new hire orientation - eprmg.net irrrl... · va irrrl: va interest rate reduction refinance loan...

TRANSCRIPT

VA IRRRL Presented by: Michelle Mottet

3/25/2014 1

Table of Contents Eligibility

Closing Costs

Maximum Loan Amount Calculation

VA Funding Fee

VA Form 26-8923

Appraisal Requirements

Resources

VA IRRRL

3/25/2014 2

Eligibility VA IRRRL: VA Interest Rate Reduction Refinance Loan An IRRRL is a VA-guaranteed loan made to refinance an existing VA-guaranteed loan, generally at a lower interest rate than the existing VA loan, and with lower principal and interest payments than the existing VA loan. Generally, no credit information or underwriting is required on an IRRRL, and any lender may close an IRRRL automatically. PRMG does have a six month seasoning requirement for newly closed loans. Loan Term: The maximum loan term is the original term of the VA loan being refinanced plus 10 years, but may not exceed 30 years and 32 days. For example, if the old loan was made with a 15-year term, the term of the new loan cannot exceed 25 years.

VA IRRRL

3/25/2014 3

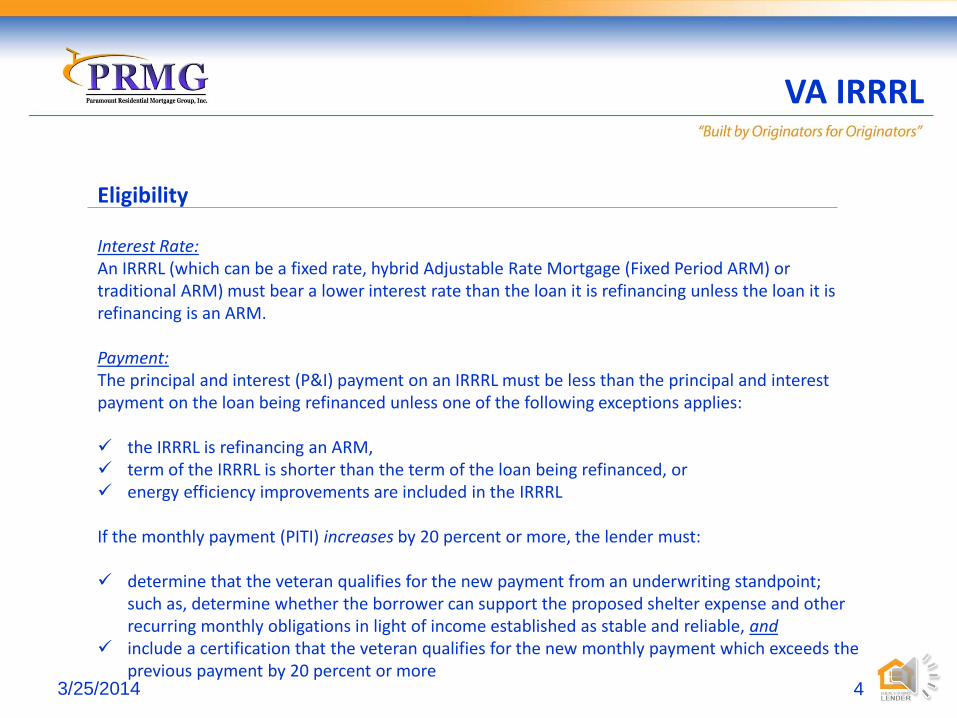

Eligibility Interest Rate: An IRRRL (which can be a fixed rate, hybrid Adjustable Rate Mortgage (Fixed Period ARM) or traditional ARM) must bear a lower interest rate than the loan it is refinancing unless the loan it is refinancing is an ARM. Payment: The principal and interest (P&I) payment on an IRRRL must be less than the principal and interest payment on the loan being refinanced unless one of the following exceptions applies: the IRRRL is refinancing an ARM, term of the IRRRL is shorter than the term of the loan being refinanced, or energy efficiency improvements are included in the IRRRL If the monthly payment (PITI) increases by 20 percent or more, the lender must: determine that the veteran qualifies for the new payment from an underwriting standpoint;

such as, determine whether the borrower can support the proposed shelter expense and other recurring monthly obligations in light of income established as stable and reliable, and

include a certification that the veteran qualifies for the new monthly payment which exceeds the previous payment by 20 percent or more

