november 6, 2009

DESCRIPTION

CCIM. November 6, 2009. Dr. Loren C. Scott Loren C. Scott & Associates, Inc. www.lorencscottassociates.com. The National Economy. Recession (NOT Depression) Environment. RGDP Forecasts(10/09). Quarter Moody’s Consensus 08-I -0.7 -0.7 08-II 1.5% 1.5% - PowerPoint PPT PresentationTRANSCRIPT

November 6, 2009

Dr. Loren C. ScottLoren C. Scott & Associates, Inc.www.lorencscottassociates.com

The National Economy

Recession (NOT Depression) Environment

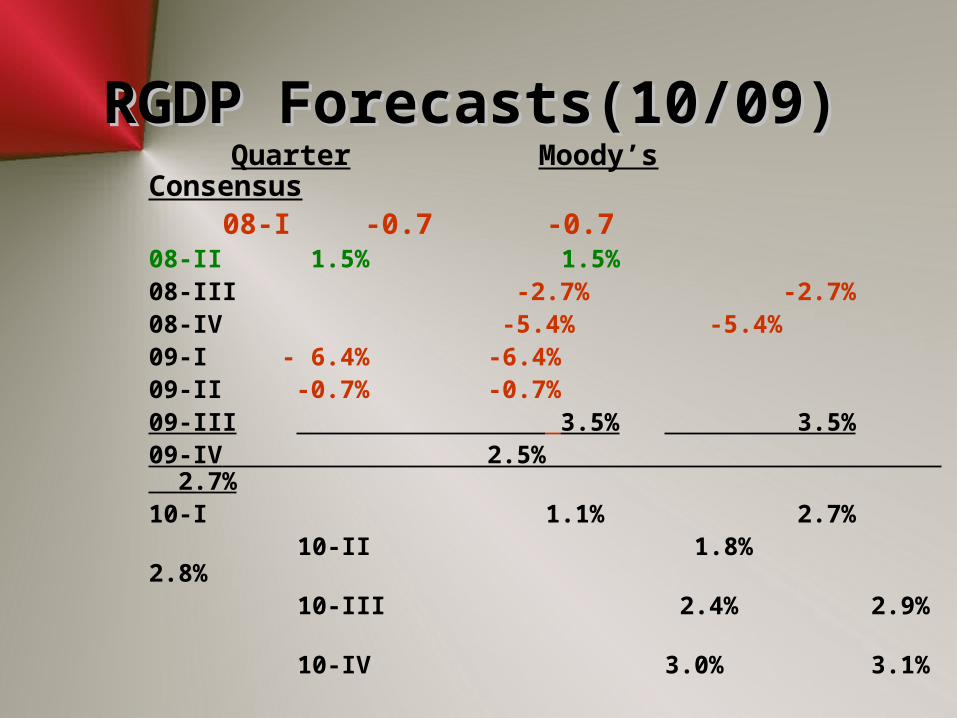

RGDP Forecasts(10/09)RGDP Forecasts(10/09) Quarter Moody’s Consensus

08-I -0.7 -0.708-II 1.5% 1.5%08-III -2.7% -2.7% 08-IV -5.4% -5.4%09-I - 6.4% -6.4%09-II -0.7% -0.7%09-III 3.5% 3.5%09-IV 2.5% 2.7%10-I 1.1% 2.7%

10-II 1.8% 2.8% 10-III 2.4% 2.9% 10-IV 3.0% 3.1%

RGDP Forecasts(10/09)RGDP Forecasts(10/09) Quarter Moody’s Consensus

08-I -0.7 -0.708-II 1.5% 1.5%08-III -2.7% -2.7% 08-IV -5.4% -5.4%09-I - 6.4% -6.4%09-II -0.7% -0.7%09-III 3.5% 3.5%09-IV 2.5% 2.7%10-I 1.1% 2.7%

10-II 1.8% 2.8% 10-III 2.4% 2.9% 10-IV 3.0% 3.1%

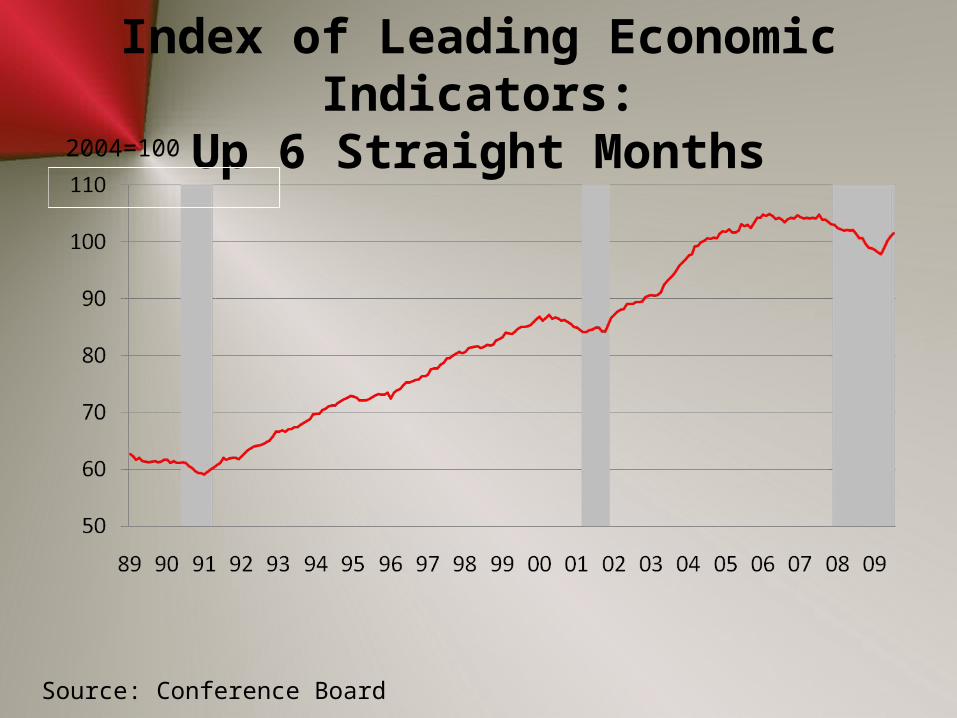

Index of Leading Economic Indicators:Up 6 Straight Months

Source: Conference Board

2004=100

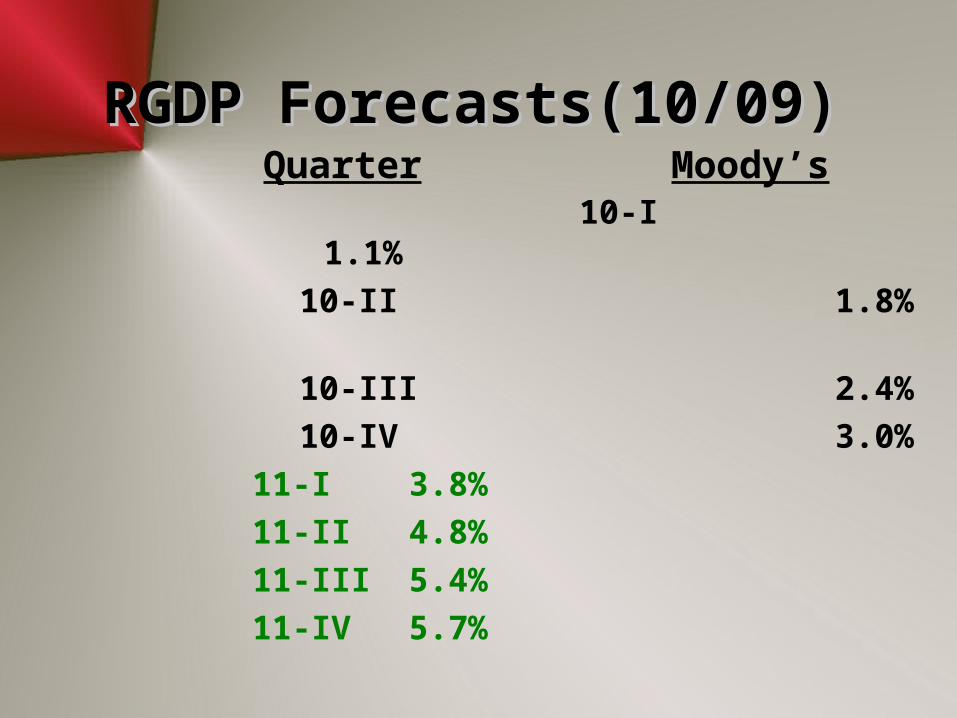

RGDP Forecasts(10/09)RGDP Forecasts(10/09) Quarter Moody’s

10-I 1.1%

10-II 1.8%

10-III 2.4%

10-IV 3.0%

11-I 3.8%

11-II 4.8%

11-III 5.4%

11-IV 5.7%

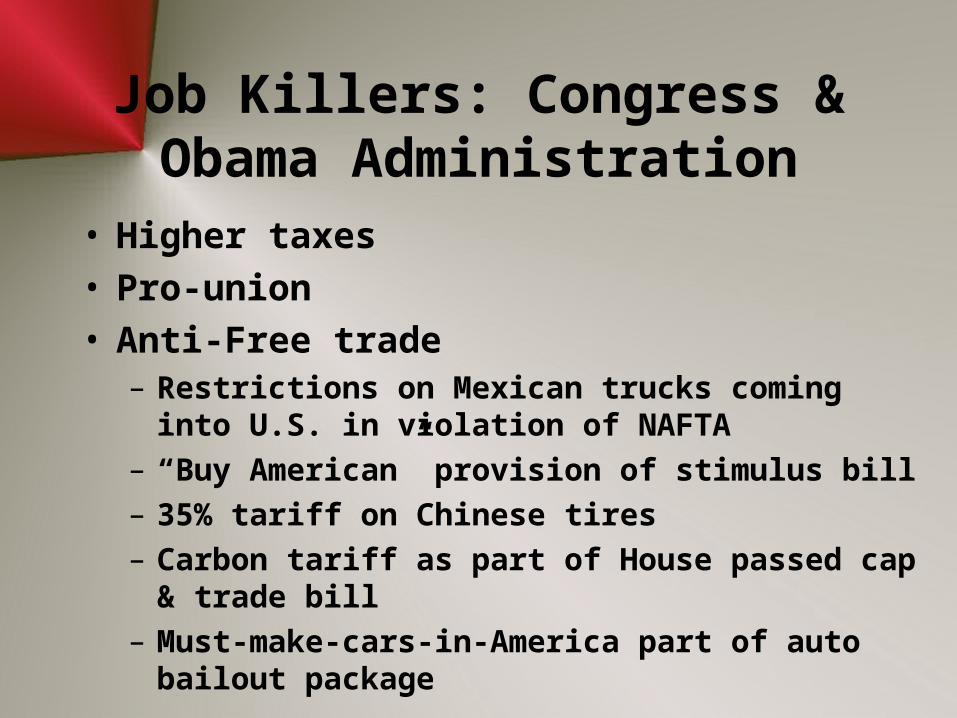

Job Killers: Congress & Obama Administration

• Higher taxes• Pro-union• Anti-Free trade

– Restrictions on Mexican trucks coming into U.S. in violation of NAFTA

– “Buy American” provision of stimulus bill

– 35% tariff on Chinese tires

– Carbon tariff as part of House passed cap & trade bill

– Must-make-cars-in-America part of auto bailout package

Add tariffs: Guess what always happens?

Retaliation!

Job Killers:Congress & Obama

Administration

• Higher taxes

• Pro-union

• Anti-Free trade

• Extreme pro-green

• More regulation

• Government-run health care

Wait Times? What Will America Tolerate?

