of niche domination financial planning - fpam · chapter updates p 42 fpam diary ... – jose rizal...

TRANSCRIPT

p 14

www.fpam.org.my

KKDN PP 11977/3/2008 Vol 7, No. 2, 2Q 2007

Datuk Bridget LaiGroup CEO, Alliance Bank Malaysia Bhd

p 10

p 34

p 32

p 19

p 8

Educat ion • Examinat ion • Experience • Ethics

OfNiche

Financial Planning&Domination

CFP Global Updates

Bank Negara-FPAM Financial Education Roadshow 2007

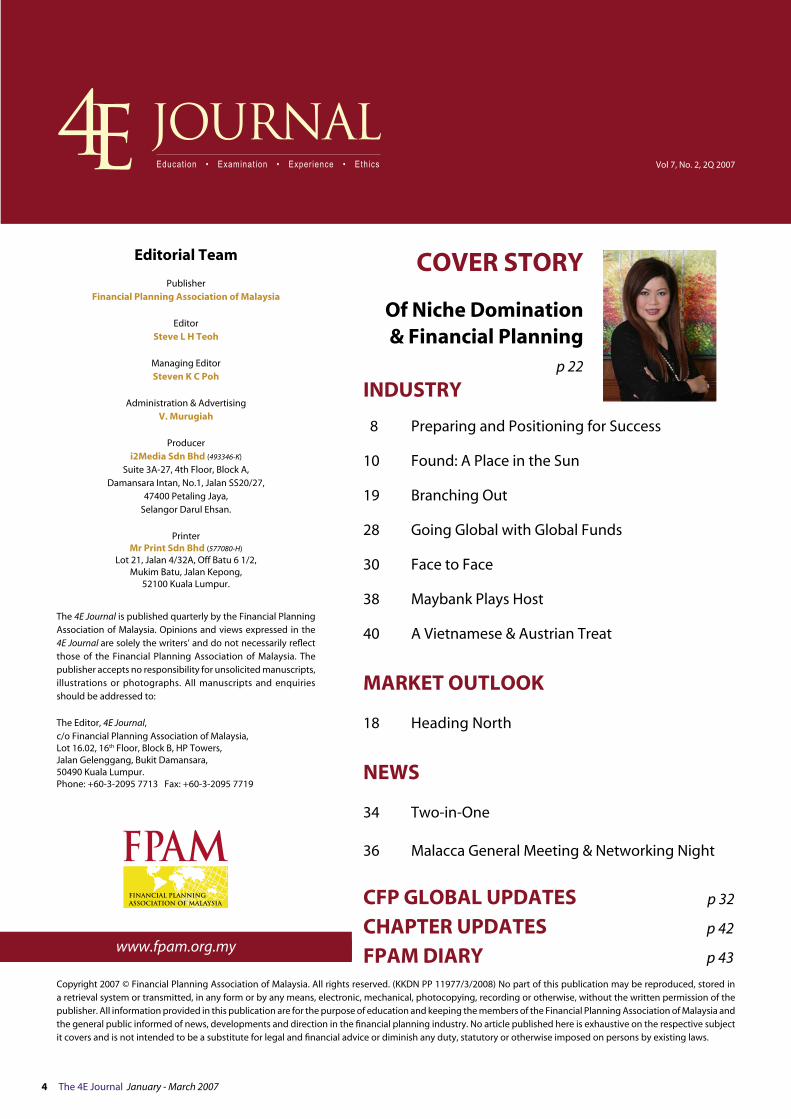

INDUSTRY

Preparing & Positioningfor Success

Found: A Place inthe Sun

Branching OutEducating the Grassroots

NEWS

Two-in-OneFancy an MSc (MAP)/CFP Combo?

MARKET OUTLOOK

Heading NorthDespite some recent bump rides, the KLCI is still poised to grow

C

M

Y

CM

MY

CY

CMY

K

145196 Left Ad D3 30-5.ai 63.25 lpi 71.57° 30/5/07 10:04:35 PM145196 Left Ad D3 30-5.ai 63.25 lpi 18.43° 30/5/07 10:04:35 PM145196 Left Ad D3 30-5.ai 66.67 lpi 0.00° 30/5/07 10:04:35 PM145196 Left Ad D3 30-5.ai 70.71 lpi 45.00° 30/5/07 10:04:35 PMProcess CyanProcess MagentaProcess YellowProcess Black

C

M

Y

CM

MY

CY

CMY

K

145196 Right Ad D3 30-5.ai 63.25 lpi 71.57° 30/5/07 10:05:47 PM145196 Right Ad D3 30-5.ai 63.25 lpi 18.43° 30/5/07 10:05:47 PM145196 Right Ad D3 30-5.ai 66.67 lpi 0.00° 30/5/07 10:05:47 PM145196 Right Ad D3 30-5.ai 70.71 lpi 45.00° 30/5/07 10:05:47 PMProcess CyanProcess MagentaProcess YellowProcess Black

4 The 4E Journal January - March 2007

www.fpam.org.my

Vol 7, No. 2, 2Q 2007

INDUSTRY

8 Preparing and Positioning for Success

10 Found: A Place in the Sun

19 Branching Out

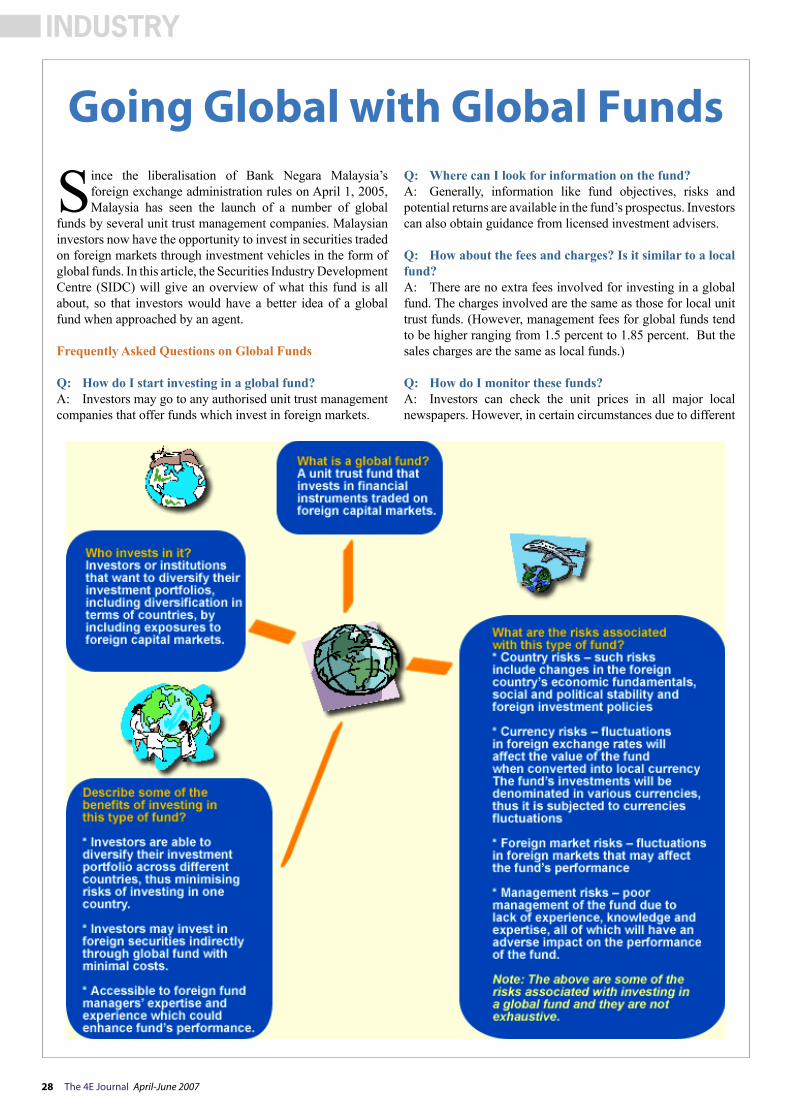

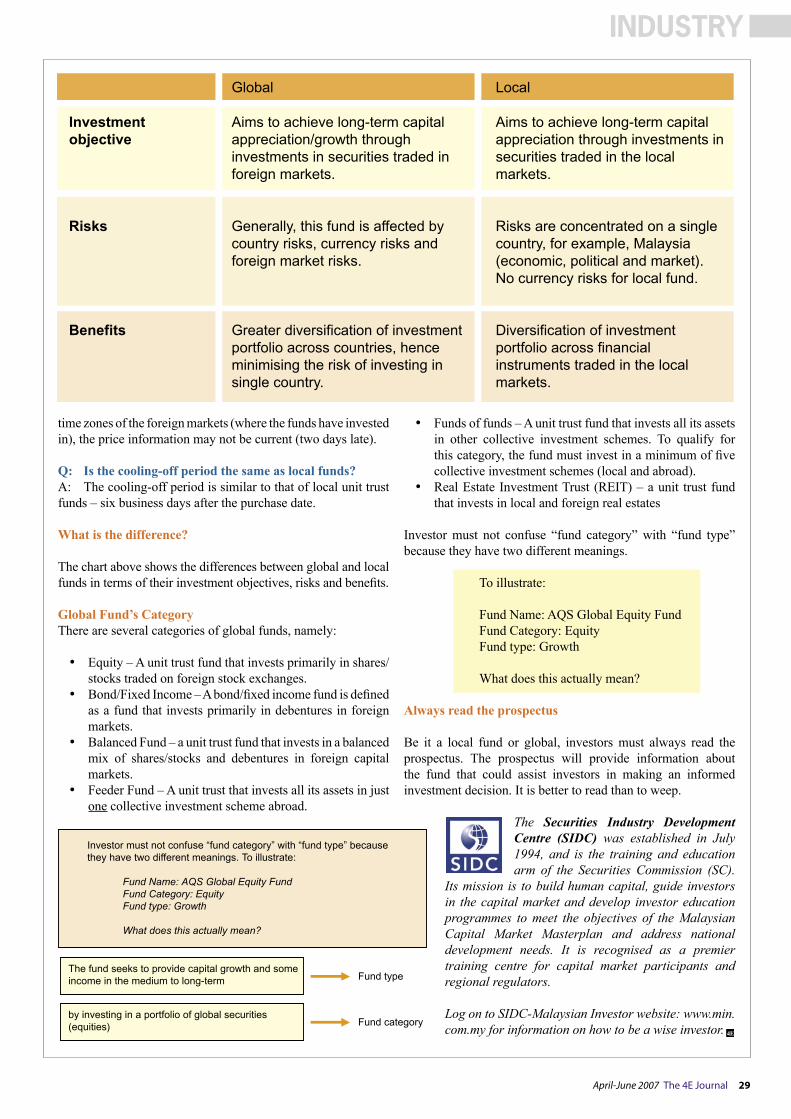

28 Going Global with Global Funds

30 Face to Face

38 Maybank Plays Host

40 A Vietnamese & Austrian Treat

MARKET OUTLOOK

18 Heading North

NEWS

34 Two-in-One

36 Malacca General Meeting & Networking Night

CFP GLOBAL UPDATES p 32

CHAPTER UPDATES p 42

FPAM DIARY p 43

Editorial Team

PublisherFinancial Planning Association of Malaysia

EditorSteve L H Teoh

Managing Editor Steven K C Poh

Administration & Advertising V. Murugiah

Produceri2Media Sdn Bhd (493346-K)

