paa amendments the key expansion to our...

TRANSCRIPT

20 August 2019

PAA amendments – the key expansion to our mandate

2

Audit Report For

Accountability

AGSA MISSION

The Auditor-General of South Africa has a constitutional

mandate and, as the Supreme Audit Institution (SAI) of

South Africa, exists to strengthen our country’s

democracy by enabling oversight, accountability and

governance in the public sector through auditing, thereby

building public confidence.

Key expansion of our mandate

3

Refer material

irregularities to

relevant public bodies

for further investigations

Issue a certificate

of debt for failure to

implement the remedial

action if financial loss

was involved

Take binding

remedial action for

failure to implement the

AG’s recommendations

for material irregularities

Material irregularity (MI) legislation

4

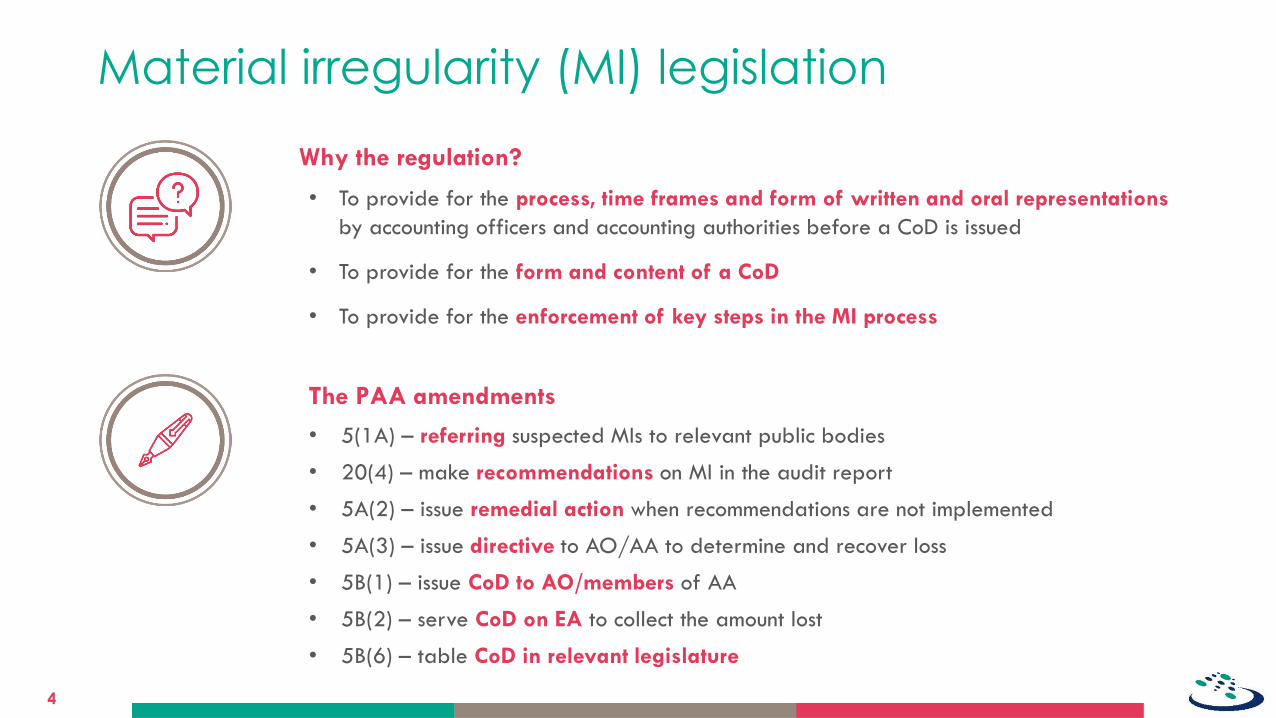

The PAA amendments

Why the regulation?

• To provide for the process, time frames and form of written and oral representations

