optimization in financial engineering yuriy zinchenko department of mathematics and statistics...

TRANSCRIPT

Optimization in Financial Engineering

Yuriy ZinchenkoDepartment of Mathematics and Statistics

University of Calgary

December 02, 2009

Why?

Objective has never been so clear:– maximize

Nobel prize winners:– L. Kantorovich

linear optimization

– H. Markowitz “Efficient Portfolio”, foundations of modern

Capital Asset Pricing theory

Talk layout

(Convex) optimization Portfolio optimization

– mean-variance model– risk measures– possible extensions

Securities pricing– non-parametric estimates– moment problem and duality– possible extensions

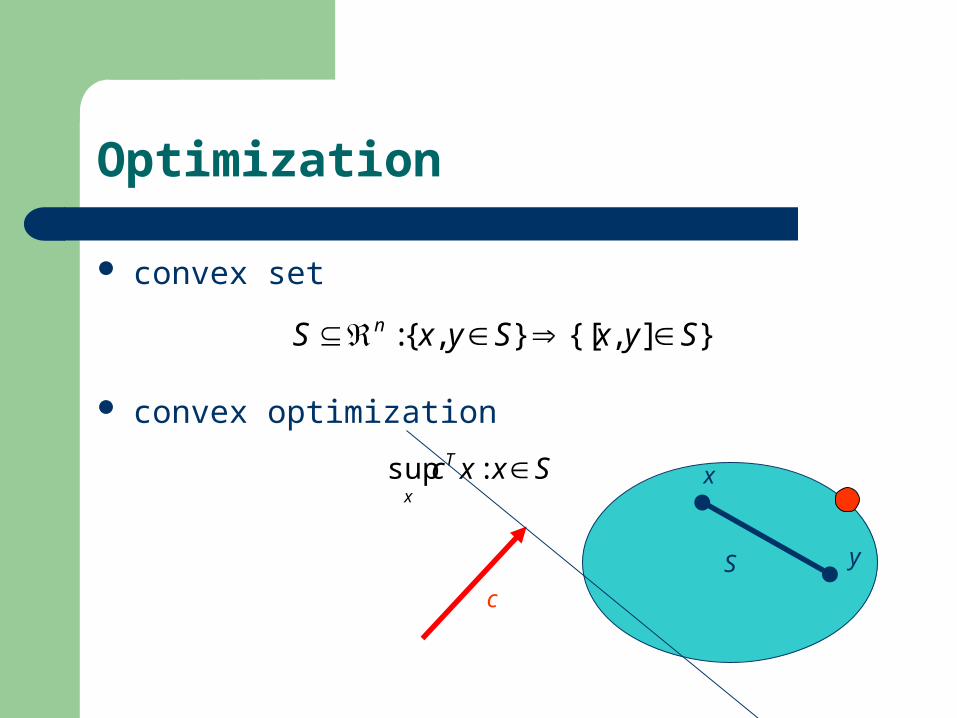

Optimization

Optimization

convex set

convex optimization

}],{[},{: SyxSyxS n

SxxcT

x:sup

S

x

y

c

Optimization

prototypical optimization problem –

Linear Programming (LP)

– any convex set admits “hyperplane representation”

),,( :max nmbAbAxxc mnmT

x

SAx ≤ b

x1

x2

c

Optimization

LP duality– re-write LP

as

and introduce

– optimal values satisfy weak duality:

– since

strong duality:

bAxxcT

x:max

(D) ,:max mT

xsbsAxxc

(P) ,:min mTT

zzczAzb

(D)alal(P) *vv xcszAxzsAxzbz TTTTT )(

(D)alal(P) *vv

Optimization

conic generalizations

where K is a closed convex cone, K* – its dual

– strong duality frequently holds and always

w.l.o.g. any convex optimization problem is conic

(D) ,:max *KsbsAxxcT

x

(P) ,:min KzczAzb TT

z

)(alal(P) * Dvv

(D) ,:max mT

xsbsAxxc

(P) ,:min mTT

zzczAzb

Optimization

conic optimization instances– LP:– Second Order Conic Programming (SOCP):

– Positive Semi-Definite Programming (SDP):

powerful solution methods and software exists– can solve problems with hundreds of thousands constraints

and variables; treat as black-box

mKK *(P) ,:min KzczAzb TT

z

||}||:),{( 1* xtxtKK m

}0:{closure* XSXKK k

Portfolio optimization

Mean-variance model

Markowitz model– minimize variance

– meet minimum return

– invest all funds

– no short-selling

where Q is asset covariance matrix,

r – vector of expected returns from each asset

0

,11

,

:min

min

x

x

rxr

Qxx

T

T

T

x

0

,11

,

,

:min

min

),(

x

x

rxr

tQxx

t

T

T

T

tx

SzzcT

x:sup

Markowitz model– explicit analytic solution given rmin

– interested in “efficient frontier” set of non-dominated portfolios

can be shown to be a “convex set”

Mean-variance model

Expectedreturn

A

Standard deviation

?B

Risk measures

mean-variance model minimizes variance– variance is indifferent to both up/down risks

coherent risk measures:– “portfolio” = “random loss” – given two portfolios X and Y, is coherent if

(X+Y) (X) + (Y) “diversification is good” (t X) = t (X) “no scaling effect” (X) (Y) if X Y a.s. “measure reflects risk” (X + ) = (X) - “risk-free assets reduce risk”

Risk measures

VaR (not coherent):– “maximum loss for a given confidence 1-”

CVaR (coherent):– “maximum expected loss for a given confidence 1-”– CVaR may be approximated using LP,

so may consider

}1)(:inf{ xXPx

)](VaR|[ XXE

0,11,:);(CVaRmin min xxrxrx TT

x

Probabilitydensity

Loss X

Possible extensions

risk vs. return models:

