online training done right basic alternatives to...

TRANSCRIPT

03-21-17

1

"Online Training Done Right"

www.thecounselorscorner.net

Basic Alternatives to Foreclosure: The Decision Tree

Tuesday, March 21, 2017

"Online Training Done Right"

www.thecounselorscorner.net

Get to Know Your Presenter

2

Robin Stout Migala

• Consultant to the industry – three years with The

Counselor’s Corner

• Over 47 years’ experience in residential lending and default

servicing

• 23 years with Freddie Mac in Housing Outreach

• Specialty in loss mitigation and foreclosure prevention for

housing counselors and real estate professionals

03-21-17

2

"Online Training Done Right"

www.thecounselorscorner.net

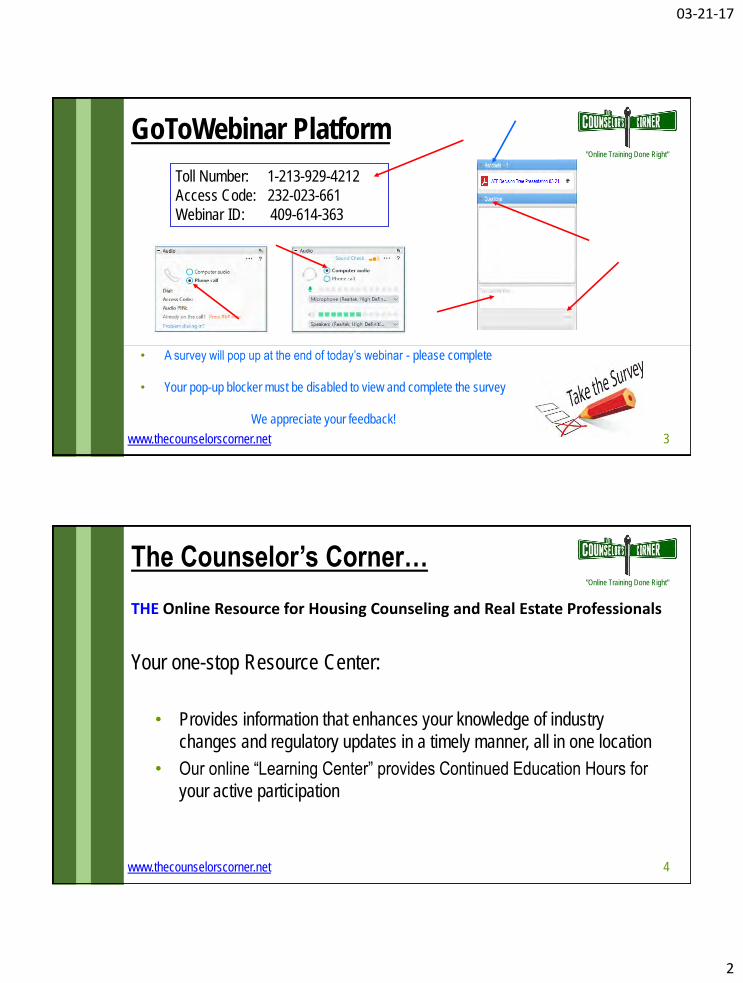

GoToWebinar Platform

3

Toll Number: 1-213-929-4212

Access Code: 232-023-661

Webinar ID: 409-614-363

• A survey will pop up at the end of today’s webinar - please complete

• Your pop-up blocker must be disabled to view and complete the survey

We appreciate your feedback!

"Online Training Done Right"

www.thecounselorscorner.net

The Counselor’s Corner…

4

THE Online Resource for Housing Counseling and Real Estate Professionals

Your one-stop Resource Center:

• Provides information that enhances your knowledge of industry

changes and regulatory updates in a timely manner, all in one location

• Our online “Learning Center” provides Continued Education Hours for

your active participation

03-21-17

3

"Online Training Done Right"

www.thecounselorscorner.net

Certificate of Completion Eligibility

5

• Only those who register for and attend a webinar online and who pass the post-webinar test will

receive a Certificate of Completion showing the hours.

• Within three hours after the webinar ends, we will e-mail the online testing link. Please check

your SPAM folder or your company’s quarantine for this e-mail.

IMPORTANT! Please add [email protected] to your address book

• Webinar attendees who pass the post-webinar test with a score of 80% or higher will be

awarded a Certificate of Completion.

"Online Training Done Right"

www.thecounselorscorner.net

Questions for You

6

• Knowledge

Checkpoint

Questions will

display during

today's presentation

• Your responses

must be entered in

the control panel

question box

We encourage you to take notes as we go.

• Polling Questions will pop up during today's presentation

• Your responses must be selected on the screen

• Case Studies will be presented toward the end of the session

• Your responses must be entered in the control panel question box

03-21-17

4

"Online Training Done Right"

www.thecounselorscorner.net

National Industry Standards

7

The Counselor’s Corner supports the mission of the National Industry Standards in Foreclosure, Homeownership Counseling & Education.

• The Standards help practitioners and organizations serve families and communities in a consistent and professional manner.

• This webinar: Promotes consistent & quality counseling Builds competency & knowledge of requirements Provides useable resources

"Online Training Done Right"

www.thecounselorscorner.net

Basic Alternatives to Foreclosure: The Decision Tree

8

Our objective today is to enable you to:

• Evaluate a borrower’s situation

• Define hardship

• Understand the alternatives to foreclosure

• Know when to consider a particular option

• Get the resources available to you and your clients

DISCLAIMER:

This training is a summary of the detailed requirements of various Investors’ policies and procedures regarding Alternatives to Foreclosure and Foreclosure Prevention and is not a

substitute for those requirements. This training is meant for educational purposes only. For additional information, please reference the applicable sections of Investors’ Guides and

Handbooks. Please note that those requirements are subject to change at any time.

03-21-17

5

"Online Training Done Right"

www.thecounselorscorner.net

Polling Question #1

9

Approximately what percentage of your agency’s business is still foreclosure

prevention?

"Online Training Done Right"

www.thecounselorscorner.net

Industry Philosophy Then

10

Servicers, investors and mortgage insurance companies are committed to

helping distressed borrowers find solutions to their delinquencies.

Alternatives to foreclosure can…

• Help reduce impact to borrower’s credit rating

• Help prevent loss of the home

• Eliminate time and expense the Servicer incurs on a defaulted loan

• Reinstate the servicing fee income the Servicer earns on a loan

• Improve the Servicer’s relationship with the borrower

• Minimize investor and mortgage insurance company credit losses

• Stabilize neighborhoods

03-21-17

6

"Online Training Done Right"

www.thecounselorscorner.net

Industry Philosophy Now

11

Servicers, investors and mortgage insurance companies are committed

to helping distressed borrowers find solutions to their delinquencies.

