norges bank 1 executive board meeting 26 september 2007

TRANSCRIPT

Norges Bank

1

Executive Board meeting26 September 2007

Norges Bank

0

1

2

3

4

5

6

7

8

9

World NorthAmerica

WesternEurope

Japan Asiaexcl.

Japan

EasternEurope

LatinAmerica

Forecasts August

Forecasts September

0

1

2

3

4

5

6

7

8

9

World NorthAmerica

WesternEurope

Japan Asiaexcl.

Japan

EasternEurope

LatinAmerica

Forecasts August

Forecasts September

Source: Consensus Forecasts

2007 2008

Growth forecasts Consensus ForecastsGDP. Percentage change on previous year

2

Norges Bank

Central bank Date Comment:

Fed

17 AugustThe Fed lowers the discount rate temporarily from 6.25 to 5.75 per cent.

24 AugustIncreases loan terms - up to 30 days. Increase in securities that are accepted as collateral for loans.

18 SeptemberThe Fed lowers the target for the federal funds rate by 0.5 percentage point to 4.75 per cent (there was a slight overweight of expectations for 0.25 percentage point in advance).

ECB23 August Extraordinary 3-month provision of liquidity.

6 SeptemberECB keeps interest rate unchanged (as expected by the majority in the market).

Bank of England

5, 13 and 20 September

Reserve requirements and fluctuation margins are increased several times.

6 SeptemberBoE keeps Bank Rate unchanged (as expected by the majority in the market).

14 and 19 September

BoE offers emergency funding to Northern Rock.

19 SeptemberBoE offers liquidity with a 3-month maturity. Increase in securities that are accepted as collateral for loans.

New measures from central banks (since 15 August)

Norges Bank

4

House prices1) and housing starts in the US Seasonally adjusted. 12-month rise.2) January 2003 – August 2007

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

2003 2004 2005 2006 2007

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

1) Median price for dwellings2) 3-month moving average

Housing starts

Existing dwellings

New dwellings

Sources: Reuters (EcoWin) and Norges Bank

Norges Bank

90

100

110

120

130

140

Nov 06 Jan 07 Mar 07 May 07 Jul 07 Sep 07

90

100

110

120

130

140

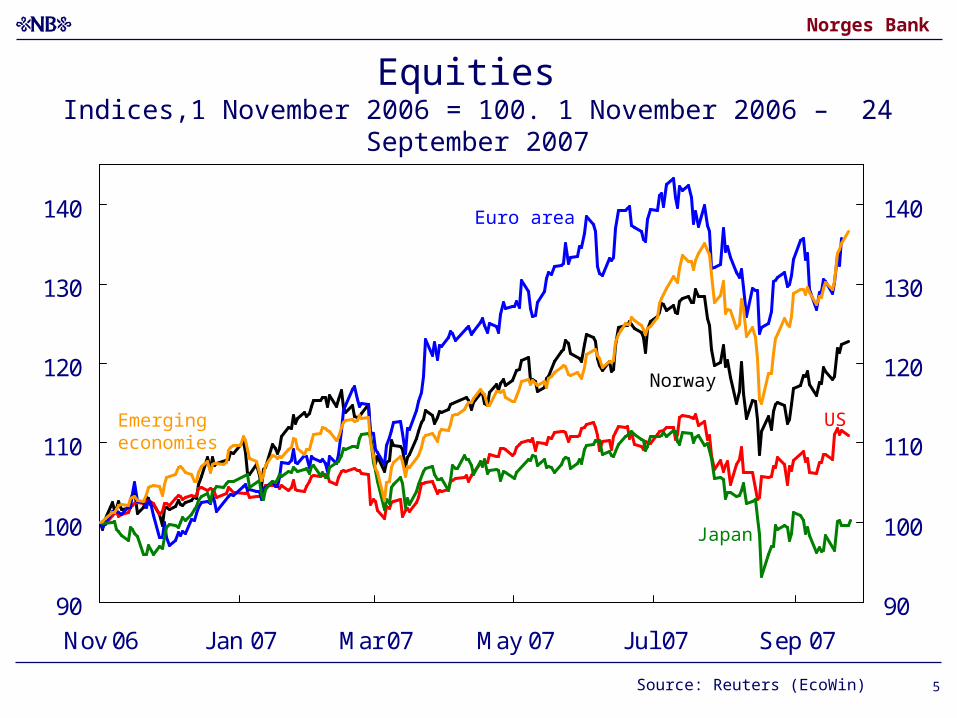

Source: Reuters (EcoWin)

