neetika kampani & joachim tan - aemo - aemos's gas statement of opportunities (gsoo) for...

TRANSCRIPT

SLIDE 1

AEMO’S GAS STATEMENT OF

OPPORTUNITIES (GSOO) FOR

AUSTRALIA

2016 WA Power and Gas Conference

15 March 2016

PRESENTED BY

NEETIKA KAPANI, A/MANAGER, SYSTEM CAPACITY (WA)

JOACHIM TAN, SENIOR ANALYST, SYSTEM CAPACITY (WA)

SLIDE 2

AGENDA

• An overview of Australia’s domestic gas markets

• Findings of the November 2015 Western Australia

GSOO

• Findings of the March 2016 GSOO (Eastern and South-

Eastern States)

• Future of gas supply in Australia

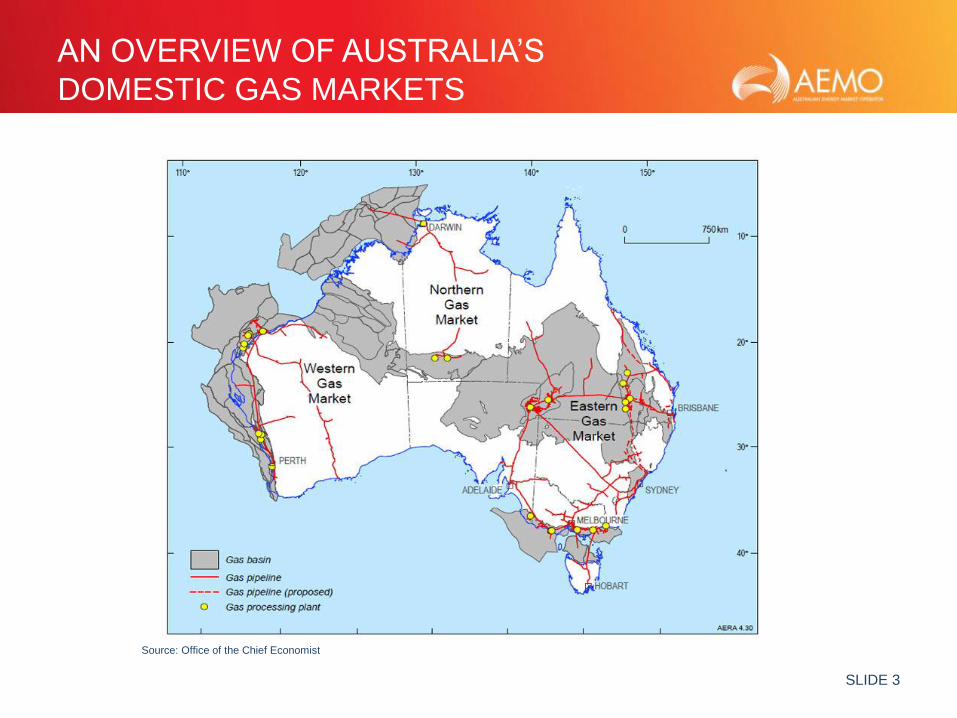

SLIDE 3

AN OVERVIEW OF AUSTRALIA’S

DOMESTIC GAS MARKETS

Source: Office of the Chief Economist

SLIDE 4

AN OVERVIEW OF AUSTRALIA’S

DOMESTIC GAS MARKETS

Source: APPEA

SLIDE 5

