“national strategy for financial education: thailand ... · “national strategy for financial...

TRANSCRIPT

“National Strategy for Financial Education: Thailand Experience ”

2014 IFIE-IOSCO Global Investor Education Conference

Washington, D.C., USA

Saovanee Suwannarong Director- Financial Literacy Department

Securities and Exchange Commission, Thailand

2

Outline

1. Thailand’s National Strategy 2. Do what we can do 2.1 Sector level 2.2 Organization level

3

Status of National Strategies Worldwide

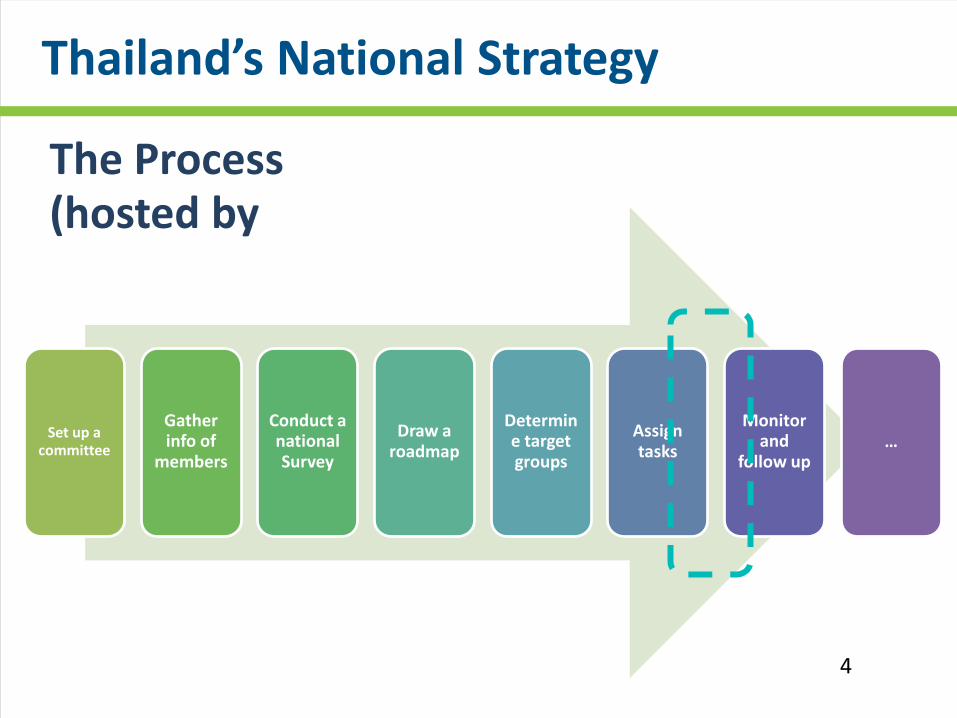

Thailand’s National Strategy

4

The Process (hosted by

Set up a committee

Gather info of

members

Conduct a national Survey

Draw a roadmap

Determine target groups

Assign tasks

Monitor and

follow up …

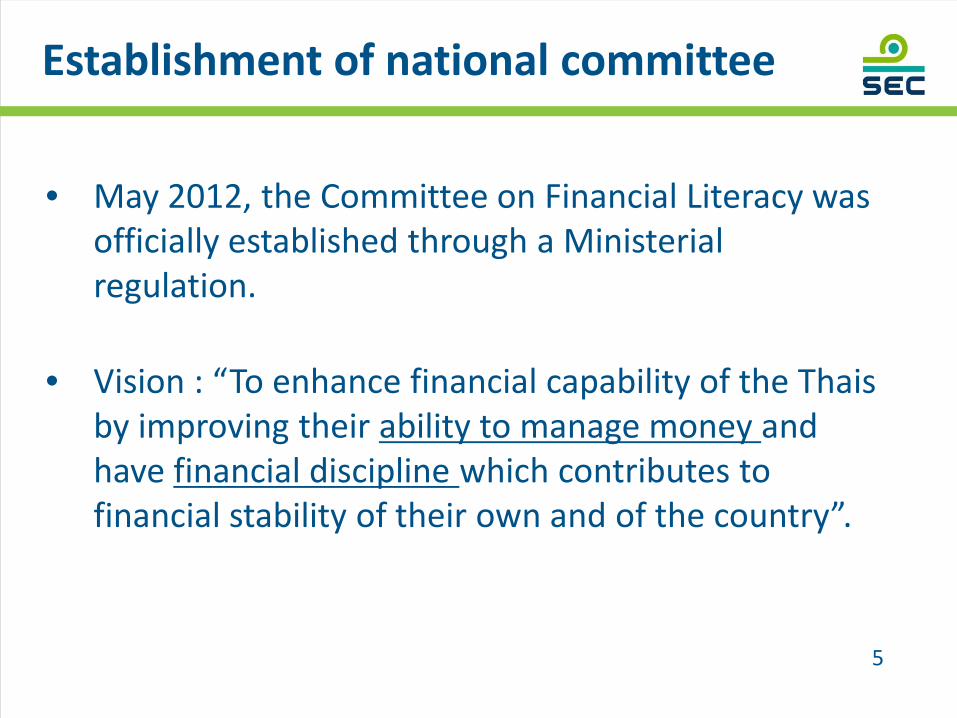

• May 2012, the Committee on Financial Literacy was officially established through a Ministerial regulation.

• Vision : “To enhance financial capability of the Thais by improving their ability to manage money and have financial discipline which contributes to financial stability of their own and of the country”.