AVERAGE WAIT TIMES: U.S. versus Canada

Type of Appointment

U.S. Wait Times Canada Wait

Times (requires referral)

Cardiologist 15.5 Days 51.1 Days

Orthopedic Surgeon

16.8 Days 256.9 Days

Family Practice Visit

20.5 Days 31.7 Days

Dermatology 22.1 Days 121.1 Days

OB-GYN 27.5 Days 112.7 Days

NOTE:

English National Health Service

(NHS) and Department of

Health (DH) have set TARGETED

WAIT TIMES of 18 weeks (126 days) for all specialist

appointments and hospital

treatments.

As of 1/1/2009, they were well

short of this goal.

Four NBER Indicators

-800

-400

0

400

800

1200

1980 1985 1990 1995 2000 2005

Fig. 1: Monthly Change in US Employment

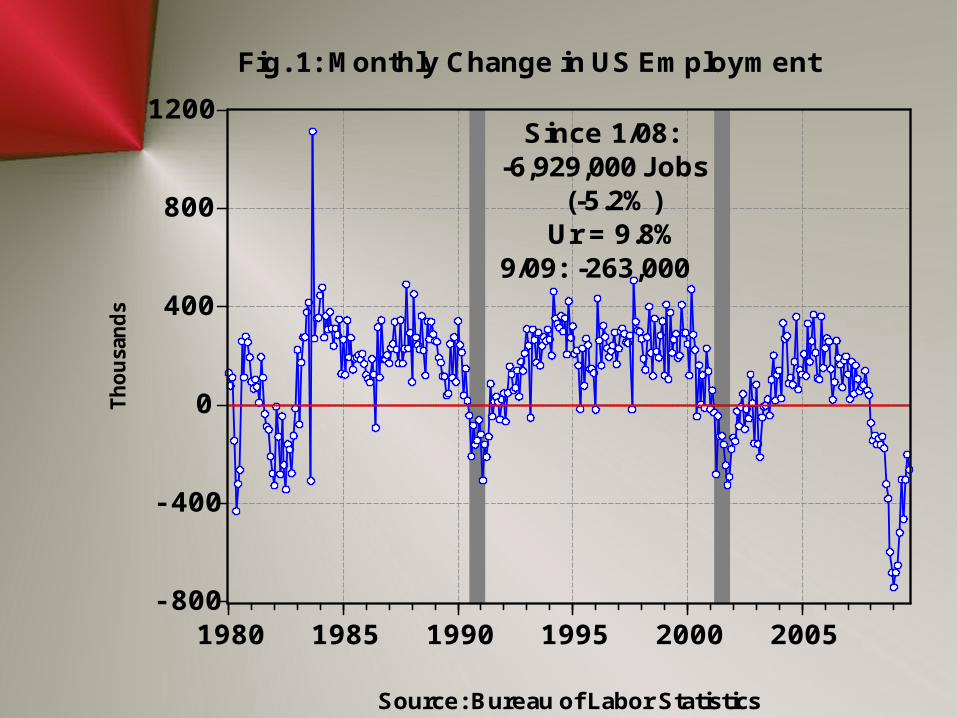

Source: Bureau of Labor Statistics

Since 1/08:-6,929,000 Jobs (-5.2%) Ur = 9.8%9/09: -263,000

Th

ou

san

ds

50

60

70

80

90

100

110

120

1980 1985 1990 1995 2000 2005

U.S. Industrial Production Index20

02=

100

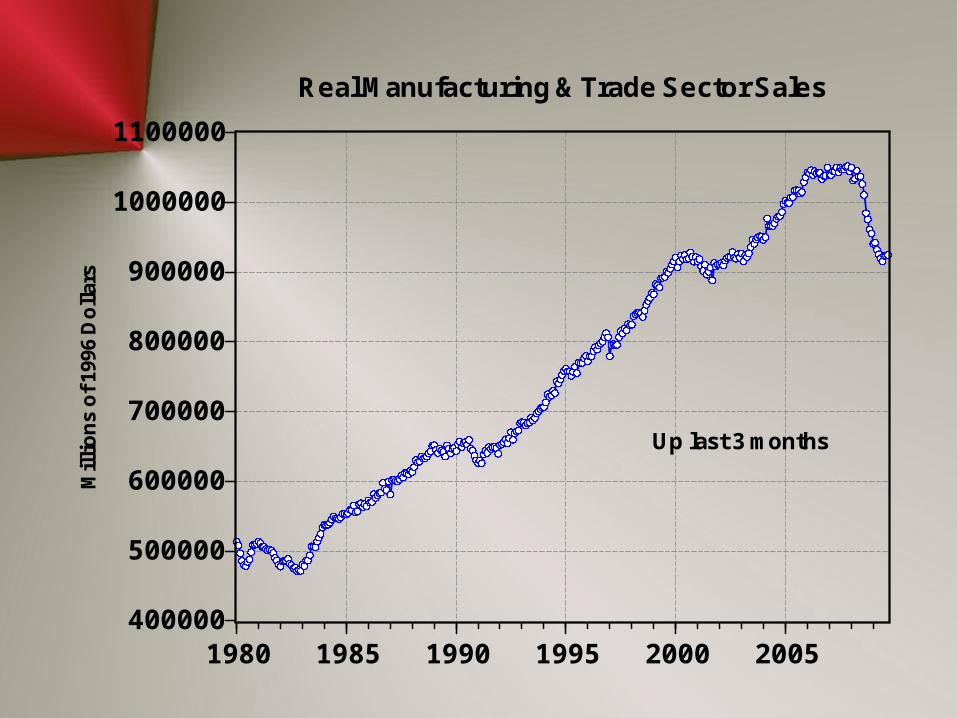

Up last 3 months

400000

500000

600000

700000

800000

900000

1000000

1100000

1980 1985 1990 1995 2000 2005

Real Manufacturing & Trade Sector SalesM

illi

on

s o

f 199

6 D

oll

ars

Up last 3 months

4000

5000

6000

7000

8000

9000

10000

1980 1985 1990 1995 2000 2005

Fig. 5: Real Personal Income Minus Transfer PaymentsB

illi

on

s o

f 20

00 D

oll

ars

Up 2 of last 3 months

Another Big Problem

The credit crunch

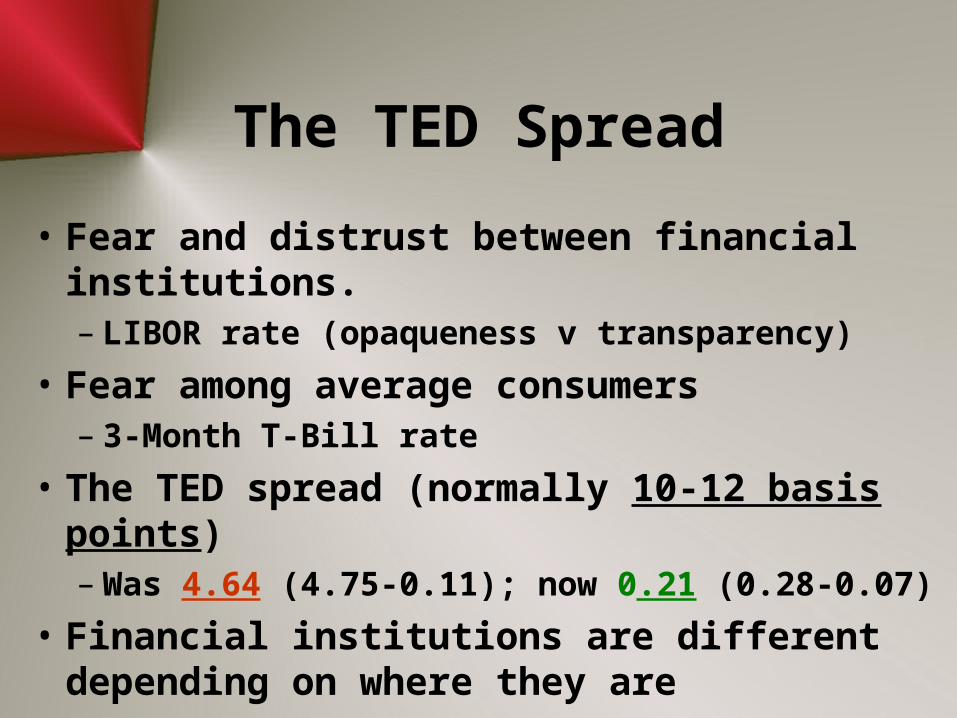

The TED Spread

• Fear and distrust between financial institutions.– LIBOR rate (opaqueness v transparency)

• Fear among average consumers– 3-Month T-Bill rate

• The TED spread (normally 10-12 basis points)– Was 4.64 (4.75-0.11); now 0.21 (0.28-0.07)

