009 drill program saw the completion of 9 diamond drill holes (46-09 to 54-09) totaling 6,100 meters (20,016 meters). These holes were not applied to the most recent resource calculation or in the preliminary economic assessment. Geology/Mineralization: CUMO is situated on the western side of the Atlanta Lobe of the granitic Idaho Batholith, which covers approximately 15,400 square miles. In the Cumo project area, the batholith ranges in age from 85 to 95 million years old and has a notable increase in CaO, MgO and Al2O3. The increased calcium indicates the presence of

Calcium Carbonate which is a potential benefit as it may impart acid neutral or even

acid reducing characteristics of tailings. This, we believe, is likely to be beneficial to the

permitting process. The deposit is within the Idaho-Montana porphyry belt, which is a northeast-southwest trend of porphyry copper and molybdenum deposits as well as precious metal deposits. Company geologists believe the CUMO deposit is situated at the intersection of two structurally controlled intrusion events which occurred several millions of years apart. The first event involved the intrusion of granites into the Idaho Batholith along east-west trending structures resulting in a typical copper porphyry deposit. The second event, which occurred several millions of years later, involved the intrusion of several porphyritic dykes along a northeast-southwest trending structure called the Trans-Challis fault system and brought molybdenum porphyry mineralization. The company believes that being located at the intersection of these two events is what resulted in both the immense size and zoned mineralization. Zoned mineralization is a common characteristic of plutonic porphyry Cu-Mo deposits – in this case Mo-Cu as molybdenum is the primary commodity of value – as described by the British Columbia Geological Survey (BCGS) in the mineral deposit profiles database. The BCGS notes that “The intrusions can display internal compositional differences as a

result of differentiation with gradational to sharp boundaries between the different

phases of magma emplacement. Local swarms of dikes (dykes), many with associated

breccias, and fault zones, are sites of mineralization.” Four primary metal domains have been identified (listed as they would appear from surface to depth down a drill hole):

- oxides - Cu-Ag - Cu-Mo - Mo

For resource estimation purposes, the oxide zone has been incorporated into the Cu-Ag zone.

The molybdenum mineralization sits within two inverted, cup-shaped shells of

mineralization that form a shape akin to a mushroom. The mineralization is strongly

zoned to form a molybdenum rich zone at depth through a copper-molybdenum

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 6

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

bearing transition zone to a copper-silver zone at the top.

Figure 2 below is a cross section of the deposit looking north and displays this mushroom shape and relative zoning of mineralization.

Figure 2: Cross section of the CUMO deposit displaying mushroom shape and zonation.

(Source: Mosquito Consolidated Gold Mines Ltd.)

It is important for readers to note that Figure 2 is focusing on molybdenum

mineralization. The copper, silver and tungsten, also within the deposit, provide

substantial additional value and have been incorporated into the current resource

estimate. Furthermore, there are by-product components of rhenium and sulphuric

acid that have been incorporated into the preliminary economic assessment.

Resource estimate: Similar to many other polymetallic deposits, the resource estimate cut-offs are based on the recoverable dollar value a block of ore holds (referred to as the Gross Recoverable Value or GRV). The resource is still split into indicated and inferred confidence levels based on proximity to drill hole composites and in this case, is based on 42 diamond drill holes totaling 23,298 meters (76,436 ft).

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 7

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Blocks are considered waste, stockpile or run of mill based on having GRV’s of: less

than US$7.50/ton, between US$7.50 and US$20/ton and greater than US$20/ton

respectively. The table below summarizes the CUMO resource.

(Source: Mosquito Consolidated Gold Mines Ltd.)