VA IRRRL

3/25/2014 4

Eligibility Certification: For all IRRRLs, the veteran must sign a statement acknowledging the effect of the refinancing loan on the veteran’s loan payments and interest rate. The statement must show the interest rate and monthly payments for the new loan versus that for the old loan. The statement must also indicate how long it would take to recoup ALL closing costs (both those included in the loan and those paid outside of closing). Note: This would not be required in those limited cases where the payment is not decreasing (reduced term of loan, etc.). The veteran’s statement may be combined with the lender’s certification and should be on the lender’s own letterhead.

VA IRRRL

3/25/2014 5

Closing Costs

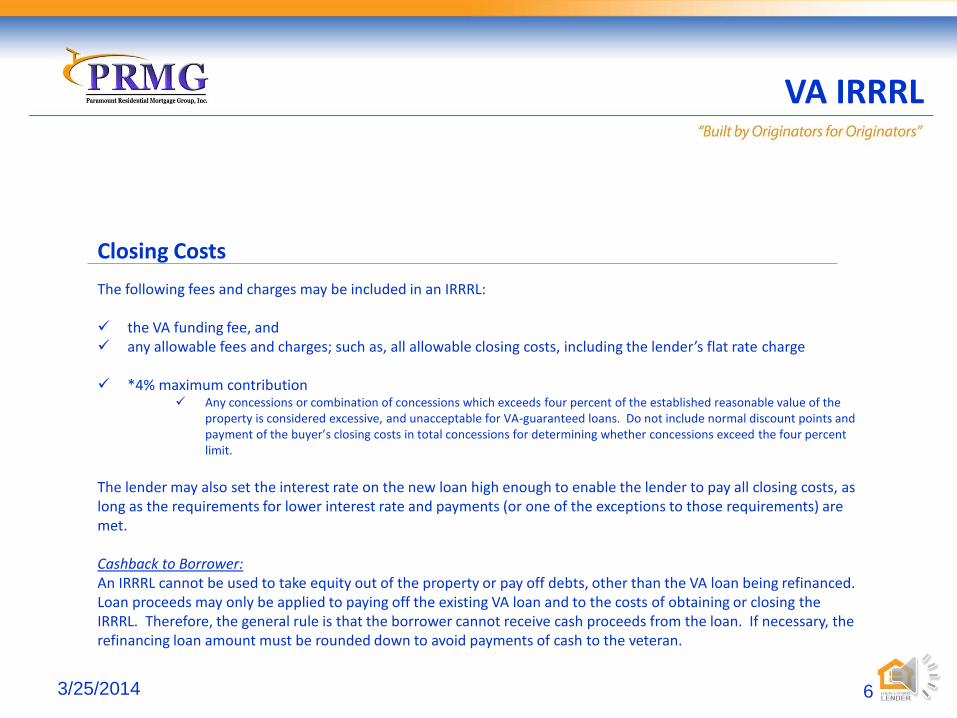

The following fees and charges may be included in an IRRRL: the VA funding fee, and any allowable fees and charges; such as, all allowable closing costs, including the lender’s flat rate charge *4% maximum contribution

Any concessions or combination of concessions which exceeds four percent of the established reasonable value of the property is considered excessive, and unacceptable for VA-guaranteed loans. Do not include normal discount points and payment of the buyer’s closing costs in total concessions for determining whether concessions exceed the four percent limit.

The lender may also set the interest rate on the new loan high enough to enable the lender to pay all closing costs, as long as the requirements for lower interest rate and payments (or one of the exceptions to those requirements) are met. Cashback to Borrower: An IRRRL cannot be used to take equity out of the property or pay off debts, other than the VA loan being refinanced. Loan proceeds may only be applied to paying off the existing VA loan and to the costs of obtaining or closing the IRRRL. Therefore, the general rule is that the borrower cannot receive cash proceeds from the loan. If necessary, the refinancing loan amount must be rounded down to avoid payments of cash to the veteran.

