non-recourse carve-outs, bad-boy guaranties, and...

TRANSCRIPT

Non-Recourse Carve-Outs, Bad-Boy Guaranties,and Personal Liability: Latest DevelopmentsStrategies to Resolve Lender and Guarantor Disputes in and Outside of Bankruptcy

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, NOVEMBER 20, 2014

Presenting a live 90-minute webinar with interactive Q&A

Today’s faculty features:

The audio portion of the conference may be accessed via the telephone or by using your computer'sspeakers. Please refer to the instructions emailed to registrants for additional information. If youhave any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Thomas W. Coffey, Senior Counsel, Tucker Ellis, Cleveland

Paul S. Magy, Member, Clark Hill, Birmingham, Mich.

James H. Schwarz, Partner, Benesch Friedlander Coplan & Arnoff, Indianapolis

Daniel K. Wright, II, Member, Tucker Ellis, Cleveland

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the qualityof your sound will vary depending on the speed and quality of your internetconnection.

If the sound quality is not satisfactory, you may listen via the phone: dial1-866-328-9525 and enter your PIN when prompted. Otherwise, pleasesend us a chat or e-mail [email protected] immediately so we can addressthe problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen,press the F11 key again.

FOR LIVE EVENT ONLY

Sound QualityIf you are listening via your computer speakers, please note that the qualityof your sound will vary depending on the speed and quality of your internetconnection.

If the sound quality is not satisfactory, you may listen via the phone: dial1-866-328-9525 and enter your PIN when prompted. Otherwise, pleasesend us a chat or e-mail [email protected] immediately so we can addressthe problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen,press the F11 key again.

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at yourlocation by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number ofattendees at your location

• Click the word balloon button to send

FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at yourlocation by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number ofattendees at your location

• Click the word balloon button to send

Moderator:

Daniel K. Wright, II, Esq.Member, Real Estate GroupTucker Ellis LLPCleveland, Ohio

Panelists:

Thomas W. Coffey, Esq.Chair, Bankruptcy GroupTucker Ellis LLPCleveland, OH

Paul S. Magy, Esq.MemberClark Hill, PLCBirmingham, MI

James H. Schwarz, Esq.PartnerBenesch Friedlander Coplan & Aronoff LLPIndianapolis, IN

Panelists:

Thomas W. Coffey, Esq.Chair, Bankruptcy GroupTucker Ellis LLPCleveland, OH

Paul S. Magy, Esq.MemberClark Hill, PLCBirmingham, MI

James H. Schwarz, Esq.PartnerBenesch Friedlander Coplan & Aronoff LLPIndianapolis, IN

5

• “Springing Recourse” and “Bad-Boy Guarantys” – Recent Cases andLegislation – Paul S. Magy, Esq.

• Recent Trends - Non-Recourse Carve-Outs – James H. Schwarz, Esq.

• Discussion of Case Study – New Market Center

• Bankruptcy Perspective – Thomas W. Coffey, Esq.

• Conclusion – Practice Tips

OVERVIEW:

• “Springing Recourse” and “Bad-Boy Guarantys” – Recent Cases andLegislation – Paul S. Magy, Esq.

• Recent Trends - Non-Recourse Carve-Outs – James H. Schwarz, Esq.

• Discussion of Case Study – New Market Center

• Bankruptcy Perspective – Thomas W. Coffey, Esq.

• Conclusion – Practice Tips

7

“SPRINGING RECOURSE” AND“BAD-BOY” GUARANTEES –RECENT CASES AND LEGISLATION

“SPRINGING RECOURSE” AND“BAD-BOY” GUARANTEES –RECENT CASES AND LEGISLATION

Paul S. Magy, Esq.MemberClark Hill, PLCBirmingham, MI

8

• Wells Fargo Bank, N.A. v. Cherryland Mall Ltd P’shp,295 Mich. App. 99, 812 N.W.2d 799 (2011)(“Cherryland I”), rev’d on remand, 300 Mich. App.361, 835 N.W.2d 593 (2013).

• 51382 Gratiot Avenue Holdings, LLC v. ChesterfieldDevelopment Co., LLC,835 F. Supp.2d 384 (E.D. Mich. 2011)

• Borman LLC vs. 18718 Borman LLC and JosephSchwebel (U.S. Sixth Circuit 2014)

• Michigan’s and Ohio’s Non-Recourse Mortgage LoanActs

• Wells Fargo Bank, N.A. v. Cherryland Mall Ltd P’shp,295 Mich. App. 99, 812 N.W.2d 799 (2011)(“Cherryland I”), rev’d on remand, 300 Mich. App.361, 835 N.W.2d 593 (2013).

