operational audit on accounts receivable (a case …

TRANSCRIPT

OPERATIONAL AUDIT ON ACCOUNTS RECEIVABLE

(A Case Study of PT Yamazaki Indonesia)

SKRIPSI

Presented in partial fulfillment of the requirements for

The Bachelor’s Degree in Accounting

By

Jose Bonifacio Pakpahan

008201500012

FACULTY OF BUSINESS

ACCOUNTING STUDY PROGRAM

PRESIDENT UNIVERSITY

CIKARANG, BEKASI

2019

ii

PLAGIARISM CHECK RESULT

OPERATIONAL AUDIT ON ACCOUNTS RECEIVABLE

(A Case Study of PT Yamazaki Indonesia)

iii

iv

v

DECLARATION OF ORIGINALITY

I hereby declare that the thesis entitled:

OPERATIONAL AUDIT ON ACCOUNTS RECEIVABLE

(A Case Study of PT Yamazaki Indonesia)

It is true of my own work or not plagiarism of the work of other. If in the future

proved that this scientific work is not my own work or plagiarism of the work of

others, then I am willing to accept sanctions in accordance with applicable laws

and regulations.

Cikarang, 17 December 2018

Jose Bonifacio Pakpahan

vi

PANEL OF EXAMINERS APPROVAL

OPERATIONAL AUDIT ON ACCOUNTS RECEIVABLE

(A Case Study of PT Yamazaki Indonesia)

Submitted by Jose Bonifacio Pakpahan, Accounting Study Program, Faculty of

Business, has been assessed and proved to pass the oral examination held on 9

January 2019.

Panel of Examiner,

Advisor,

Drs. Gatot Imam Nugroho,MBA.,CA

Examiner 1,

Examiner 2,

Andrianantenaina Hajanirina, BA.,

B.Sc.,M.Sc.,MM.

Mila Reyes BSBA.,CPA.,MBA.

Approved By

Date:………………………………

Andi Ina Yustina, M.Sc., CMA.

Head of Study Program

vii

ACKNOWLEDGEMENT

These are the best supporters that I ever have since the very beginning of

this Skripsi process. I realized that without them I would never accomplish every

single step until I reach this phase of life. They deserve all my gratitude.

1. My Father, Jesus Christ, thank You for Your love, strength and guidance

from the very beginning of my life up until now. Thank you for never letting

me down, for every tear you have turned into joy, for every single

opportunity that you entrusted to me. You have done a lot for me. This

skripsi is fully dedicated to You.

2. Papa and mama, there are not enough words to describe how thankful I am

for both of you. I know I don't show how grateful I am enough, but I really

am. You both have taught me so much, and going away to college and being

apart from you has made me realize how much you both mean to me.

Distance means nothing; since both of you are something precious for me.

Thank you for always being there for me. Without the two of you, I don't

know where I would be. I realize I do not thank you enough for everything.

And for that, I apologize. If I have learned anything while being away from

you, it is that you are the most important people in my life, and I love you

both more than anything. So, mom and dad... Thank you. For everything. I

promise I will work hard to make you proud.

viii

3. My brother and my sister, Juan Benedict and Arthia Josephine. I look up to

you in so many ways, and you inspire me more than you could ever imagine.

I know, I was once the annoying little brother who got everything you guys

wanted, and you were the mean big brother and sister who always picked on

me (if we’re being honest, you still do), but now that we are older and

somewhat more mature, I realize how lucky I am to have an older siblings. I

know I’m lucky to have you guys, and even luckier to have one that I’m so

close to. I couldn’t imagine life without you, and I wouldn’t want to. Thanks

for not only being my bro and sis but also being the greatest friend I could

ever ask for. I'm so proud to call you my big bro and sis.

4. My brother from another mother, bang Daniel Tommy Tambunan. Thank you

for having me in your company to conduct this research. Thank you for every

help you gave to me, you’re like a living savior for my skripsi. I’m glad that I

did ever spent some times in eating Indomie, playing badminton, sleep

together, playing Mobile Legends (the combination of Harith/ Gord and

Rafaela) and most importantly, working together as a team in the last

Company Dinner of PT Yamazaki Indonesia with a person like you. Thank

you for the opportunity and I feel really honored for that.

5. My advisor, Drs. Gatot Imam Nugroho, Ak., MBA., CA. Thank you for your

time, guidance and advices for me in doing this skripsi. Semangat sir

nyalegnya! Saya doain terus!

ix

6. Pak Frans, Pak Jun, Ka Rischa. Thank you for entrusting me in conducting

the research in PT Yamazaki Indonesia; it was a really expensive and great

experience.

7. My lovable friends in PT Yamazaki Indonesia, bang Hendra, bang Niko, Pak

Agung, ka Depi, bang Restu, Ius, pak Budi, ka Rachma, nci Shella, bu Fanny,

ka Dwi, Okky, Indri, ka Ganis and bu Nasha. THANK YOU VERY MUCH

FOR ALL OF THE DATAS GIVEN TO ME! WORKING IN YAMAZAKI

WAS AN EXCITEMENT FOR ME! SEE YOU ON TOP GUYS! I WILL

MISS YOU ALL. THANK YOU SO MUCH.

8. Thank you Mami Tari, for the love you gave to me during my research in PT

Yamzaki Indonesia. I will surely miss your panic expression.

9. Thank you pak Untung for the kuah soto 3 ribu that we eat together with pak

David, ka Hendra and bang Tommy. You’re surely is the funniest guy I’ve

met. I will really miss eating “soto pak Untung” together.

10. My dear skripsi survivor and a roommate of mine, Fredrik Wijaya. Thanks

for making all the way of this semester colorful by all your jokes and

encouragement. I wish you have a great career ahead and success in your

thesis defense as well. I’m sorry if I snore to loud, hehehe.

11. Komsel KomBaWa, for my partners Agatha, Fanya, Daniel, Iki, Nabila and

Feli. Thank you so much for the encouragement throughout these 2 years of

serving as Kakak Komsel together. You guys will always have a special part

in my heart. For Gilbert, Rida, Fidel, Angie and Fidel, thank you for asking

x

me “kapan sidang ko?” every single day we met and all prayers. It boosts up

my spirit. Wishing you all has a great phase on your university life.

12. My dearest friend Sonia. Thank you for reminding me of my things, cheering

me up when I’m down, and supporting me through the process of completing

this skripsi. You may think that you did nothing great, but for me, all those

“nothing great” means world to me. Now that we are apart means that we

have to be more responsible with our activities! Good luck in completing

your college life. Thank you for everything and God bless you and family.

13. Fredrik Wijaya and Ignasius Dymas, my classmates. Thank you for being a

great mate in class and also being a great supporter of mine. I wish you all a

great success on your skripsi and defense along with your career path ahead.

14. Community of Love President University. I have no regret of joining this

family. Thank you for letting me to be a part of this family and for every

opportunity given to me to serve Him through this community. I am blessed

beyond measure. Thank you for being a great supporter. May the light will

always shine in this community. Let all the glory just for Him.

15. My chit chat mates, Amsal 17:17 members. For Jovaldi, Refo, Moses,

Jeremy, Joshua, and Holy, thank you for lots of laughs, supports, and prayers.

I wish you guys a great study and career path ahead.

16. All examiners, I am not able to cross this path without you.

17. All Accounting lecturers and friends. You made up my university life. Thank

you for everything.

xi

I do realize that this skripsi is far from the perfection and I would never be

able to have it done without those great people and every one that I may not able

to mention one by one. I hope that this research will be valuable and useful for

future users.

Jose Pakpahan

The Researcher

xii

RECOMMENDATION LETTER FROM THESIS ADVISOR

This thesis is prepared and submitted by

Name : Jose Bonifacio Pakpahan

Student ID : 008201500012

Faculty : Business

Study program : Accounting

Field of study : Managerial Accounting

Thesis title : OPERATIONAL AUDIT ON ACCOUNTS

RECEIVABLE (A Case Study of PT Yamazaki

Indonesia)

Has been reviewed and found to have satisfied the necessities for oral defenseas

partial fulfillment of the requirements for the Bachelor’s Degree in Accounting.

Cikarang, 17 December 2018

Bekasi, Indonesia

Acknowledged by:

Head of Study Program Thesis Advisor

Andi Ina Yustina, M.Sc., CMA. Drs. Gatot Imam Nugroho,MBA.,CA

xiii

TABLE OF CONTENTS

SKRIPSI ............................................................................................................................ i

PLAGIARISM CHECK RESULT ................................................................................ ii

DECLARATION OF ORIGINALITY ......................................................................... v

PANEL OF EXAMINERS APPROVAL ..................................................................... vi

ACKNOWLEDGEMENT ............................................................................................ vii

RECOMMENDATION LETTER FROM THESIS ADVISOR ............................... xii

TABLE OF CONTENTS ............................................................................................. xiii

LIST OF TABLES ....................................................................................................... xvi

LIST OF FIGURES .................................................................................................... xvii

LIST OF APPENDICES.............................................................................................. xix

CHAPTER I: INTRODUCTION .................................................................................. 1

1.1 Background.............................................................................................................. 1

1.2 Problem Formulation ............................................................................................... 5

1.3 Benefits of Research ................................................................................................ 5

1.4 Scope and Limitations of Research ......................................................................... 6

CHAPTER II: LITERATURE REVIEW ..................................................................... 8

2.1 Introduction ............................................................................................................. 8

2.2 Account Receivables Management ......................................................................... 8

2.3 Account Receivables Turnover ............................................................................. 10

xiv

2.4 Aging Schedule ..................................................................................................... 11

2.5 Bad Debt and Allowance Provision ...................................................................... 13

2.6 Factors Affecting the Amount of Receivables ...................................................... 13

2.6.1 Percentage of Credit Sales .............................................................................. 14

2.6.2 Stuck Billing Customer ................................................................................... 14

2.6.3 Billing Business .............................................................................................. 14

2.7 Variables Affecting Receivables ........................................................................... 15

2.8 Receivable Billing ................................................................................................. 16

2.9 Policy for Uncollectible Accounts Receivable ...................................................... 16

CHAPTER III: METHODOLOGY ............................................................................ 17

3.1 Research Framework ............................................................................................. 17

3.2 Location and Time of Research ............................................................................. 20

3.3 Data Collection ...................................................................................................... 20

3.4 Processing and Data Analysis ............................................................................... 20

3.4.1 Analysis per Component ................................................................................. 21

3.4.2 Trend Analysis ................................................................................................ 22

3.4.3 Cash Conversion Cycle Analysis .................................................................... 23

3.4.4 Analysis of Company’s Financial Ratio ......................................................... 24

CHAPTER IV: RESULTS AND DISCUSSION ........................................................ 25

4.1 Account Receivable Management in PT Yamazaki Indonesia ............................. 25

xv

4.2 Factors Affecting the Amount of Receivables at PT Yamazaki Indonesia ........... 27

4.3 Account Receivable Management Process in PT Yamazaki Indonesia ................ 39

4.4 Debt Collection Procedure .................................................................................... 43

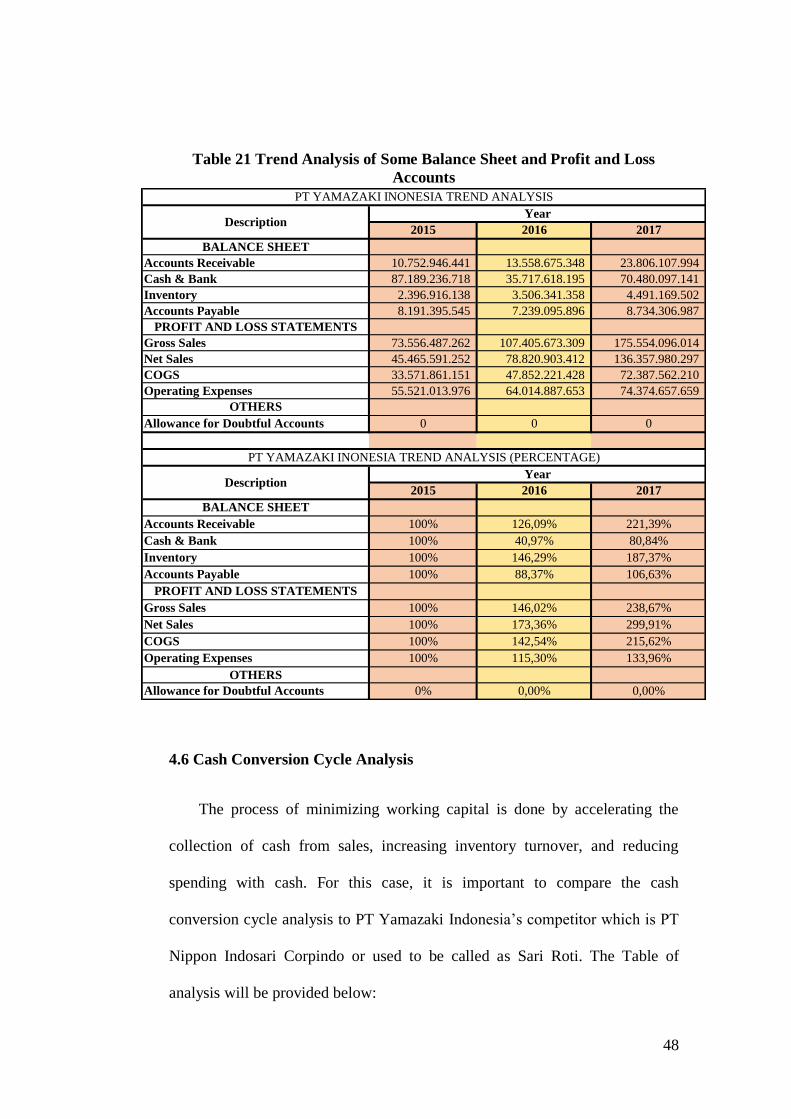

4.5 Trend Analysis....................................................................................................... 44

