other manual highlights and reminders sheralin klinthong, assoc. dir., financial services / sfsr...

TRANSCRIPT

Other Manual Highlights and Reminders

Sheralin Klinthong, Assoc. Dir., Financial Services / SFSR

Evajoy Tito, Manager, Financial Services / SFSR

Chancellor’s Office

April 24, 2015

Learning Objectives• At the end of the session, the participants will be able

to:• Define the objective of the GAAP Manual• Know the location of the GAAP Manual• Recognize the contents of the GAAP Manual• Identify updates to the GAAP Manual

April 2015 Year-End GAAP Training 2

GAAP Manual - PurposeIn order to prepare financial statements in accordance with U.S. generally accepted accounting principles (GAAP), the CSU must convert legal-basis accounting to GAAP basis accounting.

The CSU GAAP Accounting and Reporting Manual is designed to guide the user through the conversion process.

In addition, it provides information on the preparation for various external audits (i.e. financial statements, IT, A-133 and SRB audits).

April 2015 Year-End GAAP Training 3

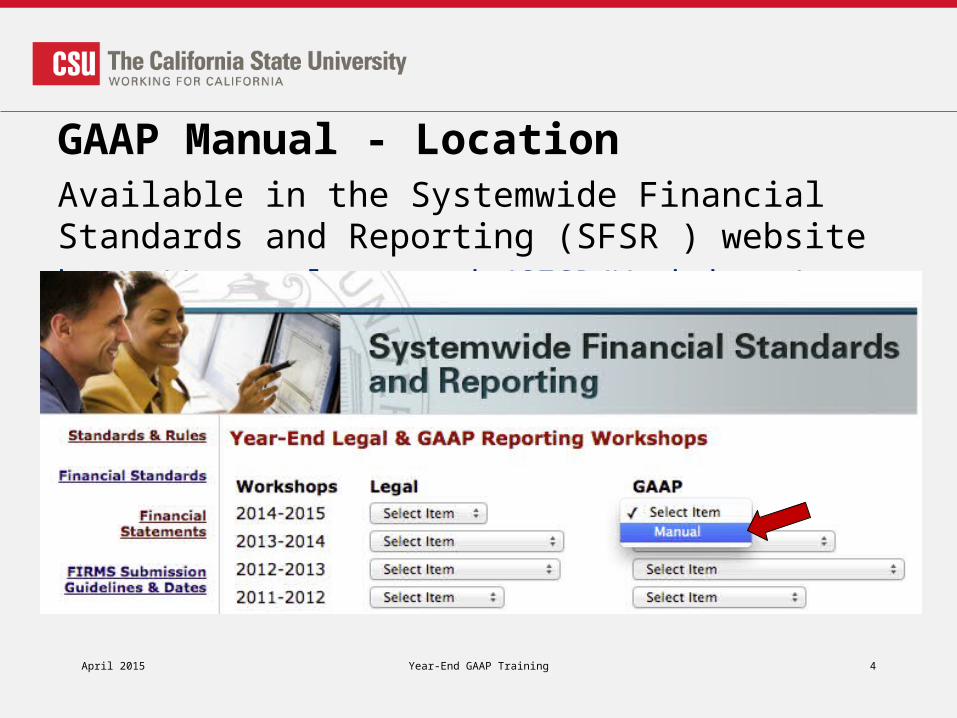

GAAP Manual - LocationAvailable in the Systemwide Financial Standards and Reporting (SFSR ) websitehttp://www.calstate.edu/SFSR/Workshops/index.shtml

April 2015 Year-End GAAP Training 4

GAAP Manual - Contents

April 2015 Year-End GAAP Training 5

Legal to GAAP Conversion

• 1 Overview• 2 Before You Begin• 3 Mapping Legal to GAAP• 4 GAAP Adjustments and

Reclassifications• 5 Passdown Schedules• 6 Statement of Cashflows• 7 YES Reporting Package