5

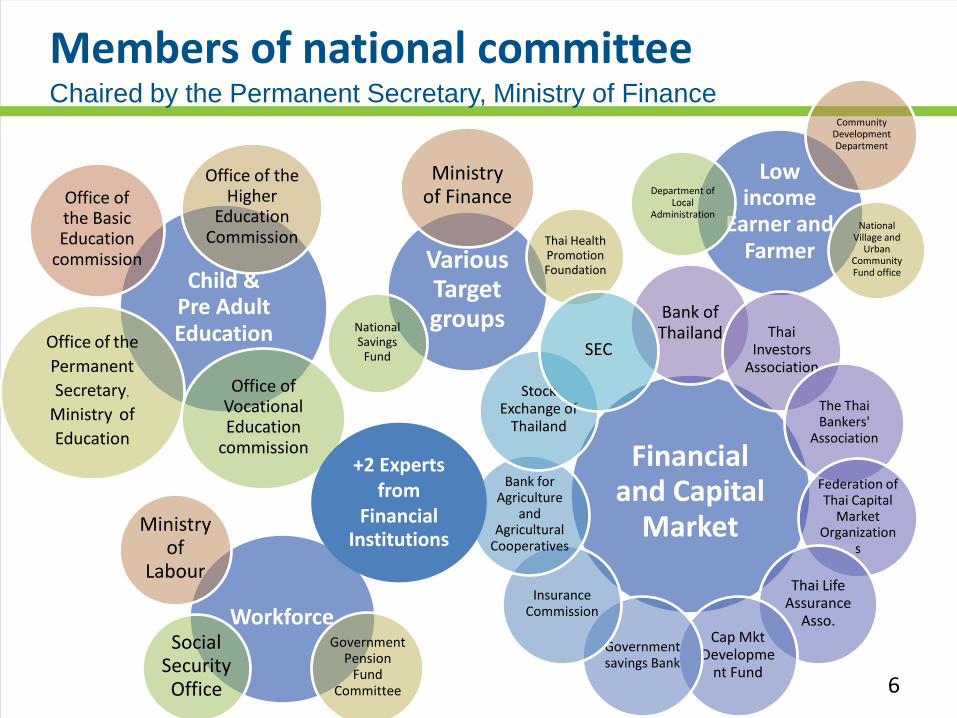

Establishment of national committee

6

Various Target groups

Ministry of Finance

Thai Health Promotion Foundation

National Savings

Fund

Child & Pre Adult Education

Office of the Basic Education

commission

Office of the Higher

Education Commission

Office of the

Permanent

Secretary,

Ministry of Education

Office of Vocational Education

commission

Low income

Earner and Farmer

Community Development Department

National Village and

Urban Community Fund office

Department of Local

Administration

Workforce

Ministry of

Labour

Government Pension

Fund Committee

Social Security Office

Financial and Capital

Market

Bank of Thailand Thai

Investors Association

The Thai Bankers'

Association

Federation of Thai Capital

Market Organization

s

Thai Life Assurance

Asso. Cap Mkt

Development Fund

Government savings Bank

Insurance Commission

Bank for Agriculture

and Agricultural

Cooperatives

Stock Exchange of

Thailand

SEC

+2 Experts from

Financial Institutions

Members of national committee Chaired by the Permanent Secretary, Ministry of Finance

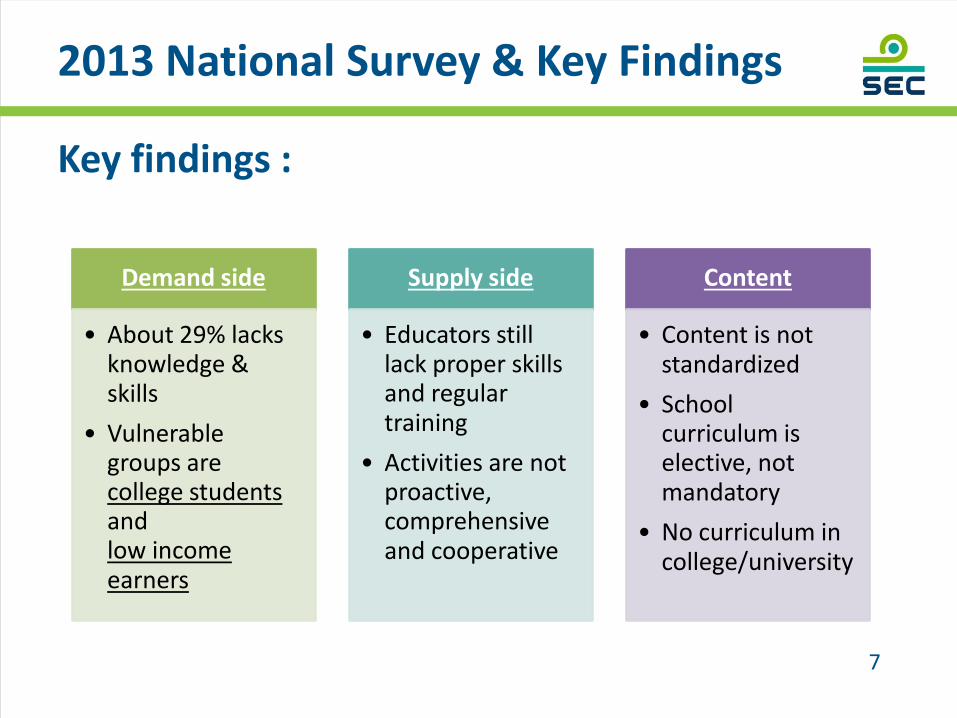

2013 National Survey & Key Findings

Key findings :