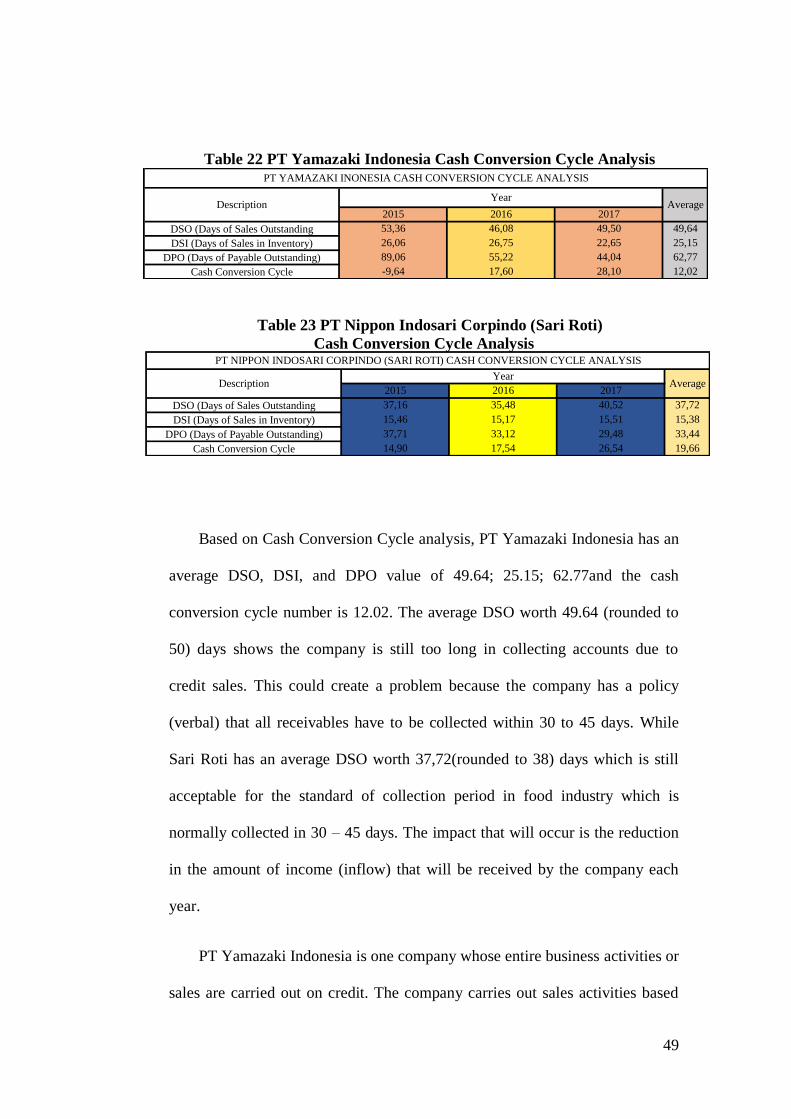

4.6 Cash Conversion Cycle Analysis .......................................................................... 48

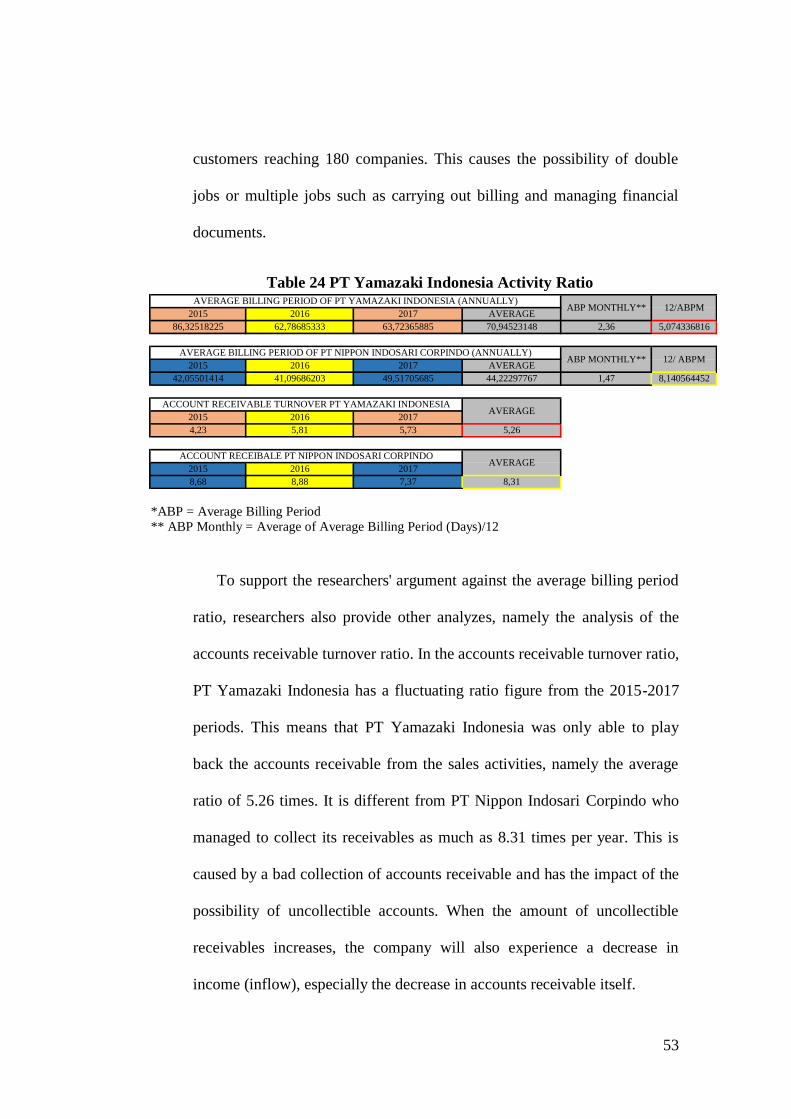

4.7 Financial Ratio Analysis........................................................................................ 51

4.7.1 Activity Ratio .................................................................................................. 51

4.8 Managerial Implications ........................................................................................ 54

4.9 Findings ................................................................................................................. 55

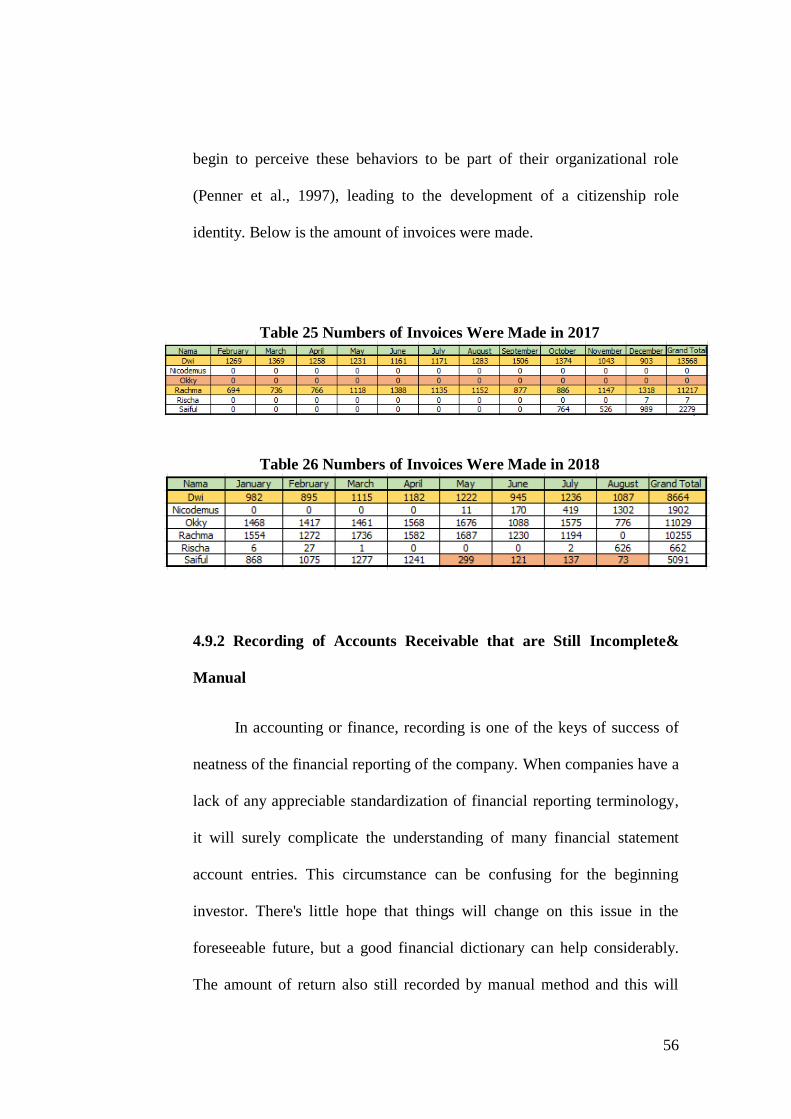

4.9.1 Insufficient and Ineffective Number of AR Employees ................................. 55

4.9.2 Recording of Accounts Receivable that are Still Incomplete ......................... 56

4.9.3 Provision ......................................................................................................... 57

4.9.3 Over Sales Returns.......................................................................................... 58

CHAPTER V: CONCLUSION AND RECOMMENDATION ................................ 60

5.1 Conclusion ............................................................................................................. 60

5.2 Recommendation ................................................................................................... 61

REFERENCE ................................................................................................................ 62

APPENDICES (INTERVIEW) .................................................................................... 65

APPENDICES (DOCUMENTATION) ....................................................................... 69

xvi

LIST OF TABLES

Table 1 Analysis per Component of Balance Sheet (Partial) .......................................... 26

Table 2 Cash Conversion Cycle Analysis ....................................................................... 27

Table 3 Trend Analysis of Some Balance Sheet and Profit and Loss Accounts............. 29

Table 4 Some Balance Sheet and Profit and Loss Accounts .......................................... 29

Table 5.1 PT Supra Boga Lestari’s July Aging Schedule ............................................... 30

Table 5.2 PT Supra Boga Lestari’s July Aging Schedule (New Orders) ........................ 30

Table 6.1 PT Fajar Mitra Indah’s July Aging Schedule.................................................. 31

Table 6.2 PT Fajar Mitra Indah’s July Aging Schedule (New Order) ............................ 31

Table 7.1 PT Lion Super Indo’s July Aging Schedule.................................................... 31

Table 7.2 PT Lion Super Indo’s July Aging Schedule (New Order) .............................. 31

Table 8.1 PT Naga Swalayan’s July Aging Schedule ..................................................... 31

Table 8.2 Naga Swalayan’s July Aging Schedule (New Order) ..................................... 31

Table 9.1 Supra Boga Lestari’s August Aging Schedule ................................................ 32

Table 9.2 Supra Boga Lestari’s August Aging Schedule (New Order) .......................... 32

Table 10.1 PT Fajar Mitra Indah’s August Aging Schedule ........................................... 32

Table 10.2 PT Fajar Mitra Indah’s August Aging Schedule (New Order) ..................... 33

Table 11.1 PT Lion Super Indo’s August Aging Schedule ............................................. 33

Table 11.2 PT Lion Super Indo’s August Aging Schedule (New Order) ....................... 33

Table 12.1 PT Naga Swalayan’s August Aging Schedule .............................................. 33

Table 12.2 PT Naga Swalayan’s August Aging Schedule (New Order) ........................ 33

Table 13.1 PT Supra Boga Lestari’s September Aging Schedule .................................. 34

Table 13.2 PT Supra Boga Lestari’s September Aging Schedule (New Orders) ........... 34

xvii

Table 14.1 PT Fajar Mitra Indah’s September Aging Schedule ..................................... 34

Table 14.2 PT Fajar Mitra Indah’s September Aging Schedule (New Order)................ 34

Table 15.1 PT Lion Super Indo’s September Aging Schedule ....................................... 34

Table 15.2 PT Lion Super Indo’s September Aging Schedule (New Order).................. 34

Table 16.1 PT Naga Swalayan’s September Aging Schedule ........................................ 35

Table 16.2 Naga Swalayan’s September Aging Schedule (New Order) ........................ 35

Table 17.1 Supra Boga Lestari’s October Aging Schedule ............................................ 35

Table 17.2 Supra Boga Lestari’s October Aging Schedule (New Order) ....................... 35

Table 18.1 PT Fajar Mitra Indah’s October Aging Schedule ......................................... 35

Table 18.2 PT Fajar Mitra Indah’s October Aging Schedule (New Order) .................... 36

Table 19.1 PT Lion Super Indo’s October Aging Schedule ........................................... 36

Table 19.2 PT Lion Super Indo’s October Aging Schedule (New Order) ...................... 36

Table 20.1 PT Naga Swalayan’s October Aging Schedule............................................. 36

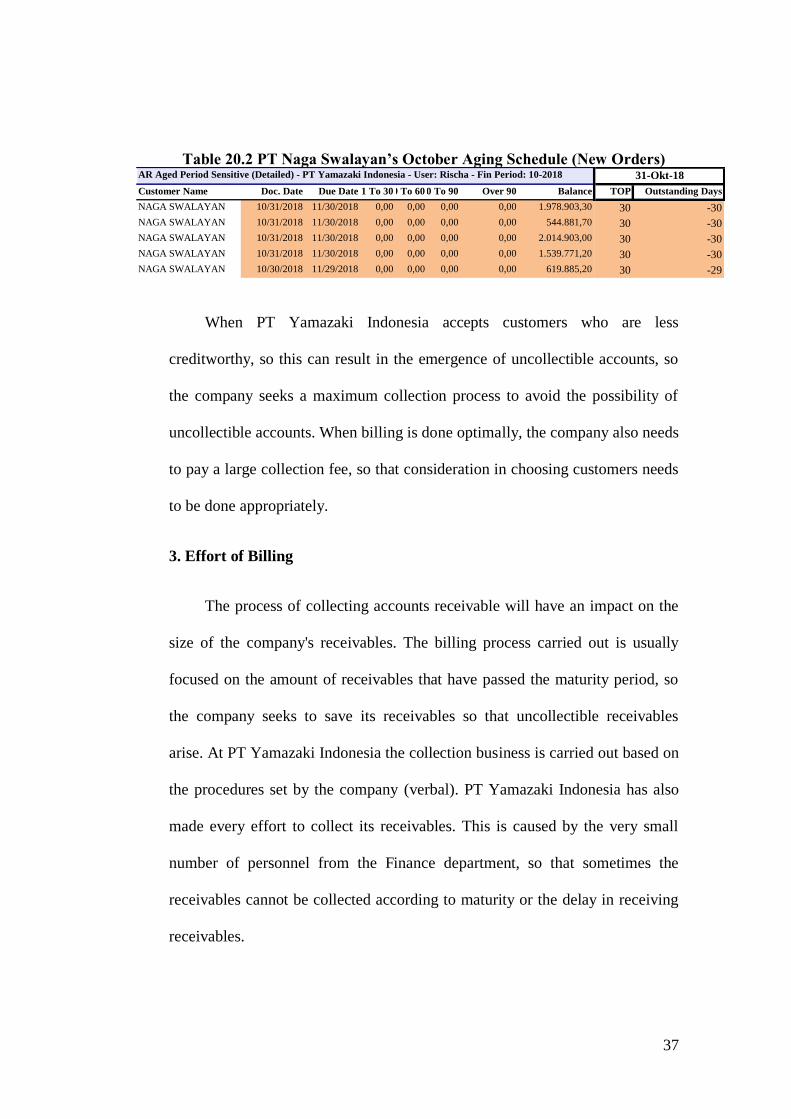

Table 20.2 PT Naga Swalayan’s October Aging Schedule (New Order) ....................... 37

Table 21 Trend Analysis of Some Balance Sheet and Profit and Loss Accounts........... 48

Table 22 PT Yamazaki Indonesia Cash Conversion Cycle Analysis ............................. 49

Table 23 PT Nippon Indosari Corpindo Cash Conversion Cycle ................................... 49

Table 24 PT Yamazaki Indonesia Activity Ratio ........................................................... 53