US

Japan

Emerging economies

Norway

Euro area

Equities Indices,1 November 2006 = 100. 1 November 2006 – 24 September 2007

5

Norges Bank

0

1

2

3

4

5

6

Jan 04 Jul 04 Jan 05 Jul 05 Jan 06 Jul 06 Jan 07 Jul 07

0

1

2

3

4

5

6

Credit premium on BBB-rated corporate bonds in the US and Europe and on the debt of emerging economies

Percentage points. 1 January 2004 – 24 September 2007

Source: Reuters (EcoWin)

US

Europe

6

Emerging economies

Norges Bank

Price of hedging credit risk. 5-year CDS prices Basis points. 1 January 2007 – 24 September 2007

Sources: Bloomberg, Reuters and Thomson Datastream 7

0

20

40

60

80

100

120

140

160

180

200

Jan 07 Mar 07 May 07 Jul 07 Sep 07

0

20

40

60

80

100

120

140

160

180

200

DnB NOR

JP Morgan ChaseEuropean banks(Itraxx index)

Citigroup

Bear Stearns

Norges Bank

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Apr 07 May 07 Jun 07 Jul 07 Aug 07 Sep 07

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Difference between money market rates and expected key rate1)

3-month maturity. Percentage points. 1 April – 24 September 2007

Sources: Reuters (EcoWin) and Norges Bank

1) The expected key rate is measured by Overnight Indexed Swap (OIS). 2) Projections. The projections for the past 3 months are based on a market bias towards an interest rate increase in September and December. Prior to this they are based on actual key rates.

US

Euro area

UK

Norway2)

Norges Bank

0

2

4

6

8

Apr 07 May 07 Jun 07 Jul 07 Aug 07 Sep 07

0

2

4

6

8

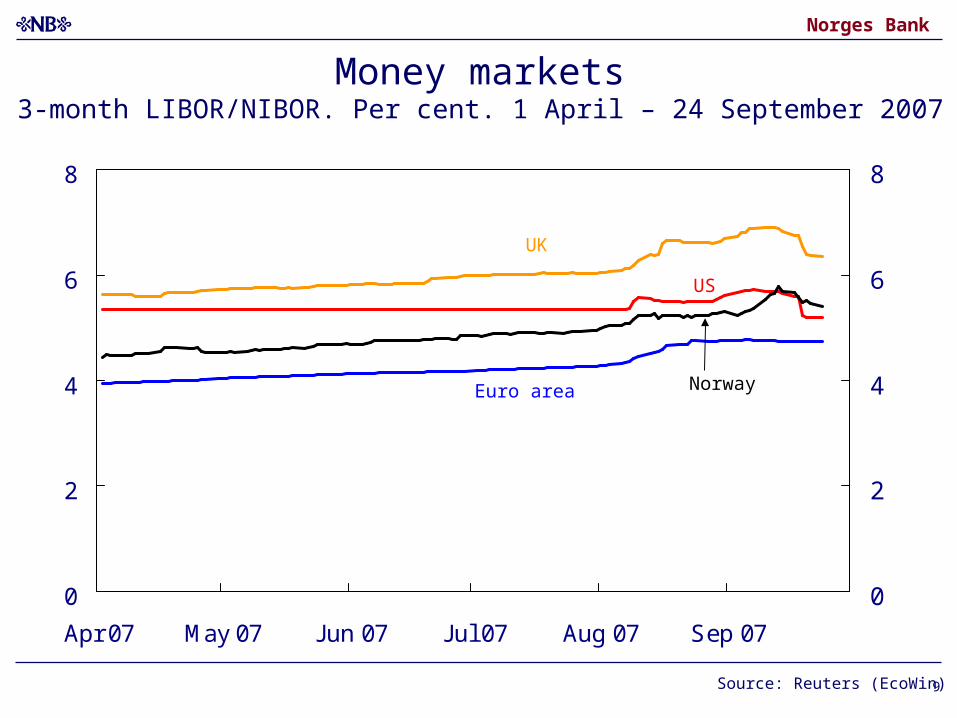

Money markets3-month LIBOR/NIBOR. Per cent. 1 April – 24 September 2007

Source: Reuters (EcoWin) 9

US

NorwayEuro area

UK

Norges Bank

1

2

3

4

5

6

Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10

1

2

3

4

5

6

Norway

US

Euro area

24 September 2007

After previous monetary policy meeting (16 August 2007)