• 51382 Gratiot Avenue Holdings, LLC v. ChesterfieldDevelopment Co., LLC,835 F. Supp.2d 384 (E.D. Mich. 2011)

• Borman LLC vs. 18718 Borman LLC and JosephSchwebel (U.S. Sixth Circuit 2014)

• Michigan’s and Ohio’s Non-Recourse Mortgage LoanActs

9

Michigan’s Non-Recourse Mortgage Loan Act[2012 Public Act 67]

• Passed through the Michigan Legislature in record time.• Characterizes inclusion or enforcement of a post-

closing solvency covenant as an unfair trade practice.• Prohibits a post-closing solvency covenant from being

used as a non-recourse carve out.• Applies statue retroactively.• Constitutionality of the Non-recourse Mortgage Loan

Act is under challenge in the state and federal courts inMichigan.

Michigan’s Non-Recourse Mortgage Loan Act[2012 Public Act 67]

• Passed through the Michigan Legislature in record time.• Characterizes inclusion or enforcement of a post-

closing solvency covenant as an unfair trade practice.• Prohibits a post-closing solvency covenant from being

used as a non-recourse carve out.• Applies statue retroactively.• Constitutionality of the Non-recourse Mortgage Loan

Act is under challenge in the state and federal courts inMichigan.

10

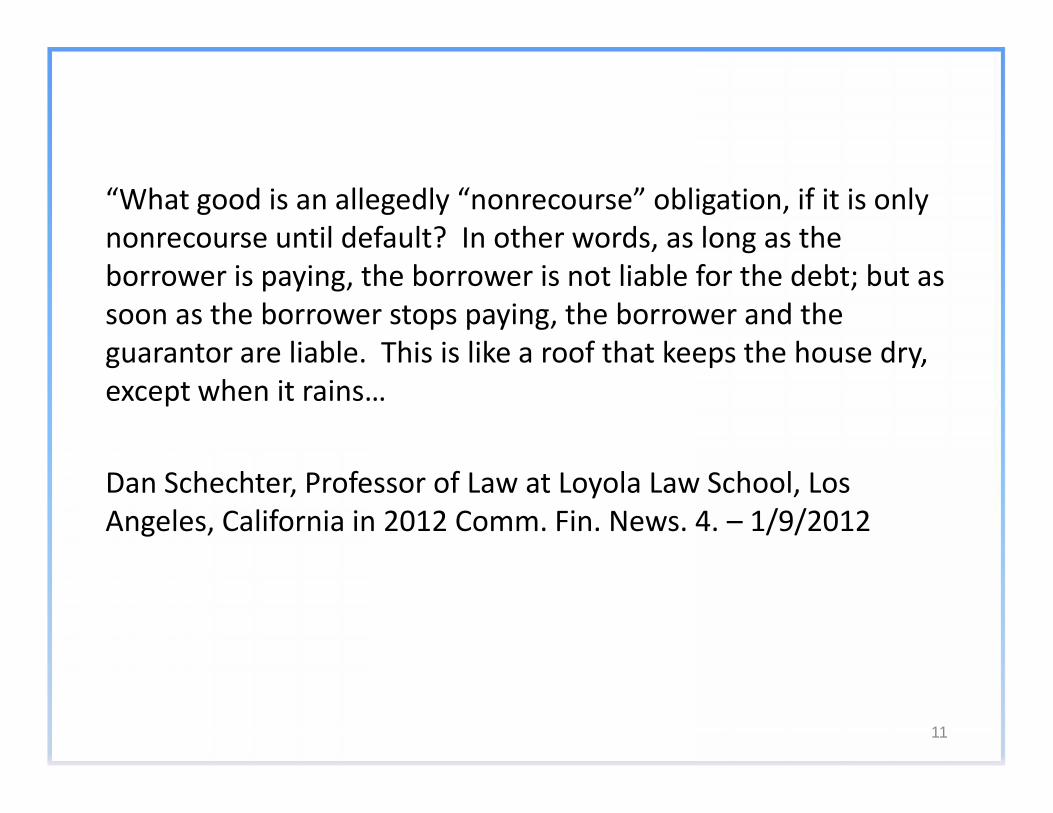

“What good is an allegedly “nonrecourse” obligation, if it is onlynonrecourse until default? In other words, as long as theborrower is paying, the borrower is not liable for the debt; but assoon as the borrower stops paying, the borrower and theguarantor are liable. This is like a roof that keeps the house dry,except when it rains…

Dan Schechter, Professor of Law at Loyola Law School, LosAngeles, California in 2012 Comm. Fin. News. 4. – 1/9/2012

“What good is an allegedly “nonrecourse” obligation, if it is onlynonrecourse until default? In other words, as long as theborrower is paying, the borrower is not liable for the debt; but assoon as the borrower stops paying, the borrower and theguarantor are liable. This is like a roof that keeps the house dry,except when it rains…

Dan Schechter, Professor of Law at Loyola Law School, LosAngeles, California in 2012 Comm. Fin. News. 4. – 1/9/2012

11

RECENT TRENDS IN NON-RECOURSECARVE OUTS

James H. Schwarz, Esq.PartnerBenesch Friedlander Coplan &

Aronoff LLPIndianapolis, IN

12

• Non-recourse loan is a secured loan that allowslenders to attach only to the collateral, and not theborrower’s personal assets, if not repaid.