Suite 3A-27, 4th Floor, Block A,Damansara Intan, No.1, Jalan SS20/27,

47400 Petaling Jaya, Selangor Darul Ehsan.

PrinterMr Print Sdn Bhd (577080-H)

Lot 21, Jalan 4/32A, Off Batu 6 1/2,Mukim Batu, Jalan Kepong,

52100 Kuala Lumpur.

The 4E Journal is published quarterly by the Financial Planning Association of Malaysia. Opinions and views expressed in the 4E Journal are solely the writers’ and do not necessarily reflect those of the Financial Planning Association of Malaysia. The publisher accepts no responsibility for unsolicited manuscripts, illustrations or photographs. All manuscripts and enquiries should be addressed to:

The Editor, 4E Journal, c/o Financial Planning Association of Malaysia, Lot 16.02, 16th Floor, Block B, HP Towers, Jalan Gelenggang, Bukit Damansara, 50490 Kuala Lumpur. Phone: +60-3-2095 7713 Fax: +60-3-2095 7719

Copyright 2007 © Financial Planning Association of Malaysia. All rights reserved. (KKDN PP 11977/3/2008) No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the written permission of the publisher. All information provided in this publication are for the purpose of education and keeping the members of the Financial Planning Association of Malaysia and the general public informed of news, developments and direction in the financial planning industry. No article published here is exhaustive on the respective subject it covers and is not intended to be a substitute for legal and financial advice or diminish any duty, statutory or otherwise imposed on persons by existing laws.

COVER STORY

Of Niche Domination& Financial Planning

p 22

��������������������������������������������������������� ���������������������

April-June 2007 The 4E Journal 7

EDITORIAL

“As the people are, so too is their government.”– Jose Rizal

La Mome

Dear readers,

Virtually in an eye blink, the half-year is upon us. So what has it been like, in particular since the last time we ‘met’ in the first quarter issue of the 4E Journal?

In one word: eventful. From collapsing ceilings and broken water pipes that render brand new, high-profile public buildings temporarily unfit for use; to published photographs of allegedly crooked lawyers, to sexist bocor-ranting MPs; and to the discriminatory lobbying of the Home Affairs Minister not to allow the ‘little dragon ladies’ from China to work as house maids here because “they come to Malaysia and cause havoc to families by enticing the husbands.” There is never a dull moment for sure. In fact of late, I am always up early to greet the newspaper man!

In Corporate Malaysia, names like NasionCom, Transmile, Wimens, SBB, and the latest, Megan Media, became famous virtually overnight. But for all the wrong reasons due to financial irregularities. Meanwhile, the contrarian bull market continues to sustain its charge, breaching record highs like never before.

Nobody drowned at the recent major flash floods in downtown Kuala Lumpur despite having spent RM1.9 billion on yet another world’s first engineering feat – this time, a flood mitigating tunnel called SMART!

But so what. Malaysians are truly a most forgiving lot. Nobody owns up to any mistakes – moral, criminal, negligence or otherwise. Any of course, virtually no one resigns in shame or gets fired for doing wrong either, much less jailed. The sun still shines bright in blessed Malaysia.

Even our Honourable Prime Minister got married again. Surely between him and those that are keeping the bull in town, they must know something more than you and I. We truly are living in very ‘colourful’ times. And perhaps we should count our blessings and look at life through rose-tinted glasses because we are so blessed that we can.

Moving closer to home, our AGM is now behind us and you have a one-third new Board, charged with a fresh mandate to serve your interests for another two-year term. As a quick update, FPAM is now 10,200 members strong, supported by no less than 42 Charter and Corporate institutional members made up of the most diverse representations from the who’s who of the financial services industry. Looking at the make-up of the new Board of Governors, I am confident that your Association is still in good hands!

On the industry front, June saw the Securities Commission (SC) covering the final consultative leg engaging the industry players and stakeholders for official feedback on the impending introduction of the much lobbied Single Licensing Framework. A comprehensive market licensing consolidation undertaking, it will rationalise all the current securities legislations culminating in the Capital Markets & Services Act 2007 (CMSA). Suffice to say inter alia, it provides for the much awaited provision for licensed financial planners to distribute different unit trust schemes. This will be another industry milestone covered.

Working in tandem with Bank Negara, June 22 will also see a forum facilitated by the SC on the proposed “Mutual Recognition between Financial Planners and Financial Advisers.” As the title suggests, the objective is to minimise the regulatory burden on the industry. As always, there will be FPAM representation to proffer our views and comments.

And finally, La Mome, a movie biography of one of the most celebrated French singer – Edith Piaf. She was brought up in a whorehouse as a child in the most heart-rendering environment of abject poverty in the poorer part of Paris during the depression years between the World Wars. From her childhood to her glory, from her victories to her pains, the movie portrays so vividly the complexity of a both frail and indestructible character.

More importantly, of the singer’s resolve and determination to be the best in her chosen calling. And then, the final encore to her short chequered career, her signature song La Vie en Rose (no regrets) she made so famous that it became synonymous with Edith Piaf herself.

Despite the sad and poignant life that she led, one could see so much grace from within her as portrayed in her song about her life of ‘no regrets.’ It just begs the question for me, as to whether I will feel the same way after I retire practising as a financial planner – having touched the lives of my clients, many of whom have become my friends.

Till we meet again, here’s wishing you, “Happy Thoughts Always!”

Steve L H Teoh, CFPEditor, Deputy President & Chairman of the Board of Membership [email protected].

8 The 4E Journal April-June 2007

Preparing and Positioningfor Success

By Vern C. Hayden, CFP®

INDUSTRY INDUSTRY

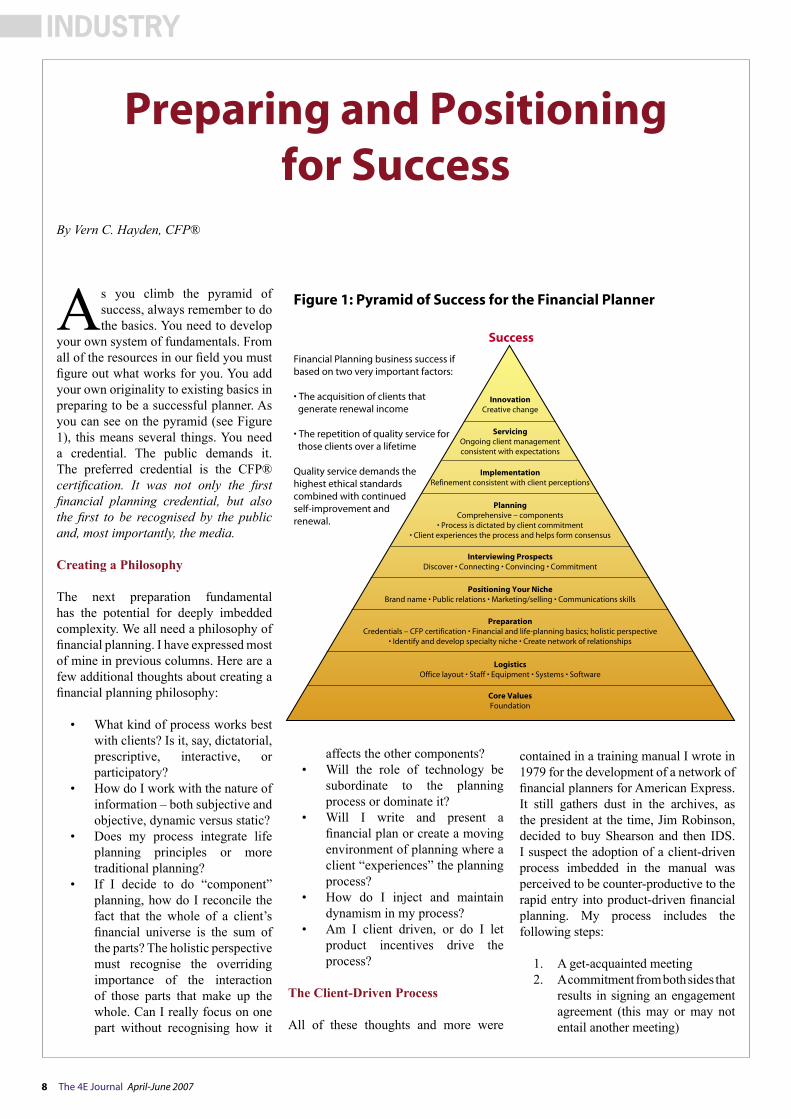

As you climb the pyramid of success, always remember to do the basics. You need to develop

your own system of fundamentals. From all of the resources in our field you must figure out what works for you. You add your own originality to existing basics in preparing to be a successful planner. As you can see on the pyramid (see Figure 1), this means several things. You need a credential. The public demands it. The preferred credential is the CFP® certification. It was not only the first financial planning credential, but also the first to be recognised by the public and, most importantly, the media. Creating a Philosophy

The next preparation fundamental has the potential for deeply imbedded complexity. We all need a philosophy of financial planning. I have expressed most of mine in previous columns. Here are a few additional thoughts about creating a financial planning philosophy:

• What kind of process works best with clients? Is it, say, dictatorial, prescriptive, interactive, or participatory?

• How do I work with the nature of information – both subjective and objective, dynamic versus static?

• Does my process integrate life planning principles or more traditional planning?