(TM1)• 10 GAAP Preparation

Checklist• 11 GAAP Financial

Reporting Checklists• 13 Capital Assets Guide

Preparation for Audits

• 9 Financial Statements Audit

• 15 Single Audit• 16 SRB Audit• 17 IT Audit

Others

• 8 Discretely Presented Component Units

• 12 National Collegiate Athletic Association Agreed-Upon Procedures Requirements

• 14 GASB Updates• 18 SCO GAAP

Submission

GAAP MANUAL UPDATES

April 2015 Year-End GAAP Training 6

Chapter 3

Mapping Legal Basis Accounts to GAAP Reporting Model

April 2015 Year-End GAAP Training 7

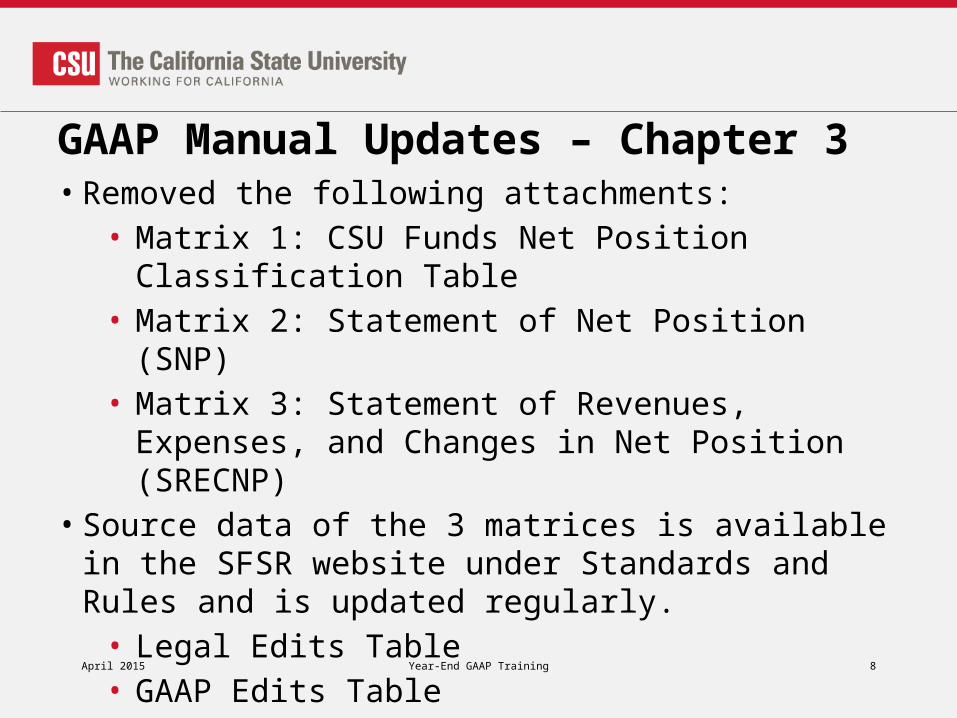

GAAP Manual Updates – Chapter 3• Removed the following attachments:• Matrix 1: CSU Funds Net Position Classification Table• Matrix 2: Statement of Net Position (SNP)• Matrix 3: Statement of Revenues, Expenses, and

Changes in Net Position (SRECNP)• Source data of the 3 matrices is available in the SFSR

website under Standards and Rules and is updated regularly.• Legal Edits Table• GAAP Edits Table• Table of Object Code and CSU Fund Definitions

April 2015 Year-End GAAP Training 8

GAAP Manual Updates – Chapter 3 (cont.)• Source data locationhttp://www.calstate.edu/sfsr/standards_and_rules/

April 2015 Year-End GAAP Training 9

GAAP Manual Updates – Chapter 3 (cont.)