• It behooves the lawyer to see what constitutes theMortgaged Property.

• If a secured loan is entered into by a specialpurpose entity, by its very nature it is a non-recourse loan.

• Non-recourse loan is a secured loan that allowslenders to attach only to the collateral, and not theborrower’s personal assets, if not repaid.

• It behooves the lawyer to see what constitutes theMortgaged Property.

• If a secured loan is entered into by a specialpurpose entity, by its very nature it is a non-recourse loan.

13

• Borrower expects to be able to walk away from theloan the Mortgaged Property is foreclosed upon.

• Lender needs a way to keep the “deep pocket”principal of the Borrower interested if the MortgagedProperty is falling in value so that the Lender canobtain possession of the Mortgaged Property in aquick and cost efficient manner with no interferenceby the Borrower if an Event of Default exists.

• The solution is to have the “deep pocket” principalenter into a Non-Recourse Carve-Out Guaranty.

• Borrower expects to be able to walk away from theloan the Mortgaged Property is foreclosed upon.

• Lender needs a way to keep the “deep pocket”principal of the Borrower interested if the MortgagedProperty is falling in value so that the Lender canobtain possession of the Mortgaged Property in aquick and cost efficient manner with no interferenceby the Borrower if an Event of Default exists.

• The solution is to have the “deep pocket” principalenter into a Non-Recourse Carve-Out Guaranty.

14

• The “Fatal Four” which cause full recourse springing liability toa Guarantor:

1. Voluntary bankruptcy filing2. Involuntary Bankruptcy caused by collusion between

Borrower and unsecured creditors3. Entry into additional indebtedness4. Making of prohibited transfers

• Failure to maintain Special Purpose Entity Status-Should thisimpose full recourse liability if “no harm no foul”? Is the testa determination by a court that the assets should beconsolidated with an entity that did become bankrupt?

• The “Fatal Four” which cause full recourse springing liability toa Guarantor:

1. Voluntary bankruptcy filing2. Involuntary Bankruptcy caused by collusion between

Borrower and unsecured creditors3. Entry into additional indebtedness4. Making of prohibited transfers

• Failure to maintain Special Purpose Entity Status-Should thisimpose full recourse liability if “no harm no foul”? Is the testa determination by a court that the assets should beconsolidated with an entity that did become bankrupt?

15

Liability limited to actual loss suffered by theLender for certain “bad boy” acts:

1. Fraud or material misrepresentation2. Gross negligence or willful misconduct of

Borrower3. Breach of environmental indemnification4. Misapplication of insurance proceeds or

condemnation awards

Liability limited to actual loss suffered by theLender for certain “bad boy” acts:

1. Fraud or material misrepresentation2. Gross negligence or willful misconduct of

Borrower3. Breach of environmental indemnification4. Misapplication of insurance proceeds or

condemnation awards

16

5. Misapplication of Rents following an Event ofDefault

6. Misapplication of Security Deposits7. Physical waste intentionally caused by Borrower8. Borrower unsuccessfully setting forth a defense

following a monetary Event of Default9. Reimbursement of Enforcement Costs and Expenses

incurred by Lender prior to delivery of possession

5. Misapplication of Rents following an Event ofDefault

6. Misapplication of Security Deposits7. Physical waste intentionally caused by Borrower8. Borrower unsuccessfully setting forth a defense

following a monetary Event of Default9. Reimbursement of Enforcement Costs and Expenses

incurred by Lender prior to delivery of possession

17

Drafting Considerations1. Don’t negotiate the carve-outs in the Loan Documents. Make sure that

they are spelled out in the term sheet.

2. The Guaranty should terminate not when Guaranteed Obligations arefully satisfied but when Loan has been fully paid or fully defeased orwhen foreclosure has been completed.

3. Make sure any Distributions to Members are not subject to claims for“recapture”. Only time when Distributions are at risk should be whenLender has provided written notice to the Borrower than an Event ofDefault exists.

4. As to be discussed, watch out for any language which requires anobligation to maintain adequate capital or not to become insolvent inthe loan covenants.

Drafting Considerations1. Don’t negotiate the carve-outs in the Loan Documents. Make sure that

they are spelled out in the term sheet.

2. The Guaranty should terminate not when Guaranteed Obligations arefully satisfied but when Loan has been fully paid or fully defeased orwhen foreclosure has been completed.

3. Make sure any Distributions to Members are not subject to claims for“recapture”. Only time when Distributions are at risk should be whenLender has provided written notice to the Borrower than an Event ofDefault exists.

