ngv retrofit vs oem: trends & european overview · ngv retrofit vs oem: trends & european...

TRANSCRIPT

NGV RETROFIT vs OEM:

Trends &

European Overview Presentation to

Informal Group on Gaseous Fuelled Vehicles

2 October 2012

presented by

Dr. Jeffrey M. Seisler

GFV-22-07

Background notes for this

presentation • The Worldwide Trends in the first part of this presentation

includes materials from various presentations by Clean Fuels

Consulting and is provided to the Informal Group on Gaseous

Fuelled Vehicles as background to the second part of the

presentation.

• The information on European OEM/retrofit NGVs has been

gathered and prepared by Clean Fuels Consulting (2011-

2012). Some of the information was developed for the

European Business Congress project, Legal and Regulatory

Environment for the Construction and Operation of CNG

Refuelling Stations in European Countries.

• The European compilation was prepared for DG Enterprise

and was supplied by CFC on behalf of NGV Global.

General Worldwide Trends

Natural Gas Vehicle

Retrofits & OEMs

No Warranty

€

Time

Conversions

Gen I II III IV V VI QVM* / OEM**

*Qualified Vehicle Modifier

**Original Equipment Manufacturer

Conversions OEMs

S

A

F

E

T

Y

R

E

L

I

A

B

I

L

I

T

Y

Europe, Japan, S. Korea,

North-America(QVM-based),

Australia

South-America Continental Asia

RETROFIT vs OEM

€

Warranty

Source: Dr. Jeffrey M. Seisler,

updated 10 2012

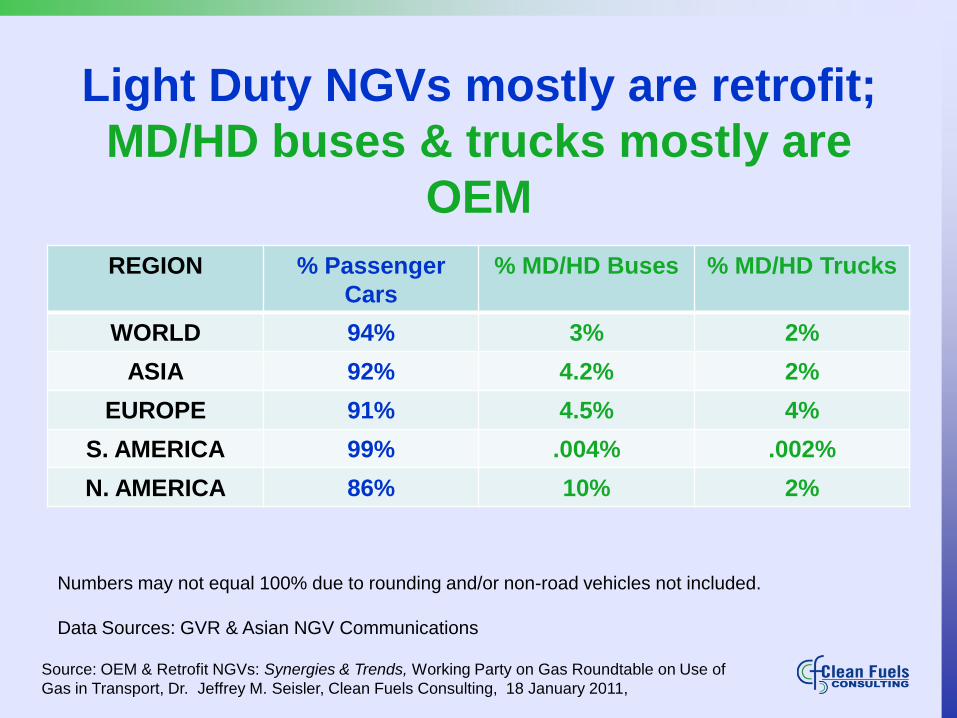

Light Duty NGVs mostly are retrofit;

MD/HD buses & trucks mostly are

OEM

REGION % Passenger

Cars

% MD/HD Buses % MD/HD Trucks

WORLD 94% 3% 2%

ASIA 92% 4.2% 2%

EUROPE 91% 4.5% 4%

S. AMERICA 99% .004% .002%

N. AMERICA 86% 10% 2%

Numbers may not equal 100% due to rounding and/or non-road vehicles not included.