• Financial institutions are different depending on where they are

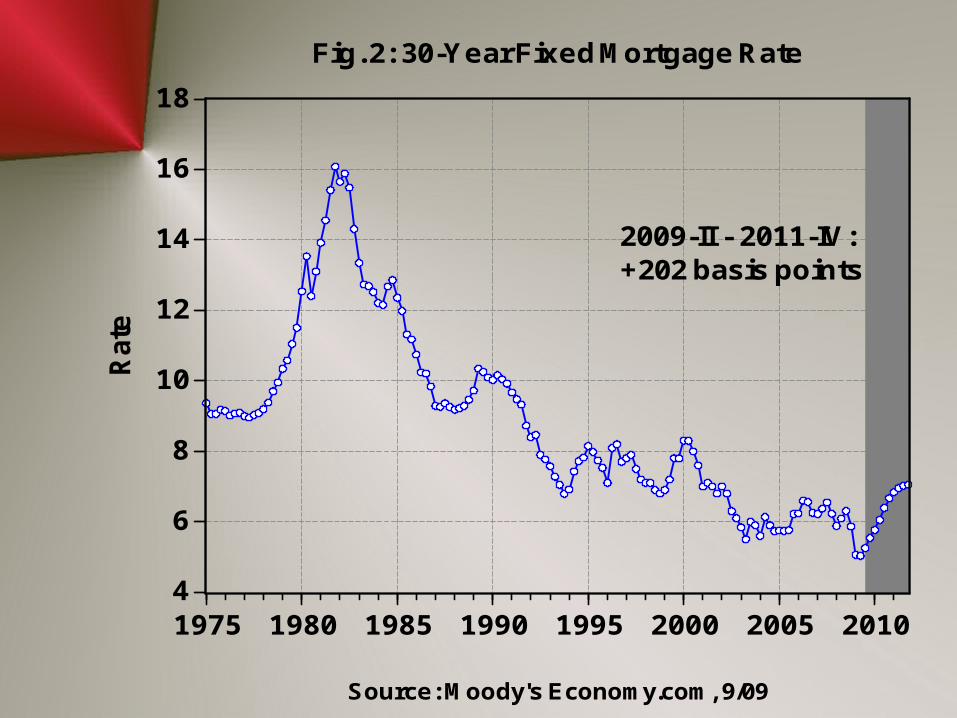

Interest Rates Still Favorable

4

6

8

10

12

14

16

18

1975 1980 1985 1990 1995 2000 2005 2010

Fig. 2: 30-Year Fixed Mortgage Rate

2009-II - 2011-IV:+202 basis points

Source: Moody's Economy.com, 9/09

Rate

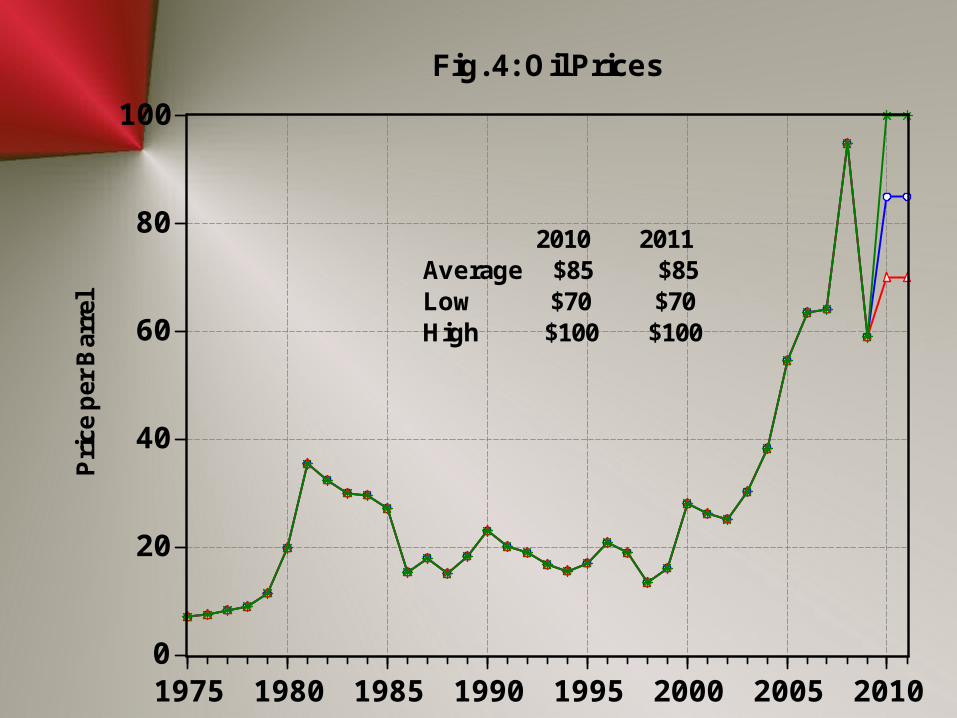

Oil Price Forecasts

The “Onagistic” Approach

0

20

40

60

80

100

1975 1980 1985 1990 1995 2000 2005 2010

Fig. 4: Oil PricesP

rice

per

Bar

rel

2010 2011Average $85 $85Low $70 $70High $100 $100

20

40

60

80

100

120

140

50 100 150 200 250

Pri

ce p

er B

arre

l

1/2/04 to 1/23/09

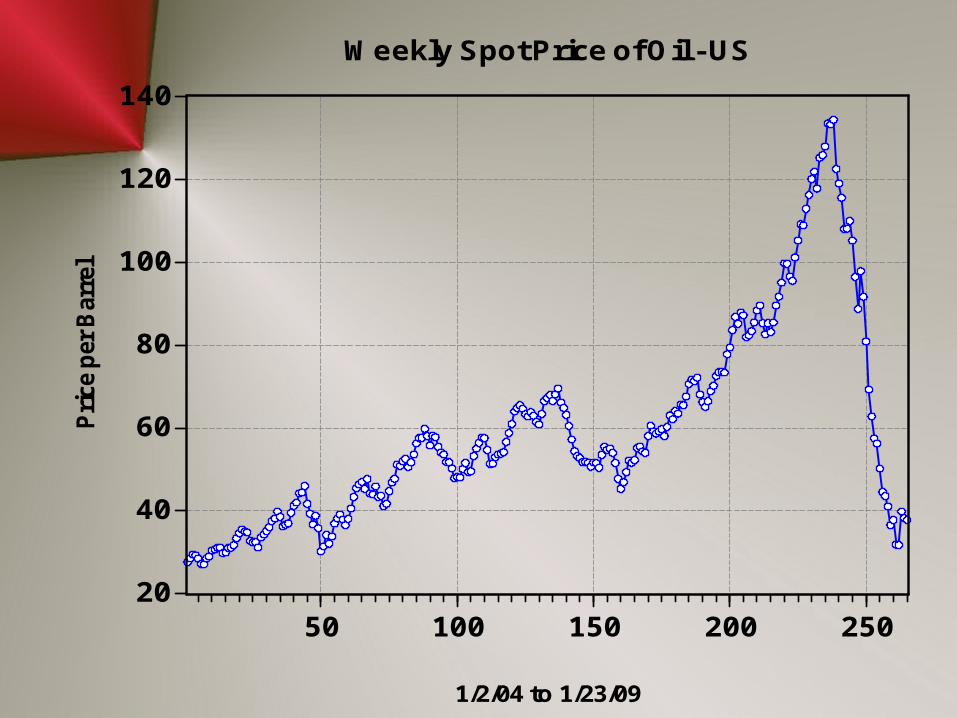

Weekly Spot Price of Oil - US

0

2

4

6

8

10

1975 1980 1985 1990 1995 2000 2005 2010

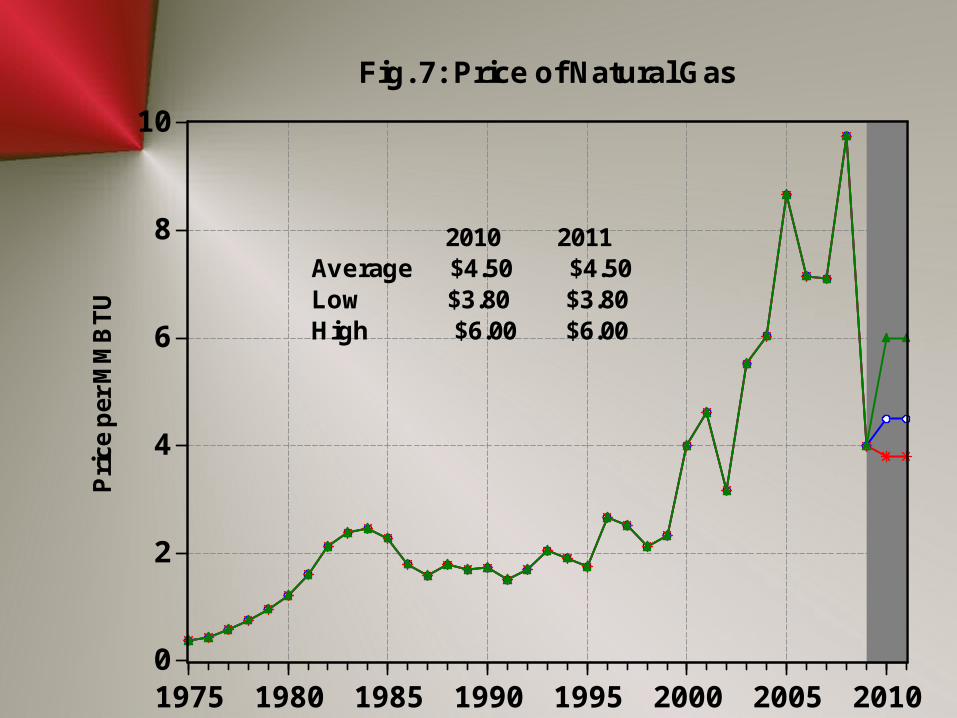

Fig. 7: Price of Natural GasP

rice

per

MM

BT

U

2010 2011Average $4.50 $4.50Low $3.80 $3.80High $6.00 $6.00

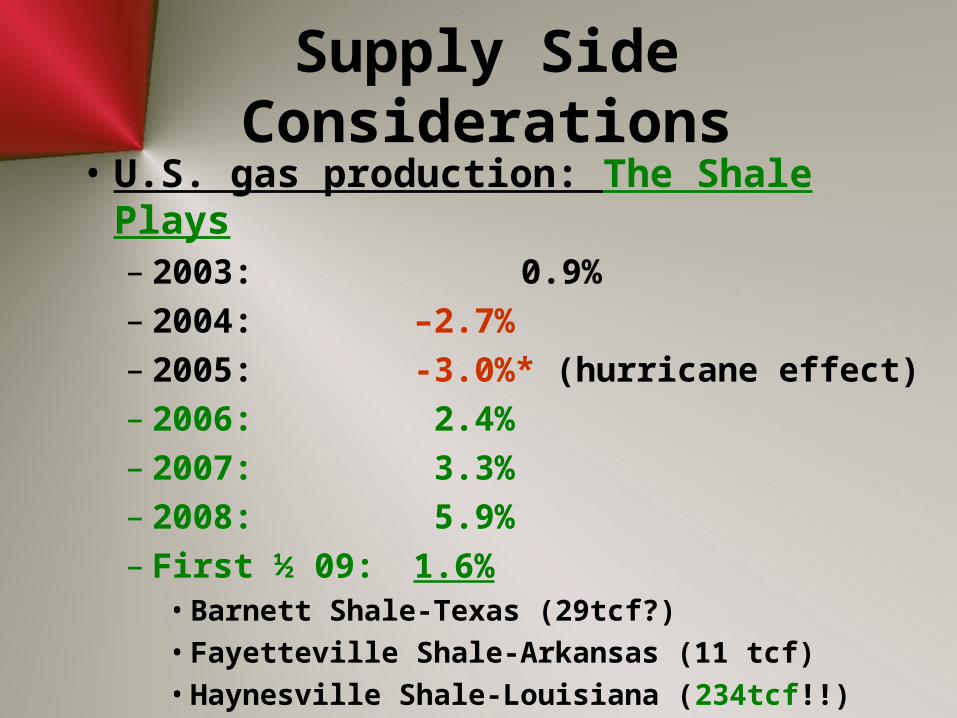

Supply Side Considerations

• U.S. gas production: The Shale Plays– 2003: 0.9%– 2004: –2.7%– 2005: -3.0%* (hurricane effect)– 2006: 2.4%– 2007: 3.3%– 2008: 5.9%– First ½ 09: 1.6%

• Barnett Shale-Texas (29tcf?)

• Fayetteville Shale-Arkansas (11 tcf)

• Haynesville Shale-Louisiana (234tcf!!)

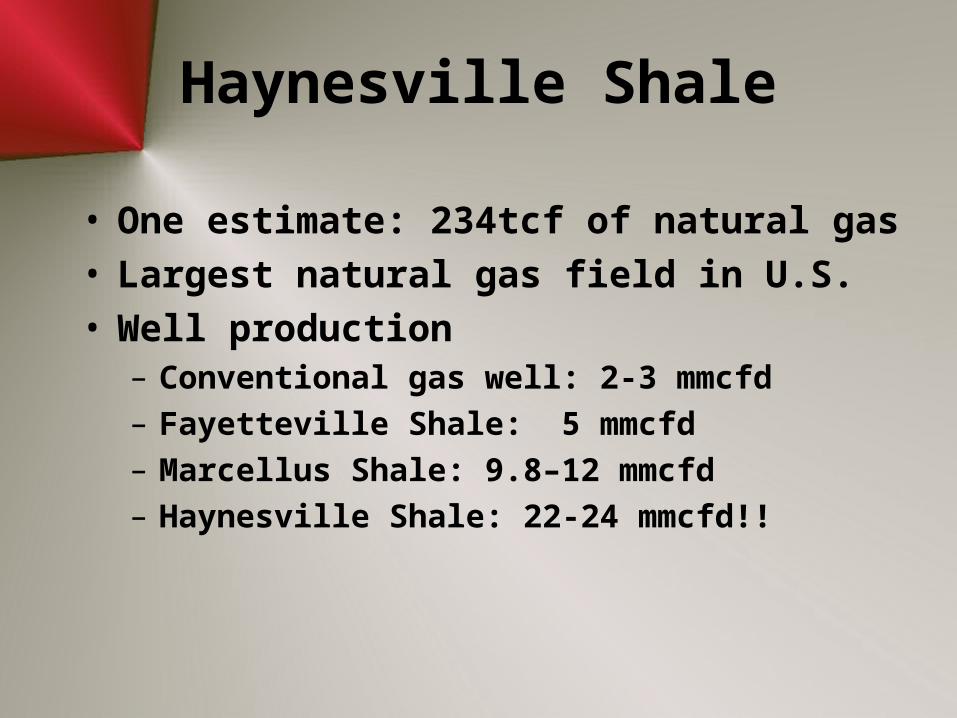

Haynesville Shale

• One estimate: 234tcf of natural gas• Largest natural gas field in U.S.• Well production

– Conventional gas well: 2-3 mmcfd

– Fayetteville Shale: 5 mmcfd

– Marcellus Shale: 9.8–12 mmcfd

– Haynesville Shale: 22-24 mmcfd!!

