october 2011. disclaimer the views expressed here contain information derived from publicly...

TRANSCRIPT

October 2011

2

Disclaimer

The views expressed here contain information derived from publicly available sources and have

not been independently verified.

No representation or warranty is made as to the accuracy, completeness or reliability of the

information.

Any forward looking information in this presentation has been prepared on the basis of a number

of assumptions which may prove to be incorrect. For additional information on these or other

factors, please see the Company’s filings on SEDAR. This presentation should not be relied upon

as a recommendation or forecast by Western Potash Corp.

Nothing in this presentation should be constructed as either an offer to sell or a solicitation of an

offer to buy or sell shares in any jurisdiction.

3

Western Potash Corp. Strengths

• World Class Resource

– Updated NI 43 101 Technical Report

• Positive Economics

– Preliminary Economic Assessment

(Scoping Study)

• Ability to Deliver the Project

– Management Experience

Financial Overview

Stock Symbol

• TSX – WPX, FSE - AHE

Cash

• CAD $28 Million

Shares Outstanding

• 160,945,183

Market Capitalization

• CAD $230, 151, 612

Warrants

• 9M($1.75), Expiry June 2013• 1.27M($1.10), Expiry June 2013

Management Holdings•14.9%

Trading Range, as of Oct. 13th, 2011

• $0.70 - 1.55 (52 week)

Average Daily Volume, (78 Days, since TSX Listing) as of Oct. 13th, 2011

• 1 ,334, 614

4

June 30, 2011 Financial Information, Close June 30th, $1.43

5

World Class Resource

Updated NI 43 101 Technical Report

• Measured (Recoverable)

64 Million Tonnes, 30.47% KCL

• Indicated (Recoverable)

180 Million Tonnes, 30.35% KCL

• Inferred (Recoverable)

701 Million Tonnes, 30.31% KCL

6

Milestone Project

Phase 1 & 2 Drill Program

(20, 153m)