VA IRRRL

3/25/2014 6

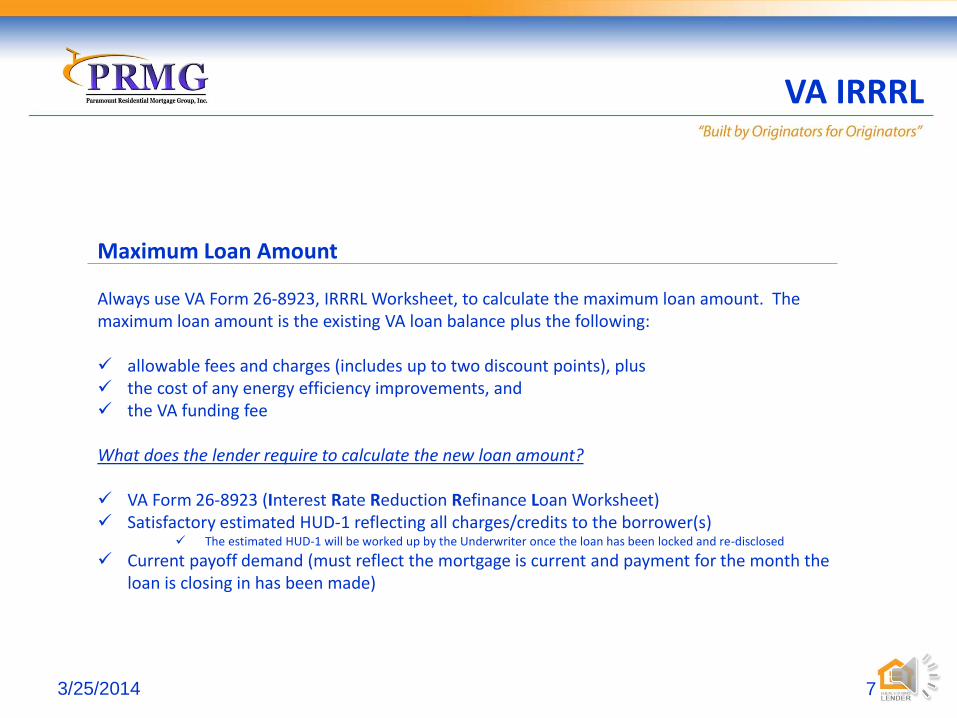

Maximum Loan Amount Always use VA Form 26-8923, IRRRL Worksheet, to calculate the maximum loan amount. The maximum loan amount is the existing VA loan balance plus the following: allowable fees and charges (includes up to two discount points), plus the cost of any energy efficiency improvements, and the VA funding fee What does the lender require to calculate the new loan amount? VA Form 26-8923 (Interest Rate Reduction Refinance Loan Worksheet) Satisfactory estimated HUD-1 reflecting all charges/credits to the borrower(s)

The estimated HUD-1 will be worked up by the Underwriter once the loan has been locked and re-disclosed

Current payoff demand (must reflect the mortgage is current and payment for the month the loan is closing in has been made)

