net present value and capital budgeting what to discount - arts

TRANSCRIPT

Net Present Value and Capital Budgeting

(Text reference: Chapter 7)Topics

what to discountthe CCA systemtotal project cash flow vs. tax shield approachdetailed CCA calculations and examplesproject interactions

AFM 271 - NPV and Capital Budgeting Slide 1

What to Discount

some general principles:1. Only cash flow is relevant

the NPV rule is stated in terms of cash flowscash flow is a simple idea: dollars in - dollars outdon’t confuse cash flow with accounting income(note that accounting income is needed in somecases to calculate taxes)

2. Always estimate cash flows on an incremental basisincremental cash flows are the additional cashflows generated by the project. To identify them,ask two questions:

What is the cash flow if the project is taken?What is the cash flow if the project is not taken?

If the answers differ, then the cash flow isincremental.

AFM 271 - NPV and Capital Budgeting Slide 2

Cont’d

some things to watch for:exclude sunk costs: it is incorrect to include costswhich have already been incurred and cannot berecoveredinclude opportunity costs: e.g. a firm owns some landworth $25 million which it is considering using as anew factory site. If the firm builds the factory, it isgiving up the $25 million it could have received byselling the land.incorporate side effects: it is important to ensure thatall effects on the remainder of a firm’s operations aretaken into account (e.g. a new product line may reducesales of existing products)

AFM 271 - NPV and Capital Budgeting Slide 3

Cont’d

include working capital requirements: most projectswill require an additional investment in working capital(e.g. due to increased inventories, accountsreceivable, etc.); such investments are typicallyrecovered later onallocated overhead costs: ensure that only thosecharges which are actually due to a project areallocated to itinterest expense: ignore this for now

AFM 271 - NPV and Capital Budgeting Slide 4

Cont’d

3. Treat inflation consistentlynotation: nominal interest rate i

inflation rate πreal interest rate r

recall the “Fisher relation”

1+ i = (1+ r)× (1+π)⇒ r =1+ i1+π

−1

example: if i = 10% and π = 3.5%, what is the FVafter 2 years of $10,000 in real and nominalterms? (assume the money is invested at i = 10%)

AFM 271 - NPV and Capital Budgeting Slide 5

Cont’d

consistency requires that nominal cash flows bediscounted at a nominal discount rate and realcash flows be discounted at a real discount rate.For example, suppose that i = 8% and π = 3% andthat we have the following real cash flows:

C0 C1 C2-1000 750 900

NPV in real terms:

NPV in nominal terms:

AFM 271 - NPV and Capital Budgeting Slide 6

Cont’d

why does this work? Let C0,C1,C2, . . . be real cash flows,so:

PVnominal = C0 +C1(1+π)

1+ i +C2(1+π)2

(1+ i)2 + . . .

= C0 +C1(1+π)

(1+ r)(1+π)+

C2(1+π)2

(1+ r)2(1+π)2 + . . .

it is important to understand how to use both real andnominal discounting since you sometimes have to useboth approaches. This is because some cash flowforecasts (e.g. sales revenue) are often made in realterms, whereas others (e.g. depreciation tax shields) arecalculated in nominal terms.

AFM 271 - NPV and Capital Budgeting Slide 7

Cont’d

for a single cash flow received at period n:

Cnominal = Creal × (1+π)n

for a series of cash flows, the growth rate must also bechanged (e.g. a perpetuity which is constant in nominalterms is actually decreasing in real terms due to inflation).The relationship between real and nominal growth rates is:

(1+gnominal) = (1+greal)× (1+π)

e.g. a perpetuity of $1,000 per year (nominal), with r = 10%and π = 3%:

AFM 271 - NPV and Capital Budgeting Slide 8

Cont’dsome examples (assume i = 10% and π = 5%):1. perpetuity Cnominal = $100, 1st payment at t = 1, gnominal = 2%

2. perpetuity Cnominal = $100, 1st payment at t = 4, greal = 2%

3. 10 period annuity Creal = $500, 1st payment at t = 1, greal = 4%

AFM 271 - NPV and Capital Budgeting Slide 9

The CCA System

depreciation or capital cost allowance (CCA) is not a cash flow,but it has cash flow consequences because it is deductiblefrom taxable income

since CCA reduces taxable income, it increases cash flowassets such as land or securities cannot be depreciated.Others are assigned to various classes, with varyingdepreciation rates. Table 7A.1 (text p. 219) provides somecommon classes: e.g. manufacturing and processingequipment is in Class 8 with a 20% rate, brick buildings arein Class 1 with a 4% rate. The depreciation rate d reflectsthe economic life of the asset.