• If I decide to do “component” planning, how do I reconcile the fact that the whole of a client’s financial universe is the sum of the parts? The holistic perspective must recognise the overriding importance of the interaction of those parts that make up the whole. Can I really focus on one part without recognising how it

affects the other components?• Will the role of technology be

subordinate to the planning process or dominate it?

• Will I write and present a financial plan or create a moving environment of planning where a client “experiences” the planning process?

• How do I inject and maintain dynamism in my process?

• Am I client driven, or do I let product incentives drive the process?

The Client-Driven Process

All of these thoughts and more were

contained in a training manual I wrote in 1979 for the development of a network of financial planners for American Express. It still gathers dust in the archives, as the president at the time, Jim Robinson, decided to buy Shearson and then IDS. I suspect the adoption of a client-driven process imbedded in the manual was perceived to be counter-productive to the rapid entry into product-driven financial planning. My process includes the following steps:

1. A get-acquainted meeting2. A commitment from both sides that

results in signing an engagement agreement (this may or may not entail another meeting)

������������������������������������������������������

��������������������������������������������������������������������������

�����������������������������������������������������������

�����������������������������������������������������������������������

�����������������������������������������������������������������������������������������������������������

�������

�������������������������

���������������������������������������������������������������

�����������������������������������������������������������

����������������������������������

���������������������������������������������������������������������������������������������������

���������������������������������������������������������������������

�����������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������

���������������������������������������������������������������

���������������������

April-June 2007 The 4E Journal 9

INDUSTRY INDUSTRY

3. An on-going discovery process, obtaining all subjective and objective information from a client (one or more meetings, phone calls, faxes, and so on)

4. The problem-solving process, which generally involves identifying, prioritising, and creating a way to resolve the various issues at stake (for example, a process driven by research coordinated with appropriate parties, model development, probabilistic thinking/discussions, and agendas for each meeting)

5. Implementation, a natural result of examining alternatives, which is executed incrementally

6. On-going monitoring and periodic meetings to assess the effectiveness of tactics and strategies

All meetings are summarised, assignments are made for each task, and implementation is specified where appropriate.

Your Niche

Once you have figured out how you are going to do financial planning with clients, you will find it extremely beneficial to identify and develop a specialty niche to get new clients. In other words, you want to be a known and recognised authority on one subject of financial planning. It’s a mistake to promote yourself as a “financial planner.” The public is confused as to its meaning. It’s perceived by many as a subterfuge to sell life insurance or stocks or other products. That’s not the way we want it to be but that’s the real world.

An example of a niche is Tim Kochis in San Francisco. He is the acknowledged expert for corporate executives and their problems. Tim is especially unique in that his niche not is only used by corporations but also by financial planners. I gladly paid US$125 for his latest expert book, titled Managing Concetrated Stock Wealth.

Another example of a niche is the famous and entertaining Ed Slott. He’s never met an IRA he couldn’t dissect for the public or the planner.

In my own less luminescent way, I am known by a limited public as “Mr Mutual Fund.” Six years ago, Bill Griffeth, on CNBC, started introducing me as “Mr Mutual Fund” and saying, “Vern knows more about mutual funds than anybody I know.” This resonated with just enough of the public to bring us a number of new clients for both portfolio management and financial planning.

Here’s why creating one niche works. You are trying to penetrate the minds of people. The mind wants something simple to react to. You want to drive that one idea into the mind repeatedly. Simplicity requires that you narrow

the options and follow a single path; by simplifying a complex issue, you are making it easy for people to make a decision without too much thought. Using “financial planning” does not unravel the complexity of a perception; therefore, an otherwise good prospect is blocked from wanting to contact you.

Your niche is the leading weapon in engaging in marketing warfare. Many financial planners feel they must explode with all their expertise and information that makes them great. That’s a big mistake. Once you get the public’s attention over one great expert idea, you can gradually help a prospect who meets with you to discover and take advantage of your many other talents.

The final note at this level in preparing for success is to create a network of relationships. The obvious points here relate to targeting CPAs, attorneys

of various specialties, and other professionals who could refer clients. Nurture them and service them in meaningful ways. My experience has taught me that it is more productive to cultivate one or two in each category. It generally takes years – not weeks or months – to develop a relationship system.

Your Network

In the public relations area, build relationships with one or two business editors and television and radio producers. My purpose here is not to suggest how to do all this or write about how I have done it, but to make sure it’s on your checklist of things to do. That being said, I will suggest one way you can start a relationship with the business editor and producers. Contact them and let them know you realise they often need to find real-life people to develop a story line. Since you have, say, over 100 clients with varying circumstances, you would be willing to help them find the right individual or couple to help the producers with their story. That’s how I got on the ABC’s World News Tonight with Peter Jennings one evening.

Your Brand

Transcending all this preparation is the theme and next step of positioning your niche. This really means, how do you promote yourself via your brand specialty to get new clients? First, get a brand name. My old friend in San Francisco, Mitchell T. Curtis, got branded by the San Francisco Chronicle as “Mr Money Man.” It takes time to get others to give you a brand name – it took me four years before Bill Griffeth called me Mr Mutual Fund. That happened because every interview I did on CNBC was about mutual funds. It was generally about a manager or a controversial issue such as load versus no load.

Just last week, on CNBC, I mentioned the “Stephanie Powers Fund.’ This is the story behind American Funds’ Capital Income Builder Fund. Ms Powers was in charge of William Holden’s Trust, her companion for years. She knew almost nothing about managing money. One

“Once you have figured out how you are going

to do financial planning with clients, you will find it extremely beneficial to

identify and develop a specialty niche to get new

clients. In other words, you want to be a known

and recognised authority on one subject of

financial planning.”

Continues on page 18

10 The 4E Journal April-June 2007

Found: A Place in the Sun

INDUSTRY INDUSTRY

When piecing this story together, Stevie Wonder’s 1966 big hit – A Place in the Sun – kept ‘singing’ in this writer’s head. It was

more than 40 years ago since the song was first released, but the tune seemed to have taken on a new meaning when it comes to what the Great Vision Advisory Group has done with the business of financial planning in Malaysia. The first verse and chorus of the song (see right), this writer thought, were indeed significant and reflective of the state of affairs of the financial planning industry in this country. Do sing along if you know the song and take a moment to perhaps be philosophical about things.

What is your take on the development of the Malaysian financial planning industry?

The development of financial planning industry in Malaysia is still slow and this is expected due to the following market conditions: firstly, we are of the opinion that the market (or consumers) is totally confused at the moment as a result of the overlapping jurisdictions between the Securities Commission (SC) and Bank Negara Malaysia (Bank Negara). As a result, there are two different types of designation in the marketplace – the ‘financial planner’ and the ‘financial adviser.’ At this juncture, we feel the regulators still lack the understanding of what the consumers really want (issues of cost versus value of services received). The truth be told … consumers actually want value for the services rendered and not buying the cheapest products or services available.

Meanwhile, there are still so many unscrupulous ‘advisers’ who camouflage themselves as financial planners to further confuse the already confused consumers. There are even financial institutions hiding behind the cloak of wealth

management to market financial products. As such, financial planning or wealth management has been synonymous with selling of financial products. And because of this, the marketplace currently associates financial planning with investing and investment products and the only objective of doing this to make money. As practitioners, we know financial planning covers more that. In Malaysia, we are of the opinion the average consumer has yet to taste the ‘sweetness’ of real financial planning advice.

Where do you think it will go from here?

There is abundant liquidity in the marketplace looking for investment opportunities. And Malaysian consumers are increasingly becoming savvier in financial matters and more exposed to investment products from abroad. Nevertheless, until and unless key structural changes are made, we expect the industry to grow slowly, as can be seen now.

What are some of the obstacles hindering this nascent industry from moving forward?

Like a long lonely stream I keep runnin’ towards a dream Movin’ on, movin’ on Like a branch on a tree I keep reachin’ to be free Movin’ on, movin’ on.

Cause there’s a place in the sun Where there’s hope for everyone Where my poor restless heart’s gotta run There’s a place in the sun And before my life is done Got to find me a place in the sun ….

While the infant industry debates and grapples with viable business models for financial planning practitioners to adopt, Great Vision Advisory Group, headed by

its affable, managing director James Tan, quietly went about carving out a place in the sun for themselves in the Malaysian financial planning industry. He is aided by executive director and head of tax and financial planning Chua Tia Guan, whose passion for the profession and previous experience in tax and financial consulting at Arthur Andersen Private Client Services have been invaluable.

Tan and Chua spoke to Steven K C Poh, the managing editor of the 4E Journal recently about that place in the sun which Great Vision has carved out, and below are excerpts of the scintillating conversation.

April-June 2007 The 4E Journal 11

INDUSTRY INDUSTRY

As we have mentioned earlier, the confusing regulatory framework – overlapping of jurisdictions between the SC and Bank Negara. This has to be rectified as soon as possible to ensure the industry develops properly. Industry players, especially practitioners, are still grappling with a viable business model (fee only, commission only, or fee and commission, etc.) Meanwhile, consumers are confused whether financial planning is about financial products or actually planning their financial affairs. Financial institutions (be it banks, insurance companies, and unit trust management companies (UTMCs), whilst having a very big role to play in promoting and growing the industry don’t seem to be very supportive of the FA (financial adviser) and IA (investment adviser) models introduced by BNM and the SC. From our observation, they seem to be mainly concerned about protecting their own turf.

What can be done to enhance it? Both from a regulatory as well as industry perspectives?

The financial planning industry is made up of the regulators, practitioners and consumers.

We are of the opinion that all industry players, including financial planners, financial product distributors and financial product suppliers should be regulated by only one government agency, and not what is being practiced at the moment. And in order for this to happen, we need to consolidate or merge the designations of “investment adviser (financial planning)” (SC) and “financial adviser” (Bank Negara) into one designation or change the “financial adviser” (Bank Negara) designation to something else.

The regulators should also liberalise the equity and employment conditions imposed on financial planning firms to create a more dynamic and vibrant environment, and ensure that financial planners clearly list down their services and that these services are actually carried out – no more hiding behind the veil of financial planning, but in actual fact peddling financial products. In this regard, bank officers should not be allowed to call themselves financial advisers or wealth management advisers unless the financial institutions are, apart from their banking license, also separately licensed by the regulators to provide financial planning services like the IAs. As such, this will provide a level playing field between the IAs and the financial institutions.