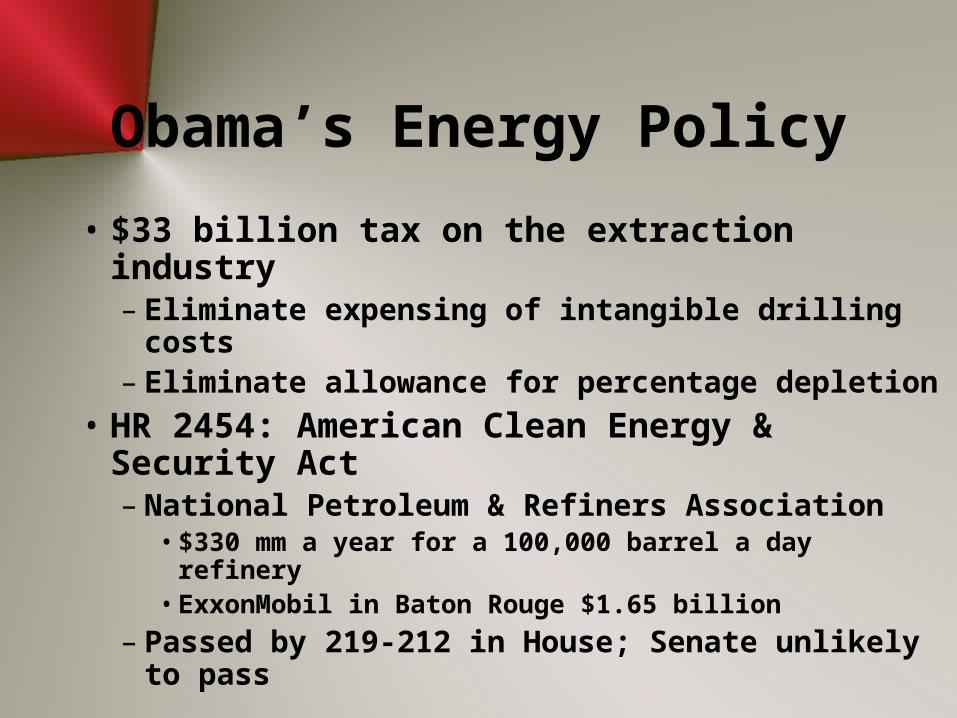

Obama’s Energy Policy

• $33 billion tax on the extraction industry– Eliminate expensing of intangible drilling costs– Eliminate allowance for percentage depletion

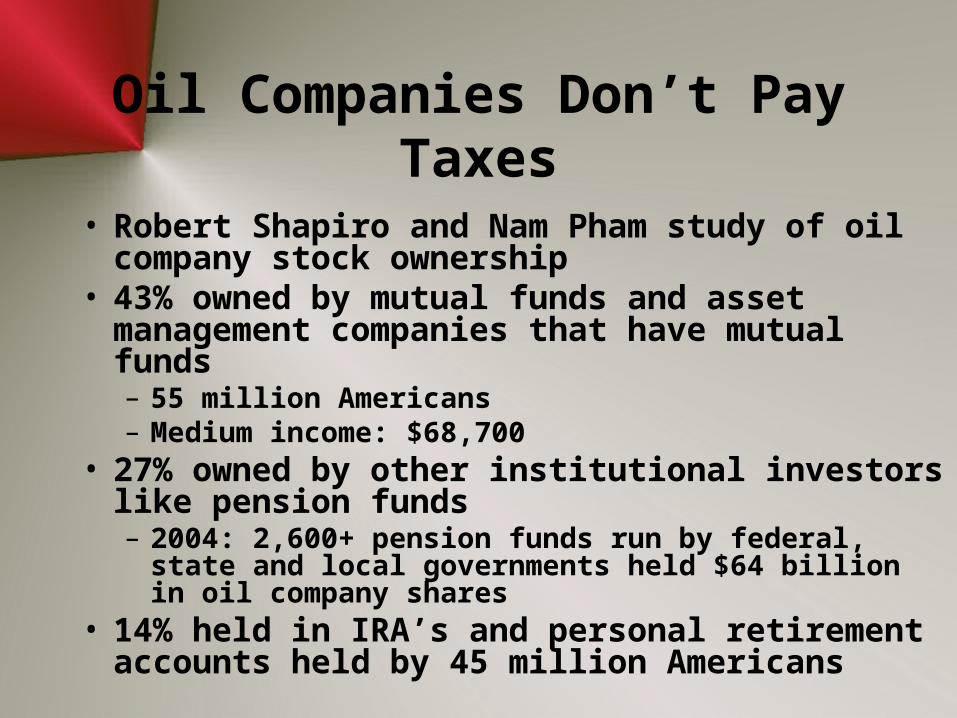

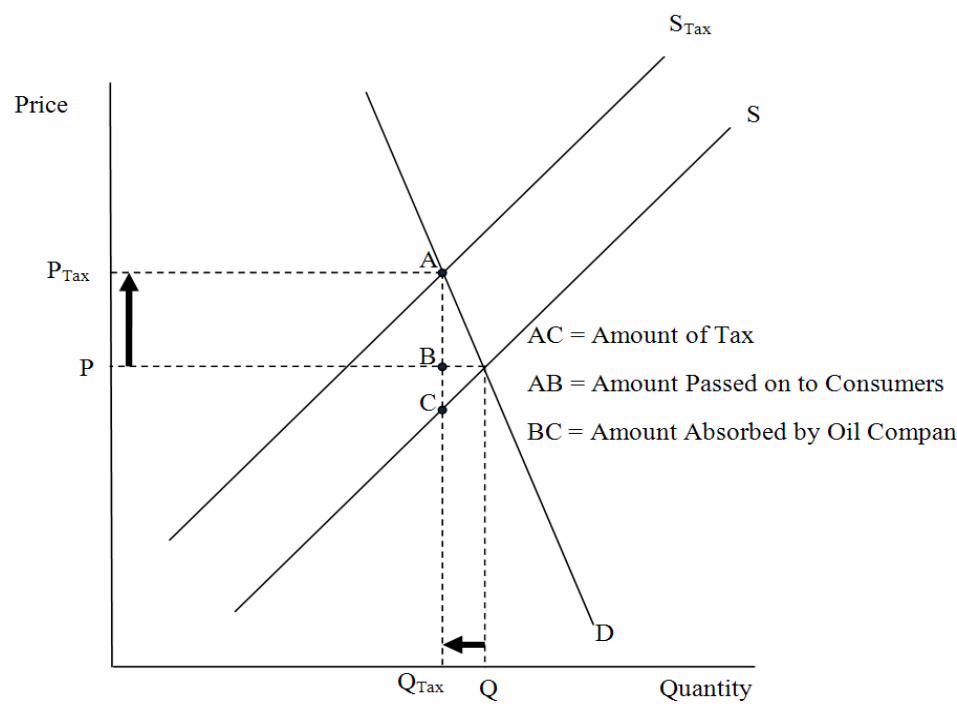

Oil Companies Don’t Pay Taxes

• Robert Shapiro and Nam Pham study of oil company stock ownership

• 43% owned by mutual funds and asset management companies that have mutual funds– 55 million Americans– Medium income: $68,700

• 27% owned by other institutional investors like pension funds– 2004: 2,600+ pension funds run by federal, state and local

governments held $64 billion in oil company shares• 14% held in IRA’s and personal retirement

accounts held by 45 million Americans

120

130

140

150

160

170

180

190

200

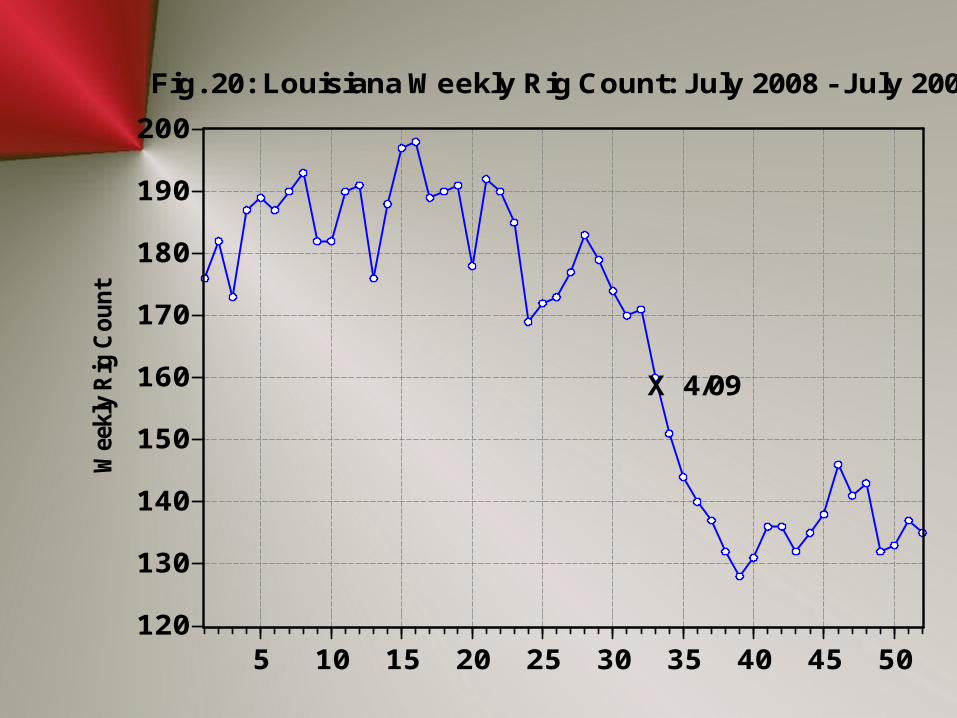

5 10 15 20 25 30 35 40 45 50

X 4/09

Fig. 20: Louisiana Weekly Rig Count: July 2008 - July 2009W

eekl

y R

ig C

ount

Obama’s Energy Policy

• $33 billion tax on the extraction industry– Eliminate expensing of intangible drilling costs– Eliminate allowance for percentage depletion

• HR 2454: American Clean Energy & Security Act– National Petroleum & Refiners Association

• $330 mm a year for a 100,000 barrel a day refinery• ExxonMobil in Baton Rouge $1.65 billion

