outlook for the u.s., florida and martin county economic council of martineconomic ... ·...

TRANSCRIPT

Outlook for the U.S., Florida Outlook for the U.S., Florida and Martin Countyand Martin CountyEconomic Council of MartinEconomic Council of MartinEconomic Council of Martin Economic Council of Martin CountyCountyyyOctober 12, 2011October 12, 2011

Hank Fishkind Ph DHank Fishkind, Ph.D.Fishkind & Associates, Inc.12051 Corporate Boulevardp

Orlando, Florida 32817

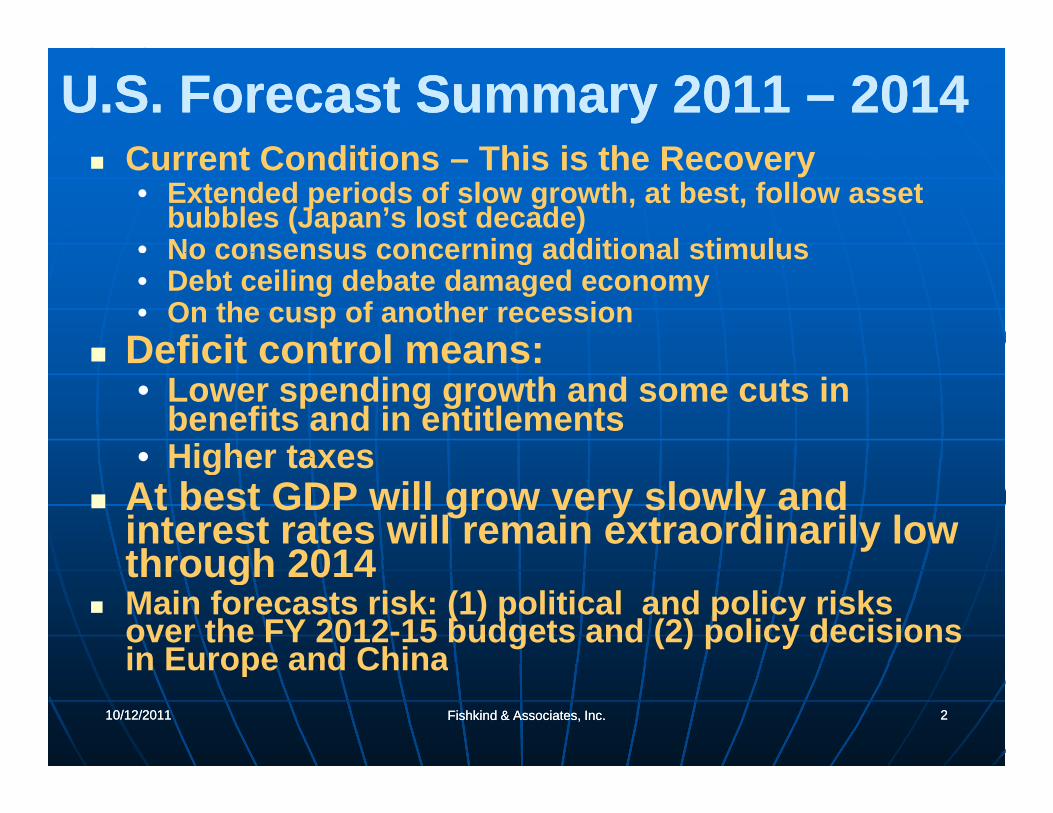

U.S. Forecast Summary 2011 U.S. Forecast Summary 2011 –– 20142014C t C diti Thi i th R Current Conditions – This is the Recovery• Extended periods of slow growth, at best, follow asset

bubbles (Japan’s lost decade)• No consensus concerning additional stimulusNo consensus concerning additional stimulus• Debt ceiling debate damaged economy• On the cusp of another recession

Deficit control means: Deficit control means: • Lower spending growth and some cuts in

benefits and in entitlements• Higher taxes• Higher taxes

At best GDP will grow very slowly and interest rates will remain extraordinarily low through 2014through 2014

Main forecasts risk: (1) political and policy risks over the FY 2012-15 budgets and (2) policy decisions in Europe and China