Table 25&26 Numbers of Invoices Were Made in 2017 & 2018 ................................... 56

Table 27&28 AR Balance Sheet Record of PT Yamazaki Indonesia 2017&2018 ......... 56

Table 29 Statements of Financial Position ...................................................................... 58

Table 30 Data Return ...................................................................................................... 59

xviii

LIST OF FIGURES

Figure 1 Accounts Receivable Ratio (Investopedia) ....................................................... 10

Figure 2 Traditional Aging Schedule .............................................................................. 12

Figure 3 Research Framework ........................................................................................ 19

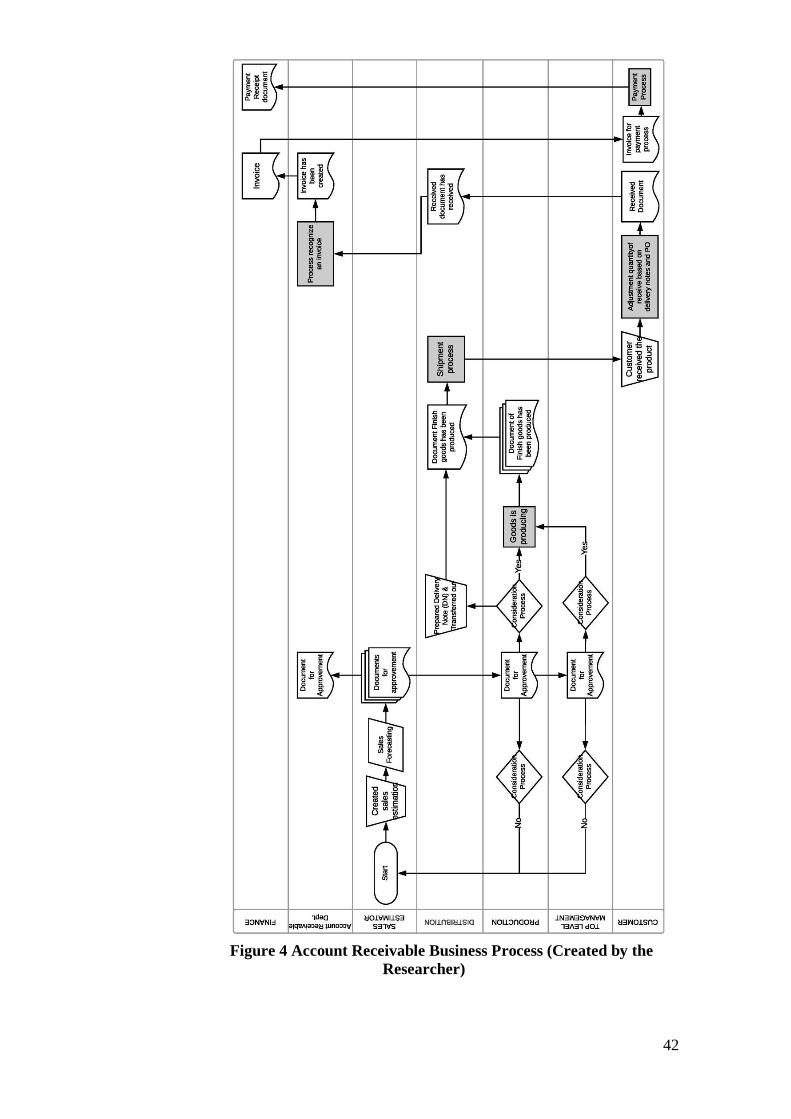

Figure 4 Accounts Receivable Business Process (Created by the Researcher) .............. 42

Figure 5 – Descriptive Statistics for FMCG and Airline Industry .................................. 50

xix

LIST OF APPENDICES

APPENDICES (INTERVIEW)

Appendix 1 – Engagement with Director, Manager & Supervisor ................................. 65

Appendix 2 – Interview with Accounts Receivable (Supervisor) ................................... 66

APPENDICES (DOCUMENTATION)

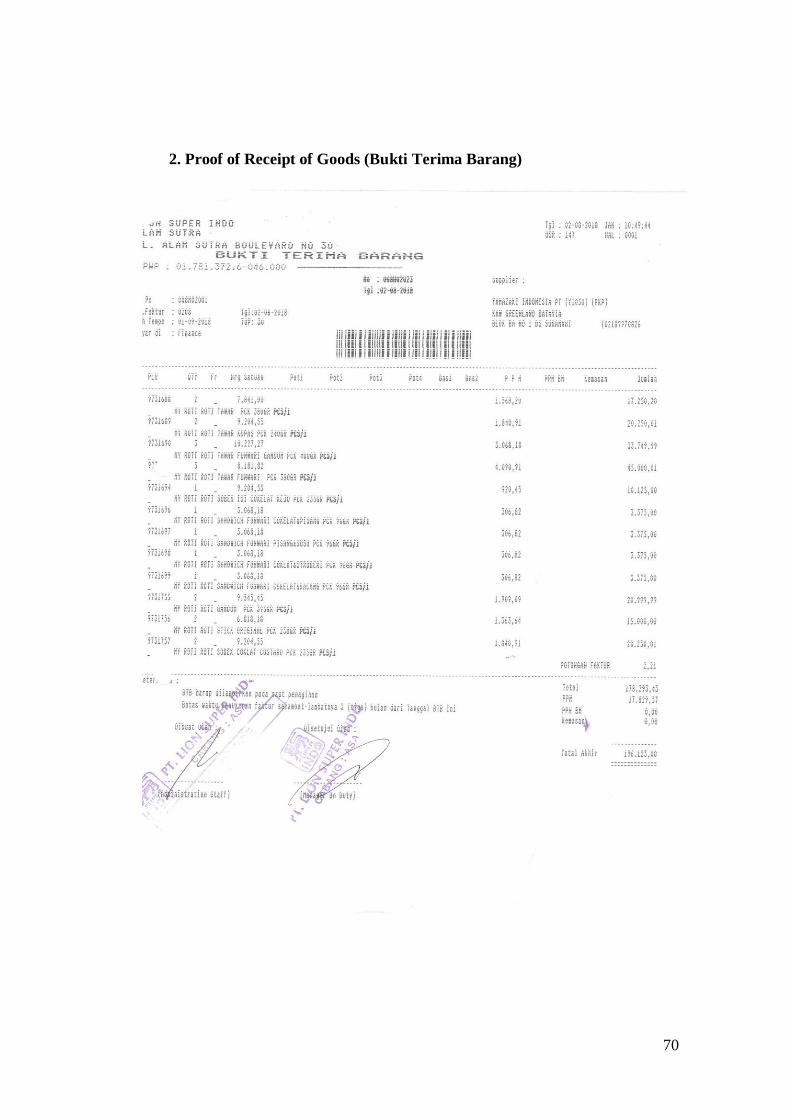

Appendix 1 – Invoice ...................................................................................................... 69

Appendix 2 – Proof of Receipt of Goods (Bukti Terima Barang) .................................. 70

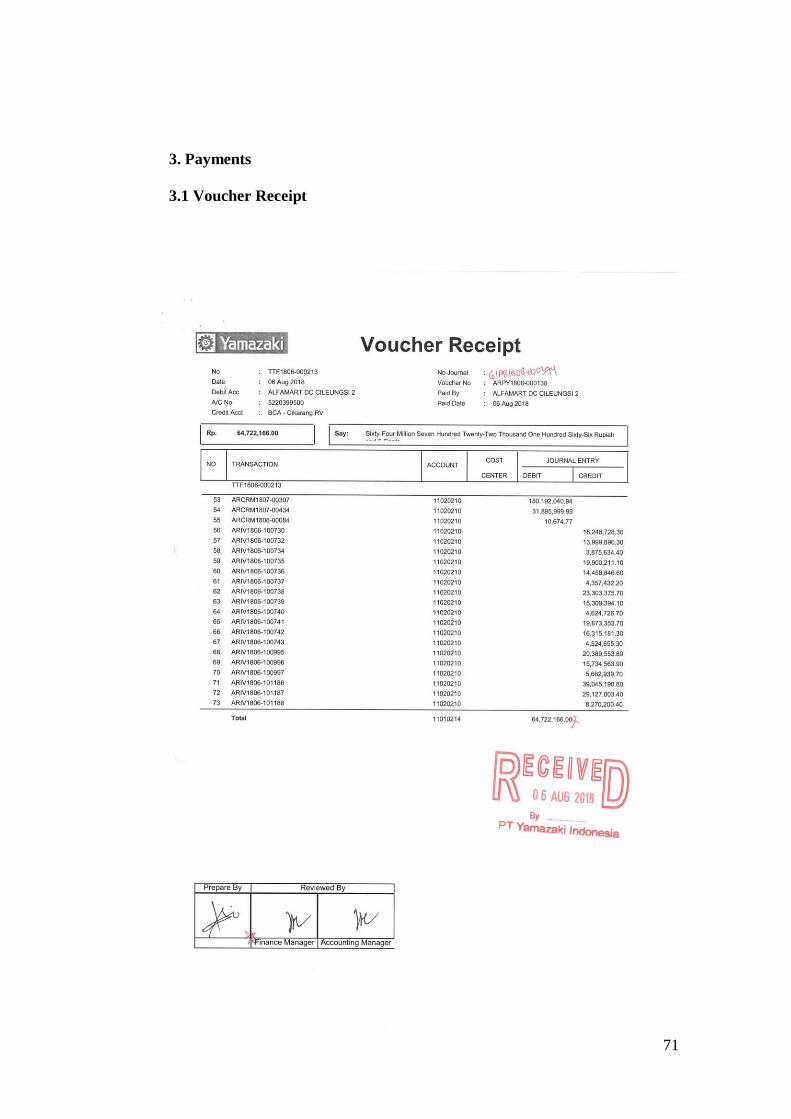

Appendix 3 – Payments .................................................................................................. 71

Appendix 3.1 – Voucher Receipt ............................................................................. 71

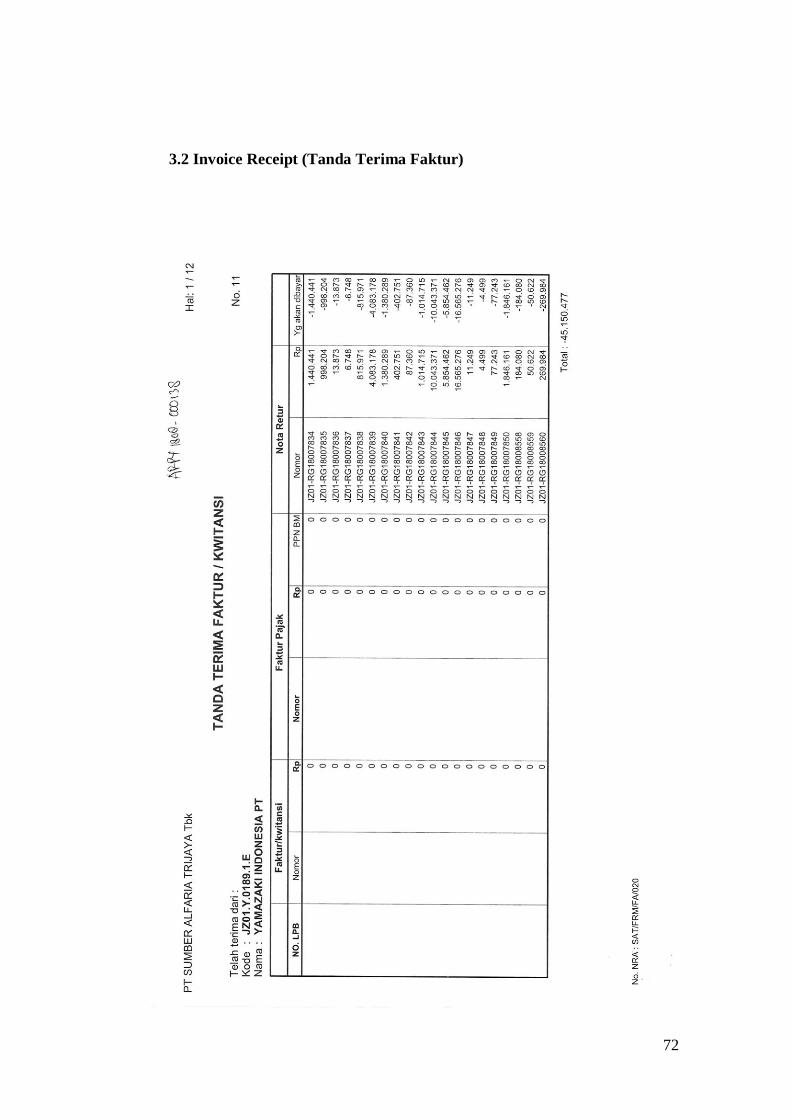

Appendix 3.2 – Invoice Receipt (Tanda Terima Faktur) ......................................... 72

Appendix 3.3 – Invoice Receipt (Compiled) ........................................................... 73

Appendix 4 – Delivery Notes .......................................................................................... 74

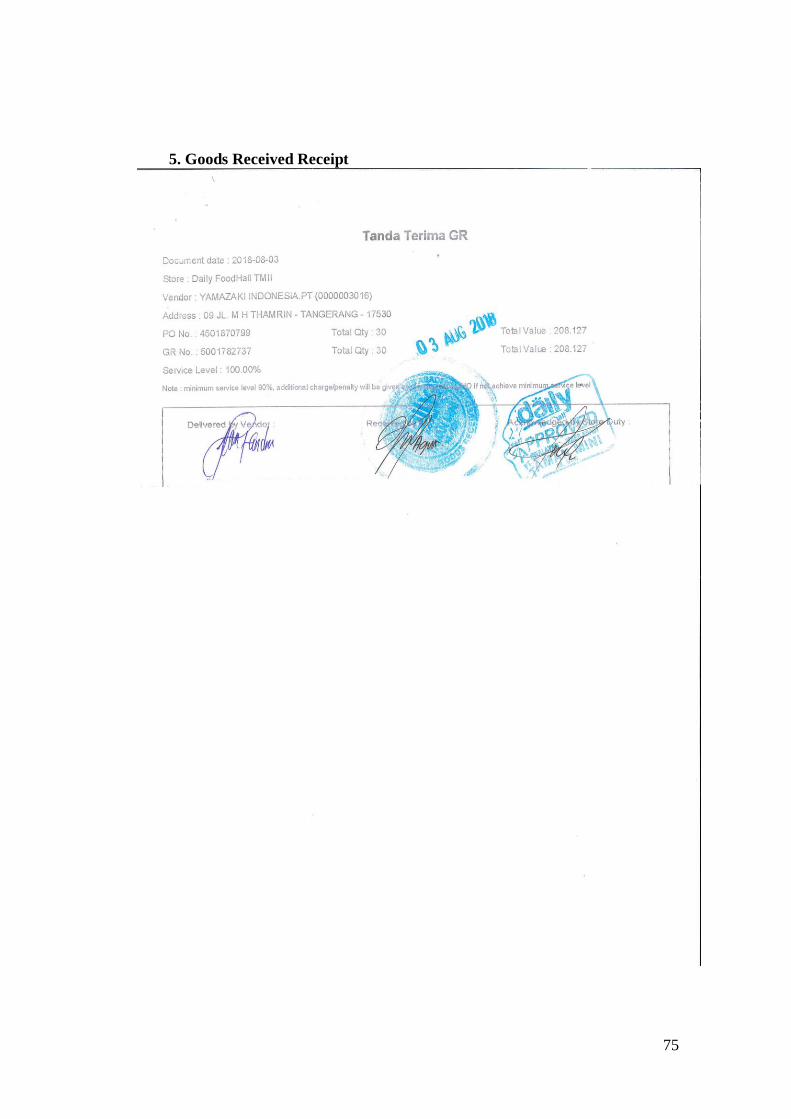

Appendix 5 – Goods Received Receipt .......................................................................... 75