• Discussion on GAAP FIRMS submission is now included in Chapter 7 GAAP Reporting in YES (TM1) and FIRMS

April 2015 Year-End GAAP Training 10

Chapter 4

GAAP Adjustments and Reclassification Entries

April 2015 Year-End GAAP Training 11

GAAP Manual Updates – Chapter 4• NEW structure• Arranged by GAAP Financial Statement line items

(vs. by accounting topic) • Combined information from Chapters 4, 5 and 7 in the

previous year GAAP manual as they relate to specific F/S line item

• Better correlation with the discussions in the Legal Manual to facilitate GAAP conversion

See hand-out on the revised table of contents for Chapter 4

April 2015 Year-End GAAP Training 12

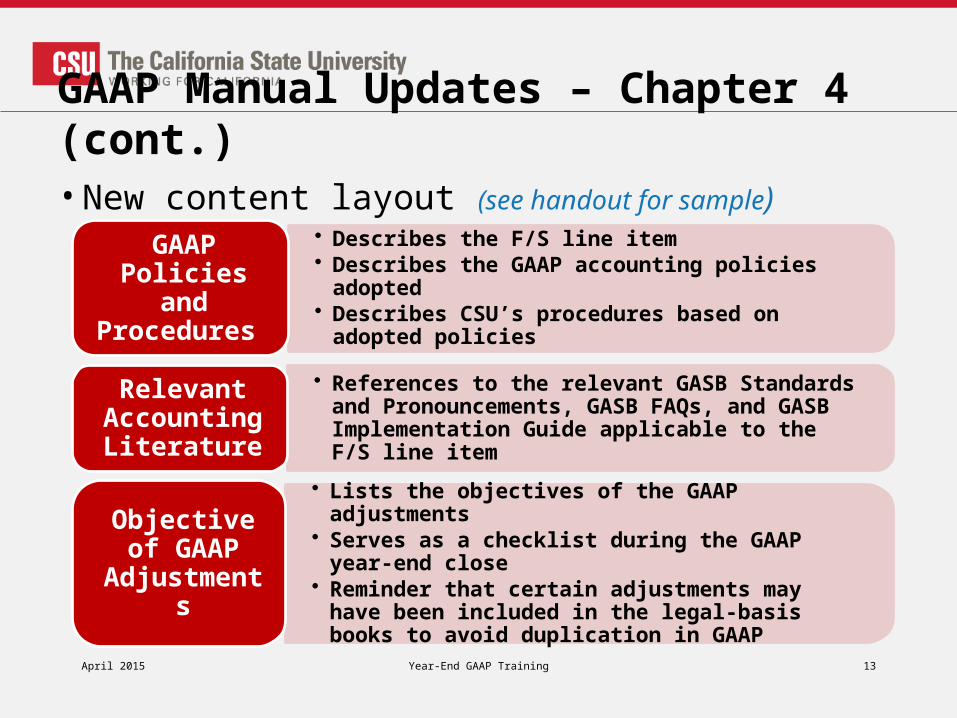

GAAP Manual Updates – Chapter 4 (cont.)• New content layout (see handout for sample)

April 2015 Year-End GAAP Training 13

• Describes the F/S line item• Describes the GAAP accounting policies adopted • Describes CSU’s procedures based on adopted

policies

GAAP Policies and

Procedures

• References to the relevant GASB Standards and Pronouncements, GASB FAQs, and GASB Implementation Guide applicable to the F/S line item

Relevant Accounting Literature

• Lists the objectives of the GAAP adjustments • Serves as a checklist during the GAAP year-end