UK

Key rates and forward rates16 August and 24 September 2007

Sources: Reuters (EcoWin), Bloomberg and Norges Bank

Norges Bank

4.0

4.5

5.0

5.5

6.0

6.5

07 Q4 08 Q2 08 Q4 09 Q2 09 Q4 10 Q2 10 Q4

4.0

4.5

5.0

5.5

6.0

6.5

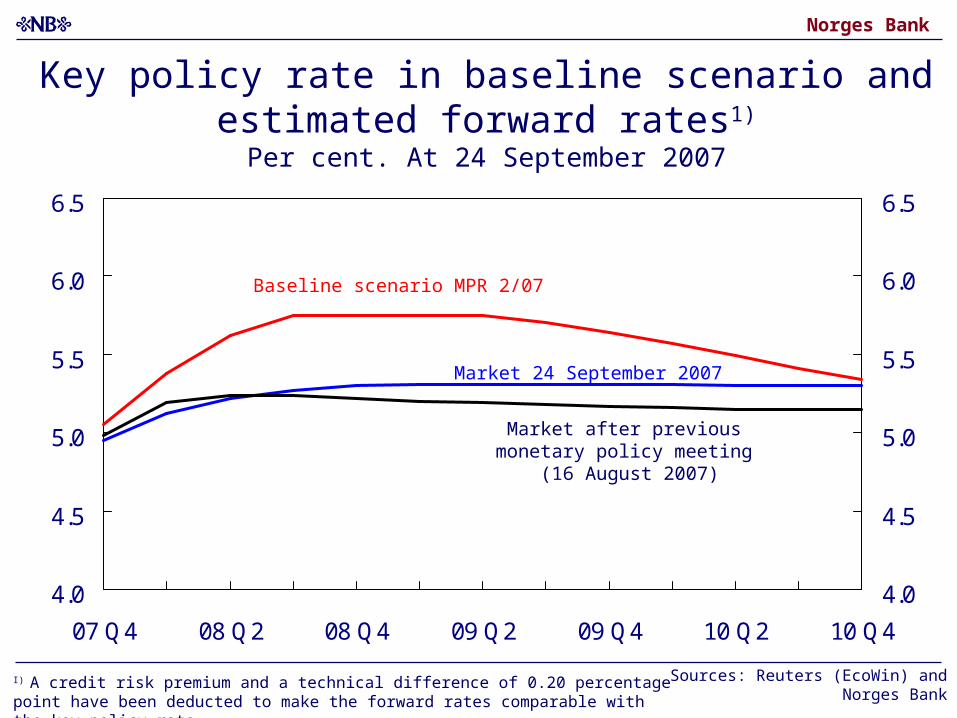

Market 24 September 2007

Market after previous monetary policy meeting

(16 August 2007)

Baseline scenario MPR 2/07

Sources: Reuters (EcoWin) and Norges Bank

Key policy rate in baseline scenario and estimated forward rates1)

Per cent. At 24 September 2007

I) A credit risk premium and a technical difference of 0.20 percentage point have been deducted to make the forward rates comparable with the key policy rate.

Norges Bank

Trading partners' forward rate curve3-month nominal money market rates

Per cent. At 24 September 2007

4

4.5

5

5.5

07 Q4 08 Q2 08 Q4 09 Q2 09 Q4 10 Q2 10 Q4

4

4.5

5

5.5

Baseline scenario MPR 2/07

Market 24 September 2007

Market after previous monetary policy meeting

(16 August 2007)

Sources: Reuters (EcoWin) and Norges Bank

Norges Bank

85

88

91

94

97

100

103

2002 2003 2004 2005 2006 2007 2008 2009 2010

-1

0

1

2

3

4

5

Sources: Bloomberg, Reuters (EcoWin) and Norges Bank

I-44 (left-hand scale)

Weighted interest rate differential (right-hand scale)

24 September 2007

1) A rising curve denotes an appreciation of the krone.

3-month interest rate differential and import-weighted exchange rate (I-44)1)

January 2002 – December 2010

Average 1 - 24 September 2007

After previous monetary policy meeting

(16 August 2007)

13

Norges Bank

14

Inflation and interval for underlying inflation1) 12-month change. Per cent. January 2002 – August 2007

-2

0

2

4

6

2002 2003 2004 2005 2006 2007

-2

0

2

4

6

Highest indicator

Lowest indicator

CPI

Sources: Statistics Norway and Norges Bank

1) Highest and lowest indicator of the CPI-ATE, a weighted median and the trimmed mean of the sub-indices in the CPI.

