okay, you think you’ve found a fraud. now what?

TRANSCRIPT

Okay, You Think You’ve Found a Fraud.

Now What?

John Tonsick, CFE, CPAFounder and Principal

Fraud Solutions

“The Conjurer” – Hieronymus Bosch – Late 15th Century

Payroll Fraud Examination

$2.25 million disappears!

Billing Scheme Examination

$1.5 million buys absolutely nothing!

The Fraud Examiner’s Challenge

Managing relationships• Victims• Suspects• Perpetrator • Co-workers• Witnesses• Attorneys• Law enforcement, DA/U.S. Attorney

Victim

Critical relationshipMake or break a fraud examination• How soon do you get involved?• What was the initial response?

Ignorance

Victims rarely understand:

Internal controlsHow fraud happensWhy fraud happensInvestigative techniques

Unaware, unprepared!

•Shock•Denial•Anger •Bargaining•Depression•Testing•Acceptance

• On Death and Dying, 1969, Elizabeth Kubler Ross

Emotions

Common Victim Mistakes

Confront the perpetratorDo nothingMake deals with the perpetratorFire the perpetratorMishandle/overlook critical evidenceCall the police

First Questions

What do they know?How do they know it?Who knows about it?What action have they taken?Do they have insurance?

First Steps

Manage expectations• Explain the process• Establish goals• Discuss the options• Make recommendations• Develop a plan

Working With Attorneys

• Advantages• Attorney client privilege• Legal guidance

• Disadvantages• Assume greater knowledge than they possess

Working With Attorneys

The right attorney can be a huge plus!

• CFEs• DAs, U.S. Attorneys• Law Enforcement• Litigators

The wrong attorney can be a huge detriment!

Working With Attorneys

Outside counsel• Appropriate skills and experience• Greater independence

In-house• Sometimes lack appropriate skills

and experience• May not keep attorney-client

privilege

Role of the Fraud Examiner

Minimize emotion

ExperienceKnowledgeIndependenceObjectivity

Investigation Goals

Determine the existence of fraud/illegal actsDetermine the extent of fraud/illegal actsIdentify the perpetratorsDetermine the methods usedRemove the perpetrators from your operationRecover assetsTake corrective actionSeek criminal prosecution

Secure Evidence

Secure and preserve evidence:

• Suspect’s office, computer, cell phone, etc.• Building access• System access• Bank accounts• Email• Voice mail• Snail mail• Keys, ID, symbols of authority

Avoid Spoliation

Avoid spoliation:

• Original documents• Chain of custody• Photographs• Computer

•If it’s on; leave it on•If it’s off; leave it off•Forensic copies require specialized software and procedures

•Secure storage

Who Will Investigate?

•Certified Fraud Examiners•Internal/External Auditors•Security/Private Investigators•Human Resources Personnel•Management •Outside Consultant•Legal Counsel

Establish Ground Rules

• Leadership• Types of communication• Need to know• Do not discuss outside team• Need to know basis• Keep the team as small as possible

Critical Basic Tools

• The Fraud Triangle• Knowledge of financial transactions

and fraud schemes• Knowledge of internal controls• Sound investigative techniques

The Fraud Triangle“Alive and Well”

OpportunityImmediate Need

Rationalization

Knowledge of Financial Transactions and Fraud Schemes

• Accounting is the language of business

• Fraud schemes – our stock in trade

Knowledge of Internal Controls

• Internal controls are a powerful weapon against fraud

• Ability to recognize control deficiencies can lead you quickly to what the fraudster did and how they did it