close• Reminder that certain adjustments may have been

included in the legal-basis books to avoid duplication in GAAP

Objective of GAAP

Adjustments

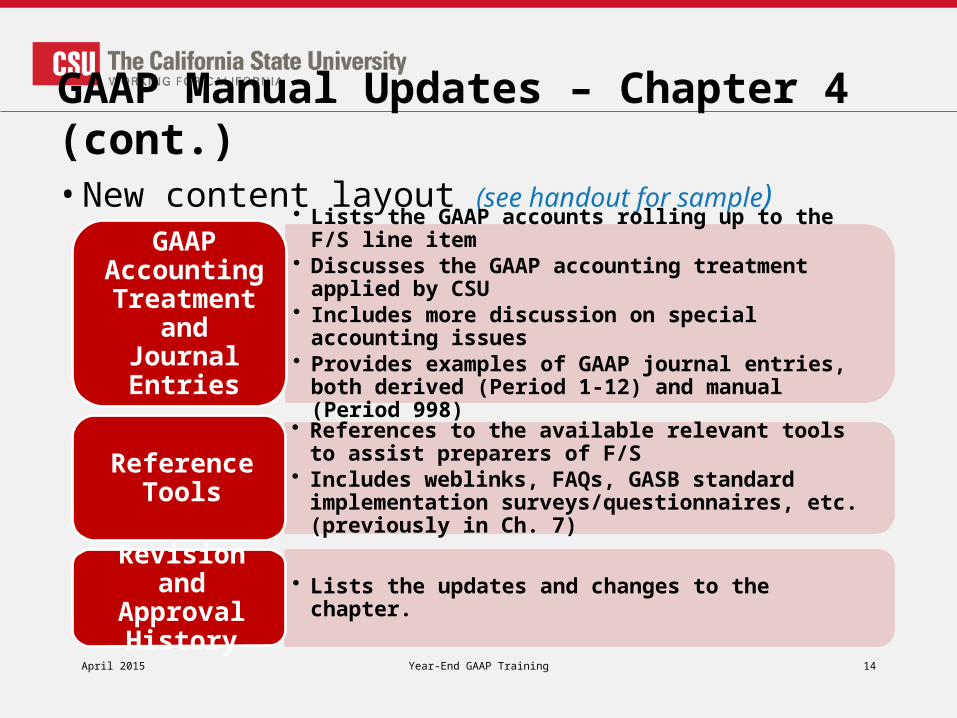

GAAP Manual Updates – Chapter 4 (cont.)• New content layout (see handout for sample) (cont.)

April 2015 Year-End GAAP Training 14

• Lists the GAAP accounts rolling up to the F/S line item• Discusses the GAAP accounting treatment applied by

CSU• Includes more discussion on special accounting issues• Provides examples of GAAP journal entries, both

derived (Period 1-12) and manual (Period 998)

GAAP Accounting Treatment

and Journal Entries

• References to the available relevant tools to assist preparers of F/S

• Includes weblinks, FAQs, GASB standard implementation surveys/questionnaires, etc. (previously in Ch. 7)

Reference Tools

• Lists the updates and changes to the chapter. Revision and

Approval History

Question #1

What is the TOOL used to guide preparers of the F/S in converting legal basis

accounting to GAAP basis?

April 2015 Year-End GAAP Training 15

Chapter 5

GAAP Adjustments or Reclassifications that Require Information from the Office of

the Chancellor

April 2015 Year-End GAAP Training 16

GAAP Manual Updates – Chapter 5• Updated the description of the passdown schedules

provided by the CO to include the following: • Description of the schedule• Purpose and use of the schedule• Method of distribution (e.g. via email, SFSR website)

• Added discussion on the new passdown schedule for Pension Obligation per GASB No. 68

April 2015 Year-End GAAP Training 17

GAAP Manual Updates – Chapter 5 (cont.)• Removed detailed discussion of accounting

treatment and moved them to appropriate sub-chapters in Chapter 4.• Capitalization of Non-Delegated Projects – Capital

Assets• Systemwide Revenue Bonds – Liabilities• Bond Anticipation Notes – Liabilities• OPEB – Liabilities• Capitalized Interest – Capital Assets

April 2015 Year-End GAAP Training 18

Chapter 6

Statement of Cash Flows

April 2015 Year-End GAAP Training 19

GAAP Manual Updates – Chapter 6• Includes the definition of cash and cash equivalents

for Statement of Cash Flows (SCF) purposes.• Provides guidance on gross vs. net reporting• Added more relevant GASB Comprehensive

Implementation Q&A Guide where applicable.• Relevant CSU examples and treatment are provided

for each activity (operating, noncapital financing).