NI 43 101 Compliant Mineral Resource Estimate

Measured & Indicated 174 Mt recoverable KCLInferred 560 Mt recoverable KCL

Scoping Study Delivered

Updated NI 43 101 Technical Report

Measured & Indicated 244 Mt recoverable KCLInferred 701 Mt recoverable KCL

Prefeasibility Study Completed

Feasibility Study Process Initiated

FeasibilityCompletion

2009 2010 2011 2012

7

Milestone Timeline

Present

8

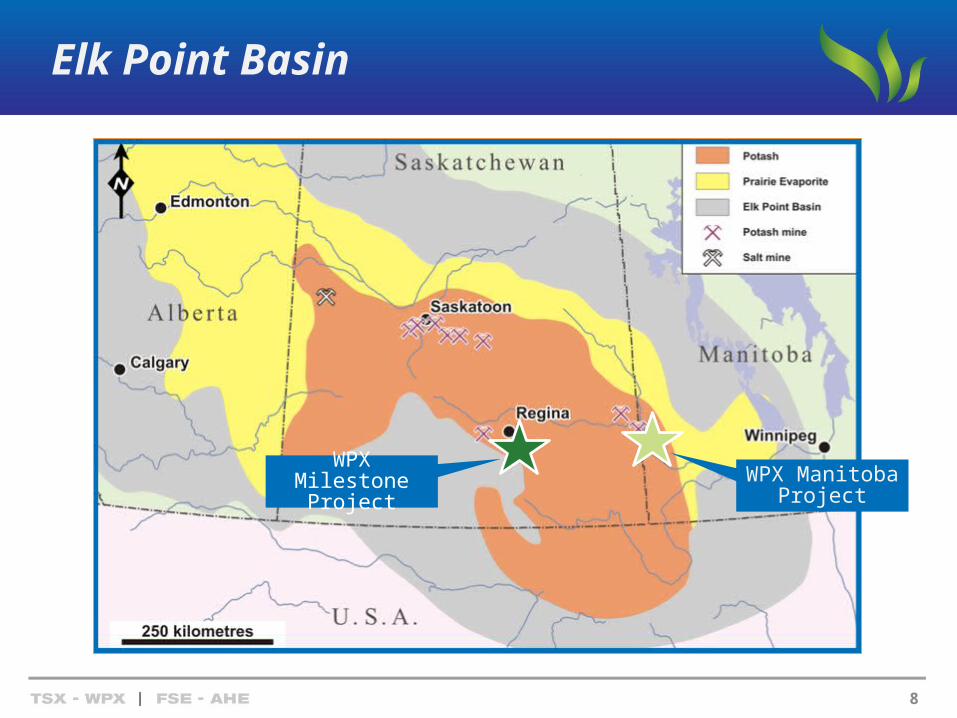

Elk Point Basin

WPX Milestone Project

WPX ManitobaProject

9

Milestone Saskatchewan

10

Solution Mining Benefits

• Proven Process, Mosaic Belle Plaine Mine

(45 yrs.)

• Reduced CAPEX

• Shorter payback period, higher IRR

• Faster timeline to production

• Scalability

• Lower technical risk

• Reduced environmental footprint

• Reduced health and safety risk

11

Positive Economics

• Positive and Robust Preliminary

Economic Assessment Delivered

– (Scoping Study)

12

Scoping Study Highlights

AMEC’s EPCM experience with five

Potash Corp mines adds credibility to

the CAPEX estimates for this project.

• (NPV10) 5.22 Bn1 CAD: IRR 27.3%*1. CRU Projected prices ($511)