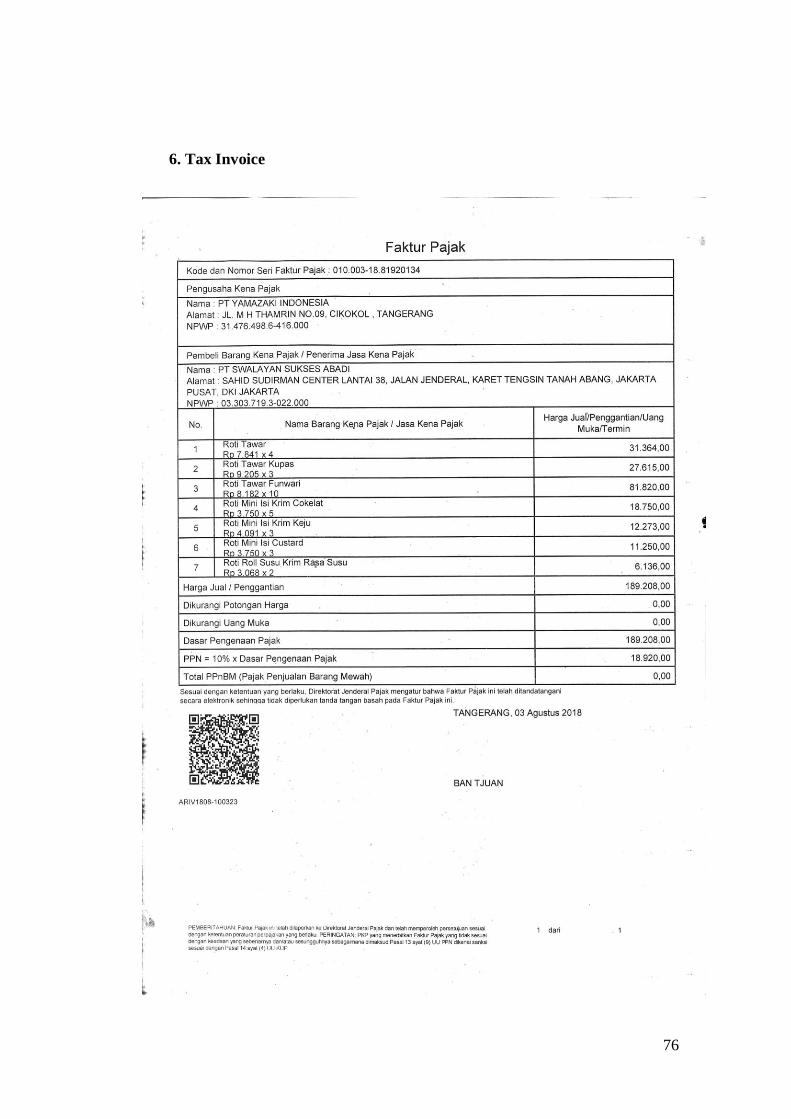

Appendix 6 – Tax Invoice ............................................................................................... 76

Appendix 7 – Company Acceptance Letter .................................................................... 77

Appendix 8 – Company’s Confirmation Letter .............................................................. 78

Appendix 9 – The Researcher with Mr. Frans (Director) ............................................... 79

Appendix 10 – The Researcher with Mr. Karno (HRGA General Manager) ................. 79

Appendix 11 – The Researcher with Fin/Acc/Mar/Dis Staff .......................................... 80

Appendix 12 – The Researcher with Mr. Furumi (Director) .......................................... 80

Appendix 13 – The researcher with Mr. Ichiro Saito (President Director) ..................... 81

xx

OPERATIONAL AUDIT ON ACCOUNTS RECEIVABLE

(A Case Study of PT Yamazaki Indonesia)

ABSTRACT

PT Yamazaki Indonesia is one company whose entire business activities or

sales are carried out on credit. The company carries out sales activities based on

policies set by the company (verbal). The applied credit policy is expected to be

able to provide optimal benefits and be able to increase customer satisfaction.

This is due to the high level of credit sales risk, which requires companies to carry

out all sales procedures based on their credit policies. This study aims to

determine the accounts receivable management system run at PT Yamazaki

Indonesia, analyze the factors that affect the size of PT Yamazaki Indonesia's

receivables, and analyze the effectiveness of controlling receivables against cash

flows. The results of this study indicate that based on an analysis of the accounts

receivable management system, PT Yamazaki Indonesia has carried out the

management, and control of accounts receivable based on the verbal SOP

(Standard Operation Procedure) that has been set by the company, but there are

still some things that are not implemented. Factors that influence the amount of

receivables are the percentage of credit sales, stuck billing customer, and effort of

billing. PT Yamazaki Indonesia has a large amount of receivables in the balance

sheet, mainly influenced by the large percentage of credit sales and effort of

billing undertaken. Based on the analysis of financial performance in the

company's financial statements for the period of 2016 - 2017, it shows that the

company still has good financial performance. This is indicated by a number of

positive financial ratios. Accounts receivable control carried out by PT Yamazaki

Indonesia has not been effective against the company's cash collection. This is

evidenced from the results of the cash conversion cycle analysis which is less than

the average value of the FMCG industry and means that the amount of

receivables owned is not good enough to be converted into cash (if compared with

FMCG industries) due to the existence of inhibiting factors such as collection and

not properly applied credit analysis to all customers.

Keyword: Accounts Receivable, Allowance for Doubtful Accounts, Provision,

financial performance, Accounts Receivable Management.

1

CHAPTER I

INTRODUCTION

1.1 Background

One of the purposes of setting any business is to maximize profit; hence

sales revenue will improve the profitability of that company. Selling by cash is

the most ideal way of improving cash inflow but at times a company must sell

on credit which is normally termed as trade credit. Effective receivables

management and the ability of a company to collect the credit must be the

prerequisite of selling on credit otherwise it will affect the liquidity and the

condition of the company. As suggested by Paramasivan and Subramanian

(2009) most businesses sell on credit or by cash. Irrespective of best efforts of

organizations to do effective credit assessment it is difficult to avoid credit

problems as indicated by Kimmel et al. (2011). Burt (2004) reaffirmed the

essence of comprehensive credit assessment of customers.

In a company, especially a manufacturing company, financial management

has an important role in a company's management function. When the company

conducts its sales system on credit, then the receivables will arise. This will

have an effect on the company's financial statements, especially the impact on

cash flows. As for a problem that often occurs is when consumers are negligent

in making payments. This will have an impact on the company, namely the

delay in repayment of accounts receivable and the company's cash flow will

decrease so that it affects the effectiveness of the company's operations.

2

Cash Conversion Cycle is an analysis that uses an approach that company

goals to minimize working capital provided that the working capital must be

sufficient to finance the company's operations. The process of minimizing

working capital is done by accelerating the collection of cash from sales,

increasing inventory turnover, and reducing spending with cash (Keown,

2010).

PT Yamazaki Indonesia is one of the companies where all business

activities or sales are carried out on credit. The company carries out sales

activities based on policies set by the company (verbal). The applied credit

policy is expected to be able to provide optimal benefits and be able to increase

customer satisfaction. This is due to the high level of credit sales risk that

requires companies to carry out all sales procedures based on their credit

policies.

The company carries out sales procedures based on its credit policies

because it relates to the characteristics of products sold, which are related to the

quality of products that provide a guarantee within the specified time limit, so

consumers will usually get a purchase return when the product used does not

match the expected performance. The purchase returns made by consumers will

have an impact on the receipt of receivables that will be paid by consumers to

the company. Therefore, in a company there needs to be a good debt control

system in order to be able to manage its finances and continue to operate to

meet market demand and maintain customer loyalty and trust.

3

According to Fabozzi and Peterson (2003) whenever a company decides to

sell to customers on credit it creates accounts receivables. Repayment of debt is

critical for the liquidity position of any company, for it is important for debtor

and creditor to agree on how the debt will be settled before the debt must be

granted as advised by Finlay (2008). In management of debtors, it is imperative

to ensure that repayment of the credit sale is done within the agreed period and

most importantly with the minimum administrative cost to the company as

suggested by Paramasivan and Subramanian (2009). Specific industry and kind

of customers can influence a company to consider credit sales. In managing

receivables among others there must be consideration in the following as

suggested by Mecklin (2007) such as creditworthy of the customer, monitoring

of debt, and sanction plan for defaulters, a policy on bad debt and possibly

factoring the debt.

Credit policy must contain a detailed procedure for granting credit and its

repayment as suggested by Burt (2004). Reuvid (2010) explained that credit

policy must guide credit management and more so ensure that there is a

balance between a liberal and stricter credit. Brigham and Ehrhardt (2011)

reaffirmed that credit policy must have captured credit terms, period for

payments and policy on the debt collection. Credit policy guides credit

management and must include credit terms and standards with debt collection

approach as advised by Burt (2004). Brealeyet al. (2011) recommended that in

dealing with debtors, companies must establish the following: assessment of

4

the credit worthiness of the customer, credit terms and effective collection

procedure.

Watson and Head (2013) stressed that the expenses of debt collection must

not surpass the amount to be recover. Paramasivan and Subramanian (2009)

indicated that it will make a business sense if companies can charge interest on

overdue repayment by customers to push them to pay on time. Kimmel et. al.

(2011) pointed out that there is the need for a company’s collection policy but

without efficient system of debt collection in place it will affect repayment on

time negatively. Watson and Head (2013) recommended that it is important for

companies to get it right between strict collection policy and the real benefits

ensuing from a decent management of credit. Brealeyet. al., (2011) suggested

that smaller companies without specialized credit department can hire debt

collection agents to help them in that direction.

Adelman and Marks (2014) recommended that factoring is an option

business can use to get their money back if it is becoming difficult to recover

the debt through the internal systems. Brigham and Ehrhardt (2011) indicated

that as much as there is the need of credit policy for a company without

effective monitoring system to check the observance of the credit policy

repayment of the credit can be delayed or will not be paid at all. Effective

follow-up measures on the debtors list of a company does not only enhances

the opportunity of getting the money on time it also put the debtors on their

alert to fulfill repayment on time as suggested by Kimmel et. al. (2011) and

5

Burt (2004). This paper examines accounts receivable management of PT

Yamazaki Indonesia

1.2 Problem Formulation

PT Yamazaki Indonesia is a company that has not long been established

(only 4 years) and is not very experienced in running its business. In its

implementation, the company is still experiencing problems with the collection

of receivables. The company has customers of up to 180 companies, which

shows that the company has been highly trusted and is able to provide products

according to customer demand but without a good management this could

possibly become a boomerang to the company. The formulation of the problem

in this study, namely:

1. How does the receivable management system run at PT Yamazaki

Indonesia?

2. What factors influence the amount of receivables of PT Yamazaki

Indonesia?

3. What is the Account Receivable performance of PT Yamazaki Indonesia in

the period 2015 – 2017?

1.3 Benefits of Research

The results of this study are expected to provide value and benefits to

various parties in need, especially for the company, such as consideration in

6

implementing the system of controlling accounts receivable and in the

decision-making process relating to the policy of accounts receivable. In

addition, this research is also expected to be used as a reference or guideline for

further research.

1.4 Scope and Limitations of Research

When conducting research, researchers only discuss the system of

controlling accounts receivable related to the effectiveness, efficiency and

accuracy. This is obtained from an analysis of the accounts receivable control

system that has been carried out and analysis of receivables held by the

company in the period 2015-2017.

This study presents the new evidence of receivables management impact

on the firm financial collectability performance, which is done by analyzing the

trend, data given by PT Yamazaki Indonesia from 2015 – 2018. The relevance

on the impact of receivables management on the firm performance, specifically

on firm financial collectability performance which in reality is still lagging.

Hence, this study attempts for broadening the research to a deeper level of

receivables management.

This research is expected to be beneficial for the readers and broaden the

point of view for both the other researcher and also the management of PT

Yamazaki Indonesia and to go beyond the other factors that may affect account

management collection performance. This research is mainly focused on the

analysis of account receivables management in PT Yamazaki Indonesia.

7

The rest of this skripsi is organized as follows. In the next chapter, that is

literature review section, the researcher will explain more about the variables

and the research done by other researcher which will be used as the basis for

reference of the study. The methods used to investigate and gather the data are

in chapter 3. The results of this study along with the discussion are outlined in

chapter 4, and the conclusion of all this skripsi will be provided in the chapter

5.

8

CHAPTER II

LITERATURE REVIEW

2.1 Introduction

This section will explain more about the variables and the research done

by other researcher which will be used as the basis for reference of the study, such

as the Account Receivables Management, Account Receivables Turnover, Aging

Schedule, Bad Debt and Allowance Provision and etc. This section will give a

clear picture about the definition of those variables, the theory being used for this

research, along with the research gaps in this study.

2.2 Account Receivables Management

If we derive a definition of an account from the AMA Dictionary of

business and management, it is defined as a statement of transaction. The

definition stated in AMA Dictionary actually relates to the definition of

accounts receivable which is defined as an amount owed to a business by

customers for invoice amounts (transactions) classified as current accounts in

the balance sheet. Many companies sell credit in order to sell more products or

services. Receivables arising from such sales are usually classified as trade

accounts receivable or notes receivable. The term receivables include all claims

in the form of money against other parties, including individuals, companies, or

other organizations. Receivables usually have a significant share of the

company's total current assets (Warren, 2005).

9

A company manages its receivables depending on what the company sells

on credit. The more that is sold on credit, the higher the proportion of assets

related to receivables. As a result, when discussing the management of

accounts receivable, it is actually also discussing one fifth of the company's

assets. In addition, because the cash flow from the sale cannot be invested until

the receivables are paid, control of the receivables becomes increasingly

important. The efficient billing determines the profitability and liquidity of the

company (Keown, 2010).

Managers and external users of financial statements need to measure how

efficiently a company uses business assets or operating assets, especially

elements of certain working capital such as accounts receivable, inventory, and

trade payables. The most common relationship commonly used to monitor

accounts receivable is the average billing period (Stice, 2004).

The importance of a good debt management provides an impact on the

company's financial statements and can then show a company's performance.