7

Demand side

• About 29% lacks knowledge & skills

• Vulnerable groups are college students and low income earners

Supply side

• Educators still lack proper skills and regular training

• Activities are not proactive, comprehensive and cooperative

Content

• Content is not standardized

• School curriculum is elective, not mandatory

• No curriculum in college/university

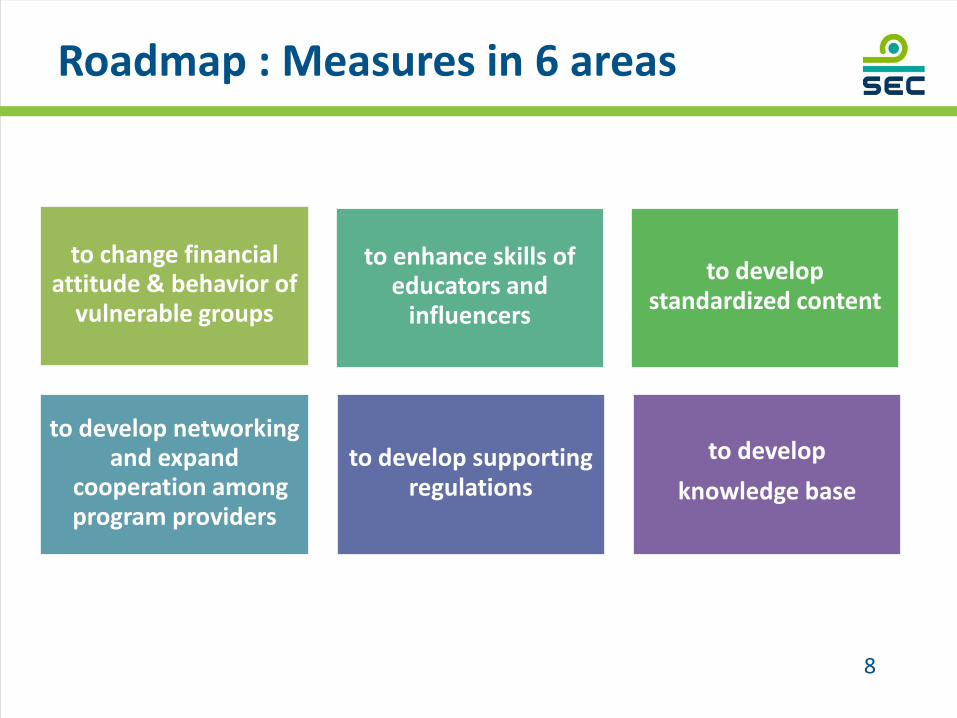

Roadmap : Measures in 6 areas

to change financial attitude & behavior of

vulnerable groups

to develop standardized content

to enhance skills of educators and

influencers

to develop networking and expand

cooperation among program providers

to develop supporting regulations

to develop knowledge base

8

9

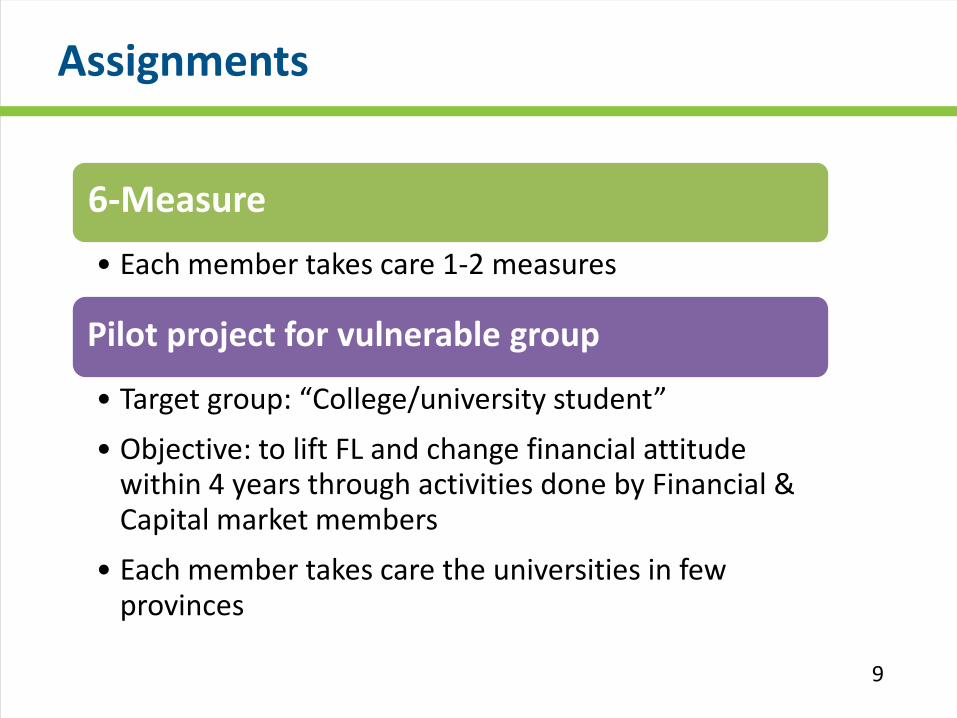

Assignments

6-Measure

• Each member takes care 1-2 measures

Pilot project for vulnerable group

• Target group: “College/university student”

• Objective: to lift FL and change financial attitude within 4 years through activities done by Financial & Capital market members

• Each member takes care the universities in few provinces

10

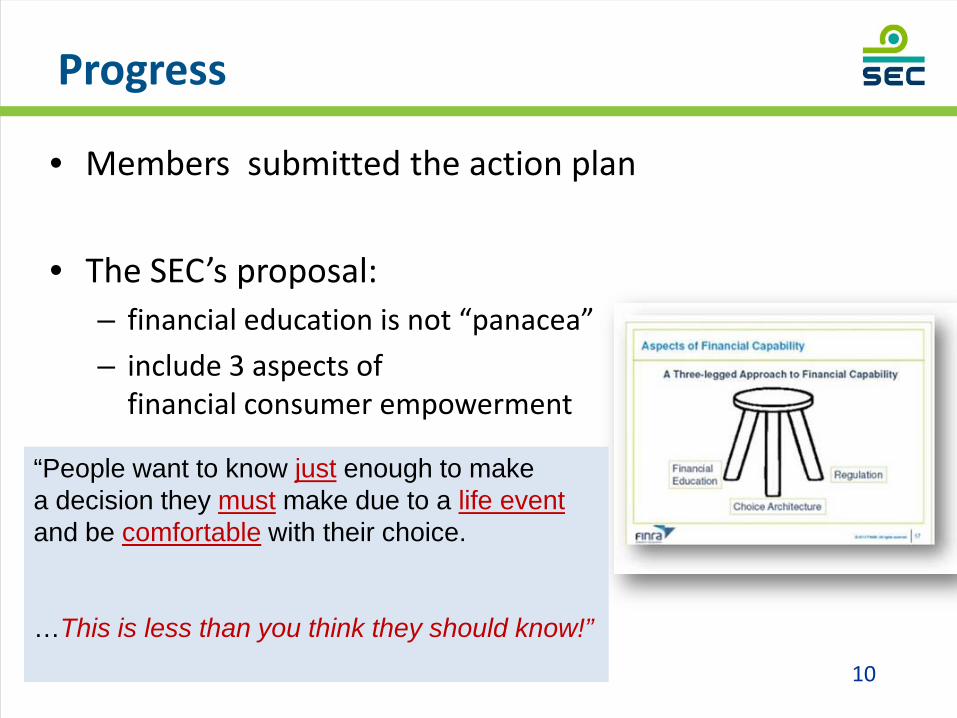

• Members submitted the action plan • The SEC’s proposal:

– financial education is not “panacea” – include 3 aspects of

financial consumer empowerment

Progress

“People want to know just enough to make a decision they must make due to a life event and be comfortable with their choice. …This is less than you think they should know!”

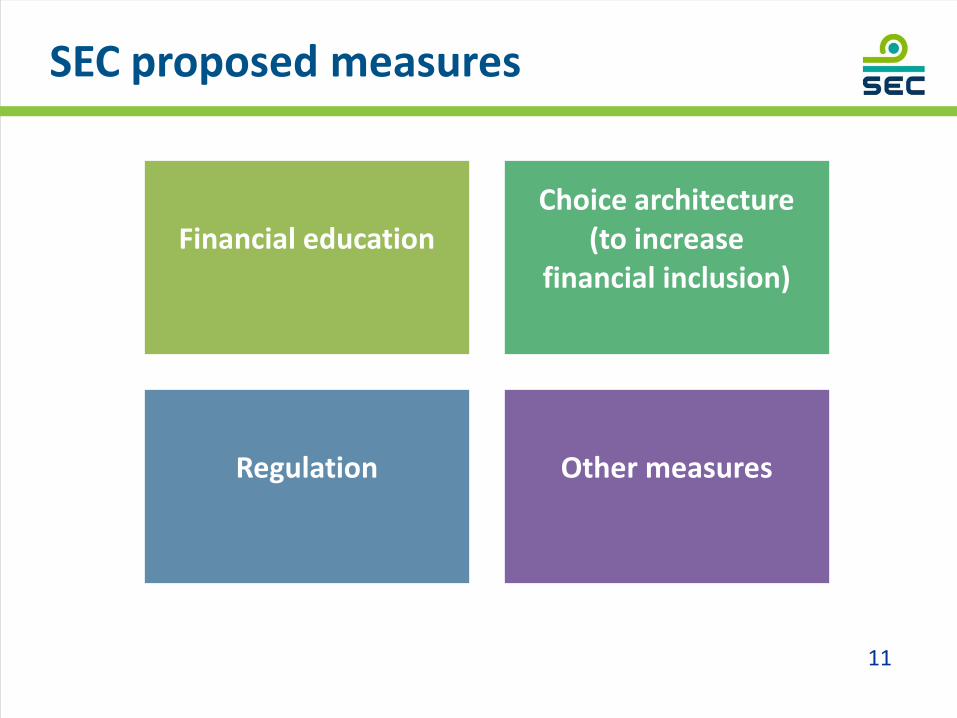

SEC proposed measures

11

Financial education

Choice architecture (to increase

financial inclusion)

