october 2015 u.s. employment update and outlook

TRANSCRIPT

U.S. employment situation: September 2013

Release date: October 22, 2013

September’s monthly growth was below

average, but is only one part of the picture

U.S. employment situation: September 2015 October 2, 2015

September 2015 employment summary

• September’s jobs figures were below expectations, with only 142,000 jobs added and August downwardly revised to 136,000. Although some

of this may be attributed to seasonality, strong external fundamentals such as consumer confidence, spending and private investment as well

as labor metrics highlighting improved employee confidence and an increasing number of job openings signal that slower figures may be the

result of an impending talent crunch.

- A labor shortage will likely lead to further wage growth in a low-inflation environment, boosting spending and, in turn, GDP growth. Hourly

wages are up 2.2 percent across the private sector, with this figure rising to 2.8 percent for professional and business services.

- Faster rates of wage growth are occurring in a time of low inflation due to fluctuating energy prices muting the overall consumer price index.

As a result, wage growth will have a greater impact than it otherwise would, with retail spending providing a boost to the economy.

• Unemployment for both the country as a whole and college graduates remained flat at 5.1 and 2.5 percent, respectively. Total unemployment

fell sharply by 30 basis points to 10.0 percent and will almost certainly reach the single digits at some point later this year. In September, the

civilian labor force contracted by 350,000 people and participation declined to 62.4 percent; combined with relatively sustained growth

elsewhere, which helped to push down the unemployment rate.

• Office-using industries contributed just 43,000 jobs to September’s growth, continuing a trend of somewhat muted office-using employment

gains. After a few months of improving fundamentals, the financial activities subsector saw no new growth, while previously lagging

information grew by 12,000 net new jobs. Due to the national slowdown in growth, this kept office-using industries’ contribution to national

gains at 30.3 percent.

• At the market level, Silicon Valley and San Francisco remain powerhouses, with total non-farm employment up 5.5 and 4.6 percent over the

year, respectively, and office-using gains even higher at 9.9 and 7.2 percent, respectively. Similarly, tech hubs such as Portland, Seattle and

Austin are posting additions ranging from 3.4 to 4.0 percent. Even in slower-growth Midwestern and Northeastern markets such as Chicago,

Philadelphia, St. Louis and Milwaukee, gains 1.0 percent or greater.

Source: JLL Research, Bureau of Labor Statistics

September 2015 labor market at a glance

+142,000 (60 consecutive months

of growth) 1-month net change

+2,752,000 (+2.0 y-o-y)

12-month change

+788,000

10-year average annual growth

Source: JLL Research, Bureau of Labor Statistics

5.1%

Unemployment rate

-80bp

12-month change in unemployment

7.0%

10-year average unemployment

5,753,000 (+21.7% y-o-y)

Job openings

4,983,000 (-0.4% y-o-y)

Hires

2,695,000 (+6.0% y-o-y)