by accounting officers and accounting authorities before a CoD is issued

• To provide for the form and content of a CoD

• To provide for the enforcement of key steps in the MI process

• 5(1A) – referring suspected MIs to relevant public bodies

• 20(4) – make recommendations on MI in the audit report

• 5A(2) – issue remedial action when recommendations are not implemented

• 5A(3) – issue directive to AO/AA to determine and recover loss

• 5B(1) – issue CoD to AO/members of AA

• 5B(2) – serve CoD on EA to collect the amount lost

• 5B(6) – table CoD in relevant legislature

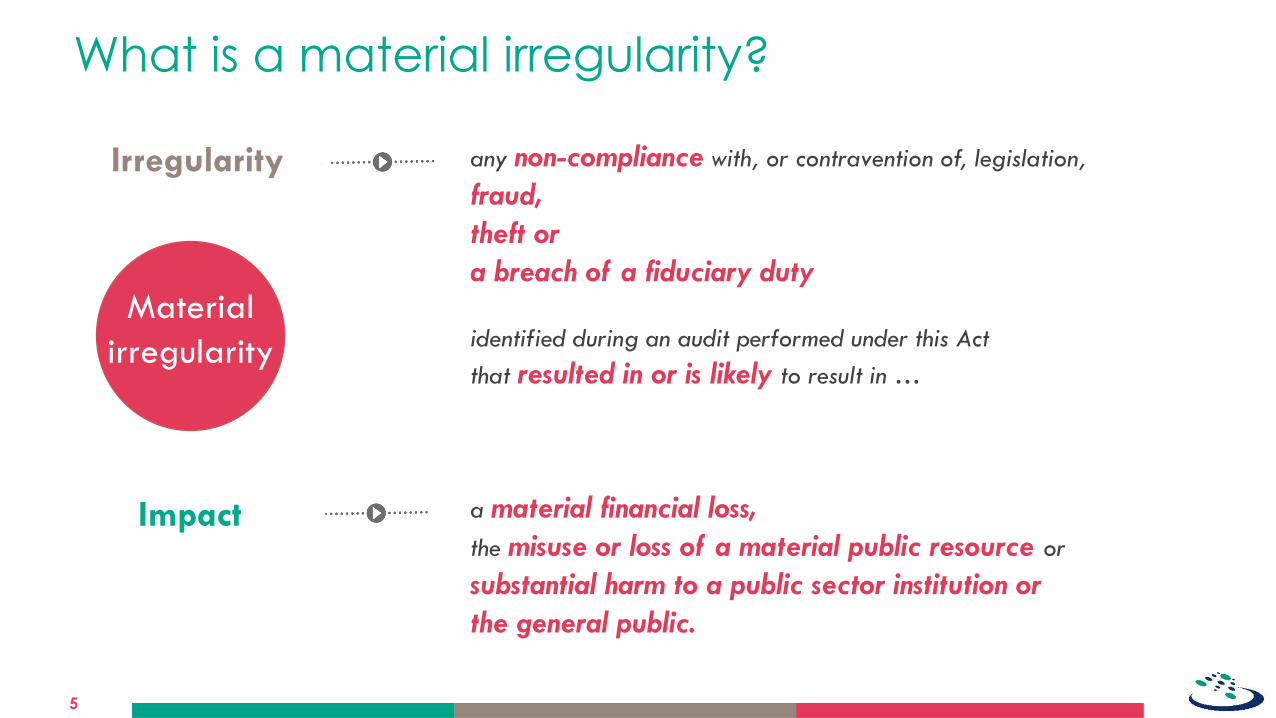

What is a material irregularity?

5

any non-compliance with, or contravention of, legislation,

fraud,

theft or

a breach of a fiduciary duty

identified during an audit performed under this Act

that resulted in or is likely to result in …

a material financial loss,

the misuse or loss of a material public resource or

substantial harm to a public sector institution or

the general public.

Irregularity

Impact

Material

irregularity

6

Irregularity Impact

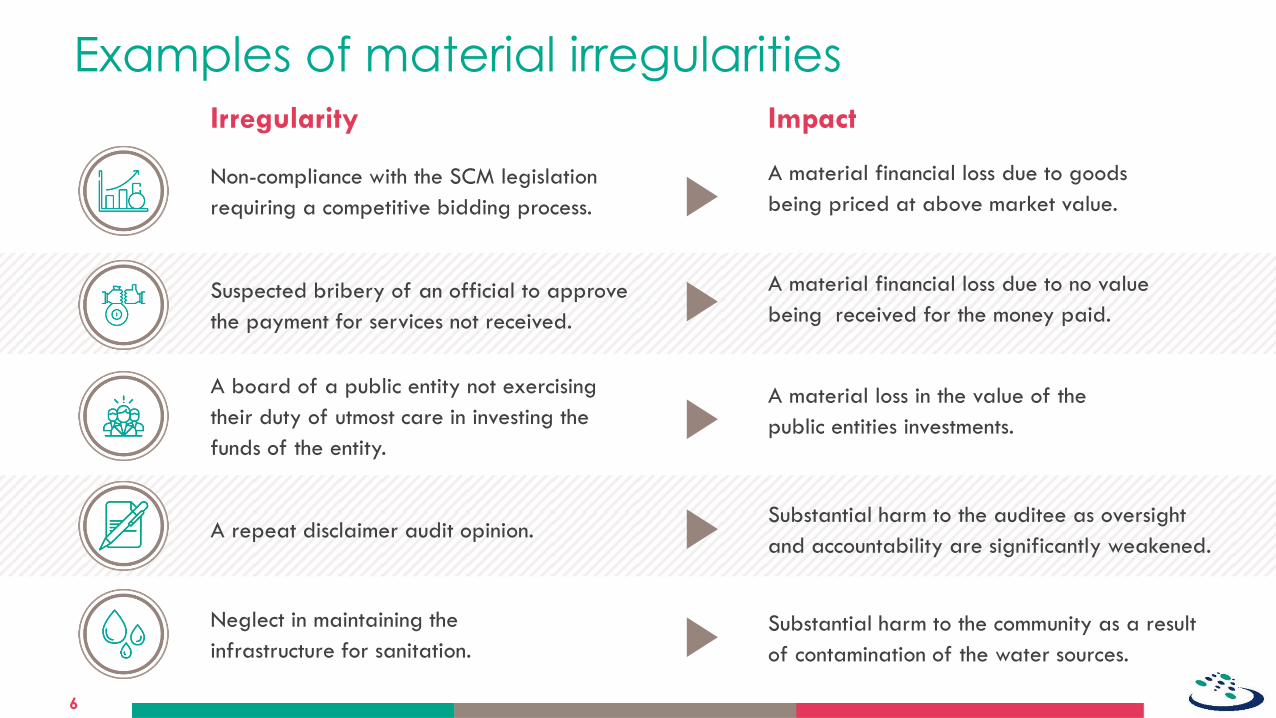

Examples of material irregularities

Non-compliance with the SCM legislation

requiring a competitive bidding process.

A material financial loss due to goods

being priced at above market value.

Suspected bribery of an official to approve

the payment for services not received.

A material financial loss due to no value

being received for the money paid.

A board of a public entity not exercising

their duty of utmost care in investing the

funds of the entity.

A material loss in the value of the

public entities investments.

A repeat disclaimer audit opinion. Substantial harm to the auditee as oversight

and accountability are significantly weakened.

Neglect in maintaining the

infrastructure for sanitation.

Substantial harm to the community as a result

of contamination of the water sources.

Overview of the MI process – as per the regulations

7

MI/suspected MI NOT APPROPRIATELY ADDRESSED by AO/AA

Audit process

Refe

rral pro

cess

Cert

ific

ate

of

debt p

roce

ss

Rem

ed

ial p

roce

ss

Perform INVESTIGATION

Take further ACTIONS based on outcomes

REFER TO PUBLIC BODY for investigation

Receive OUTCOME of investigation

Receive PROGRESS REPORTS

Follow up in SUBSEQUENT AUDITS

Include RECOMMENDATION in audit report

FOLLOW UP if remedial action implemented /if not implemented

ORAL REPRESENTATION to advisory committee who makes recommendations

FOLLOW UP if recommendation implemented

MI resulted in FINANCIAL LOSS

MI DID NOT result in financial loss

ISSUE REMEDIAL ACTION if recommendation not implemented

WRITTEN REPRESENTATION by AO/individual members of AA

REPORT TO EA and LEGISLATURE or other body/take legal action/

any appropriate other action

Issues CERTIFICATE OF DEBT

EA RECOVERS DEBT

The audit process

8

DECIDE whether

• MI should be

referred to a

relevant public

body and/or

• Recommendation

should be

included in audit

report to enable

remedial action or

• An investigation

should be done

FOLLOW UP

in subsequent

audits until

fully resolved

IDENTIFY

MI/suspected MI

INCLUDE info on

the MI in audit

report and

• Recommendations

or

• That MI was

referred to a

public body

• That MI is being

investigated

AO/AA FAIL

to submit by

stipulated

time

AO/AA

has TAKEN

appropriate

action

AO/AA has

NOT TAKEN

appropriate

action

REQUEST proof

from AO/AA by

stipulated time

on actions taken

• To stop

irregularity

• To prevent/

recover loss

or other

impact

• Against

responsible

person

Reg 4(1)