VA IRRRL

3/25/2014 7

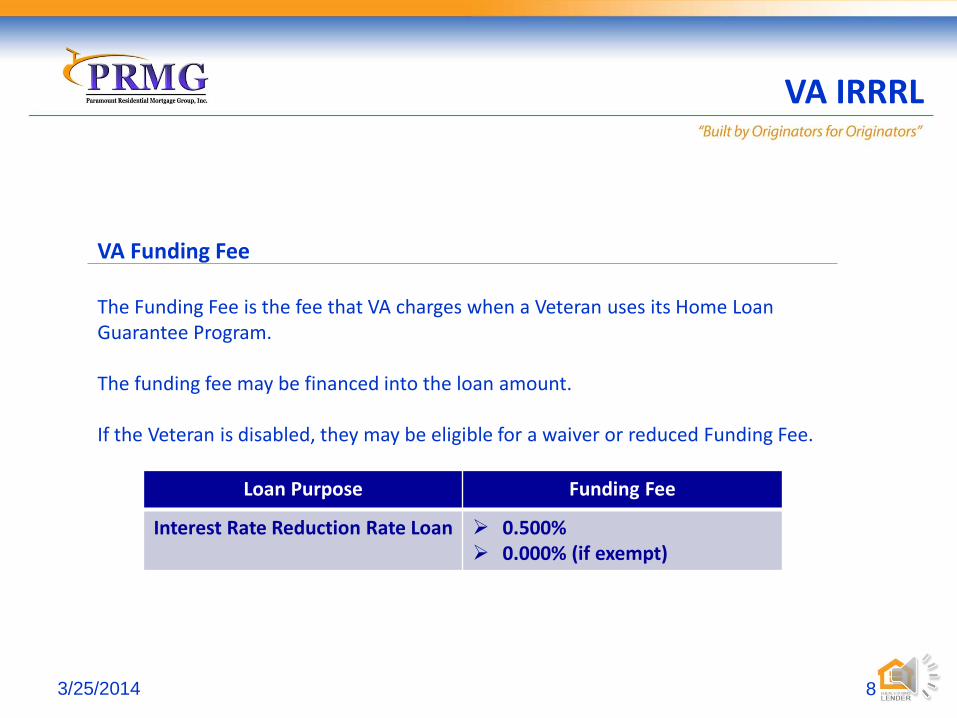

VA Funding Fee The Funding Fee is the fee that VA charges when a Veteran uses its Home Loan Guarantee Program. The funding fee may be financed into the loan amount. If the Veteran is disabled, they may be eligible for a waiver or reduced Funding Fee.

VA IRRRL

3/25/2014 8

Loan Purpose Funding Fee

Interest Rate Reduction Rate Loan 0.500% 0.000% (if exempt)

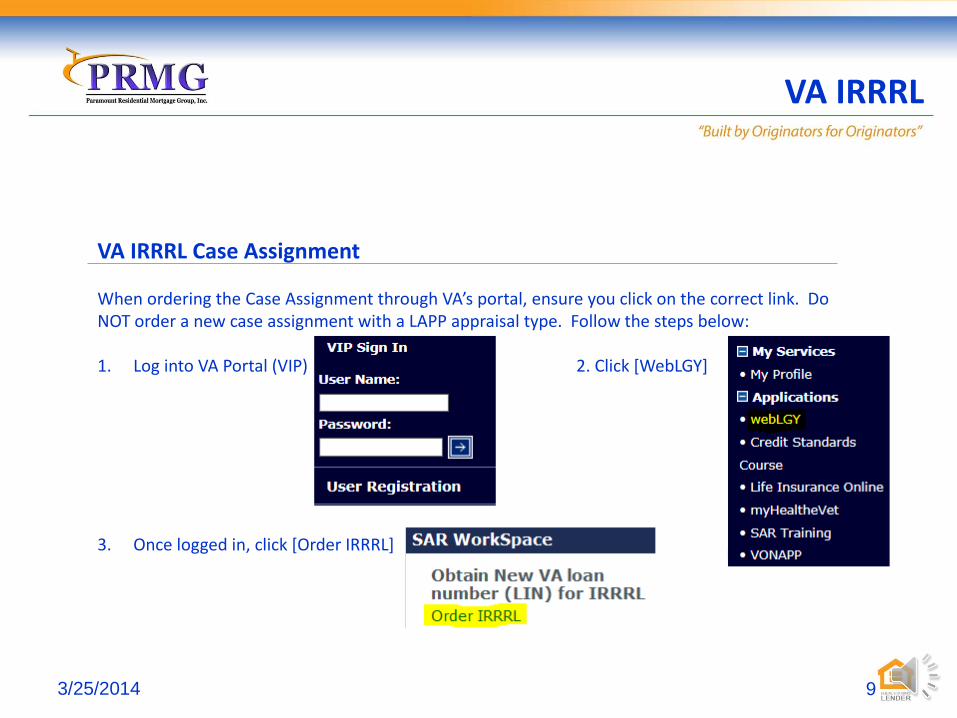

VA IRRRL Case Assignment When ordering the Case Assignment through VA’s portal, ensure you click on the correct link. Do NOT order a new case assignment with a LAPP appraisal type. Follow the steps below: 1. Log into VA Portal (VIP) 2. Click [WebLGY]