Even so, we are of the opinion that more focus should be placed on financial planning advice, instead of what financial products to buy/invest in. As such, financial institution (be it banks, insurance companies and UTMCs) should allow licensed financial planners to market their products to support the development of industry.

Prior to financial planning being regulated by the SC, many agents (from the unit trust and insurance industry) called themselves financial planners. They no longer can, unless licensed by the SC. What is your view on this, taking into account Malaysia is still in the infant stage when it comes to financial planning?

We hold the view that it is imperative that financial planners

or financial planning firms should create their own branding to differentiate themselves from the rest of the service providers who called themselves ‘financial planners’ (insurance agents, unit trust agents and bank officers). The consumers have the right to know. There must be a clear demarcation between the roles of financial planners and insurance agents or unit trust

agents or bank officers so that the consumers are not confused. The public must also be educated to know the difference between financial planners and insurance agents or unit trust agents or bank officers. That said, we should not undermine the contributions of professional insurance and unit trust agents as majority of the insurance policies and unit trust funds in Malaysia are sold and not bought. This group of professionals have an important role to play in the greater marketplace.

Is the current regulatory environment conducive for the emerging industry? We are hearing more and more SC-licensed IA(FP) practitioners not renewing their licenses. Is this phenomenon indicative of ‘all is still not well’ with the industry?

Malaysian financial planning practitioners are currently curtailed by strict compliance requirements by the regulators. There is also a lack of viable business models for these planners in the marketplace – a perennial problem. The SC is pushing for the fee-only model due to the perception of more ‘independence’ on the part of the practitioners, whereas Bank Negara is pushing for ‘Financial Adviser’ model (whereby the license holder is able to market insurance products from more than one insurance company).

Tan: All industry players should be regulated by only one government agency

12 The 4E Journal April-June 2007

As a company, what are you doing to carve out a niche for yourself?

At Great Vision … we believe we are a different breed of financial planners who religiously uphold the code of ethics and always have the clients’ interest at heart. We believe with a high level of professionalism and branding, we can make a difference in the marketplace. We have had many meetings with the regulators, be it formal or informal to put forward our views in the hope of creating a more conducive environment for this emerging industry. We believe the financial planning industry is full of potential and is a business of the future. It all depends on how it is managed and regulated. In addition, it takes a lot of passion and patience to see results.

Exactly who is your target market (that special niche)?

Business owners – mainly the small and medium enterprises (SMEs) and some listed companies. They have the financial resources and their financial planning needs are more complex when compared to the regular men-on-the-street. Why SMEs you may ask. If you were to do the research, you will discover that approximately 99 percent of companies registered in Malaysia are SMEs. In addition to assisting our clients in financial planning and business succession planning, we also help them with tax planning. In short, we are very involved in our clients’ life. We find that very meaningful as there is a lifetime relationship established with them. People depend on you. So, you can say we actually do more than just financial

planning. We are essentially doing life planning as well as imparting values.

Increasingly ... in more mature markets, the independent financial planning practitioner is becoming more sought after. Do you see that happening in Malaysia? Why? or Why not?

It is already happening in Malaysia. In 2006, we have fees from financial services and training of about RM4 million. In any ‘infant’ market, there are always mature consumers. It all depends on whether a financial planner is capable and competent enough to win them over. When we provide advice to our clients we will put their interests first and provide them with the best solutions instead of looking for the cheapest deals in town. Generally, in an inefficient market condition, ‘best advice’ is difficult to achieve. Under these circumstances, ‘proper advice’ serves as an alternative.

We have created a niche market for ourselves at Great Vision. We believe our clients feel privileged to be associated with us. They feel secure because we always have their interests at heart in whatever we do. Our professionalism speaks for itself!

There is a ‘push’ right now to untie agents in order that they may be truly independent to serve the needs of their clients from a financial planning perspective. How do you view this development from a financial planning practitioner’s perspective?

Both the Capital Market Master Plan and Financial Sector Master Plan have stressed the importance of having truly independent financial planners or advisers to give the best possible advice. And as Lao Tzu put it, “The journey of a thousand miles starts with a single step.” So a good start would be for the regulators to ‘untie’ agents (insurance or unit trust) by allowing them to represent multiple principals. This would definitely be a step forward in making financial planners truly independent.

At Great Vision, we fully support the introduction of financial adviser’s license by Bank Negara and the independent unit trust agent (IUTA) model. This will enhance the objectivity of the recommendation of financial products by the agents, which we believe, will benefit the consumers at large. Incidentally, Great Vision Financial Advisory Sdn Bhd is the second company in Malaysia that was granted the financial adviser’s license by Bank Negara.

That said, we believe the IUTAs and tied-agents must be operating on a level playing field in order to encourage more practitioners to go for the truly independent model – not just in the compensation model (commission structure), but all other incidental financial support by the principal company such as incentives, office rental and marketing expenses. With the impending reduction in commissions, the idea of IUTAs having to bear their own cost of rental and marketing will definitely be a deterrent. The traditional ‘tied’ agent will not be enticed to venture into a truly independent financial planning environment.

INDUSTRY INDUSTRY

Chua: Creating his own brand

April-June 2007 The 4E Journal 13

How do you as an independent financial planning firm intend to participate in the emerging financial planning industry in Malaysia ... in terms of positioning services?

In the last few years, we have been putting our views through writing for various newspapers and magazines, speaking in public seminars, appearing on television and radio programmes to create the awareness on the importance of financial planning. We want Great Vision to be top of the public’s mind when it comes to financial planning matters.

We have positioned ourselves as the preferred wealth management adviser in the marketplace. We advise our clients holistically – from the personal, family and business perspectives. The reason: we believe our clients’ loyalty increase exponentially with the number of services provided by us to them. Our multi-disciplinary approach enhances clients’ loyalty and increase the revenue generated per client.

Our services are highly sought after in the small and medium enterprise (SME) market. In recognition of our services, we were awarded the Sahabat SMEs Award by the SMI Association of Malaysia alongside with DHL and Standard Chartered Bank in 2006.

What is Great Vision’s business model? How is it different from the existing models in the industry?

Before Great Vision was established, in the quest for a financial planning business model, we visited various countries including the U.S., Britain, Australia, Hong Kong, Singapore and Taiwan. Our conclusion: many business models currently practised overseas (including those which have been brought into Malaysia) are not suitable for Malaysia. Most of the business models are pretty much products based and have little or no focus on advice. As a result, we created our own business model, taking into account the unique Malaysian culture and values.

Great Vision provides integrated financial services to our clients and these services can be divided into the following categories:

• Human resource development services, which covers Personal Effectiveness Programme, Financial Wellness Programme, Corporate Effectiveness Programme and In-house Human Resource Development.

• Advisory services, which encompasses Personal Financial Planning, Business Financial Planning, Islamic Financial Planning as well as Tax and Business Advisory Services.

• Distribution of financial products, which covers business loans, mortgage loans, employee benefits insurance, general insurance, life insurance and unit trusts.

At Great Vision, everyone is treated as a business partner. As long as you are good and willing to work hard, the sky is the limit. In 2006, our human resource development and advisory services raked in a gross turnover of approximately RM4 million. We also assisted our clients to invest about RM200

million in unit trust funds, and we achieved about RM20 million in first year premiums for life insurance and about RM7 million in premium for employee benefits and general insurance.

Why do you think Malaysian financial planning practitioners are all going for the high net worth individuals in their pursuit of clients? Isn’t it a fact that the ‘not so high net worth’ individuals need more financial planning than the high net worth ones?

Marketplace reality, perhaps. And presumably the high net worth individuals are more able and more willing to pay for the financial planning services when compared to the ‘not so high net worth’ group. The difference between the high net worth folks and the not so high net worth folks is their level of financial complexity, which is why they will need to engage professional advisers to assist them on how to plan and manage.

What is stopping current financial planners from serving the ‘not so high net worth’ individuals’ financial planning needs? Lack of consumer awareness? Not interested in that market segment? Or simply lack of marketing funds?

The reluctance on the part of client to pay fees for advice is one big obstacle. If the high net worth clients see the value of your services, they would pay for it, mainly also because they can afford to. As for the ‘not so high net worth clients’ (generally we are talking about wage earners), in addition to their reluctance to pay fees, their financial affairs are also not so complex; so it much easier to deal with. In lieu of fees for advice, most financial planners would be remunerated through commissions when their clients invest in the products they recommend.

At the end of the day, everyone (be they high net worth or not) needs some form of a vehicle to invest, and financial products in the form of insurance, unit trusts, private fund management, and properties would constitute part of the solution in their overall financial plan.

So how are you doing it at Great Vision?

We adopt a ‘top down approach.’ With our seminars and conference targeting at the business owners (of SMEs), more often than not, the business owners become our ‘centre of influence’ on their board of directors, middle management and employees to be more receptive to financial planning services at different levels of need. This ‘corporate marketing strategy’ enables us to reach out to the high net worth individuals without neglecting the ‘not so high net worth’ ones. We believe everyone deserves good financial planning services.

How do you intend to grow your firm?

We completed Phase I of our expansion programme in 2006. We now have 10 offices nationwide to serve ours clients who are mainly SME business owners. We also plan to duplicating our business model regionally, particularly in the Asia Pacific region due to the similarities in culture and values.