According to Warren (2005), relating to the process of controlling accounts

receivable, companies attempt to limit the value of uncollectible receivables by

implementing various control devices. The most important controls are related

to the function of credit approval. This control involves investigating the

customer's credibility. The two accounting methods for recording receivables

that are not expected to be collected, which are the allowance method and the

direct write-off method. Seeing this, the role of financial managers is very

10

influential in the management of accounts receivable which is closely related to

the overall financial condition of the company.

2.3 Account Receivables Turnover

The Account receivables turnover ratio shows how many times a company

pays off its average accounts receivable within a given period of time, it could

be monthly or yearly basis (Investopedia, 2017). The account receivables

turnover ratio is an activity ratio used by management to understand how a

company handles the collection of payments owed to the business. If the

accounts receivable turnover ratio declines from one year to the next, it may

signal a company's collections department is unable to collect from older

customers or the company has an excessive amount of debt. If the account

receivables turnover ratio increases from one year to the next, it may be a sign

of an aggressive collections department or a conservative credit policy on the

part of the company. The formula to calculate the ratio is:

Figure 1 Accounts Receivables Ratio (Investopedia)

Accounts Receivable Turnover

Accounts Receivable

Turnover =

Beginning + Ending AR

Average AR

Average Accounts

Receivable (AR) = 2

Net Sales

11

2.4 Aging Schedule

The Accounts Receivable (A/R) Aging Schedule, also known as a

Schedule of Accounts Receivable, allows a company or entities to analyze the

accounts receivable due to the company from the customers engaged. It

provides general information, at a point of time, on which the companies are

expecting payment from and can also assist with determining the likelihood of

collection. As accounts become more aged, their collectability becomes less

certain (BMO, 2016).

The Aging Schedule is a popular accounts receivable tool (Pike and

Cheng, 2001) and is widely referred to in the normative accounting and finance

literature (Peacock, et.al., 2003; Arnold, 2005). It comprises a classification of

outstanding balances according to the period of time they have been

outstanding (Equation 1).

These age categories can be calibrated according to months, weeks, or

days, depending on an organization’s requirements, and are frequently

expressed as a percentage relative to the total accounts receivable balance

(Lewellen and Johnson, 1972; Lewellen and Edmister, 1973; Zeune, 1991). If

debts are collected on time, most debts should be younger, and few should be

older. It is assumed that increased collection efficiency would reduce the

percentage of debt in the older categories.

12

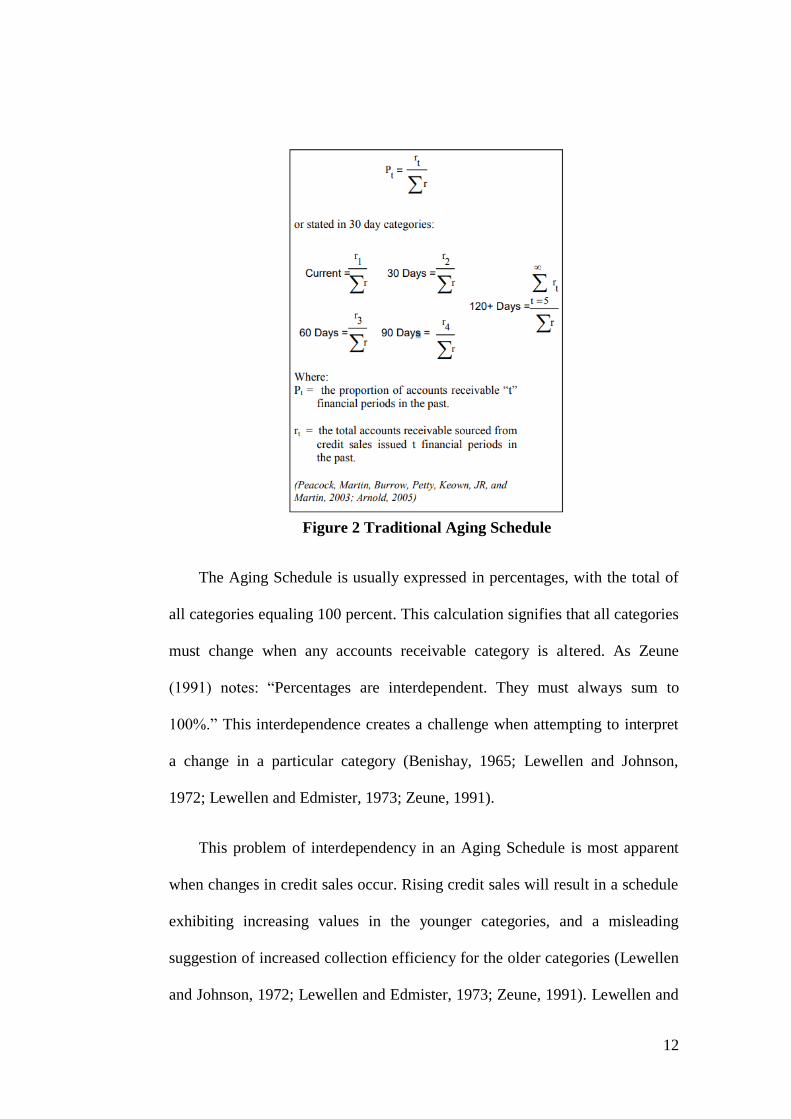

Figure 2 Traditional Aging Schedule

The Aging Schedule is usually expressed in percentages, with the total of

all categories equaling 100 percent. This calculation signifies that all categories

must change when any accounts receivable category is altered. As Zeune

(1991) notes: “Percentages are interdependent. They must always sum to

100%.” This interdependence creates a challenge when attempting to interpret

a change in a particular category (Benishay, 1965; Lewellen and Johnson,

1972; Lewellen and Edmister, 1973; Zeune, 1991).

This problem of interdependency in an Aging Schedule is most apparent

when changes in credit sales occur. Rising credit sales will result in a schedule

exhibiting increasing values in the younger categories, and a misleading

suggestion of increased collection efficiency for the older categories (Lewellen

and Johnson, 1972; Lewellen and Edmister, 1973; Zeune, 1991). Lewellen and

13

Edminster (1973) argue that it is only in periods of evenly occurring credit

sales that an Aging Schedule can be seen to represent a tool that accurately

depicts collection efficiency. Zeune (1991) and Lewellen and Johnson (1972)

conclude that the Aging Schedule produces an incorrect analysis and false

warning patterns can be raised by normal sales fluctuations. One can conclude

that the sum of credit sales achieved in the most recent 30-day period is

positively correlated to the current category in a traditional Aging Schedule.

2.5 Bad Debt and Allowance Provision

If collectability is probable at the outset, but subsequently facts and

circumstances change such that collection from the customer is no longer

probable, the amount of the debt deemed to be uncollectible should be written

off as a bad debt expense or the company should provide a bad debt provision

for the account, as it is appropriate. Contingences, provides guidance to

determine if it is probable that amounts will or will not be collected. The

company should account for any impairment of its existing receivable.

2.6 Factors Affecting the Amount of Receivables

Manufacturing companies are companies that have business or business

activities from the start of production operations to the sales of products

produced. Manufacturing companies that carry out sales activities on credit will

14

get additional assets in the current assets, which are marked by the emergence

of receivables. Then the receivables that have arrived at maturity, then cash

flow occurs. According to Keown (2010), the factors that influence the size of

investment in receivables are:

2.6.1 Percentage of Credit Sales

The greater the sales on credit, the greater the receivables that will be

obtained. When a company experiences sales growth, the level of investment in

accounts receivable will also go up.

2.6.2Stuck Billing Customer

Determining the type of customer is a decisive variable in seeing customer

qualifications in obtaining credit. When a company receives customers who

are less creditworthy, it will result in a default.

2.6.3Effort of Billing

The key to maintaining control over receivable billing is the fact that the

probability of default is increasing with the age of the bill. Control over

receivables is focused on the control and elimination of receivables that are

past due. Strength and timeliness of billing will affect the period of bills that

are due but still negligent to pay.

15

2.7 Variables Affecting Receivables

According to Jusuf (2005) internal variables are variables (factors) that are within

the control of the company. While external variables are variables (factors) that are

outside the company and the company does not have the ability to control these factors

at all. Internal variable are company policies related to accounts receivable consisting

of:

a. Sales

The greater the sales in credit, the greater the profitability. But if credit

sales are limited, the company is more concerned with credit safety.

b. Doubtful Accounts

If the greater the amount of the receivables, the greater the possibility of

uncollectible accounts.

c. Sales Return

When PT Yamazaki sales are dominated with return, then there will be a

high chance of Deductive Receivable and Revenue.

2.8 Receivable Billing

There are several techniques that can be used to increase billing on receivables

that are due. The cheapest billing is by phone and mail (Maya, 2005). Billing

techniques include:

• Sent a letter

• On the phone

16

• visited

• Using agents / other people (debt collector)

The company can use the person or the State Auction and Receivable

Affairs Agency (BUPLN) or Legal actions or civil claims

Credit insurance is formed with the intention to protect manufacturers,

retailers, service companies and other companies against unexpected credit

losses. In collection of accounts receivable, financial managers must determine

the average billing time that can be received or the level of outstanding sales

days as well as the ratio of total uncollectible receivables to total operating

revenues made.

2.9 Policy for Uncollectible Accounts Receivable

Strength and timeliness of billing will affect the period of bills that are due

but still negligent to pay and will affect the amount of receivables (Keown,

2010). The company has the possibility to obtain funding sources easily and

quickly up to 80% of the value of its sales invoice on credit, namely through

factoring (Siamat, 2005). The definition of factoring company based on the

Minister of Finance Decree No. 1251 / KMK.013 / 1988 is a business entity

that carries out financing activities in the form of purchases and / or transfers

and management of short-term receivables or bills of a company from domestic

or foreign trade transactions.

17

CHAPTER III

METHODOLOGY

3.1 Research Framework

PT Yamazaki Indonesia is one of the manufacturing companies that

entirely do credit sales activities. When a company conducts sales activities on

credit, there is a receivable for the company. The company certainly tries to

manage its receivables properly so that the company's cash flow statement is

also in good condition. By analyzing the factors that affect receivables, then it

can also analyze financial ratios obtained from the balance sheet, and Profit and

Loss statement. After that, the analysis will be carried out per component to see

the proportion of the amount of receivables contained in the balance sheet

report and then see how much influence the amount of receivables the company

has on the effectiveness of collection. The cash conversion cycle analysis is

used to see the effect of controlling accounts receivable on the effectiveness of

collection and to minimize a working capital which will then be used in

financing the company's operating activities, so that a good turnover between

inventory, cash and receivables will be seen in operating company.

PT Yamazaki Indonesia is a manufacturing company that also accepts

payment transactions in foreign currency. This is evidenced by the presence of

several consumers who make receivable payment transactions using foreign

currency units. In addition, the company also purchases raw materials from

18

foreign suppliers. This will be affected by fluctuating currency exchange rates

and impact on receivables which fluctuate as well.

The results of the analysis carried out in this study are expected to help the

company run its debt control system properly, because it will be related to sales

patterns that also affect the company's liquidity. A clearer understanding can be

seen in Figure 3, in the next page.

19

Figure 3 Research Framework

20

3.2 Location and Time of Research

This research was conducted at PT Yamazaki Indonesia which is located in

Kawasan Industri Greenland Batavia Blok BA No.1, Ds Cikarang Pusat,

Sukamahi, CikarangPusat, Bekasi, Jawa Barat 17530. The choice of research

location was done intentionally or purposively. This research was conducted in

September–December 2018.

3.3 Data Collection

This research collects data directly from the company both primary and

secondary data. Primary data is obtained from interviews with the company,

especially financial managers, regarding the control system of receivables and

the decision-making process related to the receivable policy. Secondary data

was obtained from company in the form of financial statements for the 2015 –

2017 period, sales data, Aging Schedule data, Listing Invoices Data, Balance

Sheet Data, Profit and Loss data, etc. for the period 2017 – 2018, literature

studies, and research reports.

3.4 Processing and Data Analysis

This study obtained data directly from the company and then processed

and analyzed by statistical methods, namely analysis per component, trend

analysis, cash conversion cycle analysis, and financial ratio analysis. Analysis

per component is used to see the proportion of the amount of receivables

contained in the balance sheet report and then see how much influence the

21

amount of receivables held by the company on the effectiveness of collection.

Trend analysis is used to analyze the comparison between the amount of

receivables and sales made by the company. Cash conversion cycle analysis is

used to see the effect of controlling receivables on the effectiveness of

collection and to minimize working capital owned by a company by

accelerating the collection of cash from sales, increasing inventory turnover,

and reducing spending with cash. Financial ratio analysis is used to see the

company's financial performance in each period. In addition, computer

software that will be used to process and analyze data is Microsoft Excel 2007.

3.4.1 Analysis per Component

According to Jumingan (2008), the analysis per component is percentage

of each asset element to total assets, each element of liability to the total

liability, and each element of profit and loss on the amount of net sales. Such

reports called the common size statement. General size statements are also

called quantities per component because for each total replaced with the

number 100 and each nothing changes to a percent of the total number.

Analysis per component is actually also a ratio analysis (comparison) or some

sorts of proportion, because of the amount of rupiah from each element of the

financial statements are expressed in percent of the total. The method changes

the amount of rupiah from each report element to percent of the total, done as

follows:

22

1. State the total assets, total liabilities, and total net sales with100%.

2. Calculate the ratio of each element of the financial statement with the total

is by dividing the rupiah amount of each element the financial statements in

total.