Data Sources: GVR & Asian NGV Communications

Source: OEM & Retrofit NGVs: Synergies & Trends, Working Party on Gas Roundtable on Use of

Gas in Transport, Dr. Jeffrey M. Seisler, Clean Fuels Consulting, 18 January 2011,

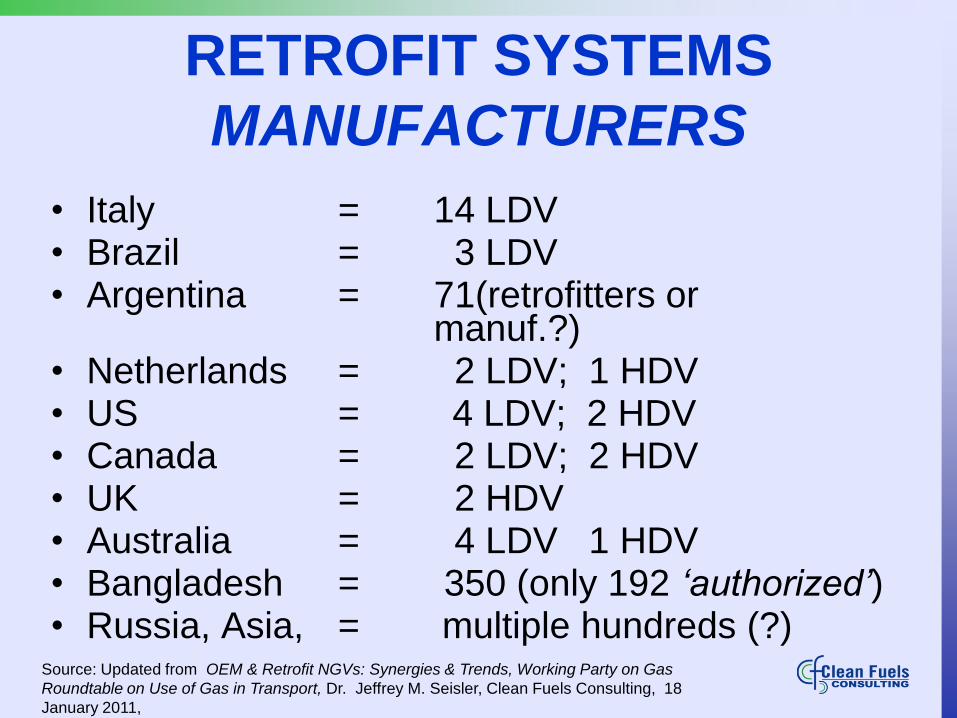

RETROFIT SYSTEMS

MANUFACTURERS

• Italy = 14 LDV • Brazil = 3 LDV • Argentina = 71(retrofitters or

manuf.?) • Netherlands = 2 LDV; 1 HDV • US = 4 LDV; 2 HDV • Canada = 2 LDV; 2 HDV • UK = 2 HDV • Australia = 4 LDV 1 HDV • Bangladesh = 350 (only 192 ‘authorized’) • Russia, Asia, = multiple hundreds (?)

Source: Updated from OEM & Retrofit NGVs: Synergies & Trends, Working Party on Gas

Roundtable on Use of Gas in Transport, Dr. Jeffrey M. Seisler, Clean Fuels Consulting, 18