– portfolio granularity likely to have contributions from nearly all assets

– robustness to errors or variation in initial data Q and r are estimated

0

,11

,

:)""other (or min

min

x

x

rxr

riskQxx

T

T

T

x

Securities pricing

Non-parametric estimates

European call option:– “at a fixed future time may purchase a stock X at price k”– present option value (with 0 risk-free rate)

know moments of X; to bound option price consider

)],0[max( kXE

0)( ,1)(

... ,][ ,][

:)],0[max( min/max

0

2

xdxx

XVarXE

kXE

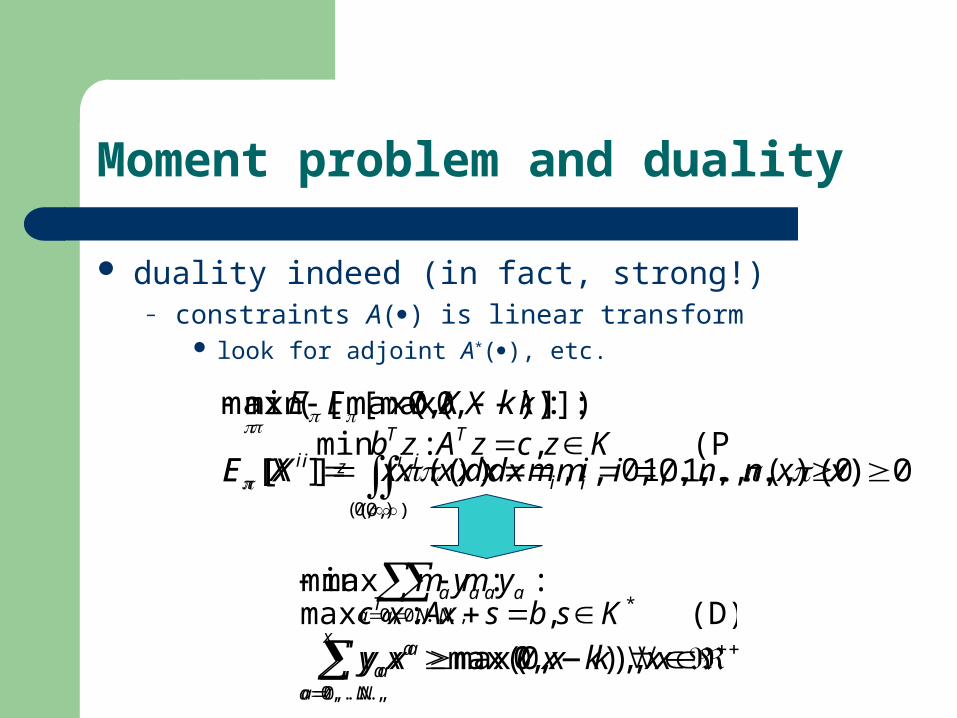

Moment problem and duality

option pricing relates to moment problem– given moments, find measure

intuitively, the more moments more definite answer semi-formally, substantiate by moment-generating function extreme example: X supported on {0,1}, let

– E[X]=1/2,– E[X2]=1/2,…

note objective and

constraints linear w.r.t. – duality?

0)( ,1)(

... ,][ ,][

:)],0[max( min/max

0

2

xdxx

XVarXE

kXE

Moment problem and duality

duality indeed (in fact, strong!)– constraints A() is linear transform

look for adjoint A*(), etc.

0)( ,,...,1,0 ,)(][

:)]),0[max((min

),0(

xnimdxxxXE

kXE

iii

Na

aa

Naaa

xkxxy

ym

,...,0

,...,0

),,0max(

:min

0)( ,,...,1,0 ,)(][

:)],0[max(max

),0(

xnimdxxxXE

kXE

iii

(D) ,:max *KsbsAxxcT

x

(P) ,:min KzczAzb TT

z

Na

aa

Naaa

xkxxy

ym

,...,0

,...,0

),,0max(

:max

Moment problem and duality

duality indeed (in fact, strong!)– constraints of the dual problem: p (x) ≥ 0, p – polynomial

– nonnegative polynomial SOS SDP representable

xxp ,0)(

Na

aa

Naaa

xkxxy

ym

,...,0

,...,0

),,0max(

:min

j i

ij

jj

ji

i txxacxtxxp 22222 )()()()( 0),,...,,,1(),...,,,1()( 2/22/2 QxxxQxxxxp NTN 0),,...,,,1(),...,,,1()( 2/22/2 TNTTN LLQxxxLLxxxxp

Moment problem and duality

due to well-understood dual, may solve efficiently

– and so, find bounds on the option price

0)( ,1)(

... ,][ ,][

:)],0[max( min/max

0

2

xdxx

XVarXE

kXE

Possible extensions

– exotic options– pricing correlated/dependent securities– moments of risk neutral measure given securities– sensitivity analysis on moment information

Few selected references

References

Portfolio optimization– (!) SAS Global Forum: Risk-based portfolio optimization using

SAS, 2009– J. Palmquist, S. Uryasev, P. Krokhmal: Portfolio optimization with

Conditional Value-at-Risk objective and constraints, 2001– S. Alexander, T. Coleman, Y. Li: Minimizing CVaR and VaR for a

portfolio of derivatives, 2005 Option pricing

– D. Bertsimas, I. Popescu: On the relation between option and stock prices : a convex optimization approach, 1999

– J. Lasserre, T. Prieto-Rumeau, M. Zervos: Pricing a Class of Exotic Options Via Moments and SDP Relaxations, 2006

Thank you