Reg 4(3)

Reg 4(3)

Reg 4(2) Reg 4(4)

Reg 3(3)

Reg 3(3)

Reg 3(2)

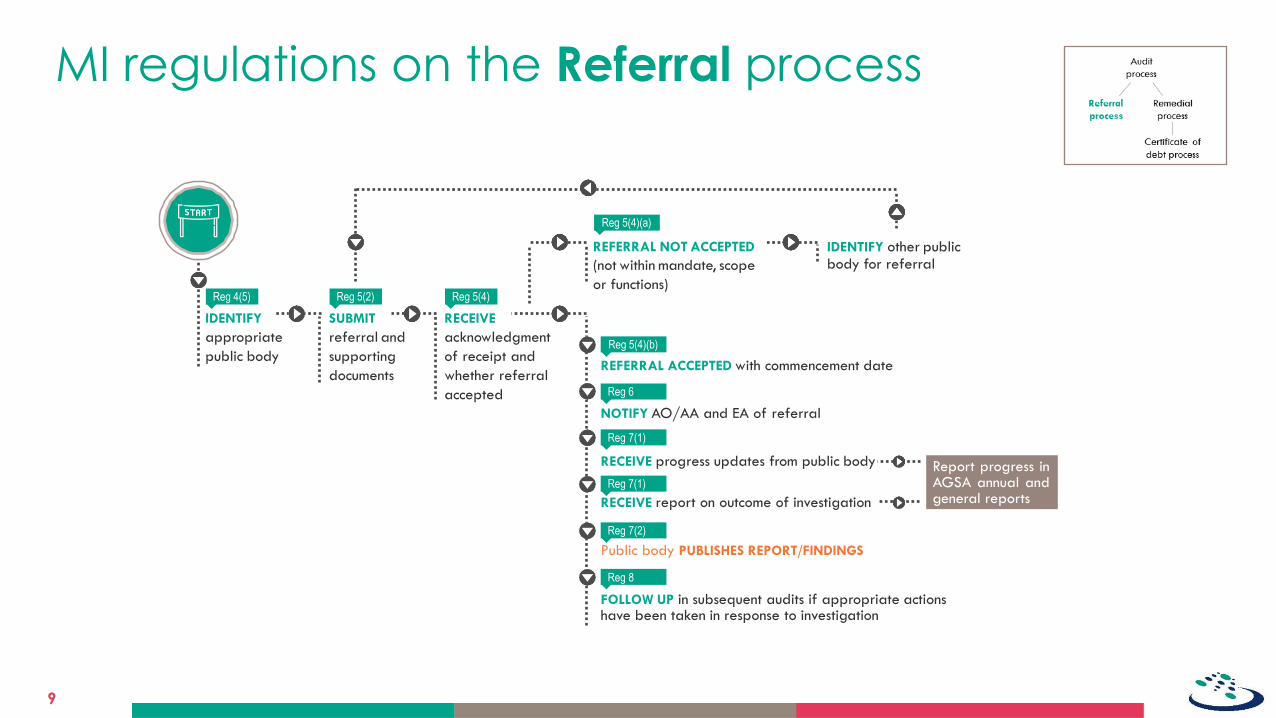

MI regulations on the Referral process

9

RECEIVE progress updates from public body

REFERRAL ACCEPTED with commencement date

REFERRAL NOT ACCEPTED

(not within mandate, scope

or functions)

IDENTIFY other public body for referral

RECEIVE report on outcome of investigation

Report progress in AGSA annual and general reports

Reg 4(5) Reg 5(2) Reg 5(4)

Reg 5(4)(b)

Reg 5(4)(a)

Reg 6

NOTIFY AO/AA and EA of referral

Reg 7(1)

Reg 7(1)

Reg 7(2)

Public body PUBLISHES REPORT/FINDINGS

Reg 8

FOLLOW UP in subsequent audits if appropriate actions have been taken in response to investigation