January 2011,

7

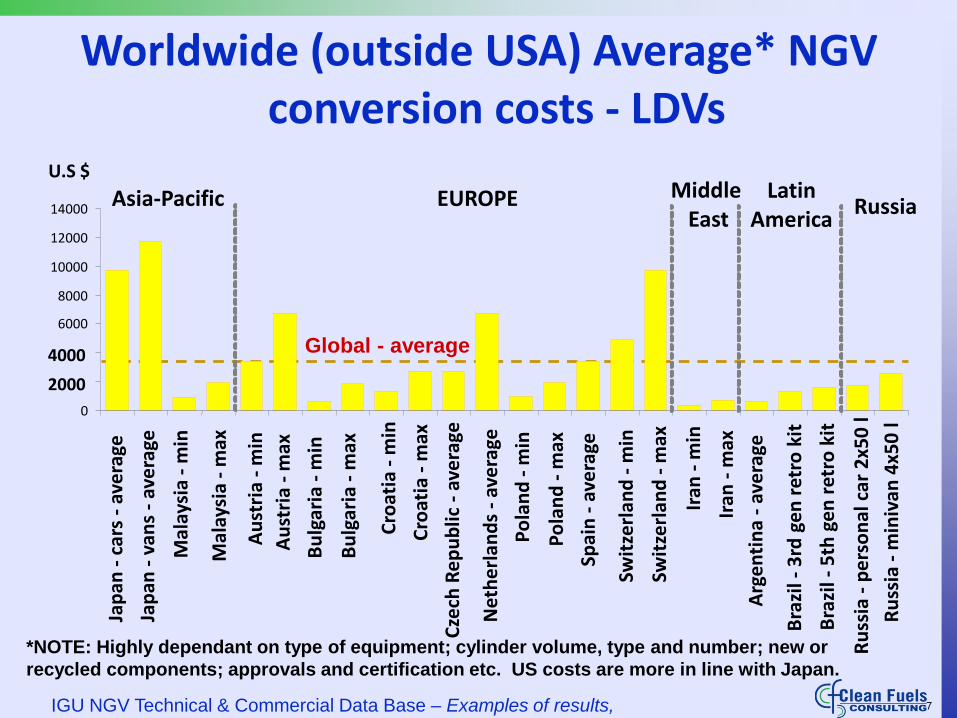

*NOTE: Highly dependant on type of equipment; cylinder volume, type and number; new or

recycled components; approvals and certification etc. US costs are more in line with Japan.

