sitc international holdings company limited - … · sitc international holdings company limited...

TRANSCRIPT

SITC International Holdings Company Limited

October 2010

This document does not constitute an offer to sell or issue or the solicitation of an offer to buy or acquire securities of SITC

International Holdings Company Limited (the “Company”) in any jurisdiction or an inducement to enter into investment activity,

nor may it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever.

Specifically, this document does not constitute a “prospectus” within the meaning of the U.S. Securities Act of 1933 or the

Hong Kong Companies Ordinance (Chapter 32 of the Laws of Hong Kong), as amended. Any decision to purchase securities

in the Company shall only be made at your own assessment of the market and the market position of the Company and at

your own risk. Shareholders and investors are reminded to exercise caution when dealing in the securities of the Company.

This document has been prepared by the Company solely for the reference of the shareholders and investors. The

information contained in this presentation has not been independently verified. No representation, warranty or undertaking,

express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness

of the information or the opinions contained herein. The information contained in this document should be considered in the

context of the circumstances prevailing at the time and has not been, and will not be, updated to reflect material developments

which may occur after the date of the document. These materials do not contain all of the relevant information relating to the

Company or its securities. None of the Company or any of its affiliates, advisors or representatives will be liable (in negligence

or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection

therewith. The Company may alter, modify or otherwise change in any manner the content of this document, without obligation

to notify any person of such revision or changes.

Any information on the past performance of the Company is not necessarily indicative of its future performance. This

document contains statements that constitute forward-looking statements that are based on current assumptions and beliefs

as well as information currently available to the Company. These statements include descriptions regarding the intent, belief or

current expectations of the Company or its officers with respect to the consolidated results of operations and financial

condition of the Company. These statements can be recognized by the use of words such as “expects,” “plans,” “will,”

“estimates,” “projects,” “intends,” or words of similar meaning. Such forward-looking statements are not guarantees of future

performance and involve risks and uncertainties, and actual results may differ significantly from those in the forward-looking

statements as a result of various factors and assumptions. The Company has no obligation and does not undertake to revise

forward-looking statements to reflect future events or circumstances.

Disclaimer

Contents

Company Overview

Business Highlights

Business Strategy

Financial Information

1

2

3

4

1

1. Company Overview

Our Business

Container shipping

Trucking

Freight forwarding

Ship agency

Depot and Warehousing

We are a leading shipping logistics company in the PRC, exclusively focused on the intra-Asia market,

providing integrated transportation solutions to our customers.

Largest Non-State-

Owned Shipping

Logistics Company in

the PRC

3rd Largest Container

Shipping Company in

the PRC

4th Largest Container

Shipping Company in

the Intra-Asia Market

1st 3rd 4th

Source: Drewry.

2 Company Overview

Our Corporate Milestones

SITC has achieved a leading market position within a short period of 19 years since its establishment in

1991.