INDUSTRY INDUSTRY

14 The 4E Journal April-June 2007

MARKET OUTLOOK MARKET OUTLOOK

By Anthony Dass

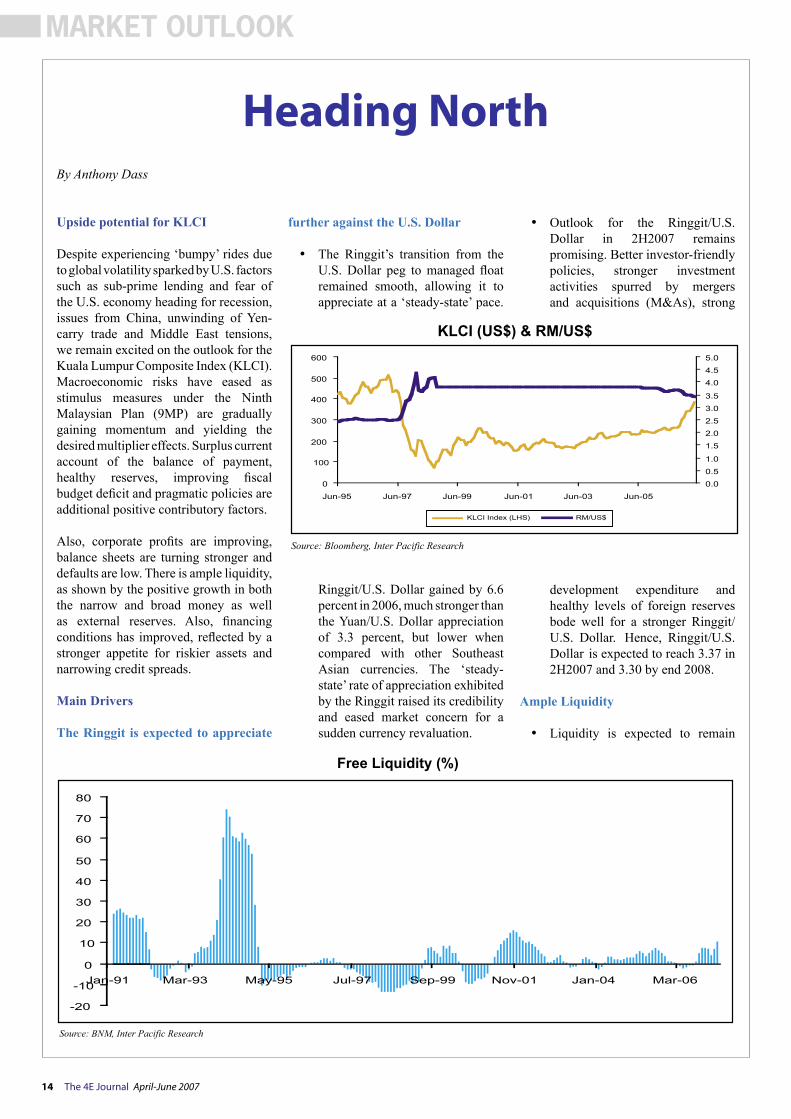

Upside potential for KLCI

Despite experiencing ‘bumpy’ rides due to global volatility sparked by U.S. factors such as sub-prime lending and fear of the U.S. economy heading for recession, issues from China, unwinding of Yen-carry trade and Middle East tensions, we remain excited on the outlook for the Kuala Lumpur Composite Index (KLCI). Macroeconomic risks have eased as stimulus measures under the Ninth Malaysian Plan (9MP) are gradually gaining momentum and yielding the desired multiplier effects. Surplus current account of the balance of payment, healthy reserves, improving fiscal budget deficit and pragmatic policies are additional positive contributory factors.

Also, corporate profits are improving, balance sheets are turning stronger and defaults are low. There is ample liquidity, as shown by the positive growth in both the narrow and broad money as well as external reserves. Also, financing conditions has improved, reflected by a stronger appetite for riskier assets and narrowing credit spreads.

Main Drivers

The Ringgit is expected to appreciate

further against the U.S. Dollar

• The Ringgit’s transition from the U.S. Dollar peg to managed float remained smooth, allowing it to appreciate at a ‘steady-state’ pace.

Ringgit/U.S. Dollar gained by 6.6 percent in 2006, much stronger than the Yuan/U.S. Dollar appreciation of 3.3 percent, but lower when compared with other Southeast Asian currencies. The ‘steady-state’ rate of appreciation exhibited by the Ringgit raised its credibility and eased market concern for a sudden currency revaluation.

• Outlook for the Ringgit/U.S. Dollar in 2H2007 remains promising. Better investor-friendly policies, stronger investment activities spurred by mergers and acquisitions (M&As), strong

development expenditure and healthy levels of foreign reserves bode well for a stronger Ringgit/U.S. Dollar. Hence, Ringgit/U.S. Dollar is expected to reach 3.37 in 2H2007 and 3.30 by end 2008.

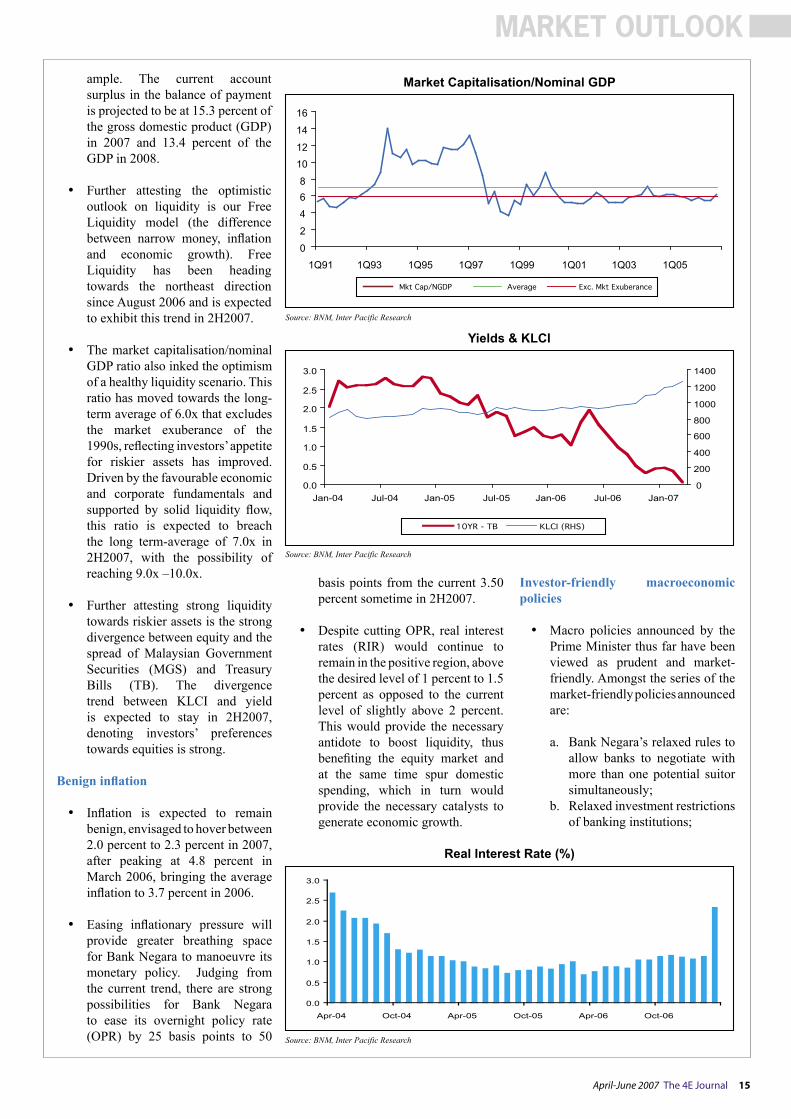

Ample Liquidity

• Liquidity is expected to remain

Heading North

0

100

200

300

400

500

600

Jun-95 Jun-97 Jun-99 Jun-01 Jun-03 Jun-05

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

KLCI Index (LHS) RM/US$

Source: Bloomberg, Inter Pacific Research

KLCI (US$) & RM/US$

-20

-10

0

10

20

30

40

50

60

70

80

Jan-91 Mar-93 May-95 Jul-97 Sep-99 Nov-01 Jan-04 Mar-06

Free Liquidity (%)

Source: BNM, Inter Pacific Research

April-June 2007 The 4E Journal 15

MARKET OUTLOOK MARKET OUTLOOK

ample. The current account surplus in the balance of payment is projected to be at 15.3 percent of the gross domestic product (GDP) in 2007 and 13.4 percent of the GDP in 2008.

• Further attesting the optimistic outlook on liquidity is our Free Liquidity model (the difference between narrow money, inflation and economic growth). Free Liquidity has been heading towards the northeast direction since August 2006 and is expected to exhibit this trend in 2H2007.

• The market capitalisation/nominal GDP ratio also inked the optimism of a healthy liquidity scenario. This ratio has moved towards the long-term average of 6.0x that excludes the market exuberance of the 1990s, reflecting investors’ appetite for riskier assets has improved. Driven by the favourable economic and corporate fundamentals and supported by solid liquidity flow, this ratio is expected to breach the long term-average of 7.0x in 2H2007, with the possibility of reaching 9.0x –10.0x.

• Further attesting strong liquidity towards riskier assets is the strong divergence between equity and the spread of Malaysian Government Securities (MGS) and Treasury Bills (TB). The divergence trend between KLCI and yield is expected to stay in 2H2007, denoting investors’ preferences towards equities is strong.

Benign inflation

• Inflation is expected to remain benign, envisaged to hover between 2.0 percent to 2.3 percent in 2007, after peaking at 4.8 percent in March 2006, bringing the average inflation to 3.7 percent in 2006.

• Easing inflationary pressure will provide greater breathing space for Bank Negara to manoeuvre its monetary policy. Judging from the current trend, there are strong possibilities for Bank Negara to ease its overnight policy rate (OPR) by 25 basis points to 50

basis points from the current 3.50 percent sometime in 2H2007.

• Despite cutting OPR, real interest rates (RIR) would continue to remain in the positive region, above the desired level of 1 percent to 1.5 percent as opposed to the current level of slightly above 2 percent. This would provide the necessary antidote to boost liquidity, thus benefiting the equity market and at the same time spur domestic spending, which in turn would provide the necessary catalysts to generate economic growth.

Investor-friendly macroeconomic policies

• Macro policies announced by the Prime Minister thus far have been viewed as prudent and market-friendly. Amongst the series of the market-friendly policies announced are:

a. Bank Negara’s relaxed rules to allow banks to negotiate with more than one potential suitor simultaneously;

b. Relaxed investment restrictions of banking institutions;

0

2

4

6

8

10

12

14

16

1Q91 1Q93 1Q95 1Q97 1Q99 1Q01 1Q03 1Q05

Mkt Cap/NGDP Average Exc. Mkt Exuberance

Market Capitalisation/Nominal GDP

Source: BNM, Inter Pacific Research

Yields & KLCI

Source: BNM, Inter Pacific Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07

0

200

400

600

800

1000

1200

1400

10YR - TB KLCI (RHS)

Real Interest Rate (%)

Source: BNM, Inter Pacific Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Apr-04 Oct-04 Apr-05 Oct-05 Apr-06 Oct-06

16 The 4E Journal April-June 2007

c. Liberalisation of a series of foreign exchange measures;

d. Revival of Ipoh-Padang Besar double-tracking project;

e. Scrapping of real property gains tax (RPGT); and

f. Introduction of a series of incentives to attract investors to the Iskandar Development Region (IDR)

• Investors currently perceive that policies are more efficiently designed and implemented to maintain a competitive advantage on the global front. Such optimism alleviated the performance of the KLCI, as shown by its buoyancy vis-à-vis regional bourses.