FINDINGS OF THE NOVEMBER 2015

WESTERN AUSTRALIA GSOO

SLIDE 6

FINDINGS OF THE NOVEMBER 2015

WESTERN AUSTRALIA GSOO

• Western domestic gas demand forecast to grow slowly

• Western domestic gas market is well supplied

• Adequate gas reserves

• More opportunities for gas consumers

SLIDE 8

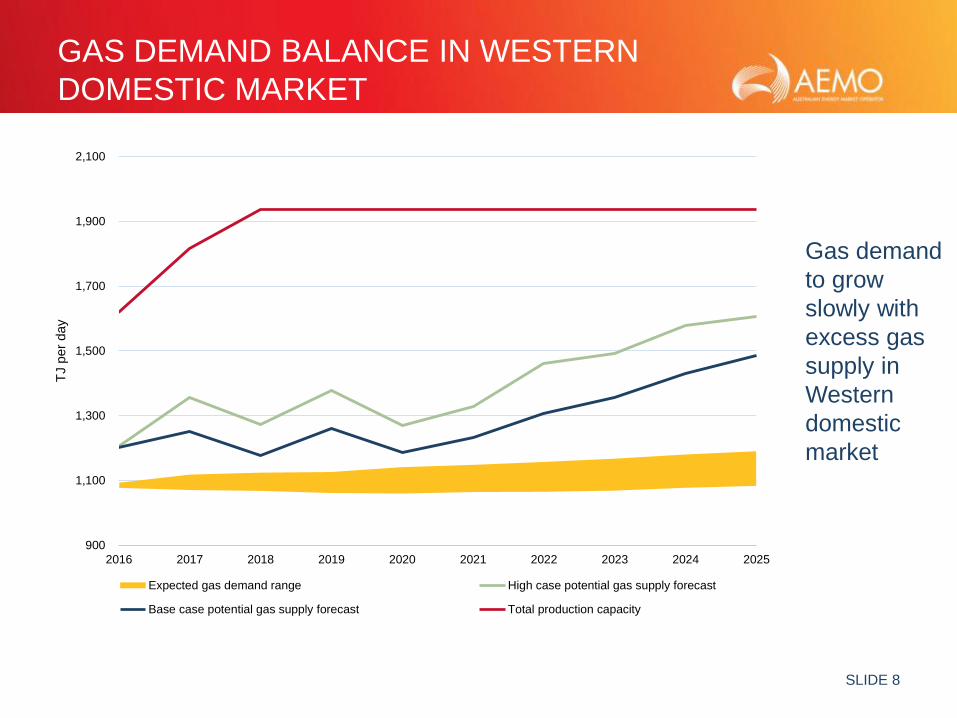

GAS DEMAND BALANCE IN WESTERN

DOMESTIC MARKET

900

1,100

1,300

1,500

1,700

1,900

2,100

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

TJ p

er

day

Expected gas demand range High case potential gas supply forecast

Base case potential gas supply forecast Total production capacity

Gas demand

to grow

slowly with

excess gas

supply in

Western

domestic

market

SLIDE 9

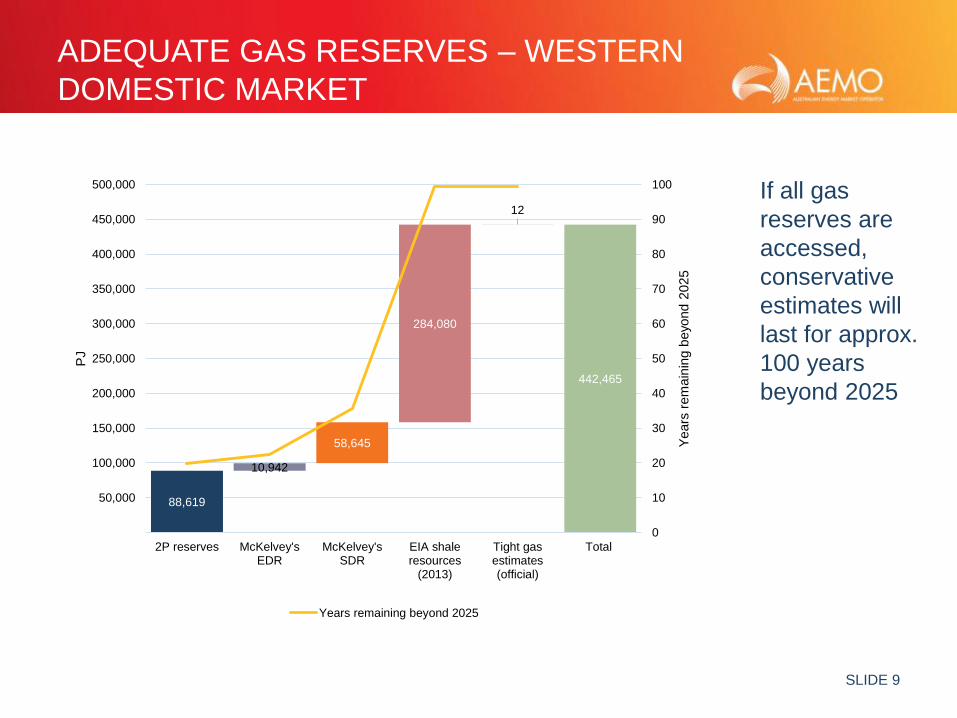

ADEQUATE GAS RESERVES – WESTERN

DOMESTIC MARKET