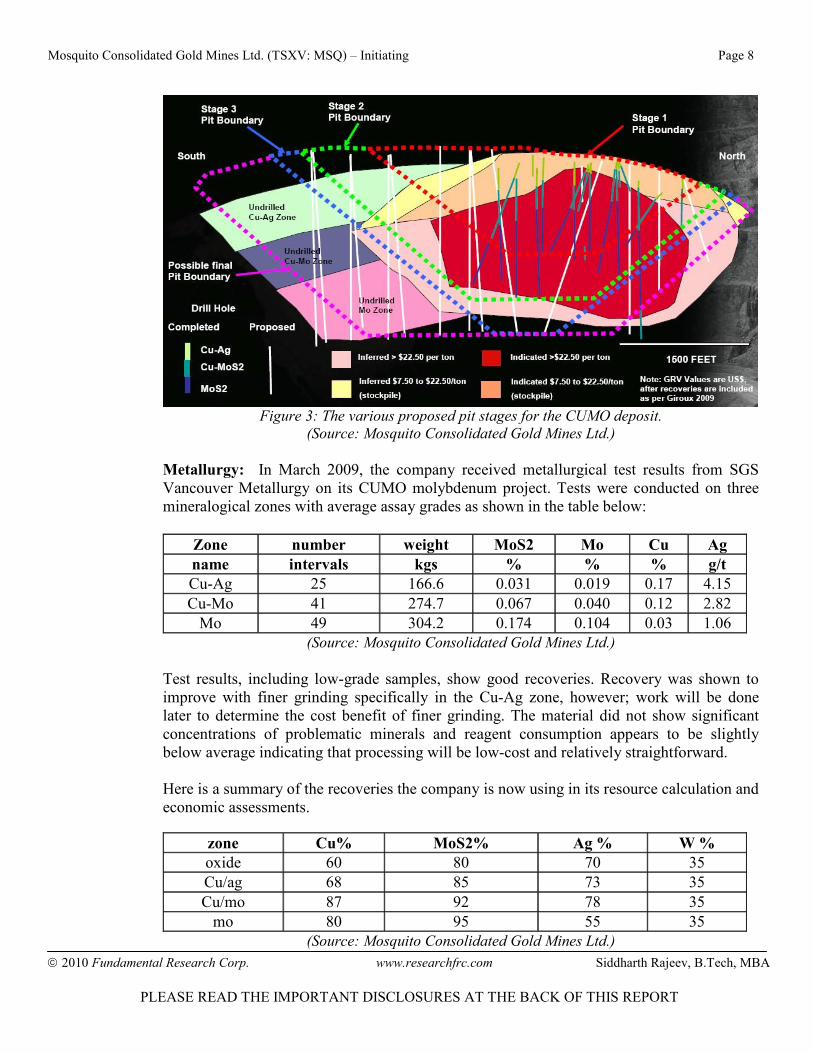

The GRV is based on (from CUMO Property Preliminary Economic Assessment, Giroux, G., 2009): MoS2 – Molybdenum is sold as molybdenum trioxide (MoO3) which has a higher Mo content. The price used for the GRV calculations in this study for MoO3 is US$15/lb. MoO3 is calculated from MoS2 by the following: Pounds Mo = MoS2 * 20/1.6681 and then Pounds MoO3 = Pounds Mo * 1.5 Cu – copper price of US$1.50/lb was used Ag – silver price of US$12.00/oz was used W – tungsten price of US$8.50/lb was used Figure 3 below is a long section of the CUMO deposit with interpreted resource areas and proposed pit boundaries. The reader will notice that slightly different numbers are used for GRV values but the image still provides the appropriate visual representation of the deposit. Several things to observe in Figure 3:

- A low strip ratio is anticipated. The company believes it will be 1:1:1 in terms of waste : stockpile : ore.

- The high-grade core described in resource estimates dominates the proposed pits. - Significant exploration potential exists to the South.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 8

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Figure 3: The various proposed pit stages for the CUMO deposit.

(Source: Mosquito Consolidated Gold Mines Ltd.)

Metallurgy: In March 2009, the company received metallurgical test results from SGS Vancouver Metallurgy on its CUMO molybdenum project. Tests were conducted on three mineralogical zones with average assay grades as shown in the table below:

Zone number weight MoS2 Mo Cu Ag

name intervals kgs % % % g/t

Cu-Ag 25 166.6 0.031 0.019 0.17 4.15

Cu-Mo 41 274.7 0.067 0.040 0.12 2.82

Mo 49 304.2 0.174 0.104 0.03 1.06

(Source: Mosquito Consolidated Gold Mines Ltd.)