4. As to be discussed, watch out for any language which requires anobligation to maintain adequate capital or not to become insolvent inthe loan covenants.

18

Case Study• New Market Center (Borrower) is a

special purpose entity.• Doe & Roe are members and

guarantors.• New Market Center operates a 60,000

square foot shopping center near alarge regional mall.

• New Market Center (Borrower) is aspecial purpose entity.

• Doe & Roe are members andguarantors.

• New Market Center operates a 60,000square foot shopping center near alarge regional mall.

19

20

Case Study

• New Market Center borrowed $5.5 millionwith interest at 7% for 10 years.

• Loan matured December 31, 2011.• Principal balance was $4.8 million at

maturity.• Non-recourse, except for “bad boy” carve

outs.

• New Market Center borrowed $5.5 millionwith interest at 7% for 10 years.

• Loan matured December 31, 2011.• Principal balance was $4.8 million at

maturity.• Non-recourse, except for “bad boy” carve

outs.

21

Case Study

• Loan has hyper-amortizationfeature which extends maturityfor 20 years with interest at 11%per annum and “hard” cash trap.

• Loan has hyper-amortizationfeature which extends maturityfor 20 years with interest at 11%per annum and “hard” cash trap.

22

Case Study

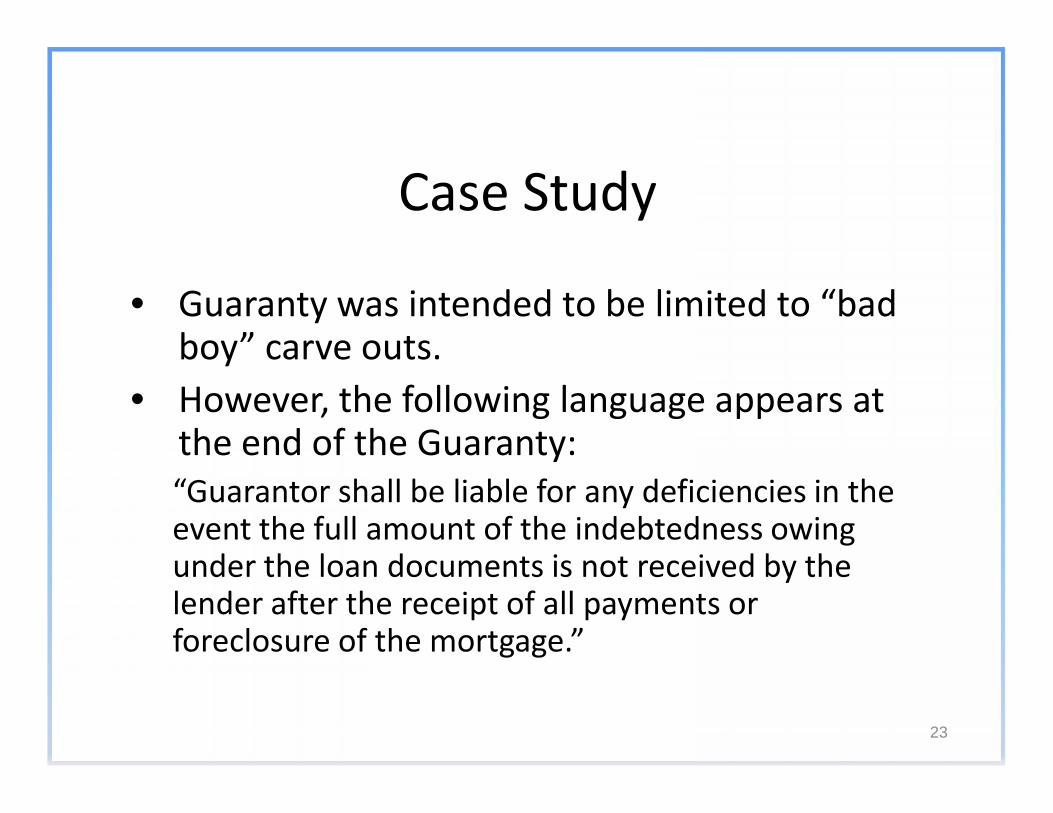

• Guaranty was intended to be limited to “badboy” carve outs.

• However, the following language appears atthe end of the Guaranty:“Guarantor shall be liable for any deficiencies in theevent the full amount of the indebtedness owingunder the loan documents is not received by thelender after the receipt of all payments orforeclosure of the mortgage.”

• Guaranty was intended to be limited to “badboy” carve outs.

• However, the following language appears atthe end of the Guaranty:“Guarantor shall be liable for any deficiencies in theevent the full amount of the indebtedness owingunder the loan documents is not received by thelender after the receipt of all payments orforeclosure of the mortgage.”