3. Percentage analysis per component can be formulated as follows:

Information:

Ryi = The percentage value for the purpose of comparing

Pyi = Post (Amount) of y in the financial statements year-i

Pyo = Post (Amount) as a basic comparison

3.4.2 Trend Analysis

Trend analysis is an analysis that compares reports from one period to

another with a single basic index approach. In trend analysis it takes one year

which can be used as the base year. Then this base year is used as a basis for

consideration to be made in the form of a percentage. Base year is usually

determined from the data or financial statements of the earliest year in the

series of years of financial statements to be analyzed. Each post of the financial

report which is used as the base year is indexed 100. Then the posts of the

period analyzed are related to the same post, namely the base year. Trend

analysis can be formulated as follows:

Pyo

100

%

Pyo

Ryi =

= Pyi

x

100%

Pyo

Pyi

=

Pyi

x

100

%

Pyo

X 100%

Pyo

23

Information:

Rxi = The percentage value for the year-i

Pxi = Post (Amount) of x in the financial statements that will be analyzed

Pxo = Post (Amount) as a year base

3.4.3 Cash Conversion Cycle Analysis

According to Keown (2005), the cash conversion cycle analysis is an analytical

method that uses an approach that is the purpose of the company working

capital with the condition that working capital must be sufficient to legalize the

company's operations. The process of working capital is done by speeding up

cash from sales, increasing preparation turnover, and reducing spending on

cash. This cash cycle can be calculated as follows:

Cash Conversion Cycle =DSO + DSI – DPO

Information:

A. Days of Sales Outstanding (DSO)

DSO can also be considered as the average age of the company's receivables or

the average billing period. Days of Sales Outstanding (DSO) can be calculated

as follows:

Days of Sales Outstanding =

Days in Period

Pxo

=

Pyi

x

100

%

Pyo

Rxi =

= Pyi

x

100%

Pyo

Pxi

]]

Pyi

x

100

%

Pyo

X 100%

Pyo

24

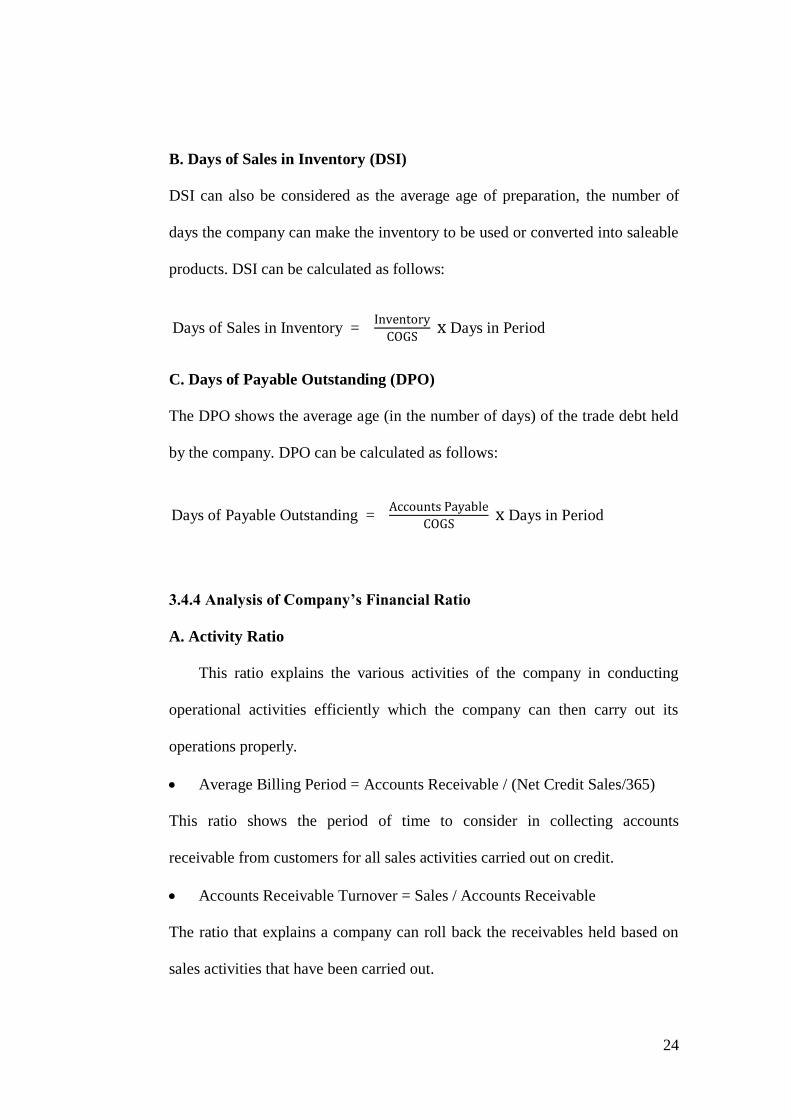

B. Days of Sales in Inventory (DSI)

DSI can also be considered as the average age of preparation, the number of

days the company can make the inventory to be used or converted into saleable

products. DSI can be calculated as follows:

C. Days of Payable Outstanding (DPO)

The DPO shows the average age (in the number of days) of the trade debt held

by the company. DPO can be calculated as follows:

3.4.4 Analysis of Company’s Financial Ratio

A. Activity Ratio

This ratio explains the various activities of the company in conducting

operational activities efficiently which the company can then carry out its

operations properly.

Average Billing Period = Accounts Receivable / (Net Credit Sales/365)

This ratio shows the period of time to consider in collecting accounts

receivable from customers for all sales activities carried out on credit.

Accounts Receivable Turnover = Sales / Accounts Receivable

The ratio that explains a company can roll back the receivables held based on

sales activities that have been carried out.

Days of Sales in Inventory =

Days in Period

Days of Payable Outstanding =

Days in Period

25

CHAPTER IV

RESULTS AND DISCUSSION

4.1 Account Receivable Management in PT Yamazaki Indonesia

The accounts receivable management system owned by PT Yamazaki

Indonesia starts from input, process, to output. At PT Yamazaki Indonesia

input from the accounts receivable management system, which is characterized

by the sale of products, are mostly carried out on credit. Credit sales conducted

by PT Yamazaki Indonesia aim to sell more to customers which will have an

impact on the company's inflow, especially the collection of receivables. When

a company makes a sale on credit, it will allow an increase in the number of

customers to buy the company's products. In terms of the company, credit sales

have a high level of risk, that is, when customers buy products on credit, the

company must compensate with a good billing process in order to reduce the

risk of loss of accounts due to customers paying off their debts.

Then the debt management process at PT Yamazaki Indonesia is marked

by the activity of preparing sales documents (such as PO letters from

customers, DRq letters from purchasing divisions, tax invoices from financial

& accounting division), issuing invoices, to carrying out receivables collection

activities to customers. The collection of receivables made will greatly affect

the amount of the company's receivables. When the company bills well, the

collection of receivables will also be good. But in its implementation, PT

Yamazaki Indonesia sometimes often faces a number of obstacles that come

26

from the customer, for example customer negligence in paying the debt or

delay in paying the debt according to the time due. In addition, there are also

several constraints that originate from the company, such as personnel who are

very limited in terms of the collection of accounts receivable, allowing double

jobs or multiple jobs to manage receivables, and factors that originate from the

internal company.

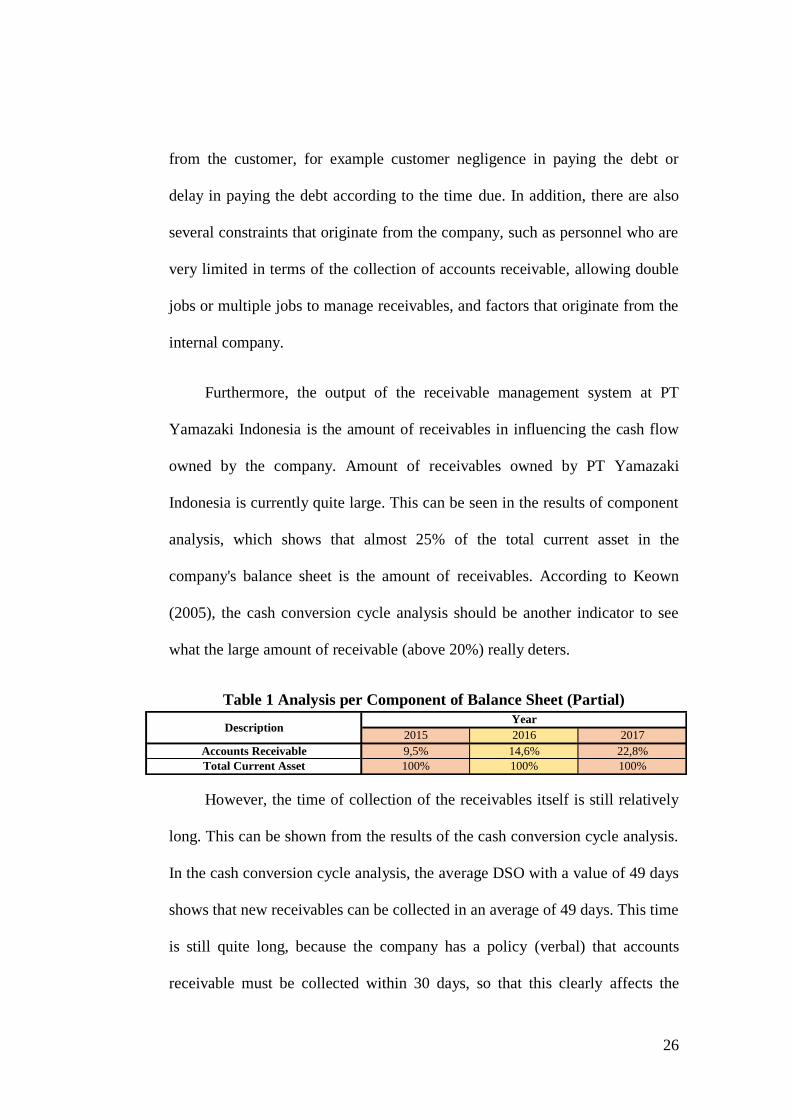

Furthermore, the output of the receivable management system at PT

Yamazaki Indonesia is the amount of receivables in influencing the cash flow

owned by the company. Amount of receivables owned by PT Yamazaki

Indonesia is currently quite large. This can be seen in the results of component

analysis, which shows that almost 25% of the total current asset in the

company's balance sheet is the amount of receivables. According to Keown

(2005), the cash conversion cycle analysis should be another indicator to see

what the large amount of receivable (above 20%) really deters.

Table 1 Analysis per Component of Balance Sheet (Partial)

However, the time of collection of the receivables itself is still relatively

long. This can be shown from the results of the cash conversion cycle analysis.

In the cash conversion cycle analysis, the average DSO with a value of 49 days

shows that new receivables can be collected in an average of 49 days. This time

is still quite long, because the company has a policy (verbal) that accounts

receivable must be collected within 30 days, so that this clearly affects the

2015 2016 2017

Accounts Receivable 9,5% 14,6% 22,8%

Total Current Asset 100% 100% 100%

YearDescription

27

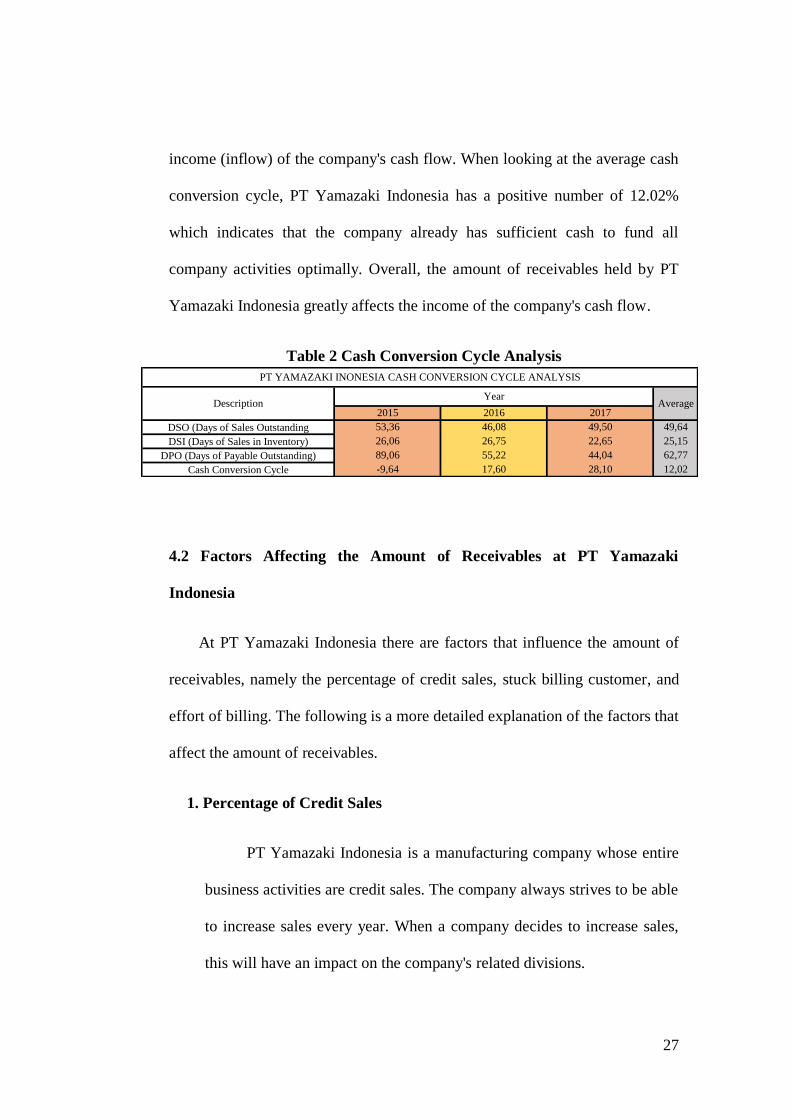

income (inflow) of the company's cash flow. When looking at the average cash

conversion cycle, PT Yamazaki Indonesia has a positive number of 12.02%

which indicates that the company already has sufficient cash to fund all

company activities optimally. Overall, the amount of receivables held by PT

Yamazaki Indonesia greatly affects the income of the company's cash flow.

Table 2 Cash Conversion Cycle Analysis

4.2 Factors Affecting the Amount of Receivables at PT Yamazaki

Indonesia

At PT Yamazaki Indonesia there are factors that influence the amount of

receivables, namely the percentage of credit sales, stuck billing customer, and

effort of billing. The following is a more detailed explanation of the factors that

affect the amount of receivables.

1. Percentage of Credit Sales

PT Yamazaki Indonesia is a manufacturing company whose entire

business activities are credit sales. The company always strives to be able

to increase sales every year. When a company decides to increase sales,

this will have an impact on the company's related divisions.

2015 2016 2017

DSO (Days of Sales Outstanding 53,36 46,08 49,50 49,64

DSI (Days of Sales in Inventory) 26,06 26,75 22,65 25,15

DPO (Days of Payable Outstanding) 89,06 55,22 44,04 62,77

Cash Conversion Cycle -9,64 17,60 28,10 12,02

AverageDescription

PT YAMAZAKI INONESIA CASH CONVERSION CYCLE ANALYSIS

Year

28

The most related division is the Sales, Marketing, Distribution and

Return division (SMDR Division), because the division greatly influences

the size of sales activities carried out to consumers. The SMDR division

strives to give customers confidence in being able to buy more company

products, or strive for new consumer searches to increase sales.

Furthermore, the purchasing division and production division also require

adjustments in terms of increasing the scale of production to meet the

decision to increase sales.

However, the four divisions mentioned above need to consider

decisions from the financial & accounting division due to the high level

of risk from sales activities carried out on credit to the company's inflow.

When the company decides to increase sales, the Sales estimator division

will estimate how much the receivables will be obtained by the company

considering the billing process carried out needs to be increased as well.

When the company has increased sales on credit, the financial &

accounting division needs to work optimally in collecting accounts

receivable, considering that financial & accounting division personnel are

very few (only 5 people) and very difficult to collect receivables from

customers (180 companies).