April 2015 Year-End GAAP Training 20

GAAP Manual Updates – Chapter 6 (cont.)• Used actual campus data from FY13/14• The different tabs in the worksheet are as follows:• Instructions – provides direction in completing this

worksheet• Worksheet – where the actual SCF data is located• SNP, SRECNP and tabs [A] to [W] – input sheets that

will facilitate in completing the SCF

See hand-out for the SCF Worksheet

April 2015 Year-End GAAP Training 21

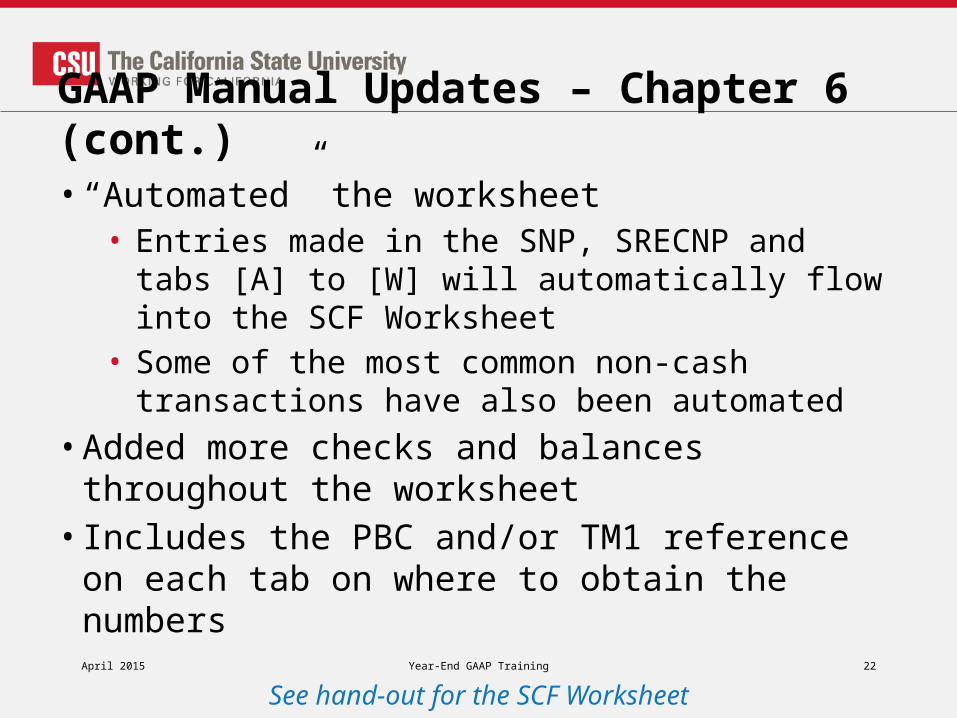

GAAP Manual Updates – Chapter 6 (cont.)• “Automated” the worksheet• Entries made in the SNP, SRECNP and tabs [A] to

[W] will automatically flow into the SCF Worksheet• Some of the most common non-cash transactions

have also been automated

• Added more checks and balances throughout the worksheet• Includes the PBC and/or TM1 reference on each tab

on where to obtain the numbers

See hand-out for the SCF Worksheet

April 2015 Year-End GAAP Training 22

GAAP Manual Updates – Chapter 6 (cont.)• Integrated the TM1 SCF prepopulated transactions

to assist in completing the reporting package• Includes the section for “amount paid to escrow”

See hand-out for the SCF Worksheet

April 2015 Year-End GAAP Training 23

GAAP Manual Updates – Chapter 6 (cont.)• Revision to the Statement of Cash Flows

Based on the GASB Comprehensive Q&A Guide (2.19.1):

The debt proceeds distributed to component units for capital purposes should be presented

as a noncapital financing cash outflows.