23

Case Study• Anchor tenant Short Circuit closed all stores nationally, filed

bankruptcy, and left the center at the end of 2009.• Borrower attempted to re-lease the store to new tenants,

but the servicer refused to approve the proposed tenants.• This resulted in several co-tenancy defaults, all of which

impaired cash flow. Guarantors have made up thedifference to a point.

• Servicer also refused to allow use of a $480,000 leasingreserve escrow to finance improvements proposed for thenew tenants.

• Anchor tenant Short Circuit closed all stores nationally, filedbankruptcy, and left the center at the end of 2009.

• Borrower attempted to re-lease the store to new tenants,but the servicer refused to approve the proposed tenants.

• This resulted in several co-tenancy defaults, all of whichimpaired cash flow. Guarantors have made up thedifference to a point.

• Servicer also refused to allow use of a $480,000 leasingreserve escrow to finance improvements proposed for thenew tenants.

24

Case Study• Guarantors said “enough is enough” and

stopped their capital contributions to theproject.

• Lender has referred the loan to a specialservicer.

• Special servicer has declared a default, andhas sent demand letters to borrower andguarantors.

• General credit conditions do not allowrefinancing at this time.

• Guarantors said “enough is enough” andstopped their capital contributions to theproject.

• Lender has referred the loan to a specialservicer.

• Special servicer has declared a default, andhas sent demand letters to borrower andguarantors.

• General credit conditions do not allowrefinancing at this time.

25

26

Case Study

• Special servicer has obtained an appraisal of theshopping center that sets the value at $2.8 milliondollars.

• Special servicer has commenced a foreclosure actionand scheduled a non-judicial sale.

• Special servicer has indicated it will use the $2.8million dollar appraisal figure as its bid at the non-judicial sale.

• Special servicer has advised guarantors that it will seekto collect the remaining $2 million dollars from themunder their guaranty.

• Special servicer has obtained an appraisal of theshopping center that sets the value at $2.8 milliondollars.

• Special servicer has commenced a foreclosure actionand scheduled a non-judicial sale.

• Special servicer has indicated it will use the $2.8million dollar appraisal figure as its bid at the non-judicial sale.

• Special servicer has advised guarantors that it will seekto collect the remaining $2 million dollars from themunder their guaranty.

27

BANKRUPTCY PERSPECTIVE –POSSIBILITIES AND OPTIONS

Thomas W. Coffey, Esq.Chair, Bankruptcy GroupTucker Ellis LLPCleveland, Ohio

28

1. Best CaseConclude a successful plan of reorganization whereby theremaining first mortgage debt is amortized over the remaining 20year “hyper amortization” period, but at a (lower) current marketinterest rate.

2. Worst CaseProvide for an orderly liquidation in bankruptcy, thus avoiding adistress sale at foreclosure. A liquidation in bankruptcy will (intheory) provide for better market exposure and a dispositionunder better conditions, yielding a higher sales price (and a lowerdeficiency claim against the guarantors).

1. Best CaseConclude a successful plan of reorganization whereby theremaining first mortgage debt is amortized over the remaining 20year “hyper amortization” period, but at a (lower) current marketinterest rate.

2. Worst CaseProvide for an orderly liquidation in bankruptcy, thus avoiding adistress sale at foreclosure. A liquidation in bankruptcy will (intheory) provide for better market exposure and a dispositionunder better conditions, yielding a higher sales price (and a lowerdeficiency claim against the guarantors).

29

3. Benefits

a) Stops a foreclosure sale – the borrower gains time to re-tenant and refinance the property.

b) Gives the borrower more control over the future of theproperty.

c) Postpones the establishment of a deficiency against theguarantors. This may be helpful in a recovering market.

3. Benefits

a) Stops a foreclosure sale – the borrower gains time to re-tenant and refinance the property.

b) Gives the borrower more control over the future of theproperty.

c) Postpones the establishment of a deficiency against theguarantors. This may be helpful in a recovering market.

30

4. Impediments to Reorganization

a) The “bankruptcy remote” provisions in the borrower’sorganizational documents.

b) Relatively few creditors/lack of an “impaired accepting class”of creditors who are not insiders.

c) Single Asset Real Estate provisions in the Code require certainpayments or a plan of reorganization promptly, upon pain ofstay relief.

d) “Bad Faith Filing” issues (not subjective bad faith, butcharacterization of case as dispute with a single creditor)provide an avenue for the lender to seek dismissal of the case.

4. Impediments to Reorganization

a) The “bankruptcy remote” provisions in the borrower’sorganizational documents.

b) Relatively few creditors/lack of an “impaired accepting class”of creditors who are not insiders.

c) Single Asset Real Estate provisions in the Code require certainpayments or a plan of reorganization promptly, upon pain ofstay relief.

d) “Bad Faith Filing” issues (not subjective bad faith, butcharacterization of case as dispute with a single creditor)provide an avenue for the lender to seek dismissal of the case.