Test results, including low-grade samples, show good recoveries. Recovery was shown to improve with finer grinding specifically in the Cu-Ag zone, however; work will be done later to determine the cost benefit of finer grinding. The material did not show significant concentrations of problematic minerals and reagent consumption appears to be slightly below average indicating that processing will be low-cost and relatively straightforward. Here is a summary of the recoveries the company is now using in its resource calculation and economic assessments.

zone Cu% MoS2% Ag % W %

oxide 60 80 70 35

Cu/ag 68 85 73 35

Cu/mo 87 92 78 35

mo 80 95 55 35

(Source: Mosquito Consolidated Gold Mines Ltd.)

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 9

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Tungsten results are preliminary and Tungsten recovery will be examined further in the feasibility metallurgical study. The preliminary flotation studies indicate cleaning and separation will yield saleable Cu (>20% Cu) and Mo (>50% Mo) concentrates. It is also predicted that the saleable molybdenum concentrate should contain between 30 and 40 gms/t Rhenium. The following table shows average grades and recoveries of producing molybdenum mines:

Company Mine Location Average Average

MoS2% %Recovery

Thompson Creek Endako BC, CAN 0.085 82

Thompson Creek ID, USA 0.140 86

Freeport Henderson CO, USA 0.384 84 (Source: Company Reports)

Based on the metallurgical findings by SGS Vancouver Metallurgy and comparison to

operative molybdenum mines, the company can attain feasible molybdenum extraction

from the Cu-Mo, and Mo ore zones. Extraction of molybdenum from the oxidized zones may still add value in areas where the oxidized zones must be mined to provide access to the higher grade sulphide deposit. Independent Preliminary Economic Assessment: In November 2009, a preliminary economic analysis was conducted by Ausenco Canada Inc. Ausenco’s findings are summarized below:

Throughput Option (short tons)

50 kt/d 100 kt/d 150 kt/d 200 kt/d

NPV (US$ billion @ 5%) 4 10 16 21

IRR% 19 29 36 39

Simple Payback Period 4.9 3 2.3 2

Discounted Payback Period (years @5%) 6.1 3.6 2.7 2.3

Total Operating Costs (per lb of Molybdenum Oxide Equivalent) 5.5 4.3 3.9 3.8

(Source: Mosquito Consolidated Gold Mines Ltd.)

These estimates were based on a 40 year mine life. The costs were found to decrease with an increased mill throughput, however; base metal projects over 100 kt/d are somewhat rare as they require significantly higher capital costs. We believe high capital costs in base metal projects can carry high risk and are more difficult to finance. See our project valuation below under Valuation. The LOF (Life of Mine) costs are summarized on the next page.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 10

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Throughput Option (short tons)

50 kt/d 100 kt/d 150 kt/d 200 kt/d

Total Initial Capital Cost ($US M) 1,600 2,200 2,800 3,400 Total LOM Operating Cost/ton Mill feed per year ($US) 11.2 8.6 7.6 7.1

Total LOM Operating Cost/ton Mill feed per year ($US) *excluding stockpile mining cost

9.6 7.8 7.2 6.8

(Source: Mosquito Consolidated Gold Mines Ltd.)

The capital costs used by Ausenco did not include any infrastructure necessary to provide sufficient power and road access to the property. However, these costs should prove relatively negligible compared to overall project costs. The operating costs consider budget quotes on all processing reagents and assume an electricity cost of $0.063/kwh as quoted from nearby Thompson Creek Mine. Average costs for other base metal mines are shown in the table below for comparison.

Mine Tons per Day Operating Cost ($US/t)

Bingham 163 000 6.25

Sierrita 143 000 4.53

Mercator - Mineral Park 50 000 4.57

Baghdad 75 000 5.1

Mt. Hope 60 625 6.81

Thompson Creek 25 000 11.63

Highland Valley 118 314 6.1

Morenci - SXEW 90 000 2.97

Morenci - all 203 314 4.75

Morenci - sulfide 68 000 16.08

(Source: Mosquito Consolidated Gold Mines Ltd.)