• Production rate of 2.5 Mt per year

• 40 year mine life

• Total CAPEX $2.51 billion CAD

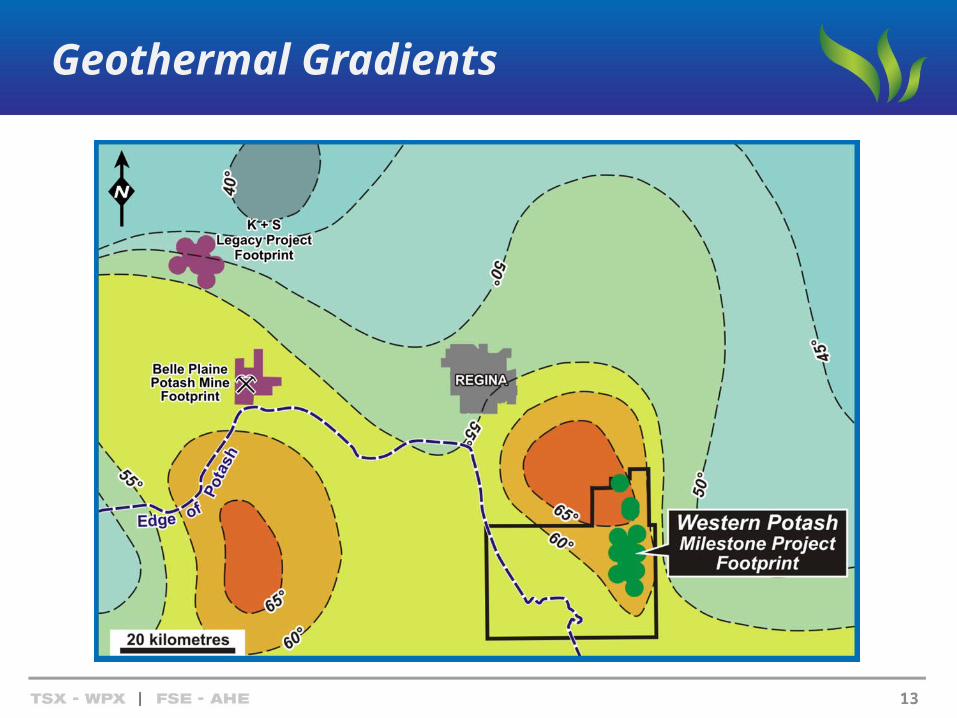

• 8.5% Reduction of production costs due to the high formation temperatures

13

Geothermal Gradients

14

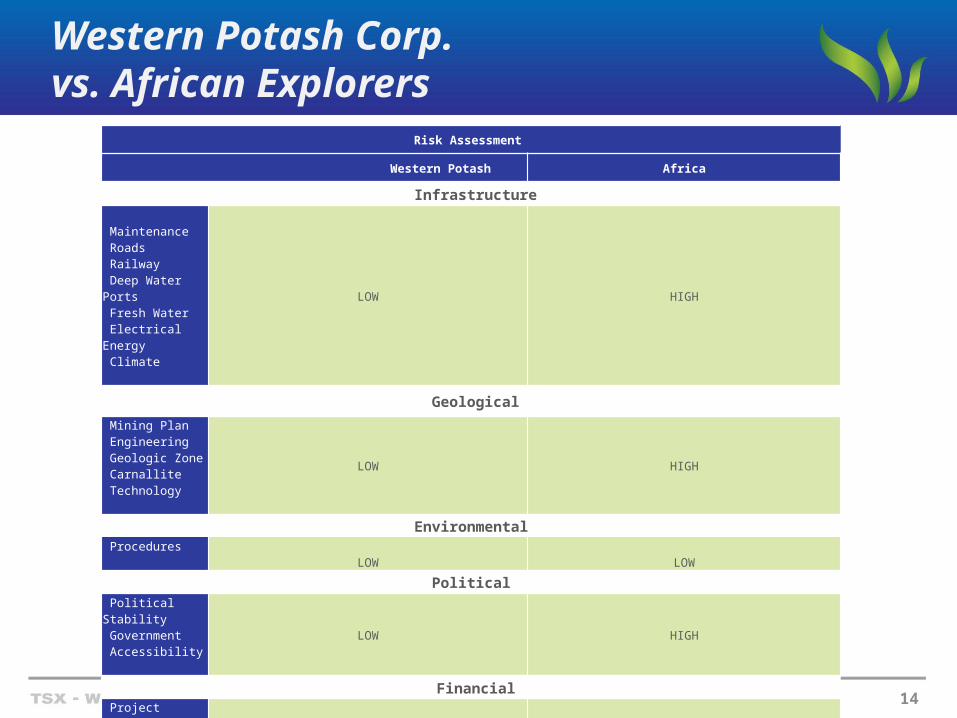

Western Potash Corp. vs. African Explorers

Risk Assessment

Western Potash Africa

Infrastructure

Maintenance Roads Railway Deep Water Ports Fresh Water Electrical Energy Climate

LOW HIGH

Geological

Mining Plan Engineering Geologic Zone Carnallite Technology

LOW HIGH

Environmental

ProceduresLOW LOW

Political

Political Stability Government Accessibility

LOW HIGH

Financial Project Financing

HIGH HIGH

15

Global GDP

1900 - 1920

1920 - 1930

1930 - 1940

1940 - 1950

1950 - 1960

1960 - 1970

1970 - 1980

1980 - 1990

1990 - 2000

2000 - 2010

2010 - 2020

2020 - 2025

0

1

2

3

4

5

6

Growth rate(% per annum)

Developing economies

Developed economies

Source: 1900 - 1980 - J. Bradford De Long ("Estimates of World GDP", 1998); 1980 to 2010 - IMF World Economic Outlook Database; 2010 to 2025 Forecast - Global Insight