Other workout options used before MHA ended still exist:

• Treasury/FHFA/HUD - Guiding Principles for the Future of Loss Mitigation: How

the Lessons Learned from the Financial Crisis Can Influence the Path Forward

• CFPB – Principles for the Future of Loss Mitigation

• MBA – Life After HAMP – The Future of Loss Mitigation

"Online Training Done Right"

www.thecounselorscorner.net

Your Steps to Help Borrowers Avoid Foreclosure

12

1. Evaluate the borrower’s situation, including the hardship and ability to repay

2. Contact the Servicer and know the timelines

3. Encourage clients to stay in contact with their Servicers

4. Evaluate the options

5. Counsel and coach the homeowner

03-21-17

7

"Online Training Done Right"

www.thecounselorscorner.net

Collection Records

13

Servicer collection records must evidence:

• Dates that letters and notices were mailed

• Dates and results of personal contact with the borrower

• Reasons for prior and current defaults

• Terms of any repayment arrangements

• Documentation of property inspections

"Online Training Done Right"

www.thecounselorscorner.net

When is a Mortgage Delinquent?

14

• Delinquency occurs when all or part of a borrower’s monthly mortgage

payment is unpaid after the due date.

• Encourage your clients to set up ACH (Automated Clearing House)

payments with their Servicers.

03-21-17

8

"Online Training Done Right"

www.thecounselorscorner.net

Collection Process

15

Most Servicers…

• Use SPOC (Single Point of Contact)

• Use skip tracing to reach borrowers

• Attempt to contact borrowers early and often

• Continue collection attempts until foreclosure begins

• If reinstatement not possible, pursue alternatives to foreclosure

"Online Training Done Right"

www.thecounselorscorner.net

Establishing Borrower Contact

16

Upon contacting the borrower, Servicers will…

• Determine the reason for default and whether it is temporary or permanent

• Determine if the property is vacant or the borrower intends to vacate

• Determine the borrower’s perception of his/her financial situation and

ability to repay

• Set payment expectations and explain alternatives to foreclosure

• Obtain a commitment from the borrower to reinstate or

try an alternative to foreclosure

03-21-17

9

"Online Training Done Right"

www.thecounselorscorner.net

Knowledge Checkpoint Question #1

17

A borrower is not considered to be delinquent on the mortgage payment until at least

one full payment is 30 days past due.

Is this true or false?

False.

The loan is delinquent if the payment has not been made as of midnight on the date the

payment is due. The grace period is for late charges only.

"Online Training Done Right"

www.thecounselorscorner.net

Hardships

18

• Unemployment

• Income reduction

• Increased housing expenses

• Divorce or legal separation

• Death

• Disability or illness

• Disaster

• Distant employment transfer (including PCS)

• Business failure

• Other

03-21-17

10

"Online Training Done Right"

www.thecounselorscorner.net

Non Hardships

19

• Property value depreciation

• Temporary income interruption with sufficient liquid assets to pay

• ARM rate adjustment or interest only converting to amortization

"Online Training Done Right"

www.thecounselorscorner.net

Alternatives to Foreclosure Hierarchy

20

Refinance

Full and partial reinstatement

Repayment and forbearance plans

Retention workout options

Liquidation workout options

03-21-17

11

"Online Training Done Right"

www.thecounselorscorner.net

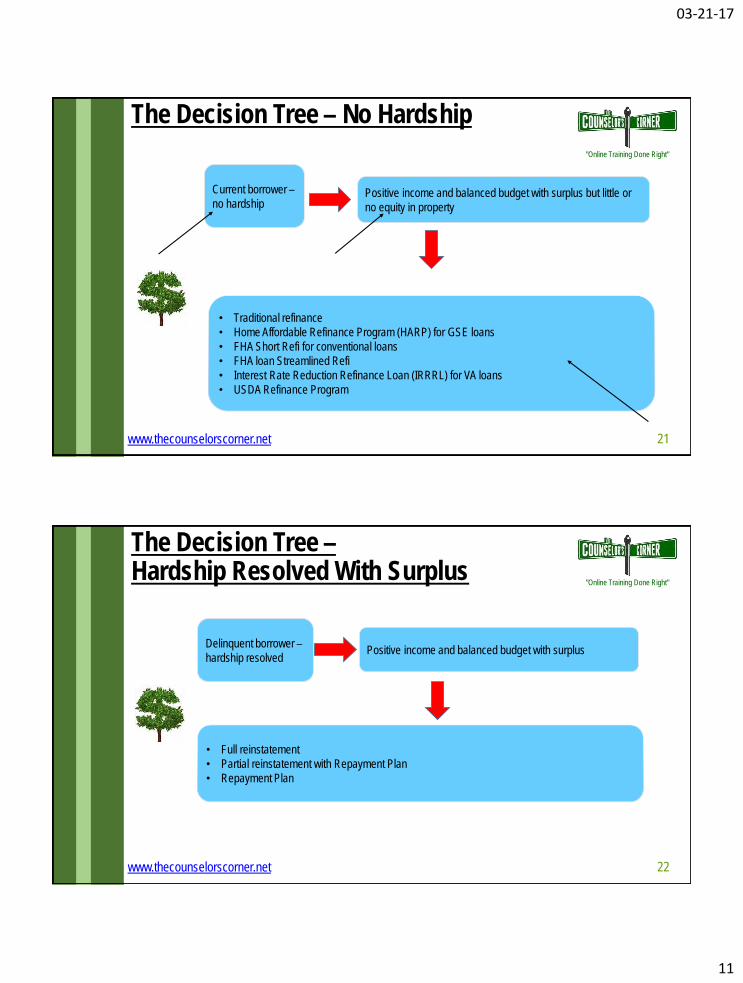

The Decision Tree – No Hardship

21

Current borrower –

no hardshipPositive income and balanced budget with surplus but little or

no equity in property

• Traditional refinance

• Home Affordable Refinance Program (HARP) for GSE loans

• FHA Short Refi for conventional loans

• FHA loan Streamlined Refi

• Interest Rate Reduction Refinance Loan (IRRRL) for VA loans

• USDA Refinance Program

"Online Training Done Right"

www.thecounselorscorner.net

The Decision Tree –Hardship Resolved With Surplus

22

Delinquent borrower –

hardship resolvedPositive income and balanced budget with surplus

• Full reinstatement

• Partial reinstatement with Repayment Plan

• Repayment Plan

03-21-17

12

"Online Training Done Right"