The estimated operating costs for the CUMO project are higher than average for a base metals project of comparable size. However, assuming the operating costs are not found to be significantly greater after further research, the estimated CUMO operating costs should prove viable. Revenues for the CUMO project were predicted using US$15/lb, US$1.50/lb, US$12/oz, US$8.50/lb, US$6500/kg, and US$135/t prices for MoO3, Cu, Ag, W, Re, and acid, respectively. Revenues were calculated excluding taxes, interest, and royalties. A sensitivity analysis was performed by Ausenco on cost and price assumptions. The results

show that the NPV was most sensitive to the price of molybdenum, and the capital costs

of the project. The NPV proved least sensitive to the price of Rhenium, and Acid, suggesting that the CUMO project can operate producing molybdenum and copper only. Current Status: The company has received assay results for the nine holes completed in the 2009 drill program. Results were positive having both extended mineralization outward from the current resource area, as well as contributing valuable information to the geologic model.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 11

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Highlight intersections so far:

Hole 47-09 – this hole intersected 589 meters grading 0.18% Cu and 0.056% MoS2. The hole also confirmed the presence of an older porphyry copper-silver system that is more dominant to the west of the deposit in an area that was previously considered as waste in the preliminary economic assessment. Hole 52-09 – This hole intersected 426.7 meters grading 0.06% Cu and 0.103% MoS2 (1.01% Cu Eq. Or 0.112% MoS2, or 2.02 lbs MoO3). The hole expanded the molybdenum mineralized zone to the south. Hole 53-09 – This hole intersected 509.3 meters grading 0.19% Cu and 0.091% MoS2 (0.97% Cu Eq. Or 0.108% MoS2 Eq, or 1.94 lbs MoO3). The hole confirms that copper mineralization is increasing to the west, while the molybdenum mineralization continues to the south and southwest, thus expanding the mineralized zone.

Subject to financing, the company is planning on completing up to 30,000 meters in drilling between June and September of 2010, with the use of up to seven drills. The program will have several purposes including delineation of the final outline of the deposit for reserve calculation/final pit designs, geotechnical drilling to determine pit wall stabilities and metallurgical holes for bulk sampling. Further goals the company anticipates on meeting include (taken from MSQ corporate presentation and discussions with management):

- Filing Environmental Assessment (EA) for public review and granting of permit for additional access (in progress)

- Initiate engineering studies to finalize locations for mill, tailing and waste dump sites. Contract various engineering specialists for tasks.

- Initiate bankable feasibility metallurgy study with 3.5 tonne bulk sample and 100-20 kg variability study.

- Complete a pre-feasibility study Development Timeline: Through discussions with management, we have come up with the following rough timeline for development of the project should exploration continue to be successful:

2010 – Completion of pre-feasibility study on the project. 2011 – Completion of a feasibility study on the project 2012 – Obtain final permitting and financing 2014/2015 – Construction

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 12

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Management

Brian A. McClay – President, Chief Executive Officer Brian A. McClay, President and Chief Executive Officer has 40 years experience in the global mining industry, and a well-earned reputation internationally, as an intuitive mine builder. His multi-faceted career includes prospecting, contracting for mineral exploration, diamond drilling, open pit mining, and managing open pit and underground mining operations. Mr. McClay has directed Mosquito Consolidated Gold Mines Limited for the past 15 years, as President and CEO from 1990 to 2000 and again from 2004 to present day. He is well known for his ability to recognize property potential, and also for his extraordinary negotiating, partnership and deal-making skills. His combined field and management experience are major assets to Mosquito Consolidated Gold Mines Limited.

Shaun M. Dykes, M.Sc., P.Geo – Exploration Manager, Director Shaun M. Dykes, Director and Exploration Manager holds a B.Sc(Eng) and a M.Sc(Eng) in Geology from Queen's University in Ontario. Prior to joining Mosquito Consolidated in 1994, he spent 15 years with Westmin Mines Ltd of Vancouver, as a Senior Project Geologist. Mr. Dykes is an integral part of the Mosquito Consolidated management team. His wealth of knowledge and incomparable passion for geology are well-suited to Mosquito Consolidated's culture of applying both state-of-the-art and contrary science to exploit previously under-developed or incorrectly explored resource projects.

Dr. Matt Ball, Ph.D., P.Geo., - Sr. Geologist, Director Dr. Ball is a member of the Association of Professional Engineers and Geoscientists of British Columbia, Canada, the Society of Economic Geologists, USA and has 25 years international experience in exploration and operations geology. He was a semi-finalist winner of the "Goldcorp Challenge" and subsequently employed by Goldcorp and the overall winner, Geoinfomatics Explorations Inc.