16

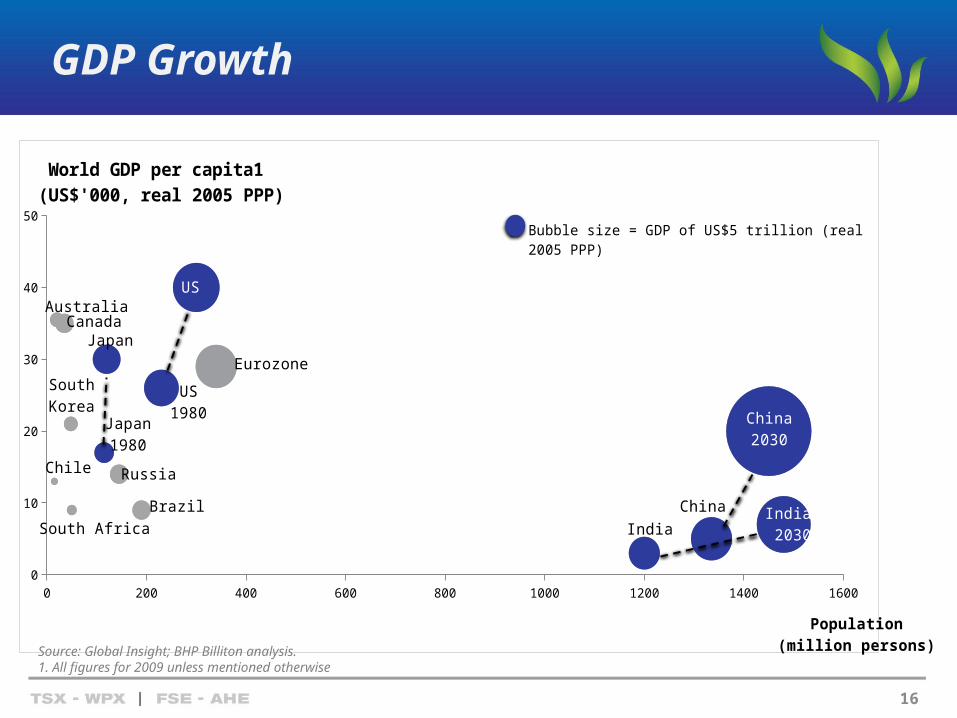

GDP Growth

0 200 400 600 800 1000 1200 1400 16000

10

20

30

40

50

South Africa

Chile

SouthKorea

AustraliaCanada

Japan

Japan1980

Russia

Brazil

US1980

US

Eurozone

India

ChinaIndia 2030

China2030

World GDP per capita1 (US$'000, real 2005 PPP)

Population(million persons)

Bubble size = GDP of US$5 trillion (real 2005 PPP)

Source: Global Insight; BHP Billiton analysis.1. All figures for 2009 unless mentioned otherwise

17

More CompetitiveLow Pricing Power

Less CompetitiveHigh Pricing Power

Share of the total production which is attributed to the top 5 companies in the industry.

Consolidation rates

Source: CRU Strategies

18

Saskatchewan, Canada

Competitive

• Largest Potash Producer in the

world, +30%

• Hosts 50% of the World`s Reserves

• Value of SK. Potash sales in 2009

were $3.1 billion

Investment Climate

• Potash Production has been continuous since 1962

• Potash Industry will invest $12 billion in development from 2005-2020

• SK. Greenfield development encouraged

19

Potash Site Costs

Assuming Full Capacity Utilization*

20

Gas Pricing Forecast ( AECO-O)

Milestone Facility

21

22

Ability to Deliver the Project

• Management Experience

• Engineering Process 3 Months

ahead of schedule

• Financed through the completion

of Robust Feasibility

• Commercial Team Formed

• Strategic Partner Identification

• Partner Acquisition strategy

23

Management

President & CEOPatricio Varas•Professional Geologist with over 24 years experience in exploration, project development and corporate management.•WPX President and CEO since inception.

Executive Vice PresidentDean Pekeski•Professional Geologist with over 17 years experience in mineral exploration.•Previously the VP of Exploration with WPX.

VP Corporate DevelopmentJohn Costigan•Over 25 years experience in technical sales and marketing to the mining, food, and pulp & paper multinationals.•VP of Corporate Development at WPX since inception.

VP Corporate Finance & DirectorPatrick Power•Over 17 years of experience as a stock market professional and as director of public companies. •Played a critical role in raising approximately 80 million for WPX to date.

Economics and ModellingIan Graham•Over 20 years of mineral exploration and evaluation experience with Anglo American and Rio Tinto.•Geological and project management experience in the field of mineral exploration and project development in Canada and abroad.