Corporate news

• Greater flow of positive corporate news is envisaged. It comes about following the implementation of projects spelt under the 9MP, primarily the IDR and the Northern Region.

• Also, Bursa Malaysia is aggressively implementing strategies to enhance the KLCI’s competitiveness against other regional bourses. Among the steps taken: to broaden its products

MARKET OUTLOOK MARKET OUTLOOK

and globalise them. Also, measures have been introduced to improve the infrastructure by creating better accessibility and liquidity.

Corporate activities and the restructuring of GLCs

• M&A and corporate restructuring activities will continue to play a significant role, going forward. Such activities would effectively improve shareholders’ value and spur the necessary excitement in the equity market.

• Government-linked corporation (GLC) restructuring has begun to yield the desired results. They have outperformed their respective key performance indexes (KPIs) and market expectations in 2006. Now, the government plans to reduce its exposure in GLCs, with the objective to improve free float and liquidity. GLCs are also expected to garner about 45 percent of the market’s earnings for FY2007.

Pre-election rally

• While the General Election must be held by mid 2009, there are strong indications that the election may be

held sometime in 2007 or latest by April 2008. The reasons:

a. The recent by-elections victories in favour of Barisan Nasional (BN) could be construed positively, reflecting there is still strong support for BN.

b. An increasingly healthy economic environment as shown by strong liquidity, healthy reserves and the appreciating Ringgit, and complemented by the buoyant equity market.

c. The recent salary adjustment for civil servants points to a strong possibility that the general election could be around the corner.

d. Avoidance of confrontation with the former Deputy Prime Minister, Datuk Seri Anwar Ibrahim, who will be eligible to stand for election in May 2008.

e. The bitter spat and strong lambasting by the former Prime Minister Tun Dr Mahathir

YTD KLCI versus Regional Bourses (Q-o-Q)

Source: Bloomberg, Inter Pacific Research

MalaysiaSingaporeThailandPhilippinesIndonesiaHong KongTaiwanKoreaChinaChinaIndiaVietnamU.S.U.S.U.S.

CompositeStraits TimesBangkok SETPSE CompositeJakarta CompositeHang SengTaiwan WeightedKorea CompositeShanghaiShenzenMumbai Sensex 30Vietnam SEDow JonesS&P 500Nasdaq

2Q

(1.3)(3.9)(7.5)(0.8)(1.0)2.9 1.4

(4.7)28.8 33.9 (5.9)2.4 0.4

(1.9)(7.2)

3Q

5.8 5.5 1.2

17.3 17.1 7.8 2.7 5.9 4.8 1.3

17.4 2.2 4.7 5.2 4.0

4Q

13.3 16.2 (0.9)16.7 17.7 13.8 13.7 4.6

52.7 25.5 10.7 42.7 6.7 6.2 6.9

2006

May 14, 2007

1359.6 3501.1 712.2

3364.6 2044.2

20979.2 8030.6 1605.8 4046.4 1127.7

13965.9 1066.0

13346.8 1503.2 2546.4

Index

21.8 27.2 (4.7)42.3 55.3 34.2 19.5 4.0

130.4 97.5 46.7

144.5 16.3 13.6 9.5

2006

YTD

13.7 8.2

(0.9)7.4 1.4

(0.8)0.8 1.3

19.0 50.0 (5.2)42.5 (0.9)0.2 0.3

2007

1Q

13.7 8.2

(0.9)7.4 1.4

(0.8)0.8 1.3

19.0 50.0 (5.2)42.5 (0.9)0.2 0.3

2007IndicesCountry

April-June 2007 The 4E Journal 17

MARKET OUTLOOK MARKET OUTLOOK

against the current Prime Minister had vapourised, thus easing tension.

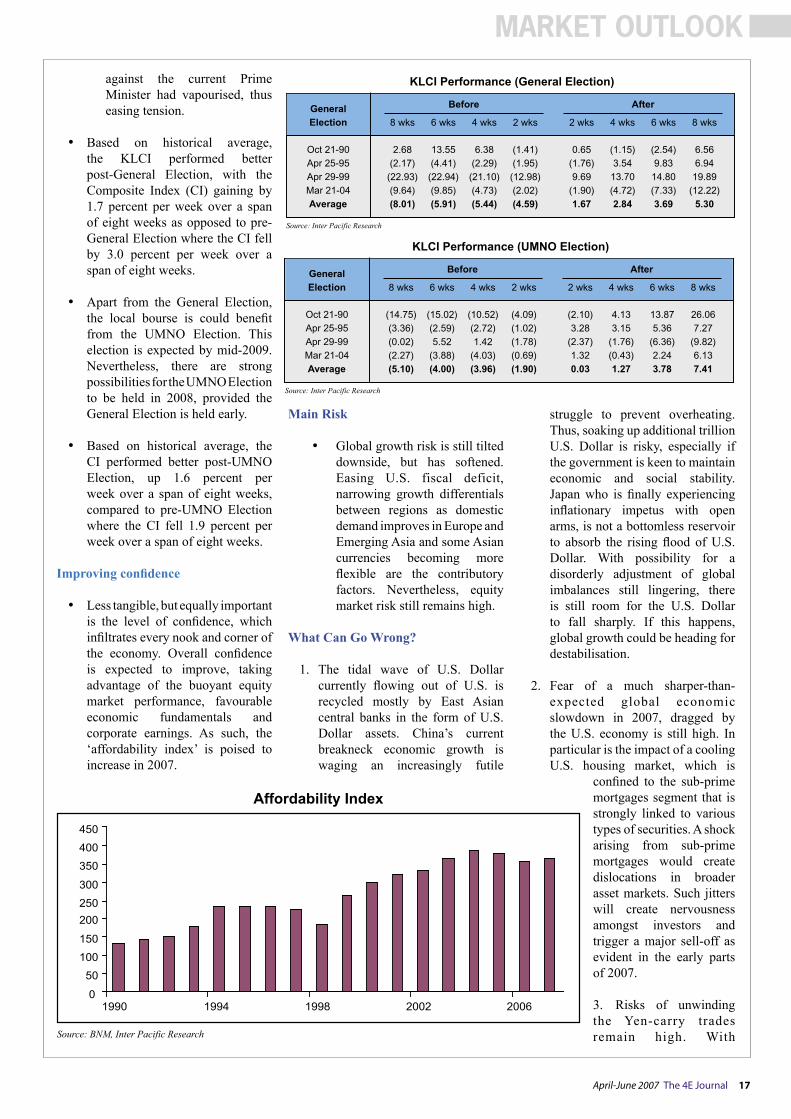

• Based on historical average, the KLCI performed better post-General Election, with the Composite Index (CI) gaining by 1.7 percent per week over a span of eight weeks as opposed to pre-General Election where the CI fell by 3.0 percent per week over a span of eight weeks.

• Apart from the General Election, the local bourse is could benefit from the UMNO Election. This election is expected by mid-2009. Nevertheless, there are strong possibilities for the UMNO Election to be held in 2008, provided the General Election is held early.

• Based on historical average, the CI performed better post-UMNO Election, up 1.6 percent per week over a span of eight weeks, compared to pre-UMNO Election where the CI fell 1.9 percent per week over a span of eight weeks.

Improving confidence

• Less tangible, but equally important is the level of confidence, which infiltrates every nook and corner of the economy. Overall confidence is expected to improve, taking advantage of the buoyant equity market performance, favourable economic fundamentals and corporate earnings. As such, the ‘affordability index’ is poised to increase in 2007.

Main Risk

• Global growth risk is still tilted downside, but has softened. Easing U.S. fiscal deficit, narrowing growth differentials between regions as domestic demand improves in Europe and Emerging Asia and some Asian currencies becoming more flexible are the contributory factors. Nevertheless, equity market risk still remains high.

What Can Go Wrong?

1. The tidal wave of U.S. Dollar currently flowing out of U.S. is recycled mostly by East Asian central banks in the form of U.S. Dollar assets. China’s current breakneck economic growth is waging an increasingly futile

struggle to prevent overheating. Thus, soaking up additional trillion U.S. Dollar is risky, especially if the government is keen to maintain economic and social stability. Japan who is finally experiencing inflationary impetus with open arms, is not a bottomless reservoir to absorb the rising flood of U.S. Dollar. With possibility for a disorderly adjustment of global imbalances still lingering, there is still room for the U.S. Dollar to fall sharply. If this happens, global growth could be heading for destabilisation.

2. Fear of a much sharper-than-expected global economic slowdown in 2007, dragged by the U.S. economy is still high. In particular is the impact of a cooling U.S. housing market, which is

confined to the sub-prime mortgages segment that is strongly linked to various types of securities. A shock arising from sub-prime mortgages would create dislocations in broader asset markets. Such jitters will create nervousness amongst investors and trigger a major sell-off as evident in the early parts of 2007.

3. Risks of unwinding the Yen-carry trades remain high. With

KLCI Performance (General Election)

Source: Inter Pacific Research

General Election

Oct 21-90Apr 25-95Apr 29-99Mar 21-04Average

8 wks

2.68(2.17)

(22.93)(9.64)(8.01)

6 wks

13.55(4.41)

(22.94)(9.85)(5.91)

4 wks

6.38(2.29)

(21.10)(4.73)(5.44)

2 wks

(1.41)(1.95)

(12.98)(2.02)(4.59)

Before

2 wks

0.65(1.76)9.69

(1.90)1.67

4 wks

(1.15)3.54

13.70(4.72)2.84

6 wks

(2.54)9.83

14.80(7.33)3.69

8 wks

6.566.94

19.89(12.22)

5.30

After

KLCI Performance (UMNO Election)

Source: Inter Pacific Research

General Election

Oct 21-90Apr 25-95Apr 29-99Mar 21-04Average

8 wks

(14.75)(3.36)(0.02)(2.27)(5.10)

6 wks

(15.02)(2.59)5.52

(3.88)(4.00)

4 wks

(10.52)(2.72)1.42

(4.03)(3.96)

2 wks

(4.09)(1.02)(1.78)(0.69)(1.90)

Before

2 wks

(2.10)3.28

(2.37)1.320.03

4 wks

4.133.15

(1.76)(0.43)1.27

6 wks

13.875.36

(6.36)2.243.78

8 wks

26.067.27

(9.82)6.137.41

After

Affordability Index

Source: BNM, Inter Pacific Research

0

50

100

150

200

250

300

350

400

450

1990 1994 1998 2002 2006

18 The 4E Journal April-June 2007

MARKET OUTLOOK

increasing possibility of the Bank of Japan raising interest rates, outlook for a stronger Yen/U.S. Dollar looks promising. Under such circumstances, there are strong possibilities for the Yen-carry trades to be unwound in a significant manner. Carry trades are positions in which investors sell a low-interest-rate currency such as the Yen and invest the proceeds in a higher-yielding currency or asset. Here, investors take the view that the foreign exchange will not move significantly, as it will erode their positive returns from the interest-rate differentials. Such carry trades are usually attractive when market volatility is relatively low.