– Passed by 219-212 in House; Senate unlikely to pass

New Orleans

460

480

500

520

540

560

580

600

620

1980 1985 1990 1995 2000 2005 2010

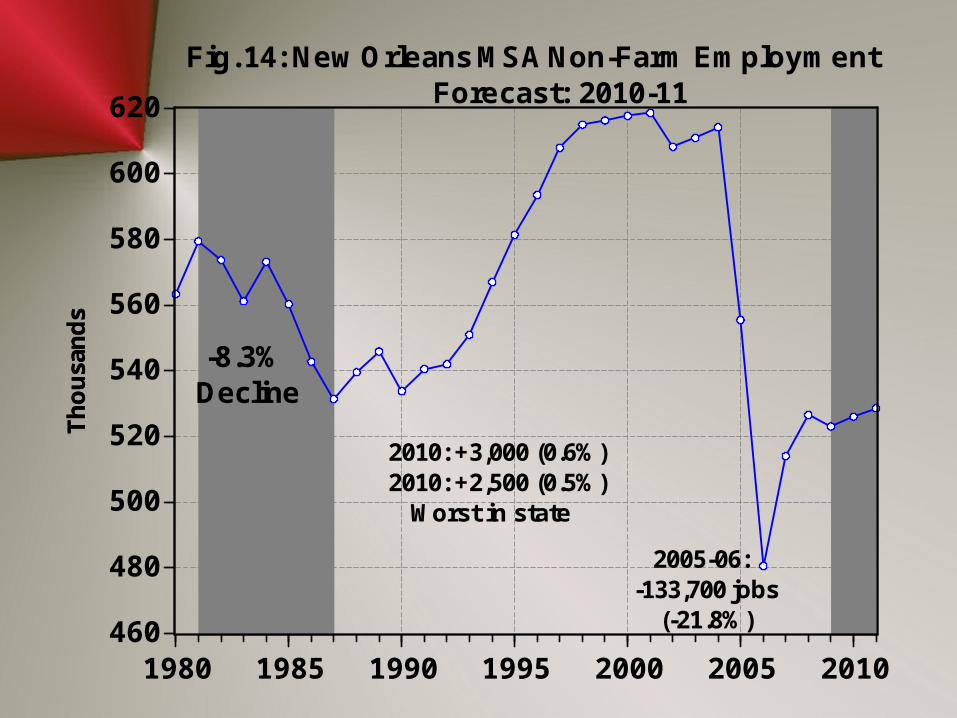

Fig. 14: New Orleans MSA Non-Farm Employment Forecast: 2010-11

Th

ou

san

ds

Th

ou

san

ds

-8.3%Decline

2005-06:-133,700 jobs (-21.8%)

2010: +3,000 (0.6%) 2010: +2,500 (0.5%) Worst in state

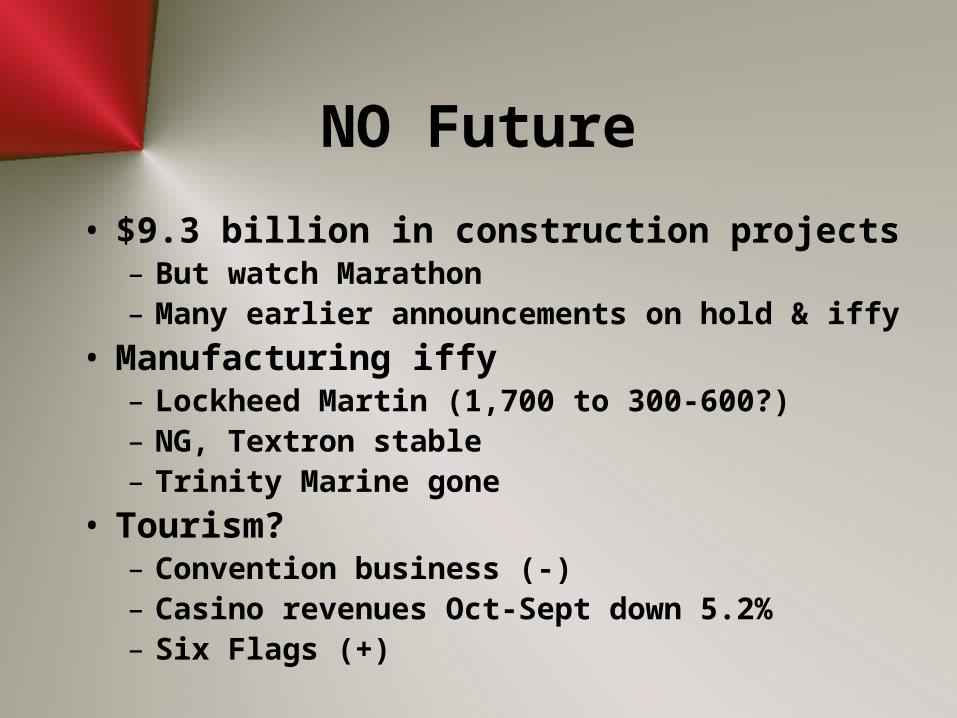

NO Future

• $9.3 billion in construction projects– But watch Marathon– Many earlier announcements on hold & iffy

• Manufacturing iffy– Lockheed Martin (1,700 to 300-600?)– NG, Textron stable– Trinity Marine gone

• Tourism?– Convention business (-)– Casino revenues Oct-Sept down 5.2%– Six Flags (+)

200

240

280

320

360

400

1980 1985 1990 1995 2000 2005 2010

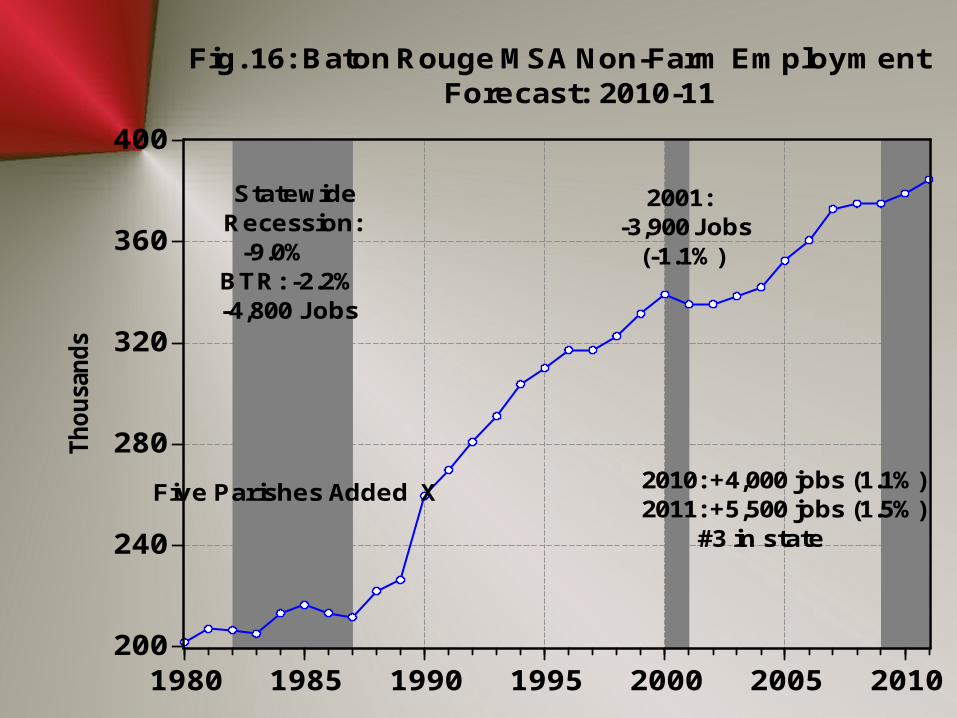

Fig. 16: Baton Rouge MSA Non-Farm Employment Forecast: 2010-11

Statewide Recession: -9.0%BTR: -2.2%-4,800 Jobs

2001:-3,900 Jobs (-1.1%)

Five Parishes Added X

Thousa

nds

2010: +4,000 jobs (1.1%)2011: +5,500 jobs (1.5%) #3 in state

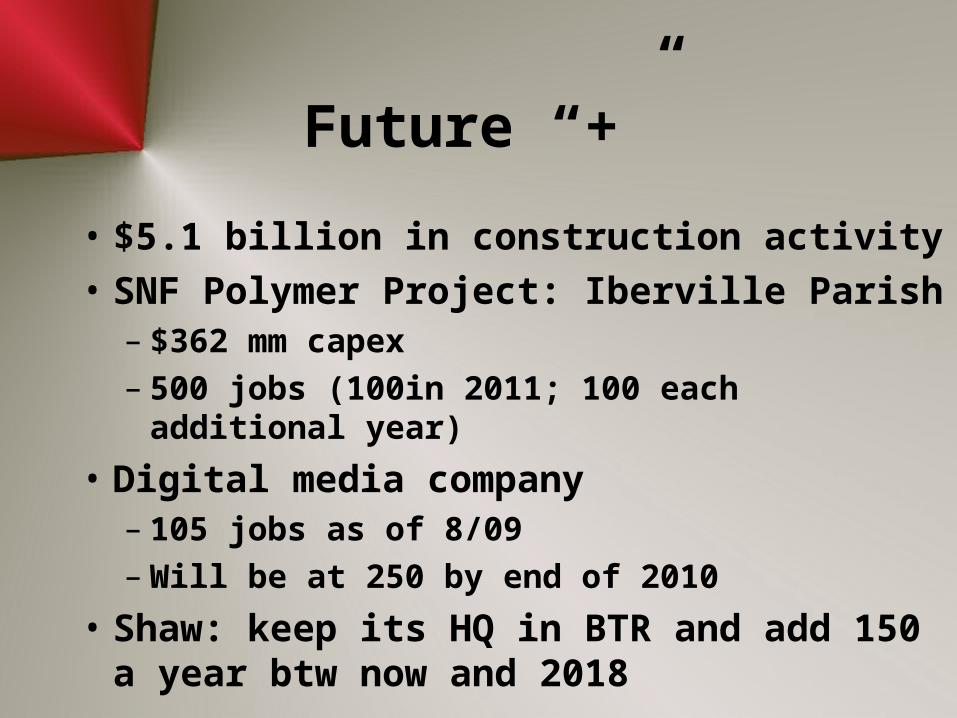

Future “+”

• $5.1 billion in construction activity

• SNF Polymer Project: Iberville Parish– $362 mm capex– 500 jobs (100in 2011; 100 each additional year)

• Digital media company– 105 jobs as of 8/09– Will be at 250 by end of 2010

• Shaw: keep its HQ in BTR and add 150 a year btw now and 2018

Future “+”

• Staples: at 154 jobs; must add 100 in 2010 & 2011 as well

• Old Tembec Paper Mill sold to PanAmerican; reopened as Renew in 7/09

• 200 new jobs initially

• To 400 w/I three years

Losses in BTR

• Dow Plaquemines: – -160 (permanent)– -400 contractors (temporary)

• IFC: -516 jobs 3/09

• Capital One: -180

• Trinity Marine: -190 (temporary?)

• Excide Batteries: -132 jobs temporarily (3/09)

Concerns

• State government?

• Chemicals/Refineries?– Cap & Trade?