Hongxue Fu – Chairman of the Board Hongxue Fu is a professional expert in energy, mining, real estate and financial service investment. He has extensive connections in a variety of industries inside China and worldwide. He has been extremely successful and accumulated valuable experiences in capital intensive businesses. Mr. Fu focused his efforts on energy and mineral resource development when he became chairman of International Energy & Mineral Resources Investment (Hong Kong) Company Limited.

Wayne Ash, P.Eng – Director

Wayne Ash, Director and Mining Engineer graduated from the Haileybury School of Mines in 1965 with a B.Sc. in Mining Engineering and Michigan Technological University in 1969 with a Doctorate in Engineering. He has 40 years experience as a miner, mine manager and consulting engineer and is currently affiliated with the Canadian Institute of Mining and Metallurgy, the American Institute of Mining, Metallurgical and Petroleum Engineers and the Association of Professional Engineers of British Columbia. Mr. Ash's vast and varied

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 13

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Management

Rating

experience has benefited all company projects, and his industry affiliates have proven beneficial to company growth worldwide.

Patrick Bronson – Director Patrick Bronson, Director, has 40 years of experience minerals and metals exploration and development industry, primarily as a project manager, drilling contractor and helicopter pilot. He acted as a Director of Mosquito Consolidated Gold Mines Limited for 16 years, relieving Mr. McClay from his position as President of the company from 2000 to 2004. Mr. Bronson's industry knowledge and contacts are tangible assets to Mosquito Consolidated's management.

William F. Jefferies – Corporate Secretary, Director William F. Jefferies, Director and Corporate Secretary was self-employed as a land developer and private business investor before joining Mosquito Consolidated in 1992. Mr. Jefferies manages the company's corporate office and oversees its efficient administration. We believe that one of the most important aspects of a junior mining company is its management. Therefore we have developed a management rating system as a quantitative way to rate management based on a number of factors, including technical experience, the ability to raise financing, and management’s time commitment to the company. We also analyzed trading records to identify for evidence of unusual trading by management. Our

net rating for MSQ (see below) is 3.6 out of 5.0, which we have rated above average.

Management Rating

3.6

5.0

3.2

3.7

3.7

3.8

4.0

0% 20% 40% 60% 80% 100%

Net Rating

Any unusual insider trading in the past 12 months

Team's focus on the company

Experience in projects similar to the current project

Track record in raising capital/working for public companies

Experience in putting mines to production/generating

prospects

Technical Experience

NO

As per the most recent “Management Information Circular”, the company's board of directors consist of seven individuals, of which two are independent. The majority of directors hold shares in the company. The Audit Committee is composed of Brian McClay, Patrick Bronson and Wayne Ash.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 14

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Outlook on

Molybdenum

According to the United States Geological Survey, about 75% of molybdenum is consumed by iron, steel and super-alloy producers. Steel demand growth has been one of the major drivers of molybdenum demand. Demand for steel (as shown in the chart below) has been primarily driven by activities in construction, mechanical machinery, metal products, and automotives sectors.

(Source: OECD, Worldsteel)

As the primary applications are related to economic growth, the global economic slowdown resulted in a significant drop in steel production, and molybdenum prices in 2009. After falling below 50% in early 2009, steel production utilization rates in the NAFTA region have recovered to around 70%, but are still below historical levels (according to the OECD Steel Committee). Increasing utilization rates, global steel consumption (as shown in the chart below) and signs of a recovery in global economic growth, we believe, should provide support for molybdenum prices in the near term.

(Source: OECD, World Steel Dynamics)

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 15

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Financials

The following chart shows molybdenum prices since June 2007. Molybdenum is currently trading at about US$14/lb.

Over the long-term, we expect prices to drop from current levels (our long-term forecast is US$10/lb) primarily because it is estimated that molybdenum resources are adequate to supply world needs for the foreseeable future. However, we expect prices to stay well above the historic average of US$6.10/lb due to the following reasons:

• Demand from BRIC countries

• Demand from the oil sector

• Increasing capital expenditures and higher production costs. • Expected decrease in Mo exports by China.