www.thecounselorscorner.net

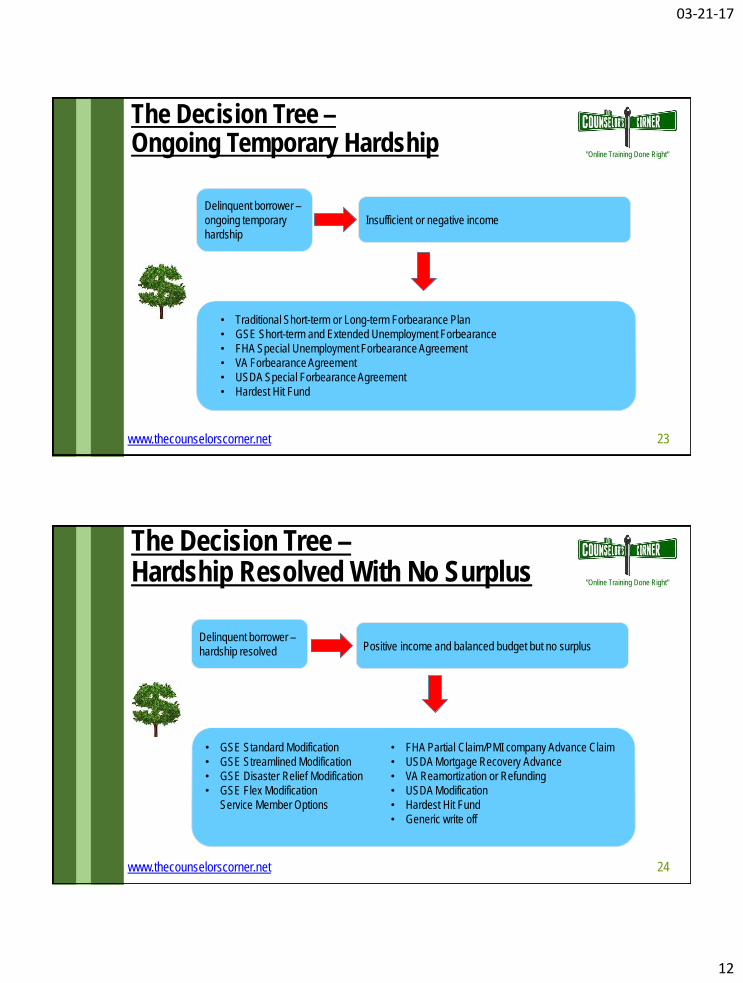

The Decision Tree –Ongoing Temporary Hardship

23

Delinquent borrower –

ongoing temporary

hardship

Insufficient or negative income

• Traditional Short-term or Long-term Forbearance Plan

• GSE Short-term and Extended Unemployment Forbearance

• FHA Special Unemployment Forbearance Agreement

• VA Forbearance Agreement

• USDA Special Forbearance Agreement

• Hardest Hit Fund

"Online Training Done Right"

www.thecounselorscorner.net

The Decision Tree –Hardship Resolved With No Surplus

24

Delinquent borrower –

hardship resolved Positive income and balanced budget but no surplus

• GSE Standard Modification

• GSE Streamlined Modification

• GSE Disaster Relief Modification

• GSE Flex Modification

Service Member Options

• FHA Partial Claim/PMI company Advance Claim

• USDA Mortgage Recovery Advance

• VA Reamortization or Refunding

• USDA Modification

• Hardest Hit Fund

• Generic write off

03-21-17

13

"Online Training Done Right"

www.thecounselorscorner.net

The Decision Tree –Permanent Hardship

25

Delinquent borrower –

permanent hardship Insufficient or negative income

• Assumption

• Straight sale (equity)

• GSE Standard Short Sale

• FHA Pre-Foreclosure Sale

• VA Compromise Claim

• USDA Pre-Foreclosure Sale

• Hardest Hit Fund

• Freddie Mac Standard (DIL)

• Fannie Mae Mortgage Release (DIL)

• FHA/VA/USDA DIL

• Service Member Options

• Bankruptcy

"Online Training Done Right"

www.thecounselorscorner.net

Polling Question #2

26

Do you use any other kind of decision tree in

your counseling process to help make

decisions?

03-21-17

14

"Online Training Done Right"

www.thecounselorscorner.net

Basic Alternatives to Foreclosure: The Decision Tree

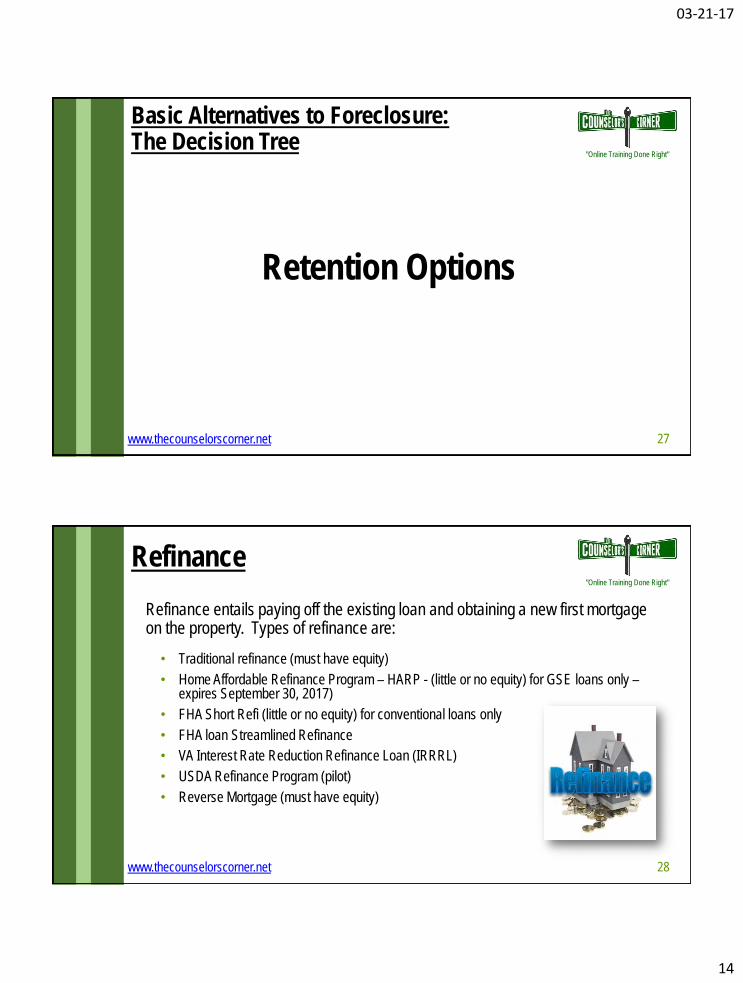

27

Retention Options

"Online Training Done Right"

www.thecounselorscorner.net

Refinance

28

Refinance entails paying off the existing loan and obtaining a new first mortgage on the property. Types of refinance are:

• Traditional refinance (must have equity)

• Home Affordable Refinance Program – HARP - (little or no equity) for GSE loans only –expires September 30, 2017)

• FHA Short Refi (little or no equity) for conventional loans only

• FHA loan Streamlined Refinance

• VA Interest Rate Reduction Refinance Loan (IRRRL)

• USDA Refinance Program (pilot)

• Reverse Mortgage (must have equity)

03-21-17

15

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Refinance When…

29

• The borrower is current on the loan and is not in imminent default

• The existing loan’s interest rate is higher than market

• The borrower wants to replace an ARM with a fixed rate mortgage

• Junior lienholders agree to subordinate

• Senior citizen with equity

"Online Training Done Right"

www.thecounselorscorner.net

Full Reinstatement

30

A full reinstatement occurs when the borrower restores a delinquent mortgage

to current status by paying the total amount delinquent, including advances,

accrued interest, legal costs and other expenses incurred.