Global - average

Worldwide (outside USA) Average* NGV conversion costs - LDVs

0

2000

4000

6000

8000

10000

12000

14000

Jap

an -

car

s -

ave

rage

Jap

an -

van

s -

ave

rage

Mal

aysi

a -

min

Mal

aysi

a -

max

Au

stri

a -

min

Au

stri

a -

max

Bu

lgar

ia -

min

Bu

lgar

ia -

max

Cro

atia

- m

in

Cro

atia

- m

ax

Cze

ch R

ep

ub

lic -

ave

rage

Net

he

rlan

ds

- av

era

ge

Po

lan

d -

min

Po

lan

d -

max

Spai

n -

ave

rage

Swit

zerl

and

- m

in

Swit

zerl

and

- m

ax

Iran

- m

in

Iran

- m

ax

Arg

en

tin

a -

ave

rage

Bra

zil -

3rd

ge

n r

etro

kit

Bra

zil -

5th

ge

n r

etro

kit

Ru

ssia

- p

ers

on

al c

ar 2

x50

l

Ru

ssia

- m

iniv

an 4

x50

l

U.S $

Asia-Pacific EUROPE Middle East

Latin America

Russia

IGU NGV Technical & Commercial Data Base – Examples of results,

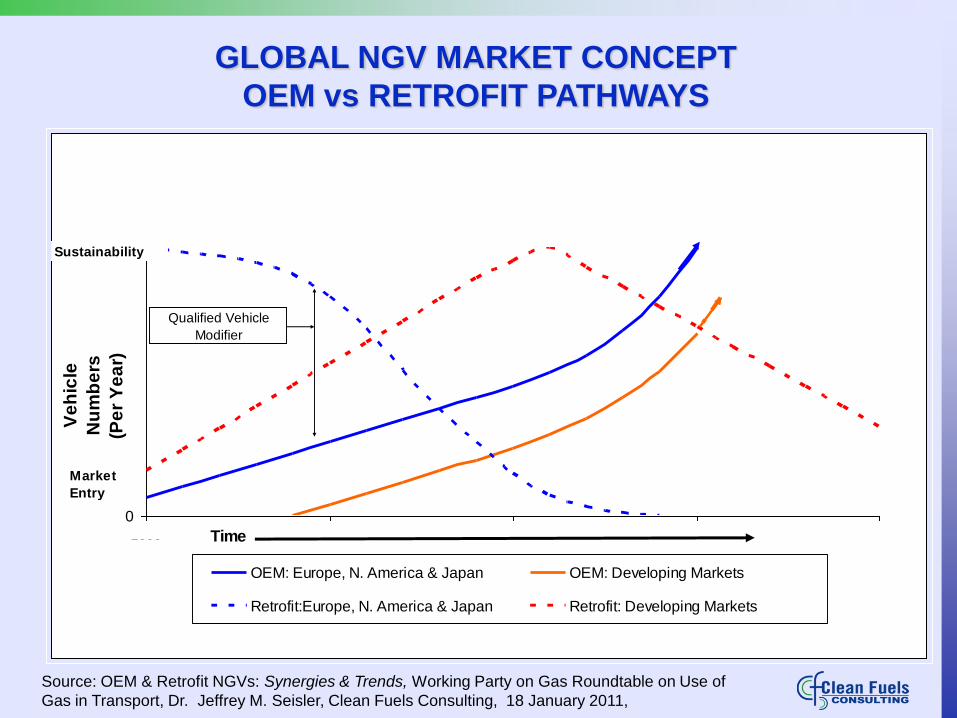

0

30000

2000 2005 2010 2015 2020Time

Ve

hic

le

Nu

mb

ers

(Pe

r Y

ea

r)

OEM: Europe, N. America & Japan OEM: Developing Markets

Retrofit:Europe, N. America & Japan Retrofit: Developing Markets

Qualified Vehicle

Modifier

Market

Entry

Sustainability

GLOBAL NGV MARKET CONCEPT

OEM vs RETROFIT PATHWAYS

Source: OEM & Retrofit NGVs: Synergies & Trends, Working Party on Gas Roundtable on Use of

Gas in Transport, Dr. Jeffrey M. Seisler, Clean Fuels Consulting, 18 January 2011,

0

30000

2000 2005 2010 2015 2020Time

Ve

hic

le

Nu

mb

ers

(Pe

r Y

ea

r)

OEM: Europe, N. America & Japan OEM: Developing Markets

Retrofit:Europe, N. America & Japan Retrofit: Developing Markets

Qualified Vehicle

Modifier

Market

Entry

Sustainability

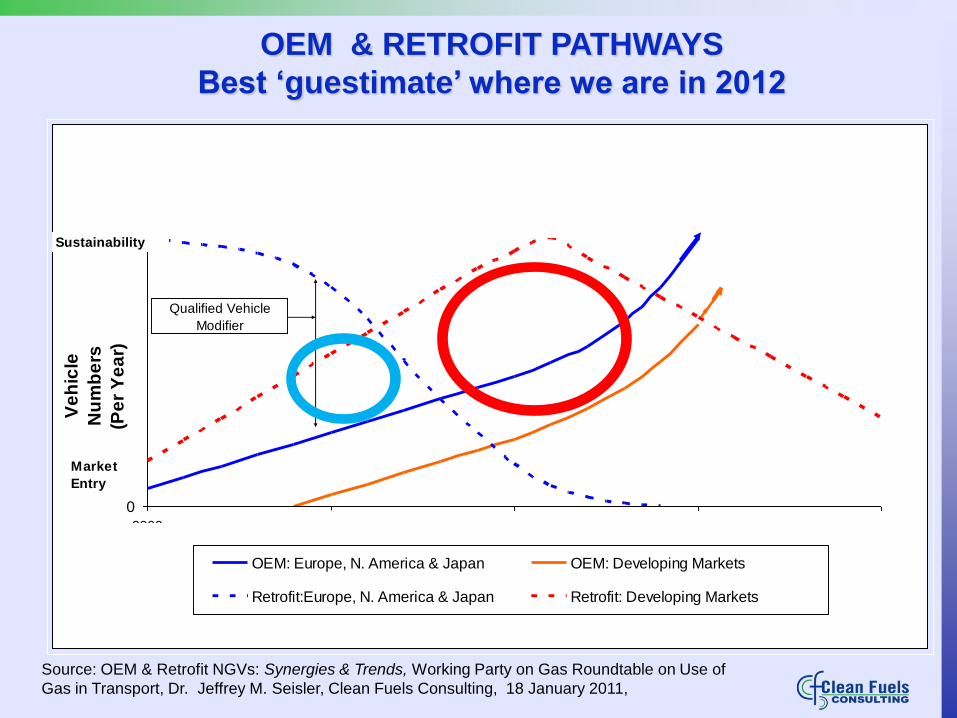

OEM & RETROFIT PATHWAYS

Best ‘guestimate’ where we are in 2012

Source: OEM & Retrofit NGVs: Synergies & Trends, Working Party on Gas Roundtable on Use of