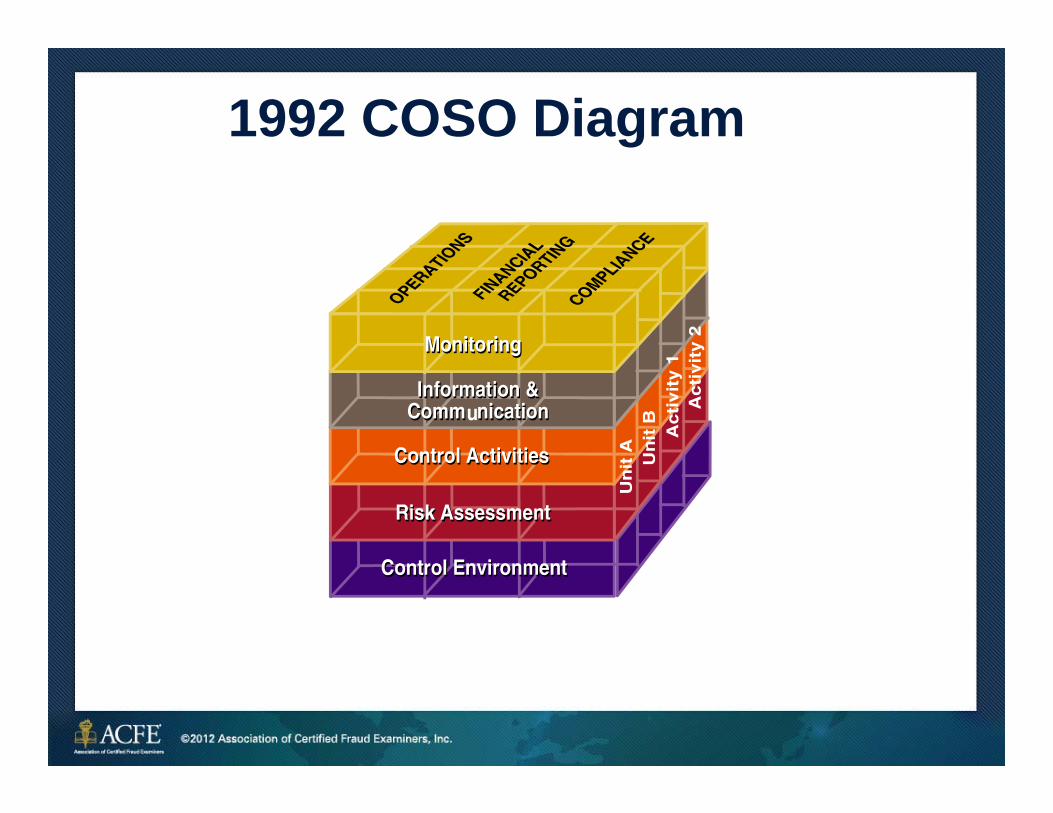

1985 COSO Diagram

1992 COSO Diagram

2004 COSO Enterprise Risk Management Diagram

2011 Proposed UpdateCOSO Enterprise Risk Management

Diagram

Evolution

Sound Investigative Techniques

• The Fraud Theory Approach –Each fraud examination begins with the proposition that all cases will end in litigation

• You won’t have time to learn from your mistakes

Sound Investigative Techniques

• ACFE Fraud Examiners Manual

• Analyzing documents• Interview theory and application• Covert examination• Sources of information• Accessing information online• Data analysis and reporting tools• Computer forensics• Tracing illicit transactions• Reporting standards• Checklists, forms, contract and opinion

letters

A Suggested Approach

1. Internal investigation2. Civil litigation3. Criminal prosecution

Existing Relationships

Never interrupt your enemy when he is making a mistake. Napoleon Bonaparte (1769–1821)

Advantages:• Maintain the element of surprise• Cooperation • Access to information• Relatively inexpensive

Civil Litigation

Advantages:• Subpoena documents• Take depositions under oath• Lower burden of proof• You retain some control• Judgment beneficial in criminal

action

Disadvantages:• Expensive• Other side has options

Civil Litigation

A Business Decision• Cost/benefit analysis• Does the other side have

assets?• How much are you willing to

spend to make a point?

Don’t start what you aren’t willing to finish!

Criminal Prosecution

Advantages:• Satisfaction• Sends a strong message

Disadvantages:• Lose control• Information becomes public• Constrained resources• Reluctance to prosecute• Higher burden of proof• Perpetrator has options

OK, You Think You’ve Found a Fraud. Now What?

February 23, 2010Thank you

John Tonsick, CFE, CPAFraud Solutions

18000 Studebaker, Suite 700Cerritos, CA 90703

213-716-0667

The contents of this presentation may not be transmitted, re-published, modified, reproduced, distributed, copied, or sold without the prior consent of the author.

“Association of Certified Fraud Examiners,” “Certified Fraud Examiner,” “CFE,” “ACFE,” and the ACFE Logo are trademarks owned by the Association of Certified Fraud Examiners, Inc.