03-21-17

16

"Online Training Done Right"

www.thecounselorscorner.net

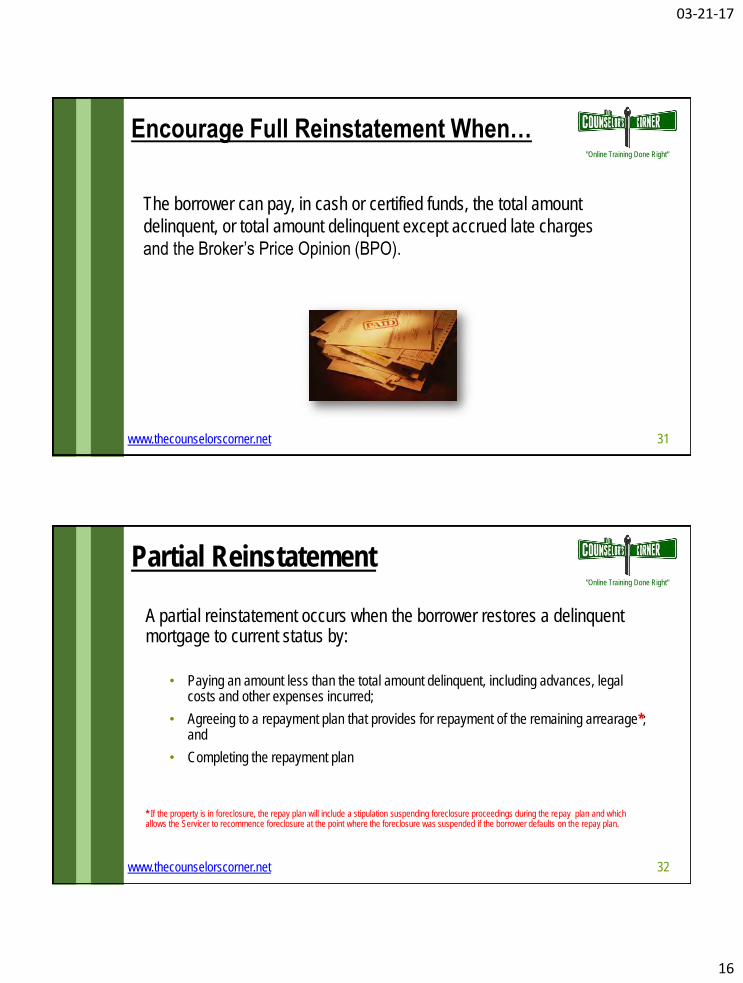

Encourage Full Reinstatement When…

31

The borrower can pay, in cash or certified funds, the total amount

delinquent, or total amount delinquent except accrued late charges

and the Broker’s Price Opinion (BPO).

"Online Training Done Right"

www.thecounselorscorner.net

Partial Reinstatement

32

A partial reinstatement occurs when the borrower restores a delinquent mortgage to current status by:

• Paying an amount less than the total amount delinquent, including advances, legal costs and other expenses incurred;

• Agreeing to a repayment plan that provides for repayment of the remaining arrearage*; and

• Completing the repayment plan

* If the property is in foreclosure, the repay plan will include a stipulation suspending foreclosure proceedings during the repay plan and which allows the Servicer to recommence foreclosure at the point where the foreclosure was suspended if the borrower defaults on the repay plan.

03-21-17

17

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Partial Reinstatement When…

33

The borrower can pay, in cash or certified funds, both of the following:

• All outstanding fees and expenses, or all outstanding

fees and expenses accept accrued late charges and the

BPO cost; and

• At a minimum, the first payment due under the

repayment plan

"Online Training Done Right"

www.thecounselorscorner.net

Knowledge Checkpoint Question #2

34

The Home Affordable Refinance Program (HARP) is only available on Freddie Mac and

Fannie Mae loans.

Is this correct?

Yes.

03-21-17

18

"Online Training Done Right"

www.thecounselorscorner.net

Repayment Plan

35

An agreement that gives the borrower a fixed period of time to bring delinquent

mortgage payments current by paying the normal monthly payment plus an additional

amount.

All Servicers and Investors allow repayment plans.

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Repayment Plan When…

36

• The reason for the delinquency has ended

• The borrower’s budget is balanced and the borrower has a monthly

surplus to apply to the mortgage payment

• The borrower can repay the delinquent amount in 12 months or less

03-21-17

19

"Online Training Done Right"

www.thecounselorscorner.net

Forbearance Plan

37

An agreement to temporarily let a borrower pay less than a full mortgage payment or pay

nothing at all during the forbearance period. The loan must be brought current (via

reinstatement, repayment plan or modification) at the end of the forbearance.

Types of forbearance plans are:

• Traditional short-term forbearance (up to six months)

• Traditional long-term forbearance (up to 12 months)

• GSE short-term Unemployment Forbearance (up to six

months)

• GSE extended Unemployment Forbearance (not to exceed

12 months’ delinquency)

• FHA Special Unemployment Forbearance

Agreement

• VA Forbearance Agreement

• USDA Special Forbearance Agreement

• Hardest Hit Fund

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Forbearance Plan When…

38

• The hardship is temporary

• The borrower wants to keep the property

• The borrower is deceased and the estate is in probate

• The borrower’s current income is insufficient to sustain the mortgage payment

• The property or borrower’s place of employment has been damaged by a natural disaster

• The hardship is due to long-term disability or serious illness of the borrower or dependent

03-21-17

20

"Online Training Done Right"

www.thecounselorscorner.net

Modification

39

A loan modification permanently changes one or more of the original terms

of the note such as:

• Increase in the unpaid principal balance (UPB) due to capitalization of interest,

escrow or other advances

• Change in the rate, monthly payment or loan term

• Forbearance or write down of a portion of the principal balance

• Change in product type (e.g., an adjustable rate mortgage to a fixed rate mortgage)

"Online Training Done Right"

www.thecounselorscorner.net

Modification Types

40

Types of loan modifications are:

• GSE Standard Modification (until October 1, 2017)

• GSE Streamlined Modification (until October 1, 2017)

• GSE Disaster Relief Modification

• Freddie Mac Flex Modification (effective October 1, 2017)

• Fannie Mae Flex Modification (effective October 1, 2017 with early use

available March 1, 2017)

• FHA Modification

• VA Reamortization/Refunding

• USDA Modification

03-21-17

21

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Modification When…

41

One of the following conditions exist:

• The borrower has income to support some level of payment

• The borrower wishes to retain the home

• The borrower had a hardship which is now resolved

• There is risk of property ownership

"Online Training Done Right"

www.thecounselorscorner.net

Knowledge Checkpoint Question #3

42

Forbearance plans are not available to borrowers who are in permanent or long-term

hardship situations.

Is this true or false?

True.

Forbearance is for temporary hardship and is always followed by another

alternative to foreclosure.

03-21-17

22

"Online Training Done Right"

www.thecounselorscorner.net

Principal Forbearance/Reduction

43

There are several programs in the industry that encourage servicers and investors to

reduce the unpaid principal balance of a loan to make the monthly payments more

affordable. Principal forbearance and reduction usually accompany a loan modification.

Types are:

• Private Mortgage Insurance company Advance Claim

• Generic write off specific to servicer/investor

• FHA Partial Claim

• USDA Mortgage Recovery Advance

• Hardest Hit Fund

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Principal Forbearance or Reduction When…

44

One of the following conditions exist:

• The first mortgage balance is higher than the property value

• The borrower has income to support the final monthly payment

• The borrower wishes to retain the home

• The borrower had a hardship which is now resolved

• There is risk of property ownership

• The investor on the loan would allow it

03-21-17

23

"Online Training Done Right"

www.thecounselorscorner.net

Mediation

45

http://www.nolo.com/legal-encyclopedia/mediation

Mediation brings together borrowers and servicers together with a mediator to

try to resolve a delinquency.

Some cities, counties and states will have mediation programs.

There is no cost to the borrower to participate in a mediation program.