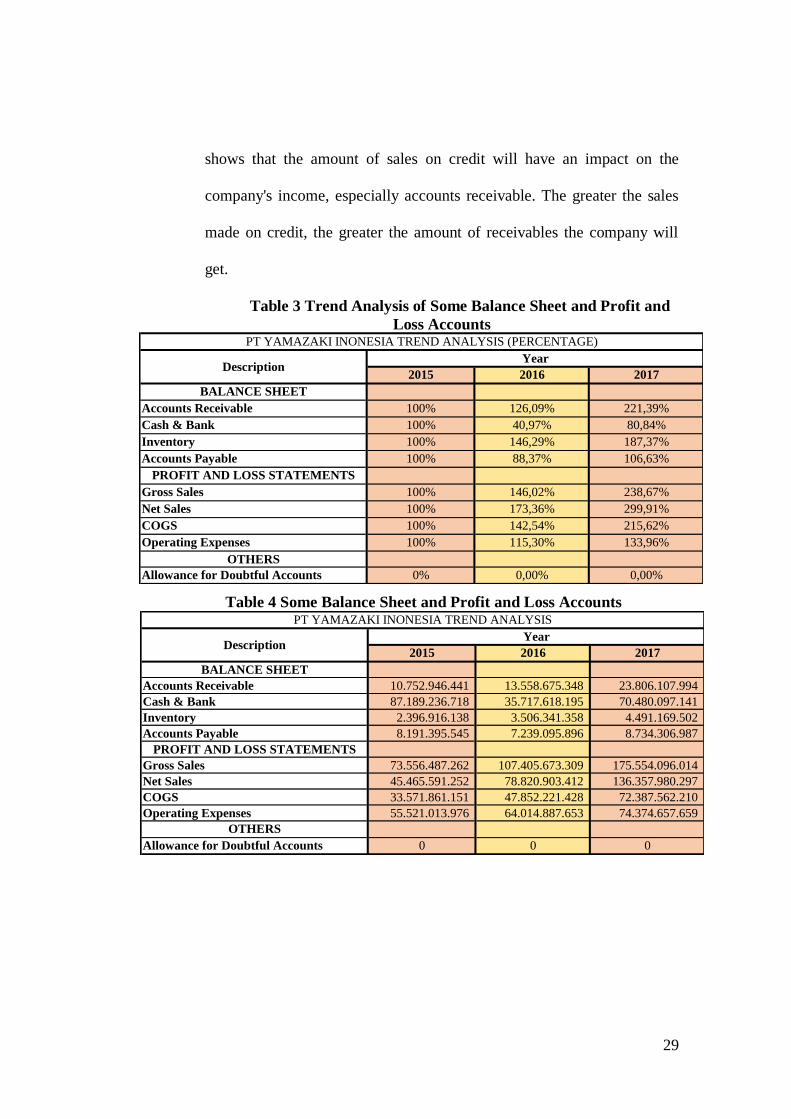

Every year the company has sales figures that tend to increase. PT

Yamazaki Indonesia has a percentage of sales on credit of 100% of total

sales. This is clearly based on a joint decision of the company's leadership

in deciding to increase sales. This can be seen in the following data which

29

shows that the amount of sales on credit will have an impact on the

company's income, especially accounts receivable. The greater the sales

made on credit, the greater the amount of receivables the company will

get.

Table 3 Trend Analysis of Some Balance Sheet and Profit and

Loss Accounts

Table 4 Some Balance Sheet and Profit and Loss Accounts

2015 2016 2017

BALANCE SHEET

Accounts Receivable 100% 126,09% 221,39%

Cash & Bank 100% 40,97% 80,84%

Inventory 100% 146,29% 187,37%

Accounts Payable 100% 88,37% 106,63%

PROFIT AND LOSS STATEMENTS

Gross Sales 100% 146,02% 238,67%

Net Sales 100% 173,36% 299,91%

COGS 100% 142,54% 215,62%

Operating Expenses 100% 115,30% 133,96%

OTHERS

Allowance for Doubtful Accounts 0% 0,00% 0,00%

DescriptionYear

PT YAMAZAKI INONESIA TREND ANALYSIS (PERCENTAGE)

2015 2016 2017

BALANCE SHEET

Accounts Receivable 10.752.946.441 13.558.675.348 23.806.107.994

Cash & Bank 87.189.236.718 35.717.618.195 70.480.097.141

Inventory 2.396.916.138 3.506.341.358 4.491.169.502

Accounts Payable 8.191.395.545 7.239.095.896 8.734.306.987

PROFIT AND LOSS STATEMENTS

Gross Sales 73.556.487.262 107.405.673.309 175.554.096.014

Net Sales 45.465.591.252 78.820.903.412 136.357.980.297

COGS 33.571.861.151 47.852.221.428 72.387.562.210

Operating Expenses 55.521.013.976 64.014.887.653 74.374.657.659

OTHERS

Allowance for Doubtful Accounts 0 0 0

DescriptionYear

PT YAMAZAKI INONESIA TREND ANALYSIS

30

2. Stuck Billing Customer

On sales procedures (verbal) owned by PT Yamazaki Indonesia, there are

several requirements that must be met by customers, namely customers have

good reputation, credibility, and integrity, customers are individuals or business

entities that are legal or legal entities and customers have the financial ability

that is relied on to pay for all sales transactions with PT Yamazaki Indonesia

Initially PT Yamazaki Indonesia is very concerned about the

requirements that must be met by customers before the sale transaction is

carried out, such as credit analysis (verbal). However, over time the company

has been quite loose on the accounts receivable that have not been paid by the

customer to the company, so that in the implementation there are customers

who are still late in paying off their debts. For example, in customer companies

that have debts of more than 500 days, they are still permitted to make new

orders in the following month. This obviously will have an impact on not only

the collection of the company's receivables but also company’s cash inflow.

JULY 2018

Table 5.1 PT Supra Boga Lestari’s July Aging Schedule

Table 5.2 PT Supra Boga Lestari’s July Aging Schedule (New Orders)

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT SUPRA BOGA LESTARI 5/3/2018 5/17/2018 0,00 0,00 582.744,80 0,00 582.744,80 14 75

PT SUPRA BOGA LESTARI 5/3/2018 5/17/2018 0,00 0,00 248.246,90 0,00 248.246,90 14 75

PT SUPRA BOGA LESTARI 5/3/2018 5/17/2018 0,00 0,00 582.744,80 0,00 582.744,80 14 75

PT SUPRA BOGA LESTARI 5/3/2018 5/17/2018 0,00 0,00 280.500,00 0,00 280.500,00 14 75

PT SUPRA BOGA LESTARI 5/3/2018 5/17/2018 0,00 0,00 248.246,90 0,00 248.246,90 14 75

31-Jul-18

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT SUPRA BOGA LESTARI 7/24/2018 8/7/2018 0,00 0,00 0,00 0,00 272.248,90 14 -7

PT SUPRA BOGA LESTARI 7/24/2018 8/7/2018 0,00 0,00 0,00 0,00 203.624,30 14 -7

PT SUPRA BOGA LESTARI 7/24/2018 8/7/2018 0,00 0,00 0,00 0,00 192.748,60 14 -7

PT SUPRA BOGA LESTARI 7/24/2018 8/7/2018 0,00 0,00 0,00 0,00 292.495,50 14 -7

PT SUPRA BOGA LESTARI 7/24/2018 8/7/2018 0,00 0,00 0,00 0,00 840.755,30 14 -7

31-Jul-18

31

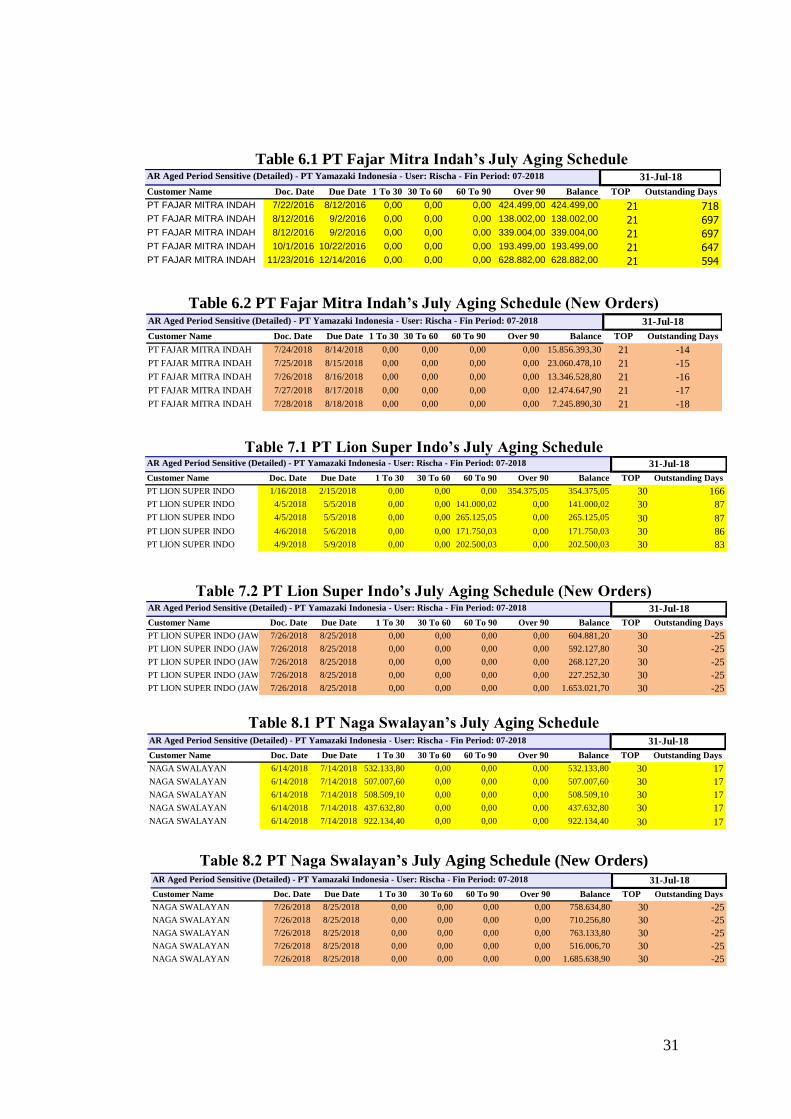

Table 6.1 PT Fajar Mitra Indah’s July Aging Schedule

Table 6.2 PT Fajar Mitra Indah’s July Aging Schedule (New Orders)

Table 7.1 PT Lion Super Indo’s July Aging Schedule

Table 7.2 PT Lion Super Indo’s July Aging Schedule (New Orders)

Table 8.1 PT Naga Swalayan’s July Aging Schedule

Table 8.2 PT Naga Swalayan’s July Aging Schedule (New Orders)

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT FAJAR MITRA INDAH 7/22/2016 8/12/2016 0,00 0,00 0,00 424.499,00 424.499,00 21 718PT FAJAR MITRA INDAH 8/12/2016 9/2/2016 0,00 0,00 0,00 138.002,00 138.002,00 21 697PT FAJAR MITRA INDAH 8/12/2016 9/2/2016 0,00 0,00 0,00 339.004,00 339.004,00 21 697PT FAJAR MITRA INDAH 10/1/2016 10/22/2016 0,00 0,00 0,00 193.499,00 193.499,00 21 647PT FAJAR MITRA INDAH 11/23/2016 12/14/2016 0,00 0,00 0,00 628.882,00 628.882,00 21 594

31-Jul-18

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT FAJAR MITRA INDAH 7/24/2018 8/14/2018 0,00 0,00 0,00 0,00 15.856.393,30 21 -14

PT FAJAR MITRA INDAH 7/25/2018 8/15/2018 0,00 0,00 0,00 0,00 23.060.478,10 21 -15

PT FAJAR MITRA INDAH 7/26/2018 8/16/2018 0,00 0,00 0,00 0,00 13.346.528,80 21 -16

PT FAJAR MITRA INDAH 7/27/2018 8/17/2018 0,00 0,00 0,00 0,00 12.474.647,90 21 -17

PT FAJAR MITRA INDAH 7/28/2018 8/18/2018 0,00 0,00 0,00 0,00 7.245.890,30 21 -18

31-Jul-18

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT LION SUPER INDO 1/16/2018 2/15/2018 0,00 0,00 0,00 354.375,05 354.375,05 30 166

PT LION SUPER INDO 4/5/2018 5/5/2018 0,00 0,00 141.000,02 0,00 141.000,02 30 87

PT LION SUPER INDO 4/5/2018 5/5/2018 0,00 0,00 265.125,05 0,00 265.125,05 30 87

PT LION SUPER INDO 4/6/2018 5/6/2018 0,00 0,00 171.750,03 0,00 171.750,03 30 86

PT LION SUPER INDO 4/9/2018 5/9/2018 0,00 0,00 202.500,03 0,00 202.500,03 30 83

31-Jul-18

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT LION SUPER INDO (JAWA BARAT)7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 604.881,20 30 -25

PT LION SUPER INDO (JAWA BARAT)7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 592.127,80 30 -25

PT LION SUPER INDO (JAWA BARAT)7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 268.127,20 30 -25

PT LION SUPER INDO (JAWA BARAT)7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 227.252,30 30 -25

PT LION SUPER INDO (JAWA BARAT)7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 1.653.021,70 30 -25

31-Jul-18

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

NAGA SWALAYAN 6/14/2018 7/14/2018 532.133,80 0,00 0,00 0,00 532.133,80 30 17

NAGA SWALAYAN 6/14/2018 7/14/2018 507.007,60 0,00 0,00 0,00 507.007,60 30 17

NAGA SWALAYAN 6/14/2018 7/14/2018 508.509,10 0,00 0,00 0,00 508.509,10 30 17

NAGA SWALAYAN 6/14/2018 7/14/2018 437.632,80 0,00 0,00 0,00 437.632,80 30 17

NAGA SWALAYAN 6/14/2018 7/14/2018 922.134,40 0,00 0,00 0,00 922.134,40 30 17

31-Jul-18

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 07-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

NAGA SWALAYAN 7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 758.634,80 30 -25

NAGA SWALAYAN 7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 710.256,80 30 -25

NAGA SWALAYAN 7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 763.133,80 30 -25

NAGA SWALAYAN 7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 516.006,70 30 -25

