nasdaq nm / tase - symbol: igld eli holtzman, ceo doron turgeman, cfo q2 2006 internet gold leading...

TRANSCRIPT

NASDAQ NM / TASE - symbol: IGLD

Eli Holtzman, CEODoron Turgeman, CFOQ2 2006

Internet GoldInternet GoldLeading Israeli communications Leading Israeli communications

and Interactive media Groupand Interactive media Group

2

Forward-Looking Statement

The statements contained herein that are not purely historical are forward-looking

statements. These forward-looking statements, and

especially those regarding the 012 merger, involve risks and uncertainties and actual

results could differ materially from the results discussed in these statements.

3

4

5

Committed to growth…2007 - crossing the 1B NIS revenue line

2006– Build-out of International

VoIP Telephony services

– Expansion of InternetAdvertising

– Expansion of BusinessServices

– 012 acquisition to be completed and operations to be consolidated - Q4/06

2007– 1st full year of the merged

operation

– Continued growth expected in all lines of business (under both ‘smile’ and ‘012’ brands)

Primary drivers:

in NIS millions

1,250

405

180 220 298

0

200

400

600

800

1000

1200

1400

2003 2004 2005 2006 2007Goal

Organic CAGR = +20%

M&A CAGR = +47%

6

Israel’s telecommunications market

Cellular, 11.9

Channel TV, 3.1

ILD, 1.6

Fixed line & data, 5.3

Internet, 1.3

Source: Israeli MoC

2005 – NIS 23.2 B

7

2006/07: riding the expansion of our marketsto the next level of revenues and profits

Access Services

Major market share in a stable market

Stronger emphasis on biz sector

VoIP/VOB/TDM Telephony

Two strong brands to drive growth in market share

Start commercial penetration of domestic VoB

Online Advertising

We expect our advertising revenues will grow as media budgets continue to shift to the Internet

Efficient merger

1 + 1 = 3…

Significant savings on opex / capex

Efficient management of the two brands

Conservative estimation of 50-60M NIS/yr savings

8

9

1 + 1 = 3 !!

Perfect synergy between the two companies

Global data networksRoaming servicesCall centersFixed domestic telephonyPre/post paid cardsTDM platform

Value Added ServicesBiz servicesHi level integrationHi level data protectionDealer networke-Media and e-

Commerce

10

Rationale for the 012 acquisition &

merger

Revenues 159.7 335 494.7 1,150

EBIT 13.6 40 53.6 175-185***

EBITDA 27.5 70 97.5 270-280***

Employees 789 1,290 2079 Synergy

Total*

H1/2006

* Based on IGLD estimate –NIS in millions

*** Communications’ EBIT / EBITDA goals for 2007 exclude one time expenses relating to the merger. These goals assumes full synergy of merger to be achieved Q2/07

2007**

** company’s goals for the 1st full year of merged communications operations

SC

L

* communications activities only

11

Leveraging state of the art telephony infrastructure

To drive further growth

Most sophisticated VoIP platform World class TDM platform Auxiliary platforms (anti-fraud / billing / CRM etc.)

ILD –growth driver for the communications industryInternational voice traffic from Israel - up 10.3% in 2005 vs. 2004

- up 12% in H1/06 vs. H1/05(Source – Israeli MoC)

+ = cash generators !!

ILD, 1.6

12

State-of-the-art telephony infrastructure

Solid investment in class 5 fixed telephony No further significant investments required Auxiliary platforms (anti-fraud / billing / CRM etc.)

Fixed telephony Total fixed telephony market in Israel - NIS 5.3B in 2005

012 currently have only ~ 13k subscribers’ lines Our goal ~ 5% market share of this significant segment within 3-4

years Future marketing to rely on existing customer base of ~ 800 k

subscribers

072 / 075 - additional potential growth driver

Fixed line &

data, 5.3

13

14

2006/2007: Growth of Online Advertising

continues

“Marketers are shifting more of their advertising budgets online… As consumers spend a larger percentage of their media time online, it is natural for the flow of advertising dollars to follow.” David Silverman, Partner, PricewaterhouseCoopers LLP

“Almost half of all marketers plan to increase online ad spending by decreasing spending in other channels…”Forrester Research

16

67

10

12

0

2

4

6

8

10

12

14

16

18

2002 2003 2004 2005 2006*

Source: PWC IAB Internet Advertising Report, Sept. ‘05

US Internet Advertising CAGR = +22%

Source: Market surveys & IGLD estimates

Israel Internet Advertising CAGR = +40%

& company's estimates

50

36

2212

65

0

10

20

30

40

50

60

70

2002 2003 2004 2005 2006

*

* Q3/06 - Media market affected by current war conditions

in US$ billions

in US$ millions

estimated

15

Israeli Online Advertising is ripe for growth

Israel’s broadband penetration is among the highest in the world

~70% of Israeli households have Internet access ~ 95% are connected via broadband!