If the delinquency cannot be reinstated, workout options are discussed.

http://www.nolo.com/legal-encyclopedia/state-foreclosure-mediation-programs

"Online Training Done Right"

www.thecounselorscorner.net 46

Please Raise Your Hand When You Return

03-21-17

24

"Online Training Done Right"

www.thecounselorscorner.net

Basic Alternatives to Foreclosure: The Decision Tree

47

Liquidation Options

"Online Training Done Right"

www.thecounselorscorner.net

Polling Question #3

48

Have you had clients who refuse to recognize that they can’t afford to keep

the property?

03-21-17

25

"Online Training Done Right"

www.thecounselorscorner.net

Delinquent Mortgage Assumption

49

Permits a qualified applicant to assume title to the property and the mortgage

obligation from a borrower who is delinquent or who is in imminent danger of

default. Some investors allow modification of the mortgage concurrent with

the assumption.

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Assumption When…

50

• The borrower has a permanent hardship

• The borrower has exhausted all other options to retain ownership of

the property

• There is a potential buyer for the property who is willing to assume

the loan

03-21-17

26

"Online Training Done Right"

www.thecounselorscorner.net

Knowledge Checkpoint Question #4

51

All investors allow principal write off on their loans.

Is this correct?

No.

The GSE temporary program ended at the end of last year and other investors may

not allow principal reduction at all.

"Online Training Done Right"

www.thecounselorscorner.net

Straight Sale

52

If there is equity in the property or if there is no equity and the shortfall will be paid

by the borrower, the Private Mortgage Insurer, insurance proceeds or any other

source, the borrower can sell the property and pay off the existing mortgage.

03-21-17

27

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Straight Sale When…

53

• The borrower has a permanent hardship

• The borrower has exhausted all other options to retain ownership

of the property

• The borrower might be able to recover some equity for future use

"Online Training Done Right"

www.thecounselorscorner.net

Short Sale

54

The sale of a property for less than the total amount necessary to pay the loan off in full, resulting in a shortfall.

Types are:

• GSE Standard Short Sale

• FHA Pre-Foreclosure Sale

• VA Compromise Claim

• USDA Pre-Foreclosure Sale

• Hardest Hit Fund

03-21-17

28

"Online Training Done Right"

www.thecounselorscorner.net

Encourage Short Sale When…

55

• The borrower has a permanent hardship

• The borrower can’t or doesn’t want to keep the home

• There is a potential buyer for the property and the net proceeds

will not be sufficient to pay off the mortgage

"Online Training Done Right"

www.thecounselorscorner.net

Deed in Lieu of Foreclosure

56

Permits the borrower to voluntarily convey clear property title to the servicer in

exchange for a discharge of the debt.

Types are:

• GSE Standard Deed in Lieu of Foreclosure

• FHA/VA/USDA Deed in Lieu of Foreclosure

03-21-17

29

"Online Training Done Right"

www.thecounselorscorner.net

Encourage DIL When…

57

• The borrower has a hardship

• The borrower can’t or doesn’t want to keep the home

• The borrower has been unable to sell the property

• There are no other liens on the property

• Foreclosure would take longer than six months

• The property is not in distressed condition

• The borrower has been discharged from a Chapter 7 bankruptcy

"Online Training Done Right"

www.thecounselorscorner.net

Polling Question #4

58

Have those clients, who are in denial, also refused to list their properties, even if

there’s equity?

03-21-17

30

"Online Training Done Right"

www.thecounselorscorner.net

Options of Last Resort

59

• Chapter 7 Bankruptcy

Liquidation of assets

Keep or not keep the home

• Chapter 13 Bankruptcy

Keep the home

Available income to pay the regular mortgage

payment plus

• Chapter 11 Bankruptcy

Corporate self-employed business failure

• Chapter 12 Bankruptcy

Farm

• Foreclosure

"Online Training Done Right"

www.thecounselorscorner.net

Options for Servicemembers

60

• In 2011, the GSEs announced that Permanent Change of Station Orders (PCS) is an

eligible hardship for Servicemembers under the Distant Employment Transfer hardship.

• FHA and VA have specific programs for service members

• USDA partners with many military support organizations to help service members

achieve and sustain homeownership

If a Servicemember believes his/her property is being unlawfully foreclosed, he/she should

contact the nearest JAG (Judge Advocate General) office for a consultation.

03-21-17

31

"Online Training Done Right"

www.thecounselorscorner.net 61

Beware of Loan Scams!

The scammer –

• accepts payment in advance but provides no service

• guarantees to stop foreclosure

• instructs the borrower to stop paying the mortgage to the servicer and pay the

scammer

• pressures distressed borrowers to turn the property deed over to the scammer

• promises a loan modification

http://www.preventloanscams.org/

"Online Training Done Right"

www.thecounselorscorner.net

Knowledge Checkpoint Question #5

62

In the majority of cases, a Deed in Lieu of Foreclosure is preferred over a Short Sale.

Is this true or false?

False.

Why? Tell me briefly in the question box.

03-21-17

32

"Online Training Done Right"

www.thecounselorscorner.net

Case Studies Ground Rules

63

These exercises are as much for discussion as they are for education.

Please share your best practices in the question box.

Thank you!

"Online Training Done Right"

www.thecounselorscorner.net

Let’s Review the Options Again

64

1. Refinance

2. Repayment Plan

3. Short-term Forbearance

4. Long-term Forbearance

5. Loan Modification

6. Assumption

7. Short Sale

8. Straight Sale

9. Deed in Lieu of Foreclosure

03-21-17

33

"Online Training Done Right"

www.thecounselorscorner.net

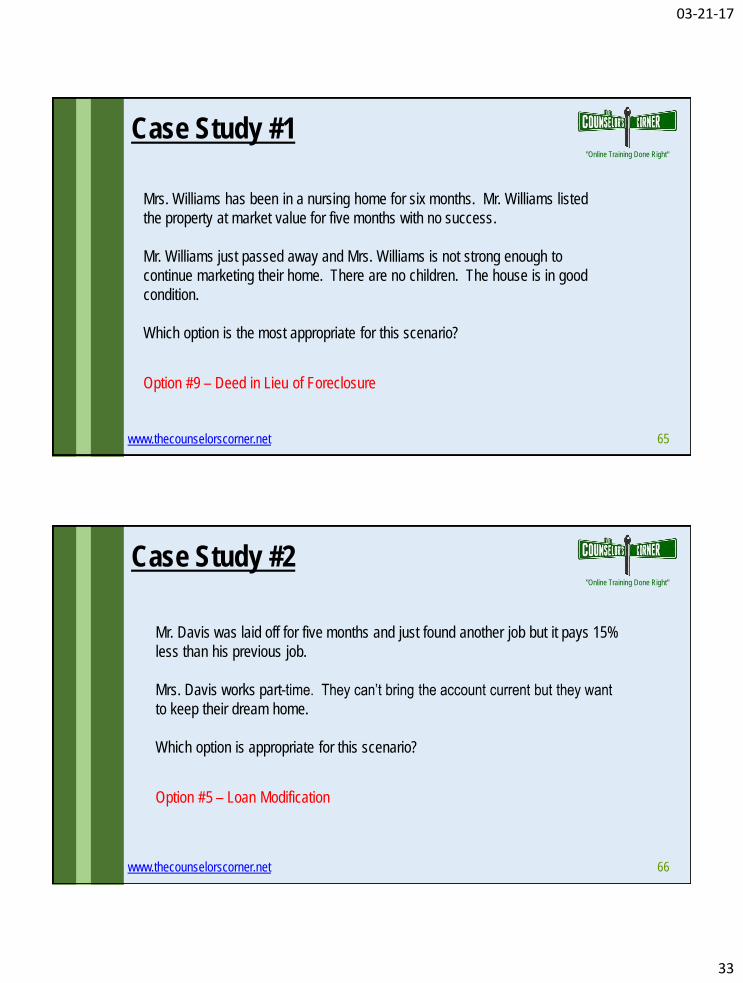

Case Study #1

65

Mrs. Williams has been in a nursing home for six months. Mr. Williams listed

the property at market value for five months with no success.