4. Risk of resurgence in oil prices underpinned by tighter refining spare capacity and the unpredictable geo-political risk remains intact. After hitting an 18-month low of US$50.5/barrel on January 18, 2007, the West Texas Intermediate (WTI) benchmark rose by 30.9 percent to US$66.1 per barrel on March 29, 2007 over Iran’s nuclear programme and the capture of 15 British military personnel by Iran.

Although these issues eased, geo-political risk and fear of supply disruptions remain high, forcing oil prices to be well above US$60 a barrel. This raises expectation that inflation could be sparked by high oil prices. Such perception could lead to the assumption of monetary tightening and raise the possibility of ‘stagflation’ arising in some economies.

Market Outlook

• Our liquidity model showed the CI is currently trading at a discount of about 17 percent. Strong macro fundamentals supported by solid liquidity provided the necessary positive impetus, and at the same time shield the local bourse from uncertainties arising from external shocks.

• Going forward, we expect the CI to remain ‘choppy,’ primarily driven by the uncertainties on the global front. Nevertheless, it is unlikely for the CI to harbinger a protracted downturn, even in the event of external shocks arising. Such adverse effects from external

shocks would be cushioned by the continued strong fundamentals and liquidity inflow. Hence, our liquidity model showed the CI’s upside potential remains strong, possibly reaching 1,450 – 1,500 in 2H2007.

• Beneath a favourable baseline economic growth and a stock market that is poised to move to greater heights, investors should look at laggard big cap stocks like Tenaga Nasional, Maybank and Telekom. There are also investment opportunities from the ‘small-to-mid’ cap stocks, primarily supported by healthy earnings. Also not forgetting, with the General election and thereafter UMNO Election in the pipeline, politically-linked stocks are expected to create some excitement. Theme plays like the 9MP, Visit Malaysia Year 2007, M&As and GLCs are expected to generate some thrill.

________________________________

The writer is the Head of Research of Inter Pacific Research Sdn Bhd.

evening, at a banquet, she found herself sitting next to Jon Lovelace, the head of Capital Research. She told him she needed three things for the portfolio: income, low risk, and some growth to offset inflation. Lovelace and his staff created the Capital Income Builder Fund and put her on the board, where she remains today.

Joe Kernan, my interviewer, was absolutely taken with this story and said he had never heard it before and found it fascinating. I tell you this because stories – especially from behind the scenes – will help market your brand.

So think of a name. Make it personal, such as “The Money Lady,” or “Mr Retirement,” and start letting people know that you’re the best at it.

Positioning yourself simply means being in places where people can see, hear, or read about your niche or brand. Work on your communication skills. Hire pros to teach you. You will never know it all. It’s a lifelong pursuit. Just try to get a little better at this each year. If your cash flow inhibits you from hiring coaches in communication and public relations, then read and devour the best books on the subject. That’s how I got started. Here are some of the books that were instrumental in my success:

• Anything by Jack Trout and Al Reis. Start with Positioning: The Battle for Your Mind and Marketing Warfare.

• Changing the Game by Larry Wilson with Hersch Wilson, Simon & Schuster, 1987.

• On Writing Well: The Classic Guide to Writing Nonfiction by William

Zinsser, Quill Harper Resource, 2001.

• Ted Levitt On Marketing, Harvard Business Review, 2006.

Think of your niche just as you would a power boat pulling a water skier. The skier is your brand, getting out there. Shut down the engine and your skier goes down. Shut down your brand and your marketing is lethally weakened.

Vern C. Hayden, CFP®, is president of Hayden Financial Group LLC in Westport, Connecticut, and author of Getting an Investing Game Plan. Reprinted with permission from the March 2007 Issue of the Journal of Financial Planning, the official publication of the Financial Planning Association.

From page 10

April-June 2007 The 4E Journal 19

The Financial Planning Association of Malaysia (FPAM)’s seventh Annual General Meeting (AGM)

was held on May 12, 2007 at the Bukit Kiara Equestrian & Country Resort. A total of 83 certified members attended the meeting.

Among the matters that were decided on that day by members were the election of several members to the Board of Governors, the proposal to increase the sponsorship fees of Corporate Members as well as a number of other routine, but no less important matters like the receipt and adoption of the audited financial statements of the Association for the year ending December 31, 2006.There was no contest in the election of Charter Member representatives. The reason: there were exactly five nominations for five vacancies. The following Charter Member representatives were elected to the Board of Governors:

• Tan Beng Wah (representing CIMB Wealth Advisors Bhd)

• U Chen Hock (representing HSBC Bank Malaysia Bhd)

• Muhamad Umar Swift (representing Malaysian Assurance Alliance Bhd)

• Zulkifly Sulaiman (representing Malayan Banking Bhd)

• Mark Toh Chin Hian (representing Prudential Assurance Malaysia Bhd)

In the case of the Certified Members that were to be represented on the Board of Governors, the situation was more competitive. There are three seats available, but the Association received a total of eight nominations. According to FPAM president, U Chen Hock, the Nomination Committee deliberated on the matter and agreed that all the nominees be accepted as candidates for the Board of Governors. U said, “We believe the decision to place all those who have expressed their desire to serve the Association – be it for the first time or as a continuance of their on-going dedication and contribution to the

Association – is the right one. As such, all of them will be placed before the members during the AGM, who will decide who they want to represent them on the Board. I believe, as do the other members of the Board of Governors, that the members will exercise their maturity and their wisdom and choose the best candidates for the Board of Governors based on their respective qualification and experience.”

The electoral process took its course and the following Certified Members were elected to the Board of Governors:

• Aida Md Daud• Steve L H Teoh• K P Bose Dasan

Meanwhile, a resolution seeking to amend the relevant section of the Constitution which will in effect increase the sponsorship sum required of Corporate Members upon joining FPAM be increased to RM3,000 was also put to vote. In the sixth FPAM AGM in 2006, members have given their approval to this resolution in principle by agreeing to give the Board the authority to vary the sponsorship amount for both Charter and Corporate Members. U said the Registrar of Society approved the amendment as voted by members, but require that the sum decided upon must also receive members’ approval.

The resolution was not passed because a simple majority was not obtained. Many members questioned the quantum of increase and the matter will have to be resolved at a later date.

In his speech, U also said the Association

turned in a strong performance in 2006 chalking an after tax surplus of income over expenditure of RM189,000. This, as U put it, will be the third year running that FPAM has recorded such a strong surplus. There was an increase in expenditure last year, he said, and this was largely attributed to chapter and membership development as well as marketing and promotional programmes, which were requested by members in previous years.

“The Association had to increase its income to offset this increase and while there was a drop in contribution from examinations, income from other categories improved including those from membership and especially the surplus from the Financial Expo,” he added. “It is my hope that we will continue to generate these surpluses to enable us to fund ongoing activities and programs for the members’ benefits and the growth of the industry.”

Also according to U, FINEX 2006 attracted more than 10,000 visitors and more than 45 exhibitors from the financial planning industry as well as the regulatory and statutory bodies participated. In addition, there was also a series of well-attended talks that were designed and targeted at both the professionals and the public.

Branching Out

U: FPAM recorded strong surplus for the third year running

INDUSTRY

20 The 4E Journal April-June 2007

U also highlighted some of the more significant activities of the Association in 2006 as well as updated members FPAM’s latest developments. “Your Association has continued with its advocacy work to streamline and develop the industry for the betterment of its members,” he said.

“Last year we achieved another milestone in the industry when Bank Negara gave its recognition to the CFP qualification for the purpose of the issuance of the Financial Advisory license. The year before, it recognised the CFP Module 1 and Module 2 as programmes meeting its continuing education requirement for insurance practitioners.

“We hope members, including those from the insurance sector, will appreciate that the CFP qualification, amongst all other financial planning qualifications offered in Malaysia, gives its holders the widest access to the marketplace should they choose to be practitioners,” U pointed out. “In Malaysia, the CFP qualification is fully recognised by the Securities Commission and Bank Negara with regards to all aspects of investment advisory (financial

planning) and financial advisory work. It is also recognised worldwide and members need only to sit for a “top-up” examination to practise in another jurisdiction. The SC also recognises the AFPM (Associate Financial Planning Malaysia) qualification which is offered to Trade Members of FPAM who have passed Module 1 of the CFP programme, as a prerequisite to allowing them to recommend the full range of financial products to match the needs of their clients.”

U said FPAM will continue with it advocacy work to gain further recognition for the CFP qualification in order that its members can participate in an even broader area of practice. “The Association is currently seeking exemptions for CFPs (Certified M e m b e r s ) from FMUTM (Federation of Malaysian Unit Trust Managers)’s u n i t t r u s t examination (UTE) and to have the IUTA (institutional unit trust agents) scheme expand beyond banks to encompass individual financial planning advisory

firms, subject to conditions that will safeguard the consumer and the industry without being unduly onerous on interested firms,” U said. “The continuing ability of the CFP qualification to gain recognition on many fronts can be attributed to the rigour of the programme

including the standards that it adheres to, which is recognised internationally.”

U also said that it is important to uphold and safeguard these standards and for the past year, FPAM’s efforts on this matter were along two main fronts.

Firstly, the FPAM Standards and Professional Review Committee was tasked with reviewing, updating and consolidating the existing Code of Ethics and Professional Responsibility and the

Practice Standards. “The Committee, in its work also drew from international resources made available to FPAM as an affiliate of an international network of national financial planning bodies,” U explained. “The draft document has been reviewed and commented on by the Board; members will be asked for their inputs on the exposure draft soon, prior to it being finalised. We believe the standards provided in the document will continue to promote the orderly development of the industry, safeguard the interests of consumers and promote professionalism among practitioners.” At the same time, U said FPAM is also working closely with other financial planning associations under the Industry Consolidation Taskforce (ICT) to streamline and establish an agreed set of practice standards for the industry. This is at an advanced stage of finalisation. “FPAM has continuously strived to be in the forefront of development in the financial planning industry,” U said matter-of-factly. “Last year, we signed two memorandums of understanding – one with University of Malaya to introduce financial planning

Delicate discussions

Patrick Nge casting his vote

“Any questions?”