Inflation target

Norges Bank

-5

-4

-3

-2

-1

0

1

2

3

4

Jul 03 Jan 04 Jul 04 Jan 05 Jul 05 Jan 06 Jul 06 Jan 07 Jul 07

-5

-4

-3

-2

-1

0

1

2

3

4

CPI-ATE1)

Total and broken down into imported and domestically produced goods and services2). Projections from MPR 2/07 (broken line).

12-month change. Per cent

Sources: Statistics Norway and Norges Bank

Goods and services produced in Norway (0.7)

Imported consumer goods (0.3)

CPI-ATE

1) CPI adjusted for tax changes and excluding energy products. A further adjustment is made for estimated effect of reduced maximum day-care prices in 2006.2) Norges Bank's projections.

Norges Bank

16

2200

2250

2300

2350

2400

2450

2500

2550

1999 2001 2003 2005 2007 1999 2001 2003 2005 2007

0

2

4

6

Sources: Statistics Norway and Norwegian Labour and Welfare Organisation (NAV)

Labour market

1) The changes to the LFS have resulted in a break in the time series between 2005 and 2006.

LFS unemployment

Registered unemployed

EmploymentIn 1000s

UnemploymentPer cent. Seasonally adjusted

LFS1)

QNA

Norges Bank

Investment intentions survey. Petroleum activitiesEstimated and actual investment. In billions of NOK

2007

2003

2004

2005

2006

Estimate made previous year Final figuresEstimate made current year

Source: Statistics Norway

2008

50

60

70

80

90

100

110

120

May Aug Nov Feb May Aug Nov Feb

50

60

70

80

90

100

110

120

Norges Bank

Investment intentions survey. ManufacturingEstimated and actual investment. In billions of NOK

Source: Statistics Norway

2007

2003

2004

2005

2006

Estimate made previous year Final figuresEstimate made current year

2008

10

15

20

25

30

May Aug Nov Feb May Aug Nov Feb

10

15

20

25

30

Norges Bank

Index of commodity consumption Volume. Seasonally adjusted. January 2000 – July 2007

100

110

120

130

140

150

160

2000 2001 2002 2003 2004 2005 2006 2007

100

110

120

130

140

150

160

Sources: Statistics Norway and Norges Bank 19

Norges Bank

Unit labour costs in mainland Norway 4-quarter rise. Smoothed. Per cent. 1996 Q1 - 2007 Q2

-2

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

-2

0

2

4

6

8

Sources: Statistics Norway and Norges Bank

Norges Bank

Wage share1)

Per cent. 1996 – 2006

60

65

70

75

1996 1998 2000 2002 2004 2006

60

65

70

75

Sources: Statistics Norway and Norges Bank1) Labour costs as a share of factor income. Market-oriented mainland industry.

Norges Bank

Enterprise sector credit1) and liquid assets2) 12-month growth3). Per cent. January 2000 – July 2007 (C3 to June)

-5

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007

-5

0

5

10

15

20

25

30

35

40

Source: Statistics Norway

Total credit (C3)

Money supply (M2)

1) Mainland non-financial enterprises (C3).2) Non-financial enterprises' liquid assets (M2).3) Transaction-based growth estimate.

22

Norges Bank

23

House prices and household debtChange on same month/quarter previous year. Per cent.

January 2001 – August 2007 (C2 to July)

-5

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007

0

2

4

6

8

10

12

14

2001 2002 2003 2004 2005 2006 2007

House prices Debt

Sources: Norwegian Association of Real Estate Agents, Association of Real Estate Agency Firms, Finn.no, ECON, Statistics Norway and Norges Bank

Real estate business

Statistics Norway

C2

Norges Bank

0

1

2

3

4

5

6

7

8

9

2005 2006 2007 2008 2009 2010

0

1

2

3

4

5

6

7

8

9

1/053/04

2/053/05

1/062/06

3/06

2/07

1/07

Key rate

Source: Norges Bank

MPR 2/07Strategy interval

Interest rate decision 15 August

Norges Bank

25

Monetary policy strategy

• The interest rate path presented in MPR 2/07 reflects the Executive

Board's trade-off between bringing inflation up to target and stabilising

developments in output and employment.

• In the light of this trade-off, the interest rate will be increased

gradually so that we can assess the effects of interest rate changes

and other new information on economic developments. Given the

inflation target, we will be mindful of the effects of higher interest rates

on the krone exchange rate when inflation is low.

• The key policy rate should lie in the interval 4½ – 5½% in the period

to the publication of the next Report on 31 October 2007, conditional

on economic developments that are broadly in line with the

projections.

Monetary Policy Report 2/07