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 22

in Europe and China

Florida SummaryFlorida SummaryFlorida SummaryFlorida Summary Very modest recovery finally underway but real recovery will be

in 2012• Sustained job growth lead by tourism and healthcare• Sustained job growth lead by tourism and healthcare• Population growth remains weak and cannot recover fully until

housing markets recover in the Northeast and in the Midwest – 2012 timeframe

• Housing continues to be troubled and will not recover until 2012 withHousing continues to be troubled and will not recover until 2012 with stronger growth in population and employment

Recovery gains momentum 2012-2014 but peak is well below prior periods even by 2014

230 000 l ti th• 230,000 population growth• 95,000 new jobs

Geographic focus growth shifted and tightened• I 4 Corridor dominate growth over next decade• I-4 Corridor dominate growth over next decade• Miami-Dade, Jacksonville and St. Lucie will enjoy strong growth lead

by job generation• Panama City area will be boosted by new airport• Other areas will grow at historically slow rates

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 33

• Other areas will grow at historically slow rates

RECENT TRENDS IN GDP RECENT TRENDS IN GDP AND INFLATIONAND INFLATION

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 44

GROWTH IN REAL GDPGROWTH IN REAL GDPININ BILLIONS OF 2002$BILLIONS OF 2002$

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 55

Job GrowthJob GrowthJob GrowthJob Growth

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 66

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 77

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 88

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 99

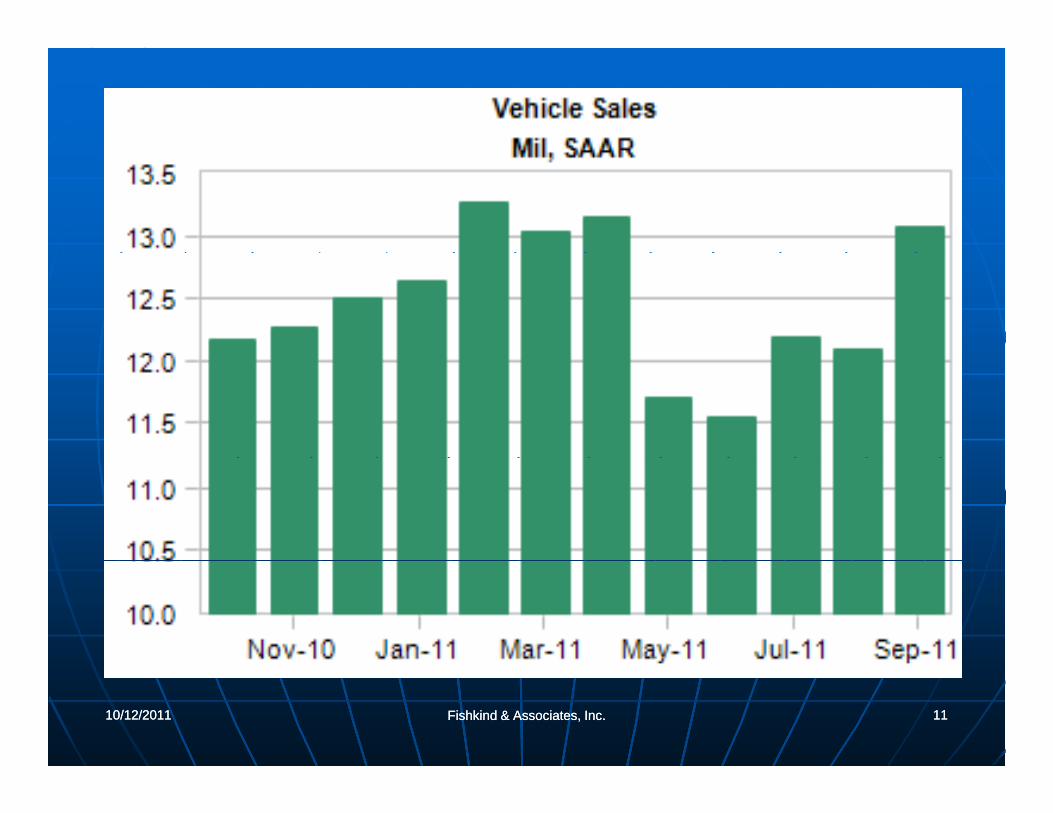

Retail SalesRetail Sales

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1010

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1111

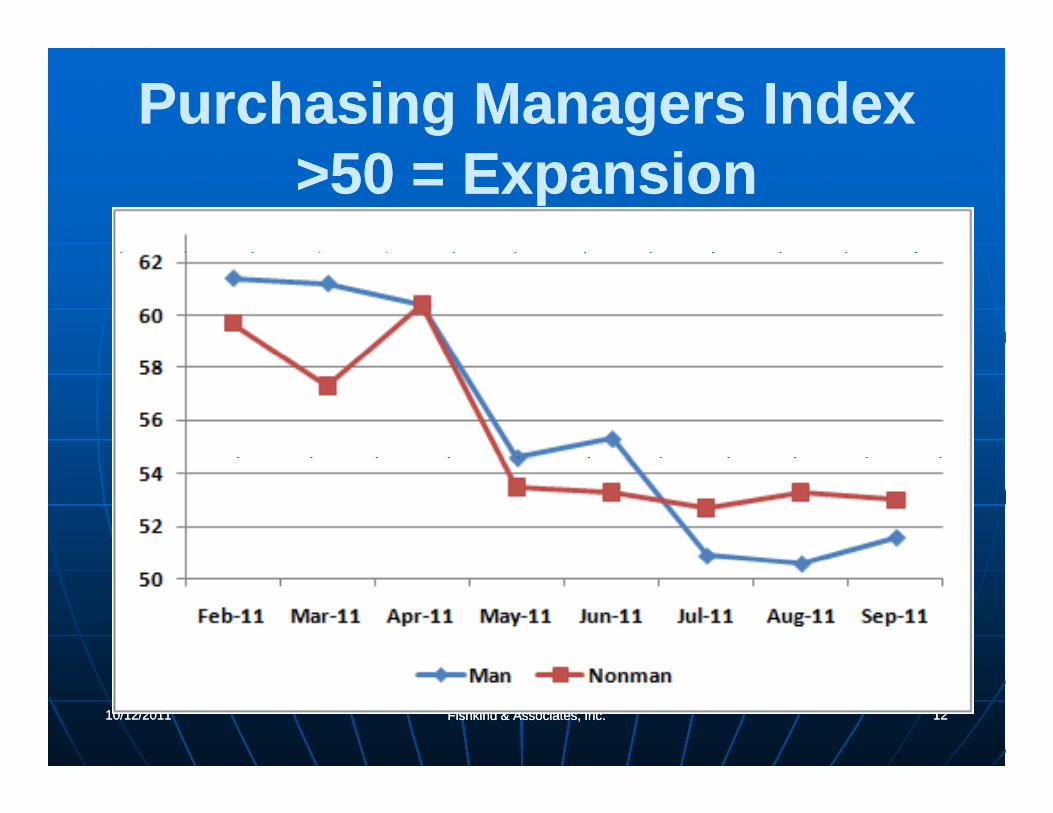

Purchasing Managers IndexPurchasing Managers Index>50 = Expansion>50 = Expansion

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1212

Sales of New and Existing Sales of New and Existing HomesHomes

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1313

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1414

Total Revenues and OutlaysTotal Revenues and OutlaysPercentage of GDPPercentage of GDP

Baseline: A benchmark for measuring the budgetary effects of proposed changes in federal revenues or spending. As defined in the Deficit Control Act of 1985, the baseline is the projection of new budget authority, outlays, revenues, and the deficit or surplus into the budget year and out‐years on the basis of current laws and policies.