Gas in Transport, Dr. Jeffrey M. Seisler, Clean Fuels Consulting, 18 January 2011,

European Natural Gas Vehicle

Retrofits & OEMs

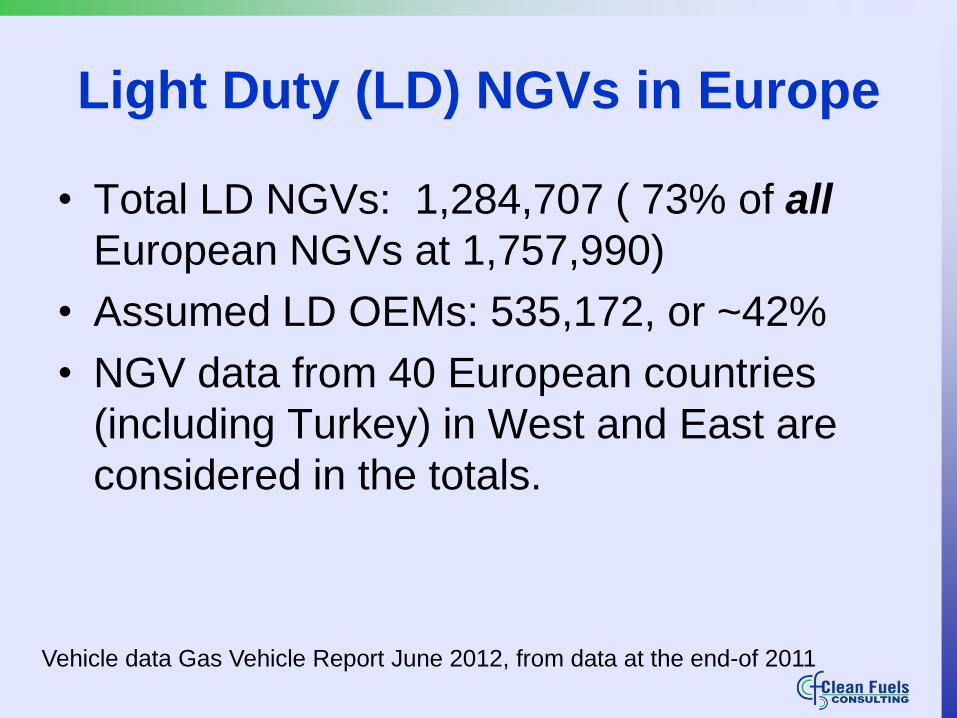

Light Duty (LD) NGVs in Europe

• Total LD NGVs: 1,284,707 ( 73% of all

European NGVs at 1,757,990)

• Assumed LD OEMs: 535,172, or ~42%

• NGV data from 40 European countries

(including Turkey) in West and East are

considered in the totals.

Vehicle data Gas Vehicle Report June 2012, from data at the end-of 2011

In Europe, OEM NGV sales dominate in

Italy, Germany and Sweden • Italy: 775,590 LD-NGVs – ‘guestimate’ 50-50 split between

OEM & retrofit, with OEMs now dominating sales.

• Germany: 94,504 LD-NGVs ~100% OEM

• Sweden: 37,700 LD-NGVs ~100% OEM including QVM

(qualified vehicle modifier) Volvos

• OEM sales play an important role in Switzerland, Austria

(90% OEM vs 10% retrofit) and Spain where the total light

duty NGV population (3 countries) is 15,816.