Regulation

Other measures

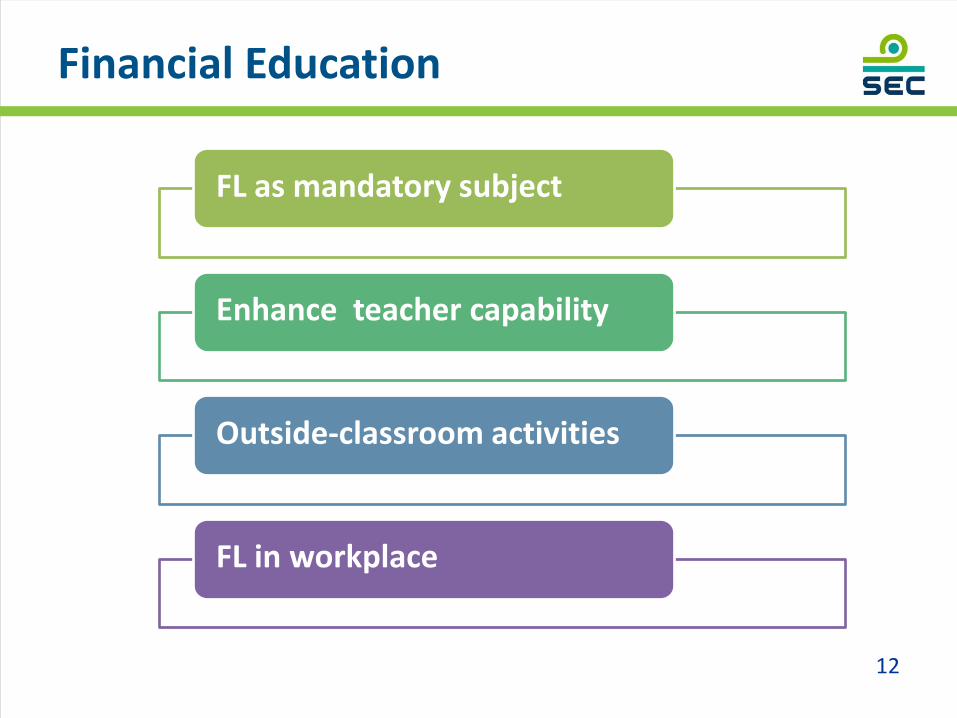

Financial Education

12

FL as mandatory subject

Enhance teacher capability

Outside-classroom activities

FL in workplace

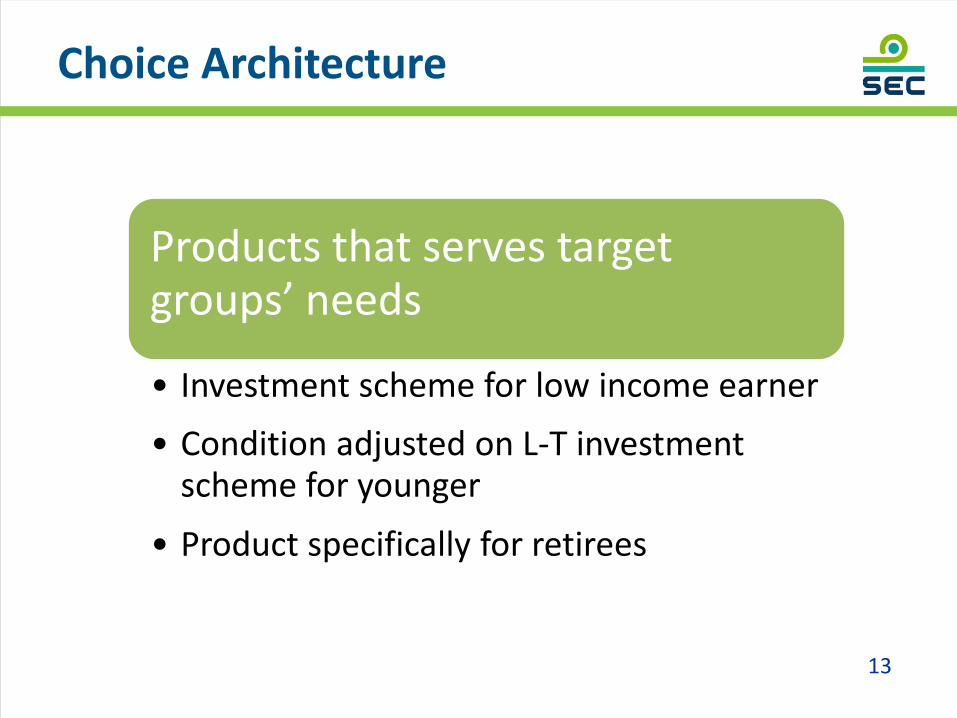

Choice Architecture

13

Products that serves target groups’ needs

• Investment scheme for low income earner

• Condition adjusted on L-T investment scheme for younger

• Product specifically for retirees

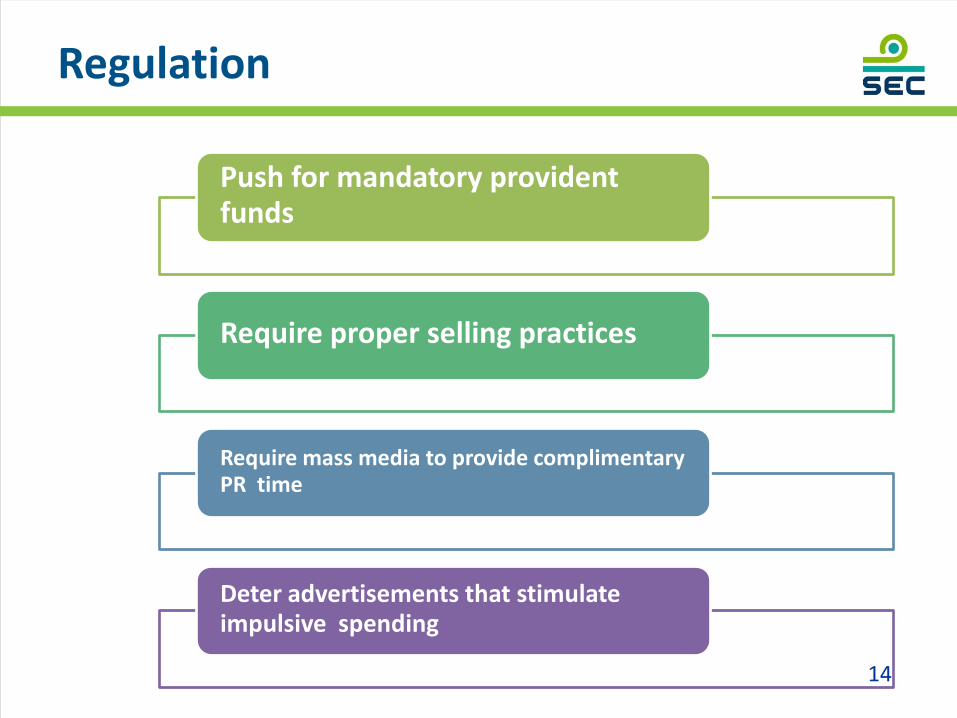

Regulation

Push for mandatory provident funds

Require proper selling practices

Require mass media to provide complimentary PR time