442,465

10,942

58,645

284,080

12

88,619

0

10

20

30

40

50

60

70

80

90

100

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2P reserves McKelvey'sEDR

McKelvey'sSDR

EIA shaleresources

(2013)

Tight gasestimates(official)

Total

Years

rem

ain

ing b

eyond 2

025

PJ

Years remaining beyond 2025

If all gas

reserves are

accessed,

conservative

estimates will

last for approx.

100 years

beyond 2025

SLIDE 10

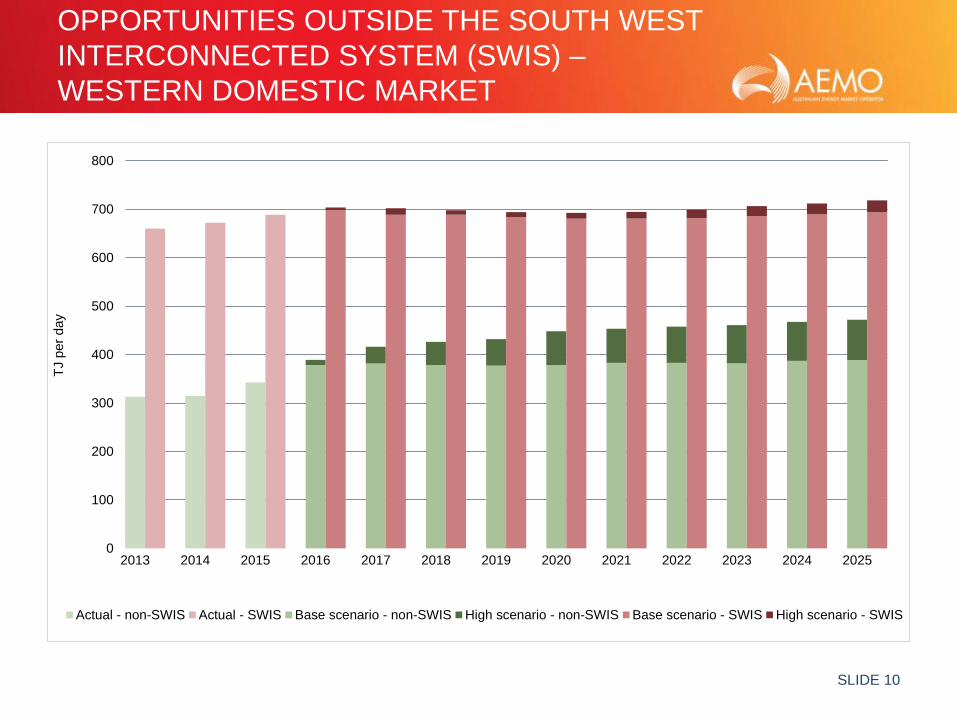

OPPORTUNITIES OUTSIDE THE SOUTH WEST

INTERCONNECTED SYSTEM (SWIS) –

WESTERN DOMESTIC MARKET

0

100

200

300

400

500

600

700

800

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

TJ p

er

day

Actual - non-SWIS Actual - SWIS Base scenario - non-SWIS High scenario - non-SWIS Base scenario - SWIS High scenario - SWIS