SITC Corp was established to operate freight forwarding

business

1991

Purchased first vessel and started serving PRC-Japan

trade lane

Began our depot and warehousing services

1992

Expanded into ASEAN Market2004

Strategically relocated operating center

from Qingdao to Shanghai

2007

Became market leader along PRC-

Japan route2008

Became market leader along

PRC-Vietnam and PRC-

Philippines routes

2009

Established Qingdao logistics park2003

Signed strategic cooperation

agreement with Shanghai Port and

Dinh Vu Port in Vietnam to jointly

develop depot, warehousing and

other logistics businesses

2010

2006 Became largest PRC-based non-state-

owned shipping logistics company

3 Company Overview

2. Business Highlights

Business Highlights

Exclusively Focused on the Fast Growing Intra-Asia Market1

Integrated “One-Stop” Logistics Services 2

Distinctive High Frequency, High Density Service Model3

Stable and Experienced Management Team4

4 Business Highlights

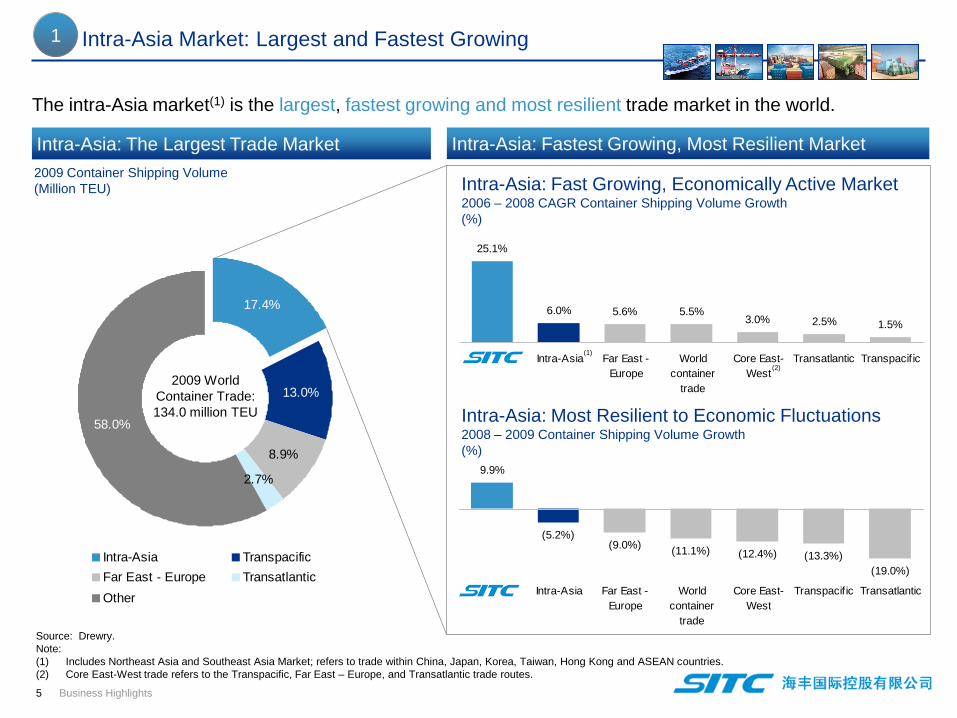

Intra-Asia Market: Largest and Fastest Growing

25.1%

6.0% 5.6% 5.5%3.0% 2.5% 1.5%

Intra-Asia Far East -

Europe

World

container

trade

Core East-

West

Transatlantic Transpacific

9.9%

(5.2%)(9.0%)

(11.1%) (12.4%) (13.3%)

(19.0%)

Intra-Asia Far East -

Europe

World

container

trade

Core East-

West

Transpacific Transatlantic

Intra-Asia: Fastest Growing, Most Resilient MarketIntra-Asia: The Largest Trade Market

17.4%

13.0%

58.0%

2.7%

8.9%

Intra-Asia Transpacific

Far East - Europe Transatlantic

Other

2009 World

Container Trade:

134.0 million TEU

Source: Drewry.

Note:

(1) Includes Northeast Asia and Southeast Asia Market; refers to trade within China, Japan, Korea, Taiwan, Hong Kong and ASEAN countries.

(2) Core East-West trade refers to the Transpacific, Far East – Europe, and Transatlantic trade routes.

The intra-Asia market(1) is the largest, fastest growing and most resilient trade market in the world.

2009 Container Shipping Volume

(Million TEU) Intra-Asia: Fast Growing, Economically Active Market2006 – 2008 CAGR Container Shipping Volume Growth

(%)

Intra-Asia: Most Resilient to Economic Fluctuations2008 – 2009 Container Shipping Volume Growth

(%)

(2)

1

(1)

5 Business Highlights

7,743 7,730

8,057

7,519

8,239

2006 2007 2008 2009 2010E

Our Leading Position in the Intra-Asia Market

845

1,080

1,187

995

2007 2008 2009 9M 2010

14,134

15,760

16,543

15,806

17,349

2006 2007 2008 2009 2010E

Southeast Asia Market (1)

Northeast Asia Market (1)

Growth driven by strong

economic growth in Southeast

Asia countries, especially

Thailand and Vietnam

The Northeast Asia Market is mature and has stable growth while the Southeast Asia Market is fast growing and

emerging. We have a leading position in the Northeast Asia Market. Since 2004, we entered into the Southeast

Asia Market and have achieved strong growth.