3. Once logged in, click [Order IRRRL]

VA IRRRL

3/25/2014 9

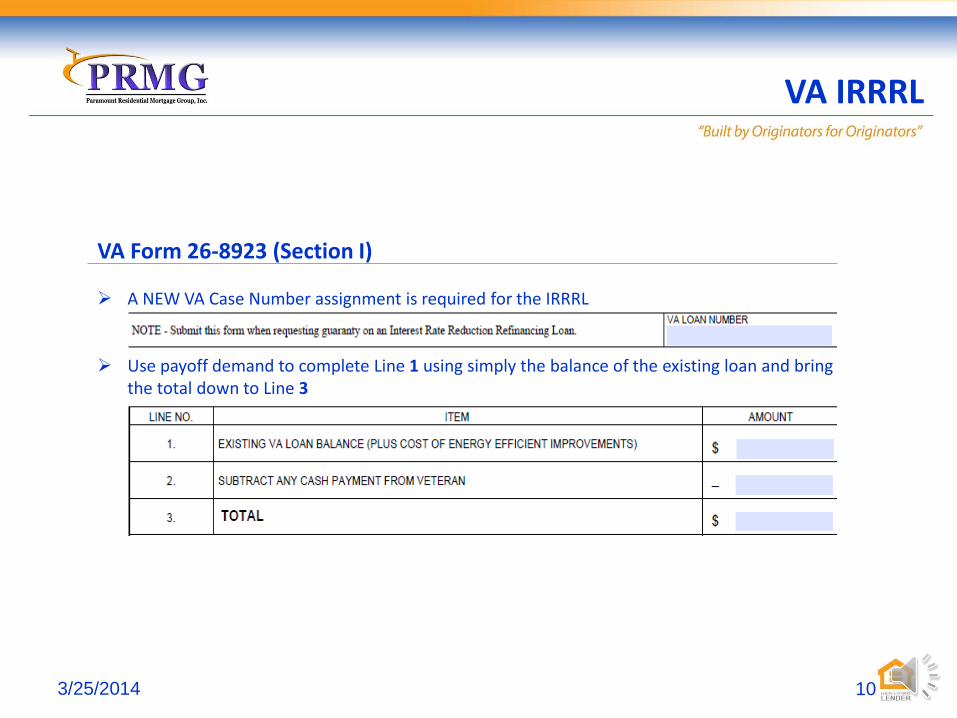

VA Form 26-8923 (Section I) A NEW VA Case Number assignment is required for the IRRRL Use payoff demand to complete Line 1 using simply the balance of the existing loan and bring