C O N G R E S S I O N A L B U D G E T O F F I C E

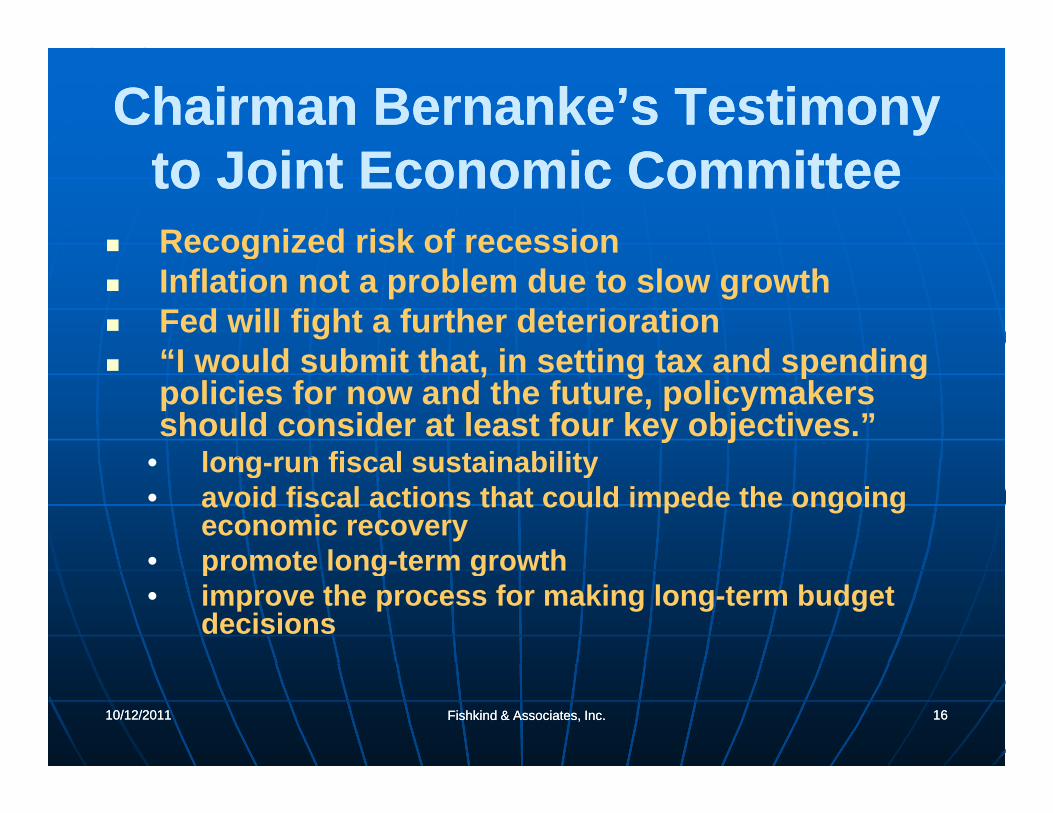

Chairman Bernanke’s Testimony Chairman Bernanke’s Testimony J i E i C iJ i E i C ito Joint Economic Committeeto Joint Economic Committee

Recognized risk of recessiong Inflation not a problem due to slow growth Fed will fight a further deterioration

“I would submit that in setting tax and spending “I would submit that, in setting tax and spending policies for now and the future, policymakers should consider at least four key objectives.”

long run fiscal sustainability• long-run fiscal sustainability• avoid fiscal actions that could impede the ongoing

economic recovery• promote long term growth• promote long-term growth• improve the process for making long-term budget

decisions

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1616

Drifting Into RecessionDrifting Into RecessionDrifting Into RecessionDrifting Into Recession