Connects the PRC and Japan,

the second and third largest

economies in the world,

respectively

These countries have fast

growing industrial sectors with

high import demand for raw

materials

Lower tariffs from China –

ASEAN Free Trade Agreement

in January 2010 to further

boost trade between PRC and

ASEAN countries

(Thousand TEU)

1

Our Container Shipping Volume

(Thousand TEU)

(Thousand TEU)

Source: Drewry.

(1) The Northeast Asia Market refers to trade solely between the PRC, Japan and China while the Southeast Asia Market

refers to trade within intra-Asia that involves Taiwan, Hong Kong or ASEAN countries6 Business Highlights

Integrated “One-Stop” Logistics Services

Our integrated “one-stop” services provide high quality and convenient supply chain solutions for our

customers.

Our sea freight logistics and land-based logistics business are closely interconnected and are equally important profit drivers

for our business.

Our ability to provide one-stop shop services is crucial to maintaining our long-term customer relationships.

Our presence along the logistics value chain allows us to provide high quality and consistent service.

2

Manufacturer Retailer

Land

TransportationDepot and

Warehousing

Freight

Forwarding ShippingCustoms

Clearance

Ship

Agency

7 Business Highlights

Extensive Logistics Service Network2

Our integrated “one-stop” services cover 7 countries and 37 major ports and cities.

Our Freight Forwarding Network

Extensive freight forwarding services network

Covers 22 major cities in China, Japan and

Korea

Our Shipping Agency Network

Covers 27 major ports in the PRC, Japan, Hong

Kong, Korea, Vietnam, Thailand and Philippines

Our shipping agency business helps to source

volumes for our freight forwarding business, and

is highly complementary to our freight forwarding

network

Freight forwarding

Shipping agency

Freight forwarding and

shipping agency

Our Integrated Logistics Service Network

Lianyungang

Hong Kong

Qinhuangdao

Manila

Ho Chi Minh City

ShidaoTokyo

Haiphong

Wenzhou

Guangzhou

Seoul

Hanoi

Bangkok

Kobe

Weihai

Dalian

Qingdao

Tianjin

Shanghai

Yantai

Ningbo

Xiamen

Nanjing

Shenzhen

Suzhou

Yiwu

Shaoxing

Osaka

Busan

ZhuhaiFoshan

Dongguan

Incheon

Pyeongtaek

Laem Chabang

Tanggu

Wuhan

8 Business Highlights

Note: As of June 30, 2010.

Highly Efficient Integrated Logistics Park Business Model

Description

Joint ventures with international and PRC-based blue-chip

companies

Include Maersk, Tsingdao Beer, Singamas, Itochu, and

Hanjin

Approximately 480,000m2 of depot and 47,000m2 of

warehousing space

Real-time monitoring of warehousing operations and

inventory management systems

Qingdao Logistics Park

Our Qingdao Logistics Park was awarded the PRC Logistics

Award for Best Solution Design from the China

Communications and Transport Association

Formed joint ventures with blue chip customers to provide

tailored logistics services, enhancing customer loyalty

Warehouses equipped with computer systems that enable

real-time operations management and allow customers to

make service inquiries online

Proximity to port, major expressway and train station

Facilitates interaction between parties involved in the supply

chain

We enhance customer loyalty through win-win partnerships to provide depot and warehousing services with

our domestic and international blue chip customers.

JV Partner JV Description

Warehousing and value-

added (e.g. goods inspection)

services

Depot and warehousing

services

Depot and warehousing

services

Location

Qingdao

Qingdao

Qingdao

Refrigerated warehousing

services

Qingdao

Depot and warehousing

services

Qingdao

Depot and warehousing

services

Shanghai

2

9 Business Highlights

Note: As of June 30, 2010.