NAGA SWALAYAN 7/26/2018 8/25/2018 0,00 0,00 0,00 0,00 1.685.638,90 30 -25

31-Jul-18

32

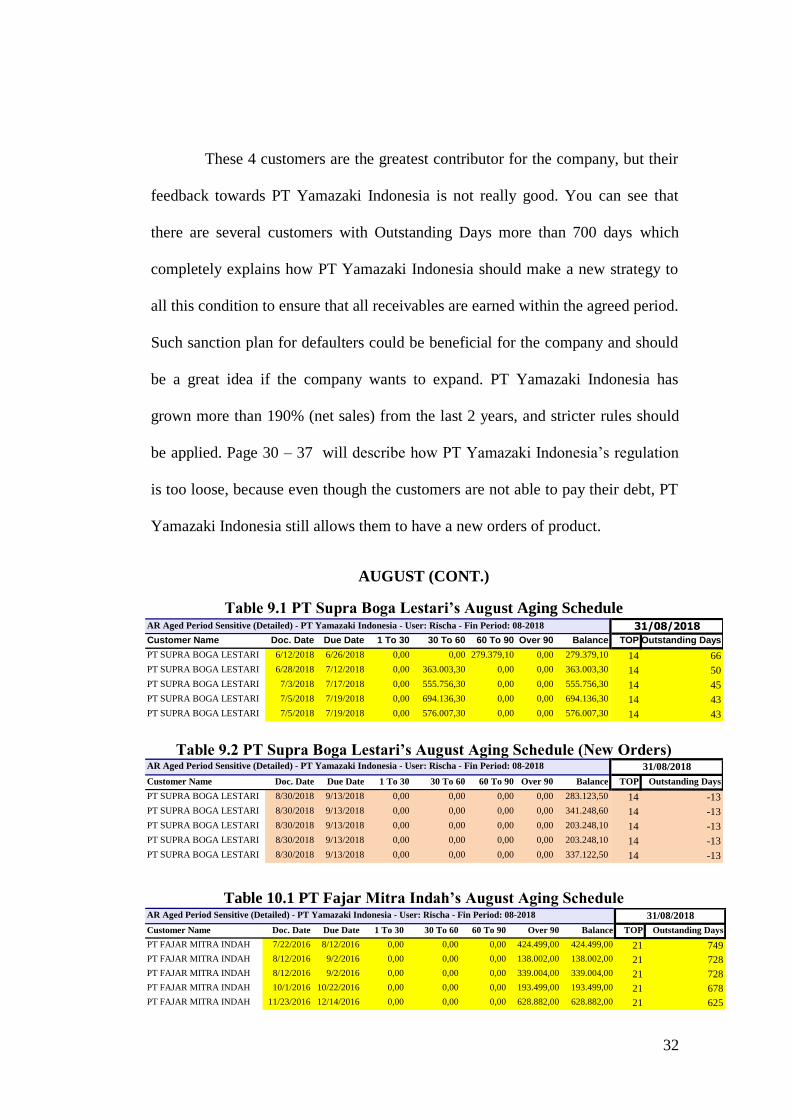

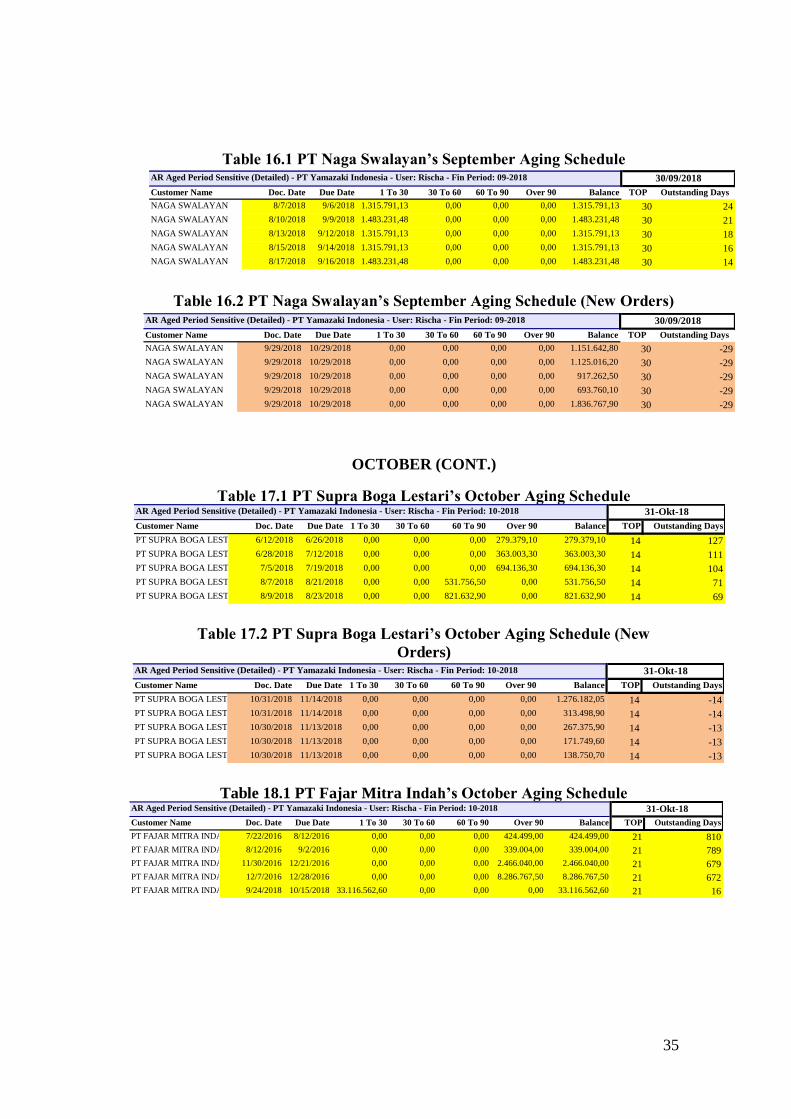

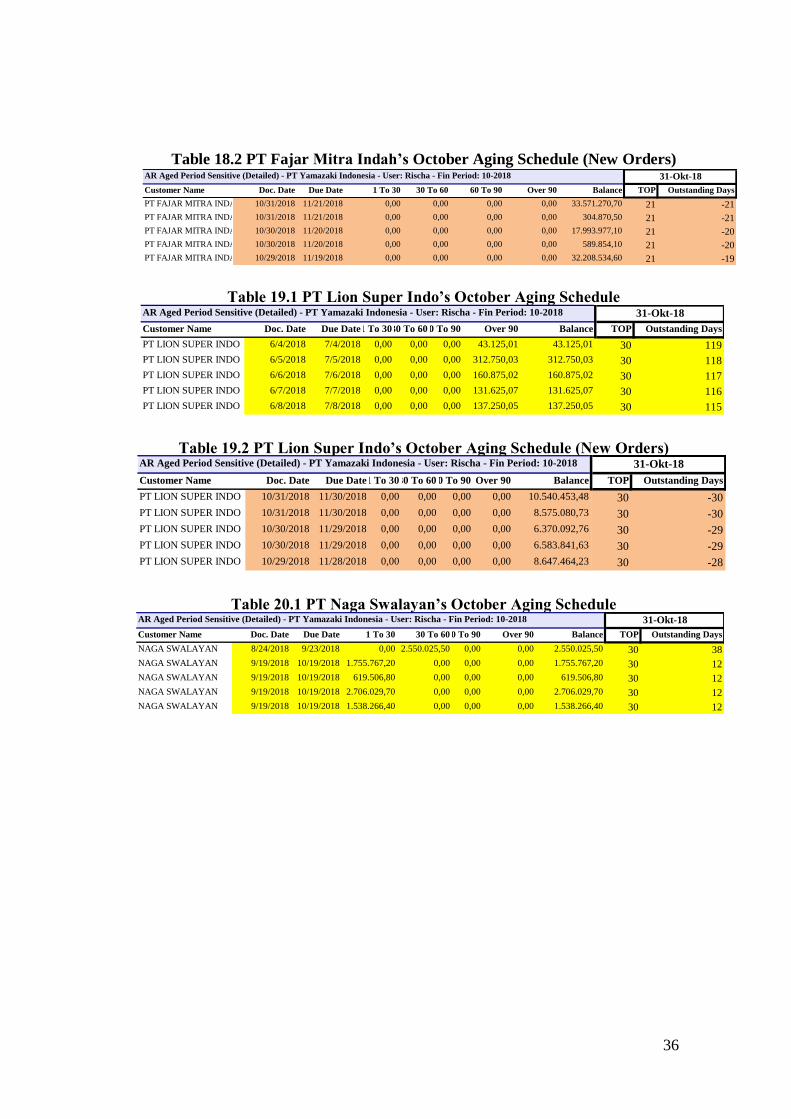

These 4 customers are the greatest contributor for the company, but their

feedback towards PT Yamazaki Indonesia is not really good. You can see that

there are several customers with Outstanding Days more than 700 days which

completely explains how PT Yamazaki Indonesia should make a new strategy to

all this condition to ensure that all receivables are earned within the agreed period.

Such sanction plan for defaulters could be beneficial for the company and should

be a great idea if the company wants to expand. PT Yamazaki Indonesia has

grown more than 190% (net sales) from the last 2 years, and stricter rules should

be applied. Page 30 – 37 will describe how PT Yamazaki Indonesia’s regulation

is too loose, because even though the customers are not able to pay their debt, PT

Yamazaki Indonesia still allows them to have a new orders of product.

AUGUST (CONT.)

Table 9.1 PT Supra Boga Lestari’s August Aging Schedule

Table 9.2 PT Supra Boga Lestari’s August Aging Schedule (New Orders)

`

Table 10.1 PT Fajar Mitra Indah’s August Aging Schedule

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT SUPRA BOGA LESTARI 6/12/2018 6/26/2018 0,00 0,00 279.379,10 0,00 279.379,10 14 66

PT SUPRA BOGA LESTARI 6/28/2018 7/12/2018 0,00 363.003,30 0,00 0,00 363.003,30 14 50

PT SUPRA BOGA LESTARI 7/3/2018 7/17/2018 0,00 555.756,30 0,00 0,00 555.756,30 14 45

PT SUPRA BOGA LESTARI 7/5/2018 7/19/2018 0,00 694.136,30 0,00 0,00 694.136,30 14 43

PT SUPRA BOGA LESTARI 7/5/2018 7/19/2018 0,00 576.007,30 0,00 0,00 576.007,30 14 43

31/08/2018

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT SUPRA BOGA LESTARI 8/30/2018 9/13/2018 0,00 0,00 0,00 0,00 283.123,50 14 -13

PT SUPRA BOGA LESTARI 8/30/2018 9/13/2018 0,00 0,00 0,00 0,00 341.248,60 14 -13

PT SUPRA BOGA LESTARI 8/30/2018 9/13/2018 0,00 0,00 0,00 0,00 203.248,10 14 -13

PT SUPRA BOGA LESTARI 8/30/2018 9/13/2018 0,00 0,00 0,00 0,00 203.248,10 14 -13

PT SUPRA BOGA LESTARI 8/30/2018 9/13/2018 0,00 0,00 0,00 0,00 337.122,50 14 -13

31/08/2018

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT FAJAR MITRA INDAH 7/22/2016 8/12/2016 0,00 0,00 0,00 424.499,00 424.499,00 21 749

PT FAJAR MITRA INDAH 8/12/2016 9/2/2016 0,00 0,00 0,00 138.002,00 138.002,00 21 728

PT FAJAR MITRA INDAH 8/12/2016 9/2/2016 0,00 0,00 0,00 339.004,00 339.004,00 21 728

PT FAJAR MITRA INDAH 10/1/2016 10/22/2016 0,00 0,00 0,00 193.499,00 193.499,00 21 678

PT FAJAR MITRA INDAH 11/23/2016 12/14/2016 0,00 0,00 0,00 628.882,00 628.882,00 21 625

31/08/2018

33

Table 10.2 PT Fajar Mitra Indah’s August Aging Schedule (New Orders)

Table 11.1 PT Lion Super Indo August Aging Schedule

Table 11.2 PT Lion Super Indo’s August Aging Schedule (New Orders)

Table 12.1 PT Naga Swalayan’s August Aging Schedule

Table 12.2 PT Naga Swalayan’s August Aging Schedule (New Orders)

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT FAJAR MITRA INDAH 8/31/2018 9/21/2018 0,00 0,00 0,00 0,00 18.500.340,10 21 -21

PT FAJAR MITRA INDAH 8/31/2018 9/21/2018 0,00 0,00 0,00 0,00 691.848,30 21 -21

PT FAJAR MITRA INDAH 8/30/2018 9/20/2018 0,00 0,00 0,00 0,00 16.102.702,00 21 -20

PT FAJAR MITRA INDAH 8/29/2018 9/19/2018 0,00 0,00 0,00 0,00 27.253.982,80 21 -19

PT FAJAR MITRA INDAH 8/28/2018 9/18/2018 0,00 0,00 0,00 0,00 17.799.171,50 21 -18

31/08/2018

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT LION SUPER INDO 1/16/2018 2/15/2018 0,00 0,00 0,00 354.375,05 354.375,05 30 197

PT LION SUPER INDO 4/26/2018 5/26/2018 0,00 0,00 0,00 245.250,05 245.250,05 30 97

PT LION SUPER INDO 4/28/2018 5/28/2018 0,00 0,00 0,00 231.750,02 231.750,02 30 95

PT LION SUPER INDO 4/28/2018 5/28/2018 0,00 0,00 0,00 423.000,07 423.000,07 30 95

PT LION SUPER INDO 4/28/2018 5/28/2018 0,00 0,00 0,00 399.000,05 399.000,05 30 95

31/08/2018

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

PT LION SUPER INDO (JAWA BARAT)8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 686.628,80 30 -30

PT LION SUPER INDO (JAWA BARAT)8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 529.125,30 30 -30

PT LION SUPER INDO (JAWA BARAT)8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 371.625,10 30 -30

PT LION SUPER INDO (JAWA BARAT)8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 434.253,60 30 -30

PT LION SUPER INDO (JAWA BARAT)8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 1.710.016,00 30 -30

31/08/2018

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

NAGA SWALAYAN 7/2/2018 8/1/2018 777.007,00 0,00 0,00 0,00 777.007,00 30 30

NAGA SWALAYAN 7/2/2018 8/1/2018 878.257,60 0,00 0,00 0,00 878.257,60 30 30

NAGA SWALAYAN 7/4/2018 8/3/2018 1.031.631,70 0,00 0,00 0,00 1.031.631,70 30 28

NAGA SWALAYAN 7/4/2018 8/3/2018 1.755.015,90 0,00 0,00 0,00 1.755.015,90 30 28

NAGA SWALAYAN 7/6/2018 8/5/2018 2.054.268,70 0,00 0,00 0,00 2.054.268,70 30 26

31/08/2018

AR Aged Period Sensitive (Detailed) - PT Yamazaki Indonesia - User: Rischa - Fin Period: 08-2018

Customer Name Doc. Date Due Date 1 To 30 30 To 60 60 To 90 Over 90 Balance TOP Outstanding Days

NAGA SWALAYAN 8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 2.860.904,20 30 -30

NAGA SWALAYAN 8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 1.184.638,40 30 -30

NAGA SWALAYAN 8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 4.357.548,80 30 -30

NAGA SWALAYAN 8/31/2018 9/30/2018 0,00 0,00 0,00 0,00 2.782.532,50 30 -30

NAGA SWALAYAN 8/30/2018 9/29/2018 0,00 0,00 0,00 0,00 914.639,00 30 -29

31/08/2018

34

SEPTEMBER (CONT.)

Table 13.1 PT Supra Boga Lestari’s September Aging Schedule

Table 13.2 PT Supra Boga Lestari’s September Aging Schedule (New

Orders)

Table 14.1 PT Fajar Mitra Indah’s September Aging Schedule

Table 14.2 PT Fajar Mitra Indah’s September Aging Schedule (New