31

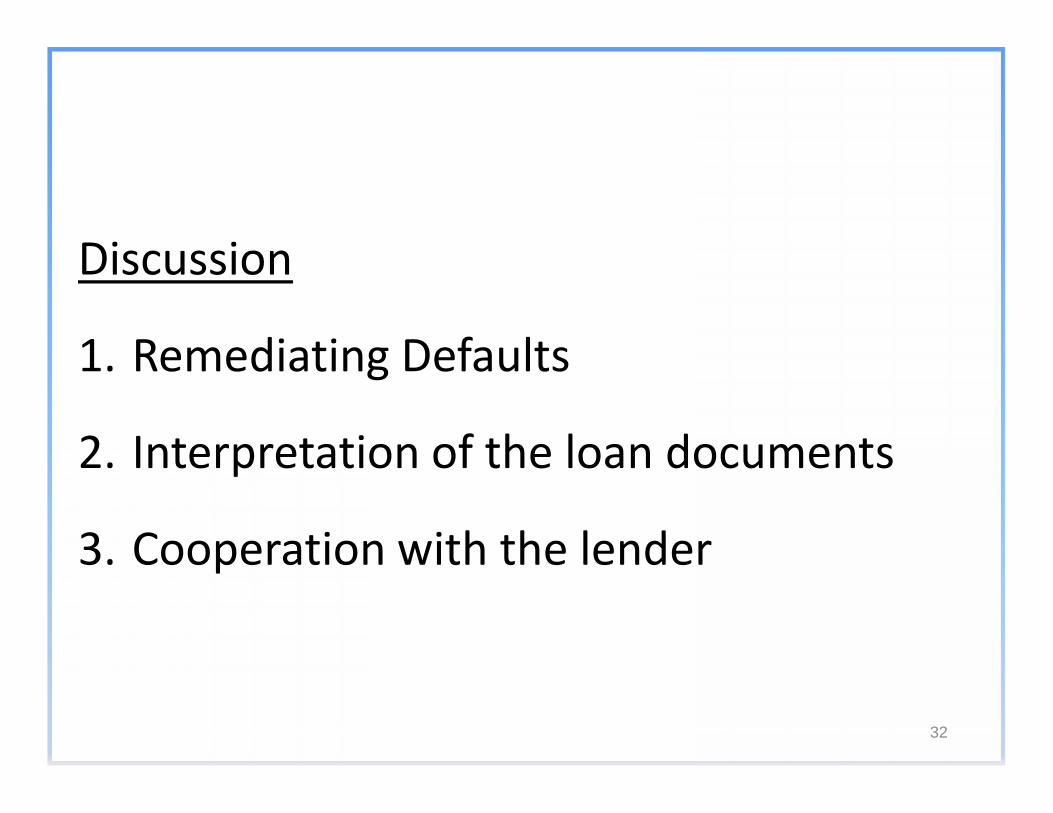

Discussion

1. Remediating Defaults

2. Interpretation of the loan documents

3. Cooperation with the lender

Discussion

1. Remediating Defaults

2. Interpretation of the loan documents

3. Cooperation with the lender

32

Discussion

4. Pre-negotiation agreements

5. Leasing

6. Transfers

Discussion

4. Pre-negotiation agreements

5. Leasing

6. Transfers

33

Discussion

7. Distributions

8. Deficiency Judgment

9. Options for Resolution

Discussion

7. Distributions

8. Deficiency Judgment

9. Options for Resolution

34

Best Course of Actiona. Settlement/Extension?b. Foreclosure/Litigation?c. Bankruptcy?

Best Course of Actiona. Settlement/Extension?b. Foreclosure/Litigation?c. Bankruptcy?

35

Possible Solutions

a) Standing: Determine if the REMIC Trustee “holds” the originalpromissory note and guaranty. The borrower does not want to paytwice!

b) Amend organizational documents.c) Find a class, even if small, of creditors other than the lender.d) Make payment of interest or file a plan in accordance with Section

362(d)(3).e) Move quickly and seize the upper hand with a fast plan and

disclosure statement.f) Obtain a pre-petition loan to:

i. Create a small but independent “impaired accepting class.”ii. Fund shortfall in cash flow to pay interest due the

mortgagee during the Chapter 11 proceeding.

Possible Solutions

a) Standing: Determine if the REMIC Trustee “holds” the originalpromissory note and guaranty. The borrower does not want to paytwice!

b) Amend organizational documents.c) Find a class, even if small, of creditors other than the lender.d) Make payment of interest or file a plan in accordance with Section

362(d)(3).e) Move quickly and seize the upper hand with a fast plan and

disclosure statement.f) Obtain a pre-petition loan to:

i. Create a small but independent “impaired accepting class.”ii. Fund shortfall in cash flow to pay interest due the

mortgagee during the Chapter 11 proceeding.