• Longer lead times to build new molybdenum mines.

• Not easily substitutable due to its unique characteristics, availability and versatility At the end of March 2010, the company had $4.61 million in cash. Working capital was $4.15 million. The company reported a net loss of $2.87 million (EPS: -$0.05) in the first nine months of FY2010. We estimate the company had a burn rate (spending on operating and investing activities) of $0.37 million per month for the first nine months in FY2010, down from $0.51 million in FY2009 (12 month period). The table below shows a summary of the company’s cash and liquidity position.

(in C$) 2009 2010 (9 MO)

Working Capital 1,084,009 4,150,739

Current Ratio 2.1 6.7

LT Debt / Assets - -

Burn Rate (per month) (508,776) (372,006)

Cash from financing activities 7,015,387 6,103,922

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 16

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

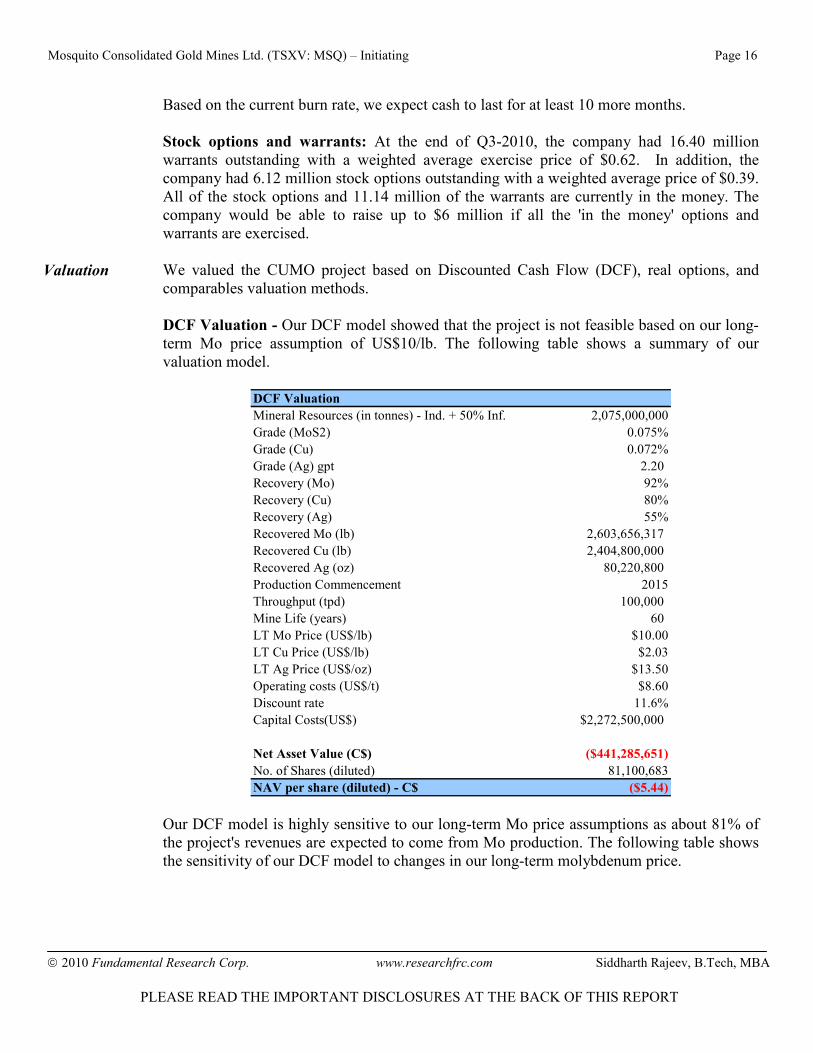

Valuation

Based on the current burn rate, we expect cash to last for at least 10 more months.

Stock options and warrants: At the end of Q3-2010, the company had 16.40 million warrants outstanding with a weighted average exercise price of $0.62. In addition, the company had 6.12 million stock options outstanding with a weighted average price of $0.39. All of the stock options and 11.14 million of the warrants are currently in the money. The company would be able to raise up to $6 million if all the 'in the money' options and warrants are exercised. We valued the CUMO project based on Discounted Cash Flow (DCF), real options, and comparables valuation methods. DCF Valuation - Our DCF model showed that the project is not feasible based on our long-term Mo price assumption of US$10/lb. The following table shows a summary of our valuation model.

