os biocombustíveiskpmg’s global automotive executive survey2017. for the 2017 survey we gathered...

TRANSCRIPT

Ricardo BACELLAR KPMG Brazil Head of Automotive

Osbiocombustíveise ofuturo da mobilidade

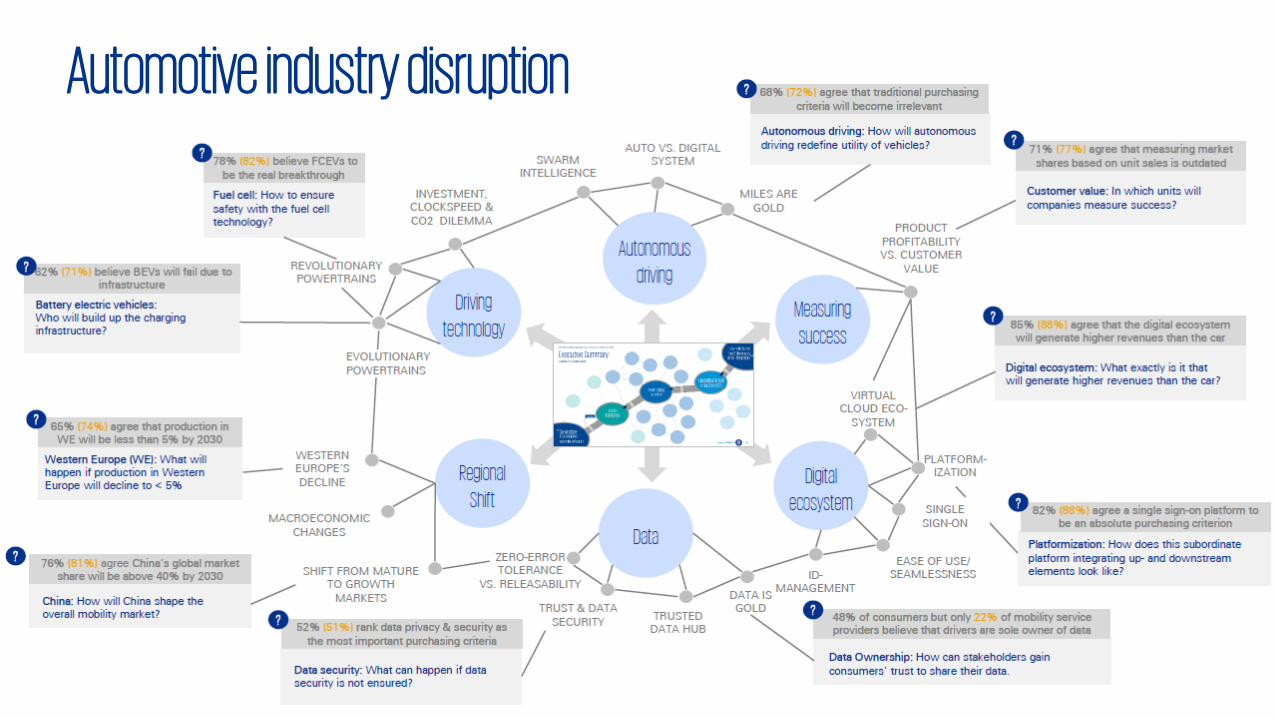

Automotive industry disruption

Mature Asia

China

North America

South America

Western Europe

Eastern Europe

India & ASEAN

Rest of World

Note: Map shows number of respondents from each country | Source: KPMG’s Global Automotive Executive Survey 2017

For the 2017 survey we gathered the opinions of 953 executives from 42 countries.