90

100

110

120

130

140

150

160

1980 1985 1990 1995 2000 2005 2010

Th

ou

san

ds

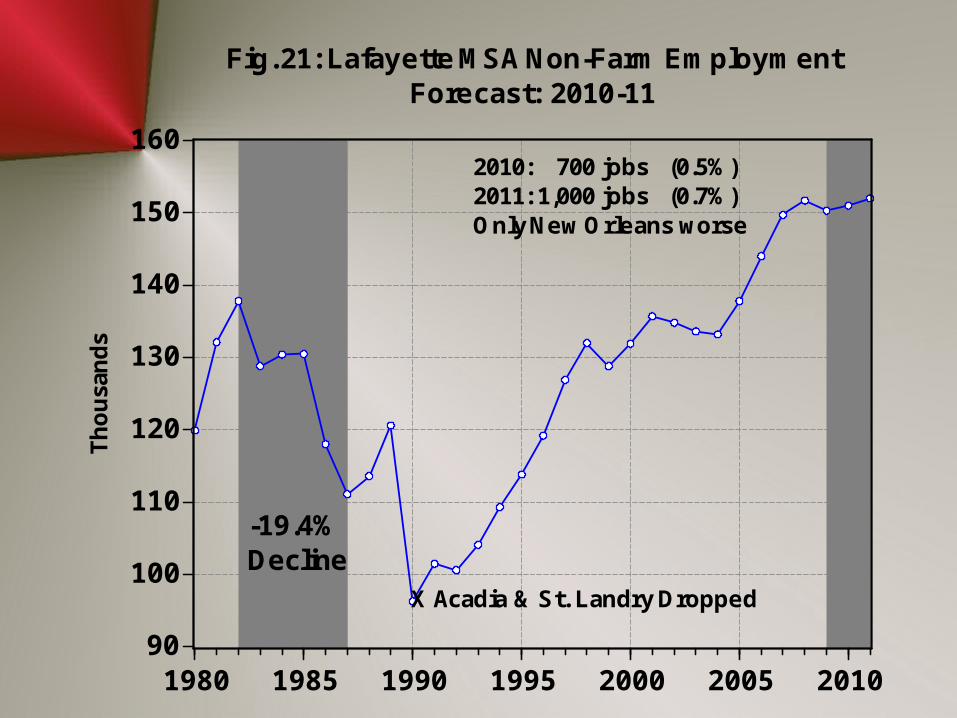

Fig. 21: Lafayette MSA Non-Farm Employment Forecast: 2010-11

-19.4%Decline

X Acadia & St. Landry Dropped

2010: 700 jobs (0.5%)2011: 1,000 jobs (0.7%)Only New Orleans worse

Lafayette Future

• Lethargic Extraction big problem• $474.2 million in construction

– Much done in 2010• Stuller adding 100• Acadian Ambulance adding 25• TransComm: +700• Flight Safety International:

– $120 mm, 70,000sq ft flight simulator facility (about finished)

– 50-60 jobs @ $60,000• TETRA creating 140 new jobs @$35k: start 11/09

50

60

70

80

90

100

1980 1985 1990 1995 2000 2005 2010

Th

ou

san

ds

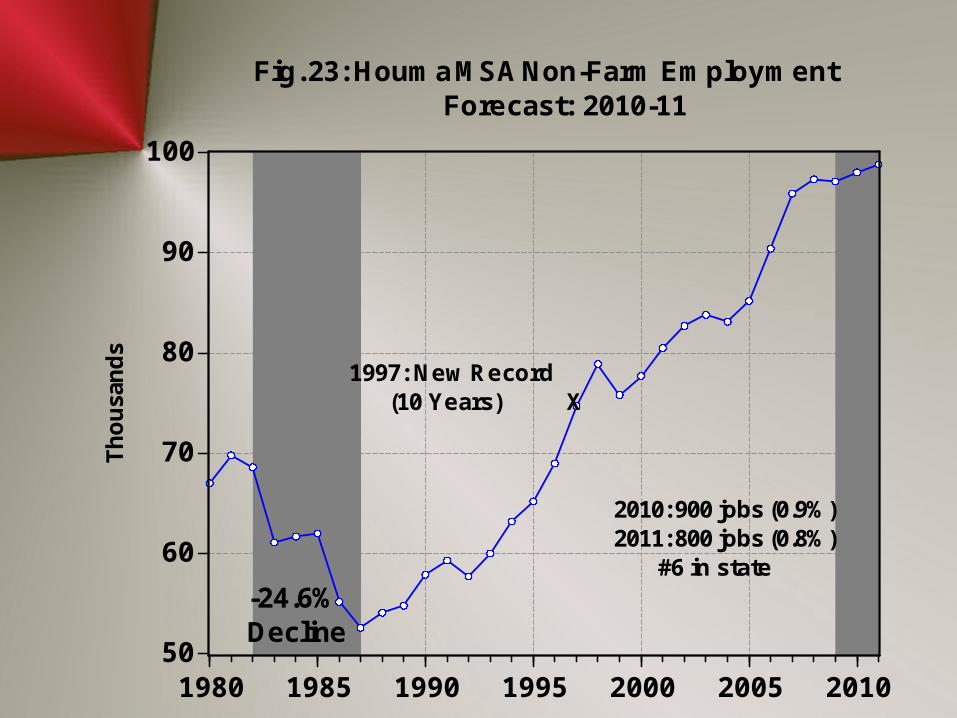

Fig. 23: Houma MSA Non-Farm Employment Forecast: 2010-11

-24.6%Decline

1997: New Record (10 Years) X

2010: 900 jobs (0.9%)2011: 800 jobs (0.8%) #6 in state

Houma Future

• Lethargic extraction sector• Shipbuilding a plus

– Edison Chouest: at least +1,000– Bollinger: stable

• Fabricators: If hit on contracts– Gulf Island: +350– J. Ray McDermott: +250

• $184.6 million in road & coastal restoration

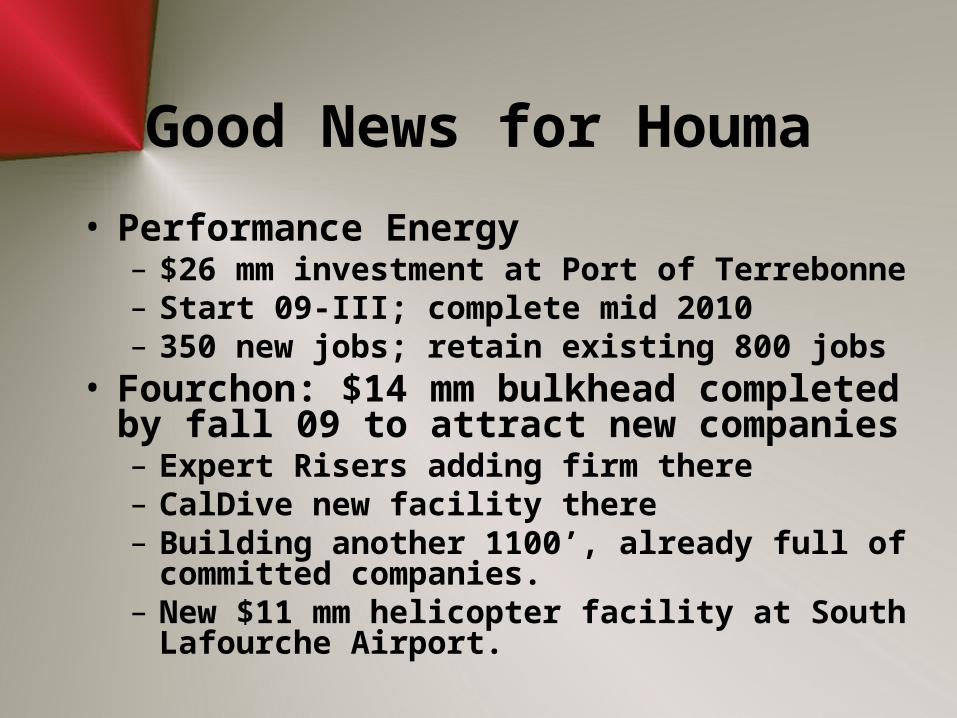

Good News for Houma

• Performance Energy– $26 mm investment at Port of Terrebonne– Start 09-III; complete mid 2010– 350 new jobs; retain existing 800 jobs

• Fourchon: $14 mm bulkhead completed by fall 09 to attract new companies– Expert Risers adding firm there– CalDive new facility there– Building another 1100’, already full of committed

companies.– New $11 mm helicopter facility at South Lafourche

Airport.

50

60

70

80

90

100

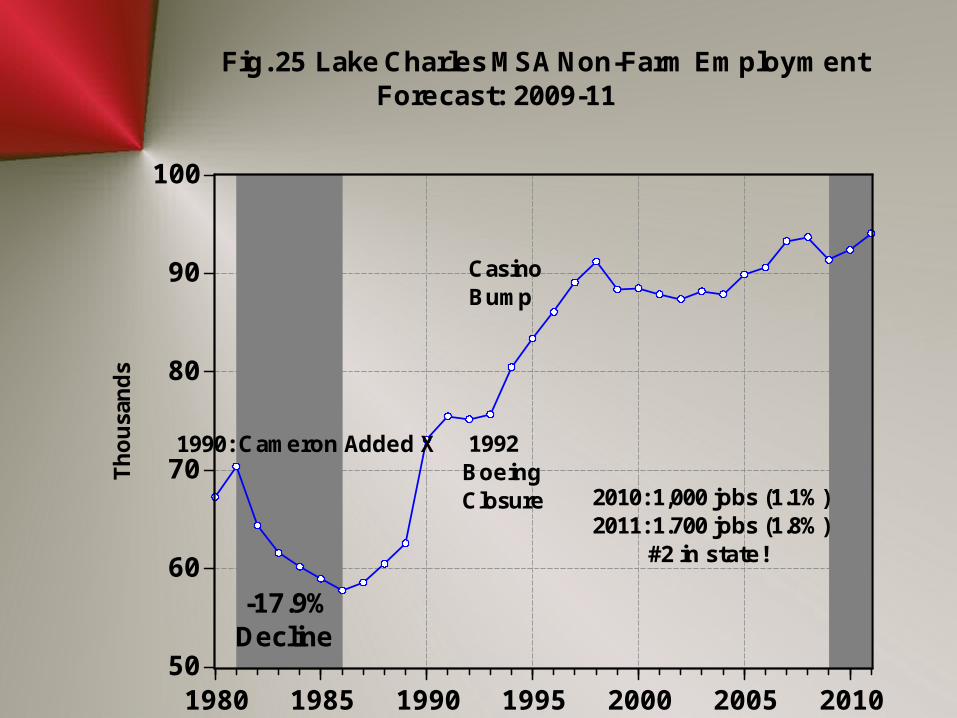

1980 1985 1990 1995 2000 2005 2010

Fig. 25 Lake Charles MSA Non-Farm Employment Forecast: 2009-11

Th

ou

san

ds

-17.9%Decline

1992BoeingClosure

CasinoBump

1990: Cameron Added X

2010: 1,000 jobs (1.1%)2011: 1.700 jobs (1.8%) #2 in state!

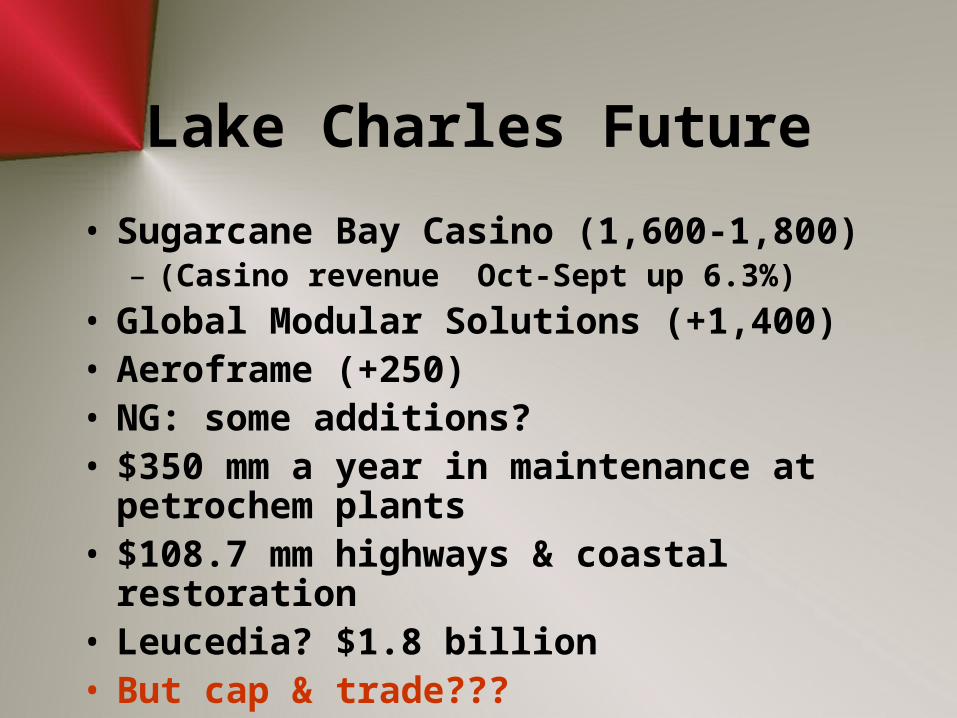

Lake Charles Future

• Sugarcane Bay Casino (1,600-1,800)– (Casino revenue Oct-Sept up 6.3%)

• Global Modular Solutions (+1,400)• Aeroframe (+250)• NG: some additions?• $350 mm a year in maintenance at petrochem

plants• $108.7 mm highways & coastal restoration• Leucedia? $1.8 billion• But cap & trade???