SLIDE 11

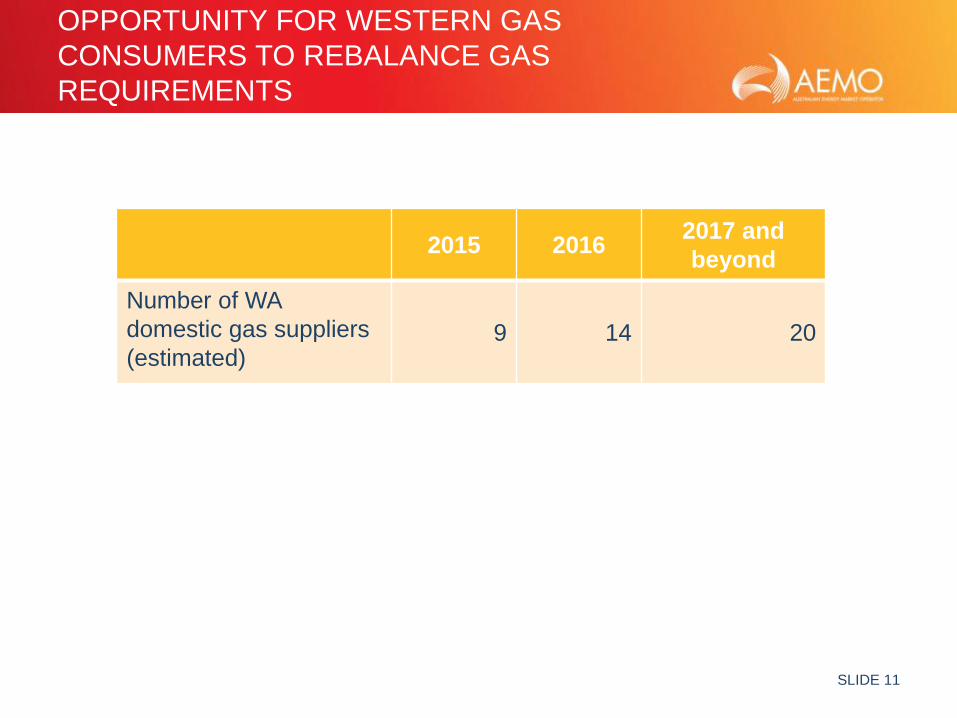

OPPORTUNITY FOR WESTERN GAS

CONSUMERS TO REBALANCE GAS

REQUIREMENTS

2015 20162017 and

beyond

Number of WA

domestic gas suppliers

(estimated)9 14 20

SLIDE 12

OPPORTUNITES TO SHIP GAS

THROUGHOUT WESTERN MARKET

SLIDE 13

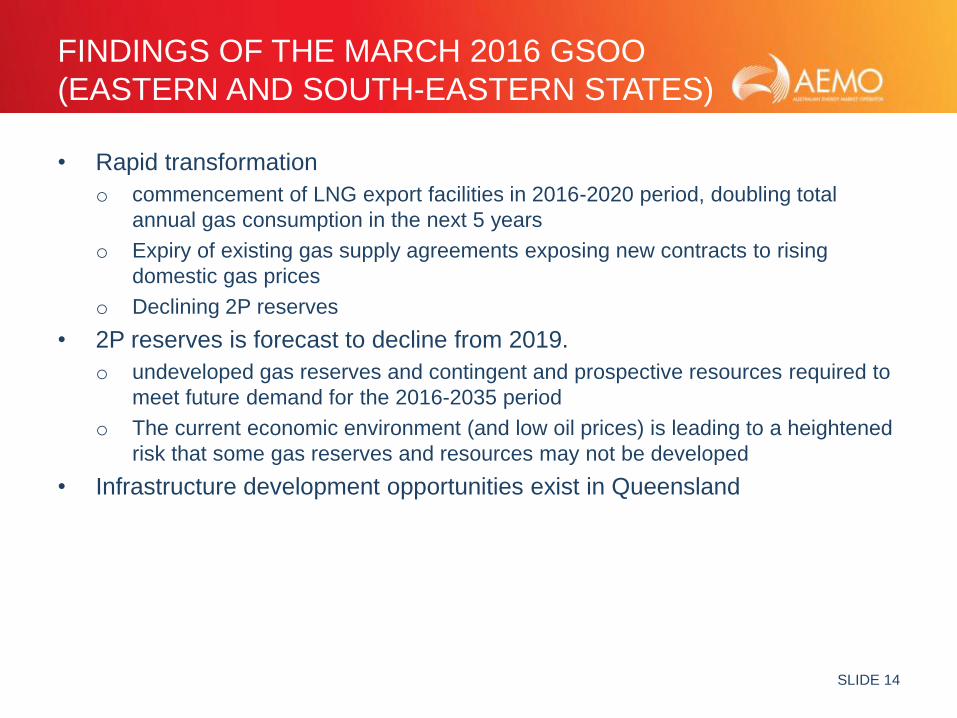

FINDINGS OF THE MARCH 2016 GSOO

(EASTERN AND SOUTH-EASTERN STATES)