note that all assets of a firm within a particular class are treatedas if they are a single asset (a “pool”)

AFM 271 - NPV and Capital Budgeting Slide 10

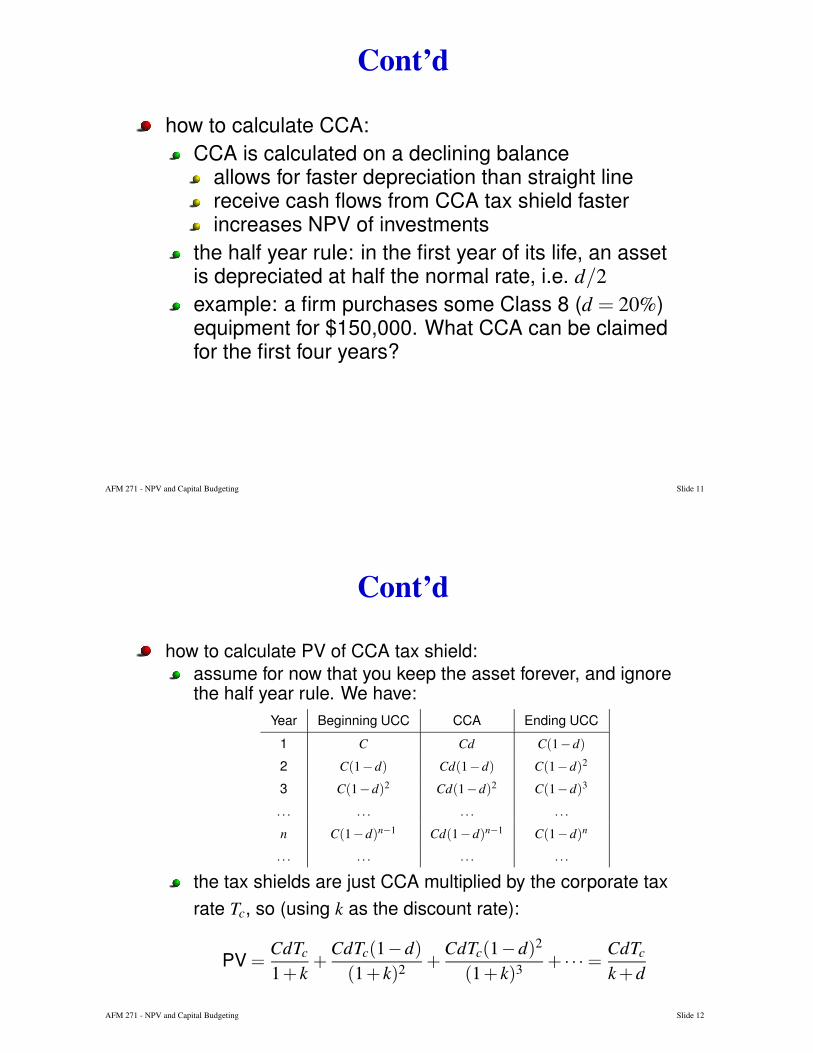

Cont’d

how to calculate CCA:CCA is calculated on a declining balance

allows for faster depreciation than straight linereceive cash flows from CCA tax shield fasterincreases NPV of investments

the half year rule: in the first year of its life, an assetis depreciated at half the normal rate, i.e. d/2example: a firm purchases some Class 8 (d = 20%)equipment for $150,000. What CCA can be claimedfor the first four years?

AFM 271 - NPV and Capital Budgeting Slide 11

Cont’d

how to calculate PV of CCA tax shield:assume for now that you keep the asset forever, and ignorethe half year rule. We have:

Year Beginning UCC CCA Ending UCC1 C Cd C(1−d)

2 C(1−d) Cd(1−d) C(1−d)2

3 C(1−d)2 Cd(1−d)2 C(1−d)3

. . . . . . . . . . . .

n C(1−d)n−1 Cd(1−d)n−1 C(1−d)n

. . . . . . . . . . . .

the tax shields are just CCA multiplied by the corporate taxrate Tc, so (using k as the discount rate):

PV =CdTc1+ k +

CdTc(1−d)

(1+ k)2 +CdTc(1−d)2

(1+ k)3 + · · · =CdTck +d

AFM 271 - NPV and Capital Budgeting Slide 12

Cont’d

now incorporate the half year rule. We have twoperpetuities, decreasing at rate d, one with firstpayment after one year, the other after two years:

PV =12CdTck +d +

12CdTck +d ×

11+ k

=CdTck +d

[

12 +

12

1+ k

]

=CdTck +d

[

12(1+ k)+ 1

21+ k

]

=CdTck +d

[

1+ k2

1+ k

]

AFM 271 - NPV and Capital Budgeting Slide 13

Cont’d

now assume that the asset is sold for an amount S atthe end of year n. If the firm has other assets in thisCCA class, this might reduce the PV of the CCA taxshield as follows:

PV =CdTck +d

[

1+ k2

1+ k

]

−min(C,S)dTc

k +d ×1

(1+ k)n

note that the above formula is only an example: itand the similar equation (7.6) from p. 203 of the textare not always applicable!

AFM 271 - NPV and Capital Budgeting Slide 14

Cont’d

in general, the following steps apply when a firm sells a CCAeligible asset:1. The UCC in the asset class is reduced by the lesser of the sale price or the initial

cost.2. If step 1 leaves a negative balance, this amount is added to taxable income

(recaptured depreciation), and the UCC of the asset class is reset to zero.3. If step 1 leaves a positive balance and there are no other assets in the asset

class, this amount is deducted from taxable income (terminal loss), and the UCCof the asset class is reset to zero.

4. If step 1 leaves a positive balance and there are assets left in the class, thebalance becomes the new UCC for the class.

5. If the asset is sold for more than its initial cost, the difference is a capital gain(50% inclusion rate).

6. Suppose there is a new acquisition in the same year as an asset is sold. Definenet acquisitions as acquisitions less disposals. If net acquisitions are > 0, applythe half year rule to net acquisitions; if net acquisitions are < 0, do not apply thehalf year rule.

AFM 271 - NPV and Capital Budgeting Slide 15

Cont’d

example: Atlantic Trucking Co. is starting up business and hasjust purchased its first truck for $25,000. The truck is in Class10 with a CCA rate of 30%. Calculate applicable CCA for years1, 2, and 3:

Year Beginning UCC CCA Ending UCC123

now suppose that the firm buys a second truck for $35,000 inyear 2 and that it sells the first truck for $7,000 in year 3:

AFM 271 - NPV and Capital Budgeting Slide 16

Cont’d

Year Beginning UCC CCA Ending UCC1 12,500 3,750 8,75023

instead suppose that the firm buys a second truck for $35,000in year 2 and that it sells the first truck for $7,000 in year 2:

Year Beginning UCC CCA Ending UCC1 12,500 3,750 8,75023

AFM 271 - NPV and Capital Budgeting Slide 17

Cont’d

to illustrate some asset disposition cases, consider the following four scenarios. Herea firm purchased a number of assets in a single class some time ago for $117,000,and at the beginning of the current year, this pool of assets had a UCC of $82,500.

Scenario 1 2 3 4Beginning UCC $82,500 $82,500 $82,500 $82,500Capital cost ofassets sold $35,000 $117,000 $85,000 $117,000Sale proceeds $12,000 $100,000 $90,000 $50,000Capital gainsUCC after saleTerminal lossRecaptureEnding UCC

AFM 271 - NPV and Capital Budgeting Slide 18

Total Project Cash Flow vs. Tax Shield Approach

to illustrate, we will consider in detail the MMCCexample from the text (pp. 188-193, 200-204). Theinformation provided includes:

Expected life of machine 8 yearsCosts of test marketing $250,000Current market value of factory site $0Cost of machine $800,000Salvage value after 8 years $150,000Production in thousands of units (by year) 6, 9, 12, 13, 12, 10, 8, 6Unit price in first year $100Growth rate in unit price after first year 2%Unit production costs in first year $64Growth rate in production costs after first year 5%Corporate tax rate 40%Working capital: initial $40,000Working capital: end $0Working capital: during 15% of salesInflation: 5%Fixed costs: $50,000 per year

AFM 271 - NPV and Capital Budgeting Slide 19

Cont’d

the total project cash flow approach:the basic idea is to determine the project cash flowsyear by year, add them up, and discount to obtainNPVsome notes:

in general, cannot use convenient PV formulas(annuities, perpetuities)requires that all cash flows (for a given year) mustbe either in real terms or in nominal termsrequires that all cash flows be discounted at thesame ratemust use this approach if we want to calculateIRR, payback, or AAR

see spreadsheet handouts for MMCC exampleAFM 271 - NPV and Capital Budgeting Slide 20