50

55

60

65

70

75

80

85

1980 1985 1990 1995 2000 2005 2010

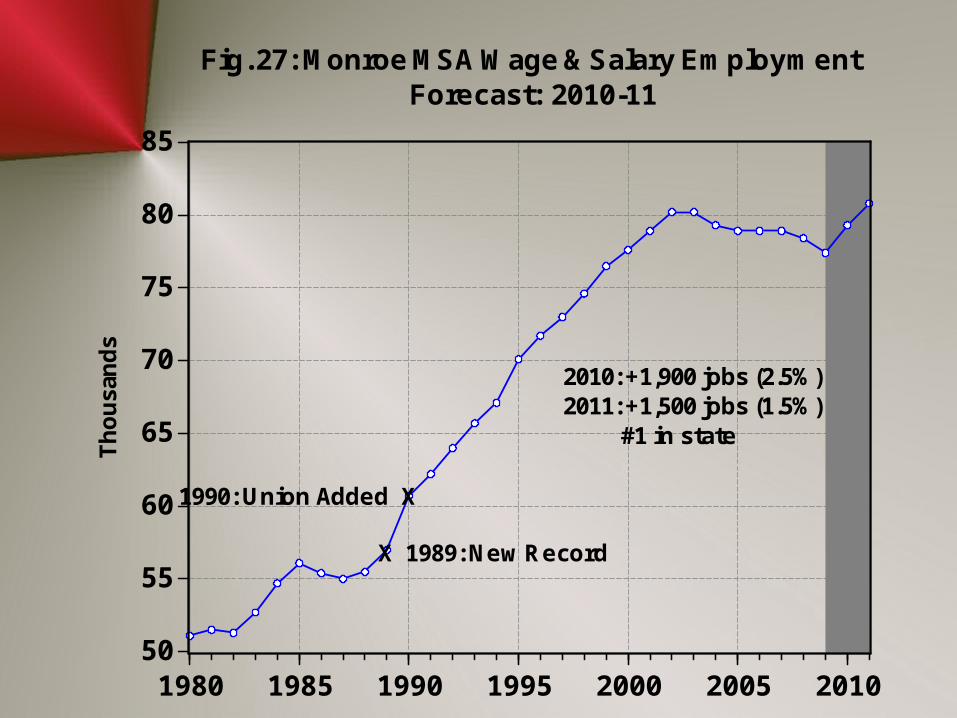

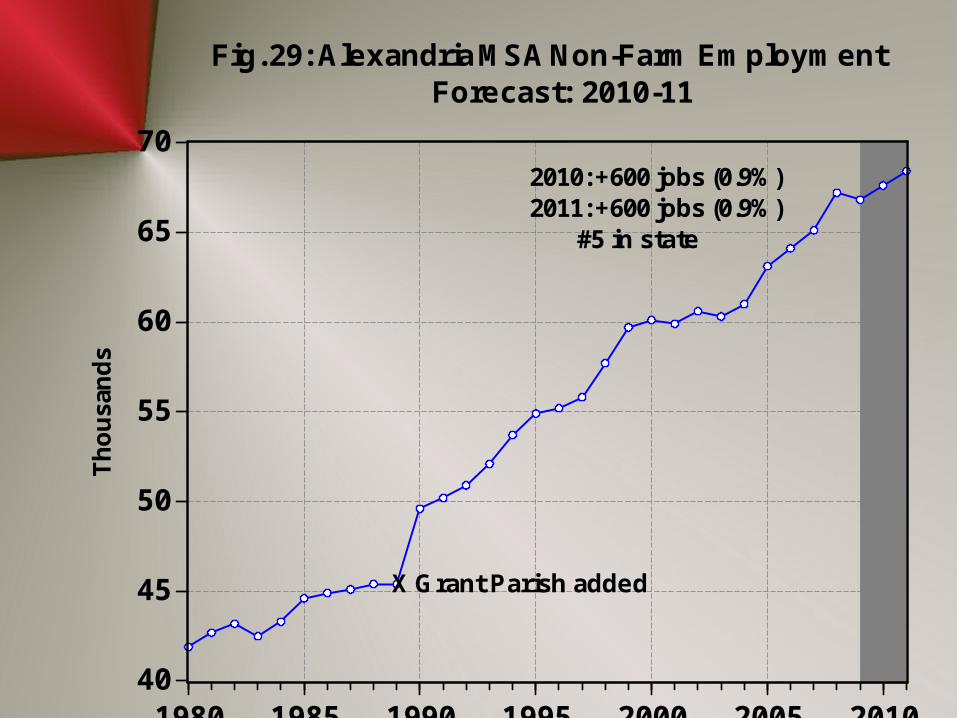

Fig. 27: Monroe MSA Wage & Salary Employment Forecast: 2010-11

Th

ou

san

ds

X 1989: New Record

1990: Union Added X

2010: +1,900 jobs (2.5%)2011: +1,500 jobs (1.5%) #1 in state

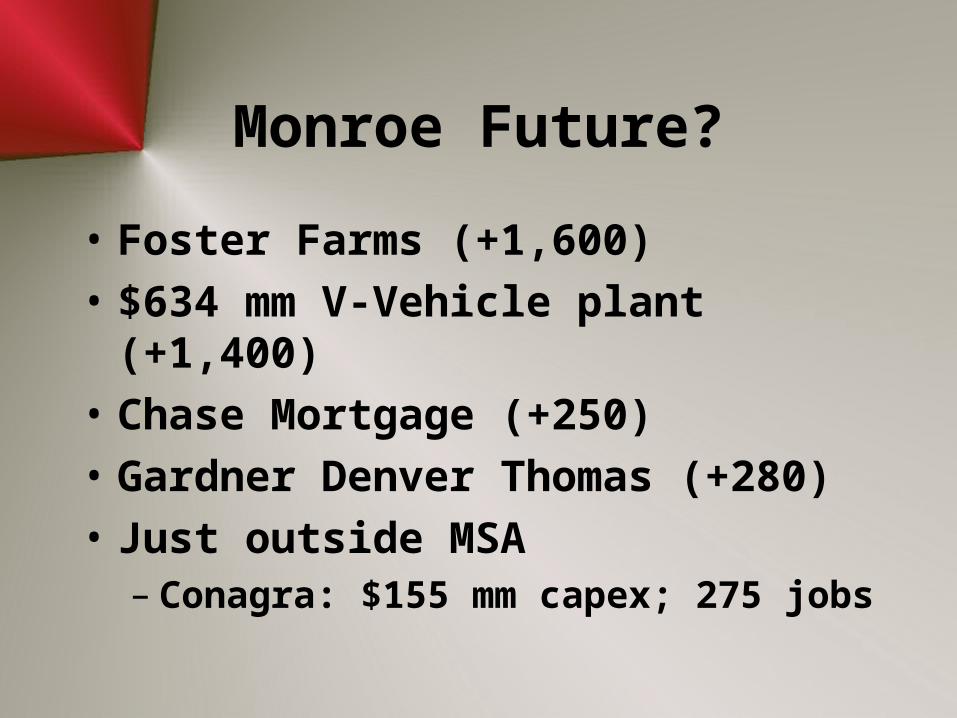

Monroe Future?

• Foster Farms (+1,600)

• $634 mm V-Vehicle plant (+1,400)

• Chase Mortgage (+250)

• Gardner Denver Thomas (+280)

• Just outside MSA– Conagra: $155 mm capex; 275 jobs

40

45

50

55

60

65

70

1980 1985 1990 1995 2000 2005 2010

Th

ou

san

ds

Fig. 29: Alexandria MSA Non-Farm Employment Forecast: 2010-11

X Grant Parish added

2010: +600 jobs (0.9%)2011: +600 jobs (0.9%) #5 in state

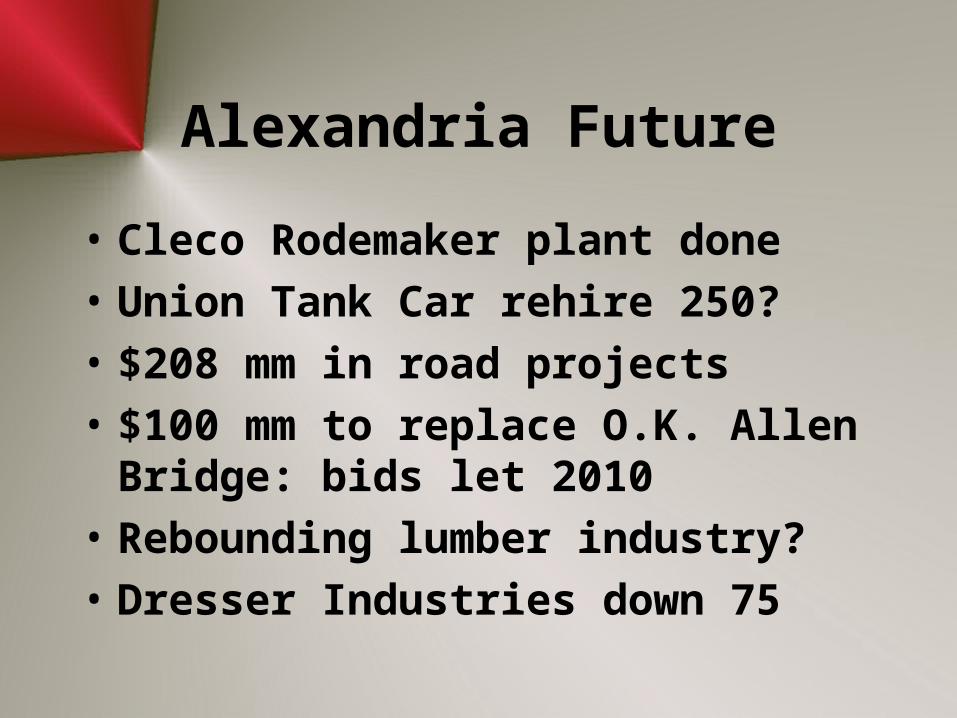

Alexandria Future

• Cleco Rodemaker plant done

• Union Tank Car rehire 250?

• $208 mm in road projects

• $100 mm to replace O.K. Allen Bridge: bids let 2010

• Rebounding lumber industry?