TOP 5 RESPONDENTS -EXECUTIVES

7

6139

887667820

15

20

4

25

7

20

83

70

24

13

10

20

127

1410

84

38

3

4

74

3110

31

7

293119

423

43

JapanSouthKorea

ChinaTaiwanIndiaVietnamPhilippinesThailand

Malaysia

Indonesia

Australia

SaudiArabiaIran

SouthAfrica

Sweden

Norway

Denmark

Germany

Austria

Switzerland

NetherlandsBelgium

Colombia

USA

Brazil

Argentina

Nigeria

UKCanada

Mexico

Ecuador

FranceItaly

Spain

Morocco

Czech RepublicPoland

HungaryRomania

FinlandTurkey

Russia

83 USA

88 China

61 Japan

66 India

70 Brazil

Global Automotive Survey

4© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

ExecutiveBRAZIL

27%

42%

15%

8%

2% Absolutely disagree

Partly agree

Partly disagree

Neutral

Absolutely agree

8%

28%

48%

12%

10%

2% Absolutely disagree

Partly agree

Partly disagree

Neutral

Absolutely agree

Exe

cuti

veo

pin

ion

30%

47%

11%

11%

1% Absolutely disagree

Partly agree

Partly disagree

Neutral

Absolutely agree

Co

nsu

mer

op

inio

n

Source NextGen Analytics Graphic: KPMG Automotive Institute 2017, LMC Automotive

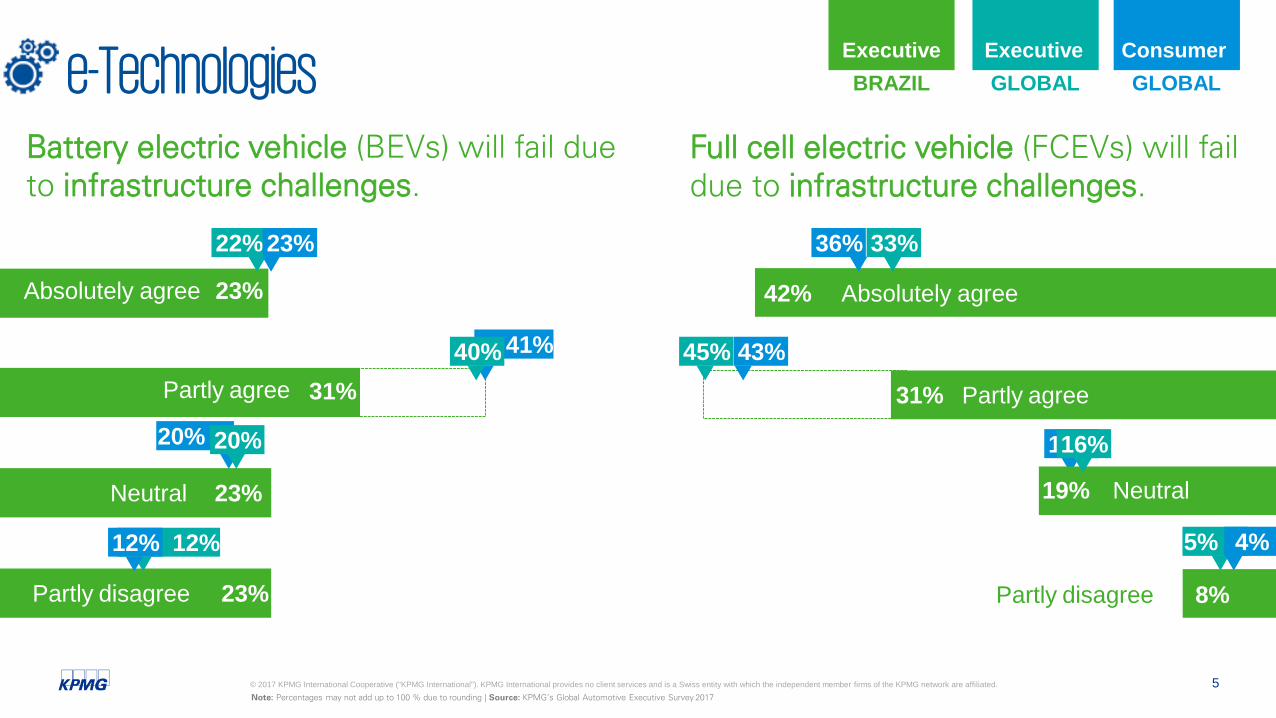

Fossil drivetrain technologiesInternal Combustion Engine (ICEs) will still be important for a long time.

5© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

41%

16%

ExecutiveBRAZIL

Absolutely agree

45%

33%22%

40%

16%

5%12%

36%23%

20%

12%

43%

4%

ConsumerGLOBALGLOBAL

Executive

20%

23%

31%

23%

23%

Partly agree

Partly disagree

Neutral

42%

31%

19%

8%

Partly agree

Partly disagree

Neutral

Absolutely agree

Battery electric vehicle (BEVs) will fail dueto infrastructure challenges.

Full cell electric vehicle (FCEVs) will faildue to infrastructure challenges.

e-Technologies

6© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

FHEV

ICE

FCEV PHEV

BEV EREV

0%

5%

10%

15%

20%

25%

40%

48%

Executives% of executives planning high investments

54%

What powertrain technology to invest in and when to make the shift

50% 52%

35%

30%

BEV (Battery EV), EREV (Battery EV withRange Extender)

FHEV (Full Hybrid EV)

PHEV (Plugin Hybrid EV)

ICE (Gasoline/ Diesel)

FCEV (Fuel Cell EV)

Con

sum

ers

(% o

f con

sum

ers

choo

sing

a ce

rtain

pow

ertra

inte

chno

logy

as

next

car

7© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

X

8© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

9© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

10© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

11© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

12© 2017 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.Note: Percentages may not add up to 100 % due to rounding | Source: KPMG’s Global Automotive Executive Survey 2017

Thank you

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timelyinformation, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future.No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG Inter- national. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG Internationalhave any such authority to obligate or bind any member firm. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

www.kpmg.com/automotive

www.kpmg.com/socialmedia

Ricardo BacellarHead of AutomotiveKPMG in [email protected](21) 98833-3000https://br.linkedin.com/in/bacellar