IDENTIFY

appropriate

public body

SUBMIT

referral and

supporting

documents

RECEIVE

acknowledgment

of receipt and

whether referral

accepted

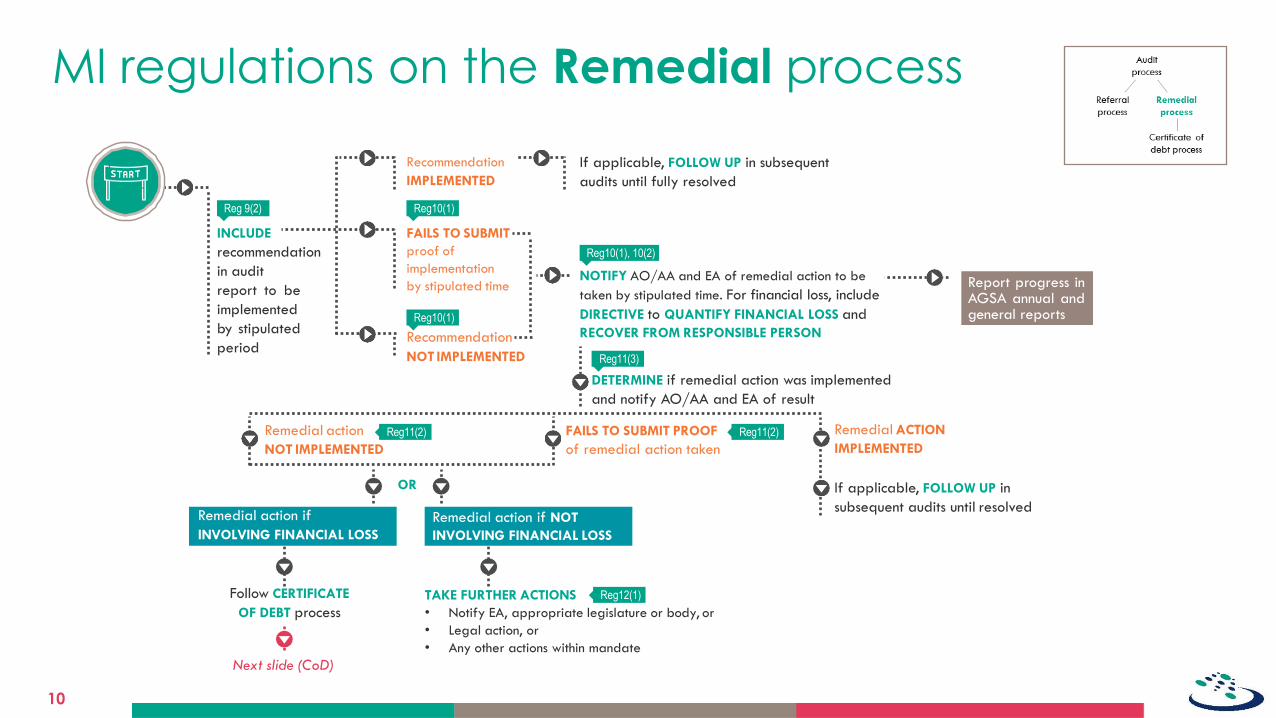

MI regulations on the Remedial process

10

INCLUDE

recommendation

in audit

report to be

implemented

by stipulated

period

FAILS TO SUBMIT

proof of

implementation

by stipulated time

Recommendation

IMPLEMENTED

Recommendation

NOT IMPLEMENTED

Reg10(1)

Reg10(1)

Reg10(1), 10(2)

Reg 9(2)

If applicable, FOLLOW UP in subsequent

audits until fully resolved

NOTIFY AO/AA and EA of remedial action to be

taken by stipulated time. For financial loss, include

DIRECTIVE to QUANTIFY FINANCIAL LOSS and

RECOVER FROM RESPONSIBLE PERSON

OR

Reg11(3)

DETERMINE if remedial action was implemented

and notify AO/AA and EA of result

Remedial action

NOT IMPLEMENTED

Follow CERTIFICATE

OF DEBT process

Next slide (CoD)

Remedial action if

INVOLVING FINANCIAL LOSS

FAILS TO SUBMIT PROOF

of remedial action taken

TAKE FURTHER ACTIONS

• Notify EA, appropriate legislature or body, or

• Legal action, or

• Any other actions within mandate

Remedial action if NOT

INVOLVING FINANCIAL LOSS

Remedial ACTION

IMPLEMENTED

If applicable, FOLLOW UP in

subsequent audits until resolved

Reg11(2) Reg11(2)

Reg12(1)

Report progress in AGSA annual and general reports

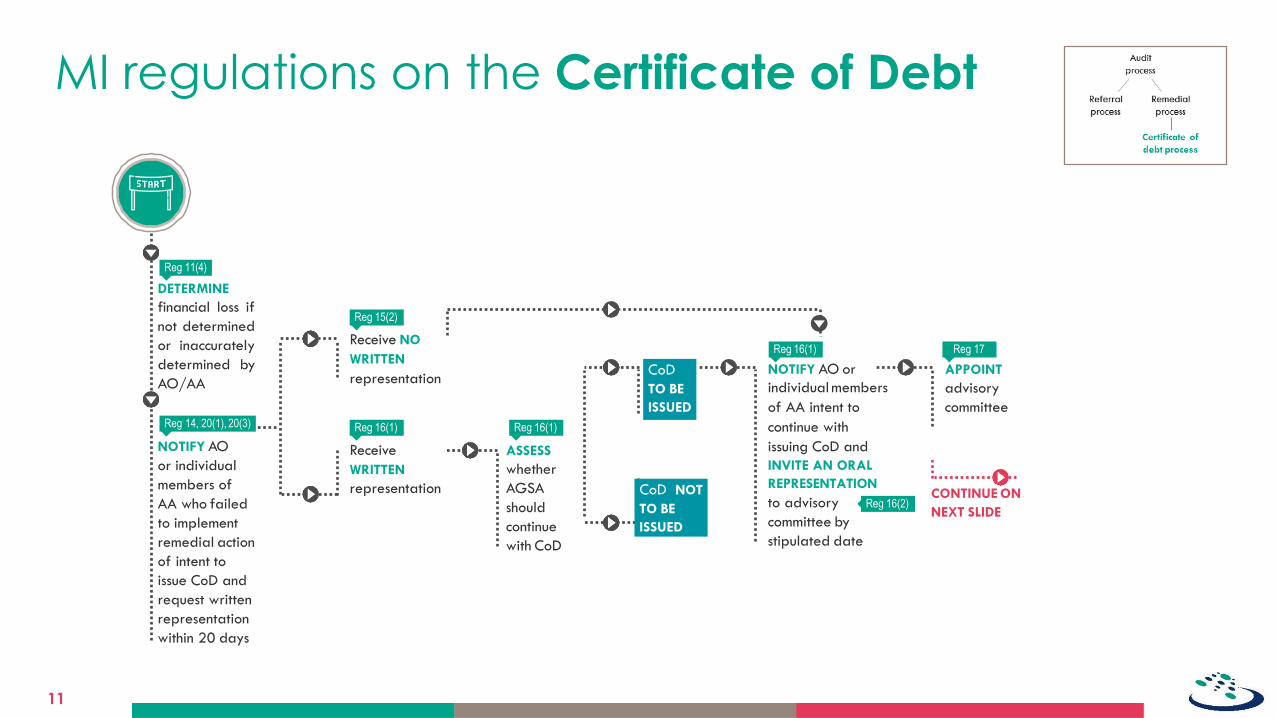

MI regulations on the Certificate of Debt

11

DETERMINE

financial loss if

not determined

or inaccurately

determined by

AO/AA

NOTIFY AO

or individual

members of

AA who failed

to implement

remedial action

of intent to

issue CoD and

request written

representation

within 20 days

Receive

WRITTEN

representation CoD

NOT TO

BE ISSUED

ASSESS

whether

AGSA

should

continue

with CoD

Receive NO

WRITTEN

representation CoD

TO BE

ISSUED

NOTIFY AO or

individual members

of AA intent to

continue with

issuing CoD and

INVITE AN ORAL

REPRESENTATION

to advisory

committee by

stipulated date

APPOINT

advisory

committee

CONTINUE ON

NEXT SLIDE

Reg 11(4)