the total down to Line 3

VA IRRRL

3/25/2014 10

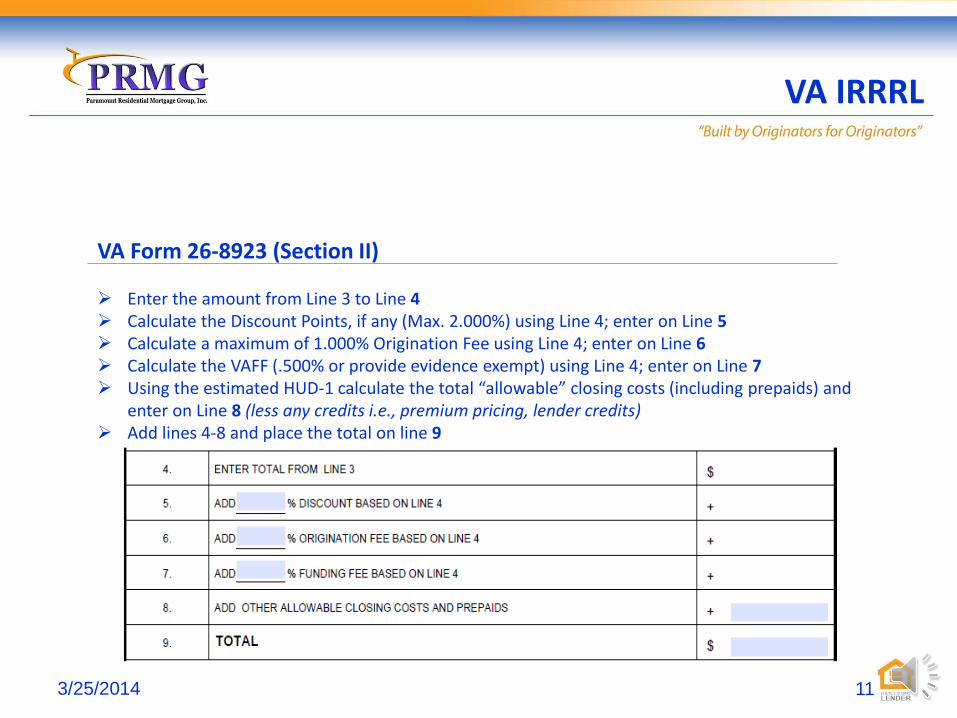

VA Form 26-8923 (Section II) Enter the amount from Line 3 to Line 4 Calculate the Discount Points, if any (Max. 2.000%) using Line 4; enter on Line 5 Calculate a maximum of 1.000% Origination Fee using Line 4; enter on Line 6 Calculate the VAFF (.500% or provide evidence exempt) using Line 4; enter on Line 7 Using the estimated HUD-1 calculate the total “allowable” closing costs (including prepaids) and

enter on Line 8 (less any credits i.e., premium pricing, lender credits) Add lines 4-8 and place the total on line 9

VA IRRRL

3/25/2014 11

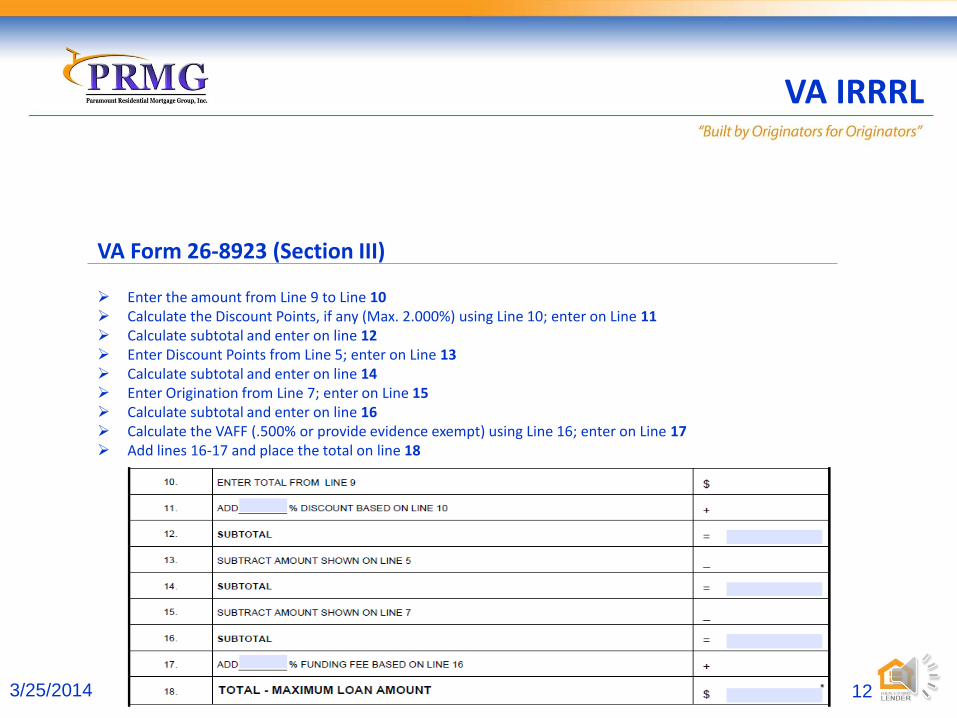

VA Form 26-8923 (Section III) Enter the amount from Line 9 to Line 10 Calculate the Discount Points, if any (Max. 2.000%) using Line 10; enter on Line 11 Calculate subtotal and enter on line 12 Enter Discount Points from Line 5; enter on Line 13 Calculate subtotal and enter on line 14 Enter Origination from Line 7; enter on Line 15 Calculate subtotal and enter on line 16 Calculate the VAFF (.500% or provide evidence exempt) using Line 16; enter on Line 17 Add lines 16-17 and place the total on line 18