SLIDE 14

FINDINGS OF THE MARCH 2016 GSOO

(EASTERN AND SOUTH-EASTERN STATES)

• Rapid transformation

o commencement of LNG export facilities in 2016-2020 period, doubling total

annual gas consumption in the next 5 years

o Expiry of existing gas supply agreements exposing new contracts to rising

domestic gas prices

o Declining 2P reserves

• 2P reserves is forecast to decline from 2019.

o undeveloped gas reserves and contingent and prospective resources required to

meet future demand for the 2016-2035 period

o The current economic environment (and low oil prices) is leading to a heightened

risk that some gas reserves and resources may not be developed

• Infrastructure development opportunities exist in Queensland

SLIDE 15

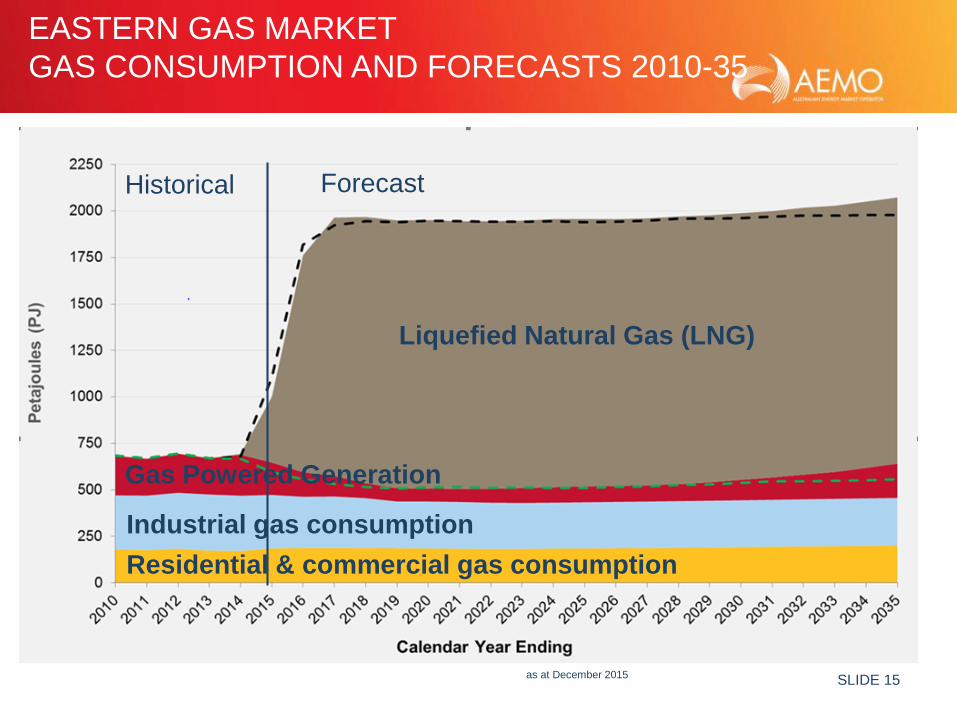

EASTERN GAS MARKET

GAS CONSUMPTION AND FORECASTS 2010-35

Liquefied Natural Gas (LNG)