Reg 15(2)

Reg 16(1) Reg 16(1)

Reg 17 Reg 16(1)

Reg 16(2)

Reg 14, 20(1), 20(3)

CoD NOT

TO BE

ISSUED

MI regulations on the Certificate of Debt (continued)

12

CONTINUED FROM

PREVIOUS SLIDE

Reg 18, 19(1)

ORAL

REPRESENTATION

by AO/individual

member

of AA and

consideration

by advisory

committee

RECEIVE

RECOMMENDATIONS

from advisory

committee

CONSIDER

recommendations

and MAKE

DECISION and

inform AO/

individual

member of AA

SERVE

COPY OF

CoD on EA

who should

recover

debt and

provide

progress

PROGRESS made with recovery

INADEQUATE PROGRESS with recovery

INFORM EA of intention to report

failure to relevant legislature REPORT FAILURE to

relevant legislature

Reg 19(2)

Reg 20(2), 20(4)

Reg 20(5)(a), 20(6) Reg 20(5)(b)

SERVE CoD on

AO/ individual

member of AA

in prescribed

form and

signed by AG

RECEIVE progress

reports on

recovery of debt

CoD NOT

TO BE

ISSUED

DOES NOT RECEIVE

progress reports

Reg 21(2)

Reg 21(3)

Reg 21(3)

Reg 21(3)

Report progress in AGSA annual and general reports

Main legal considerations

13

Are the amendments to the PAA constitutional?

Possibility of overreach?

Does the law permit strict liability in the manner it is envisaged in the Amendment Act?

The Amendment Act commenced on 1 April 2019. Are the amendments retrospectively applicable?

Which audits and audit related services do these amendments apply to?

How will the rights of AAs/AOs be protected?

How effective will these enforcement powers be if AOs/AAs will simply resign?

Is it lawful to adopt a phased implementation approach?

Importance of adhering to the provisions just administrative process

14

The Promotion of Administrative Justice Act, 2000 (PAJA) defines administrative action as any decision taken, or

failure to take a decision, by an organ of state when -

Exercising a power in terms of the Constitution or a provincial Constitution, or

Exercising a power or performing a public function in terms of any legislation which adversely affects the

rights of any person and has a direct, external, legal effect.

Remedial action and Certificate of debt = Administrative action.

Administrative action is subject to judicial review on the basis of rationality and procedural fairness under PAJA.

Importance of adhering to the provisions just administrative process (continued)

Right to administrative justice is protected in the Bill of Rights in the Constitution

Section 33 of the Constitution guarantees the following –

Lawful, reasonable and procedurally fair administrative action

Right to be given written reasons.

Administrative action that fails to meet these requirements can be reviewed and set aside

15

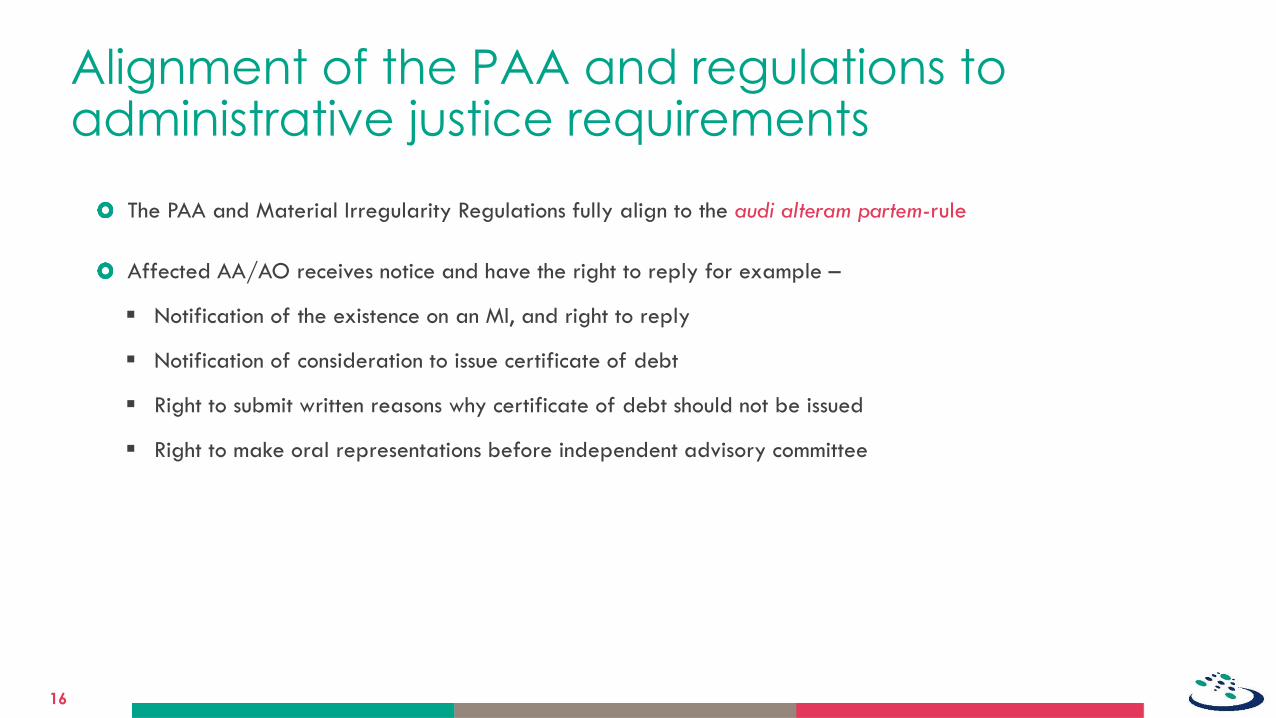

Alignment of the PAA and regulations to administrative justice requirements

The PAA and Material Irregularity Regulations fully align to the audi alteram partem-rule

Affected AA/AO receives notice and have the right to reply for example –

Notification of the existence on an MI, and right to reply

Notification of consideration to issue certificate of debt

Right to submit written reasons why certificate of debt should not be issued

Right to make oral representations before independent advisory committee

16

Material irregularity vs irregular expenditure

17

What is the Irregular Expenditure Material Irregularity

Definition

Expenditure incurred in contravention of,

or that is not in accordance with a

requirement of any applicable

legislation.