Deter advertisements that stimulate impulsive spending

14

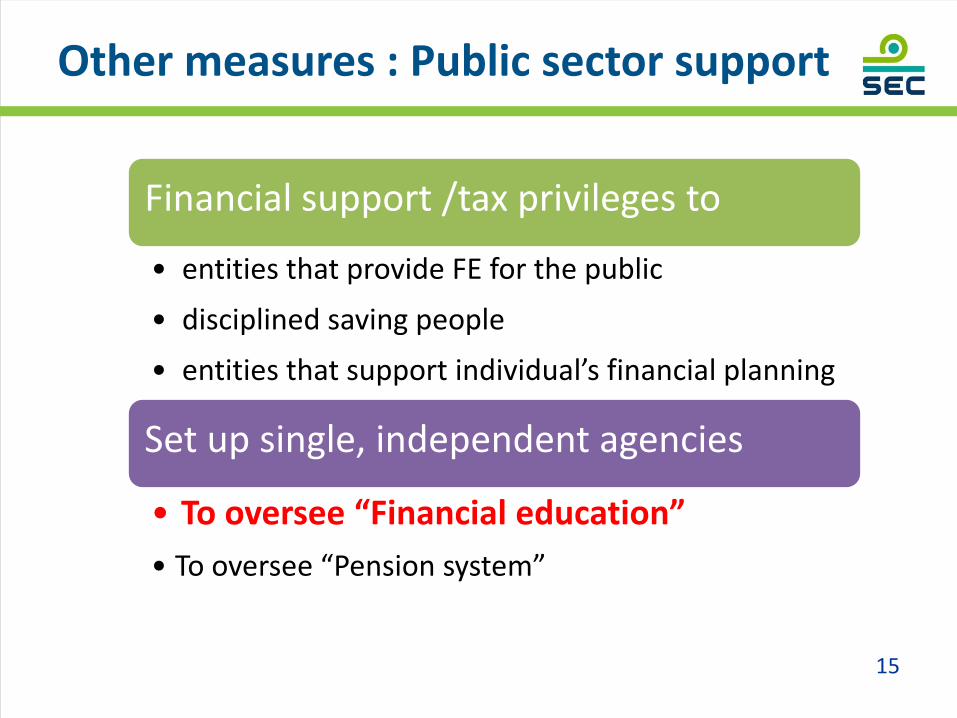

Other measures : Public sector support

15

Financial support /tax privileges to

• entities that provide FE for the public

• disciplined saving people

• entities that support individual’s financial planning

Set up single, independent agencies

• To oversee “Financial education”

• To oversee “Pension system”

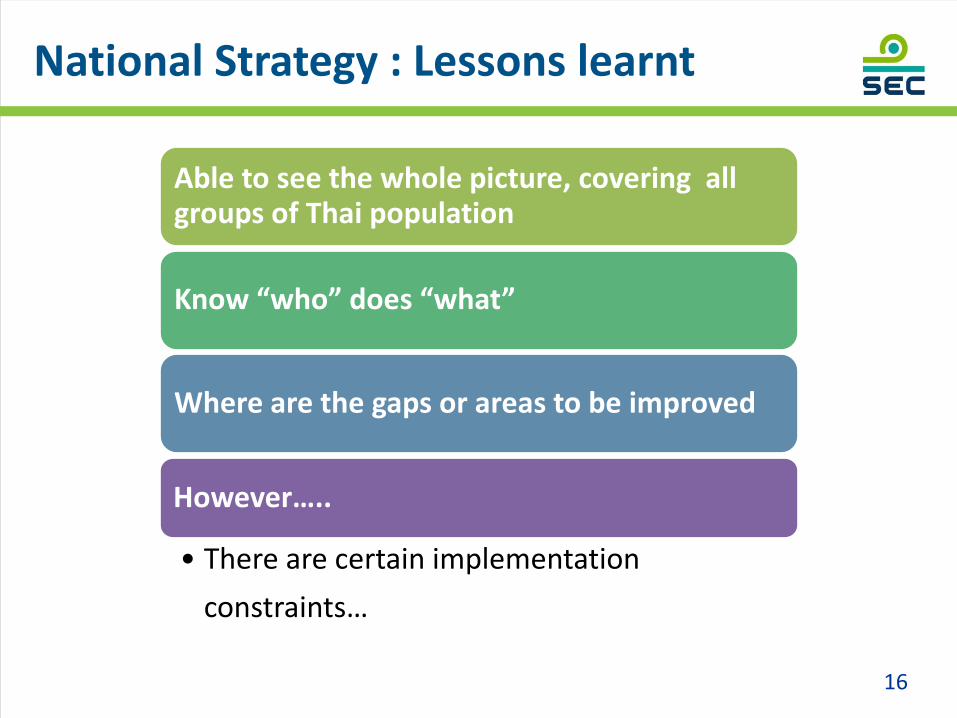

National Strategy : Lessons learnt

16

Able to see the whole picture, covering all groups of Thai population

Know “who” does “what”

Where are the gaps or areas to be improved

However…..