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1717

INTEREST RATES INTEREST RATES

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1818

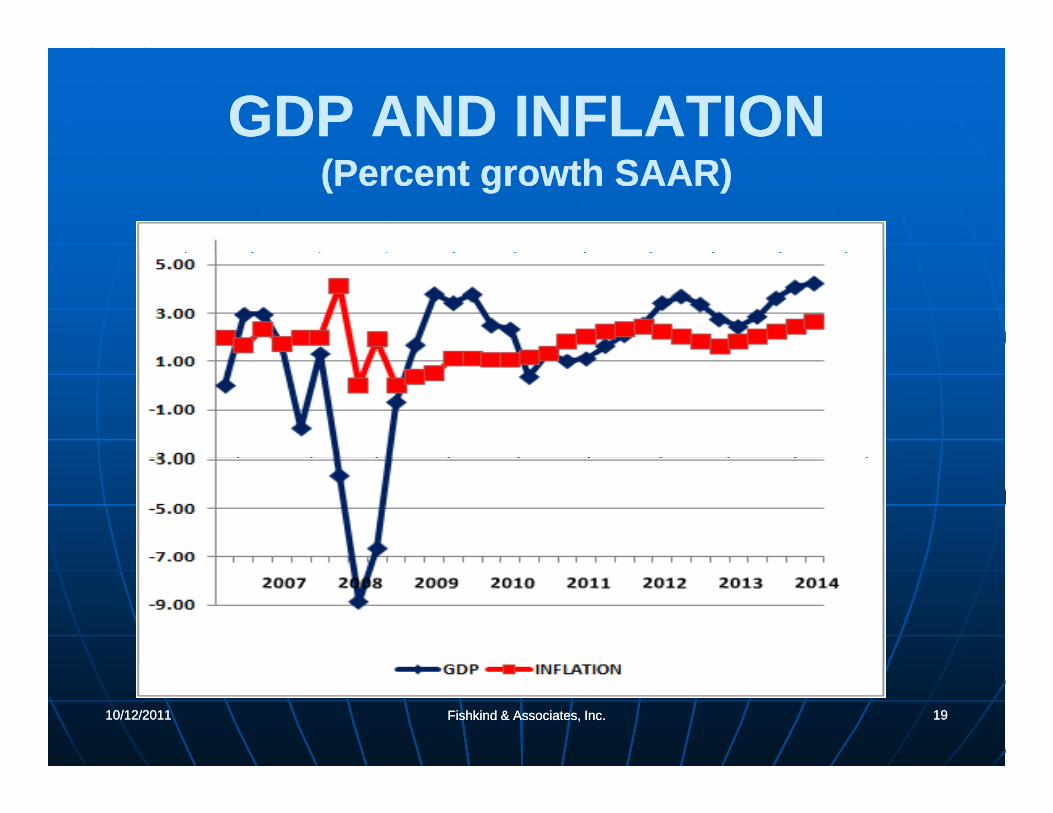

GDP AND INFLATIONGDP AND INFLATION(Percent growth SAAR)(Percent growth SAAR)

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 1919

Growth in Real GDPGrowth in Real GDPWith and Without Jobs ActWith and Without Jobs Act

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2020

Florida Population GrowthFlorida Population GrowthFlorida Population GrowthFlorida Population Growth

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2121

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2222

Florida Employment GrowthFlorida Employment GrowthYearYear--overover--Year ChangesYear Changes

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2323

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2424

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2525

More People 65+ ButMore People 65+ ButFewer Will Move/RetireFewer Will Move/Retire

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2626

Florida Growth ForecastFlorida Growth ForecastP l ti d E l tP l ti d E l tPopulation and EmploymentPopulation and Employment

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2727

Housing StartsHousing Starts

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2828

SingleSingle--Family Pricing and Family Pricing and Closing VolumesClosing Volumes