VA IRRRL

3/25/2014 12

VA Form 26-8923

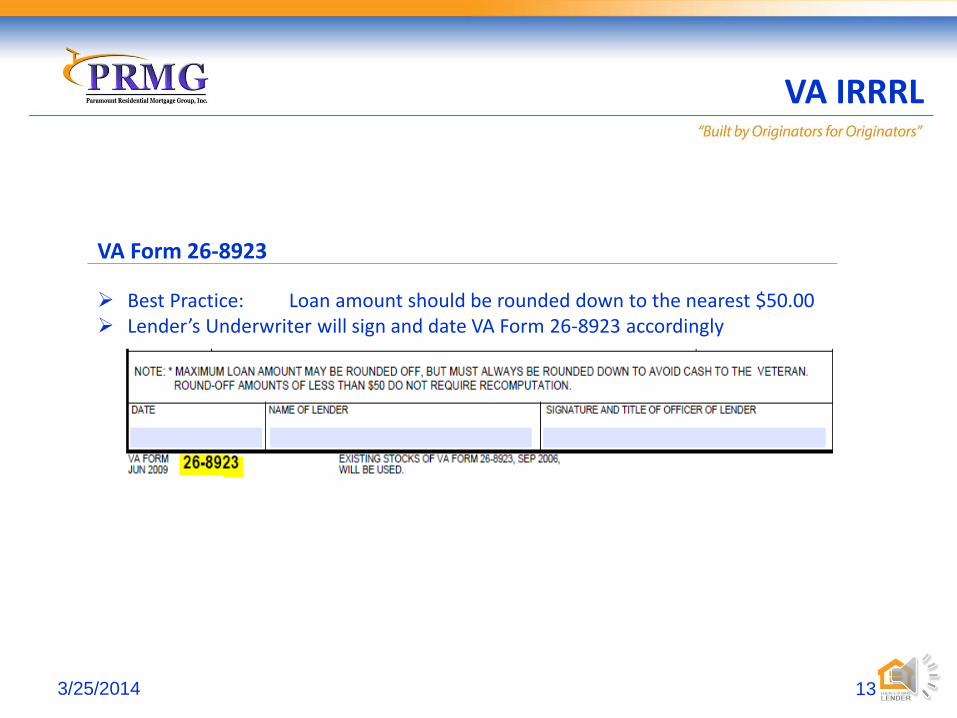

Best Practice: Loan amount should be rounded down to the nearest $50.00 Lender’s Underwriter will sign and date VA Form 26-8923 accordingly

VA IRRRL

3/25/2014 13

Appraisal Requirements:

Conventional full appraisal or exterior-only (2055/1075) appraisal report with 1004MC Addendum required on all one unit property types

The appraisal report must have a C1 to C5 condition rating The appraisal must be dated within 120 days of the Note Subject property must be rated as average or higher condition Any repair requirements noted by the Appraiser that impact the safety, structural

soundness, and habitability of the subject property must be completed PRMG reserves the right to require additional appraisal reviews/reports at the