>40% of users are online >10 hours per week. 2.7M users per day!

Israel’s online advertising budgets are low compared to “eyeball” exposure –ad spending always follows rating

Internet Advertising in Israel is currently > 6-7% of overall media spending (~ $900M in 05’) - growing fast

SEARCH - additional growth potential: US search revenues - 40% of total e-Adv. much higher than in Israeli market

16

Smile.Media – diversification

msn-Israel

50.1% SML

49.9% MS Corp.

Hebrew language portal Messenger, Hotmail Israel & MSN Search Israel

start 100% General portal & Search engine

nirshamim 100% Academic portal

zahav.ru 100% Russian language portal

V-games 100% Games content portal

seret 51% Cinema portal

yahala 51% Arab-language portal

TheMoney 50.1% Lead-generation financial

portal

tipo 50% Children’s portal

netex Search engine & directory

goop Exclusive marketing rights Youth portal

GPG e-Advertising network

17

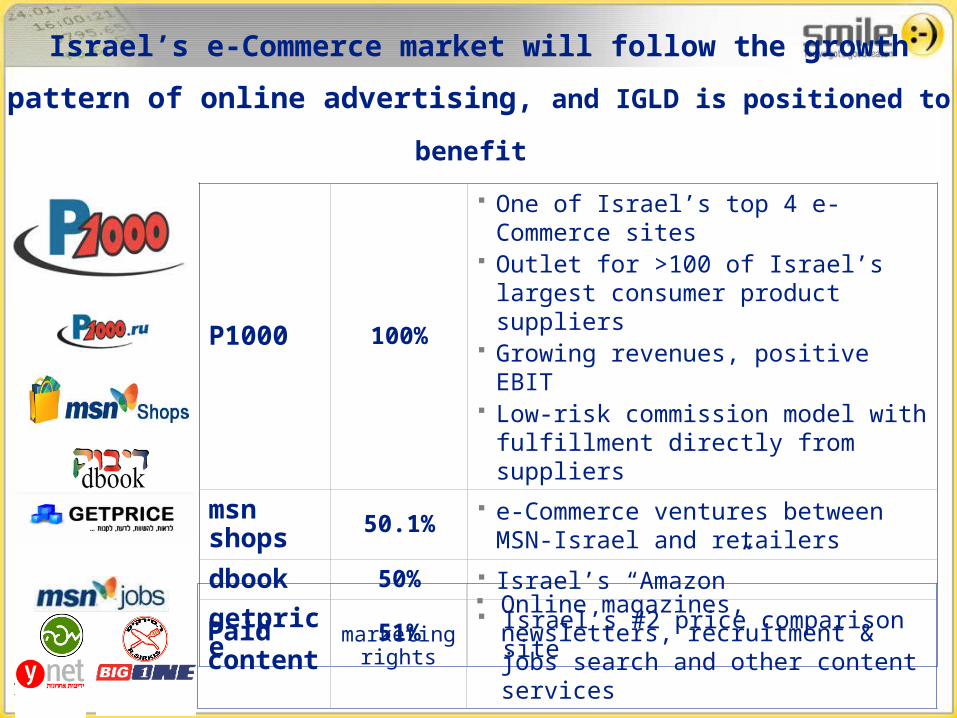

Israel’s e-Commerce market will follow the growth

pattern of online advertising, and IGLD is positioned to

benefit

P1000 100%

One of Israel’s top 4 e-Commerce sites

Outlet for >100 of Israel’s largest consumer product suppliers

Growing revenues, positive EBIT Low-risk commission model with

fulfillment directly from suppliers

msn shops 50.1%

e-Commerce ventures between MSN-Israel and retailers

dbook 50% Israel’s “Amazon”

getprice 51% Israel’s #2 price comparison site

Paid content

marketing rights

Online magazines, newsletters, recruitment & jobs search and other content services