Quits

September continued the slower growth seen in August; three-

month trailing total stands at 501,000 new jobs

360,

000

226,

000

243,

000

96,0

00

110,

000

88,0

00

106,

000

122,

000

221,

000

183,

000

164,

000 19

6,00

0 36

0,00

0 22

6,00

0 24

3,00

0 96

,000

11

0,00

0 88

,000

16

0,00

0 15

0,00

0 16

1,00

0 22

5,00

0 20

3,00

0 21

4,00

0 19

7,00

0 28

0,00

0 14

1,00

0 20

3,00

0 19

9,00

0 20

1,00

0 14

9,00

0 20

2,00

0 16

4,00

0 23

7,00

0 274,

000

84,0

00

166,

000

188,

000 22

5,00

0 33

0,00

0 23

6,00

0 28

6,00

0 24

9,00

0 21

3,00

0 250,

000

221,

000

423,

000

329,

000

201,

000

266,

000

119,

000

221,

000 26

0,00

0 24

5,00

0 22

3,00

0 13

6,00

0 14

2,00

0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep

-15

1-m

onth

net

cha

nge

4

Source: JLL Research, Bureau of Labor Statistics

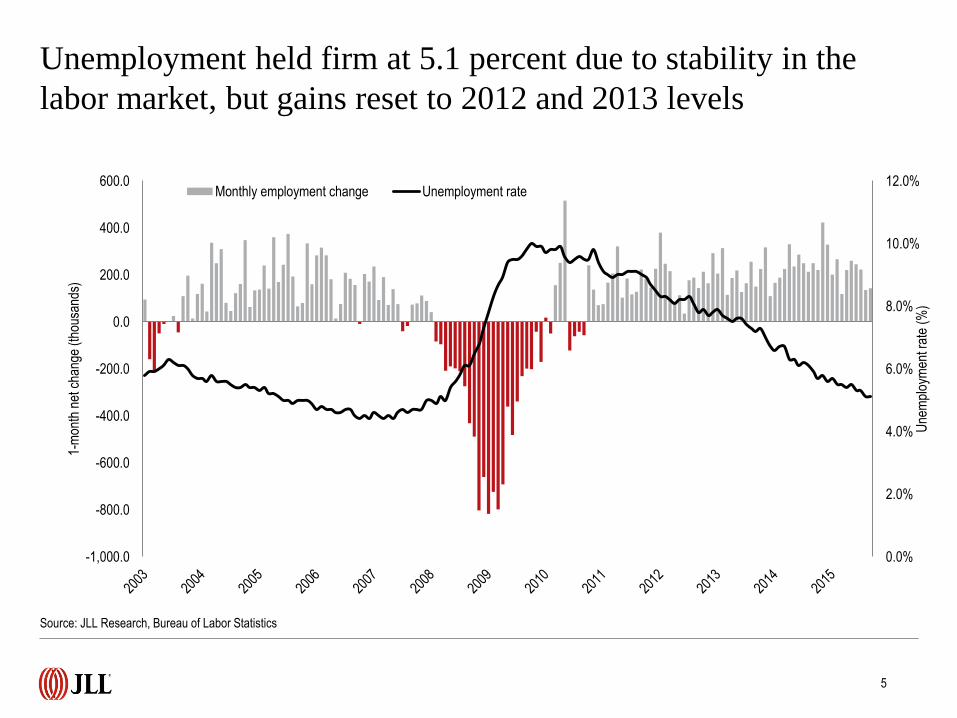

Unemployment held firm at 5.1 percent due to stability in the

labor market, but gains reset to 2012 and 2013 levels

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

Une

mpl

oym

ent r

ate

(%)

1-m

onth

net

cha

nge

(tho

usan

ds)

Monthly employment change Unemployment rate

Source: JLL Research, Bureau of Labor Statistics

5

As corporates’ search for talent intensifies, job openings have

risen by 21.7 percent over the year

Source: JLL Research, Bureau of Labor Statistics

6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Job

open

ings

(th

ousa

nds)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Con

sum

er c

onfid

ence

inde

x In contrast to jobs, consumer confidence rose to a near-high

during the recovery of 103 points in September

Source: JLL Research, Bureau of Labor Statistics

7

-12.0

-9.0

-5.0

-4.1

-4.0

-0.7

0.0

1.0

2.1

3.5

4.6

8.0

12.0

23.7

24.0

29.0

31.0

35.0

36.4

-20 -10 0 10 20 30 40

Mining and logging

Manufacturing

Durable goods

Wholesale trade

Nondurable goods

Utilities

Financial activities

Other services

Motor vehicles and parts

Transportation and warehousing

Temporary help services

Construction

Information

Retail trade

Government

Education and health services

Professional and business services

Leisure and hospitality

Health care and social assistance

1-month net change (thousands)

While health, leisure and PBS remained somewhat healthy,

financial activities and transportation stalled in September

Source: JLL Research, Bureau of Labor Statistics

8

Leisure and hospitality

PBS

Education and health

All other subsectors

Top three

subsectors

responsible for

66.9 percent of

monthly

growth.

Manufacturing and mining saw another month of contractions,

bringing down goods-producing employment once again

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

2008 2009 2010 2011 2012 2013 2014 2015

1-m

onth

net

cha

nge

(tho

usan

ds)