Cont’d

the tax shield approach:a “divide and conquer” methodrecall that after tax operating cash flow = revenues -expenses - taxessince taxable income = revenues - expenses - CCA, wehave

taxes = Tc × ( revenues − expenses − CCA )

this implies

after tax operating cash flow =

revenues × (1−Tc)− expenses × (1−Tc)+Tc × CCA

see spreadsheet handout for MMCC exampleAFM 271 - NPV and Capital Budgeting Slide 21

Detailed CCA Calculations and Examples

assume that salvage takes place at the end of year n,and consider the following formula for the PV of CCAtax shields:

PV of CCA =CdTck +d

[

1+ k2

1+ k

]

−∆UCCdTc

k +d × (1+ k)−n

∆UCC depends on circumstances. Let theundepreciated capital cost of the asset class just beforethe asset is disposed of be UCCn.if the firm only ever has one asset in the class, then

UCCn = C(1−d/2)(1−d)n−1

AFM 271 - NPV and Capital Budgeting Slide 22

Cont’d

Calculate the value X = UCCn −min(C,S). Then:

1. If X < 0 ⇒ recaptured depreciation

add X to taxable income in year n:

PV of recapture =−XTc

(1+ k)n

set UCC of asset class to zero (so∆UCC = UCCn):

PV of CCA =CdTck +d

[

1+ k2

1+ k

]

−UCCndTc

k +d × (1+ k)−n

AFM 271 - NPV and Capital Budgeting Slide 23

Cont’d

2. If X > 0 and there are no other assets in the class ⇒

terminal losssubtract X from taxable income in year n:

PV of terminal loss =XTc

(1+ k)n

set UCC of asset class to zero (so∆UCC = UCCn):

PV of CCA =CdTck +d

[

1+ k2

1+ k

]

−UCCndTc

k +d × (1+ k)−n

AFM 271 - NPV and Capital Budgeting Slide 24

Cont’d

3. If X > 0 and there are other assets in the classX becomes the new UCC of the asset class (so∆UCC = min(C,S)):

PV of CCA =CdTck +d

[

1+ k2

1+ k

]

−min(C,S)dTc

k +d × (1+ k)−n

three further points:1. If S > C, there is a capital gain:

PV of tax liability = −(S−C)Tc/2× (1+ k)−n

2. Formulas for CCA tax shields are always given innominal terms.

AFM 271 - NPV and Capital Budgeting Slide 25

Cont’d3. The formulas given on the preceding slides have a half year rule adjustment

applied to the first term but not the second term. This may not always be thecase: the half year rule may instead be applied to both terms, neither term, or thesecond term but not the first, depending on circumstances. In particular, the netacquisitions rule works as follows. Recall that all assets of a given firm within asingle CCA class are treated as part of a common pool. In practice, firms oftenbuy and sell many assets in a single class within a year. Define net acquisitionsfor an asset class as the total capital cost of all acquisitions (in a year) less thetotal adjusted cost of all disposals within that class and in that year. If netacquisitions is positive, apply the half year rule. If net acquisitions is negative,there is no adjustment for the half year rule.

AFM 271 - NPV and Capital Budgeting Slide 26

Cont’d

illustrative problem: you are considering whether to undertake a project that willgenerate revenues of $50,000 per year for 8 years and expenses of $20,000 per yearfor 8 years. The project requires an investment of $150,000 today in class 8 machinery(d = 25%). Assume k = 12%, Tc = 40%, and all cash flows are nominal, and calculateproject NPV under the following scenarios:1. You always have many other class 8 assets and a positive UCC in that class and

you can salvage the machinery at the end of the 9th year for (i) $10,000; and (ii)$200,000. (Assume there are no other acquisitions or disposals of class 8 assetsin either the current year or in the 9th year.)

2. The machinery will always be in its own class and it can be salvaged in 9 years for(i) $10,000; (ii) $20,000; and (iii) $200,000.

3. From this point on, the machinery will be in its own class and it can be salvaged in9 years for $10,000. However, you purchased one other class 8 asset 5 years agofor $200,000 which you have just sold for (i) $100,000; and (ii) $175,000.