Non-compliance with, or contravention of, legislation,

fraud, theft or a breach of fiduciary duty identified

during an audit that resulted in or is likely to result in a

material financial loss, the misuse or loss of a material

public resource, or substantial harm to a public sector

institution or the general public.

Difference:

Irregularity

The irregularity is only non-compliance

with legislation when incurring

expenditure.

The irregularity is any non-compliance (not limited to

expenditure) as well as fraud, theft or a breach of

fiduciary duty.

Difference:

Impact

The impact is not specified, as the PFMA

requires the accounting officer or authority

to determine the impact.

There can be irregular expenditure that

did not result in any losses, misuse of harm.

The irregularity must have resulted in or there must be

indicators that it is likely to result in a material financial

loss/ misuse of loss of a material public resource or

substantial harm to a public sector institution or the

general public.

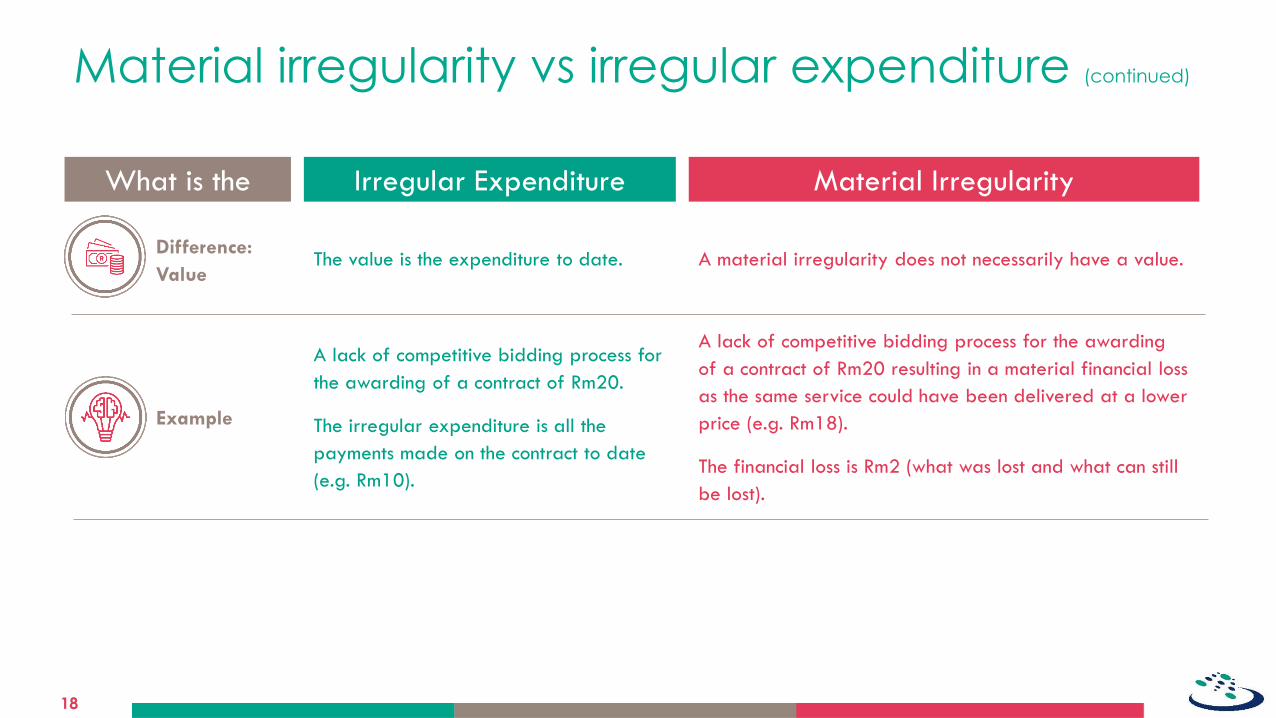

Material irregularity vs irregular expenditure (continued)

18

What is the Irregular Expenditure Material Irregularity

Difference:

Value The value is the expenditure to date. A material irregularity does not necessarily have a value.

Example

A lack of competitive bidding process for

the awarding of a contract of Rm20.

The irregular expenditure is all the

payments made on the contract to date

(e.g. Rm10).

A lack of competitive bidding process for the awarding

of a contract of Rm20 resulting in a material financial loss

as the same service could have been delivered at a lower

price (e.g. Rm18).

The financial loss is Rm2 (what was lost and what can still

be lost).