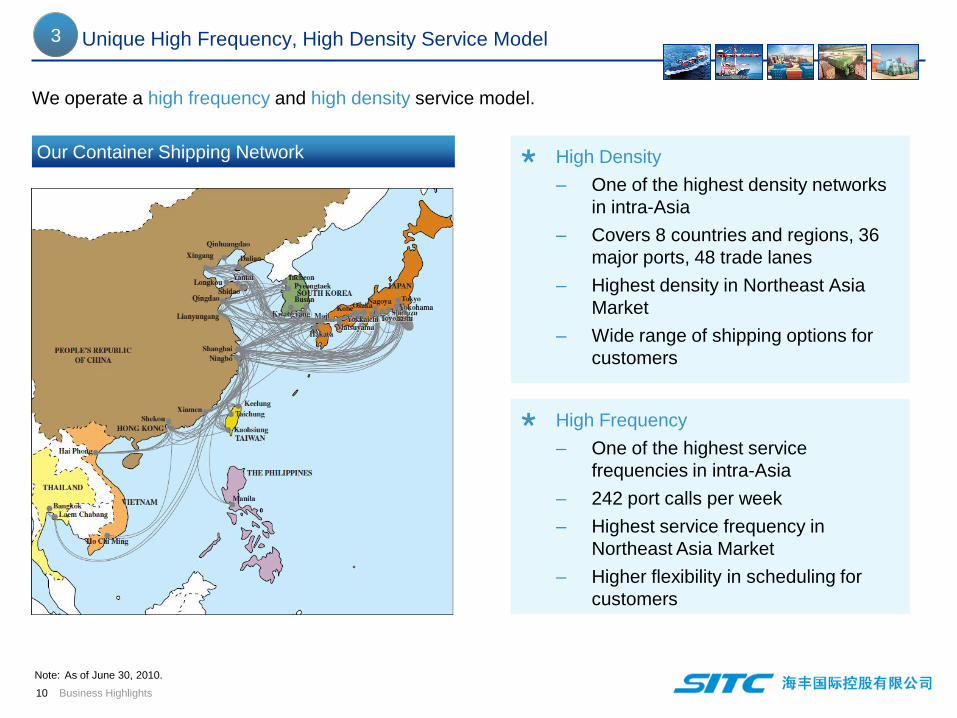

Unique High Frequency, High Density Service Model

High Density

– One of the highest density networks

in intra-Asia

– Covers 8 countries and regions, 36

major ports, 48 trade lanes

– Highest density in Northeast Asia

Market

– Wide range of shipping options for

customers

High Frequency

– One of the highest service

frequencies in intra-Asia

– 242 port calls per week

– Highest service frequency in

Northeast Asia Market

– Higher flexibility in scheduling for

customers

Our Container Shipping Network

We operate a high frequency and high density service model.

3

10 Business Highlights

Note: As of June 30, 2010.

Manila

Tokyo

Advantage of Our Network Driven Model

Hong Kong

Shanghai

Bangkok

Ho Chi Ming

Model Network Driven Model Hub-Spoke Model

Players SITC Other container shipping companies

Illustrative

Diagram

Objective Maximize overall vessel load factors Fill large vessel on the long-haul route using small

feeder vessels

Resilience Adapt shipping routes to achieve optimal

overall load factors

Profitability may be affected due to inability to fill

large vessels during industry downturn

Routes Uses a combination of point-to-point,

continuous loop and network services

Able to flexibly combine different service

formats within network

Relatively linear routes that call at major ports

In contrast to many long-haul carriers and feeder service providers that use the hub-spoke shipping model,

our model seeks to optimize efficiency and profitability through our high-frequency, high-density short-haul

service network

Hong Kong

(Hub)

Feeder lines

connect various

points within

network to the hub

New York

(Hub)

Source: Drewry.

3

Pyeongtaek

Haiphong

11 Business Highlights

Single-Typed, Flexible Fleet Drives Our Network Driven Model

Our single-typed fleet provides us with higher flexibility and lower vessel costs, and is fundamental to our

network driven model.

3

86%

14%

Young fleet with average age of 5.7 years. Younger

vessels are more efficient, technologically advanced and

have lower maintenance cost

1,000 TEU type vessel best suits our business model in

terms of space utilization, operating efficiency and speed

Lower operating cost from lower port charges and lower

maintenance cost as a result of fleet standardization

Uniformed fleet provides higher flexibility in allocating

vessels along different routes1,000 TEU type

Other

36 of 42 Vessels are 1,000 TEU Type

Self owned

Chartered

15 Out of 42 Vessels Are Self Owned

Able to flexibly adjust fleet size to respond to changing

demand, with large proportion of chartered vessels on

one year charters

Self owned vessels purchased at relatively low cost,

providing long term cost advantage

36%

64%

12 Business Highlights

Note: As of June 30, 2010.