36

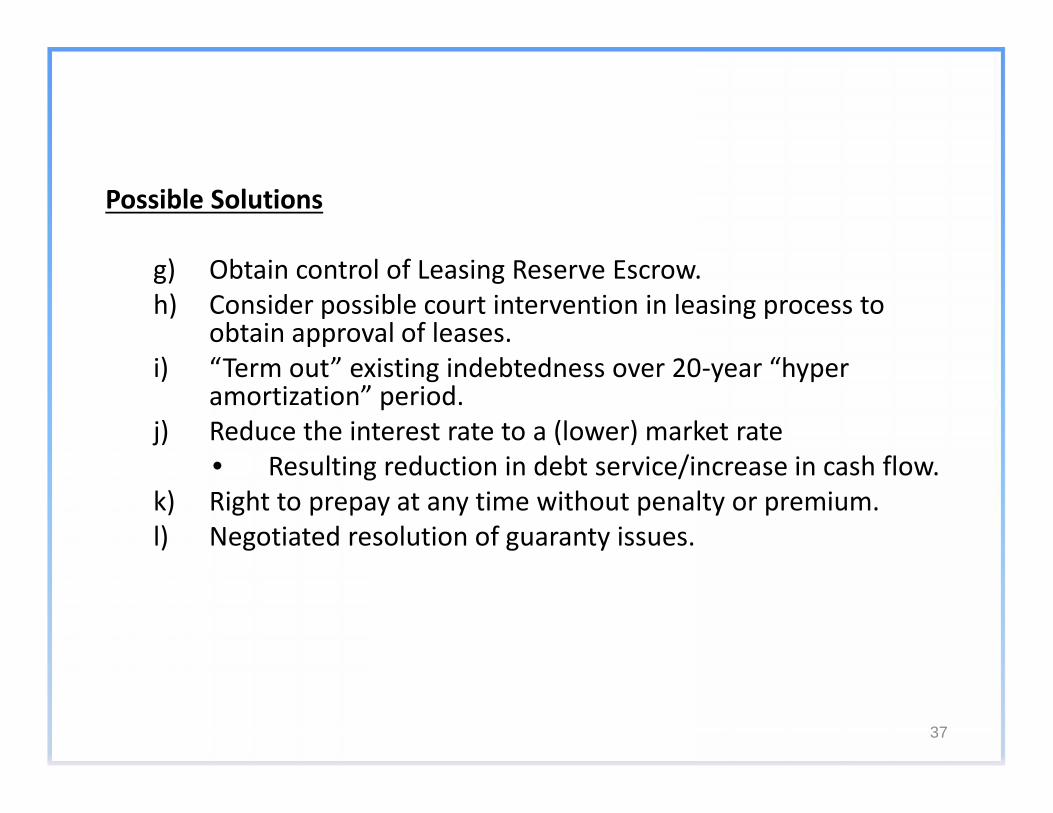

Possible Solutions

g) Obtain control of Leasing Reserve Escrow.h) Consider possible court intervention in leasing process to

obtain approval of leases.i) “Term out” existing indebtedness over 20-year “hyper

amortization” period.j) Reduce the interest rate to a (lower) market rate

• Resulting reduction in debt service/increase in cash flow.k) Right to prepay at any time without penalty or premium.l) Negotiated resolution of guaranty issues.

Possible Solutions

g) Obtain control of Leasing Reserve Escrow.h) Consider possible court intervention in leasing process to

obtain approval of leases.i) “Term out” existing indebtedness over 20-year “hyper

amortization” period.j) Reduce the interest rate to a (lower) market rate

• Resulting reduction in debt service/increase in cash flow.k) Right to prepay at any time without penalty or premium.l) Negotiated resolution of guaranty issues.