Mr. Williams just passed away and Mrs. Williams is not strong enough to

continue marketing their home. There are no children. The house is in good

condition.

Which option is the most appropriate for this scenario?

Option #9 – Deed in Lieu of Foreclosure

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #2

66

Mr. Davis was laid off for five months and just found another job but it pays 15%

less than his previous job.

Mrs. Davis works part-time. They can’t bring the account current but they want

to keep their dream home.

Which option is appropriate for this scenario?

Option #5 – Loan Modification

03-21-17

34

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #3

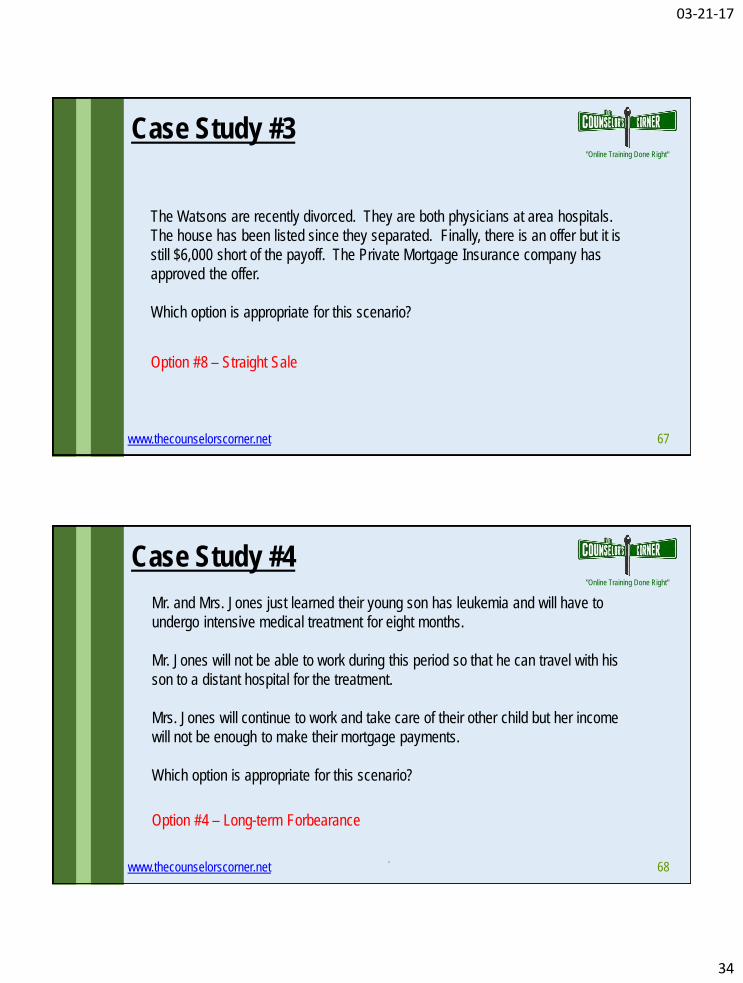

67

The Watsons are recently divorced. They are both physicians at area hospitals.

The house has been listed since they separated. Finally, there is an offer but it is

still $6,000 short of the payoff. The Private Mortgage Insurance company has

approved the offer.

Which option is appropriate for this scenario?

Option #8 – Straight Sale

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #4

68

Mr. and Mrs. Jones just learned their young son has leukemia and will have to

undergo intensive medical treatment for eight months.

Mr. Jones will not be able to work during this period so that he can travel with his

son to a distant hospital for the treatment.

Mrs. Jones will continue to work and take care of their other child but her income

will not be enough to make their mortgage payments.

Which option is appropriate for this scenario?

Option #4 – Long-term Forbearance

.

03-21-17

35

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #5

69

Mrs. Edwards was out of work for three months and even though Mr. Edwards

was working, they couldn’t make their mortgage payments.

Mrs. Edwards just got a new job making more than her previous job. They want

to catch up on their mortgage payments.

Which option is appropriate for this scenario?

Option #2 – Repayment Plan – 1.5 payments for six months

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #6

70

Mr. Kincaid has been unemployed for two years and just completed an extended

unemployment forbearance program but he has no prospects for another job.

He was counseled to put his house on the market. A buyer presented a good offer on

the property. The loan to value ratio is 170%.

Which option is appropriate for this scenario?

Option #7 – Short Sale

03-21-17

36

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #7

71

Ms. Howard has developed a serious medical problem that prohibits her from

working as a florist. Her possibilities for future employment are slim.

Her neighbor, Mr. Green, has been renting the house next door and has always

liked Ms. Howard’s house. Mr. Green has a good job and is interested in buying

the house. The loan to value ratio is 100%.

Which option is appropriate for this scenario?

Option #6 – Assumption

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #8

72

Mr. Smith and 50 other employees were furloughed from their jobs at a manufacturing

plant. Mr. Smith doesn’t have enough savings to make his mortgage payments.

He expects to be back to work in two months.

Which option is appropriate for this scenario?

Option #3 – Short-term Forbearance

03-21-17

37

"Online Training Done Right"

www.thecounselorscorner.net

Case Study #9

73

Mr. Marshall has a 6.5%, 30-year conventional mortgage on his condo. Mr. Marshall

is financially secure, has never been delinquent on his loan, is not in financial distress

and can afford to make his monthly mortgage payments.

Mr. Marshall would like to get his rate lowered to less than 5% on his mortgage.

He has little or no equity in the property.

Which option is appropriate for this scenario?