• There are certain implementation constraints…

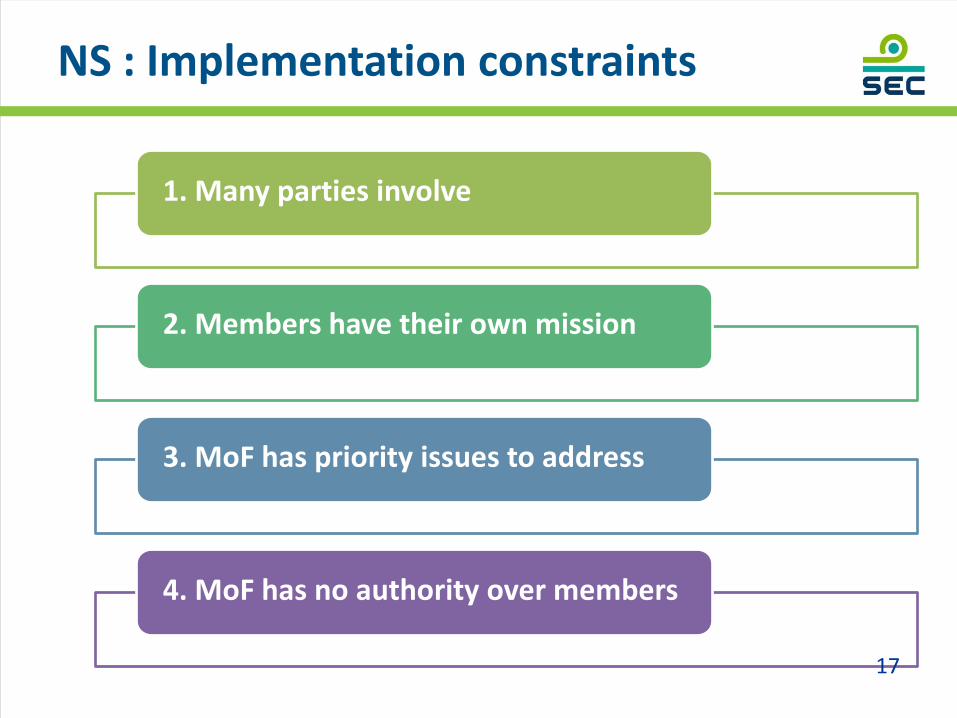

NS : Implementation constraints

1. Many parties involve

2. Members have their own mission

3. MoF has priority issues to address

4. MoF has no authority over members

17

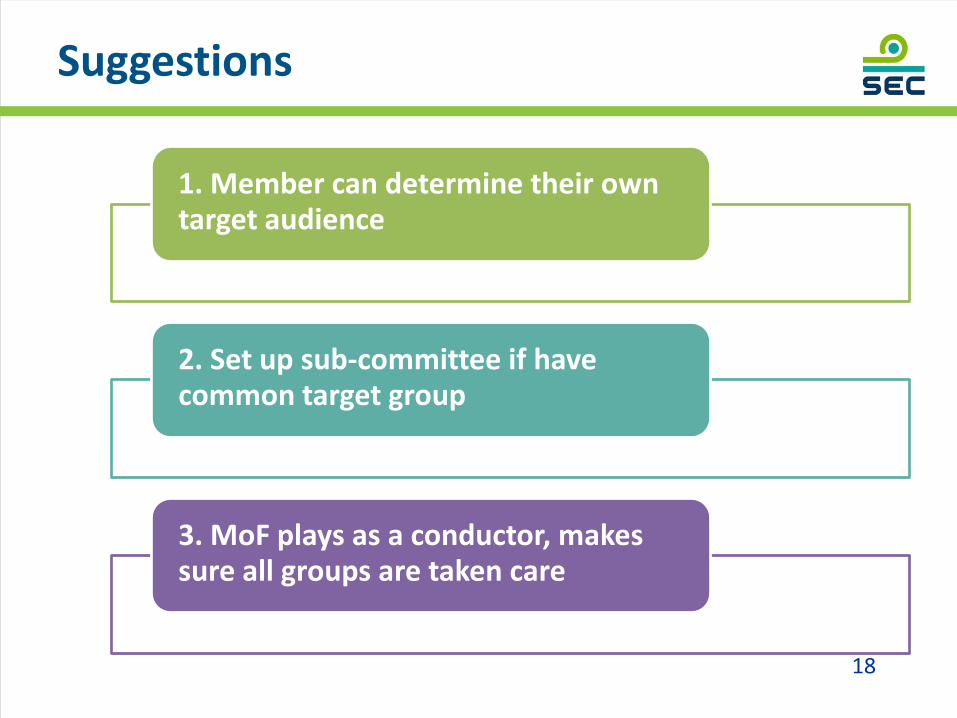

Suggestions

18

1. Member can determine their own target audience

2. Set up sub-committee if have common target group

3. MoF plays as a conductor, makes sure all groups are taken care

Example: Thailand Village Fund (TVF)

• Microcredit scheme for Their villagers. • TVF can efficiently collect savings and debt replacement on a

daily basis. • TVF has insights villager’s behavior and create money

collection method accordingly.

19

20

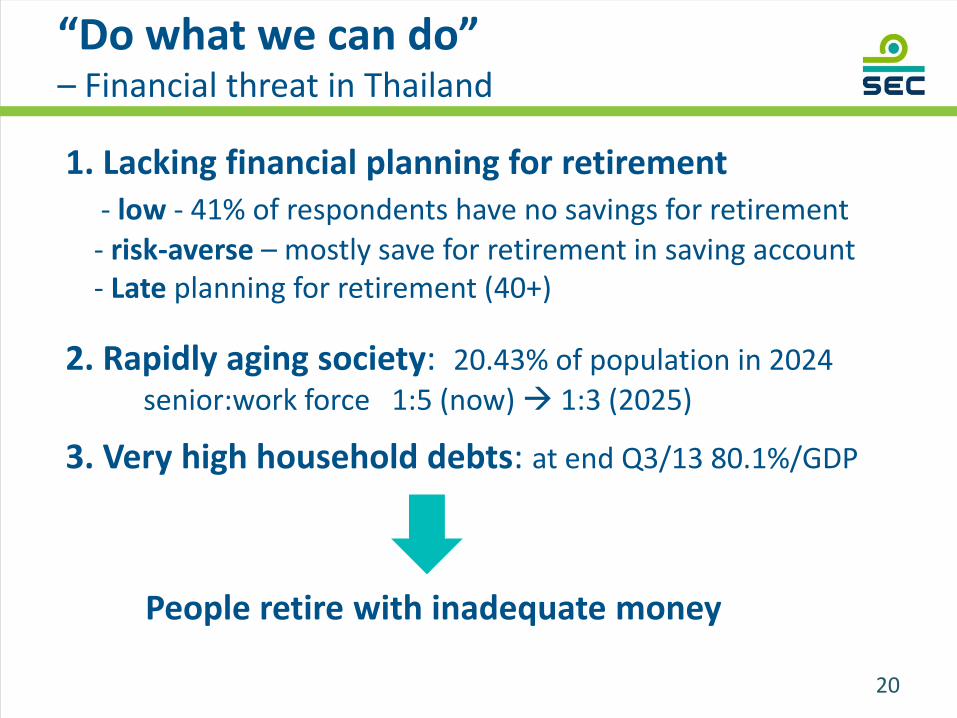

“Do what we can do” – Financial threat in Thailand

1. Lacking financial planning for retirement - low - 41% of respondents have no savings for retirement - risk-averse – mostly save for retirement in saving account - Late planning for retirement (40+)

2. Rapidly aging society: 20.43% of population in 2024 senior:work force 1:5 (now) 1:3 (2025)

3. Very high household debts: at end Q3/13 80.1%/GDP

People retire with inadequate money

21

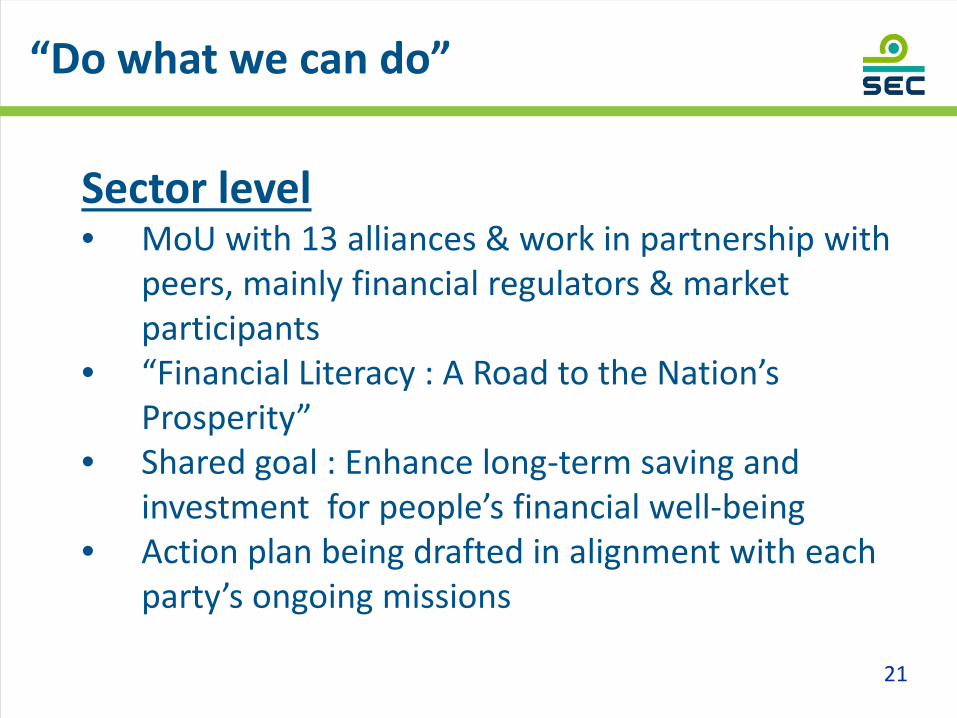

Sector level • MoU with 13 alliances & work in partnership with

peers, mainly financial regulators & market participants

• “Financial Literacy : A Road to the Nation’s Prosperity”