18

19

13.3 16.5 17.5

59.4 67.878.4 79.7

13.9

73.381.1

94.9 97.2

Q3 05 Q4 05 Q1 06 Q2 06

Smile.media Smile.communications

Revenues

2.64.0 3.5

2.8 4.5

5.7

2.9

7.9

11.49.7

7.15.7

03 05 Q4 05 Q1 06 Q2 06

Smile.media Smile.communications

NIS in millions

EBIT

Quarterly Growth

NIS in millions

Two pure-play subsidiaries

20

43 52 72146 176 246

333

1,150

34 100

1,250

180 220298

405

2003 2004 2005 2006* 2007**

Smile.media Smile.communications

Revenues

7 10 1422 18 1932

180

222

202

24 25 29 46

2003 2004 2005 2006* 2007**

Smile.media Smile.communications

NIS in millionsEBIT

Two pure-play subsidiaries

Annual Growth* company’s goals

** Ebitda goal for 2007 ~ 300 / estimate for finance exp. ~ 45

IGLD’s estimate for 2006/07, excludes one time expenses relating to the merger

21

Balance sheet overview

* Including cash and cash equivalents of NIS 257.5 million attributable to the 012 acquisition.

Current assets* 353

Total assets 500

Current liabilities 92.2

Working capital 260.8

Total shareholders’ equity 170.9

in NIS millions

22

ComparablesInteresting market opportunity…

as of August 11, 2006 Q1 / Q2 2006

Company Internet Gold Sify Pacific Thestreet.com Sina.ComTicker IGLD Sify PCNTF TSCM SINAShare price $5.17 $7.43 $9.03 $9.64 $22.08

CommunicationsRevenues (M$) 17.9 26.5 27.9Operating Income (M$) 1.8 2.4 1.5Market cap (M$) N/A N/A 122.1 N/A N/Aprice to revenues multiple N/ A N/ A 1.1 N/ A N/ Aprice to EBIT multiple N/ A N/ A 20.7 N/ A N/ A

MediaRevenues (M$) 4.0 2.2 12.4 53.7Operating Income (M$) 0.8 0.1 2.8 7.6Market cap (M$) N/A N/A N/A 261.0 1,181.9price to revenues multiple N/ A N/ A N/ A 5.3 5.5price to EBIT multiple N/ A N/ A N/ A 23.7 38.7

TotalRevenues (M$) 21.9 28.7 27.9 12.4 53.7Operating Income (M$) 2.6 2.5 1.5 2.8 7.6Market cap (M$) 95.3 315.0 122.1 261.0 1,181.9price to revenues multiple 1.1 2.7 1.1 5.3 5.5price to EBIT multiple 9.3 31.5 20.7 23.7 38.7

23

24

Goal: to become Israel’s Leading Full

Suite Alternative Service Provider

Technology Value added services

VoB & business integration

VoWi-Fi / Wi-MAX

IP seamless mobility

IPTV

e-Commerce & paid content

International Long Distance (ILD) & Internet Access

Portals & e-Advertising

20091997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20081996

25

Strong Shareholders / Dedicated Management

Public ~ 31%

Eurocom Communications ~ 69% Focused, communications-oriented controlling parent group Leading Israeli private communications group representing

exclusively Nokia, Panasonic, GE and more Also holds equity in radio stations, DBS TV service provider,

satellite communications, cellular and more

Closely-knit, results-oriented management team Most all level of management grows from within Experienced upper level management

26

Investment highlights

Leading Communications Group

Today: controls 1/3 of its markets with a continuously growing market share

Tomorrow: entering new markets

Positioned to lead rapidly growing media markets

Owns over 18 portals & e-Commerce sites

High rate of market growth

Working from strong cash generating platform

All activities in both companies are major cash generators

Merger anticipated to save ~ NIS 50-60M in exp/inv

No difficulty in servicing loan (fin. exp. ~15% of Ebitda)

Proven management & ownership

Both company's management teams, working together with Eurocom (as controlling shareholder), have proven capable of carrying out aggressive growth / leadership strategies

Thank you!