Stable and Experienced Management Team

80% of senior management team has been with us for over 10

years, with average shipping industry experience of about 20

years

Chairman and CEO each have over 30 and 20 years of

experience in the shipping logistics industry. Both were

awarded “Outstanding Person in the Shipping and Logistics

Industry over the 60 Years since 1949” by China

Communications and Transportation Association

Independent directors have diverse and international business

and finance experience

– Tsui Yung Kwok: 17 years of finance and accounting

experience; previously served on the board of several Hong

Kong listed entities

– Yeung Kwok On: Expert in organizational management and

human resource management; advisor for several

universities including Harvard University

– Dr. Lo Wing Yan, William: PhD from Cambridge University;

strong international experience in a wide range of business;

adjunct professor at several Hong Kong universities; and

independent director for several listed companies

– Dr. Ngai Wai Fung: Expert in corporate governance; served

as company secretary for China Unicom, ICBC Asia, and

other well-known listed companies; and is currently an

independent director of several listed companies

Management has excellent industry and management acumen,

strong grasp of the industry cycle and strong ability to identify

and mitigate potential risks

Our stable and experienced management team has been critical to our success.

4

Board of Directors

Management Team

13 Business Highlights

Management Team Has Strong Grasp of Industry Cycle

1,000 – 1,100 TEU New-Build Prices

10

15

20

25

30

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Clarksons, Company.

Our management team has strong grasp of the industry cycle, purchasing a majority of our vessels at

relatively low prices, giving us a long term cost advantage

(US$ million)

4

Purchased 2

ships in 2001

1,694 TEU

Purchased 4

ships in 2004

3,628 TEU

Purchased 1

ship in 2007

938 TEU

Purchased 3

ships in 2003

2,493 TEU

40%

drop

Purchased 3

ships in 2009

3,048 TEU

Purchased 2

ships in 1998

1,574 TEU

14 Business Highlights

3. Business Strategy

Business Strategy

Strengthen and Expand Our Intra-Asia Service Network, and Replicate Our Integrated Services Model

Throughout Our Network1

Expand Fleet and Optimize Composition2

Seek Opportunities for Complementary Acquisitions and Partnerships3

Northeast Asia Market: Solidify our leading position and create additional headroom for growth. Expand into

South China and Northeast Asia countries trade

Southeast Asia Market: Capture growth opportunities through route and network expansion

Acquire new sites to build warehousing and other logistics facilities near ports

Replicate integrated services model throughout intra-Asia network, beginning with Ningbo, Shanghai and

Vietnam.

Enhance Information Technology Systems4

Take advantage of attractive new build prices to expand our fleet and further solidify our long term cost

advantage

Expand self-owned fleet by 15 to 25 vessels by 2013

Our long term objective is to be a world-class integrated logistics service provider.

15 Business Strategy

4. Financial Information

6.0%10.3%

4.9%

14.1% 14.6% 16.1%

15.4%

15.3%

Financial Snapshot

(US$ million)

Net Income and Net Income Margin

Gross Profit and Gross Profit Margin

88.634.3 35.4 37.1

32.5

4.6

2007 2008 2009 9M 2010

6.0%4.6%

13.7%

5.3%

Share based

compensation

Profit from continuing

operationsMargin

(US$ million) Sea Freight Logistics Land-Based Logistics

24.459.6 77.031.8

40.7

43.8

47.756.2

100.4

70.0

124.7

26.2

2007 2008 2009 9M 2010

16 Financial Information

353.7497.0

346.1

222.7

274.9264.0

301.3

576.4

771.9694.2

647.4

430.1

2007 2008 2009 9M 2010

Revenue

(US$ million) Sea Freight Logistics Land-Based Logistics

(%)

Return on Equity and Return on Assets

85.1%

42.6%

32.6%41.1%

13.6% 11.3% 10.2%14.8%

2007 2008 2009 1H 2010

Return on equity Return on assets

Sea Freight Logistics Revenue and Profitability

11.7%

58.4%29.9%

Equipment and cargo transportation

Voyage

Vessel

Container Shipping Volume and Freight Rate

845

1,0801,187

846995

2007 2008 2009 9M

2009

9M

2010

300

400

500

600

2007 2008 2009 9M

2009

9M

2010

Container Shipping Volume

(Thousand TEU)

Average Freight Rate

(US$/TEU)

(1) Revenue before inter-segment elimination.