• Shared goal : Enhance long-term saving and investment for people’s financial well-being

• Action plan being drafted in alignment with each party’s ongoing missions

“Do what we can do”

22

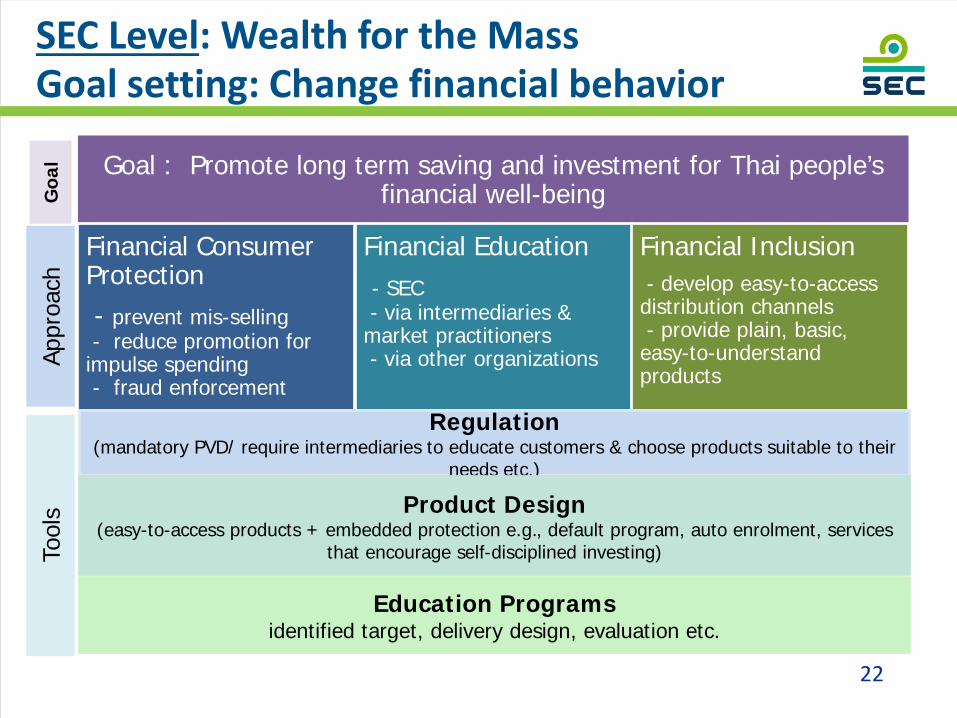

SEC Level: Wealth for the Mass Goal setting: Change financial behavior

Goal : Promote long term saving and investment for Thai people’s financial well-being

Financial Consumer Protection - prevent mis-selling - reduce promotion for impulse spending - fraud enforcement

Financial Education - SEC - via intermediaries & market practitioners - via other organizations

Financial Inclusion - develop easy-to-access distribution channels - provide plain, basic, easy-to-understand products

Regulation (mandatory PVD/ require intermediaries to educate customers & choose products suitable to their

needs etc.)

Product Design (easy-to-access products + embedded protection e.g., default program, auto enrolment, services

that encourage self-disciplined investing)

Education Programs identified target, delivery design, evaluation etc.

Goa

l Ap

proa

ch

Tool

s

23

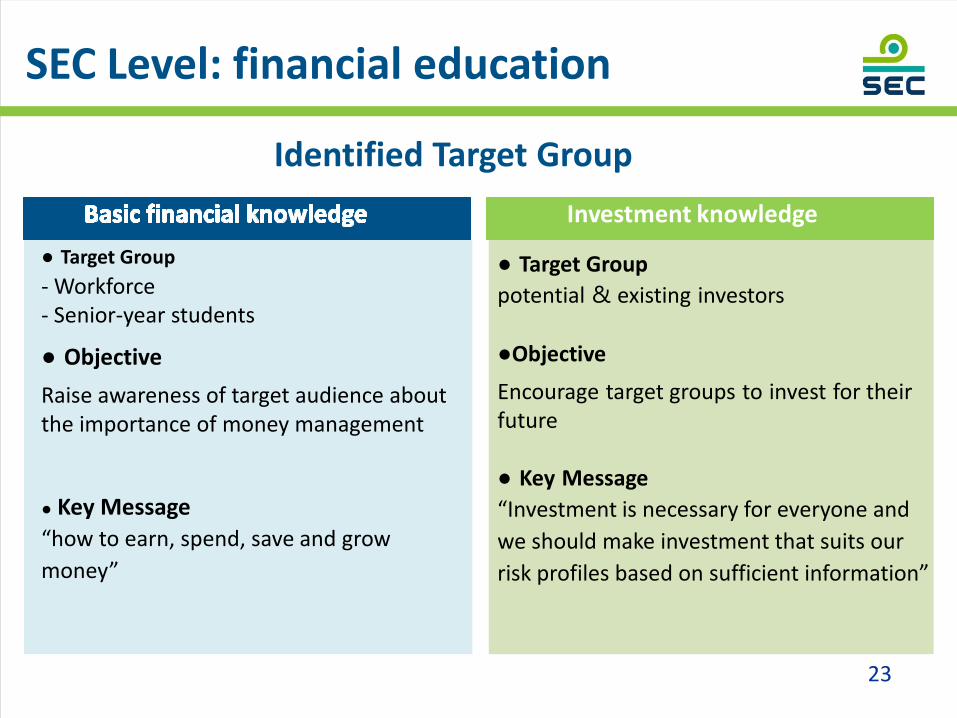

SEC Level: financial education

● Target Group potential & existing investors

●Objective

Encourage target groups to invest for their future ● Key Message “Investment is necessary for everyone and we should make investment that suits our risk profiles based on sufficient information”

Investment knowledge ● Target Group - Workforce - Senior-year students

● Objective Raise awareness of target audience about the importance of money management

● Key Message “how to earn, spend, save and grow money”