If the campus distributes the proceeds to the component units, it is not using the proceeds to acquire, construct, or improve its own capital assets. Therefore, the debt should not be considered capital debt for purposes of the Statement of

Cash Flows.

April 2015 Year-End GAAP Training 24

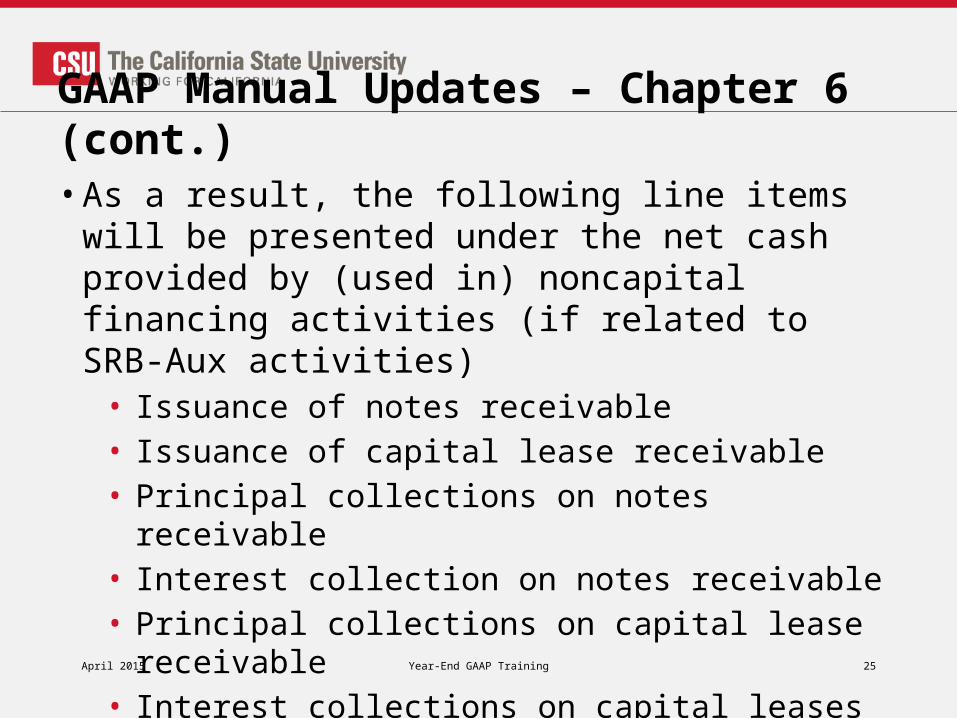

GAAP Manual Updates – Chapter 6 (cont.)• As a result, the following line items will be presented

under the net cash provided by (used in) noncapital financing activities (if related to SRB-Aux activities)• Issuance of notes receivable• Issuance of capital lease receivable• Principal collections on notes receivable• Interest collection on notes receivable• Principal collections on capital lease receivable• Interest collections on capital leases receivable

April 2015 Year-End GAAP Training 25

GAAP Manual Updates – Chapter 6 (cont.)• Benefits of using the SCF Worksheet• Huge time saver• Achieve consistency in preparation of SCF for

consolidation purposes• Other users such as Finance & Treasury (F&T)

usually requires detailed breakdown of cash flows and the SCF will assist them to meet their specific needs

• Facilitates easier review for audit purposes

April 2015 Year-End GAAP Training 26

GAAP Manual Updates – Chapter 6 (cont.)• Final Reminders:• NO decimals• Use the template as guide.

• Transactions in the SCF template are not all inclusive.• The campus may have “uncommon” transaction.• There might be a more accurate way of presenting your

cash flows

• Analyze accounts that typically have non-cash transactions (capital assets, other assets, long-term debt)

April 2015 Year-End GAAP Training 27

Question #2

Under which category in the SCF should the debt proceeds distributed to component units for capital projects be presented?