INDUSTRY INDUSTRY

April-June 2007 The 4E Journal 21

into their curriculum and the other with IBFIM (Islamic Banking and Financial Institutions Malaysia) to introduce an Islamic financial planning programme.

“We consider both of these initiatives important pioneering moves. Introducing financial planning as a subject into the academic curriculum of institutions of higher learning promotes financial literacy among young adults and increases their awareness of the importance of, and need for financial planning. The structure we put in place also in effect pegged the CFP qualification as one that requires a relevant degree as the entry requirement. In the coming years, we will be moving in this direction given the quality of the CFP programme, and in tandem with international trends where in many countries it is now the norm that a member must have a first degree before being eligible to enroll in the CFP course.

“The introduction of the Islamic financial planning programme is in recognition of the need in the market and in support of the Government’s many initiatives in establishing Malaysia as a pioneer and a

centre of excellence in Islamic finance,” U said.

U also said the many activities and programmes at the chapter level have already started and are expected to increase with the formal election of members to the various committees. The Malacca chapter is the first to have its election on March 10 and the Penang chapter will have its elections in late June and the others are expected to follow suit. Among the activities lined up, U said the chapters will be participating in a roadshow promoting financial planning among the public that will also feature the participation of a Bank Negara agency – the Credit Counseling and Debt Management Agency (AKPK), and the Securities Industry Development Centre (SIDC), a unit within the SC.

“The regulatory authorities are supportive of FPAM’s initiatives and have generously agreed to part fund the roadshow,” U pointed out. “We will continue to explore other ways to work closely with the regulators as well as relevant statutory bodies who share our interest in promoting financial planning awareness to the public.

At the international level, U said a number of initiatives have been launched by the Financial Planning Standards Board (FPSB) in collaboration with its affiliates, of which FPAM is a member. They include developing a global competency profile for financial planning and developing a global brand campaign for the CFP qualification and mark. When launched, U said it would further cement the reputation of the mark as the global gold standard for financial planning. FPAM, U said, is also looking at fostering closer cooperation with other national associations especially those in the region for the purpose of learning from one another and jointly organising events for the benefit of FPAM members.

“We shall continue to focus on establishing standards and practice, on building the CFP mark as the preferred financial planning qualification, on developing membership benefits and on gaining widespread acceptance for financial planning in the marketplace,” he said. “We believe we can and will remain the premier financial planning association if our efforts are applied diligently and in the right place.”

“All in favour, raise your hands”

INDUSTRY INDUSTRY

22 The 4E Journal April-June 2007

COVER STORY COVER STORY

Of Niche Domination& Financial Planning

Alliance Bank Malaysia Bhd (Alliance)’s Group CEO Datuk Bridget Lai is no stranger to the local banking scene. The fact of the matter is, she is an

icon of sorts. Her track record in consumer banking speaks for itself. Lai is known in the banking circles as a turnaround specialist, utilising strategic planning and management to breathe life into underperforming operations. She is also a tough negotiator, but understands the need for persuasion

in tactical corporate maneuverings, and is a stickler on customer service and quality. She has a keen eye on strategic market domination and leadership, and is a firm believer in building alliances and partnerships. Her focus: always improving shareholder value and earnings through top-notch products and services.

So with consumer banking now the focus of the banking industry, it was no wonder Alliance sought Lai out for the job. Malaysia’s smallest banking group needs a master tactician and saw Lai as the perfect candidate to steer them to dominate a niche. Industry observers said Lai’s experience would make her a good appointment for the group, given the potential that consumer banking offers. The reason: the changing consumer base is a big attraction. The younger, more educated and more exposed generation of consumers is willing to spend. They incidentally also have greater purchasing power as a result of better paying jobs and Malaysia’s overall vibrant economic climate.

Prior to her move to Singapore, the Sabah-born Lai, who is of Sino Kadazan decent, was head of consumer banking at Standard Charted Bank Malaysia Bhd and was also acting CEO of Stanchart Malaysia for a while in 2004. She was the group head of sales, service, shared distribution and priority banking in Stanchart Singapore for almost a year before joining Alliance in September 2005.

Lai has an MBA from Britain’s University of Hull and is a CFP (Certified Financial Planner). She recently spoke with the 4E Journal managing editor, Steven K C Poh, about her plans for the Alliance Banking Group and her observations on the development of the financial planning industry in Malaysia. Excerpts ....

April-June 2007 The 4E Journal 23

COVER STORY COVER STORY

How is the bank is positioning itself in an increasingly intense competitive environment (liberalisation and globalisation)?

That is a broad question. With WTO (World Trade Organisation) on the horizon, liberalisation and globalisation has to happen. I don’t think we have an option here. Market liberalisation in Malaysia, however, has happened in a structured way as planned by Bank Negara, and this has enabled Malaysian banks to scale up and close the gap against the competition. We are gradually getting more competitive in the marketplace.

Globalisation, on the other hand, has led to the introduction of many best practices amongst domestic banks and as a result, we are more international in our deliverables. As such, domestic banks are now in a stronger position to confront and withstand a liberalised market, which is essential to remain competitive and survive.

On our end, we are strengthening the Bank to be resilient and to be able to face challenges in an increasingly intense competitive environment. In the past 18 months we have also been restructuring to strengthen the management, delivery channels and infrastructure to be on a stronger financial footing.

Can you share some of your restructuring initiatives?

Some of our transformation initiatives include:

• Remodeling our businesses to four main lines – consumer, commercial, wholesale and Islamic

• Reshaping our loan portfolio for sustainable growth• Improving asset quality• Putting in place a robust risk management framework

and infrastructure• Leveraging on synergies across businesses and

improve efficiency through centralisation of functions and integration of subsidiaries

• Strengthening distribution channels with a more aggressive sales force and incentive structure as well as new branch strategies

• Adopting new distribution trends via direct marketing, third party agents, and property developer tie-ups

• Sharpening value proposition to customers via enhance product franchise and better service experience

Sure looks like a lot of hard work has been put in and a lot has been done.

Bank Negara Governor Tan Sri Dr Zeti Akhtar Aziz, has said before that she sees the domestic banking scene will have about three to four large banks which are also regional players while the rest will be smaller niche banks which operate only in the domestic market. I like to use the example of Sinsei Bank, a domestic bank in Japan, which is very successful in its own right.

Malaysia as a financial market is still growing one as it has a young banking population. As such, I believe there are plenty of opportunities for domestic banks to gain market share

and build niches. Alliance Bank is focused in its strategy for selective growth as well as growth with stronger portfolio quality. We are intent on growing the bank organically, rather than through acquisition. But if the opportunities arise, we will look at them. For now, the focus is to grow our consumer banking and commercial banking businesses. In consumer banking we aspire to be top five best managed bank and top three (currently top six) bank for SME (small and medium enterprises) financing.

What is Temasek Holdings Pte Ltd’s role, as a shareholder, in the Bank?

Temasek Holdings has a solid capital investment capability and from its diverse experience in investing in properties, banks and telecommunications, it is able to provide the transfer of best practices into the group. We may be a small local bank, but we have the opportunity to tie up strategic partnerships with other Temasek operations outside Malaysia and benefit from the transfer of best practices from other countries. What is the role of financial planning services in the Bank’s overall marketing strategy?

Financial planning plays a significant role in the Bank’s wealth management services. In 2006, the Bank repositioned its wealth management business with the objective to grow fee income. To this end, we have restructured the wealth management business to provide end-to-end wealth management services to our customers, engage new business partners and build customer value proposition for key target segments.

Contrary to popular belief, financial planning is not only for the wealthy, but for the mass market as well. As such, our wealth management business aims to provide a comprehensive range of products and services to our customers.

How does the Bank capitalise on its status as an IUTA (institutional unit trust agent), and in particular in the financial planning industry?

We are well placed to be a distributor of premier unit trust funds through our strategic alliance with Fullerton Fund Management, for example, for global funds. Our objective is to bring top performing funds to the investing public and by doing so, giving them better and wider choices to suit each stage of their life and enhancing their returns on investment. We also want to increase our investment offerings to meet the investment needs of our customers, and this is done through new partnerships and on-going product innovation.

But I tend to be cautious here in terms of the products that are ‘thrown’ into the market because I think we have to move in tandem with the readiness and sophistication level of the investors. Some of these products are great if you are very savvy and you have a certain level of risk appetite and you have already hedged your investments under different asset classes so you can afford a certain amount of risk on other investments. But I do not believe the ‘mass market’ investors are at this level yet. They are also the ones who tend not to be willing to share with their financial planner everything about

24 The 4E Journal April-June 2007

their assets and wealth, and as a result, nobody is really certain about how much risk they are is taking and whether or not they are properly hedged and so on. I think there are a lot of products which are coming on to the market now which are international by nature and standard, but may not be match to the mass market consumers in terms of their risk profile and their net worth profile. And they may not be sophisticated and savvy enough to know what they are investing in.

So what is the Bank doing to educate the marketplace to better manage their financial affairs and increase their personal finance and financial planning knowledge?

In the pipeline, we are planning to conduct roadshows and investment clinics to bring the concept of financial planning to the masses and educate them that everyone, regardless of age, gender or financial status, should know and start financial planning. We recognise that women are becoming a financial force in their own right even though findings have revealed that the majority still leave the task of managing their finances to their male counterparts (husband or father). Some of the initiatives that we have put together to enhance awareness among women of need to take charge of their own finances and financial future include:

• Women Sphere groups within the organisation to increase awareness that it is hip for women to be financially savvy

• Financial literacy programme for students

• Risk profiling to educate customers on their different risk tolerance and how they can invest in products which suit their investment appetites and meet their financial goals

• The Alliance Wealth Guide – the 24/7 e-portal capable of making the bank’s wealth management offerings to customers so that they can keep themselves updated on their investment portfolio

• Partnering media owners to raise awareness of importance of financial planning via well-written financial advisory columns

What is the Bank’s IT/Web strategy in view of the emerging Web lifestyle of the 21st Century?