Identified Target Group

24

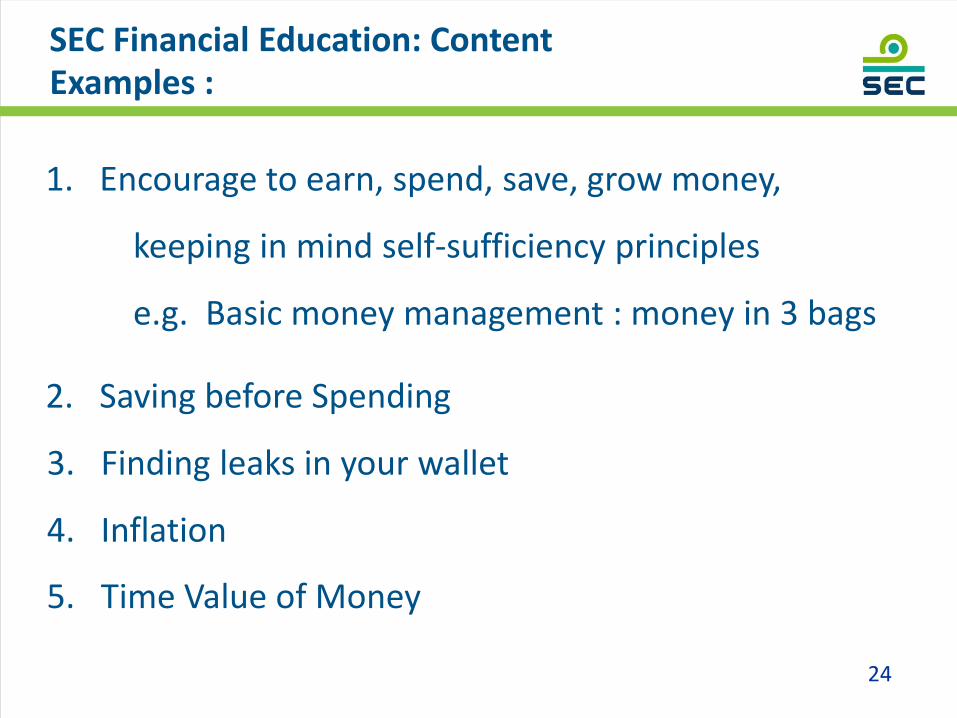

SEC Financial Education: Content Examples :

1. Encourage to earn, spend, save, grow money,

keeping in mind self-sufficiency principles

e.g. Basic money management : money in 3 bags

2. Saving before Spending

3. Finding leaks in your wallet

4. Inflation

5. Time Value of Money

25

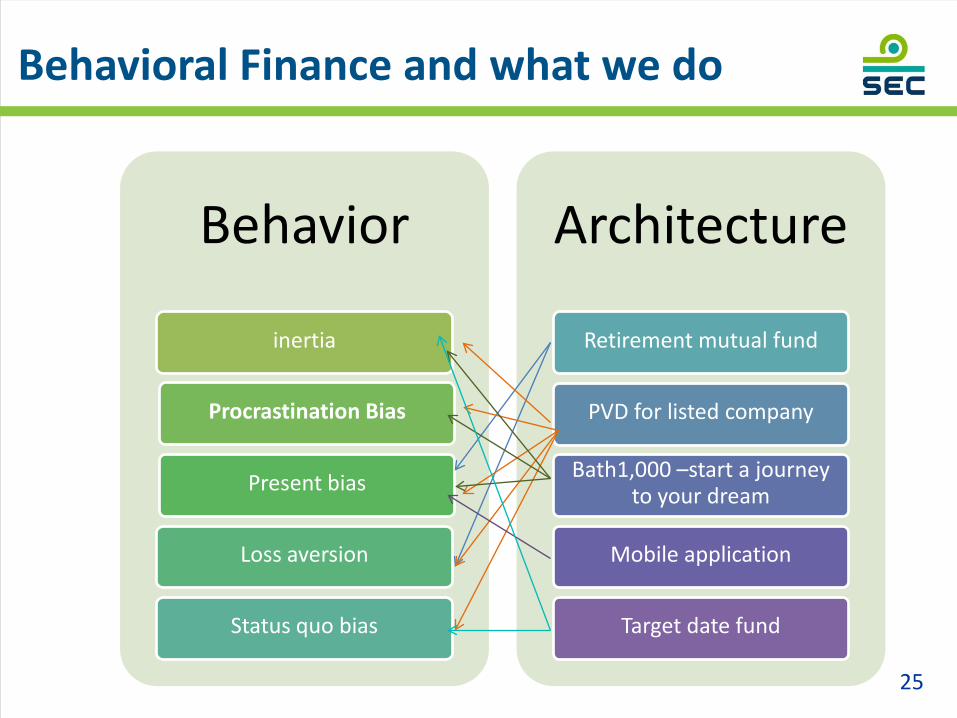

Behavioral Finance and what we do

Behavior

inertia

Procrastination Bias

Present bias

Loss aversion

Status quo bias

Architecture

Retirement mutual fund

PVD for listed company

Bath1,000 –start a journey to your dream

Mobile application

Target date fund

26

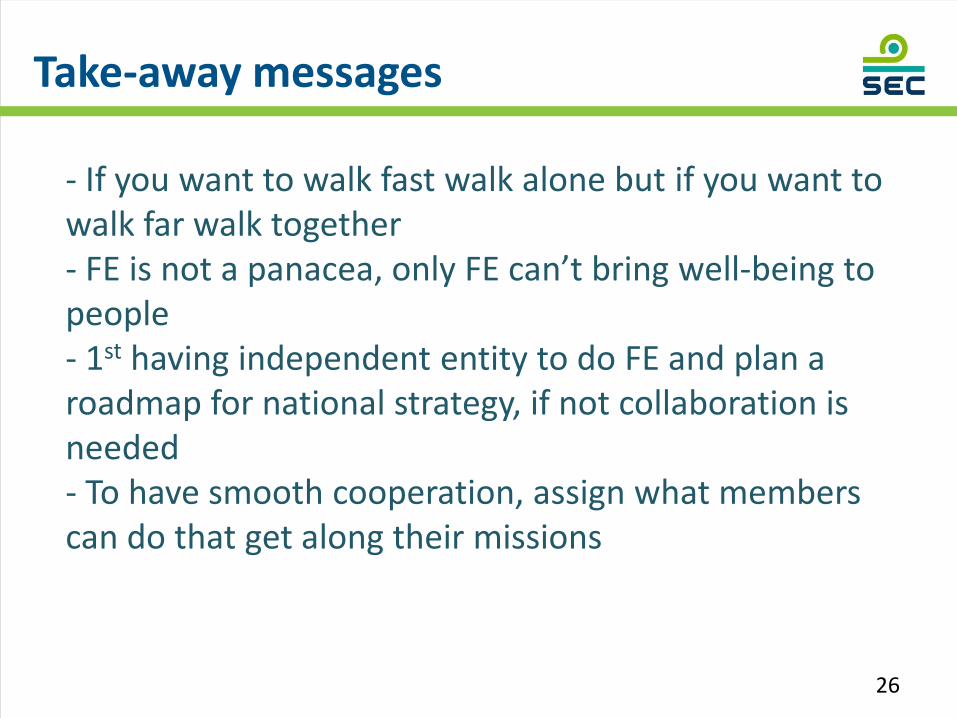

Take-away messages

- If you want to walk fast walk alone but if you want to walk far walk together - FE is not a panacea, only FE can’t bring well-being to people - 1st having independent entity to do FE and plan a roadmap for national strategy, if not collaboration is needed - To have smooth cooperation, assign what members can do that get along their missions