• Dresser Industries down 75

1400

1500

1600

1700

1800

1900

2000

1980 1985 1990 1995 2000 2005 2010

Fig. 31: Louisiana Non-Farm Employment: 2010-11T

ho

usa

nd

s

2009: -11,000 jobs (-0.6%)

2010: +17,800 Jobs (0.9%)2011: +18,000 Jobs (0.9%)

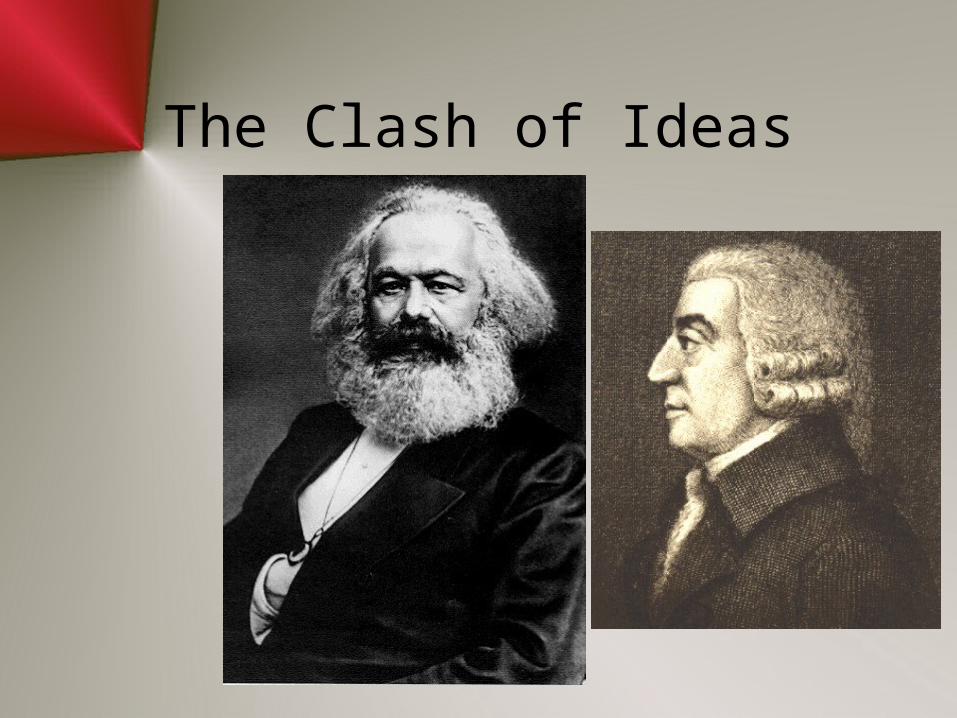

The Clash of Ideas

Karl Marx

• “From each according to his abilities, to each according to his needs”

• “The theory of Communism may be summed up in one sentence: Abolish all private property.”

Adam Smith

• “Competition alone can regulate prices with equity; it alone restricts them to a moderation which varies little; it alone attracts with certainty provisions where they are wanted or labour where it is required.”

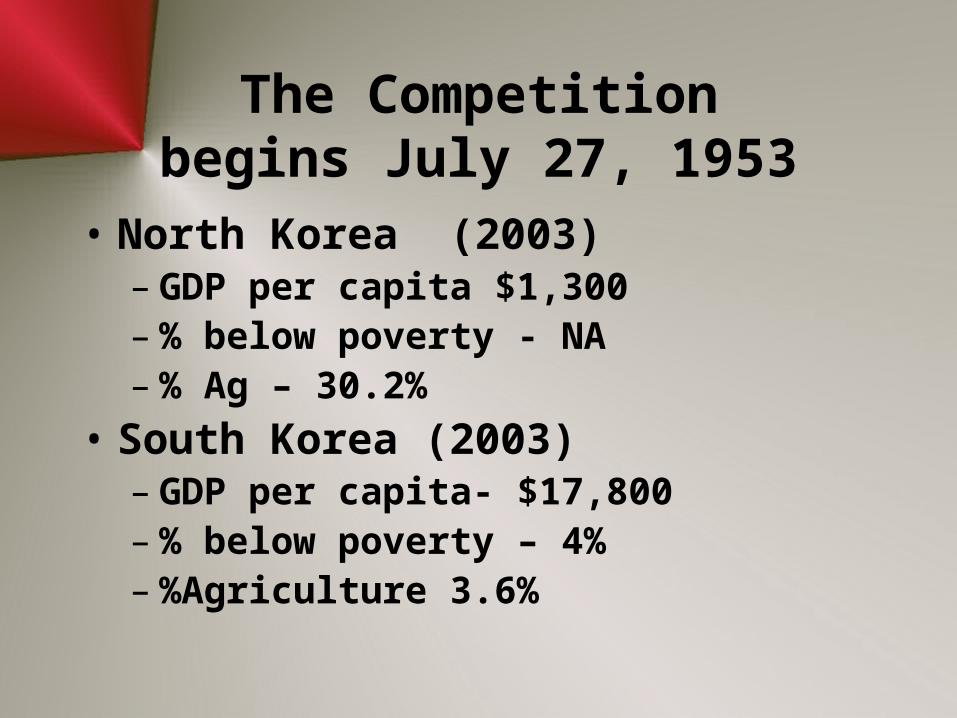

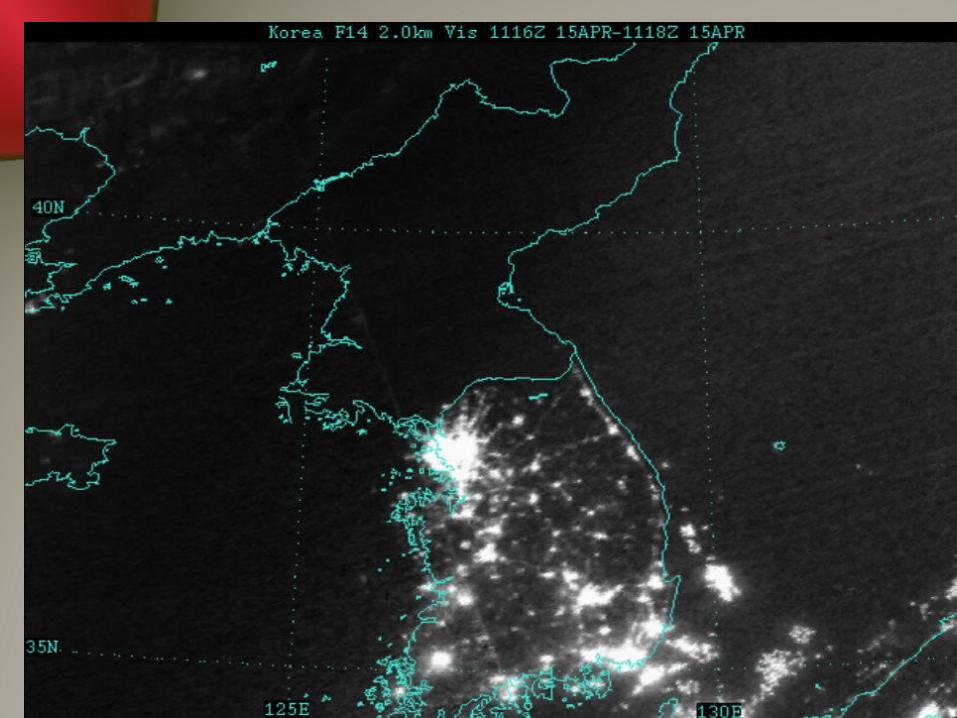

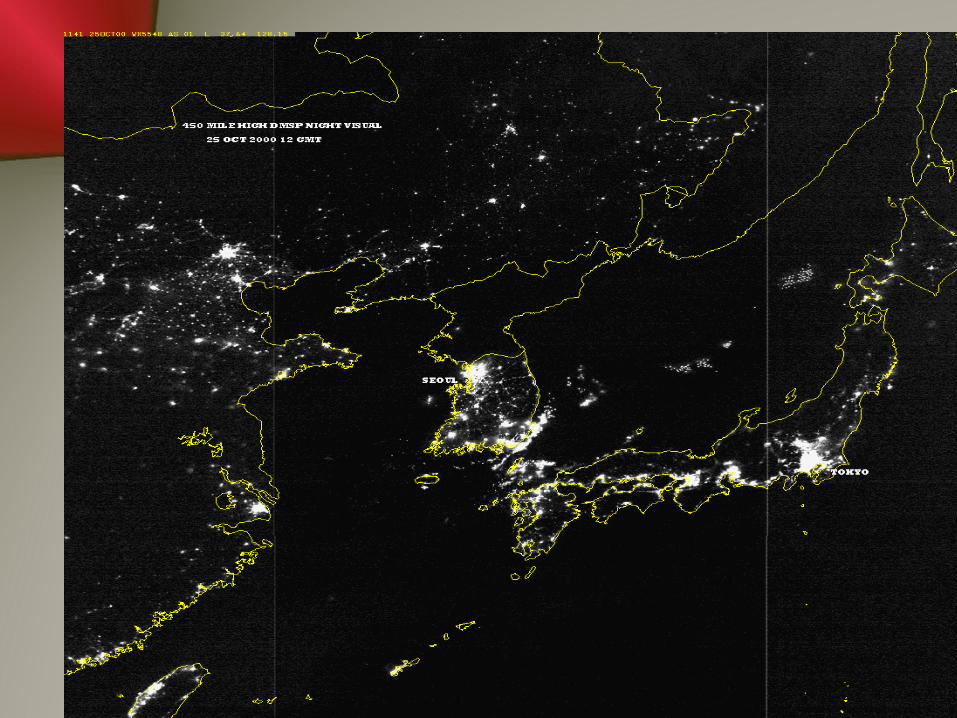

The Competitionbegins July 27, 1953

• North Korea (2003)– GDP per capita $1,300– % below poverty - NA– % Ag – 30.2%

• South Korea (2003)– GDP per capita- $17,800– % below poverty – 4%– %Agriculture 3.6%

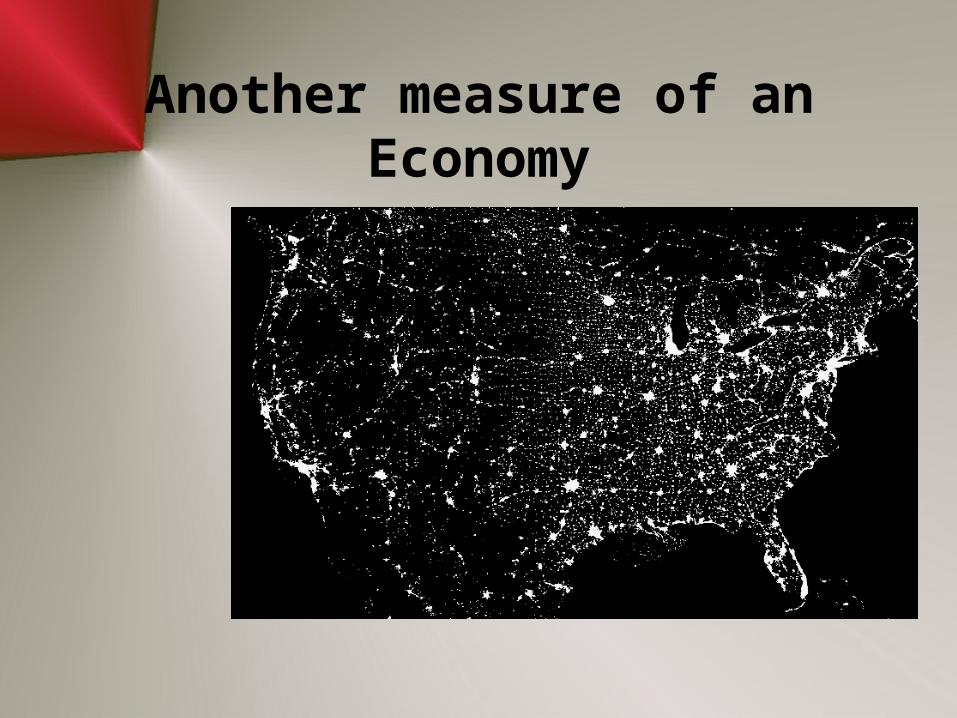

But these are just technical economic measures

Is there another indicator of economic health?

Another measure of an Economy

November 6, 2009

Dr. Loren C. ScottLoren C. Scott & Associates, Inc.www.lorencscottassociates.com