• Netherlands OEM NGV population also is increasing but it

is difficult to judge how many of their 3,530 LD NGVs are

OEMs since they have had a strong conversion network

(‘guestimate’ 25% OEM)

Vehicle data Gas Vehicle Report June 2012, from data at the end-of 2011

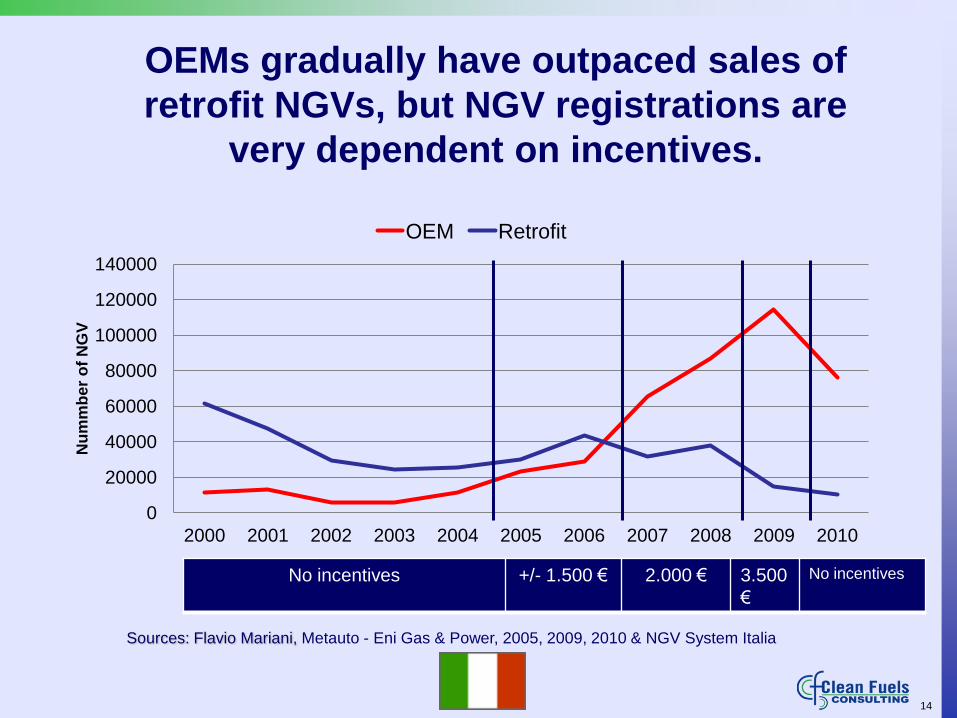

ITALY

14

No incentives +/- 1.500 € 2.000 € 3.500

€

No incentives

OEMs gradually have outpaced sales of

retrofit NGVs, but NGV registrations are

very dependent on incentives.

0

20000

40000

60000

80000

100000

120000

140000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Nu

mm

ber

of

NG

V

OEM Retrofit

Sources: Flavio Mariani, Metauto - Eni Gas & Power, 2005, 2009, 2010 & NGV System Italia