DCF Valuation

Mineral Resources (in tonnes) - Ind. + 50% Inf. 2,075,000,000

Grade (MoS2) 0.075%

Grade (Cu) 0.072%

Grade (Ag) gpt 2.20

Recovery (Mo) 92%

Recovery (Cu) 80%

Recovery (Ag) 55%

Recovered Mo (lb) 2,603,656,317

Recovered Cu (lb) 2,404,800,000

Recovered Ag (oz) 80,220,800

Production Commencement 2015

Throughput (tpd) 100,000

Mine Life (years) 60

LT Mo Price (US$/lb) $10.00

LT Cu Price (US$/lb) $2.03

LT Ag Price (US$/oz) $13.50

Operating costs (US$/t) $8.60

Discount rate 11.6%

Capital Costs(US$) $2,272,500,000

Net Asset Value (C$) ($441,285,651)

No. of Shares (diluted) 81,100,683

NAV per share (diluted) - C$ ($5.44) Our DCF model is highly sensitive to our long-term Mo price assumptions as about 81% of the project's revenues are expected to come from Mo production. The following table shows the sensitivity of our DCF model to changes in our long-term molybdenum price.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 17

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Mo Price (US$) VPS (C$)

-5

$4.00 ($17.17)

$6.00 ($13.26)

$8.00 ($9.35)

$10.00 ($5.44)

$12.00 ($1.53)

$14.00 $2.37

$16.00 $6.28

$18.00 $10.19

$20.00 $14.10

Real options valuation - Unlike DCF models, real options valuation models account for the volatility in commodity prices, and also management’s ability to pursue or abandon projects. Since early stage mining projects can be considered as options, we used a real options valuation model to value the project as if it were an option. Our real options valuation model, using the same inputs as we used for our DCF model, gave a fair value estimate of $10.49 per share.

Estd.Value of Minerals if extracted today (US$) 832,148,609$

Annualized Standard Deviation of Mineral prices 49.0%

Capital Investment (US$) 1,252,420,658$

Estd. Mine Life (years) 60

Riskfree Rate 3.16%

Stock Price $832,148,609 T.Bond rate 3.16%

Strike Price $1,252,420,658 Variance 0.24

Expiration (in years) 60 Annualized div yield 0%

d1 = 2.289

N(d1) = 0.989 Value of Option (C$) $851,051,911

d2 = -1.507 No of outstanding shares 81,100,683

N(d2) = 0.066 Value per share $10.49

Real Options Valuation

Output

Inputs relating to the underlying asset

Comparables Valuation - Based on an average peer Enterprise Value (EV) to resource (Mo. equivalent in lbs) ratio of $0.06/lb, we believe the CUMO project should be valued at $2.53 per share.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 18

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Conclusions &

Rating

Company Symbol EV /

Resource

1 Velocity Minerals Ltd. VLC $0.186

2 Western Troy Capital Resources Inc. WRY $0.071

3 Creston Moly Corp. CMS $0.050

4 International PBX Ventures Ltd. PBX $0.038

5 Bard Ventures Ltd. CBS $0.021

6 Torch River Resources Ltd. TCR $0.030

7 Inca Pacific Resources Inc. IPR $0.001

Average EV/Resource ($/lb) $0.06

Fair Value of CUMO $2.53

* Resources = Measured and Indicated + 50% Inferred/Historic Resource Estimates

* Molybdenum equivalent was determined based on copper price of US$2.03/lb,

silver price of US$13.5/oz, gold price of US$900/oz, and molydenum price of US$10/lb Adding working capital, and the book value of the company's other projects to the average valuation of the CUMO project (based on our DCF, real options and comparables valuation models), we arrived at a fair value of $2.67 per share.

Valuation Summary

CUMO Project

DCF ($5.44)

Real Options $10.49

Comparables $2.53

Average $2.53

Book Value of Other Projects $0.10

Working Capital $0.04

Fair Value $2.67 The sensitivity of our fair value to changes in our long-term Mo prices is shown below.