Option #1 – GSE HARP refinance

"Online Training Done Right"

www.thecounselorscorner.net

HUD Certification Exam Resources

74

• HUD Housing Counseling Certification Final Rule – https://www.hudexchange.info/resource/5191/housing-counseling-new-certification-

requirements-final-rule/

• HUD Housing Counseling Certification Press Release – https://www.hudexchange.info/resource/5193/hud-press-release-hud-announces-new-

housing-counseling-certification-requirements/

• HUD Housing Counseling Certification Requirements Overview – https://www.hudexchange.info/programs/housing-counseling/certification/

• HUD Housing Counseling Certification Requirements FAQs – https://www.hudexchange.info/resource/5194/housing-counseling-new-

certification-requirements-faqs/

• HUD other Programs Covered Under Final Rule – https://www.hudexchange.info/resource/5192/other-hud-programs-covered-under-huds-

final-rule-for-housing-counseling-certification/

• HUD training and certification exam website – http://www.hudhousingcounselors.com/

• HUD housing counseling resources – https://www.hudexchange.info/programs/housing-counseling/

• HUD certification final rule key provisions and dates – https://www.hudexchange.info/resources/documents/Housing-Counseling-Certification-

Chart-of-Key-Provisions-and-Dates.pdf

• HUD Stakeholders December 19, 2016 recorded conference call on the certification final rule –

https://www.hudexchange.info/trainings/courses/stakeholders-conference-call-on-the-final-rule-on-housing-counseling-certification/

03-21-17

38

"Online Training Done Right"

www.thecounselorscorner.net

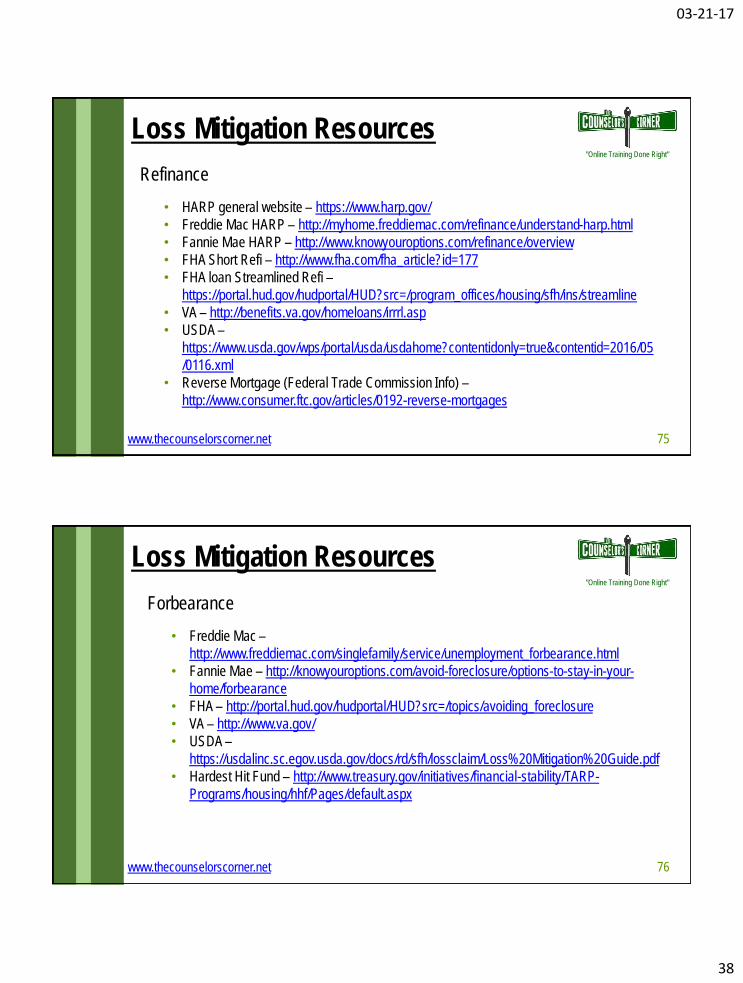

Loss Mitigation Resources

75

Refinance

• HARP general website – https://www.harp.gov/

• Freddie Mac HARP – http://myhome.freddiemac.com/refinance/understand-harp.html

• Fannie Mae HARP – http://www.knowyouroptions.com/refinance/overview

• FHA Short Refi – http://www.fha.com/fha_article?id=177

• FHA loan Streamlined Refi –

https://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/ins/streamline

• VA – http://benefits.va.gov/homeloans/irrrl.asp

• USDA –

https://www.usda.gov/wps/portal/usda/usdahome?contentidonly=true&contentid=2016/05

/0116.xml

• Reverse Mortgage (Federal Trade Commission Info) –

http://www.consumer.ftc.gov/articles/0192-reverse-mortgages

"Online Training Done Right"

www.thecounselorscorner.net

Loss Mitigation Resources

76

Forbearance

• Freddie Mac –

http://www.freddiemac.com/singlefamily/service/unemployment_forbearance.html

• Fannie Mae – http://knowyouroptions.com/avoid-foreclosure/options-to-stay-in-your-

home/forbearance

• FHA – http://portal.hud.gov/hudportal/HUD?src=/topics/avoiding_foreclosure

• VA – http://www.va.gov/

• USDA –

https://usdalinc.sc.egov.usda.gov/docs/rd/sfh/lossclaim/Loss%20Mitigation%20Guide.pdf

• Hardest Hit Fund – http://www.treasury.gov/initiatives/financial-stability/TARP-

Programs/housing/hhf/Pages/default.aspx

03-21-17

39

"Online Training Done Right"

www.thecounselorscorner.net

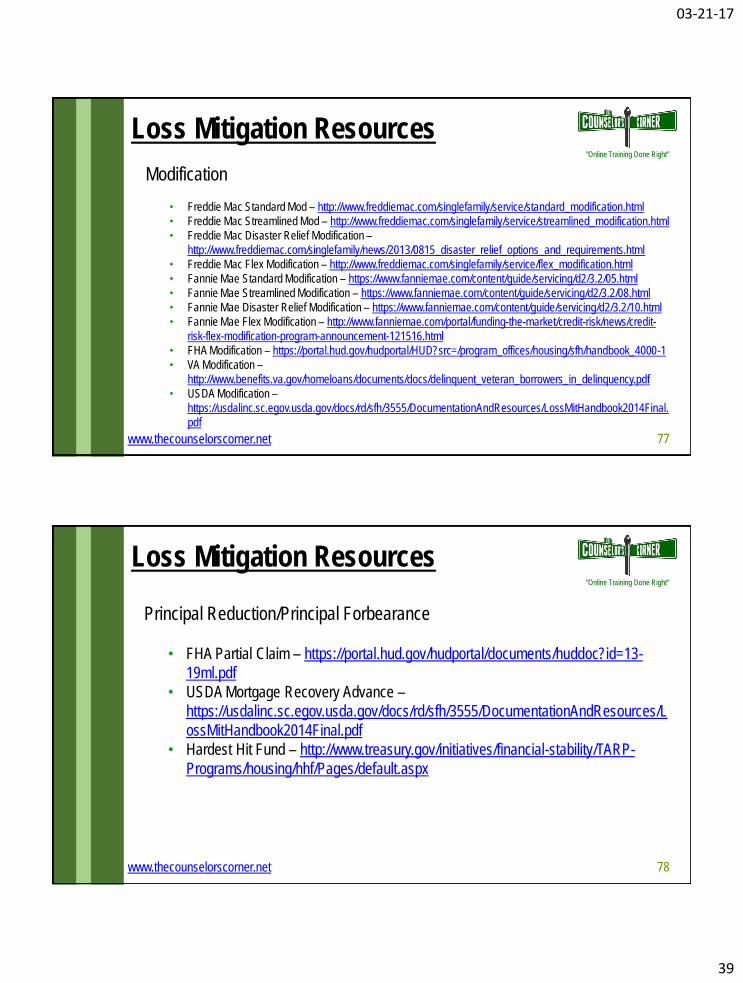

Loss Mitigation Resources

77

Modification

• Freddie Mac Standard Mod – http://www.freddiemac.com/singlefamily/service/standard_modification.html

• Freddie Mac Streamlined Mod – http://www.freddiemac.com/singlefamily/service/streamlined_modification.html

• Freddie Mac Disaster Relief Modification –

http://www.freddiemac.com/singlefamily/news/2013/0815_disaster_relief_options_and_requirements.html

• Freddie Mac Flex Modification – http://www.freddiemac.com/singlefamily/service/flex_modification.html

• Fannie Mae Standard Modification – https://www.fanniemae.com/content/guide/servicing/d2/3.2/05.html

• Fannie Mae Streamlined Modification – https://www.fanniemae.com/content/guide/servicing/d2/3.2/08.html

• Fannie Mae Disaster Relief Modification – https://www.fanniemae.com/content/guide/servicing/d2/3.2/10.html

• Fannie Mae Flex Modification – http://www.fanniemae.com/portal/funding-the-market/credit-risk/news/credit-

risk-flex-modification-program-announcement-121516.html

• FHA Modification – https://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/handbook_4000-1

• VA Modification –

http://www.benefits.va.gov/homeloans/documents/docs/delinquent_veteran_borrowers_in_delinquency.pdf

• USDA Modification –

https://usdalinc.sc.egov.usda.gov/docs/rd/sfh/3555/DocumentationAndResources/LossMitHandbook2014Final.