Cost of Sales Breakdown

Container handling costs

Container rental and

depreciation

Slot swap expenses

Other container handling

and equipment related

costs

Time-charter fees

Vessel crew

expenses

Vessel depreciation

and maintenance

24.4

59.6

26.2

4.0

77.0

4.9%

15.4%

6.0%

10.3%1.1%

2007 2008 2009 9M 2009 9M 2010

Margin

Gross Profit and Margin

Fuel

Port charges

9M 2010 Cost of Sales Breakdown

(%)(US$ million)

408.1

580.1534.1

373.0

499.7

2007 2008 2009 9M 2009 9M 2010

Sea Freight Logistics Revenue(1)

(US$ million)

17 Financial Information

12.0% 12.5% 13.8%17.1%

13.2%

38.2% 36.7%

48.3%45.5%

43.0%

14.1% 14.6% 16.1%19.6%

15.3%

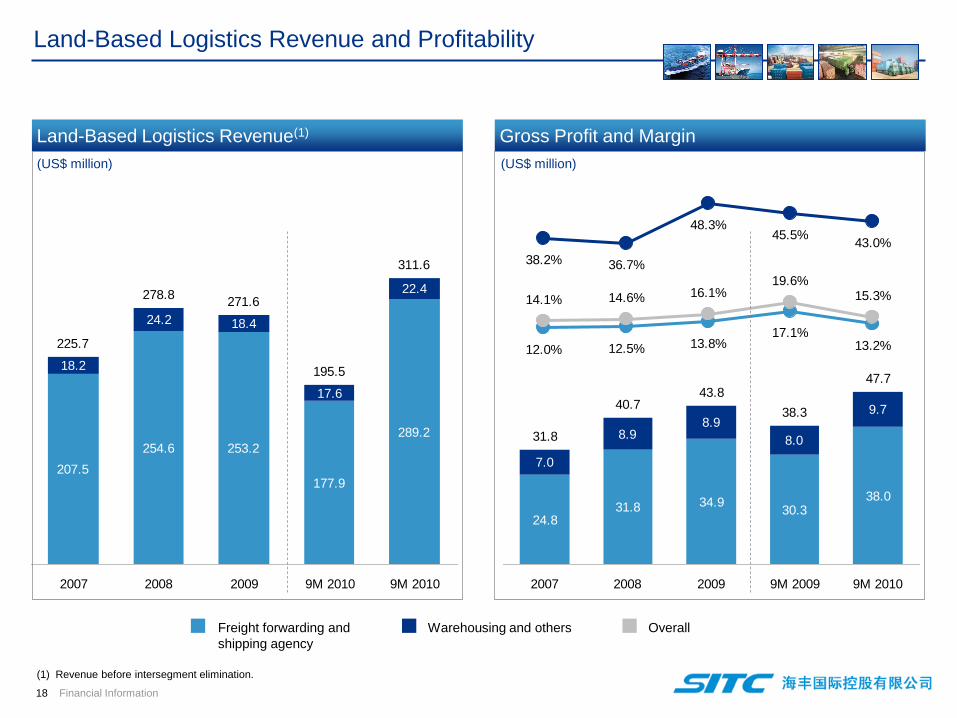

Land-Based Logistics Revenue and Profitability

24.831.8 30.3

38.0

7.0

8.9 8.0

9.7

31.8

40.743.8

38.3

47.7

34.9

8.9

2007 2008 2009 9M 2009 9M 2010

Land-Based Logistics Revenue(1)

207.5

254.6

177.9

289.2

18.2

24.2 18.4

17.6

22.4

225.7

278.8271.6

195.5

311.6

253.2

2007 2008 2009 9M 2010 9M 2010

Freight forwarding and

shipping agency

Warehousing and others

(US$ million)

Gross Profit and Margin

Overall

(US$ million)

(1) Revenue before intersegment elimination.

18 Financial Information