AFM 271 - NPV and Capital Budgeting Slide 27

Cont’d

1. (i)

Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $3,606.10PV perpetual tax shield on $150,000: $38,368.73PV lost tax shield: -$974.62NPV: -$19,582.28

AFM 271 - NPV and Capital Budgeting Slide 28

Cont’d

1. (ii)

Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $72,122.00PV capital gain tax: -$3,606.10PV perpetual tax shield on $150,000: $38,368.73PV lost tax shield: -$14,619.33NPV: $31,682.81

AFM 271 - NPV and Capital Budgeting Slide 29

Cont’d

2. (i)

Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $3,606.10PV perpetual tax shield on $150,000: $38,368.73PV lost tax shield: -$1,280.64PV terminal loss: $452.90NPV: -$19,435.40

AFM 271 - NPV and Capital Budgeting Slide 30

Cont’d

2. (ii)

Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $7,212.20PV perpetual tax shield on $150,000: $38,368.73PV lost tax shield: -$1,280.64PV recapture: -$989.54NPV: -$17,271.74

AFM 271 - NPV and Capital Budgeting Slide 31

Cont’d

2. (iii)

Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $72,122.10PV capital gain tax: -$3,606.10PV perpetual tax shield on $150,000: $38,368.73PV lost tax shield: -$1,280.64PV recapture: -$19,741.26NPV: $25,280.24

AFM 271 - NPV and Capital Budgeting Slide 32

Cont’d

3. (i)Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $3,606.10PV perpetual tax shield on $50,000: $12,789.58PV continuing tax shield on $55,371.09 $14,965.16PV lost tax shield: -$832.08PV recapture (year 9): -$210.96PV avoided recapture today: $17,851.56NPV: -$12,413.13

AFM 271 - NPV and Capital Budgeting Slide 33

Cont’d

3. (ii)

Cost of machine: -$150,000.00PV after-tax operating revenues: $149,029.19PV after-tax operating expenses: -$59,611.68PV salvage: $3,606.10PV perpetual tax shield on $30,371.09: $8,208.40PV lost tax shield: -$222.25PV recapture (year 9): -$1,113.51PV avoided recapture today: $47,851.56NPV: -$2,252.19

AFM 271 - NPV and Capital Budgeting Slide 34

Project Interactions

many projects have effects on others, e.g. it is important toincorporate effects on other aspects of a firm’s business incapital budgeting analysis (including opportunity costs), andCCA pooling of assets can lead to other interactions betweenprojects

another aspect of this is choosing between investments ofunequal lives. Suppose that two machines produce the sameoutput but have the following after-tax operating costs per year:

Machine C0 C1 C2 C3

A -1,000 -500 -500 0B -2,000 -100 -100 -100

At a 10% discount rate, which is cheaper to operate?AFM 271 - NPV and Capital Budgeting Slide 35

Cont’d

the replacement chain:why not just use NPV and choose the machine withlower discounted costs?assume that machines are needed foreverthe matching cycle approach:

run the example for 6 years. A has 3 completecycles, B has 2:

PV of costs over 6 years:

AFM 271 - NPV and Capital Budgeting Slide 36

Cont’d

the equivalent annual cost (EAC) approach:idea is to convert PV of costs for machine into anappropriate annuity:

firm is indifferent between PV of costs and EACsince the project is assumed to continue forever,the EAC lasts forever, so choose the machine withlower EAC

AFM 271 - NPV and Capital Budgeting Slide 37

Cont’d

when to replace an old machine?1. Calculate EAC for new machine (EACnew)2. Calculate cost of operating old machine for 1 more

year (Cold)3. Replace just before Cold > EACnew

example: a firm has an existing machine, which could be salvaged for $2,800 today,$2,100 after one year, $1,200 after two years, or zero after 3 years (at which point itwould have to be replaced). Maintenance costs on this old machine are $1,175 afterone year, $1,600 after two years, and $1,800 after three years. A new machine isavailable which costs $5,000 and can be salvaged after four years for $1,800. Itsmaintenance costs are $1,000 after one year, $1,250 after two years, $1,500 afterthree years, and $2,000 after four years. The new machine produces the same outputas the old machine. When should the firm replace the old machine? Assume adiscount rate of 10%.

AFM 271 - NPV and Capital Budgeting Slide 38

Cont’d

the EAC for the new machine is:

should the existing machine be replaced now?

AFM 271 - NPV and Capital Budgeting Slide 39

Cont’d

what about replacing it after one year?

note that these types of decisions can easily get farmore complicated (e.g. different output levels for themachines, different numbers of machines required,anticipated new technology, etc.)

AFM 271 - NPV and Capital Budgeting Slide 40