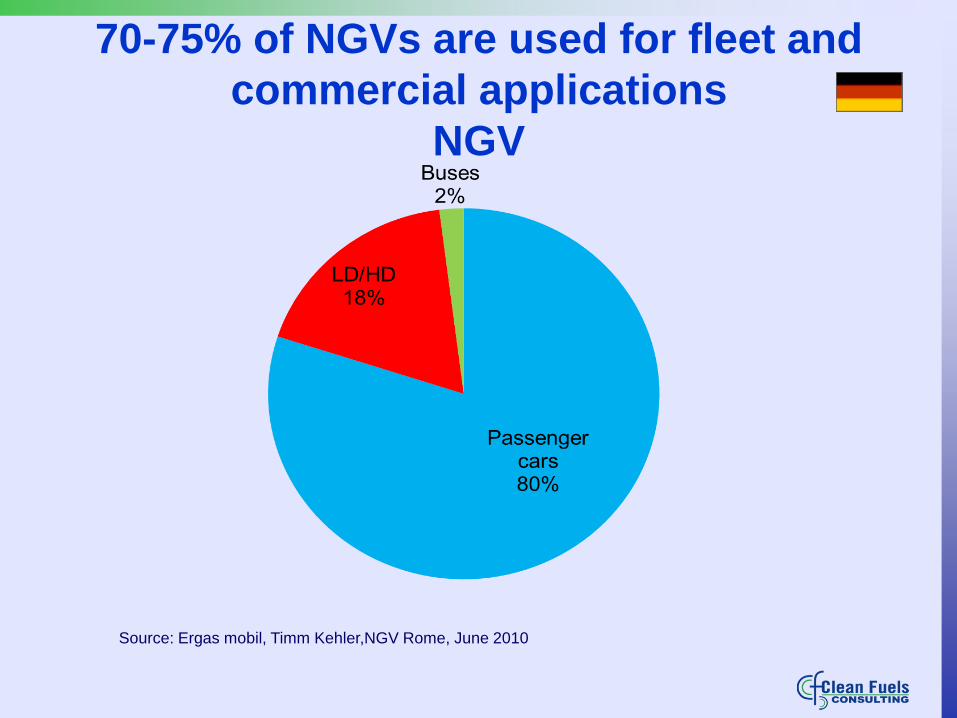

GERMANY

70-75% of NGVs are used for fleet and

commercial applications

NGV

Source: Ergas mobil, Timm Kehler,NGV Rome, June 2010

Volkswagen dominates the German

NGV market with 49%

6 German OEM are

currently in the market:

• Volkswagen

• Mercedes

• Opel

• Ford

• Evobus

• MAN

2 foreign OEM:

• FIAT

• IVECO Source: Ergas mobil, Timm Kehler,NGV Rome, June 2010

Associated ‘conversion industries’ based

in Germany tend to be design &

engineering firms but do not produce

mainstream NGV retrofit systems

• Brachetti and Partner

• IAV (engineering & development)

• IvS

• Air LNG (investigating LNG applications

for turbines for stationary and mobile

applications

CNG passenger car registration is

projected to approach diesel cars by

2020

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

CNG Registrations

Diesel Registrations

Source: BGW, Natural Gas Vehicles 2020

NGVs are anticipated to impact more

on diesel car sales then on gasoline

cars

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

T housands

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

CNG

Diesel

Gasol ine + other

CNG

Diesel

Gasoline

Source: BGW, Natural Gas Vehicles 2020

NGVs should be 8% of total vehicles in

Germany in 2016 (challenging target!)

Source: ENI, Compressed natural gas as fuel for NGV – potential, synergy and development , September 2011

SWEDEN

In Sweden the majority of the NGVs are

passenger cars

Source: Biogas Renewable Methane Gas, Leif Holmberg, Swedish Gas Association

OEMs offer a variety of NGVs in Sweden

VOLVO*

• V70 Bi-fuel

FIAT

• Punto Evo

• Doblò

• Fiorino

IVECO

• EcoDaily

MERCEDES

• Sprinter NGT

• E Class

• B 170 NGT

OPEL

• Zafira

• Combo

VOLKSWAGEN

• Passat

• Touran

• Caddy

• Caddy Maxi

• Transporter

Source: Fordonsgas *Qualified vehicle modifier now owned by Westport LD

Volkswagen dominated

2009 Swedish NGV car market

• Volkswagen TSI Passat EcoFuel accounted

for 68% of the total NG passenger cars

sales in Sweden

• Then follow Mercedes B 170 NGT (24 %),

VW Touran, VW Caddy, Opel Zafira,

Mercedes E 200 NGT, Opel Combo, and

Fiat Punto

Source: NGVA Europe, 2009

Volkswagen also is leading on

medium duty NGV sales

• Volkswagen Caddy accounts for some 45

% of the total sales

• Followed by Opel Combo, VW

Transporter, Fiat Fiorino, Iveco Daily, and

Fiat Doblò

Source: NGVA Europe, 2009

Swedish target is to reach 500,000

NGVs by 2020

0

50

100

150

200

250

300

350

400

450

500

550

600

2012 2013 2014 2015 2016 2017 2018 2019 2020

Target NGVs (x 1000)

NGV RETROFIT vs OEM:

Trends &

European Overview Presentation to

Informal Group on Gaseous Fuelled Vehicles

2 October 2012

presented by

Dr. Jeffrey M. Seisler