Gas Powered Generation

Industrial gas consumption

Residential & commercial gas consumption

as at December 2015

Historical Forecast

SLIDE 16

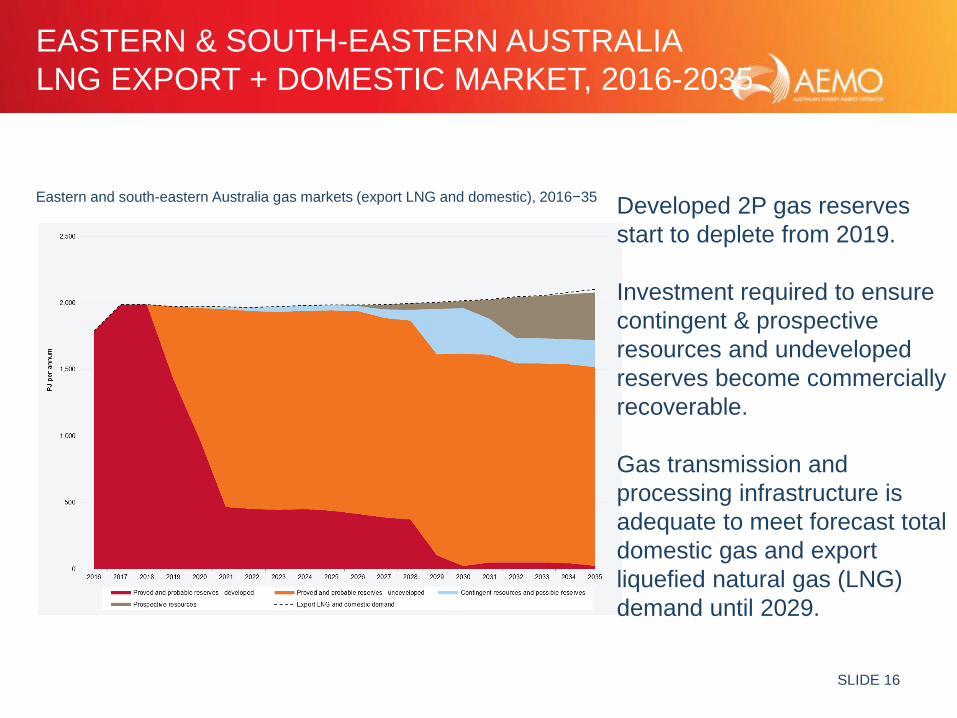

EASTERN & SOUTH-EASTERN AUSTRALIA

LNG EXPORT + DOMESTIC MARKET, 2016-2035

Eastern and south-eastern Australia gas markets (export LNG and domestic), 2016−35Developed 2P gas reserves

start to deplete from 2019.

Investment required to ensure

contingent & prospective

resources and undeveloped

reserves become commercially

recoverable.

Gas transmission and

processing infrastructure is

adequate to meet forecast total

domestic gas and export

liquefied natural gas (LNG)

demand until 2029.

SLIDE 17

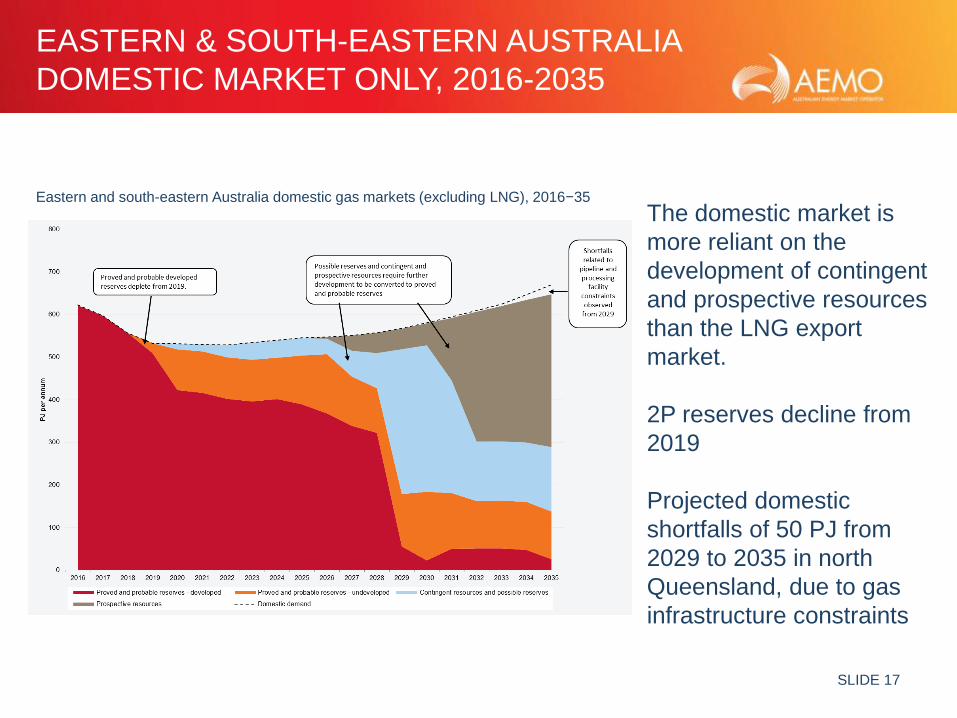

EASTERN & SOUTH-EASTERN AUSTRALIA

DOMESTIC MARKET ONLY, 2016-2035

Eastern and south-eastern Australia domestic gas markets (excluding LNG), 2016−35

The domestic market is

more reliant on the

development of contingent

and prospective resources

than the LNG export

market.