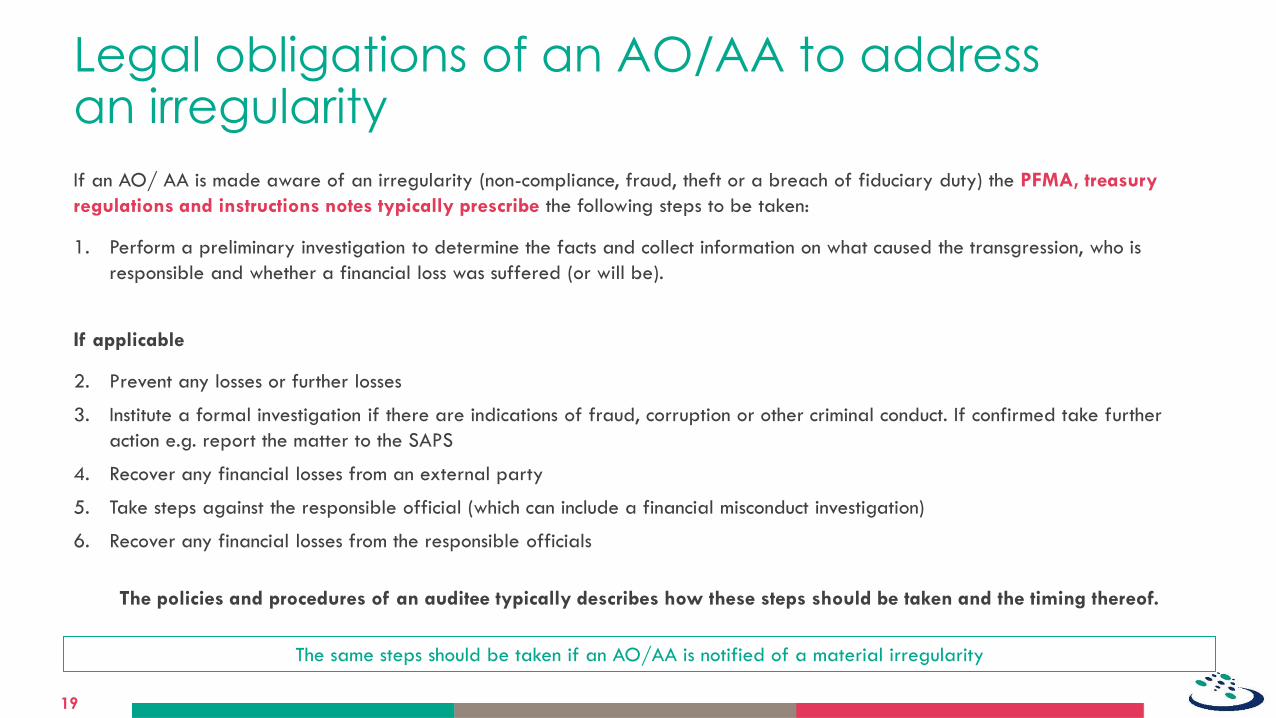

Legal obligations of an AO/AA to address an irregularity

If an AO/ AA is made aware of an irregularity (non-compliance, fraud, theft or a breach of fiduciary duty) the PFMA, treasury

regulations and instructions notes typically prescribe the following steps to be taken:

1. Perform a preliminary investigation to determine the facts and collect information on what caused the transgression, who is

responsible and whether a financial loss was suffered (or will be).

If applicable

2. Prevent any losses or further losses

3. Institute a formal investigation if there are indications of fraud, corruption or other criminal conduct. If confirmed take further

action e.g. report the matter to the SAPS

4. Recover any financial losses from an external party

5. Take steps against the responsible official (which can include a financial misconduct investigation)

6. Recover any financial losses from the responsible officials

The policies and procedures of an auditee typically describes how these steps should be taken and the timing thereof.

The same steps should be taken if an AO/AA is notified of a material irregularity

19

Example - MI Process for an irregularity that caused a material financial loss (remedial route)

20

1

Notify the AO/AA of

the MI - provide 20

working days to

respond on actions

taken and planned

[Regulation 3(2)]

May 2019

2

Identify the MI during

the 2018-19 audit

April 2019

3

Conclude based on

AO/AA response if

appropriate action is

taken or planned.

June 2019

4

Follow-up whether the recommendations

have been implemented. If not

implemented, issue remedial action to

the AO/AA that must be implement by a

specific date (e.g. within 3 months).

[Regulation 9(1)]

February 2020

5

If actions were not

appropriate, include

recommendations in the

audit report on how the MI

should be addressed by a

specific date (e.g. within 6

months) [Regulation 4(3)]

31 July 2019

NB Note:

Appropriate action

is the steps the

AO/AA is legally

obligated to take

NB Note:

The recommendations

are the steps the

AO/AA is legally

obligated to take

NB Note:

The remedial action remains the steps

the AO/AA is legally obligated to

take and includes a directive to

quantify the financial loss and recover

it from the responsible person

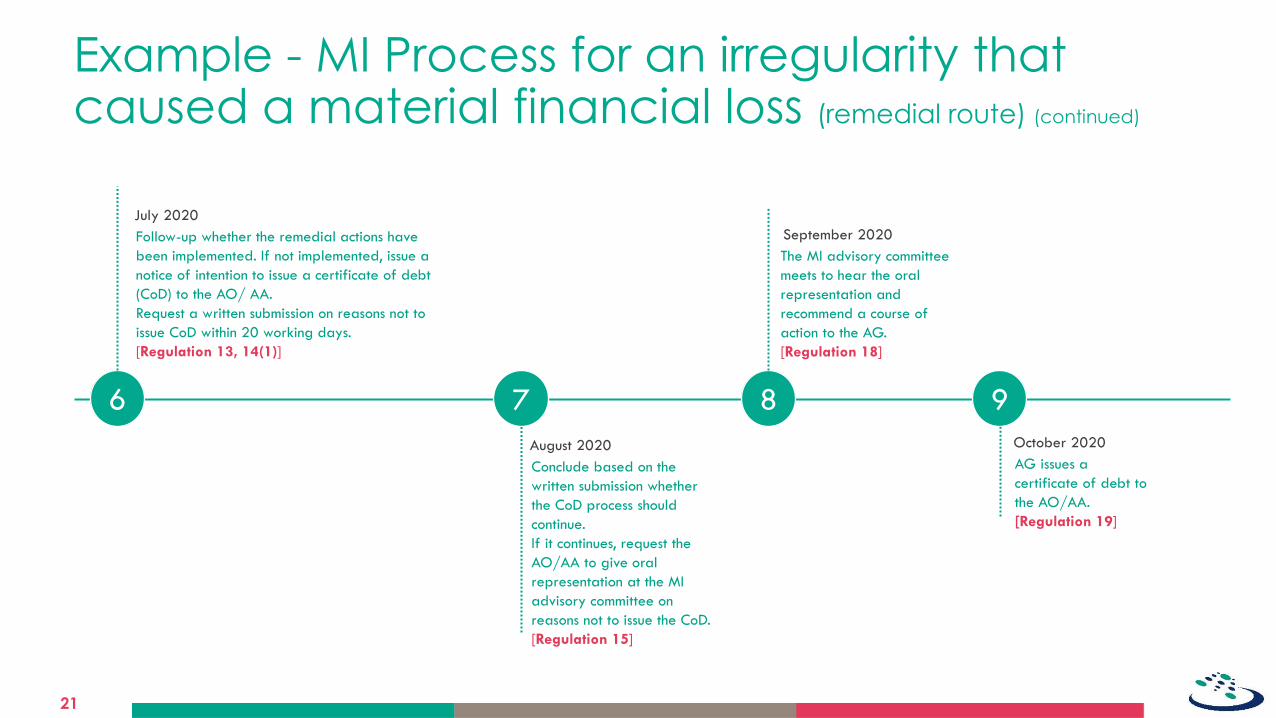

Example - MI Process for an irregularity that caused a material financial loss (remedial route) (continued)

21

6

Conclude based on the

written submission whether

the CoD process should

continue.