Underwriter's discretion

VA IRRRL

3/25/2014 14

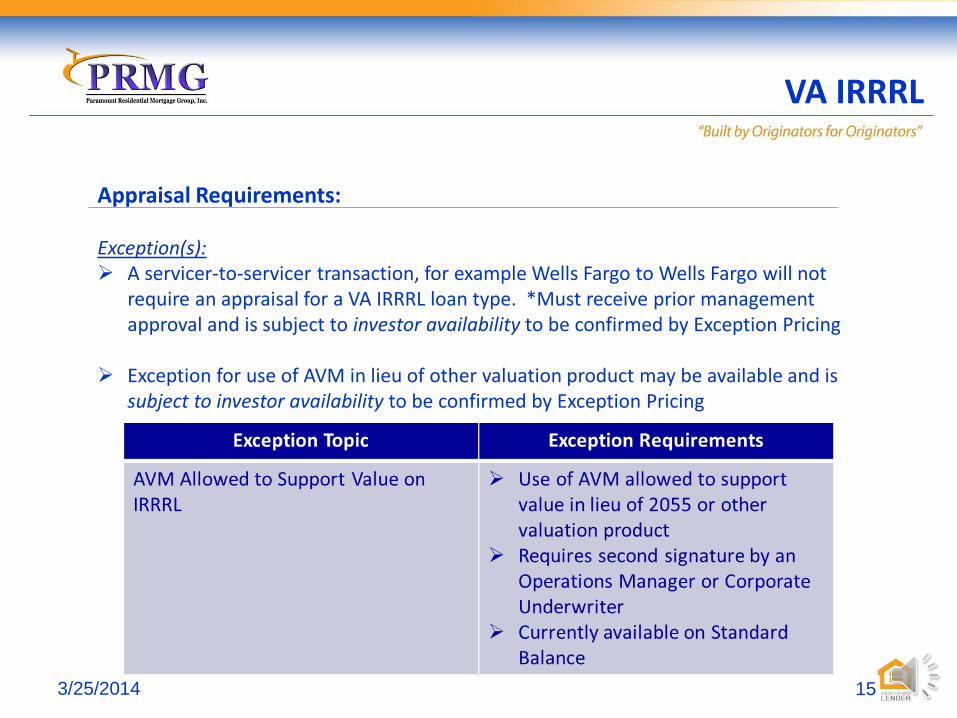

Appraisal Requirements: Exception(s): A servicer-to-servicer transaction, for example Wells Fargo to Wells Fargo will not

require an appraisal for a VA IRRRL loan type. *Must receive prior management approval and is subject to investor availability to be confirmed by Exception Pricing

Exception for use of AVM in lieu of other valuation product may be available and is

subject to investor availability to be confirmed by Exception Pricing

VA IRRRL

3/25/2014 15

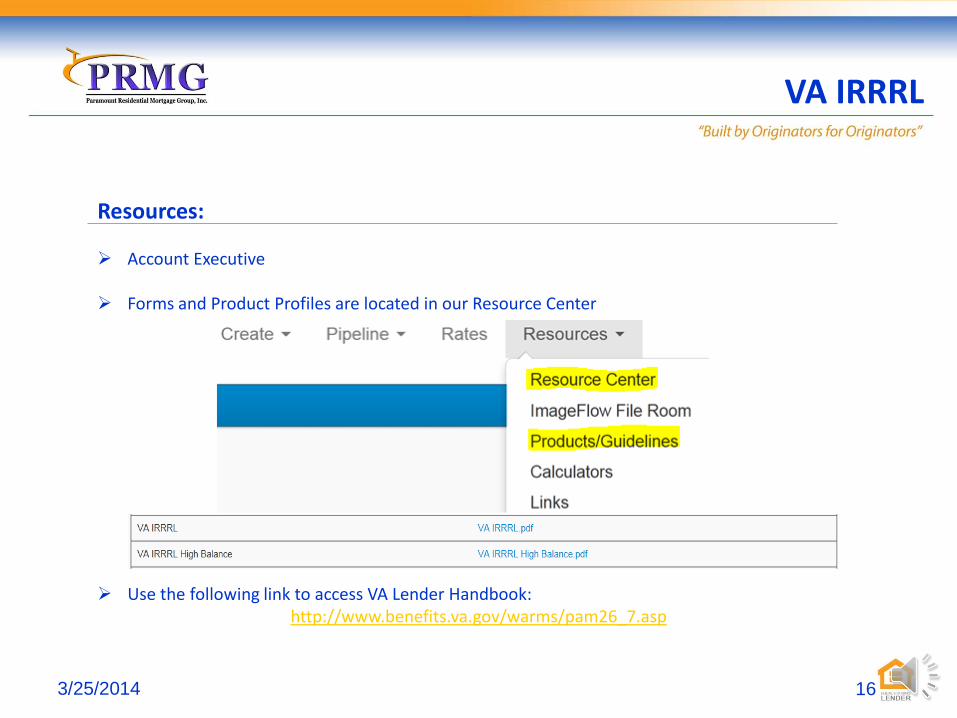

Resources: Account Executive

Forms and Product Profiles are located in our Resource Center

Use the following link to access VA Lender Handbook: http://www.benefits.va.gov/warms/pam26_7.asp

VA IRRRL

3/25/2014 16

Thank You for Your Attendance!

VA IRRRL

3/25/2014 17