"Online Training Done Right"

www.thecounselorscorner.net

Loss Mitigation Resources

78

Principal Reduction/Principal Forbearance

• FHA Partial Claim – https://portal.hud.gov/hudportal/documents/huddoc?id=13-

19ml.pdf

• USDA Mortgage Recovery Advance –

https://usdalinc.sc.egov.usda.gov/docs/rd/sfh/3555/DocumentationAndResources/L

ossMitHandbook2014Final.pdf

• Hardest Hit Fund – http://www.treasury.gov/initiatives/financial-stability/TARP-

Programs/housing/hhf/Pages/default.aspx

03-21-17

40

"Online Training Done Right"

www.thecounselorscorner.net

Loss Mitigation Resources

79

Short Sale and Deed-in-Lieu of Foreclosure

• Freddie Mac Short Sale –

http://www.freddiemac.com/singlefamily/service/short_sales.html

• Fannie Mae Short Sale – http://knowyouroptions.com/avoid-foreclosure/options-to-

leave-your-home/short-sale

• Freddie Mac DIL –

http://www.freddiemac.com/singlefamily/service/standard_deed_in_lieu.html

• Fannie Mae DIL – http://knowyouroptions.com/avoid-foreclosure/options-to-leave-

your-home/mortgage-release

"Online Training Done Right"

www.thecounselorscorner.net

Additional Resources

80

• General

Freddie Mac loan lookup – https://ww3.freddiemac.com/corporate/?intcmp=LLT-HPimage

Freddie Mac Guide – http://www.freddiemac.com/singlefamily/guide/

Fannie Mae loan lookup – https://knowyouroptions.com/loanlookup

Fannie Mae Guide – https://www.fanniemae.com/singlefamily/guides?taskId=task-58

HUD – http://portal.hud.gov/hudportal/HUD

VA – http://www.va.gov/

USDA – http://www.usda.gov/wps/portal/usda/usdahome

• USDA contacts –

USDA guaranteed loans customer service > 1-866-550-5887

USDA direct loans customer service > 1-800-414-1226 and fax number to send

authorizations > 314-457-4431

USDA multifamily customer service > 1-866-600-7984

03-21-17

41

"Online Training Done Right"

www.thecounselorscorner.net

Additional Resources

81

• Hardest Hit Fund new allocation announcement – https://www.treasury.gov/press-center/press-

releases/Pages/jl0358.aspx

• CFPB consumer complaint page – http://www.consumerfinance.gov/complaint/

• CFPB help for struggling borrowers – http://files.consumerfinance.gov/f/201402_cfpb_mortgages_help-for-

struggling-borrowers.pdf

• HUD Office of Fair Housing and Equal Opportunity – http://www.hud.gov/fairhousing

• National Industry Standards for Homeownership Education and Counseling –

http://www.homeownershipstandards.com/Home/Home.aspx

• Bankruptcy

Legal Aid – http://www.lsc.gov/local-programs/program-profiles

"Online Training Done Right"

www.thecounselorscorner.net

General Resources

82

• Free credit report – https://www.annualcreditreport.com/index.action

Equifax – 1-800-685-1111 – http://www.Equifax.com

Experian – 1-888-397-3742 – http://www.Experian.com

Trans Union – 1-800-888-4213 – http://www.transunion.com

• Property value estimates –

http://www.zillow.com

http://www.eppraisal.com

http://www.realtor.com

• Freddie Mac Housing Professionals Resource Center Subscribe –

http://www.freddiemac.com/singlefamily/housingpros/subscribe.html

• Freddie Mac Real Estate Professionals Resource Center Subscribe –

http://www.freddiemac.com/singlefamily/housingpros/real_estate_professionals_resource_center.html

03-21-17

42

"Online Training Done Right"

www.thecounselorscorner.net

Military Resources

83

• Freddie Mac – http://myhome.freddiemac.com/mortgage-help/military-assistance.html

• Fannie Mae – http://knowyouroptions.com/news/help-for-military-homeowners

• CFPB – http://www.consumerfinance.gov/blog/servicemembers-you-have-new-mortgage-

protections-in-2014/

• Help for homeless Veterans – http://www.va.gov/homeless/

• Armed Forces Legal Assistance Program Office –

http://legalassistance.law.af.mil/content/locator.php

• Veterans Crisis Line – http://veteranscrisisline.net/

"Online Training Done Right"

www.thecounselorscorner.net

News Resources

84

• CFPB

• DSNews

• Equifax

• Experian

• Fannie Mae

• Federal Trade Commission

• Freddie Mac

• Google Alerts – set up alerts for any topic

• HousingWire

• HUD listserv

• myFICO

• The Counselor’s Corner free membership

• TransUnion

03-21-17

43

"Online Training Done Right"

www.thecounselorscorner.net

What is the Housing Counselor’s Responsibility?

85

To know the programs and the options to assist in your client’s coaching and counseling needs.

To stay up to date with industry news and training, maintain your membership with The Counselor’s Corner and invite your associates to join.

Membership and all webinars are free!

"Online Training Done Right"

www.thecounselorscorner.net

Continued Education Hours

86

• 2.0 hours for today’s session

• Must take the short test to receive the Certificate of Completion

• The test link will be sent to you within three hours after the end of this webinar

IMPORTANT! Please add [email protected] to your address book

• Once you pass the test, you can print your certificate right away at the test site

Please complete the survey that will pop up at the end of today’s webinar.

03-21-17

44

"Online Training Done Right"

www.thecounselorscorner.net

Upcoming Webinars

87

"Online Training Done Right"

www.thecounselorscorner.net

Strategic Partnership

88

• Additional online training events

• Increased resources

• Extended networking opportunities

• More Continued Education Hours

http://www.afcpe.org/

03-21-17

45

"Online Training Done Right"

www.thecounselorscorner.net 89

Self-care for Housing Counselors

http://www.eleanorbrownn.com/

"Online Training Done Right"

www.thecounselorscorner.net 90

03-21-17

46

"Online Training Done Right"

www.thecounselorscorner.net 91

Please complete the post session survey.

Disable your pop-up blocker now!

Thanks for your participation today and…

Have a great rest of the week!

Basic Alternatives to Foreclosure: The Decision Tree