April 2015 Year-End GAAP Training 28

Chapter 7

GAAP Reporting in YES (TM1) and FIRMS

April 2015 Year-End GAAP Training 29

GAAP Manual Updates – Chapter 7• Old Chapter 7 entitled New GASB Standards

Implementation Tools is now incorporated in:• Chapter 4 (Service Concession Arrangements and

Pollution Remediation Obligation) • Chapter 8 (GASB No. 61 - Component Units)

• New contents on this chapter: • Standard practices and preparation of Reporting

Package in Year-End System (YES) (TM1)• GAAP FIRMS Submission (previously in Chapter 3)

April 2015 Year-End GAAP Training 30

GAAP Manual Updates – Chapter 7• Year-end System (YES) Reporting Package• The YES reporting package is a comprehensive

financial statement using TM1 application database• Consists of input sheets for the basic financial

statements and underlying footnotes for campuses and discretely presented component units

• Gathered information are used for consolidation of SW financial statements and Statement of Expenditures of Federal Awards (SEFA)

Please refer to the presentation slides from the breakout session for further discussion about this new chapter.

April 2015 Year-End GAAP Training 31

GAAP Manual Updates – Chapter 7• This chapter includes the following:

April 2015 Year-End GAAP Training 32

• Defines the purposes and use of the YES Reporting Package

Purpose of Reporting Package

• Provides the protocol in requesting access to TM1 (YES) applicationAccessibility

• Illustrates the steps taken in the submission and review of reporting package by SFSR and KPMG

Logistics for RP

Submission

GAAP Manual Updates – Chapter 7 (cont.)• This chapter includes the following(cont.):

April 2015 Year-End GAAP Training 33

• Lists all the input sheets that needs to be completed

• Includes the corresponding preparer (i.e. campus vs. SFSR on behalf of the campus)

• Includes the timing of the input sheet completion based on which reporting package version to which it was assigned

YES Input Sheets

• Summarizes the standard practices (in excel) that are used by SFSR and KPMG in performing review of reporting packages in order to ensure complete and accurate reporting package

• Serves as self-review checklist prior to submission

Standard Practices

• FAQ’s and tips when using TM1 application Frequently

Asked Questions

Chapter 8

Presentation of Component Units

April 2015 Year-End GAAP Training 34

GAAP Manual Updates – Chapter 8• Added the discussion on GASB No. 61 previously in

Chapter 4 as this should be used in deciding whether or not a component unit should be blended vs. discretely presented. • Added the GASB No. 61 Questionnaire (previously in

Chapter 7) as a tool in the decision making.

April 2015 Year-End GAAP Training 35

Chapter 9

Preparation for Financial Audit

April 2015 Year-End GAAP Training 36

GAAP Manual Updates – Chapter 9

• Updated PBC List for FY14/15 SW audit • Added new and modified existing exhibits or

query/report instructions to certain PBC items

Please refer to the PBC presentation slides prepared by KPMG and CO for further discussion of the changes.

April 2015 Year-End GAAP Training 37

Chapter 10 & 11

GAAP Preparation and Financial Reporting Checklists

April 2015 Year-End GAAP Training 38

GAAP Manual Updates – Chapters 10 & 11

• As a result of the changes in Chapter 4 GAAP Adjustments and Reclassification Entries, the following checklists are modified: • GAAP Preparation Checklist• GAAP Financial Reporting Checklist

• Use the updated checklist in complying with the PBC requirements

April 2015 Year-End GAAP Training 39

Chapter 12

NCAA

Agreed-Upon-Procedures Requirements

April 2015 Year-End GAAP Training 40

GAAP Manual Updates – Chapter 12• NCAA recently issued the updates to the AUP

reporting requirements effective for fiscal year ending June 30, 2015. • Summary of the updates is included in this chapter

for reference. • Campus coordinators are requested to work closely

with the Athletics Division to ensure compliance with the deliverable and deadline (January 15th).

April 2015 Year-End GAAP Training 41

Question #3

GASB No. 61 Questionnaire can now be found in which Chapter of the GAAP

Manual?

April 2015 Year-End GAAP Training 42