37

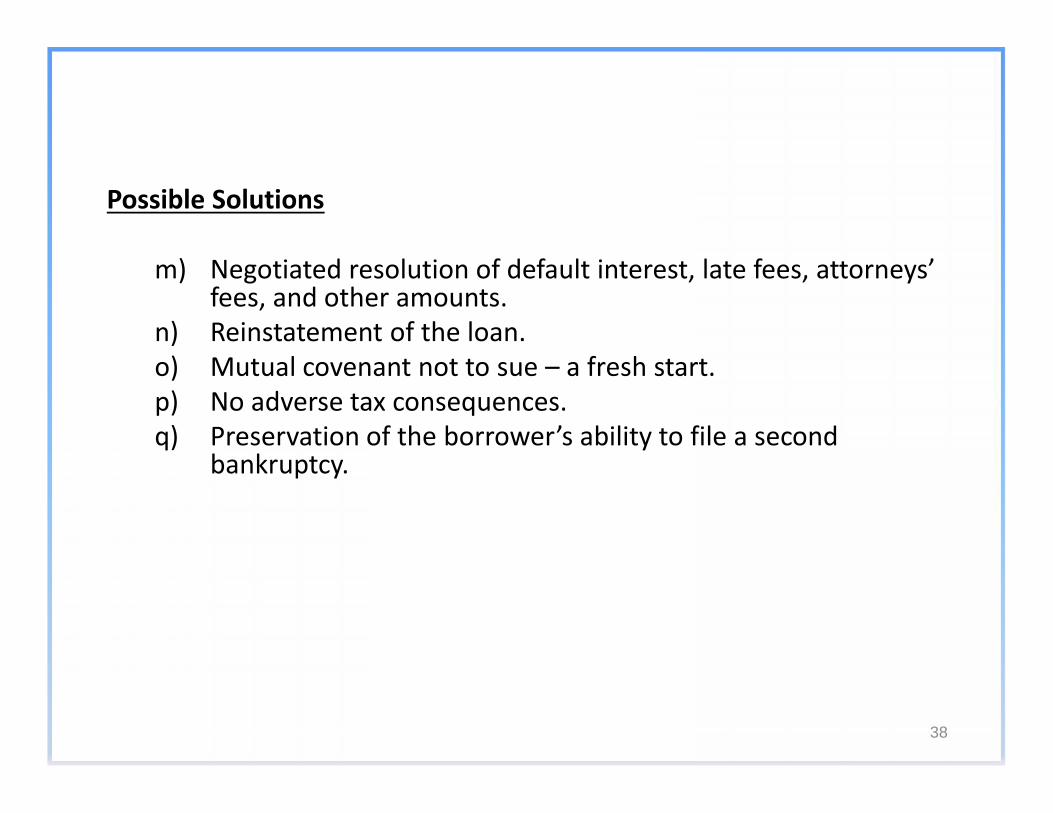

Possible Solutions

m) Negotiated resolution of default interest, late fees, attorneys’fees, and other amounts.

n) Reinstatement of the loan.o) Mutual covenant not to sue – a fresh start.p) No adverse tax consequences.q) Preservation of the borrower’s ability to file a second

bankruptcy.

Possible Solutions

m) Negotiated resolution of default interest, late fees, attorneys’fees, and other amounts.

n) Reinstatement of the loan.o) Mutual covenant not to sue – a fresh start.p) No adverse tax consequences.q) Preservation of the borrower’s ability to file a second

bankruptcy.

38

Bring the Mortgagee to the Table

a) “Cram down” will be objectionable to the mortgagee.b) Dismissal or conversion is very objectionable to the Debtor.c) A wide range of middle ground exists between these two

extremes.d) A consensual plan affords certainty and is appreciated by the

Court.e) Avoiding the cram down fight is so beneficial that it has been

described as the “settlement imperative.”

Bring the Mortgagee to the Table

a) “Cram down” will be objectionable to the mortgagee.b) Dismissal or conversion is very objectionable to the Debtor.c) A wide range of middle ground exists between these two

extremes.d) A consensual plan affords certainty and is appreciated by the

Court.e) Avoiding the cram down fight is so beneficial that it has been

described as the “settlement imperative.”

39

Pro-FormaMarket Center

Pre-Bankruptcy Post-Bankruptcy DifferenceIncome $ 280,476 1 $ 580,000 2 $ 299,524

Expenses $ (161,644) $ (161,644) $ -0-NOI $ 118,832 $ 418,356 $ 299,524Interest $ (350,000) (@7%) $ (294,788) (@5.9%) $ (55,212)Principal $ (121,965) $ (61,784) $ (60,181)Principal $ (121,965) $ (61,784) $ (60,181)Repair and TI Escrows $ (51,180) $ (61,784) $ 10,604

Net $ (404,313) $ -0- $ 404,313

1 Includes Shoe Circus at reduced rent due to failure of co-tenency. Excludes Old Army (expired).

2 Includes Shoe Circus at full rent, new Old Army lease, and new Betty Ann lease.

40

Economic Summary• Borrower keeps the Center;• Cash flow increases by over $400,000;• The value increases by $2.9 Million from

$2.8 to approximately $5.7 Million; and• The Guarantors avoid all liability

Economic Summary• Borrower keeps the Center;• Cash flow increases by over $400,000;• The value increases by $2.9 Million from

$2.8 to approximately $5.7 Million; and• The Guarantors avoid all liability

41

Conclusion

•Practice tipsConclusion

•Practice tips

42

Jim Schwarz

• Don’t negotiate the carve-outs in theLoan Documents. Make sure thatthey are spelled out in the termsheet.

Jim Schwarz

• Don’t negotiate the carve-outs in theLoan Documents. Make sure thatthey are spelled out in the termsheet.

43

Paul Magy

• Get releases upon a deed in lieu.

Paul Magy

• Get releases upon a deed in lieu.

44

Tom Coffey

• Do not do anything that makesanyone else the master of your

destiny.

Tom Coffey

• Do not do anything that makesanyone else the master of your

destiny.

45

QUESTIONS?

Thank you!46