Financial AdvisorJohn King Burns

•Experience with Drexel Burnham Lambert Inc. and Barclays Bank Plc, Metals Group.•Provides both strategic and tactical advice to management in combination with financial advisory services.

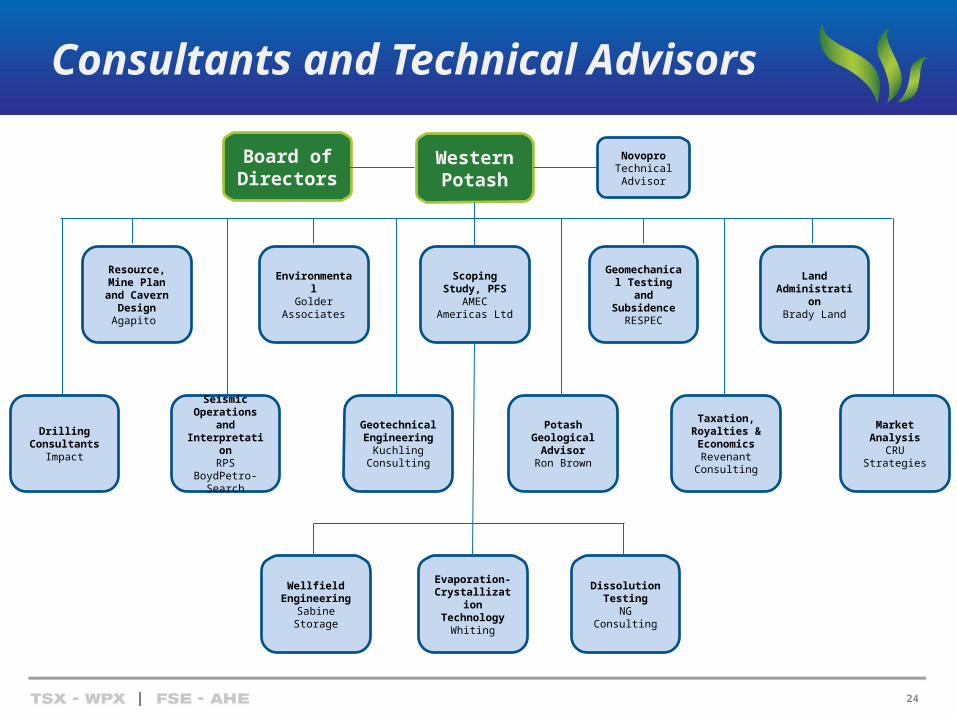

Consultants and Technical Advisors

24

Western Potash

Seismic Operations and Interpretation

RPS BoydPetro-Search

Resource, Mine Plan and

Cavern DesignAgapito

Scoping Study, PFS

AMEC Americas Ltd

EnvironmentalGolder

Associates

Land Administration

Brady Land

Geomechanical Testing and Subsidence

RESPEC

Taxation, Royalties & EconomicsRevenant Consulting

Potash Geological

AdvisorRon Brown

Geotechnical Engineering

Kuchling Consulting

Evaporation-Crystallization

TechnologyWhiting

Wellfield Engineering

Sabine Storage

Dissolution Testing

NG Consulting

NovoproTechnical Advisor

Drilling Consultants

Impact

Market Analysis

CRU Strategies

Board of Directors

25

Conclusion

• World Class Resource

– Updated NI 43 101 Technical Report

– High Grades (+30% KCL)

– Low Risk Development Environment

• Positive Economics

– PEA (Scoping Study)

– 40+ year mine life at 2.5 TPY

– IRR: 27.3%, CAPEX: $2.51 billion

– Reduction in Production Costs of 8.5%

• Ability to Deliver the Project

– Management Experience

– Amec Americas, Feasibility process (ahead of

schedule)Source: AMEC Americas Ltd.

Suite 1818 - 701 West Georgia St.Vancouver, British ColumbiaV7Y 1C6, Canada604.689.WEST (9378)[email protected]

26