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 2929

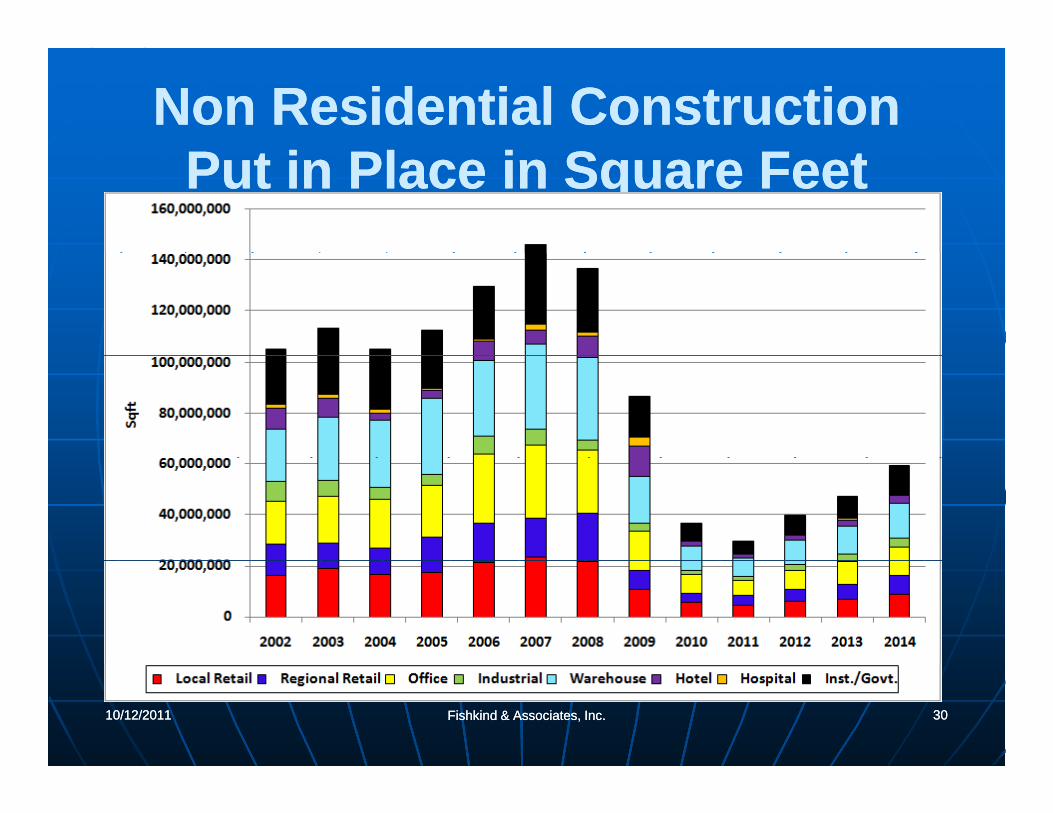

Non Residential Construction Non Residential Construction P i Pl i S FP i Pl i S FPut in Place in Square FeetPut in Place in Square Feet

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3030

Martin CountyMartin CountyM j E i D iM j E i D iMajor Economic DriversMajor Economic Drivers

Retirement, tourism and luxury residential , ydevelopment drive the economy.

Broward County is almost built out and Palm Beach County has chosen to restrict futureBeach County has chosen to restrict future growth. This pushes growth pressures up the coast, but Martin has chosen to restrict its growth as well and focus on high endits growth as well and focus on high end development.

The political environment has been hostile to i d l d l ieconomic development and to population

growth, and there is every reason to believe that this posture will remain in place.

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3131

p p Proposed new DRIs will tell the story

South Florida’s Growth PatternSouth Florida’s Growth Pattern

3232

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3333

MARTIN COUNTY GROWTH IN MARTIN COUNTY GROWTH IN POPU ATION & EMP OYMENTPOPU ATION & EMP OYMENTPOPULATION & EMPLOYMENTPOPULATION & EMPLOYMENT

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3434

MARTIN COUNTYMARTIN COUNTYHOUSING STARTSHOUSING STARTSHOUSING STARTSHOUSING STARTS

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3535

SingleSingle--Family ClosingsFamily Closings

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3636

Martin CountyMartin CountyC i l C iC i l C iCommercial ConstructionCommercial Construction

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3737

Florida’s Economic Florida’s Economic $$Incentives for BioIncentives for Bio--Tech $MTech $M

Big money and large local matches needed for success. Is Martin really in this game?

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3838

Is Martin really in this game?

Martin County Economic Martin County Economic DevelopmentDevelopment

Without dramatic and expensive actions to pchange market perception and permitting realities:• County will grow slowlyy g y• Retail and service will predominate

Major changes in policy can have dramatic impacts:impacts:• Martin has good reputation• Desirable location• Impact fees too high and permitting too hostile• Tool Kit is a great start• Real economic incentives needed

10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 3939

The End10/12/201110/12/2011 Fishkind & Associates, Inc.Fishkind & Associates, Inc. 4040

The End

QUESTIONS?Adobe Acrobat PDF copy of this presentationAdobe Acrobat PDF copy of this presentationwill be available in the PowerPoint Presentationsarea on our website (fishkind.com). In order todownload the PDF file please use the followingaccess code:

MXWJKD