Mo Price (US$) VPS (C$)

3

$6.00 ($2.50)

$8.00 $0.08

$10.00 $2.67

$12.00 $5.26

$14.00 $7.86

$16.00 $10.45

$18.00 $13.05

$20.00 $15.65

We initiate coverage on MSQ with a BUY rating and fair value of $2.67 per share.

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 19

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Risks

The following risks, though not exhaustive, may cause our estimates to differ from actual results:

• The value of the company is dependent on commodity prices.

• At this time, the company does not own a producing mineral property.

• Development of a project the size of CUMO requires extensive capital investment.

• Access to capital and share dilution.

We rate the company’s shares a RISK of 5 (Highly Speculative).

Mosquito Consolidated Gold Mines Ltd. (TSXV: MSQ) – Initiating Page 20

2010 Fundamental Research Corp. www.researchfrc.com Siddharth Rajeev, B.Tech, MBA

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Fundamental Research Corp. Equity Rating Scale:

Buy – Annual expected rate of return exceeds 12% or the expected return is commensurate with risk Hold – Annual expected rate of return is between 5% and 12% Sell – Annual expected rate of return is below 5% or the expected return is not commensurate with risk Suspended or Rating N/A— Coverage and ratings suspended until more information can be obtained from the company regarding recent events. Fundamental Research Corp. Risk Rating Scale:

1 (Low Risk) - The company operates in an industry where it has a strong position (for example a monopoly, high market share etc.) or operates in a regulated industry. The future outlook is stable or positive for the industry. The company generates positive free cash flow and has a history of profitability. The capital structure is conservative with little or no debt. 2 (Below Average Risk) - The company operates in an industry where the fundamentals and outlook are positive. The industry and company are relatively less sensitive to systematic risk than companies with a Risk Rating of 3. The company has a history of profitability and has demonstrated its ability to generate positive free cash flows (though current free cash flow may be negative due to capital investment). The company’s capital structure is conservative with little to modest use of debt. 3 (Average Risk) - The company operates in an industry that has average sensitivity to systematic risk. The industry may be cyclical. Profits and cash flow are sensitive to economic factors although the company has demonstrated its ability to generate positive earnings and cash flow. Debt use is in line with industry averages, and coverage ratios are sufficient. 4 (Speculative) - The company has little or no history of generating earnings or cash flow. Debt use is higher. These companies may be in start-up mode or in a turnaround situation. These companies should be considered speculative. 5 (Highly Speculative) - The company has no history of generating earnings or cash flow. They may operate in a new industry with new, and unproven products. Products may be at the development stage, testing, or seeking regulatory approval. These companies may run into liquidity issues, and may rely on external funding. These stocks are considered highly speculative.

Disclaimers and Disclosure

The opinions expressed in this report are the true opinions of the analyst about this company and industry. Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The analyst and Fundamental Research Corp. “FRC” does not own any shares of the subject company, does not make a market or offer shares for sale of the subject company, and does not have any investment banking business with the subject company. Fees of less than $30,000 have been paid by MSQ to FRC. The purpose of the fee is to subsidize the high costs of research and monitoring. FRC takes steps to ensure independence including setting fees in advance and utilizing analysts who must abide by CFA Institute Code of Ethics and Standards of Professional Conduct. Additionally, analysts may not trade in any security under coverage. Our full editorial control of all research, timing of release of the reports, and release of liability for negative reports are protected contractually. To further ensure independence, MSQ has agreed to a minimum coverage term including an initial report and three updates starting with this report. Coverage can not be unilaterally terminated. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time. The performance of FRC’s research is ranked by Investars. Full rankings and are available at www.investars.com. The distribution of FRC’s ratings are as follows: BUY (73%), HOLD (8%), SELL (4%), SUSPEND (15%). To subscribe for real-time access to research, visit http://www.researchfrc.com/subscription.htm for subscription options. This report contains "forward looking" statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company's products/services in the marketplace; acceptance in the marketplace of the Company's new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company's periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. A report initiating coverage will most often be updated quarterly while a report issuing a rating may have no further or less frequent updates because the subject company is likely to be in earlier stages where nothing material may occur quarter to quarter. Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated, and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report. The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.