2P reserves decline from

2019

Projected domestic

shortfalls of 50 PJ from

2029 to 2035 in north

Queensland, due to gas

infrastructure constraints

SLIDE 18

THE FUTURE OF GAS SUPPLY IN AUSTRALIA

SLIDE 19

NEW OPPORTUNITIES

• The transformation of Australia’s domestic gas landscape presents new opportunities and requires further transparency:

o Near to medium-term (next 10 years) Western market

excess gas supply allows existing gas consumers to rebalance their gas requirements

existing and future projects (in non-SWIS areas) may consider of fuel switching and the potential development of a larger chemicals industry

Eastern market shortage of gas reserves increases gas supply opportunities as GPG consumption is

projected to increase in the 2020-2025 period

New Northern gas pipeline will bring greater security of domestic supply

sustained higher gas prices increases the prospects of new exploration and the development of new gas supply from the Northern and Eastern markets

o Longer-term (beyond 10 years) More efficient use of gas resources

The impact of Paris COP 21 2015

Australia’s gas resources remains vital in lowering our carbon intensity for the continual expansion of the gas industry

SLIDE 20

GAS BULLETIN BOARD – WESTERN

MARKET

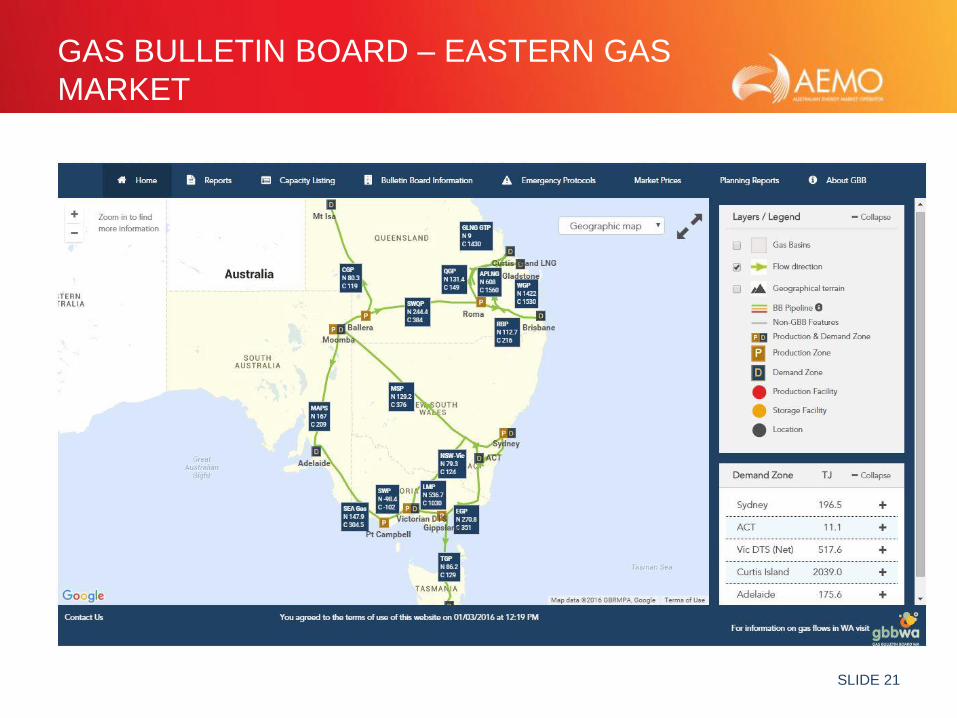

SLIDE 21

GAS BULLETIN BOARD – EASTERN GAS

MARKET

SLIDE 22

THANK YOU