Goods-producing Service-providing

Source: JLL Research, Bureau of Labor Statistics

9

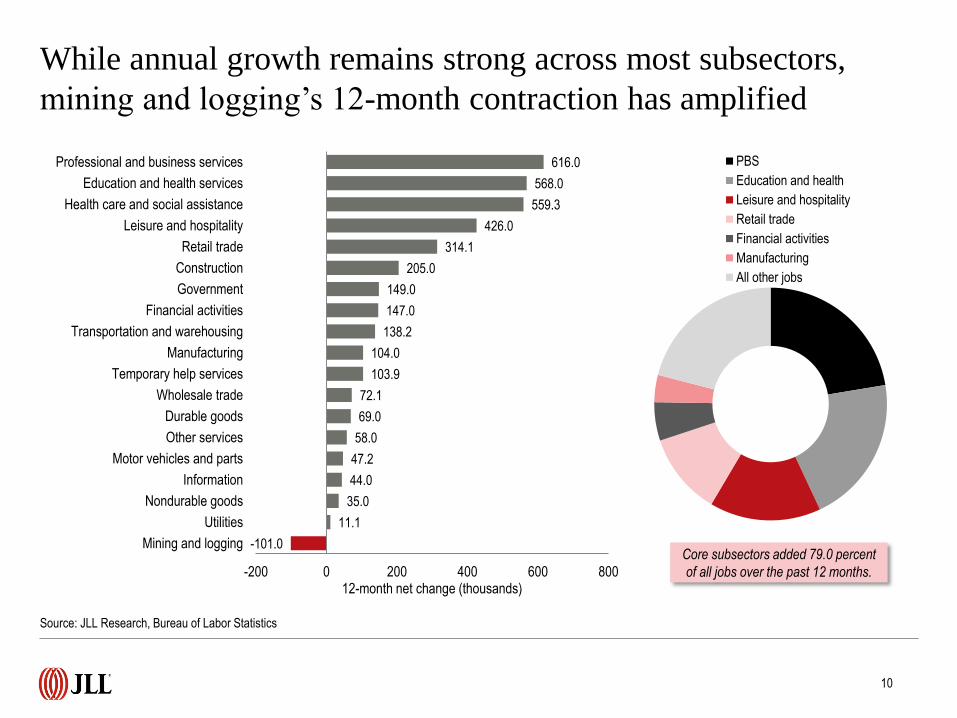

-101.0

11.1

35.0

44.0

47.2

58.0

69.0

72.1

103.9

104.0

138.2

147.0

149.0

205.0

314.1

426.0

559.3

568.0

616.0

-200 0 200 400 600 800

Mining and logging

Utilities

Nondurable goods

Information

Motor vehicles and parts

Other services

Durable goods

Wholesale trade

Temporary help services

Manufacturing

Transportation and warehousing

Financial activities

Government

Construction

Retail trade

Leisure and hospitality

Health care and social assistance

Education and health services

Professional and business services

12-month net change (thousands)

PBS

Education and health

Leisure and hospitality

Retail trade

Financial activities

Manufacturing

All other jobs

While annual growth remains strong across most subsectors,

mining and logging’s 12-month contraction has amplified

Source: JLL Research, Bureau of Labor Statistics

10

Core subsectors added 79.0 percent

of all jobs over the past 12 months.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Une

mpl

oym

ent (

%)

As the talent crunch approaches, unemployment for college

graduates remains at a low of 2.5 percent, challenging

companies to hire

Source: JLL Research, Bureau of Labor Statistics

11

Tech maintains its 6.1-percent annual increases, while energy

remains in falling mode and total non-farm remains positive, but

slips to 2.0 percent growth

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2008 2009 2010 2011 2012 2013 2014 2015

High-tech Energy, Mining, and Utilities Office-using industries Total non-farm

Source: JLL Research, Moody’s. Note: Due to data lags, high-tech employment only available through July 2015.

12

12-m

onth

% c

hang

e (jo

bs)

Tech job creation hovers slightly above 6.0 percent with

sustained industry demand Year-on-year percent employment growth

Source: JLL Research, Bureau of Labor Statistics

13

Weekly claims over the course of 2015 have fallen to an average

of around 275,000

Source: JLL Research, U.S. Department of Labor

14

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Cla

ims

Initial claims 4-week moving average

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Hire

s an

d qu

its (

thou

sand

s)

Hires Quits

Hires have been relatively stable over the past few months,

while quits remain on the rise

Source: JLL Research, Bureau of Labor Statistics

Tech hubs remain dominant and comprise most markets with

significant employment gains over the past year

Source: JLL Research, Bureau of Labor Statistics

16

Silicon Valley

5.5%

San

Francisco

4.6%

Portland

4.0%

Austin

3.4% Fort

Lauderdale

3.6%

Salt Lake

City

3.7%

Seattle

3.7%

Some East Coast and Midwestern markets are still growing

slower, but have seen a small bump of late

17

Source: JLL Research, Bureau of Labor Statistics

Richmond

-0.2%

Philadelphia

1.1%

Chicago

1.0% Milwaukee

1.2%

Kansas City

1.2% St. Louis

1.2%

Total unemployment dropped by 30 basis points to 10.0

percent; will likely fall into the single digits later this year

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Total unemployment U-6 10-year average

Source: JLL Research, Bureau of Labor Statistics

18

At 62.4 percent, labor force participation declined once again

(-20bp), keeping unemployment low as well

Source: JLL Research, Bureau of Labor Statistics

19

60.0%

61.0%

62.0%

63.0%

64.0%

65.0%

66.0%

67.0%

2008 2009 2010 2011 2012 2013 2014 2015

Labo

r fo

rce

part

icip

atio

n ra

te (

%)

A boost in information and stable PBS growth kept office-using

contribution to total at 30.3 percent despite flat financial figures

Source: JLL Research, Bureau of Labor Statistics

20

After months of increase, financial activities saw no net new job

growth in September; information spiked by 12,000 jobs

-300

-250

-200

-150

-100

-50

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015

Information Professional and business services Financial activities

Source: JLL Research, Bureau of Labor Statistics

21

Temporary employment continues to rise, but has been revised

downward in recent months

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

2009 2010 2011 2012 2013 2014 2015

Tem

pora

ry h

elp

serv

ices

(th

ousa

nds)

Mon

thly

net

cha

nge

in jo

bs (

ths)

Temporary employment monthly net change Temporary employment

Source: JLL Research, Bureau of Labor Statistics

22

©2015 Jones Lang LaSalle Research IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

For more information, please contact:

Ben Breslau

Managing Director - Americas Research

Phil Ryan

Research Analyst – Office and Economy Research

Or, find more employment, business and real estate

research at jll.com.

>>> Click here to check it out.