If it continues, request the

AO/AA to give oral

representation at the MI

advisory committee on

reasons not to issue the CoD.

[Regulation 15]

August 2020

7

Follow-up whether the remedial actions have

been implemented. If not implemented, issue a

notice of intention to issue a certificate of debt

(CoD) to the AO/ AA.

Request a written submission on reasons not to

issue CoD within 20 working days.

[Regulation 13, 14(1)]

July 2020

8

The MI advisory committee

meets to hear the oral

representation and

recommend a course of

action to the AG.

[Regulation 18]

September 2020

9

AG issues a

certificate of debt to

the AO/AA.

[Regulation 19]

October 2020

Implementation of expanded mandate

The AG has a sole discretion to determine the nature, frequency and scope of audits

[section 13(1) of the PAA]

The AG may refer material irregularities to public bodies for investigation [section 5(1A)

of the PAA]

The AG may make recommendations in the audit report regarding any matter, including

material irregularities [section 20(4) of the PAA]

The AG consulted SCoAG on the notion of a phased implementation of the material

irregularity process

22

Implementation of expanded mandate

To allow for establishing capacity and

processes, a phased-in approach for

implementation was agreed with

SCoAG on the basis of:

1. the type of material irregularity to

be identified and reported

2. the auditees where it will be

implemented

3. Auditees which are not part of the

phase in will be dealt with in terms

of the NOCLAR requirements

Selection of auditees

Selection criteria

Latest audit outcome not clean or unqualified with findings – except

if there was a material finding on prevention or follow-up of

irregular expenditure

High irregular expenditure over the last three years

Sufficient coverage across spheres of government and provinces.

Type of material irregularity = Material non-compliance

(which would be reported in the audit report)

that resulted in (or is likely to result in) a material financial loss

2018-19 implementation

Type of material irregularity

Commencement date 1 April 2019

23

Implementation of expanded mandate

The phasing-in of the implementation of the amendments allowed us to:

Responsibly align the organisational resources with the demand placed on us by the PAA

• Develop understanding of the required additional resources to implement the powers

• Reassess the audit methodology and the audit process to accommodate the additional work

• Develop the requisite content and capacitate the audit teams via extensive training

• Develop tools and system to facilitate the remedial action and referral processes

• Build adequate support capacity

• Ensure that we are able to fund the additional effort

• Develop adequate materiality threshold to ensure value for audit fees

• Enhance the relevant internal processes to ensure adequate accountability reporting.

Ensure that our external partners are on adequately prepared

• Establish relationships with the identified public bodies

Due to the lack of accountability in the public sector it resulted in the acceleration of the PAA amendments in less than a year which

was unprecedented given the various legal steps to pass a legislation. This meant that AGSA had to assess and take cautious steps in

order to ensure that the it had adequate capacity to carry out the new mandate in a responsible manner.

24

Implementation of expanded mandate

The phasing-in of the implementation of the amendments allowed us to:

Create the required level of awareness of the Act and the Regulations in the external environment

• Extensive engagement with constitutional stakeholders

• accounting officers, accounting authorities, executive authorities and audit committees

• oversight – deferred to accommodate the election and post-election processes

• Non-constitutional stakeholders

• Media

• Professional bodies

• Civil society

• Audit firms

Due to the lack of accountability in the public sector it resulted in the acceleration of the PAA amendments in less than a year which

was unprecedented given the various legal steps to pass a legislation. This meant that AGSA had to assess and take cautious steps in

order to ensure that the it had adequate capacity to carry out the new mandate in a responsible manner.

25

Implementation of expanded mandate (Phase in Auditees)

1. Department of Cooperative Governance

2. Passenger Rail Agency of SA

3. Department of Defence

4. Department of Correctional Services

5. Department of Water and Sanitation

6. Water Trading Entity

7. SAA Technical

8. Department of Basic Education

9. Department of Education(EC)

10. Department of Health(NC)

11. Department of Health(KZN)

12. Department of Human Settlements(FS)

13. Gauteng Department of Health

14. Department of Health(MP)

15. Community Safety and Transport Management(NW)

16. Department of Education(LP)

1. Nelson Mandela Bay(EC) Metropolitan Municipality

2. Matjhabeng Local Municipality(FS)

3. City of Tshwane Metropolitan Municipality(GP)

4. Ethekwini Metropolitan Municipality(KZN)

5. Mogalakwena Municipality(LP)

6. Dr JS Moroka Municipality(MP)

7. Ga-Segonayana Local Municipality(NC)

8. Ngaka Modiri Molema District Municipality(NW)

9. City of Cape Town Metropolitan Municipality(WC)

PFMA LIST MFMA LIST

26

Role of Scopa

In line with Scopa’s mandate, the committee may:

Consider the AG’s accountability report that provides information on the material irregularities raise during the

specific audit cycle

Request regular updates form the accounting officers / authorities on the implementation of the AG’s

recommendation

Convene oversight discussions with any organs of state

Set the tone for accountability and consequence management by investigating and dealing with any allegations

of financial misconduct and irregularities by accounting officers and authorities and monitor the progress of

investigations

Oversee and influence progress made by public bodies with investigations and executive authorities (for

recovery of debt)

27

Measures of success

28

Robust financial and performance management systems

• Sound financial management systems

• Successful implementation of the audit recommendations

• Reduction in irregular and fruitless and wasteful expenditure

Commitment and ethical behaviour

• Visible commitment by all players in the public service to contribute towards the financial

health of the country and an improved social reality for our people

• Demonstrated ethical behaviour and professionalism in the public sector as cementing

characteristics of a capable state.

Oversight and accountability

• Accurate and empowering financial and performance reporting

• An appreciation of the role of applying consequences for transgressions and poor performance

• Improved accountability leading to limited referrals for investigation and certificates of debt issued

Thank you

www.agsa.co.za

@AuditorGen_SA

The Auditor-General of South Africa

The Auditor-General of South Africa

29